corporate insurance and tax planning - cindy david - june 18, 2015

TRANSCRIPT

June 17th, 2015

Corporate Insurance and Tax Planning

Presented to: EPC Abbotsford, BC

Presented By:Cindy David, CFP, CLU, FEA, TEPPresident, Estate Planning AdvisorCindy David Financial Group Ltd.

The Opportunity

45.80*Personal Tax

13.50Corporate Tax

Shouldn’t you keep the difference?

*Reverting back to 43.7% after 2015

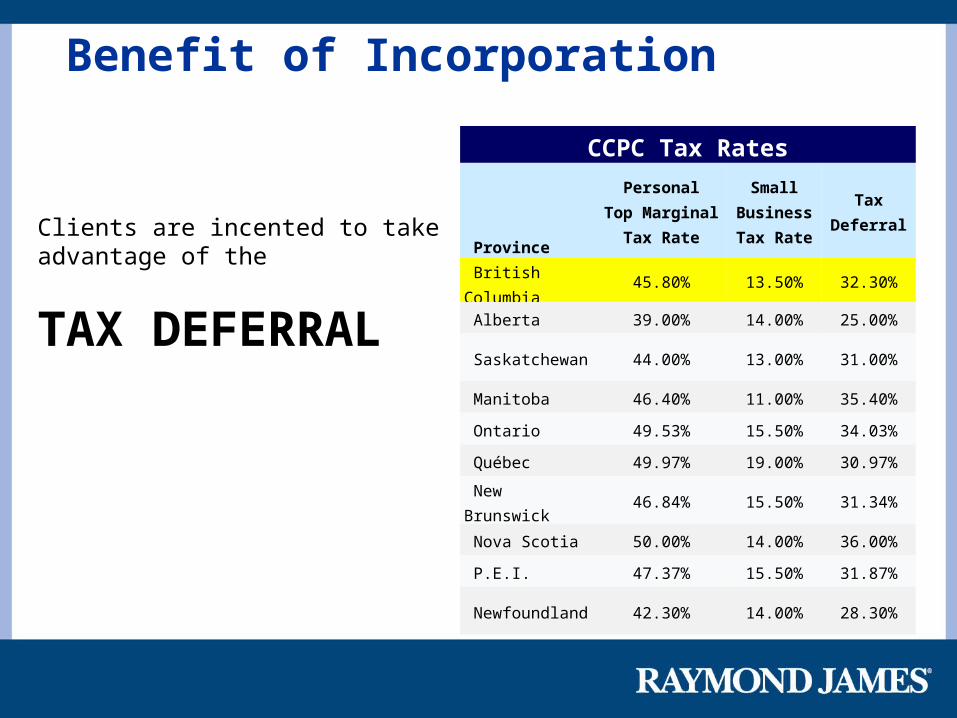

Benefit of Incorporation

Clients are incented to take advantage of the

TAX DEFERRAL

CCPC Tax Rates

Province

PersonalTop Marginal

Tax Rate

Small BusinessTax Rate

Tax Deferral

British Columbia 45.80% 13.50% 32.30%

Alberta 39.00% 14.00% 25.00%

Saskatchewan 44.00% 13.00% 31.00%

Manitoba 46.40% 11.00% 35.40%

Ontario 49.53% 15.50% 34.03%

Québec 49.97% 19.00% 30.97%

New Brunswick 46.84% 15.50% 31.34%

Nova Scotia 50.00% 14.00% 36.00%

P.E.I. 47.37% 15.50% 31.87%

Newfoundland 42.30% 14.00% 28.30%

Incorporation

Savings on non-deductible and some deductible expenses:

• Pay non-deductible expenses such as life insurance premiums and entertainment expenses with after tax SBD income.

• Leveraged insurance strategies create NCPI and Cost of Insurance deductions

NCPI and CDA credits reducing dramatically after January 1, 2017

The Dilemma

But then clobbered over the head with

PASSIVE

investment income tax

Potential Solutions

• Individual Pension Plans• RRSPs • Retirement Compensations Arrangements

• Corporate Estate Bond• Insured Retirement Strategy• Corporate Insured Annuity• Immediate Financing Arrangements (IFA)• Cascade Strategy

Access to Tax-Preferred Investing

Requires Salary

Ways To Pay Estate Tax Traditional Insurance Solutions

• Buy $2,700,000 of Joint-Last-To-Die life insurance• Term to 100, or• Universal Life with Level Cost of Insurance

Every insurance solution is much cheaper than the present value of self insuring: $803,595

