corporate governance guidelines for building high ... contents canadian coalition for good...

TRANSCRIPT

THE VOICE OF THE SHAREHOLDER

Corporate Governance Guidelines

for

Building High Performance Boards

VERSION 1.0

NOVEMBER 2005

WEB SITE: WWW.CCGG.CA E-MAIL: [email protected]

2

CONTENTS Canadian Coalition for Good Governance 3

The Importance of Corporate Share Ownership 4

INDIVIDUAL DIRECTORS: OUTSTANDING BOARDS RECRUIT EFFECTIVE, COMMITTED AND INDEPENDENT DIRECTORS GUIDELINE ONE: Ensure Quality Motivation of Board Members 7

GUIDELINE TWO: Require Director Share Ownership 9

GUIDELINE THREE: Appoint Majority of Independent Directors 11

BOARD STRUCTURE: OUTSTANDING BOARDS HAVE CLEARLY DESIGNED ROLES AND RESPONSIBILITIES GUIDELINE FOUR: Separate Chair and Chief Executive Officer 12

GUIDELINE FIVE: Establish Independence and Mandates of Board Committees 13

GUIDELINE SIX: Follow “New” Audit Committee Requirements 14

BOARD PROCESSES: OUTSTANDING BOARDS STRIVE TO CONTINUOUSLY IMPROVE THEIR PERFORMANCE GUIDELINE SEVEN: Evaluate Performance of Boards and Committees 15

GUIDELINE EIGHT: Review Performance of Individual Board Members 16

GUIDELINE NINE: Assess CEO and Plan Succession 17

GUIDELINE TEN: Provide Management Oversight and Strategic Planning 18

GUIDELINE ELEVEN: Oversee Management Evaluation and Compensation 19

GUIDELINE TWELVE: Report Governance Policies and Initiatives to Shareholders 21

APPENDICES ONE: Director Share Ownership Requirements at Selected Canadian Corporations 24

TWO: Further Definitions of Director Independence 26

THREE: Sample Annual Board Effectiveness Survey 29

FOUR: Charter of Expectations for Directors 32

FIVE: Sample Director Peer Feedback Survey 33

SIX: Coalition Members 34

3CANADIAN COALITION FOR GOOD GOVERNANCE

The Canadian Coalition for Good Governance is a not-for-profit corporation.

The Coalition’s mission is the promotion of high performance boards to ensure the

interests of boards and management are aligned with those of the shareholder.

Coalition members manage approximately $825 billion in assets on behalf of pension

fund contributors, mutual fund unit holders and other individual investors. Shares in

publicly traded Canadian corporations are a substantial proportion of these assets.

The investment returns on the assets managed by pension funds, mutual funds and

independent money managers are critical to financing the retirement security of millions

of Canadians. To enhance the likelihood of real value creation it is paramount that

corporations be governed to the highest performance standards.

As a result, the Coalition is dedicated to the continuing improvement of corporate

governance practices.

4THE IMPORTANCE OF CORPORATE SHARE OWNERSHIP

The Coalition’s goal is to support boards of directors in achieving best governance

practices. Our members want the companies they invest in to succeed.

The governance concerns of institutional investors have grown in recent years as

pension funds, mutual funds and independent money managers acquired significant

ownership positions in publicly traded corporations. Today, as much as one-third of the

shares of Canada’s major corporations are owned by institutions managing the savings

of Canadians. With this shift in corporate ownership, clearer expectations of how

corporations should be governed have emerged.

As suppliers of corporate capital, Coalition members are dedicated shareholders. Being

patient and supportive shareowners involves sharing the responsibility to work with

boards in adopting progressive governance practices that are likely to enhance long-

term investment returns and reduce governance risk.

Being shareholders, Coalition members exercise their franchise to vote their shares.

They wish to do so in a responsible manner. By creating a set of governance guidelines,

the members of the Coalition will be able to work with boards of directors and senior

managers to reduce governance risk and to vote their shares responsibly.

Coalition members believe in one share – one vote structures. There are some 45

Canadian listed companies on the S&P/TSX Composite Index with share structures that

do not represent one share – one vote. While there are special circumstances to be

considered, the Coalition is not in favour of capital structures that provide more than one

vote for one share.

Coalition members recognize that many other Canadian corporations are closely held by

virtue of equity holdings rather than voting rights. Shareholders who control companies

through large equity positions will be closely involved in the affairs of that company. The

Coalition recognizes that such companies may not meet all the standards set out in the

guidelines but may well have an effective governance structure that balances the

interests of minority shareholders with the interests of the controlling shareholder.

5Companies with such controlling shareholders should be able to demonstrate a strong

long-term record of creating shareholder value for both the controlling shareholder and

the minority shareholders.

We are committed to considering carefully the balance between financial performance

and appropriate corporate governance definitions, structures and processes to judge

whether the interests of minority shareholders are appropriately recognized and

protected. There are few easy governance solutions that apply to all companies or all

situations.

Our focus is on:

1. How individual directors of extraordinary qualities are selected. Outstanding

boards recruit outstanding directors.

2. How boards are structured to create team governance strengths. Outstanding

boards have clearly designed roles and responsibilities.

3. How boards work to ensure good governance processes. Outstanding boards

strive to continuously improve their performance.

Many companies already have excellent governance and first-rate executive leadership

committed to the healthy growth of the company in the best interests of shareholders. At

most, these companies may require fine-tuning of their governance as investor

expectations evolve and change. Other companies have yet to achieve what we

describe in this document as “minimum standards”.

The twelve guidelines that follow include “minimum standards” and “best practices”.

“Minimum standards” are exactly that: standards we would normally expect a

publicly held corporation to meet.

“Best practices” are a combination of:

o “best practices” from high performing boards that we would like to see

in most cases and

o innovative ideas from outstanding boards that may be applicable to

other boards

Board chairs and governance committees will assess their own practices. Some “best

practice” ideas and “innovative ideas” may be adopted and others rejected.

6

Corporate governance will continue to grow in importance. For example, governance-

scoring systems are being developed by securities rating agencies, proxy voting firms

and university business schools. These scoring systems are benchmarks for helping

investors to make more informed decisions about the governance risk of corporations in

which they invest. The Coalition uses a governance rating system, developed by the

Rotman School of Management (University of Toronto), as a tool in identifying areas for

improvement and the overall state of governance risk in the companies owned by

Coalition members.

As Canadian institutional investors, our priority is to work with the boards of S&P/TSX

Composite Index companies. We want to engage in a constructive dialogue with the

directors of these companies around the concepts of minimum governance standards

and best practices. A range of governance practices provides some evolutionary

flexibility for companies in view of their history, share structure and ownership.

This document is a “living” document as evidenced in the label “Version 1.0”. The

document will evolve as the world changes and as the conversations with boards and

their directors deepen. Over time there will be many new “best practices” and today’s

”best practices” will become minimum standards1.

*****

We believe that a thoughtful approach to understanding each other’s governance

concerns will ultimately serve the long term best interests of corporate boards,

management and shareholders as well as the millions of Canadians on whose behalf

Coalition members invest.

