corporate finance lecture 8. announcements 2nd quiz 2nd quiz –opens at midnight tonight –valid...

Post on 21-Dec-2015

213 views

TRANSCRIPT

Corporate FinanceCorporate Finance

Lecture 8Lecture 8

AnnouncementsAnnouncements

2nd quiz2nd quiz– Opens at midnight tonightOpens at midnight tonight– Valid for 48 hoursValid for 48 hours– Closes at midnight of Thursday Closes at midnight of Thursday

2nd case : Boeing 7E72nd case : Boeing 7E7– Questions will be posted on May 8Questions will be posted on May 8– Delivery deadline: May 13Delivery deadline: May 13– Discussion: May 15Discussion: May 15

Topics coveredTopics covered

MM MM proposition without taxproposition without tax MM proposition with taxMM proposition with tax Cost of financial distressCost of financial distress

– Direct costDirect cost– Indirect costIndirect cost

Reducing cost of debtReducing cost of debt Integration of tax benefit and Integration of tax benefit and

financial distress cost of debtfinancial distress cost of debt

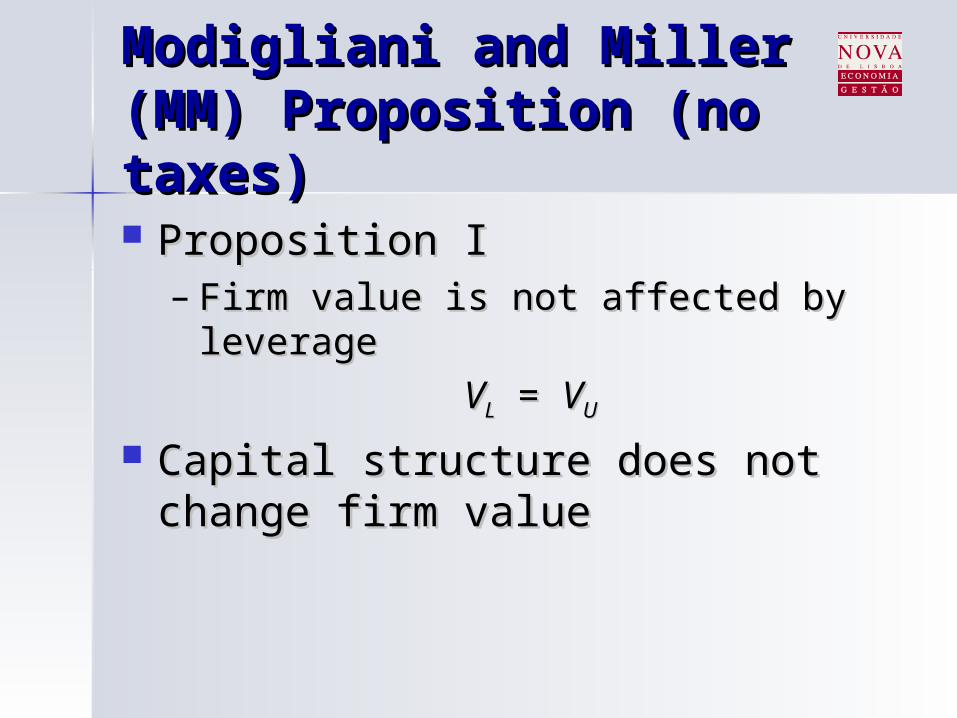

Modigliani and Miller Modigliani and Miller (MM) Proposition (no (MM) Proposition (no taxes)taxes) Proposition IProposition I

– Firm value is not affected by Firm value is not affected by leverageleverage

VVLL = = VVUU

Capital structure does not change Capital structure does not change firm valuefirm value

