corporations: retained earnings and the income statement€¦ · ppt file · web...

TRANSCRIPT

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Corporations: Effects on Retained Earnings and the Income Statement

Chapter 13

1

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Learning Objectives

2

Account for stock dividendsAccount for stock splitsAccount for treasury stock

Report restrictions on retained earningsComplete a corporate income statementincluding earnings per share

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Account for stock dividends

3

1

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Dividend variationsCash dividends

Actual money goes out to share holders. This is real money. Shareholders can spend it.

Stock dividendsThis is not money. No money is sent to anybody.The company sends additional shares of stock to every owner, proportional to their shares held.Every owner maintains the exact same percentage ownership in the company.

Question: Which does not involve the cash account?

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Stock Dividend A distribution of a corporation’s own stock

Affects only stockholders’ equity accounts No effect on total stockholders’ equityNo effect on assets or liabilities

Stockholders receive proportionate sharesExample–10% stock dividend; every stockholder receives 10% more shares

If you own 100 shares, you get 10 moreIf I own 10 shares, I get 1 moreTotal number of shares issued and outstanding increasesOwnership percentages remain the same

5

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Why Do Companies Issue Stock Dividends?

Conserve cashContinue dividends without using cash

Reduce market price per share

6

Share supply increases; market price decreasesLess expensive; more attractive investment

Reward investorsShareholders receive something of perceived value

If I just got more shares, and everyone else got more shares too, are any of us really better off?

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

The point of this transaction is to put the retained earnings more visibly “in the hands” of the investor.

A small stock dividend shouldn’t materially affect the stock price, so we do the transaction at market price.

1) Take the market value of the new shares out of retained earnings {Debit Retained earnings}

2) Put that amount into Common stock account subject to that accounts par value limits

{Credit Capital stock} {Or, Credit: Stock dividend to be distributed}

3) Put the residual in the Additional paid In capital account {Credit: Additional paid in capital}

Small Stock Dividend Logic Path

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Entries for Small Stock Dividend

Same three dates for a stock dividendDeclaration date; record date; distribution dateWe are preparing one single summary transaction

Pull full market value from retained earningsPut it in the common stock account, subject to par

Demo: Issue a 5% stock dividend on common stockThere are 2,000,000 shares of $1 par stock outstandingThe stock is trading at $50 (market value)

What did we just do to the usefulness of the balance sheet?

8

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Large stock dividendsThese are greater than 25%, large enough to affect stock price.

So, there is no pretending that they won’t.

Since we aren’t pretending to support market price, we just take the par value out of retained earnings and reposition that as common stock

This keeps the stock price affordable to smaller investors and placates investor return desires.

9

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Entries for Large Stock DividendLarge

Distribution is greater than 20% to 25% of issued sharesDebit Retained earnings for par or stated value of sharesCredit Common stock for par or stated value of sharesRare

Journal entry demo: 50% stock dividend2,100,000 shares outstanding$1 par value

These are quite rare, normally a company will either do a small stock dividend, or a stock split.

10

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Account for stock splits

16

2

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Which is a better deal?

2 big slices at $4 each?

4 little slices at $2 each?

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Casual investor perceptions

$100 stocks seem too expensive

$50 stocks must be

doing well

$0.50 stocks must be

underperforming companies

Stock splits can be performed to

put the per share price

wherever you want it.

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Why is there price movement around stock splits?

Small investors view the stock as more affordable.

Sustainable stock price increase indicator.

To the extent that people agree that the price will move, this belief alone may cause the move – especially if it is helped along a little…...

2-for-1.com

GE, MSFT, HOG, AAPL, HD

Stock Split Market Price Effects

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Stock SplitsA stock split:

Cuts par value per shareIncreases the number of shares of stock issued and outstandingLeaves all account balances and total stockholders’ equity unchanged

Balances in the accounts are unchangedRecord in a memorandum entry–a journal entry without debits and credits