1 Following the fifth major governance study since the 1992 Cadbury Report the United Kingdom has just published a new Combined Code on Corporate Governance following the reports of Derek Higgs on ‘Improving the Effectiveness of Non-Executive Directors’ (January, 2003), Nigel Turnbull on ‘Internal Controls’ (September, 1999) and Sir Robert Smith on “Audit Committees” (January, 2003). The new “Combined Code” can be found at www.frc.org.uk

7

Individual Directors: Outstanding Boards Recruit Effective, Committed and Independent Directors

GUIDELINE ONE: Ensure Quality Motivation of Board Members The single most important corporate governance requirement is the quality of directors.

By quality we mean directors with the integrity, competencies, capabilities and

motivation to carry out their fiduciary duties in the long term best interests of the

corporation and all of its shareholders.

While quality is a subjective requirement and defies legislative or regulatory definition, it

is essential for good governance. Boards should examine their membership to ensure

that directors meet standards of quality, individually and collectively as a governance

team.

Minimum Standards (for individual directors and board as a whole):

Demonstrate integrity and high ethical standards.

Have career experience and expertise relevant to the corporation’s business

purpose, financial responsibilities and risk profile. Each director’s career

experience and qualifications should appear in all appropriate public documents.2

Have proven understanding of fiduciary duty.

Have financial accreditation and/or be financially literate.

Demonstrate well developed listening, communicating and influencing skills so

that the individual directors can actively participate in board discussions and

debate.

Devote time to serve effectively as a director by not over-committing to other

corporate and not-for-profit boards.

2 The goal of the company should be to attain continuous and conspicuous disclosure of all significant facts, policies and procedures to all shareholders simultaneously.

8 Best Practices (for individual directors and board as a whole):

Create a formal, rigorous and transparent procedure for the appointment of new

directors to the board. Maintain a ‘matrix’ of director talents and board requirements to identify skill gaps

on the board. Build an “ever-green” list of candidates to ensure outstanding candidates with the

needed talents can be identified to fill planned or unplanned vacancies.3

Ensure plans are in place for orderly succession of directors to keep the board

appropriately balanced in terms of skills and experience.

Establish a full, formal and tailored induction program for each new director.4

Encourage all directors to continuously update their skills as well as their

knowledge of the company, its businesses and key executives.

3 Planning director succession well in advance will enrichen and deepen the pool of potential candidates. The Higgs report in the United Kingdom put great emphasis on recruiting outside the “old boys” network. Laura D’Andrea Tyson, dean of the London Business School, chaired a committee seeking to create broader pools of talent with varied and complementary skills, experiences and perspectives to enhance board effectiveness see http://www.womenandequalityunit.gov.uk/boardroom_diversity/index.htm4 A listing of materials commonly used in UK induction programmes can be found at www.icsa.org.uk. This site also contains useful examples of committee charters and a draft “letter of offer” to prospective directors.

9

GUIDELINE TWO: Require Director Share Ownership Directors can more effectively represent the interests of shareholders if they are also

shareholders. This alignment occurs when directors have a significant investment in the

shares of the companies they govern.5,6

Boards should determine an appropriate share ownership level for their members, such

as five times the annual director fees. See Appendix One for examples from some of

Canada’s largest corporations. This level of share ownership should be required after a

reasonable phase-in period for new directors and the approved market-value level

should be maintained throughout board tenure.

As part of their compensation, shares should be granted to directors at market value or

as deferred share units (DSUs). DSUs are bookkeeping entries, equivalent in value to a

common share and with the dividend rights of a common share. Units are maintained

until the director retires at which time the director can claim the shares or the cash

equivalent of the face value of the shares.

Stock options are an inappropriate form of compensation for the directors of large and

established corporations. Directors are governing fiduciaries. Consequently, their

compensation should not be incentive based, which is the usual purpose of stock

options. Directors entitled to stock options have no capital at risk, which means their

financial interests are not aligned with the interests of shareholders. Stock options focus

attention on short-term and volatile share performance so that they can be granted when

share prices decline and exercised when share prices rise. None of this is in the long

term best interests of shareholders and can undermine the focus of directors and

5 A 1999 study by Bhagat, Carey and Elson concluded that “there was a significant correlation between the amount of stock owned by individual outside directors and firm performance … The greater the dollar value of the individual outside director’s equity holdings in the enterprise, the more likely a disciplinary-type CEO turnover in a poorly performing company would exist.” 6 “Outside Directors with a Stake: The Linchpin in Improving Governance” by Donald C. Hambrick and Eric M. Jackson, published in California Management Review, Summer 2000, found that the greatest board-level predictor of a company’s long-term total shareholder returns was the percentage of outside board members with significant equity stakes in the company.

10management on the company’s long-term sustainability.7 Numerous Canadian

companies have abolished stock options for directors and replaced them with stock

grants and minimum ownership requirements during tenure with the company.8

Minimum Standards:

Require directors to own at least the equivalent of three years’ annual fees in the

form of shares or deferred share units after five years on the board.

Stop stock option grants (but grants of shares or DSUs are acceptable).

Hold the prescribed minimum market value level of shares during board tenure.

Define and report to shareholders on the share ownership requirements and

conditions for directors.

Best Practices:

Require directors to own the equivalent of five years’ annual fees in the form of

shares or deferred share units after five years on the board.

Stop stock option grants (but grants of shares or DSUs are acceptable).

Continue to invest a significant portion of annual compensation in shares once

the required multiple is met (as appropriate to individual circumstances).

Provide full disclosure of the actual compensation of each director9 and disclose

the percent of total compensation taken in shares or DSUs by each director.

Disclose share ownership changes, if any, by each director annually in all

appropriate public documents.

7 “Taking Stock” an article by Roger Martin, Dean of the Rotman School of Management, University of Toronto, published in the January 2003 Harvard Business Review, argues that if stock-based compensation is used, long vesting periods should be required, selling should be prohibited until leaving the company, stock (rather than stock options) should be granted, and directors and managers should announce their intention to sell stock or exercise options one week before the actual transaction. 8 Appendix One lists the practices of some leading Canadian corporations that have abolished Director stock options and installed minimum share ownership requirements. 9 The Bank of Nova Scotia is an example of suggested practice in disclosing director fees. See page 13 of the 2005 Management Proxy Circular for the 173rd Annual and Special Meeting of Shareholders.

11GUIDELINE THREE: Appoint Majority of Independent Directors

Independent directors should form the majority of every board. Independence is usually

taken to mean that the director is independent of management and has no material

relationship with or financial benefit from the company other than director fees and share

ownership. Consequently, the interests of an independent director should align with

those of shareholders.

The TSX guidelines refer to an “unrelated” director. The definition of independence we

use is based on that definition. American stock exchanges and institutional investors

have gone further and defined independence more rigourously. (See Appendix Two).

Minimum Standards: Build a board where the majority of directors are independent of management

and have no material relationship with the company other than director fees and

share ownership.