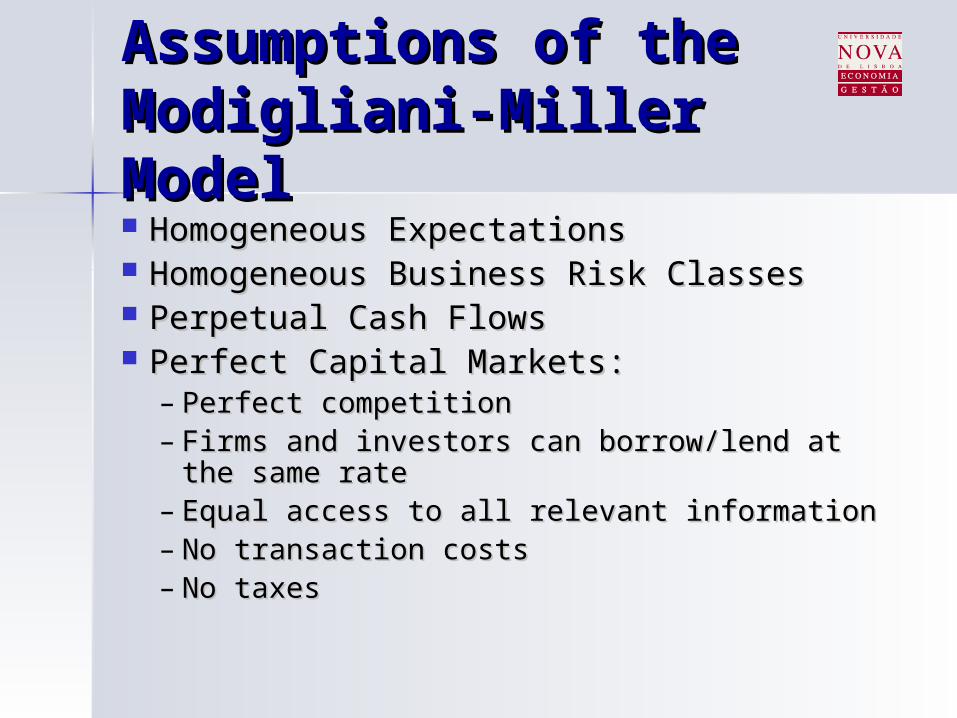

Assumptions of the Assumptions of the Modigliani-Miller ModelModigliani-Miller Model Homogeneous ExpectationsHomogeneous Expectations Homogeneous Business Risk ClassesHomogeneous Business Risk Classes Perpetual Cash FlowsPerpetual Cash Flows Perfect Capital Markets:Perfect Capital Markets:

– Perfect competitionPerfect competition– Firms and investors can borrow/lend at the Firms and investors can borrow/lend at the

same ratesame rate– Equal access to all relevant informationEqual access to all relevant information– No transaction costsNo transaction costs– No taxesNo taxes

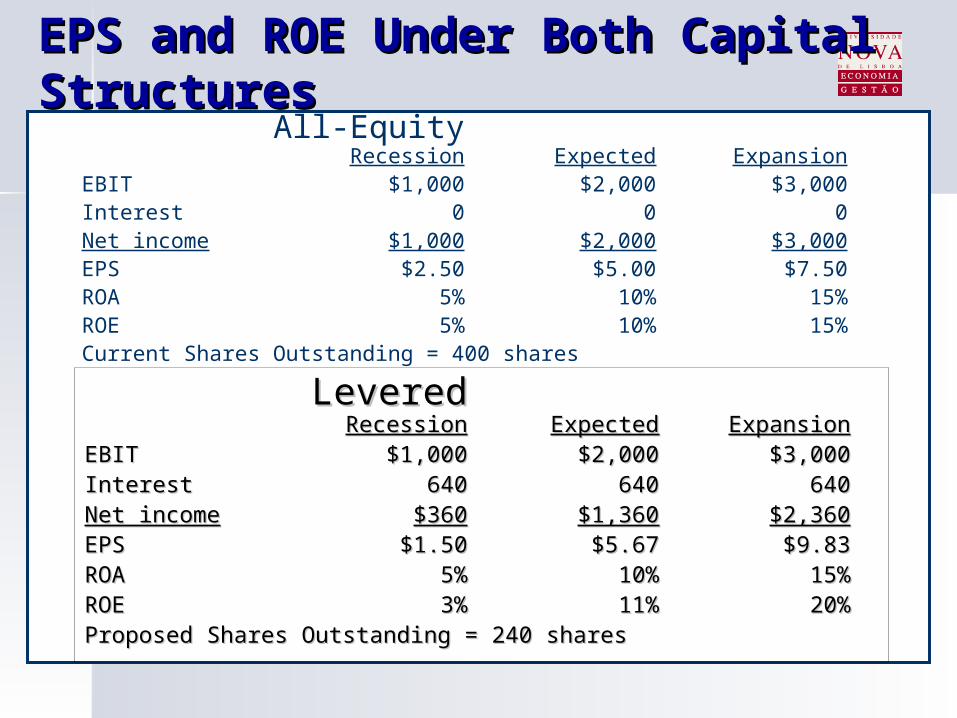

EPS and ROE Under Both Capital EPS and ROE Under Both Capital StructuresStructures

LeveredLeveredRecessionRecession ExpectedExpected ExpansionExpansion

EBITEBIT $1,000$1,000 $2,000$2,000 $3,000$3,000InterestInterest 640640 640640 640640Net incomeNet income $360$360 $1,360$1,360 $2,360$2,360EPSEPS $1.50$1.50 $5.67$5.67 $9.83$9.83ROAROA 5%5% 10%10% 15%15%ROEROE 3%3% 11%11% 20%20%Proposed Shares Outstanding = 240 sharesProposed Shares Outstanding = 240 shares

All-EquityRecession Expected Expansion

EBIT $1,000 $2,000 $3,000Interest 0 0 0Net income $1,000 $2,000 $3,000EPS $2.50 $5.00 $7.50ROA 5% 10% 15%ROE 5% 10% 15%Current Shares Outstanding = 400 shares