20

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

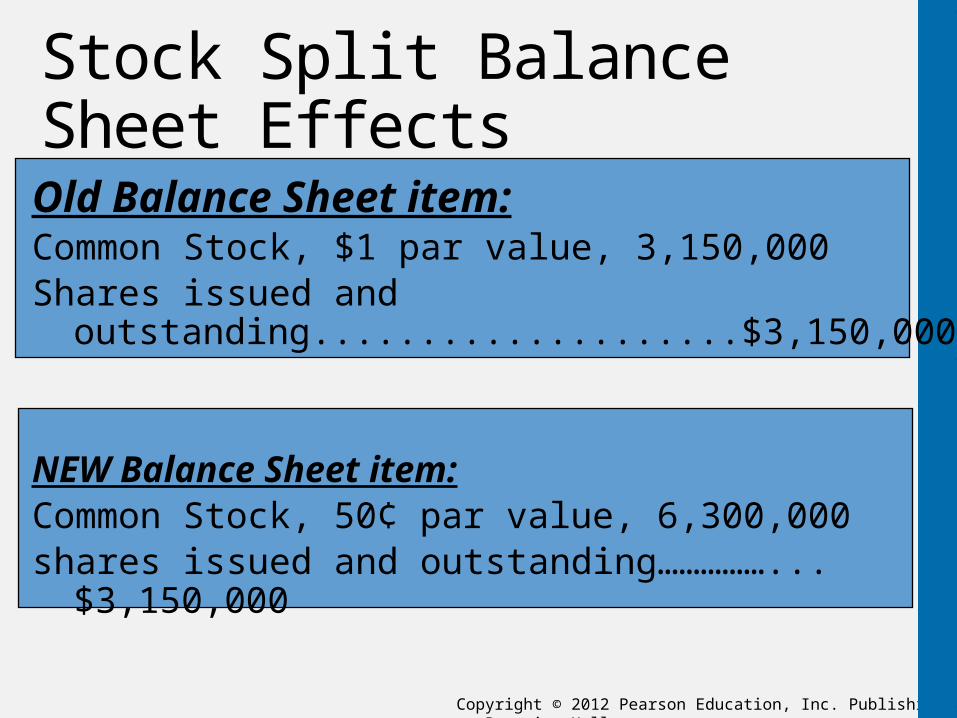

Stock Split Balance Sheet Effects

Old Balance Sheet item:Common Stock, $1 par value, 3,150,000Shares issued and outstanding....................$3,150,000

NEW Balance Sheet item:Common Stock, 50¢ par value, 6,300,000shares issued and outstanding……………...$3,150,000

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Account for treasury stock

28

3

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Treasury StockShares that a company has issued and later reacquired

Held as a contra equity account at repurchase costNo entry made to original capital stock account

Reasons corporations purchase their own stock:Buy low and sell high to increase wealthTo boost the company’s stock priceTo avoid a takeover by an outside partyTo make stock available for employee rewardsAn alternate way to give cash to shareholders

29

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

The maximum number of

shares of capital stock that may be sold to the

public.

AuthorizedShares

Where Treasury Stock Comes From

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Issued shares are authorized

shares of stock that have

been sold.

Unissued shares are authorized

shares of stock that never have

been sold.

AuthorizedShares

Where Treasury Stock Comes From

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

UnissuedShares

TreasuryShares

OutstandingShares

Treasury shares are issued shares that have been

repurchased by the corporation.

IssuedShares

Outstanding shares are issued shares that are currently owned

by stockholders.Authorized

Shares

Where Treasury Stock Comes From

NO voting rights!No dividends!

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

UnissuedShares

OutstandingSharesIssued

Shares

Outstanding shares are issued shares that are currently owned

by stockholders.Authorized

Shares

Where Treasury Stock Comes From

When treasury stock is re-issued it

becomes regular stock again!

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Treasury Stock Journal EntriesPurchase of treasury stock

Company debits Treasury stock and credits Cash

Sale of treasury stock at cost

Next: Treasury stock earnings bypass the income statement!

36

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Treasury Stock Journal EntriesSell 200 shares of that $5 cost stock @ $6 each

Difference is credited to Paid-in capital from treasury stock transactions

Sell 200 shares of that $5 treasury stock @ $4.30

Difference is debited to Paid-in Capital from treasury stock transactions, if available

Debit Retained earnings if that account is empty37

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Treasury Stock Journal EntriesSell 200 shares of that $5 Treasury stock @ $4.50 per share.