T100 UL UL

Life Pay 10 Pay 5 Pay

Annual Outlay $19,206 $44,430 $94,371

Years Payable 41 10 5

Total Outlay $787,446 $444,300 $471,855

Present Value at 3% $463,148 $423,436 $369,198

Savings with insurance $340,447 $380,159 $434,397

Use Insurance for Tax-Sheltered Investing

MTAR – Maximum Tax Actuarial Reserve, S148 ITA

Investment

Tax (45.67%)

Investment

Insurance

Plan A Plan B

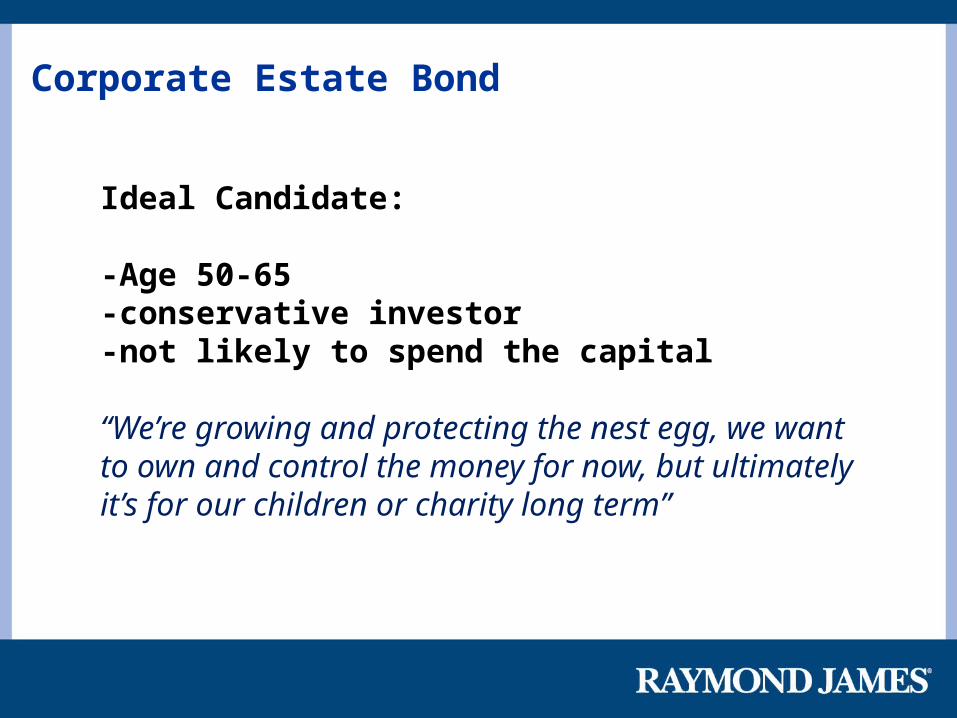

Corporate Estate Bond

Ideal Candidate:

-Age 50-65-conservative investor-not likely to spend the capital

“We’re growing and protecting the nest egg, we want to own and control the money for now, but ultimately it’s for our children or charity long term”

Corporate Estate Bond

8.83%

Corporate Insured Retirement Strategy

Ideal Candidate:

-ages 30-50-wants to create long term retirement income-good saver

“We’re saving so we can spend it in retirement. We’re looking to create pension-style income since we don’t have pensions through employment. Any estate benefit is a bonus”

Corporate Retirement StrategyRate: 4.84% 1st 10 years, 6.84% thereafter Corporate Tax Rate on Investment Income: 44.67%

Initial Death Benefit Shareholder Dividend Tax Rate: 33.71%

Corporate Insured Retirement Strategy (CIRP)

Taxable Corporate Investment

Year Age Annual Deposit

After Tax Dividend to Shareholder

Net Estate Value

After Tax Dividend to Shareholder

Net Estate Value

1 41 46,000 0 1,095,400 0 31,9582 42 46,000 0 1,139,278 0 65,4303 43 46,000 0 1,183,843 0 100,4634 44 46,000 0 1,230,148 0 137,1115 45 46,000 0 1,280,222 0 175,425

6 46 46,000 0 1,330,294 0 215,4607 47 46,000 0 1,380,729 0 257,2738 48 46,000 0 1,430,590 0 300,9239 49 46,000 0 1,481,622 0 346,46810 50 46,000 0 1,534,035 0 393,972

11 51 46,000 0 1,611,623 0 443,50012 52 46,000 0 1,697,803 0 495,11713 53 46,000 0 1,793,081 0 548,89314 54 46,000 0 1,897,977 0 604,89915 55 46,000 0 2,013,018 0 663,207