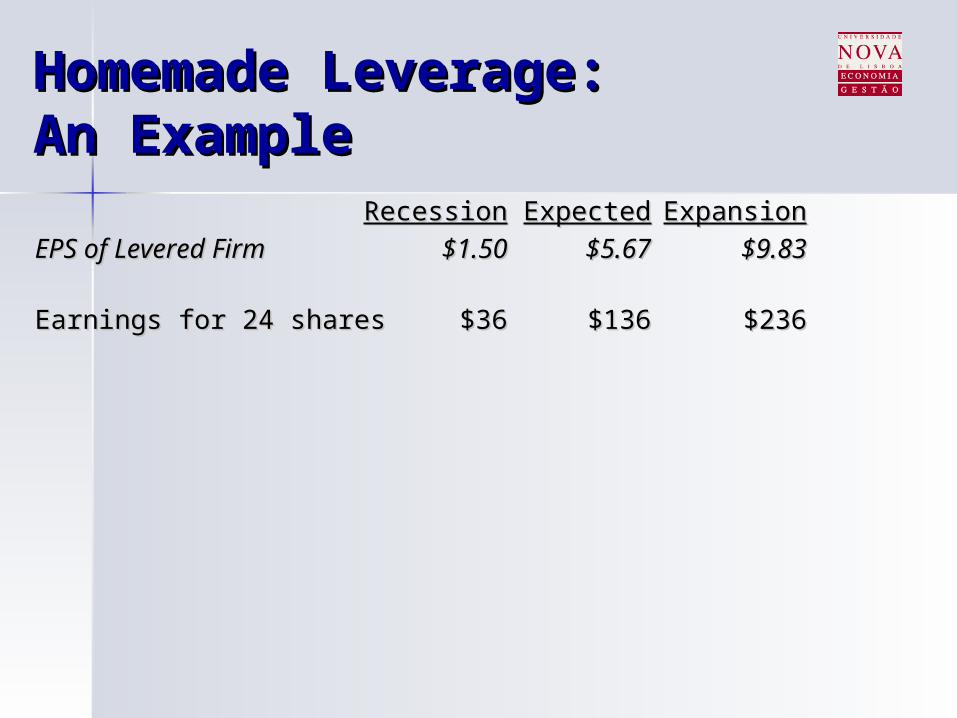

Homemade Leverage:Homemade Leverage:An ExampleAn Example

RecessionRecession ExpectedExpected ExpansionExpansion

EPS of Levered FirmEPS of Levered Firm $1.50$1.50 $5.67$5.67 $9.83$9.83

Earnings for 24 sharesEarnings for 24 shares $36$36 $136$136 $236$236

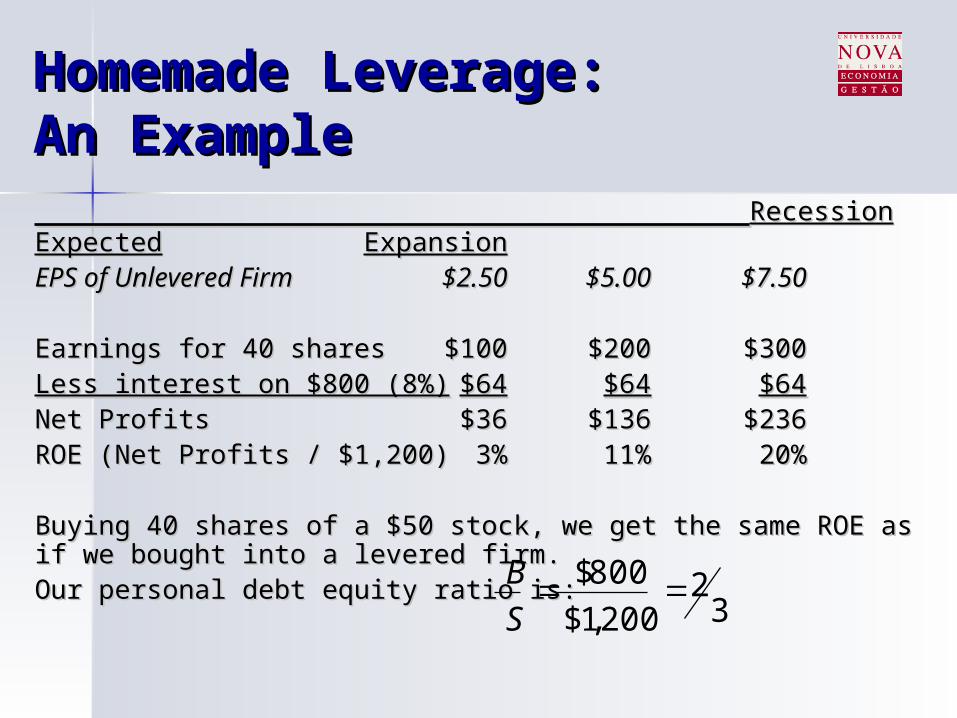

Homemade Leverage:Homemade Leverage:An ExampleAn Example RecessionRecessionExpectedExpectedExpansionExpansion

