corporate office:: retail business unit::home loan ... h… · h) kyc verification, pre –...

TRANSCRIPT

Page 1 of 12

CORPORATE OFFICE:: RETAIL BUSINESS UNIT::HOME LOAN VERTICAL (email: [email protected])

Date: 15.07.2019

HOME LOAN COUNSELOR- ELIGIBILITY CRITERIA, APPLICATION FORM &

OTHER RELATED INFROMATION:

1. Eligibility Criteria for Individual HLCs / Retired bank employees /

Corporate HLCs

a) Individuals with 2 years’ experience in the line of activity (either individual

practice or worked under HLC).

b) Ex-Employees of Public sector / Private Banks / NBFC’S / HFC’S (including

our Bank). The applicant should have exposure in the line of activity.

Employees who have been dismissed from the services or those against

whom disciplinary actions were initiated are not eligible.

c) Firms/LLPs/Companies/Association of persons who are engaged in this

type of activity with at least 2 years’ experience and already empanelled

with commercial Banks/Financial institutions like LIC Housing finance,

Canfin Homes etc. will be eligible for empanelment as Corporate HLCs.

d) Individuals with minimum 21 years of age and not exceeding of 70 years.

e) Individuals should be local resident with 10th standard or equivalent ability

of communicating effectively in local language and English and is having

minimum Two years’ experience in marketing financial products like

Insurance, Mutual funds etc.

f) There shall not be adverse remarks in the CIBIL report.

2. Eligibility for engagement of Builders or Builder’s representative as

business partner(HLBPs).

a) The builder or builder representative will be empanelled only for approved

project approved by our bank.

b) The commission payable other guidelines will be same as applicable to

Individual / Corporate HLCs.

3. List of documents to be submitted:

a) Application form in the prescribed format.

b) Resume containing bio-data of the applicant.

Page 2 of 12

c) Copy of PAN card.

d) Copy of Aadhaar card.

e) Copy of address proof.

f) Copy of educational qualification.

g) Copy of partnership deed/MOA/AOA, list of Directors/Partners with

their bio-data, details of authorized signatories in respect of entities

other than individuals.

h) **Copy of 2 years IT returns/audited financial statements for Corporate

HLCs.(**Zonal Manager can permit deviation on submission of Income

Tax returns / Audited financial statements on case to case basis)

i) Copy of empanelment letter from other Banks/FIs.

j) Copy of experience certificate (in the line of activity) from the employer,

if any.

k) Reference letter from reputed persons.

l) Statement of Bank account for the last 6 months.

4. Empanelment Procedure:

i) Empanelment Procedure for Individual HLCs/Retired Bank Employees:

a) Respective Regional Offices shall issue an advertisement in local

newspaper calling for applications for empanelment in all RMLC

centers across the country.

b) Aspirants to become HLC of the bank shall submit application for

empanelment at the respective Branch.

5. Roles & Responsibilities of HLCs/HLBPs:

a) Maintain close liaison with builders/architects/City Improvement or

Development authorities for sourcing Housing loan proposals.

b) Source Housing loan proposals from various sources like personal contacts,

respondents to the websites of builders/authorities who launch housing

projects.

c) Source housing loan proposals from print/social media applications from

intending residential property buyers.

d) Meet intending Home Loan borrowers at a place and time convenient to the

intending applicants and explain unique features of Home Loan product of the

bank as per the prevailing scheme of the Bank.

e) To render necessary service to the applicants to comply with the various

requirements including legal clearance, valuation etc.

Page 3 of 12

f) To carry out the preliminary scrutiny of loan applications, KYC Documents and

supporting documents / papers, to ensure that the application is properly filled

in and is supported by documents/papers and deliver them to the respective

branch/Retail loan center for further processing.

g) Role of Home Loan Counselor will be limited to the sourcing of proposal only

and assisting in KYC verification and due diligence.

h) KYC verification, Pre – sanction inspection, appraisal, documentation,

disbursement and Post – sanction inspections etc. in respect of Home loans

are to be done by the Branch.

i) Acquaint themselves with our Home loan products like calculation of eligibility

through Eligibility calculator, margin norms, income and cutback criteria,

insurance coverage of life of the borrower and also property insurance,

through our Marketing officers/Officers/Executives of Regional Offices.

j) Assist Bank Officials/ Advocate/ Valuer for proper identification of the property

during site inspection/follow up visit of the property.

k) Help the customers in completing the formalities and speedy disposal of the

loan proposal.

l) Closely follow up with the applicant, branch / retail loan center for speedy

disposal of the proposal.

m) Maintain confidentiality of information of the applicant/Bank as required under

law.

n) Assist the Bank for recovery of dues, in case of need.

