corporate financial management assignment - ratio analysis of hays plc

TRANSCRIPT

Ratio Analysis of Hays plc

Amany Hamza

Student number: 21202244

Tutor: Pat Coyle

Course

MBA / CFM

Word Count: 1990

(excluding Table of Contents, Cover Page, References and other

Appendices)

Date

14th December 2012

Table of Contents

1. INTRODUCTION ................................................................................................................................. 1

2. RATIO ANALYSIS OF HAS .................................................................................................................... 1

2.1. PROFITABILITY RATIOS ................................................................................................................ 1

2.1.1. RETURN ON CAPITAL EMPLOYED (ROCE) ............................................................................... 1

2.1.2. PROFIT MARGIN ................................................................................................................ 2

2.2. LIQUIDITY RATIOS ...................................................................................................................... 2

2.2.1. CURRENT RATIO ................................................................................................................ 2

2.3. GEARING RATIOS ....................................................................................................................... 3

2.3.1. BORROWING RATIO ........................................................................................................... 3

2.4. LEVERAGE RATIOS ...................................................................................................................... 3

2.4.1. INTEREST COVER RATIO ....................................................................................................... 3

2.5. INVESTMENT RATIOS .................................................................................................................. 4

2.5.1. DIVIDEND YIELD ................................................................................................................ 4

2.5.2. RETURN ON EQUITY (ROE) .................................................................................................. 4

2.6. EFFICIENCY RATIOS .................................................................................................................... 4

2.6.1. ASSET TURNOVER .............................................................................................................. 5

3. NAV, DVM AND PER: ....................................................................................................................... 5

3.1. SHARES VALUATION USING NAV .................................................................................................. 5

3.2. DIVIDEND VALUATION MODEL ..................................................................................................... 5

3.3. THE PER MODEL ....................................................................................................................... 6

4. CONCLUSION .................................................................................................................................... 8

5. REFERENCES ..................................................................................................................................... 9

1

1. INTRODUCTION

This report investigates the performance of Hays plc (HAS) during the period 2011-2012 to evaluate

the worthiness of HAS as a good investment.

HAS are ‘leading global experts in qualified, professional and skilled recruitment…They employ 7,800

staff in 245 offices across 33 countries’ (Hays plc, 2012)

2. RATIO ANALYSIS OF HAS

Gerald et al (2003) suggests that ‘Financial Ratios are computed by the managers to evaluate the

performance, progress and achievements of the company…They also help investors, creditors,

lenders and analysts in critically analysing an investment opportunity and credit decisions.’

2.1. PROFITABILITY RATIOS

They tell us whether a business is making profits - and if so whether at an acceptable rate

(Tutor2u, 2012).

2.1.1. RETURN ON CAPITAL EMPLOYED (ROCE)

It indicates the efficiency and profitability of a company's capital investments (Investopedia,

2012).

Return on Capital Employed (ROCE) = x 100%

On 30 June (£s millions)

2011 2012

= 25.9%110.70x 100

878.3-450.1

= 30.7%122.4x 100

862.5-463.6

Interpretation:

ROCE of 2012 is higher than 2011, which is an indication that the efficiency and

profitability of the company's capital investments in 2012 are better than 2011.

The ROCE grew by 4.8% which means that the return is £30.7 for every £100 of capital

employed. That can be due to:

1. The increase of 14m in the operating profit from 110.7m in 2011 to 122.4m in

2012.

2. The reduction in the amount of total assets by 15.8m; which could be associated

with the efficiency of assets’ utilization and generating more trade receivable as

noted¹ in the Annual Report.