EPS of Unlevered FirmEPS of Unlevered Firm $2.50$2.50 $5.00$5.00 $7.50$7.50

Earnings for 40 sharesEarnings for 40 shares $100$100 $200$200 $300$300Less interest on $800 (8%)Less interest on $800 (8%) $64$64 $64$64 $64$64Net ProfitsNet Profits $36$36 $136$136 $236$236ROE (Net Profits / $1,200)ROE (Net Profits / $1,200) 3%3% 11%11% 20%20%

Buying 40 shares of a $50 stock, we get the same ROE as if we Buying 40 shares of a $50 stock, we get the same ROE as if we bought into a levered firm.bought into a levered firm.Our personal debt equity ratio is:Our personal debt equity ratio is:

32

200,1$

800$ S

B

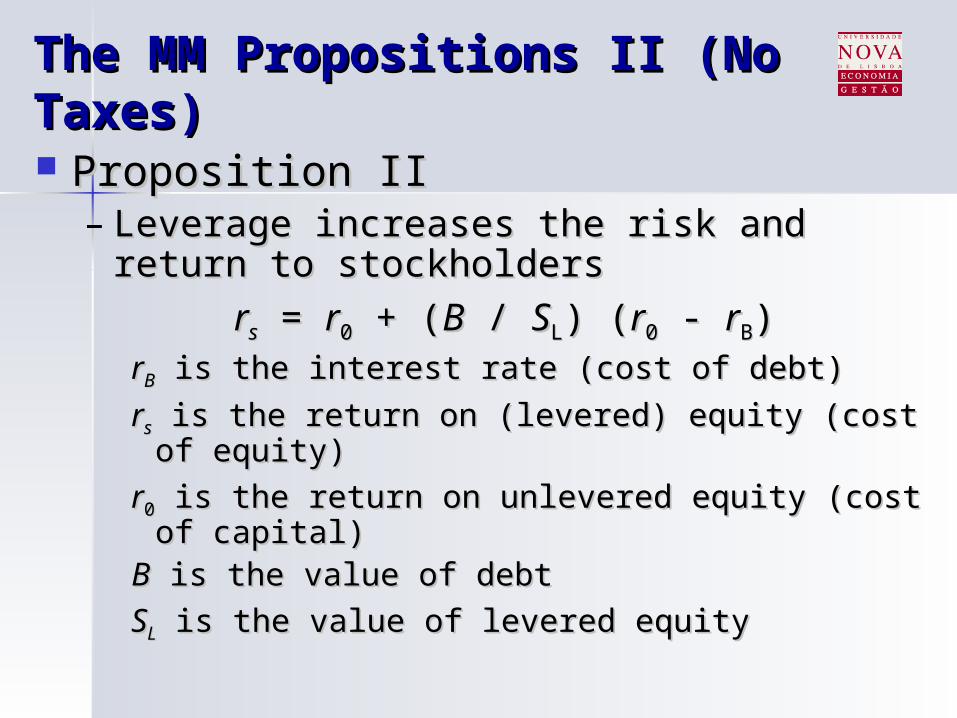

The MM Propositions II (No The MM Propositions II (No Taxes)Taxes) Proposition IIProposition II

– Leverage increases the risk and return to Leverage increases the risk and return to stockholdersstockholders

rrss = = rr00 + ( + (BB / / SSLL) () (rr00 - - rrBB))rrBB is the interest rate (cost of debt) is the interest rate (cost of debt)

rrss is the return on (levered) equity (cost of is the return on (levered) equity (cost of equity)equity)

rr00 is the return on unlevered equity (cost of is the return on unlevered equity (cost of capital)capital)