6. Operational area / Jurisdiction of the HLCs/HLBPs:

Housing loans pertaining to the jurisdiction of the respective RMLC where it is located.

7. Monthly targets to the HLC: Disbursement of minimum 2 sourced Home Loans per month or 6 Home Loan

in a quarter (new + take over).

8. De-empanelment of HLC:

Any HLC who does not source even a single Home Loan during the preceding 3 months will be De-empanelled. The HLC is to be de-empanelled by respective ZO based on the recommendations of the RO. The same shall be notified through In-house portal by RO on receipt of communication from ZO.

9. Terms & Conditions:

a) Empanelment is valid initially for 3 years subject to annual review by

respective Regional office.

Page 4 of 12

b) Empanelment of the Home Loan Counselor is on commission for the business

canvassed and is not be construed as providing employment on a regular

basis by the Bank.

c) HLC shall not appoint any Sub agent or delegate his powers to any other

person/ entity.

d) Commission is based on the leads provided by the HLC which is converted to

real business. 90 % Commission shall be paid only after first disbursement**

is made to the seller / builder Balance 10 % of the commission shall be payable

once 75 % of the sanctioned loan amount is disbursed. (** A Loan shall be

considered as disbursed once the first disbursement to the seller /

builder/towards construction is made. First disbursement towards Insurance

Premium, Commission Payable or towards any other such charges/fees shall

not be construed as disbursement for the purpose of considering a loan as

disbursed for the purpose of calculation of commission payable to HLCs)

e) If a top up loan is also sanctioned for a Takeover home loan, at the time of

takeover of a Home Loan the commission at the same rate as applicable to

home loan will be payable to HLCs for Top Up Loan as well.

f) No commission will be payable to HLC s for sourcing top up loans to the

existing home loan borrowers

g) The Commission includes the travelling and other incidental expenses

connected with the loan proposal and no other charge is payable by the Bank.

h) The Bank shall pay the GST which will be in addition to the commission

payable at the stipulated rate.

i) Commission payable is subject to compliance of Income Tax guidelines for

TDS.

j) HLCs to educate the Home Loan applicants about details of the Housing loan

scheme guidelines, charges/expenses (like advocates fees, valuers fee,

customer verification processing/documentation charges, mortgage charges,

inspection charges, insurance charges etc) as per norms payable to the Bank.

k) Commission will not be payable to Individual HLCs / Corporate HLCs/ Builders

for walk in business and also for the business directly canvassed by the bank

officials / employees.

l) HLCs not to levy any fees for providing services to the loan applicant, any

violation are liable for termination.

m) HLCs will be held responsible for and shall indemnify the Bank for any loss

caused due to:

Mis-representation of facts in respect of loan product, proposals and

any other thing which is connected to or incidental to the loan

proposal.

Page 5 of 12

Loan proposals declared as “fraud” on account of impersonation,

fake title deeds, property documents, non-existent / dubious

property, fake financial statements / IT Returns/statement of

accounts, KYC documents of the loan applicants or any such

instance which has resulted in fraud, provided the lapse is

attributable to the Home Loan counselor. The instances mentioned

above are only illustrative but not conclusive.

HLCs will indemnify the bank for any loss caused to the Bank

directly or indirectly due to violation of any of the terms and

conditions mentioned in this agreement as well as guidelines of the

Bank by HLC.