Ensure former employees and professionals who provided services to the

company are not nominated for at least three years after leaving their

employment (for NYSE listed companies this will be five years).

Define and report to shareholders the company’s definition of independence and

conflict of interest guidelines.

Best Practices: Build a board where at least two-thirds of directors are independent of

management and have no material relationship to the company other than

director fees and share ownership.

Define and report to shareholders the number of board interlocks10 that exist on

the board and the number the board considers appropriate as a policy guideline.

10 Interlock definition - when two Directors of Company A sit on the board of Company B that is called an interlock. Too many interlocks on any board suggests a degree of inter-related interests that might be detrimental to director independence.

12

Board Structure: Outstanding Boards Have Clearly Designed Roles and Responsibilities

GUIDELINE FOUR: Separate Chair and Chief Executive Officer

The board chair is responsible for leading the board and ensuring that it acts in the long

term best interests of shareholders in overseeing management and the company’s future

growth. These responsibilities should require a considerable commitment of time and

effort, as the chair is the board’s primary contact with the company. The chief executive

officer is responsible for leading management, developing and implementing the

company’s growth strategy, and reporting progress to the board.

The responsibilities and focus of the two positions are different. Separating the roles

resolves inherent conflicts of interest and clarifies accountability – the chair to the

shareholders and the CEO to the board.

It is not easy for companies that combine the chair/CEO functions to set aside a tradition

that they believe works in order to adopt a new model. As a transition, these companies

should consider appointing an independent lead director.

Minimum Standards:

Appoint a lead director separate from the chair/CEO. Define and report to shareholders the responsibilities of the lead director and the

chair. Have the lead director set board agendas with the chair/CEO and

be responsible for the quality of the information sent to directors. Require the lead director to call and chair quarterly meetings of independent

directors without management present. Require the former CEO to leave the board following retirement.

Best Practices:

Appoint an independent director as the chair. Define and report to shareholders the responsibilities of the chair. Establish and report to shareholders the annual review process for the chair. Have the independent chair set board agendas with the CEO and be responsible

for the quality of the information sent to directors. Require chair to hold in camera sessions of independent directors, without

management present, at every board meeting and every committee meeting.

13

GUIDELINE FIVE: Establish Independence and Mandates of Board Committees

A large part of board work is done in committee. Most conflicts between the interests of

management and those of shareholders are likely to first arise at the committee level.

Most, if not all, board committees should be composed only of independent directors. It

is poor governance for management directors to approve on behalf of shareholders the

policies, procedures and appointments that they themselves have recommended. The

audit committee, for example, reviews and approves the financial statements, as well as

risk management and internal controls, developed by management. (See Guideline Six).

The compensation committee reviews and approves the performance and compensation

of the chief executive officer and other senior executives. The nominating/governance

committee selects and recommends board candidates to oversee management.

Standards:

Appoint a majority of independent directors to the nominating/governance and

compensation committees.

Disclose the mandate of each committee in all relevant public documents.

o Ensure nominating/governance committee is responsible for the response

to the TSX governance guidelines.

o Ensure the nominating/governance committee has developed policies

and procedures to allow a director to engage outside advisors at the

expense of the board in appropriate circumstances.

Hold in camera sessions, without management present, of independent directors

as a regular part of all committee meetings.

14GUIDELINE SIX: Follow “New” Audit Committee Requirements The work of audit committees is critical to the restoration of confidence in Canadian

capital markets. The rigour of Canadian provisions for audit committees should be

comparable to provisions (now law) in the United States. This means boards must select

experienced and engaged directors for audit committees. Under such leadership, audit

committees are responsible for having transparent and understandable financial

statements prepared that fairly reflect the financial affairs of the corporation.

Under the SEC regulations in the United States and the rules of the Canadian Securities

Administrators, a number of profound changes have begun to take effect.

The Coalition expects every Audit Committee to comply fully with the enacted and

emerging regulatory standards and has no further standards to propose.

The Canadian Securities Administrators’ rule can be found at:

http://www.osc.gov.on.ca/Regulation/Rulemaking/Current/Part5/rule_20040326_52-108-aud-oversight.jsp

The Securities and Exchange Commission (SEC) in the United States has enacted a

final rule that can be found at:

http://www.sec.gov/rules/final/33-8220.htm

15

Board Processes: Outstanding Boards Strive to Continuously Improve their Performance

GUIDELINE SEVEN: Evaluate Performance of Boards and Committees

The board, through the nominating/governance committee, should have processes to

evaluate and improve its performance and that of its committees. A growing governance

practice is for boards to confidentially survey members once a year with the results

reviewed by the nominating/governance committee. This should better enable boards to

make structural and process changes. See Appendix Three for a sample survey.

Minimum Standards: Publish a charter of expectations for directors in all appropriate public

documents. An example can be found in Appendix Four.

Review annually the performance of the board and its committees measured

against criteria defined in the board and committee mandates as well as the

directors’ charter. Disclose the process in all appropriate public documents.

Manage succession planning for directors (see also Guideline One – Best

Practices) to keep the board appropriately balanced in terms of skills and

experience. Publish each director’s experience, expertise and other directorships annually in

all appropriate public documents to disclose the mix of directors currently

serving.

Allow shareholders to vote for individual directors annually; no slates.

Best Practices: Monitor closely at the governance committee level the emerging best practices at

leading corporations.

16GUIDELINE EIGHT: Review Performance of Individual Board Members

The board, through the nominating/governance committee, can improve their

performance over time by helping individual directors build on their strengths and take

advantage of improvement opportunities.

Annual performance reviews enable directors to assess their personal strengths and

weaknesses, make decisions about their need for further education, and may even lead

to a decision as to the appropriate time to step down.

Minimum Standards: Establish a minimum attendance expectation for the directors.

Publish the attendance of individual board members annually in all appropriate

public documents.

Decide upon the types of events that would normally lead to a director tendering

a resignation to the governance committee (i.e. failure to meet attendance

expectations; age limit; change in principal occupation or place of residence).

Depending upon the individual circumstances the resignation may or may not be

accepted.

Best Practices: Evaluate the performance of individual directors annually through a confidential

peer-review survey. The independent board chair, chair of the governance

committee or independent third party should conduct the survey. Open-ended

questions should be included to provide an opportunity for suggesting

improvements.11,12 See Appendix Five for a sample.

Evaluate the performance of the chair annually against the standards established

in the role of the chair in Guideline Four.

Report the performance review processes in all appropriate public documents

with sufficient detail to indicate there is a strong and viable system in use.

11 The United Kingdom’s new Combined Code on Corporate Governance calls for the performance evaluation of individual directors in section A.6. The new “Combined Code” can be found at www.frc.org.uk12 In the United States the Conference Board Commission on Public Trust and Private Enterprise calls for a “three tier evaluation of the performance of the board as a whole, the performance of each committee, and the performance of each individual director.”