BB is the value of debt is the value of debt

SSLL is the value of levered equity is the value of levered equity

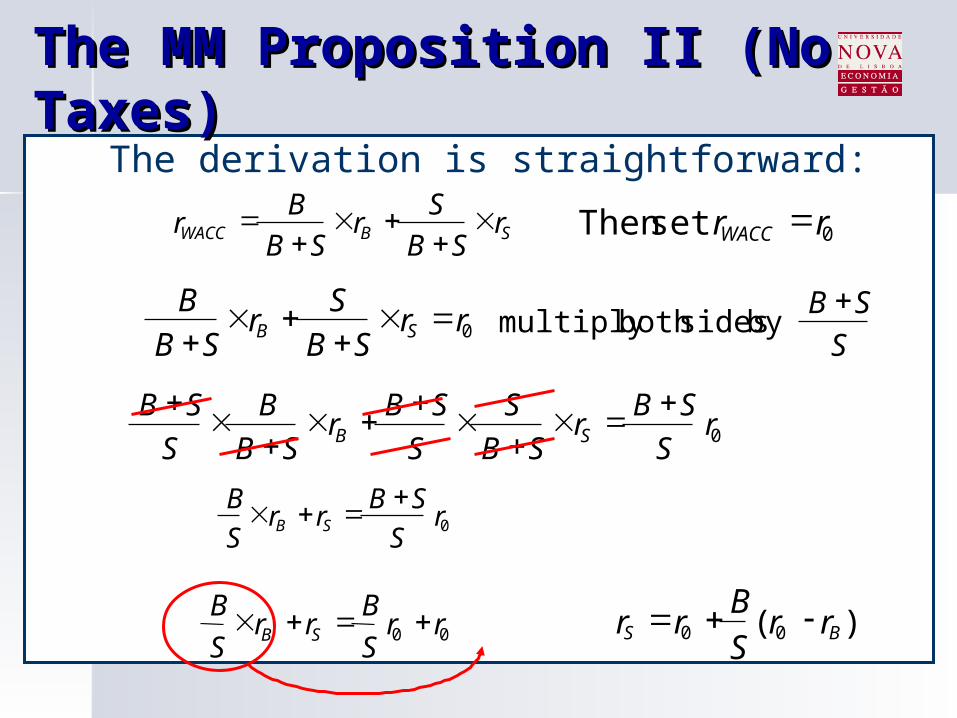

The MM Proposition II (No The MM Proposition II (No Taxes)Taxes)

The derivation is straightforward:

SBWACC rSB

Sr

SB

Br

0set Then rrWACC

0rrSB

Sr

SB

BSB

S

SB by sidesboth multiply

0rS

SBr

SB

S

S

SBr

SB

B

S

SBSB

0rS

SBrr

S

BSB

00 rrS

Brr

S

BSB

)( 00 BS rrS

Brr

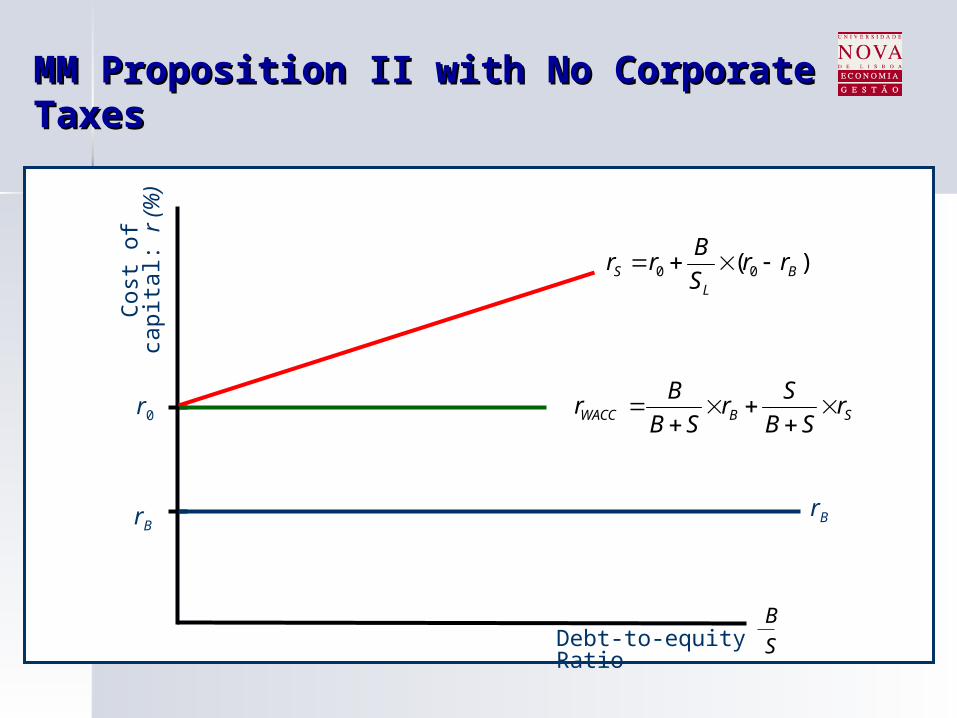

MM Proposition II with No Corporate MM Proposition II with No Corporate TaxesTaxes