The Bank further reserves the right to initiate criminal proceedings

against the HLC for the above lapses.

n) HLCs shall act in the best interest of the Bank and always protect the interest

of the Bank while dealing with their clients, while representing the Bank.

o) HLCs shall abide by the code of conduct while dealing with the clients on behalf

of the Bank.

p) HLCs shall not use the Bank’s name /logo in any manner while doing business

without express permission from the Bank.

q) HLCs shall not do anything that brings dis-repute to the Bank’s name/image

while doing business with the clients.

r) Bank reserves the right to terminate services of HLCs at any time, without

assigning any reasons and notice whatsoever.

s) Any HLC who does not source even a single Home Loan during the preceding

3 months will be De-empanelled.

t) Services of HLCs shall be engaged only for the branches which are linked to RMLCs.

u) Branches cannot sanction Home Loans sourced by HLCs/HLBPs.

v) All loans sourced by HLCs/HLBPs mandatorily need to be processed and sanctioned at RMLCs

w) Each HLC will be issued an identity card valid for one year from the date of

empanelment.

x) Every year a new identity card will be issued after reviewing performance of

HLC.

y) HLCs will co-ordinate with applicant, RMLC and branch for sanction and disbursement of the Loan.

Page 6 of 12

z) HLCs will market home loan proposal, collect all the required documents and submit the same to RMLC through the linked branch.

10. Other Guidelines:

a) The Home Loan Leads sourced by HLCs/HLBPs shall be routed through Synd

Saathi App. The Branches to monitor the leads generated in Synd Saathi

immediately and follow up with HLCs/HLBPs and the applicants.

b) Commission will be payable strictly based on reports generated from LAPS &

CBS.

c) Branch will recommend for payment of bill at monthly intervals to Regional

Office.

d) Regional Manager to approve payment through In house portal.

e) Commission paid will be subject to audit by the banks auditors as part of the

regular branch audit at the time of branch audit.

f) The Bank shall pay / bear the GST which will be in addition to the commission

payable at the stipulated rate.

g) No commission will be payable to HLCs for sourcing top up loans to the

existing home loan borrowers.

h) RO on receipt of communication of approval from respective ZO shall follow

procedure for onboard of the approved the HLCs, obtain relevant agreements

from HLCs, and enter the details in the relevant portal, issue identity card to

HLCs and inform the respective branch to enable them to avail the services of

HLCs.

i) At Corporate office, the Department shall create a utility (with the help of CO:

DIT) to maintain data base of HLCs with a unique identification serial Number

to each HLCs and link the same in LAPS. There shall be a system for

generating the required for MIS from the Utility for monitoring / evaluating the

functioning of HLCs.

j) Performance of the HLC will be based on the reports generated from utility

provided for the purpose.

k) RO’s shall conduct HLCs review meetings quarterly and take steps to improve

performance of HLCs and de-empanelment of non-performing HLCs as per

laid down guidelines. All HLCs working in the jurisdiction shall participate in

the review meeting.

l) HLCs shall submit monthly report as on last day of the month to RO on

application sourced/sanctioned/disbursement.

Page 7 of 12

m) Each of the HLC should have SB or Current Account with Syndicate Bank for

payment of commission. Their KYC and address verification has to be carried

out and their police verification also needs to be done.

o) Police verification can be waived by Regional Manager for Retired Bank/LIC / Govt. Employees and also for others who are having existing valuable relationship with the Bank for more than a year as on the date of submission of application for empanelment.

11. Indemnity:

a. The Home Loan Counselor will indemnify and keep indemnified the Bank

against any claim or claims, loss or damages, actions, costs including legal

charges if any, charges and expenses whatsoever which may be brought or

made against or sustained or incurred by the Bank (and whether paid by the

Bank or not) or which the Bank become liable under or in respect of or

incidental to or relating to empanelling the Home Loan Counselor under this

agreement.

b. HLC will be held responsible for and shall indemnify the Bank for any loss

caused due to:

1. Mis-representation of facts in respect of loan product, proposals and

any other thing which is connected to or incidental to the loan proposal.

2. Loan proposals declared as “fraud” on account of impersonation, fake

title deeds, property documents, non-existent / dubious property, fake

financial statements/ IT Returns/statement of accounts, KYC

documents of the loan applicants or any such instance which has

resulted in fraud provided the lapse is attributable to the Home

Loan counselor. The instances mentioned above are only illustrative

but not conclusive.

3. HLC will indemnify the bank for any loss caused to the Bank directly

or indirectly due to violation of any of the terms and conditions

mentioned in this agreement as well as guidelines of the Bank by HLC.

4. The Bank further reserves the right to initiate criminal proceedings

against the HLC for the above lapses.