17GUIDELINE NINE: Assess CEO and Plan Succession The board is responsible for hiring and if necessary firing the chief executive officer,

reviewing annually his or her performance, and having a succession plan in place. To

remove any doubt of the CEO’s accountability to the board, it is essential for boards to

have a job description for the CEO, to establish with the CEO annual and longer term

performance targets, expectations and related compensation incentives, and to establish

a formal review process in which directors and the CEO can candidly exchange views on

the CEO’s performance. A clear understanding between the board and the CEO

regarding the CEO’s expected performance and leadership should produce a supportive

board.

Often the work on these matters is done at the committee level and brought back to the

full board for discussion and approval.

Minimum Standards:

Develop a CEO job description and publish in all appropriate public documents.

Establish annually short-term and long-term CEO performance objectives.

Develop an annual CEO review process by the board with the CEO.

Review annually the CEO succession plan, including a review with the CEO on

the performance of direct reports.

Best Practices:

Expect directors to make it their business to know the senior executives and high

potential candidates by visiting them in their workplace.13

Create opportunities for high-potential executives to make frequent presentations

to the board and to meet socially with the board.

13 General Electric is an example of a company with best governance practices that requires each director to visit two GE businesses a year without corporate management present so that the director has direct exchanges with operating leaders.

18GUIDELINE TEN: Provide Management Oversight and Strategic Planning

On behalf of the owners, the board delegates the management of the company to a

team of executives committed to enhancing shareholder value. The directors are

responsible for setting the overall vision and long-term direction of the company,

including risk and return expectations and non-financial goals. Management’s primary

job is to develop and implement an appropriate growth strategy that responds to the

board’s direction. This process involves reviewing, questioning, discussing and

ultimately approving management’s recommended (or amended) growth strategy. The

directors should subsequently ensure that management’s decisions are consistent with

the vision, objectives, goals and parameters of the approved strategy. Management’s

compensation and tenure should be based on management having successfully

implemented the growth strategy it recommended to the board.

Minimum Standards:

Meet annually to review in depth the company’s strategic plan.

Conduct an annual review of human, technological and capital resources

required to implement the company’s growth strategy and the regulatory, cultural

or governmental constraints on the business or businesses.

Monitor the execution of the strategy and the achievement of objectives.

Best Practices:

Review at every board meeting recent developments (if any) that may impact

growth strategy.

Evaluate management’s analysis of the strategies of competitors or ‘quasi’

competitors.14

14 Too often companies think of themselves as operating in isolation. A healthier attitude is the adoption of Andrew S. Grove’s title “Only The Paranoid Survive.” Mr. Grove was CEO of Intel and his book describes the tortuous challenges of recognizing and responding to the need for change. Also see Clayton M. Christensen “The Innovators Dilemma” on why great companies can fail.

19GUIDELINE ELEVEN: Oversee Management Evaluation and Compensation

Senior executives should be fairly and competitively compensated. Preferably a large

portion of compensation should be performance based, with an emphasis on granting

shares (not options) as a performance incentive.15

Executives should be significant shareholders in the company they lead. This will better

align their financial interests with those of shareholders.

Minimum Standards: Structure the compensation committee to consist of only independent directors.16

Link the management compensation program to meaningful and measurable

performance targets.

Disclose the overall compensation philosophy for senior executives in all

appropriate public documents explaining the rationale for salary levels, incentive

payments, stock grants (real or phantom), stock options, pensions (including all

supplemental plans) and all other components of executive compensation.

Empower the compensation committee to have authority to seek independent

compensation advice as required.

Build in camera sessions of independent directors, without management present,

into every compensation committee meeting and at the full board meeting when

executive compensation issues are discussed.

Limit stock options strictly in number and ensure those that are granted are

focused on long-term remuneration and subject to vesting periods.

Ensure all equity-based compensation plans are subject to shareholder approval.

Best Practices: Include at least one director experienced in executive compensation on the

compensation committee.

15 Professors Brian Hall of the Harvard Business School and Kevin Murphy of the University of Southern California estimate that the cost of granting stock options to the employees is far greater than their value to employees. The incentive effects of options are also ‘fragile’ as employees do not usually regard an underwater option as a benefit. 16 Originally this guideline stated that there should be a majority of independent directors on the Compensation Committee. This guideline was changed to coincide with Guideline One: Build an Independent Compensation Committee of the Guidelines for Principled Executive Compensation.

20 Have the chair of the compensation committee answer questions at the Annual

General Meeting that relate to executive compensation.

Require senior executives to hold shares throughout their tenure with the

company.

Design options that have performance hurdles so that pulmonary success alone

does not determine their vesting.

Consider establishing holding conditions for options to ensure that the stock

ownership targets are met and exceeded.

21GUIDELINE TWELVE: Report Governance Policies and Initiatives to Shareholders

In their accountability to the company’s owners, boards should make every effort to help

shareholders better understand their policies with respect to governance, and their

management oversight and control responsibilities. Communicating with shareholders

should be undertaken using every possible media channel including print, the company

web site and web casts, to Annual General Meetings where questions are encouraged.

The goal of the company should be to attain continuous and conspicuous disclosure of

all significant facts, policies and procedures to all shareholders simultaneously.

Standards:

Report in the proxy circular (and all other appropriate public documents)

compliance with the governance requirements of regulators17, stock exchanges18

and professional authorities in all jurisdictions where the company’s securities

trade and explain any non-compliance. These disclosures should be as specific

as possible to engender confidence that more than lip service is being paid in

complying with these requirements.

Report in the annual report the company’s governance philosophy, practices and

monitoring processes where these standards incorporate or exceed regulated

requirements.

Report in the chair’s section of the annual report substantive issues, changes

and developments in corporate governance practices at the company that could

affect shareholder interests.

Guideline Two: Provide full disclosure of the actual compensation of each

director in the proxy circular and disclose the percent of total compensation taken

in shares or DSUs by each director.

Disclose all changes in director share ownership annually.

Guideline Three: Define and report to shareholders the company’s definition of

independence and conflict of interest guidelines.

17 The Canadian Securities Administrators’ corporate governance disclosure requirements can be found at http://www.osc.gov.on.ca/Regulation/Rulemaking/Current/Part5/rule_20050617_58-101_disc-corp-gov-pract.jsp. 18 The current TSX corporate governance disclosure guidelines are found at http://142.201.0.1/en/pdf/CompanyManual.pdf Sections 473 and 474.

22 Guideline Four: Define and report to shareholders on the responsibilities of the

chair (or lead director). Establish and report to shareholders the annual review process for the chair (or

lead director).

Guideline Five: Disclose mandate of each committee.

Guideline Six: Conform to all regulatory requirements.

Guideline Seven: Publish a charter of expectations for directors. An example

can be found in Appendix Four.

o Include reasonable estimates of the time required for directors to prepare

for and attend board and committee meetings.

o Specify the criteria that trigger a resignation, such as poor meeting

attendance, a change in principal occupation, an age limit, or poor board

and committee performance in the opinion of fellow directors.

Publish each director’s experience, expertise and other directorships annually.