Debt-to-equity Ratio

Cos

t of

capi

tal:

r (%

)

r0

rB

SBWACC rSB

Sr

SB

Br

)( 00 BL

S rrS

Brr

rB

S

B

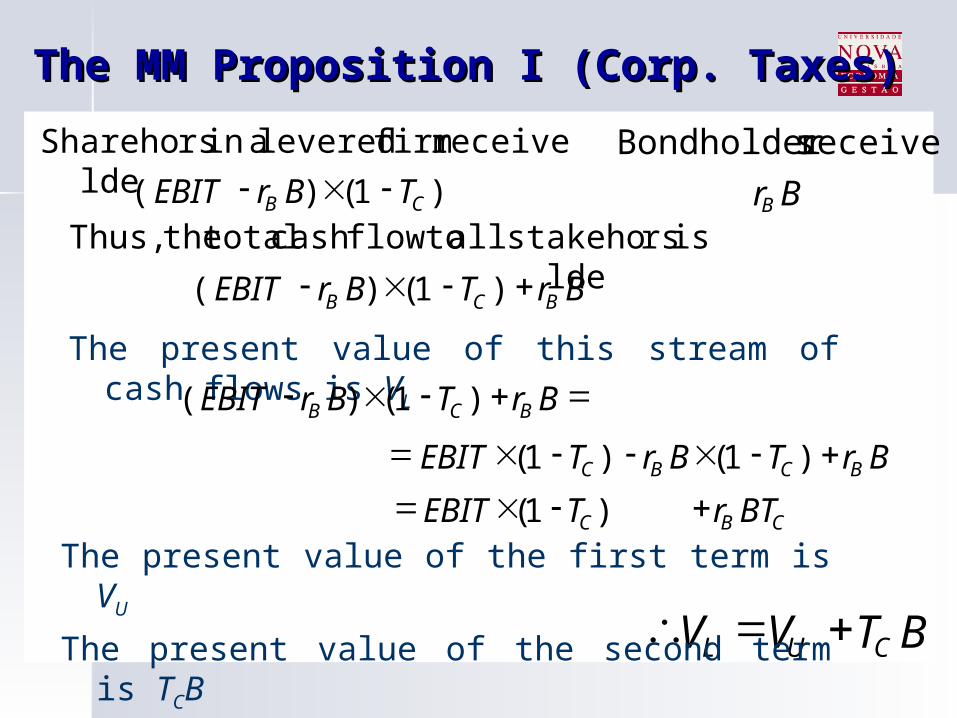

The MM Proposition I (Corp. Taxes)The MM Proposition I (Corp. Taxes)

BTVV CUL

)1()(

receive firm levered ain rsShareholde

CB TBrEBIT BrB

receive sBondholder

BrTBrEBIT BCB )1()(

is rsstakeholde all toflowcash total theThus,

The present value of this stream of cash flows is VL BrTBrEBIT BCB )1()(

The present value of the first term is VU

The present value of the second term is TCB

BrTBrTEBIT BCBC )1()1(

BTrTEBIT CBC )1(

The MM Proposition II (Corp. The MM Proposition II (Corp. Taxes)Taxes)