Page 8 of 12

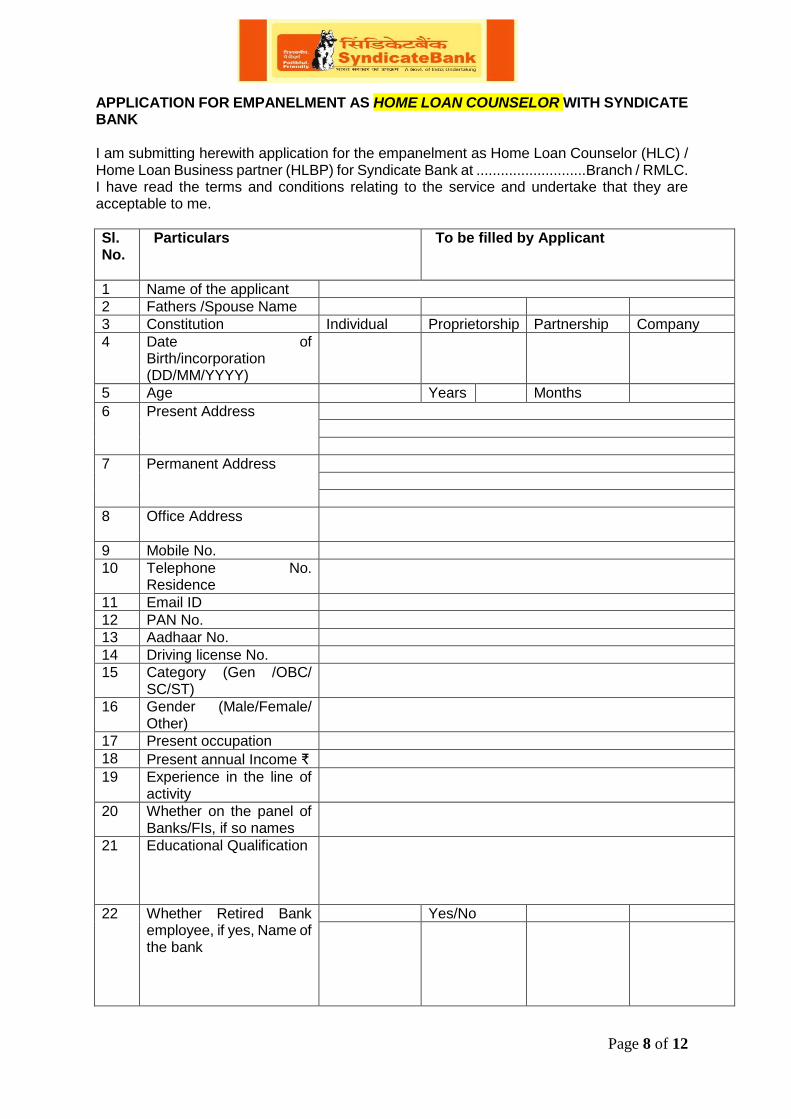

APPLICATION FOR EMPANELMENT AS HOME LOAN COUNSELOR WITH SYNDICATE BANK I am submitting herewith application for the empanelment as Home Loan Counselor (HLC) / Home Loan Business partner (HLBP) for Syndicate Bank at ...........................Branch / RMLC. I have read the terms and conditions relating to the service and undertake that they are acceptable to me.

Sl. No.

Particulars

To be filled by Applicant

1 Name of the applicant

2 Fathers /Spouse Name

3 Constitution Individual Proprietorship Partnership Company 4 Date of

Birth/incorporation (DD/MM/YYYY)

5 Age Years Months 6 Present Address

7 Permanent Address

8 Office Address

9 Mobile No.

10 Telephone No. Residence

11 Email ID

12 PAN No.

13 Aadhaar No.

14 Driving license No.

15 Category (Gen /OBC/ SC/ST)

16 Gender (Male/Female/ Other)

17 Present occupation

18 Present annual Income ₹

19 Experience in the line of activity

20 Whether on the panel of Banks/FIs, if so names

21 Educational Qualification

22

Whether Retired Bank employee, if yes, Name of the bank

Yes/No

Page 9 of 12

Sl. No.