16 56 46,000 0 2,135,665 0 723,89517 57 46,000 0 2,226,273 0 787,04118 58 46,000 0 2,405,379 0 852,72519 59 46,000 0 2,553,537 0 921,03120 60 46,000 0 2,711,333 0 992,047

e&oe

21 61 46,000 0 2,878,223 0 1,065,86222 62 46,000 0 3,053,407 0 1,142,56823 63 46,000 0 3,237,354 0 1,222,26224 64 46,000 0 3,430,536 0 1,305,04125 65 46,000 0 3,633,414 0 1,391,008

26 66 0 114,748 3,669,064 114,748 1,329,87827 67 0 114,748 3,707,914 114,748 1,266,81028 68 0 114,748 3,750,008 114,748 1,201,74129 69 0 114,748 3,795,422 114,748 1,134,60330 70 0 114,748 3,772,300 114,748 1,065,326

31 71 0 114,748 3,733,408 114,748 993,83932 72 0 114,748 3,693,375 114,748 920,06733 73 0 114,748 3,652,070 114,748 843,93334 74 0 114,748 3,609,350 114,748 764,65735 75 0 114,748 3,566,397 114,748 681,541

36 76 0 114,748 3,521,771 114,748 594,39637 77 0 114,748 3,475,306 114,748 503,01938 78 0 114,748 3,426,829 114,748 407,20139 79 0 114,748 3,376,152 114,748 306,71940 80 0 114,748 3,306,868 114,748 201,341

41 81 0 114,748 3,234,371 114,748 90,82142 82 0 114,748 3,158,416 90,821 043 83 0 114,748 3,078,744 0 044 84 0 114,748 2,995,087 0 045 85 0 114,748 2,907,161 0 0

46 86 0 2,294,960 2,653,282 1,926,789 0

Corporate Retirement StrategyCorporate Insured Retirement

Strategy (CIRP)Taxable Corporate Investment

Year Age Annual DepositAfter Tax Dividend

to Shareholder Net Estate ValueAfter Tax Dividend

to Shareholder Net Estate Value

e&oe

Insurance Funding Options – Immediate Financing Arrangements (IFA)

Reduce insurance cash flow costs further by using two tax advantages

1. Tax-deferred investment growth inside a tax-exempt life insurance policy

2. tax deductible loan interest and deductible NCPI when loan proceeds used for investment purposes

Immediate Financing Arrangements – Who Can Benefit?

• Real estate corporations

• CCPC with high cash flow

• Holding Companies with trapped corporate

surplus

• Oversized RRSPs

• High marginal tax bracket

Mechanics of an IFA

1. Buy Permanent life insurance plan and pay maximum deposits (MTAR), deposits can be short term -3yrs, medium term 8-10 years, or lifetime

2. Borrow and invest suitably so that the interest is tax deductible• The loan increases each year which provides larger tax

deductions and reduces the cash outflow• Loan collateral grows by return of the insurance funds

3. Loan is fully underwritten by 3rd party lender

Zero Cash Flow

Corporate Insured Annuity

Combination of permanent life insurance and annuity income (2 insurance products)

WHO?