Report performance review process.

Guideline Eight: Publish the attendance of individual board members annually.

Report the performance review processes with sufficient detail to indicate there is

a strong and viable system in use.

Guideline Eleven: Disclose the overall compensation philosophy for senior

executives explaining the rationale for salary levels, incentive payments, stock

grants (real or phantom), stock options, pensions (including all supplemental

plans) and all other components of executive compensation.

23

APPENDICES

24

APPENDIX ONE: DIRECTOR SHARE OWNERSHIP REQUIREMENTS There are three kinds of targets established for director share ownership at major corporations:

1. Based on a multiple of the annual retainer: for example,

Bank of Montreal requires each director to hold 6 times the value of the annual retainer of $30,000 (or $180,000 in aggregate) in company stock.

2. Based on an absolute number of shares: for example,

BCE requires each director to hold 10,000 shares (approximately $300,000).

3. Based on a total dollar investment in company stock: for example,

George Weston requires an aggregate investment of $250,000.

Each of the companies in the following table has a share ownership target plus a DSU or RSU plan in place as a tax-efficient method for directors to acquire company stock.

Value of Target Shares as a Multiple

of the Retainer

Bank of Montreal 6

BCE 2a

Canadian Imperial Bank of Commerce 6

Canadian National Railway 5.7b

George Weston Limited 7c

Loblaw Companies Limited 7c

Manulife 5

Petro-Canada 5

Royal Bank of Canada 10d

Sun Life Financial 6

TransCanada PipeLines Limited 5

Torstar 4e

a Requirement to hold 10,000 shares. Retainer paid in DSUs until threshold reached. The

multiple is low as the annual retainer was raised to $150,000. b Directors required to hold $250,000 in stock within 5 years of joining the board. c Directors are required to take their retainer and annual fees in DSUs until they hold $250,000 in

company stock. d Directors are required to hold $300,000 in company stock within 5 years. e Directors are required to hold 8,000 shares in company stock or DSUs within 4 years. All

compensation paid in DSUs until threshold is reached.

25DIRECTOR OPTION PLANS

More and more companies have stopped granting stock options to directors. The following companies are examples of corporations that have recently discontinued their director stock option plans. Agrium

Astral Media

Bank of Montreal

BCE

BCE Emergis

Canadian Imperial Bank of Commerce

Canadian National Railway

CI Funds

Gildan Activewear

Manulife Financial

Nexen

Royal Bank of Canada

Sun Life Financial

Torstar

26APPENDIX TWO: DEFINITIONS OF DIRECTOR INDEPENDENCE

Toronto Stock Exchange: Section 474 (2) of the TSX Company Manual

“An unrelated director is a director who is independent of management and is free from any interest and any business or other relationship which could, or could reasonably be perceived to, materially interfere with the director’s ability to act with a view to the best interests of the corporation, other than interests and relationships arising from shareholding.” New York Stock Exchange: http://www.nyse.com/pdfs/corp_recommendations_nyse.pdf

Listing standard adopted August 1, 2002; “NYSE Approves Measures to Strengthen Corporate Accountability”.

“For a director to be deemed ‘independent’, the board must affirmatively determine the director has no material relationship with the listed company (either directly or as a partner, shareholder or officer of an organization that has a relationship with the company). “Material relationships can include commercial, industrial, banking, consulting, legal, accounting, charitable and familial relationships (among others). “Independence also requires a five-year ‘cooling off’ period for former employees of the listed company, or of its independent auditor; and for immediate family members of the above.”

CalPERS: The California Public Employees' Retirement System http://www.calpers-governance.org/principles/domestic/us/page13.asp

1. Has not been an executive employed by the company in the last 5 years.

2. Is not, and is not affiliated with a company that is an advisor or consultant to the company in the last 5 years.

3. Is not affiliated with a significant customer or supplier to the company in the last 5 years.

4. Has no personal service contracts with the company or a member of senior management in the last 5 years.

5. Is not affiliated with a not-for-profit that is a significant beneficiary of the company over the last 5 years.

6. Is not employed by a public company of which an executive officer of the company serves as a director.

7. Has not had any of the above relationships with an affiliate of the company.

8. Is not related to any senior managers in the company, its suppliers or customers.

27

TIAA-CREF: Teachers Insurance and Annuity Association College Retirement

Equities Fund http://www.tiaa-cref.org/pubs/html/governance_policy/board_directors.htmlIndependence means no present or former employment by the company or any significant financial or personal tie to the company or its management that could compromise the director's objectivity and loyalty to the shareholders. An independent director does not regularly perform services for the company, if a disinterested observer would consider the relationship material. It does not matter if the service is performed individually or as a representative of an organization that is a professional adviser, consultant, or legal counsel to the company.

*****

For audit committee independence see the following:

Canadian Securities Regulators on Audit Committees (MI 52-110) Published June 27, 2003 for comment To qualify as independent, all committee members must not have a direct or indirect material relationship with the issuer. A material relationship is defined as a relationship that could, in the view of the issuer’s board of directors, reasonably interfere with the exercise of a member’s independent judgement. Certain categories of persons that are considered to have a material relationship are identified, some examples of those include: (i) a person who is or whose immediate family member is, an officer or employee of the issuer, its parent or any subsidiary or affiliated entity; (ii) a person who accepts any consulting, advisory or other compensatory fee from the issuer; or (iii) a person who is, or has been, an affiliated entity of, a partner of, or employed by, a current or former internal or external auditor of the issuer, unless the prescribed period has elapsed since the person’s relationship with the internal or external auditor, or the auditing relationship, has ended. U.S. Securities and Exchange Commission: http://www.sec.gov/rules/final/33-8220.htm#audit

Under the “Final Rule: STANDARDS RELATING TO LISTED COMPANY AUDIT COMMITTEES” there is a very detailed and extensive discussion of the standards of independence to be achieved.

28

United Kingdom: Independence in the July 2003 Combined Code The Combined Code on Corporate Governance (July, 2003) promulgated by the Financial Reporting Council of the United Kingdom www.frc.org.uk A.3.1 The board should identify in the annual report each non-executive director it considers to be independent. The board should determine whether the director is independent in character and judgement and whether there are relationships or circumstances which are likely to affect, or could appear to affect, the director’s judgement, The board should state its reasons if it determines that a director is independent notwithstanding the existence of relationships or circumstances which may appear relevant to its determination, including if a director:

• Has been an employee of the company or group within the last five years;

• Has, or has had within the last three years, a material business relationship with the company either directly, or as a partner, shareholder, director or senior employee of a body that has such a relationship with the company;

• Has received or receives additional remuneration from the company apart from a director’s fee, participates in the company’s share option or performance-related pay scheme, or is a member of the company’s pension scheme;

• Has close family ties with any of the company’s advisers, directors or senior employees;

• Holds cross-directorships or has significant links with other directors through involvement in other companies or bodies;

• Represents a significant shareholder; or

• Has served on the board for more than nine years from the date of their first election.