Particulars

To be filled by Applicant

23 Presently banking with Name of the Bank :

Name of the Branch :

Account Number :

IFSC Code :

24 Reference if any

25 *Details of Assets in lakh

26 *Detail of liabilities in lakh

27 Language Known Read Write Speak Understand i)

ii)

iii)

iv)

* Separate annexure giving full details of assets and liabilities to be submitted. Declaration: I hereby declare that

I. No case of CBI or any other Law Enforcement Agency is pending against me,

and I /we am are physically fit and lawfully entitled to carry out duties of the

Home Loan Counselors.

II. I / We have not been de-panelled / delisted / black listed from any other Bank

/ financial institutions / insurance companies or any other professional body /

company/ firm for any misconduct on my/our part.

III. I shall abide by the Model Code of Conduct and guidelines on empanelment

of Home Loan Counselors.

IV. All my liabilities are regular and I am not a defaulter of any loan with Banks/

Financial Institutions.

I /We further declare that all statements made in this application are true, complete and correct to the best of my knowledge and belief. I /We understand that in the event of any information being found untrue or incorrect at any stage or of my/our not satisfying any of the eligibility criteria prescribed by Syndicate Bank from time to time, my/our candidature is liable to be cancelled at any time without any notice. Place: Signature of the applicant Date:

Page 10 of 12

DOCUMENTS TO BE SUBMITTED ALONG WITH APPLICATION

I / We submit self-attested copies of following documents: LIST OF DOCUMENTS TO BE SUBMITTED: (please √ wherever submitted)

Document √ wherever submitted

Application form in the prescribed format.

Resume containing bio-data of the

applicant.

Copy of PAN card and Aadhaar card.

Copy of address proof

Copy of educational qualification

Copy of partnership deed/MOA/AOA, list

of Directors/Partners with their bio-data,

details of authorized signatories in

respect of entities other than individuals.

Copy 3 years audited financial

statements, IT returns.

Copy of empanelment letter from other

Banks/Financial Institutions.

Copy of experience certificate, if any.

Reference letter from reputed persons.

Statement of Bank account for the last 6

months.

Signature of the applicant

-------------------------------------------------Office use only ----------------------------------------------

Branch: Observations / Remarks / Recommendations:

Date Asst Manager /Manager Branch Head

Regional Office: Observations / Remarks / Recommendations: Date Officer/Executive Regional Head

Recommended to ZO for empanelment of Home Loan Counselor with our bank Date Home Loan Nodal Executive Zonal Manager

Page 11 of 12

Commission Payable to Home Loan Counselor:

Category Proposed Commission

Housing loan below ₹ 10.00 lakhs and top up housing loans

Commission payable is NIL

Housing Loans from ₹ 10 Lakh to less than

₹.50 Lakh

0.40% + GST of the Housing Loan amount

Housing Loans of ₹ 50 Lakh and above 0.50% + GST of the Housing Loan amount

with a Maximum cap of ₹1.50 Lakh per

Housing Loan

For Takeover of Housing Loans from ₹10

Lakh to less than ₹ 50 Lakh

0.50% + GST of the Housing Loan amount.

For Takeover of Housing Loans of ₹ 50 Lakh and above

0.60% + GST of the Housing Loan amount

with a Maximum cap of ₹2.00 Lakh per

Housing Loan.

Total Home Loan disbursements Per Month

of ₹ 1.00 Crore to less than Rs.3.00 Crore.

Bonus of 0.05% + GST of the total Home

Loans business booked during the month by

the Agent (New + Take Over

Total Home Loan disbursements Per Month of

₹ 3.00 Crore to less than ₹ 5.00 Crore

Bonus of 0.10% + GST of the total Home

Loans business booked during the month by

the Agent concerned. (New + Take Over)

Total Home Loan disbursements Per Month

of ₹ 5.00 Crore and above

Bonus of 0.15% + GST of the total Home

Loans business booked during the month by

the Agent concerned. (new + Take Over)

Commission is payable only in respect of proposals received approved builders.

Commission is payable for proposals for construction of residential houses /

purchase of ready built house.

Commission will not be payable to HLCs for walk in business and also for the

business directly canvassed by the Bank officials /employees.

Individual HLCs –Target: Disbursement of minimum 2 Home Loans per month

or 6 Home Loan in a quarter (new + take over).