Pre-tax Profit

Capital Employed

1 2

3 4 5 6

2

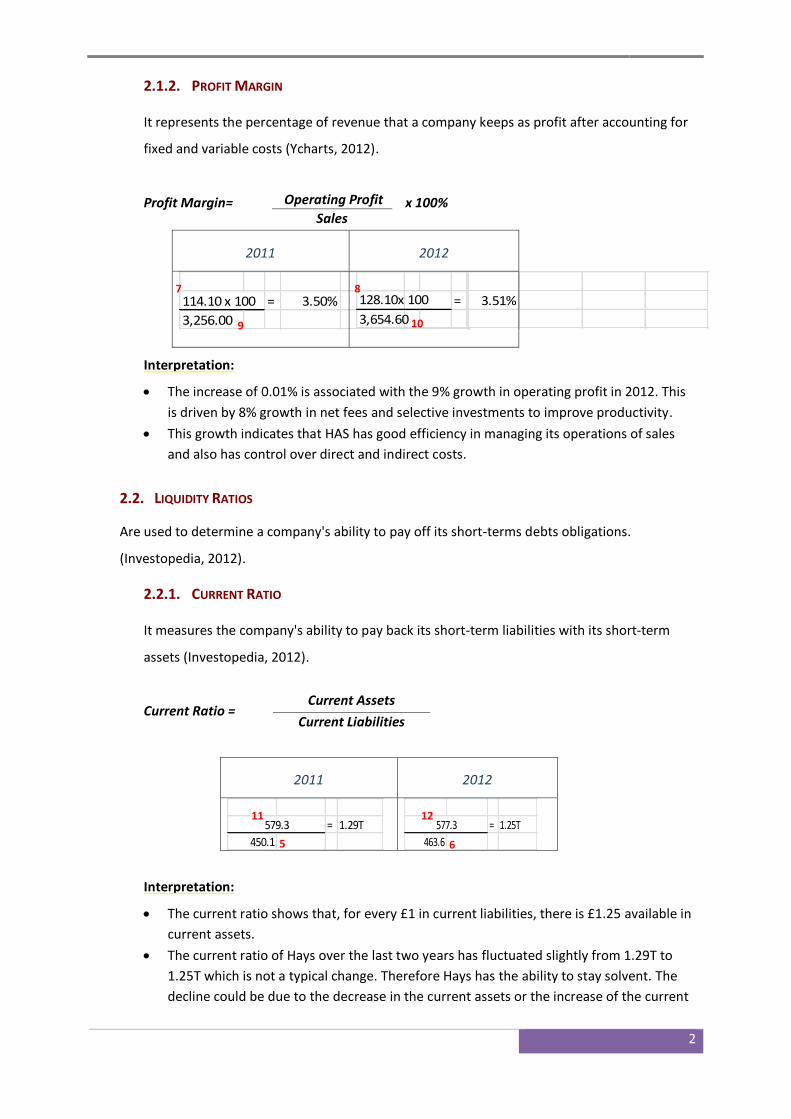

2.1.2. PROFIT MARGIN

It represents the percentage of revenue that a company keeps as profit after accounting for

fixed and variable costs (Ycharts, 2012).

Profit Margin= x 100%

2011 2012

= 3.50%

3,256.00

114.10 x 100

= 3.51%

3,654.60

128.10x 100

Interpretation:

The increase of 0.01% is associated with the 9% growth in operating profit in 2012. This

is driven by 8% growth in net fees and selective investments to improve productivity.

This growth indicates that HAS has good efficiency in managing its operations of sales

and also has control over direct and indirect costs.

2.2. LIQUIDITY RATIOS

Are used to determine a company's ability to pay off its short-terms debts obligations.

(Investopedia, 2012).

2.2.1. CURRENT RATIO

It measures the company's ability to pay back its short-term liabilities with its short-term

assets (Investopedia, 2012).

Current Ratio =

2011 2012

= 1.29T

450.1

579.3

= 1.25T

463.6

577.3

Interpretation:

The current ratio shows that, for every £1 in current liabilities, there is £1.25 available in

current assets.

The current ratio of Hays over the last two years has fluctuated slightly from 1.29T to

1.25T which is not a typical change. Therefore Hays has the ability to stay solvent. The

decline could be due to the decrease in the current assets or the increase of the current

Operating Profit

Sales

Current Assets

Current Liabilities

7 8

9 10

11 12

5 6

3

liabilities as a result of the state of fragile stability in the recruitment business (Ezine

Articles 2012)

2.3. GEARING RATIOS

A general term describing a ratio that compares some form of owner's equity (or capital) to

borrowed funds (Investopedia, 2012)

2.3.1. BORROWING RATIO

x 100% Total debt/Total equity =

2011 2012

= 96.69%

196.4

(185 + 4.9) X 100%

= 90.03%

190.6

(170 + 1.6) x 100%

Interpretation:

The 2012 ratio indicates that every £1.00 of capital that stockholders provided, creditors

provided £0.90. That means external debts are equal to 90.03% of shareholders’ funds.