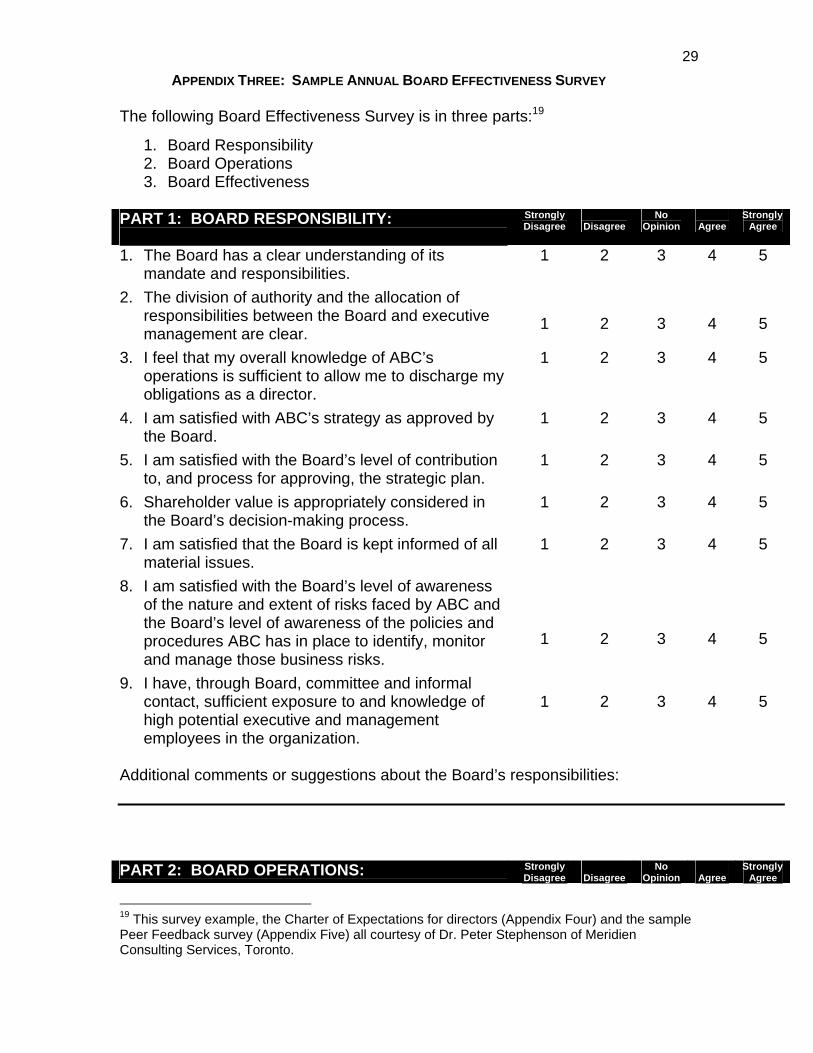

29APPENDIX THREE: SAMPLE ANNUAL BOARD EFFECTIVENESS SURVEY

The following Board Effectiveness Survey is in three parts:19

1. Board Responsibility 2. Board Operations 3. Board Effectiveness

PART 1: BOARD RESPONSIBILITY:

Strongly Disagree

Disagree

No Opinion

Agree

Strongly Agree

1. The Board has a clear understanding of its mandate and responsibilities.

1 2 3 4 5

2. The division of authority and the allocation of responsibilities between the Board and executive management are clear.

1

2

3

4

5

3. I feel that my overall knowledge of ABC’s operations is sufficient to allow me to discharge my obligations as a director.

1 2 3 4 5

4. I am satisfied with ABC’s strategy as approved by the Board.

1 2 3 4 5

5. I am satisfied with the Board’s level of contribution to, and process for approving, the strategic plan.

1 2 3 4 5

6. Shareholder value is appropriately considered in the Board’s decision-making process.

1 2 3 4 5

7. I am satisfied that the Board is kept informed of all material issues.

1 2 3 4 5

8. I am satisfied with the Board’s level of awareness of the nature and extent of risks faced by ABC and the Board’s level of awareness of the policies and procedures ABC has in place to identify, monitor and manage those business risks.

1

2

3

4

5

9. I have, through Board, committee and informal contact, sufficient exposure to and knowledge of high potential executive and management employees in the organization.

1

2

3

4

5

Additional comments or suggestions about the Board’s responsibilities: PART 2: BOARD OPERATIONS: Strongly

Disagree

Disagree No

Opinion

Agree Strongly

Agree

19 This survey example, the Charter of Expectations for directors (Appendix Four) and the sample Peer Feedback survey (Appendix Five) all courtesy of Dr. Peter Stephenson of Meridien Consulting Services, Toronto.

30

10. The frequency of Board and committee meetings

is adequate for me to fulfill my obligations as a director.

1 2 3 4 5

11. Sufficient time is scheduled for Board and committee meetings.

1 2 3 4 5

12. My time and talents are well-utilized at Board and committee meetings.

1 2 3 4 5

13. The Board has the right number of directors. 1 2 3 4 5 14. The Board has the right mix of experience and

skills to guide ABC towards achieving its strategic goals.

1 2 3 4 5

15. I am satisfied with the Board’s current committee structure.

1 2 3 4 5

16. I am satisfied that each of the following committees is performing as it should: • Audit Committee • Compensation Committee • Nominating and Corporate Governance

1 1 1

2 2 2

3 3 3

4 4 4

5 5 5

17. I am satisfied that the processes now in place to manage director succession and to nominate candidates for the Board are working well.

1

2

3

4

5

18. I am satisfied with the frequency and amount of time for discussion among independent directors without management present.

1

2

3

4

5

19. The briefing materials I receive are adequate and timely.

1 2 3 4 5

20. The performance and competitive information I receive allows me to monitor results, identify potential areas of concern and understand important industry issues/trends.

1

2

3

4

5

21. I have adequate access to officers outside of Board and committee meetings.

1 2 3 4 5

22. The Board should codify conflict of interest guidelines for directors.

1 2 3 4 5

Additional comments or suggestions about enhancing how the Board operates:

31

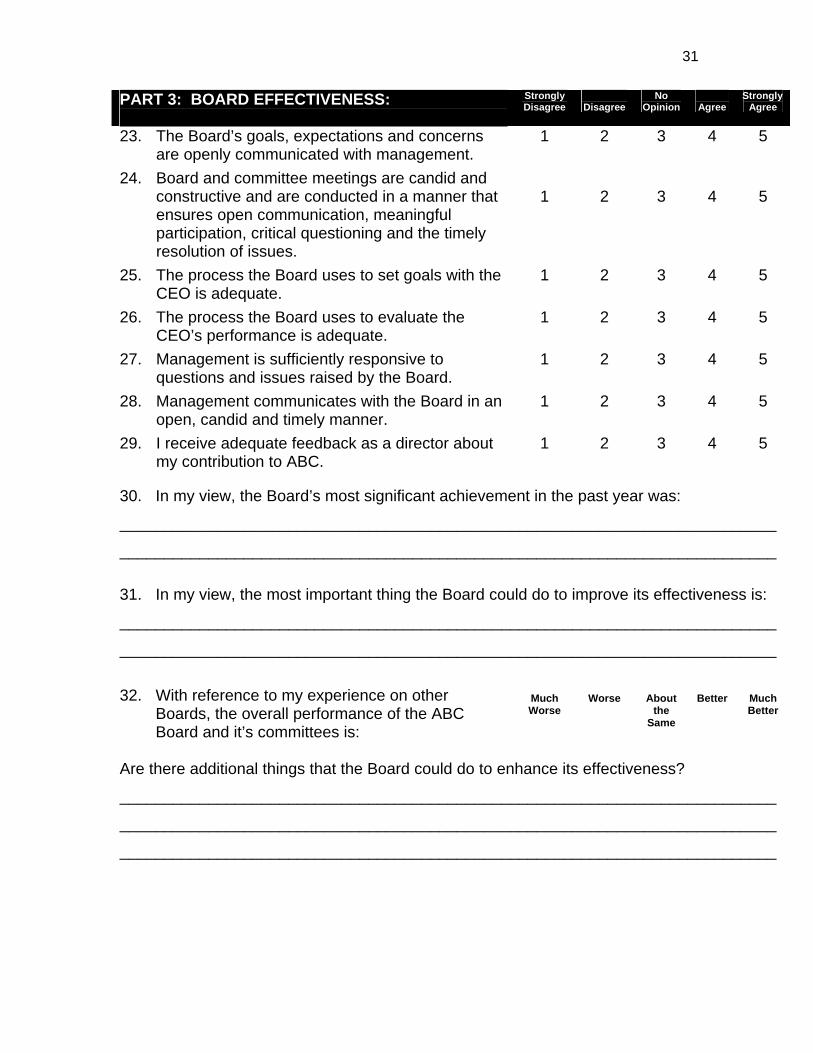

PART 3: BOARD EFFECTIVENESS:

Strongly Disagree

Disagree

No Opinion

Agree

Strongly Agree

23. The Board’s goals, expectations and concerns are openly communicated with management.

1 2 3 4 5

24. Board and committee meetings are candid and constructive and are conducted in a manner that ensures open communication, meaningful participation, critical questioning and the timely resolution of issues.

1

2

3

4

5

25. The process the Board uses to set goals with the CEO is adequate.

1 2 3 4 5

26. The process the Board uses to evaluate the CEO’s performance is adequate.

1 2 3 4 5

27. Management is sufficiently responsive to questions and issues raised by the Board.

1 2 3 4 5

28. Management communicates with the Board in an open, candid and timely manner.

1 2 3 4 5

29. I receive adequate feedback as a director about my contribution to ABC.

1 2 3 4 5

30. In my view, the Board’s most significant achievement in the past year was:

__________________________________________________________________________

__________________________________________________________________________

31. In my view, the most important thing the Board could do to improve its effectiveness is:

__________________________________________________________________________

__________________________________________________________________________

32. With reference to my experience on other

Boards, the overall performance of the ABC Board and it’s committees is:

Much Worse

Worse

About the

Same

Better

Much Better

Are there additional things that the Board could do to enhance its effectiveness?

__________________________________________________________________________

__________________________________________________________________________

__________________________________________________________________________

32

APPENDIX FOUR: CHARTER OF EXPECTATIONS FOR DIRECTORS

A Charter of Expectations for a Board of Directors sets out the roles and responsibilities to be discharged by directors. The Charter should also specify how the board delegates authority to manage the business of the organization to management. Components of a Board of Directors Charter might include: • An overall statement of the Board of Director’s responsibilities for supervising

the management of the business. • Strategic planning process and approval of strategy. • Selection, goal-setting, evaluation and compensation of senior management. • Management of risk, capital and internal controls. • Monitoring of progress against strategic and business goals. • Financial reporting and regulatory compliance. • Review and approval of material transactions. • Board operations and the evaluation of board and individual director

effectiveness. The Charter, or a separate document, should also specify the professional and personal competencies and characteristics expected of directors. These form the basis for the recruitment, selection and evaluation of directors. These competencies and characteristics might include: • Proven track record of sound business judgement and good business

decisions. • Demonstrated integrity and high ethical standards. • Financial literacy. • Appropriate knowledge of business and industry issues. • Specific knowledge and experience to support the development and/or

implementation of business strategy. • Communication and influencing skills. • Ability to contribute to the board’s effectiveness and performance. • Availability for board and committee work. In addition the Charter, or a separate document, should specify policies and guidelines for directors that might include: terms of office, share ownership, orientation, conflict of interest, attendance, compensation, change of occupation, media interaction and role of the Chair or Lead Director.