Paid-in capital from treasury stock transactions is insufficient to cover shortfallDebit Retained earnings for the difference

38

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Treasury Stock and Stockholders' Equity

Reported beneath Retained earnings as a reduction

39

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Complete a corporate income statement including earnings per share

46

5

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Reporting the Results of Operations

Information about net income can be divided into two major categories

Income from continuing operations.

1. The results of

discontinued operations

2. The impact of

extraordinary items.

3. The effects of changes in

accounting principles.

Normal, recurring revenue and expense transactions.

Unusual, nonrecurring events that affect net income.

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

The Corporate Income StatementContinuing Operations

Why use this number?This should be the basis of forecasting future year earningsIf you are buying into a company now, this is the basis you care about, not those other non-repeating items.

49

Should continue from period to periodUseful for making projections about future earnings

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Special ItemsReported after income from continuing operationsReported net of any tax effectsTwo distinctly different gains and losses:

Discontinued operationsExtraordinary itemsNote: Plant asset gains/losses are part of continuing operations

50

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Discontinued OperationsSegment of a business that has been sold

Each segment is an identifiable division of companyReported separately because the segment will not be around in the futureOperating profits/lossGain/loss on sale of the segment

51

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Material in amount.Gains or losses that are both unusual in nature and not expected to recur in the foreseeable future.Reported net of related taxes.NOT: lawsuits, strikes, recurring acts of nature, plant asset gains/losses

Extraordinary Items

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Extraordinary ItemsBoth unusual and infrequentNot expected to recur in the foreseeable futureExamples:

Losses from natural disastersForeign government takeover (expropriation)

Reported net of income tax effectItems not qualifying as extraordinary

Gains and losses on the sale of plant assetsLosses due to lawsuitsLosses due to employee labor strikesNatural disasters that occur frequently in the area

53

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

During 2011, an earthquake caused $75,000 damage to Apex’s factory.

The company reported income before extraordinary item of $175,000.

All gains and losses are subject to a 30% tax rate.

How would this item appear on the 2011 income statement?

Extraordinary Items - Example

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Earnings before extraordinary item 175,000$ Extraordinary Loss: Earthquake loss (net of tax benefit of $?) ?Net Income ?

Earnings before extraordinary item 175,000$ Extraordinary Loss: Earthquake loss (net of tax benefit of $22,500) (52,500) Net Income 122,500$

Income Statement Presentation:

Extraordinary Loss (75,000)$ Less: Tax Benefits ($75,000 × 30%) 22,500 Net Loss (52,500)$

Extraordinary Items - Example

Income Statement Presentation:

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

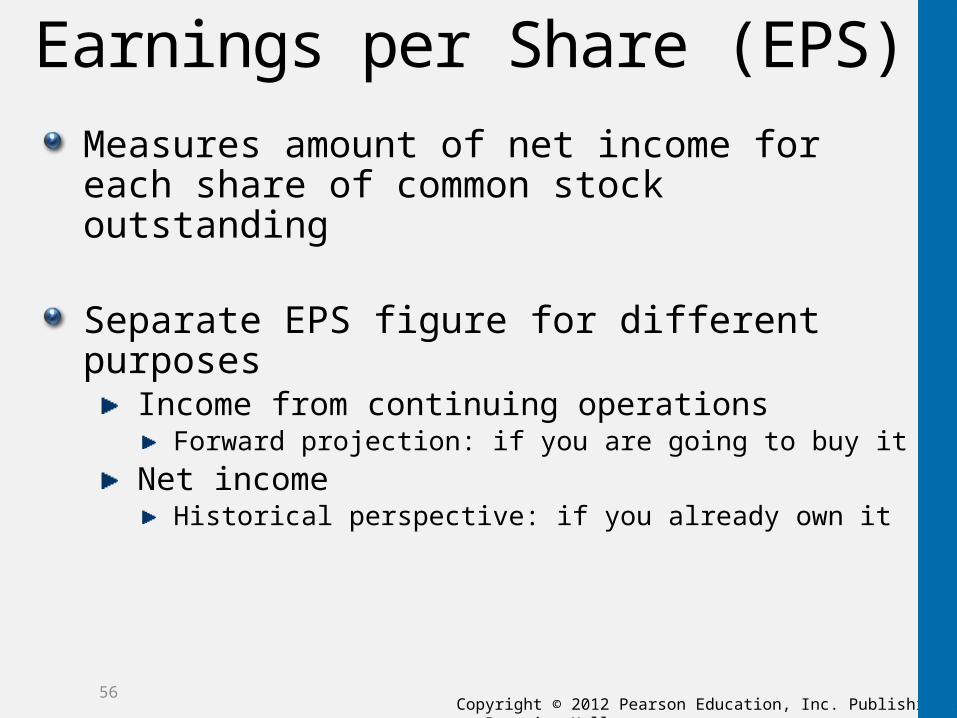

Earnings per Share (EPS)Measures amount of net income for each share of common stock outstanding

Separate EPS figure for different purposesIncome from continuing operations

Forward projection: if you are going to buy itNet income

Historical perspective: if you already own it

56

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

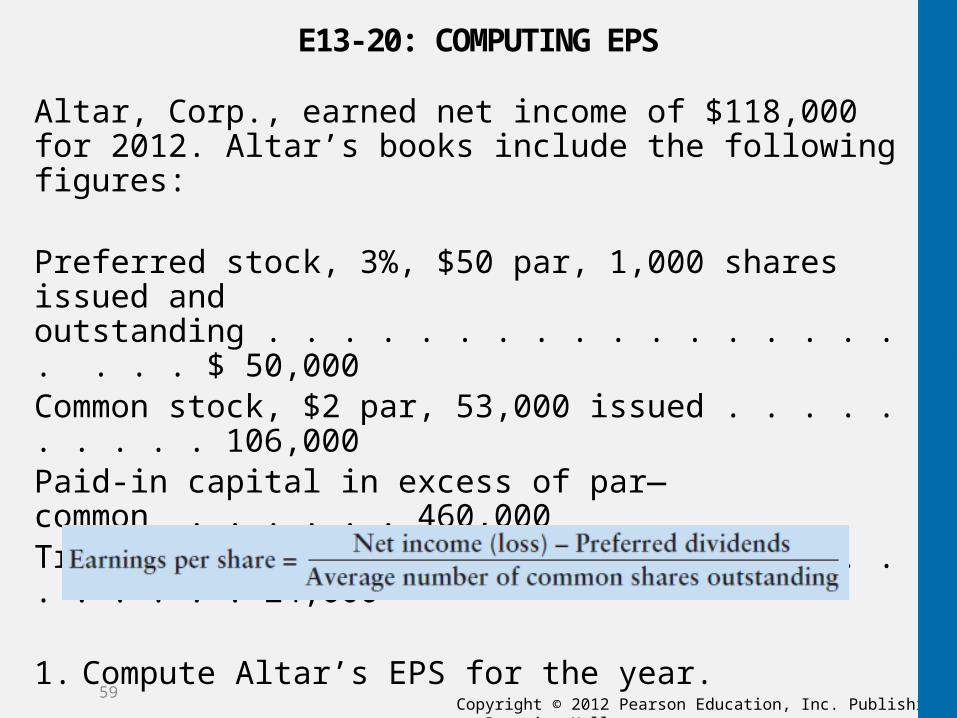

E13-20: COMPUTING EPS

Altar, Corp., earned net income of $118,000 for 2012. Altar’s books include the following figures:

Preferred stock, 3%, $50 par, 1,000 shares issued and outstanding . . . . . . . . . . . . . . . . . . . . . $ 50,000Common stock, $2 par, 53,000 issued . . . . . . . . . . 106,000Paid-in capital in excess of par—common . . . . . . 460,000Treasury stock, common, 1,200 at cost . . . . . . . . . . 24,000

1. Compute Altar’s EPS for the year.

$(118,000 – 15,000)/51,800 = $2.25*(2.249034749034749) rounded

59

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Evaluating Earnings Per Share

Growth rateCompanies aim to increase earnings per share to demonstrate increasing wealth building power

Earnings relative to stock priceComparing the stock price per share to the earnings per share provides a measure of value of the stockThe Price to Earnings ratio compares stock price to earnings per share

A measure of how much it costs to buy $1.00 in a company’s earnings.A high p/e ratio indicates an expensive stockA low p/e ratio indicates a value stock