The decline in the total debt-to-equity is a positive indicator of Hays having sufficient

funds to meet its financial obligations when they fall due.

2.4. LEVERAGE RATIOS

A company's leverage relates to how much debt it has on its balance sheet (Morningstar 2010).

2.4.1. INTEREST COVER RATIO

It gives a clear picture of the short-term financial health of a business.

Interest Cover =

2011 2012

114.1 = 15.21

8.5 - 1.0

128.1 = 22.47

6.6 - 0.9

Interpretation:

The ratio indicates that HAS can cover its interest charges as the operating profit is

considerably higher than net interest payable.

In the previous year, this ratio was 15.21T associated with higher net interest payable –

Finance cost was 7.5m - on total borrowing for the year 189.9m though HAS managed to

Total borrowings (Long-term +short term debt)

Equity

Operating Profit

Net Interest Payable

13 14 15 16

17 18

7 8

19 20 21 22

4

lower its borrowing in 2012 to 171.6m. Therefore the interest cover in 2012 came better

indicating a better financial health which means that Hays is more capable of meeting its

interest obligations from operating earnings.

2.5. INVESTMENT RATIOS

2.5.1. DIVIDEND YIELD

Dividend Yield = x 100%

2011 2012

5.80 x 100 = 7.49%

77.41

As of 26/11/2011

16:35:03 GMT | GBX

2.50 x 100 = 3.23%

77.35

As of 26/11/2012

16:35:03 GMT | GBX

Interpretation:

DY is relatively low compared to previous year which is associated with the drop in DPS

from 5.80p in 2011 to 2.50p in 2012. Since the Yield depends on dividend policy-

dividends should be covered by the range 2.0x to 3.0x⁽²⁾- to be in line with appropriate

pay-out policy covered by earnings and cash flow.

DY dropped dramatically from 7.49% in 2011 to 3.23% in year. This occurred because

HAS holds the DPS at low amount to allow for reinvestment of profits.

2.5.2. RETURN ON EQUITY (ROE)

Return on Equity = x 100%

2011 2012

80.1 x 100 = 41.00%

196.4

= 45.00%

190.6

86.5 x 100%

Interpretation:

In 2012, HAS generated £0.45 of profit for every £1 of shareholders' equity, giving the

stock an ROE of 45%.

HAS ROE is much higher than the industry norm of 11.59 which is a boost for its stock in

the market indicating how well HAS’s management is deploying the shareholders'

capital.

2.6. EFFICIENCY RATIOS

Measures how effectively the company utilizes its assets, as well as how well it manages its

liabilities.

Dividend Per Share

Market Price of Share

Profit Attributable to shareholders

Book Value Equity

23 24

25 26

17 18

5

2.6.1. ASSET TURNOVER

The higher the ratio, the more sales generated from its assets.

Asset turnover = Revenue / Average total assets

2011 2012

= 3.90

(878.3+782.4)/2

3256

= 4.20

(878.3+862.5)/2

3654.6

Interpretation:

The asset turnover has risen from 3.92x per year to 4.20x which is higher than industry

norm 2.10x.

This means that for every £1 of HAS's assets, HAS generated £4.20 in revenue.

The increase indicates that HAS is utilizing its assets efficiently to produce sales.

3. NAV, DVM AND PER:

Dividend Per Share(Pence)

2012 2.50

2011 5.80

2010 5.80

2009 5.80

2008 5.80

3.1. SHARES VALUATION USING NAV

NAVPS = Net Assets / Number of Share in issue

NAVPS= 190.60/ 21,398.83 = 13.62p

This means HAS market share price is over-valued.

Whereas Market Cap is a long way from NAV because

NAV is historical and it does not take into account

the future earnings potential while market cap does.