-age 70+

-high tax bracket

-GIC refugee

-non-smoker

-insurable

-lots of corporate cash

Corporate Insured Annuity

Annuity Type: Single Life Corporate Tax Rate on Investment Income: 45.67%

Initial Death Benefit: $150,000 Personal Dividend Tax Rate: 29.12%

Corporate Insured Annuity

Annuity Type: Single Life Corporate Tax Rate on Investment Income: 45.67%

Initial Death Benefit: $150,000 Personal Dividend Tax Rate: 29.12%

Corporate Insured Annuity

Annuity Type: Single Life Corporate Tax Rate on Investment Income: 45.67%

Initial Death Benefit: $150,000 Personal Dividend Tax Rate: 29.12%

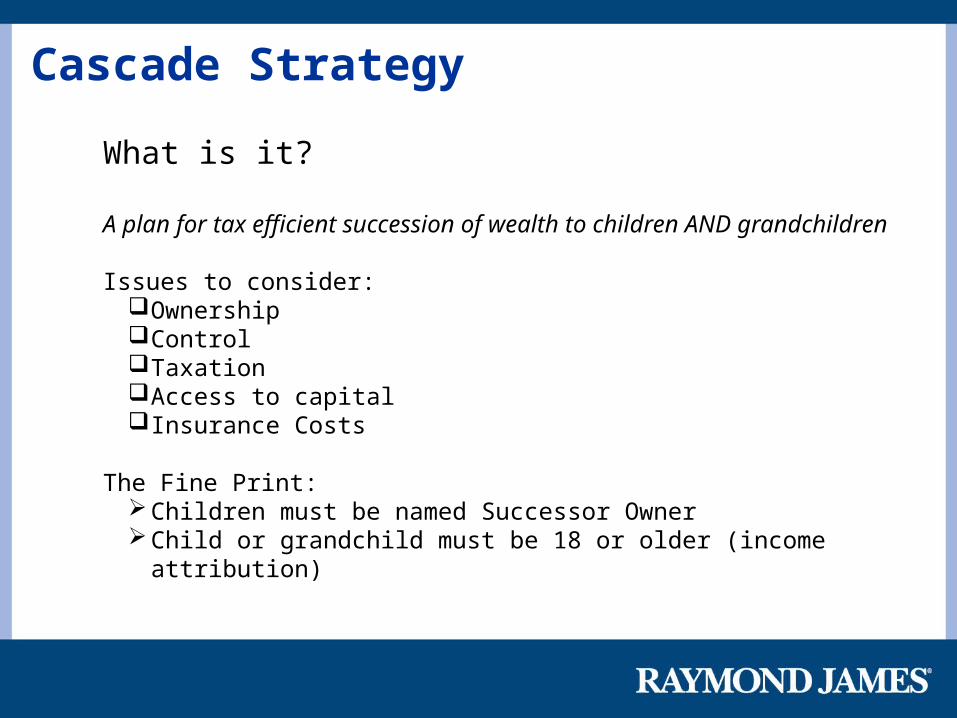

Cascade Strategy

What is it?

A plan for tax efficient succession of wealth to children AND grandchildren

Issues to consider:OwnershipControlTaxationAccess to capitalInsurance Costs

The Fine Print:Children must be named Successor OwnerChild or grandchild must be 18 or older (income attribution)

Cascade Strategy

Initial Policy Owner: Parent Marginal Tax Rate: 43.7%Life Insured: Son (Male, 57)& Daughter-in-law (Female, 58) Ownership Transfer: Year 5Initial Death Benefit: $240,040

Withdrawals Net Values

Year Age Annual Deposit Before-tax Withdrawals Cash Surrender Value Death Benefit

1 58 20,000 0 11,247 316,027 2 59 20,000 0 23,087 340,898 3 60 20,000 0 35,584 365,971 4 61 20,000 0 48,945 391,625 5 62 20,000 0 63,566 418,586 6 63 20,000 0 81,161 445,473 7 64 20,000 0 108,357 472,329 8 65 20,000 0 128,153 498,730 9 66 20,000 0 144,177 525,473

10 67 20,000 0 166,296 552,580 11 68 0 0 176,350 553,033 12 69 0 0 188,346 555,276 13 70 0 0 202,397 559,395 14 71 0 0 218,397 565,481 15 72 0 0 237,179 573,625 16 73 0 0 257,609 583,054 17 74 0 0 280,046 593,819 18 75 0 0 304,589 606,017 19 76 0 0 331,388 619,746 20 77 0 0 360,541 635,107 21 78 0 19,316 364,151 624,654 22 79 0 19,316 365,765 614,876 23 80 0 19,316 367,598 605,599 24 81 0 19,316 369,666 596,841 25 82 0 19,316 371,984 588,622 26 83 0 19,316 371,450 576,750 27 84 0 19,316 370,808 564,999 28 85 0 19,316 370,043 553,360 29 86 0 19,316 369,154 541,823 30 87 0 19,316 368,132 530,381 31 88 0 19,316 366,975 519,023 32 89 0 19,316 365,684 507,741