90% of the commission shall be payable at the time of first disbursement of loan

( to the seller / builder) at the stipulated rate on sanctioned amount balance 10%

of the commission shall be payable after 75% of the sanctioned loan amount is

disbursed.

Page 12 of 12

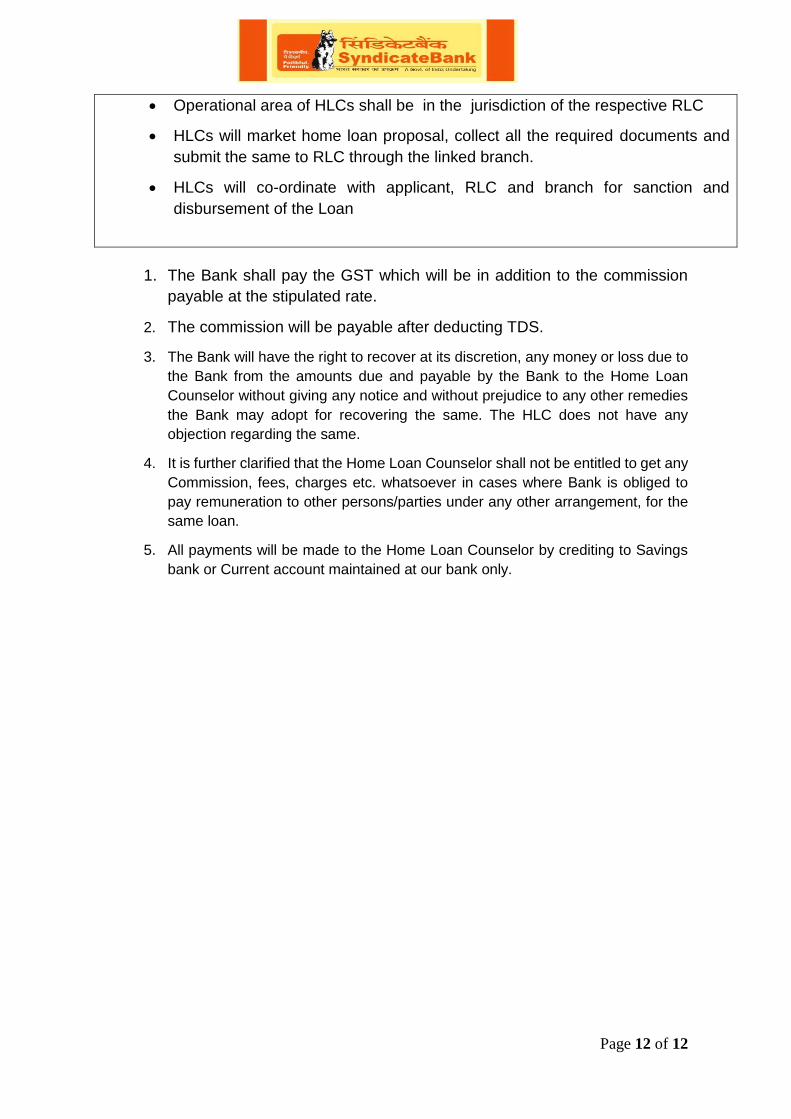

Operational area of HLCs shall be in the jurisdiction of the respective RLC

HLCs will market home loan proposal, collect all the required documents and

submit the same to RLC through the linked branch.

HLCs will co-ordinate with applicant, RLC and branch for sanction and

disbursement of the Loan

1. The Bank shall pay the GST which will be in addition to the commission

payable at the stipulated rate.

2. The commission will be payable after deducting TDS.

3. The Bank will have the right to recover at its discretion, any money or loss due to

the Bank from the amounts due and payable by the Bank to the Home Loan

Counselor without giving any notice and without prejudice to any other remedies

the Bank may adopt for recovering the same. The HLC does not have any

objection regarding the same.

4. It is further clarified that the Home Loan Counselor shall not be entitled to get any

Commission, fees, charges etc. whatsoever in cases where Bank is obliged to

pay remuneration to other persons/parties under any other arrangement, for the

same loan.

5. All payments will be made to the Home Loan Counselor by crediting to Savings

bank or Current account maintained at our bank only.