33

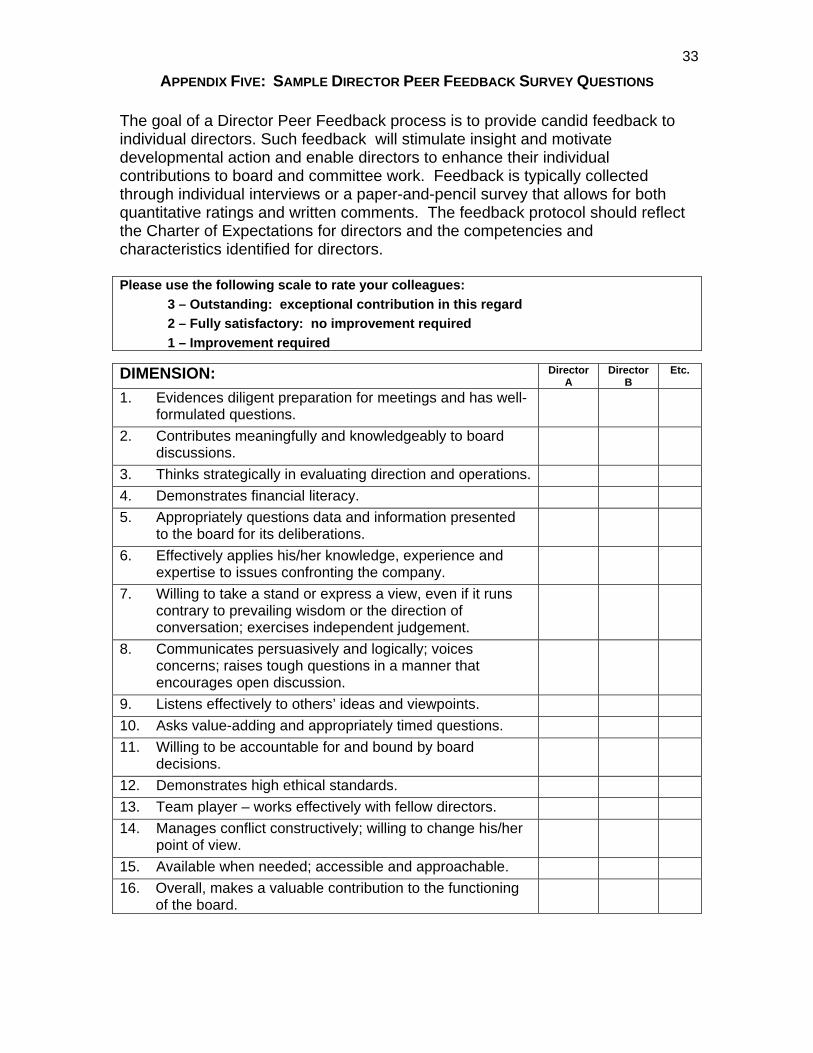

APPENDIX FIVE: SAMPLE DIRECTOR PEER FEEDBACK SURVEY QUESTIONS

The goal of a Director Peer Feedback process is to provide candid feedback to individual directors. Such feedback will stimulate insight and motivate developmental action and enable directors to enhance their individual contributions to board and committee work. Feedback is typically collected through individual interviews or a paper-and-pencil survey that allows for both quantitative ratings and written comments. The feedback protocol should reflect the Charter of Expectations for directors and the competencies and characteristics identified for directors. Please use the following scale to rate your colleagues:

3 – Outstanding: exceptional contribution in this regard 2 – Fully satisfactory: no improvement required 1 – Improvement required

DIMENSION: Director A

Director B

Etc.

1. Evidences diligent preparation for meetings and has well-formulated questions.

2. Contributes meaningfully and knowledgeably to board discussions.

3. Thinks strategically in evaluating direction and operations. 4. Demonstrates financial literacy. 5. Appropriately questions data and information presented

to the board for its deliberations.

6. Effectively applies his/her knowledge, experience and expertise to issues confronting the company.

7. Willing to take a stand or express a view, even if it runs contrary to prevailing wisdom or the direction of conversation; exercises independent judgement.

8. Communicates persuasively and logically; voices concerns; raises tough questions in a manner that encourages open discussion.

9. Listens effectively to others’ ideas and viewpoints. 10. Asks value-adding and appropriately timed questions. 11. Willing to be accountable for and bound by board

decisions.

12. Demonstrates high ethical standards. 13. Team player – works effectively with fellow directors. 14. Manages conflict constructively; willing to change his/her

point of view.

15. Available when needed; accessible and approachable. 16. Overall, makes a valuable contribution to the functioning

of the board.

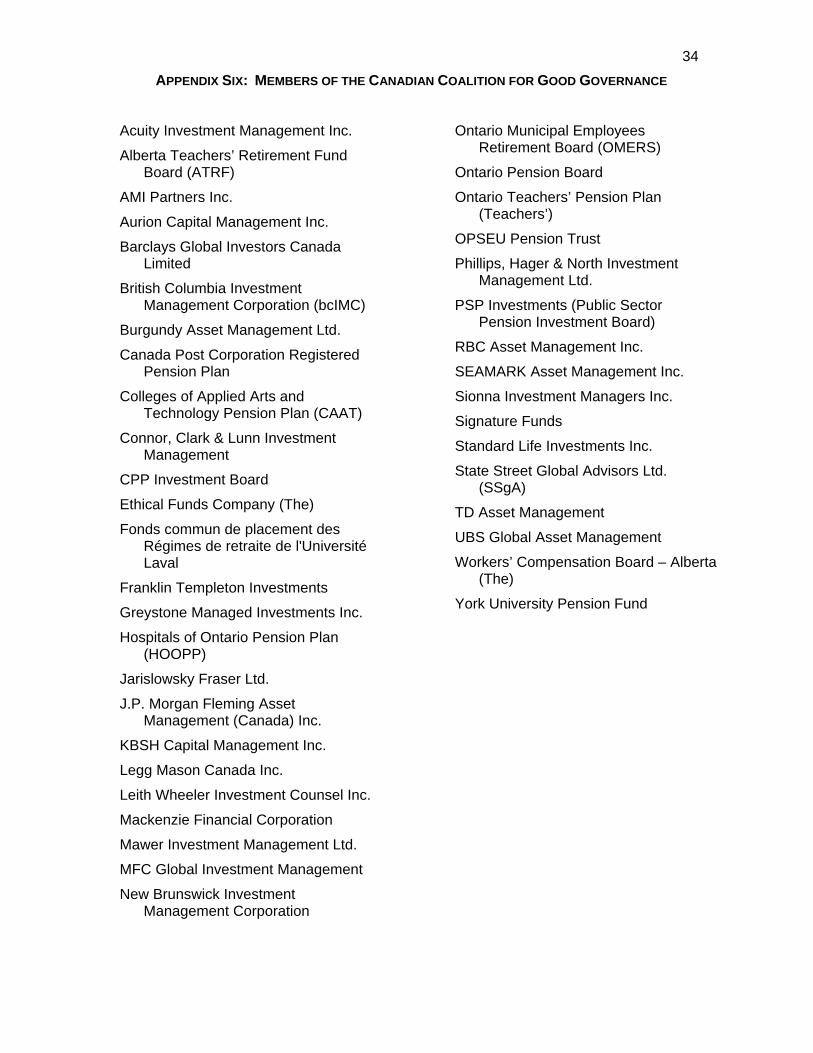

34 APPENDIX SIX: MEMBERS OF THE CANADIAN COALITION FOR GOOD GOVERNANCE

Acuity Investment Management Inc.

Alberta Teachers’ Retirement Fund Board (ATRF)

AMI Partners Inc.

Aurion Capital Management Inc.

Barclays Global Investors Canada Limited

British Columbia Investment Management Corporation (bcIMC)

Burgundy Asset Management Ltd.

Canada Post Corporation Registered Pension Plan

Colleges of Applied Arts and Technology Pension Plan (CAAT)

Connor, Clark & Lunn Investment Management

CPP Investment Board

Ethical Funds Company (The)

Fonds commun de placement des Régimes de retraite de l'Université Laval

Franklin Templeton Investments

Greystone Managed Investments Inc.

Hospitals of Ontario Pension Plan (HOOPP)

Jarislowsky Fraser Ltd.

J.P. Morgan Fleming Asset Management (Canada) Inc.

KBSH Capital Management Inc.

Legg Mason Canada Inc.

Leith Wheeler Investment Counsel Inc.

Mackenzie Financial Corporation

Mawer Investment Management Ltd.

MFC Global Investment Management

New Brunswick Investment Management Corporation

Ontario Municipal Employees Retirement Board (OMERS)

Ontario Pension Board

Ontario Teachers’ Pension Plan (Teachers’)

OPSEU Pension Trust

Phillips, Hager & North Investment Management Ltd.

PSP Investments (Public Sector Pension Investment Board)

RBC Asset Management Inc.

SEAMARK Asset Management Inc.

Sionna Investment Managers Inc.

Signature Funds

Standard Life Investments Inc.

State Street Global Advisors Ltd. (SSgA)

TD Asset Management

UBS Global Asset Management

Workers’ Compensation Board – Alberta (The)

York University Pension Fund