200,000 231,792

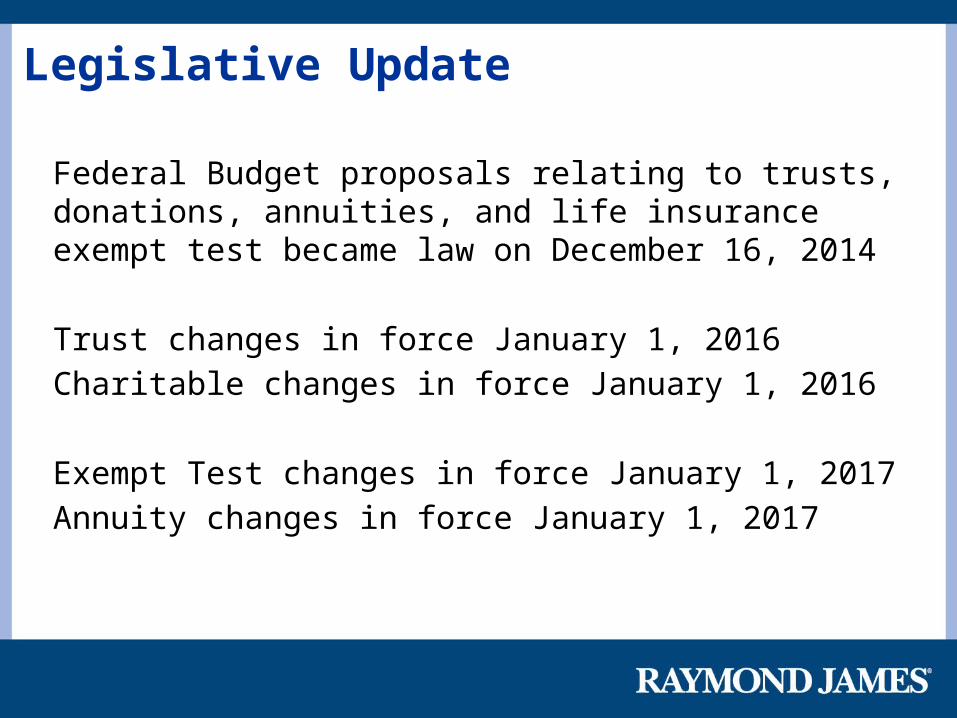

Legislative Update

Federal Budget proposals relating to trusts, donations, annuities, and life insurance exempt test became law on December 16, 2014

Trust changes in force January 1, 2016

Charitable changes in force January 1, 2016

Exempt Test changes in force January 1, 2017

Annuity changes in force January 1, 2017

Legislative Update

Source: CALU

$100,000 Life Annuity with 3 year Guarantee

Current Interest Environment Age 70

Legislative Update

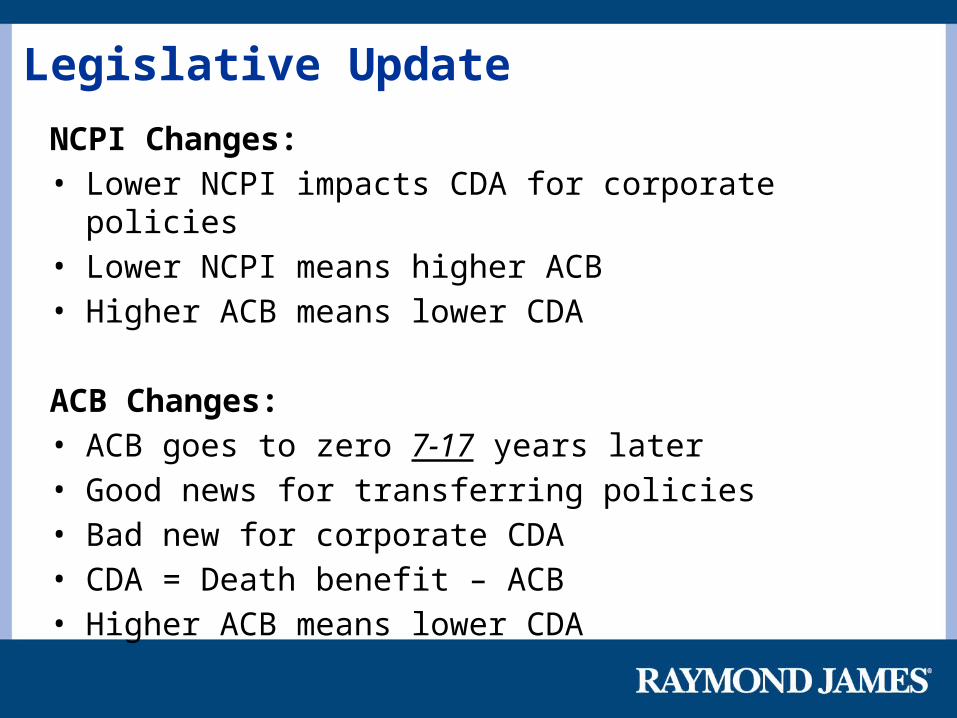

NCPI Changes:• Lower NCPI impacts CDA for corporate policies• Lower NCPI means higher ACB• Higher ACB means lower CDA

ACB Changes:• ACB goes to zero 7-17 years later• Good news for transferring policies• Bad new for corporate CDA• CDA = Death benefit – ACB• Higher ACB means lower CDA

Legislative Update

OPPORTUNITIES!

• Higher NCPI is good news for:− Collateral loan deduction on leveraged insurance− Capital Dividend Account for corporate insurance

• Term Conversions

• Prescribed Annuities

Thank you!

Questions??