Shareholders are rating HAS based on market value.

3.2. DIVIDEND VALUATION MODEL

On the assumption using the variables giving: RF 2%, RM 3.5% alongside that HAS will pay

dividends to infinity, discounted to present value:

1 Based on information from http://www.reuters.com/finance/stocks/overview?symbol=HAYS.L 2 http://shares.telegraph.co.uk/fundamentals/?section=profile&epic=HAS

1Beta: 1.27

Market Cap (£m):

Current Share Price

£1,139.07

77.40GBp

30 Nov. 2012

Balance Sheet 30 Jun '12

Non-Current Assets

285.20

Current Assets 577.30 Current Liabilities (463.60) Non-Current Liabilities

(208.30)

Net Assets Value 190.60

10 9

3 3 27 4

6

KE = 2+1.27(3.5-2) = 3.905%

G = (1-payout) x ROE = (1-(2.5/5.47)) x 0.4538= 25%

P0 = d₁ + P₁ === 2.5(1+0.25) + 110 = 3 + 105.87 = 108.87p

1 + KE 1 + KE 1+0.039 1+0.039

HAS stock was trading at 80.425p which would make it under -valued.

In terms of technical analysis, HAS is experiencing a decline phase in its life-cycle with respect to

negative dividend growth. DPS for 2012 decreased to 2.50p from 5.80p in 2011; the dividend

growth rate for the next 5 years is 3-12.94% with DPS as following:

Fiscal Y EPS Mean (p)

2013 2.49

2014 2.74

2015 3.18

2016 5.044

In HAS case the growth factor is negative, therefore the Gordon Model has a significant loss of

generality. Hence HAS is cyclical firm which is going through one of its life-cycle of decline to

accumulate cash and increase profit in near future in line with sustainable growth in future

Earnings and Dividends. Based on this best fit model would be the two-stage as it decreased the

growth for 4 years and will revert back to stable growth at 0.4%.

dn = d0 (1+g) = as per table (EPS MEAN)

g= 0.4% (an assumption for a reasonable growth after a decline for a number of years.)

STAGE1:

P0 = d0 (1+g) + d0(1+g)² + d0(1+g)³ + d0 (1+g)4 + P4

1+KE (1+KE)² (1+KE) ³ (1+KE)4 (1+KE) 4

STAGE2:

P4 = d4 = 4.3248 (1+0.004) = 124.06p

KE – g 0.039 - .004

P0 = 2.40 + 2.53 + 2.83 + 4.32 + 106.46 = 118.54p

Therefore HAS is seemed to be under present value 80.425p.

3.3. THE PER MODEL

1. Historic PER = Current Market price = 580p = 14.63

Last year EPS 6 5.47p

3 Dividend Growth rate as per forecasting by http://www.reuters.com/finance/stocks/financialHighlights?symbol=HAYS.L and http://www.bloomberg.com/quote/HAS:LN 4 Future Dividend forecasted on http://shares.telegraph.co.uk/fundamentals/?section=broker&epic=HAS 5 Share price on 11th Dec 12, historic prices on http://tools.morningstar.co.uk/uk/stockreport/default.aspx?tab=2&vw=sp&SecurityToken=0P00007OEM]3]0]E0GBR$$ALL&Id=0P00007OEM&ClientFund=0&CurrencyId=GBP

7

Investors are prepared to pay 14.63T historic earnings for this type of share. HAS PER is higher than the norm for sector 714.45x and more than market 12.49x.

Competitors 8PER

Robert Walters PLC 14.02

Michael Page International Plc. 20.20

Harvey Nash Group Plc. 7.31

SThree Plc. 19.17

Investors are willing to buy Michael shares at 20.20x last year’s earning compared with only

7.31x last year’s earnings for Harvey. One explanation for the difference in PERs is that

companies with higher PER are expected to show faster growth in earnings in the future appear

expensive relative to Harvey but the differential maybe justified based on forecasts of earnings.

2. Prospective PER

The PER for HAS is related to its fundamentals. Since HAS estimated EPS 2013 is 4.24p.