60

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Price to Earnings Ratio

P/E ratio = Price per share ÷ Earnings per share

Using the P/E ratio:Find a company you like based on:

Earnings – strong income statementBalance sheet – strong financial standingCash flows – learn next weekSituation analysis

THEN, evaluate whether or not it is worth the purchase price by using the p/e ratio

61

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

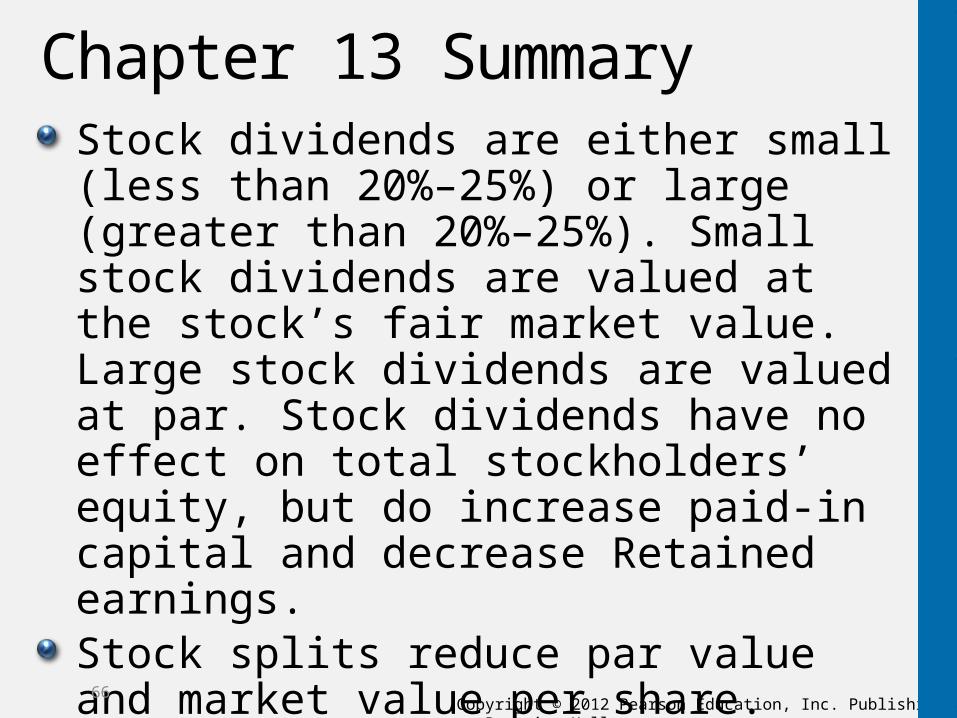

Chapter 13 SummaryStock dividends are either small (less than 20%–25%) or large (greater than 20%–25%). Small stock dividends are valued at the stock’s fair market value. Large stock dividends are valued at par. Stock dividends have no effect on total stockholders’ equity, but do increase paid-in capital and decrease Retained earnings.Stock splits reduce par value and market value per share. Stock splits increase the number of issued and outstanding shares. Stock splits have no effect on any general ledger accounts.

66

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Chapter 13 SummaryTreasury stock occurs when a company repurchases previously issued shares. Treasury stock is a contra equity account; therefore, increases in Treasury stock decrease total stockholders’ equity. Treasury stock purchases are recorded at cost, not par. All gains/losses on treasury stock sales are reported in the stockholders’ equity accounts.Restrictions on retained earnings most often arise from loan restrictions. These restrictions usually require companies to maintain minimum levels of retained earnings, thereby restricting amounts available for cash dividends and treasury stock purchases. Restrictions must be disclosed in the footnotes to the financial statements.

67

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Chapter 13 SummaryThe corporate income statement extends its coverage to include items that aren’t continuing. Extraordinary items—those infrequent and unusual—are reported separately, net of their tax effect on the income statement. Earnings per outstanding common share are reported for each major income statement item. The statement of retained earnings may include prior-period adjustments for corrective items. Comprehensive income includes the four items identified that aren’t normally reported on the income statement.

68

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.69

Copyright © 2012 Pearson Education, Inc. Publishing as Prentice Hall.

Copyright

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America.

70