P0 = 2.49/4.24 = 16.77

0.039 – 0.004

It means that investors will pay the equivalent of 16.77 years' worth of earnings to own a share

in HAS. And they will recover their investment in a share after 16.77 years. Comparing this to

PER 2012 = 80.425/5.47= 14.70x. However, investors like the current performance of HAS and

are buying its shares at highly inflated values relative to its earnings taken to reserves.

6 Basic EPS 7http://tools.morningstar.co.uk/uk/stockreport/default.aspx?tab=11&SecurityToken=0P00007OEM]3]0]E0GBR$$ALL&Id=0P00007OEM&ClientFund=0&CurrencyId=GBP 8 One prior year EPS and Current market prices as www.lse.co.uk/share-fundamentals.asp, accessed on 11th Dec 12

8

4. CONCLUSION

Based on the Ratios, the expectations of the HAS performance look profitable. This is because they delivered good net fee growth of 8% driven by a strong performance of the International business, and taking appropriate action to defend the profit of the Group by focusing on strong cost control. This has positive impact on the financial performance in the long-term by increasing sales and reducing costs. This will give positive signals to investors that HAS is well worth buying.

On the other hand, Share Valuations which are based on projected characteristics rated shares as under-valued. However these intrinsic values have to take into account adjustments to estimate other value-enhancing traits to be a constructive tool. However low share prices comparable with competitors would be attractive to new investors who looked over consensus market analysis and found out that HAS is a good prospective share.

The capital structure of the Group consists of net debt of 90% of its equity, represented in cash and cash equivalents (note 19, p86), bank loans and overdrafts (note 20) and equity attributable to equity holders of the parent, comprising issued share capital, reserves and retained earnings (notes 24 to 28, p.93). HAS has an unsecured £300 million revolving credit facility, in place until January 2014. HAS has begun refinancing discussions with their banking group. Therefore they significantly decreased 18.3m in the debt from 189.90m to 171.60m to get better credit facilities.

So , based on this analysis, HAS seems to be a good company to invest in, since the company has showed sustainable growth in profit, and hacked back on dividends to restructure its capital to pay for its debt in terms of getting better credit facility and inject it into its capital with cheap cost. The investor sentiment is to pay for HAS stock which will get the price to increase piecemeal.

9

5. REFERENCES

EzineArticles (2012) What is the current ratio? [Accessed 13 Dec 2012] http://ezinearticles.com/?What-is-Current-Ratio?&id=1621448 Gerald I. White, Ashwinpaul C. Sondhi and Dov Fried (2003) The Analysis and Use of Financial Statements, 3rd edn, Wiley, p111 HAS (2012) Our business|Hays – Recruiting Experts Worldwide [Accessed 12 Dec 2012] http://www.hays.com/about-hays/our-business/index.htm Investopedia (2012) Return on Capital Empoyed (ROCE) Definition [Accessed 12 Dec 2012] http://www.investopedia.com/terms/r/roce.asp#axzz2EsRuris1 Investopedia (2012) Liquidity Ratios Definition [Accessed 13 Dec 2012] http://www.investopedia.com/terms/l/liquidityratios.asp#axzz2EsRuris1 Investopedia (2012) Current Ratio Defintion [Accessed 13 Dec 2012] http://www.investopedia.com/terms/c/currentratio.asp#axzz2EsRuris1 Investopedia (2012) Gearing Ratio Definition [Accessed 13 Dec 2012] http://www.investopedia.com/terms/g/gearingratio.asp#axzz2EsRuris1 Morningstar (2012) Leverage Ratios [Accessed 13 Dec 2012] http://news.morningstar.com/classroom2/course.asp?docId=145093&page=5&CN= Morningstar (2010) Efficiency Ratios [Accessed 13 Dec 2012] http://news.morningstar.com/classroom2/course.asp?docId=145093&page=3&CN Tutor2u (2012) Main Financial Ratios [Accessed 12 Dec 2012) http://www.tutor2u.net/business/accounts/main_ratios.htm Ycharts (2012) Profit Margin Definition [Accessed 13 Dec 2012) http://ycharts.com/glossary/terms/profit_margin