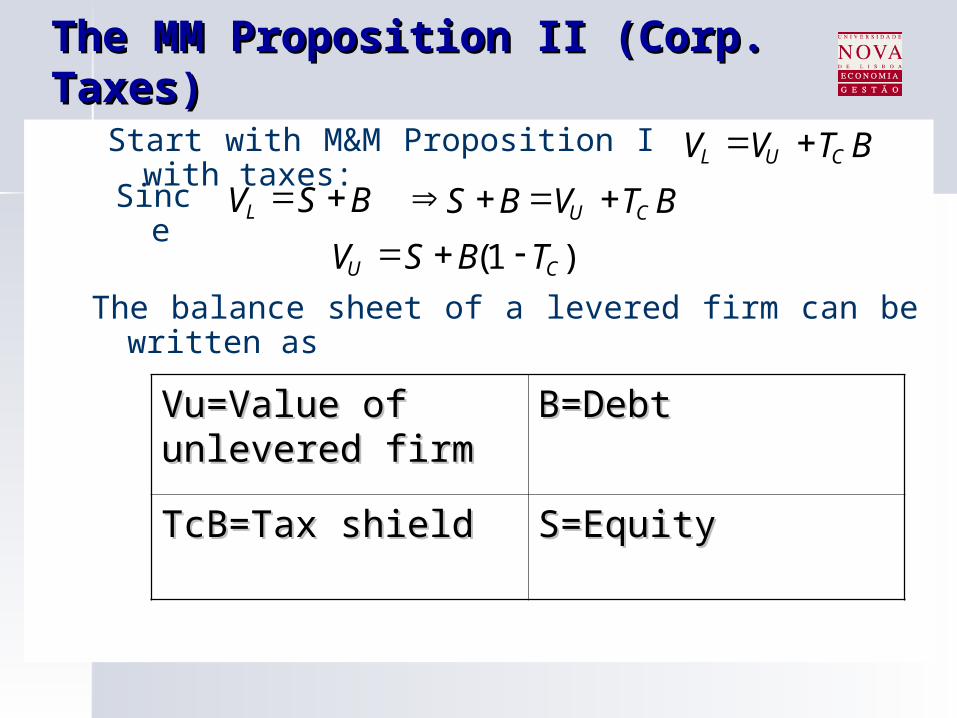

Start with M&M Proposition I with taxes: BTVV CUL

Since BSVL

The balance sheet of a levered firm can be written as

BTVBS CU

)1( CU TBSV

Vu=Value of Vu=Value of unlevered firmunlevered firm

B=DebtB=Debt

TcB=Tax shieldTcB=Tax shield S=EquityS=Equity

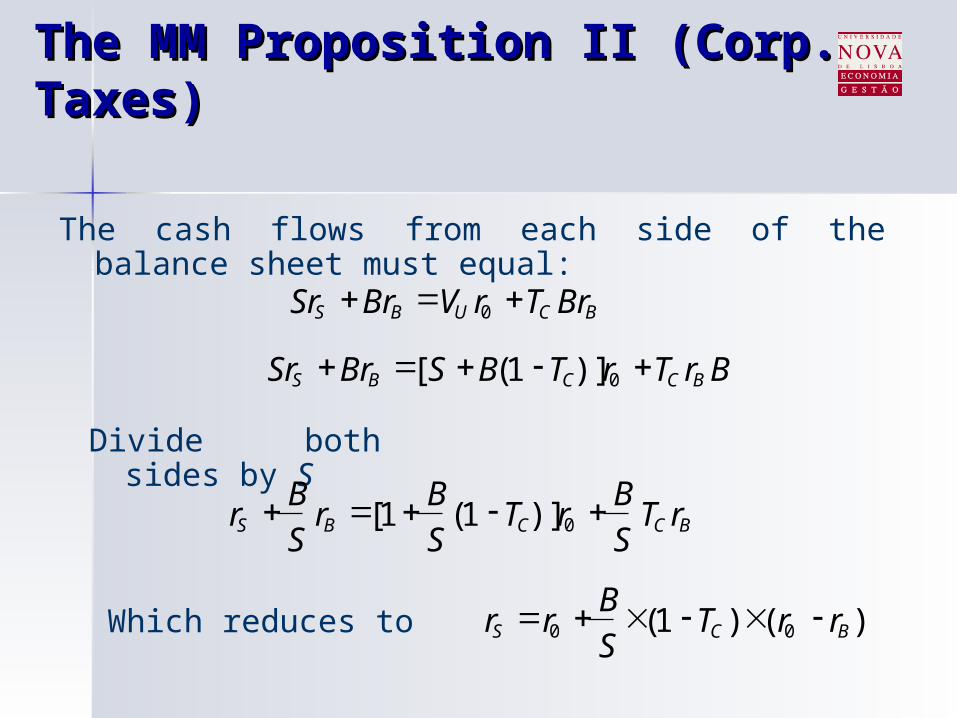

The MM Proposition II (Corp. The MM Proposition II (Corp. Taxes)Taxes)

)()1( 00 BCS rrTS

Brr

The cash flows from each side of the balance sheet must equal:

BCUBS BrTrVBrSr 0

BrTrTBSBrSr BCCBS 0)]1([

Divide both sides by S

BCCBS rTS

BrT

S

Br

S

Br 0)]1(1[

Which reduces to

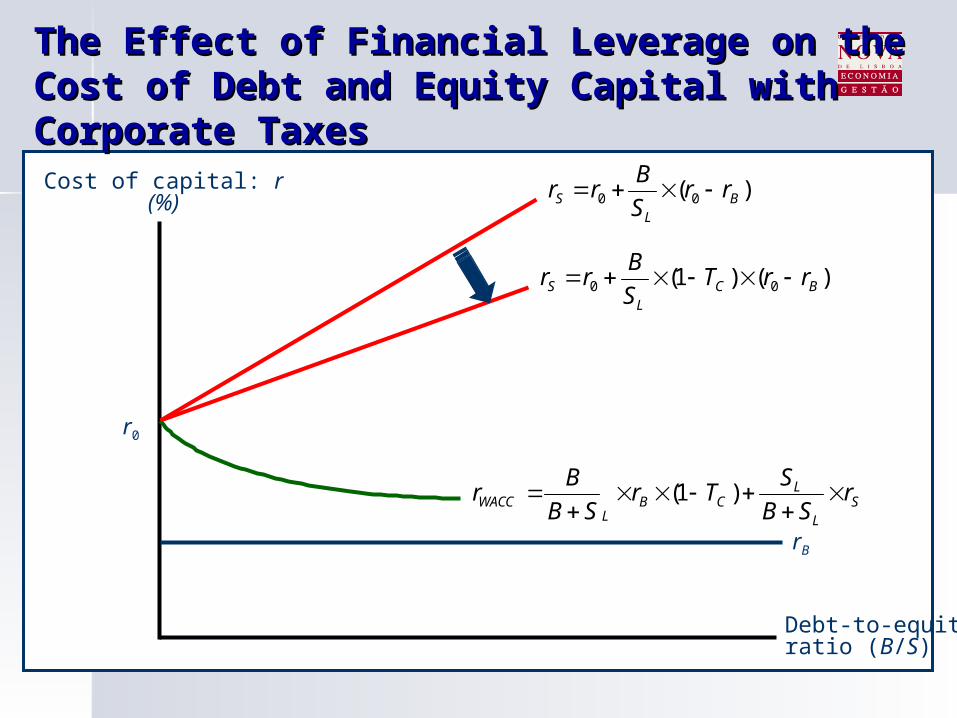

The Effect of Financial Leverage on the The Effect of Financial Leverage on the Cost of Debt and Equity Capital with Cost of Debt and Equity Capital with Corporate TaxesCorporate Taxes

Debt-to-equityratio (B/S)

Cost of capital: r(%)

r0

rB

)()1( 00 BCL

S rrTS

Brr

SL

LCB

LWACC r

SB

STr

SB

Br

)1(

)( 00 BL

S rrS

Brr

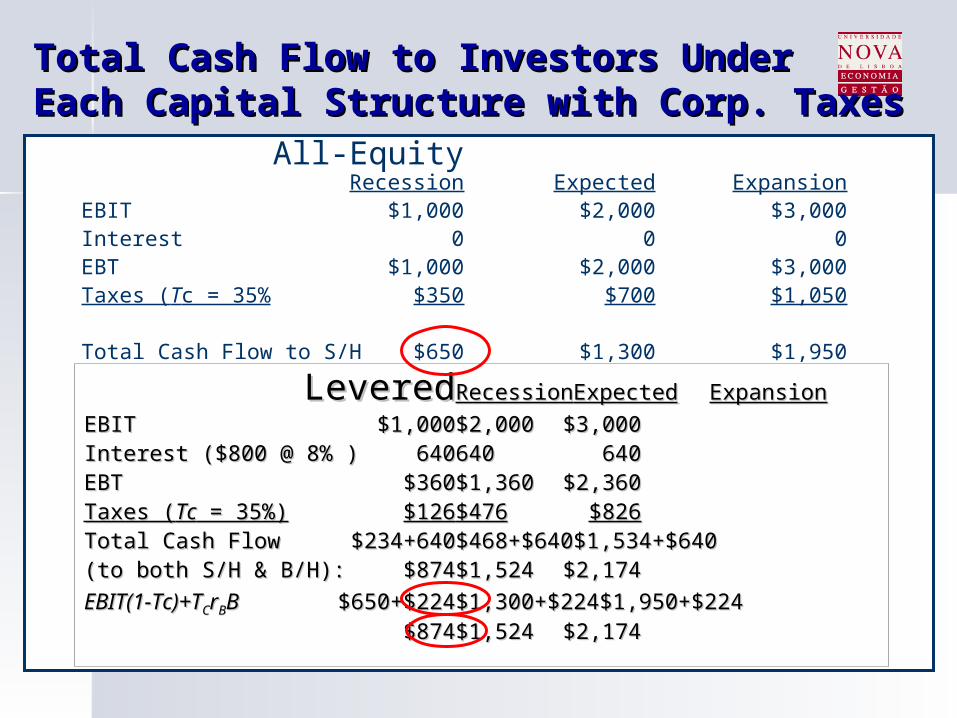

Total Cash Flow to Investors Under Total Cash Flow to Investors Under Each Capital Structure with Corp. TaxesEach Capital Structure with Corp. Taxes

All-EquityRecession Expected Expansion

EBIT $1,000 $2,000 $3,000Interest 0 0 0EBT $1,000 $2,000 $3,000Taxes (Tc = 35% $350 $700 $1,050

Total Cash Flow to S/H $650 $1,300 $1,950

LeveredLeveredRecessionRecession ExpectedExpected ExpansionExpansion

EBITEBIT $1,000$1,000 $2,000$2,000 $3,000$3,000Interest ($800 @ 8% )Interest ($800 @ 8% ) 640640 640640 640640EBTEBT $360$360 $1,360$1,360 $2,360$2,360Taxes (Taxes (TcTc = 35%) = 35%) $126$126 $476$476 $826$826Total Cash Flow Total Cash Flow $234+640$234+640 $468+$640$468+$640 $1,534+$640$1,534+$640(to both S/H & B/H): (to both S/H & B/H): $874$874 $1,524$1,524 $2,174$2,174

EBIT(1-Tc)+TEBIT(1-Tc)+TCCrrBBBB $650+$224$650+$224 $1,300+$224$1,300+$224 $1,950+$224$1,950+$224$874$874 $1,524$1,524 $2,174$2,174

Tax effect of debtTax effect of debt

In a world without taxes, debt does not affect In a world without taxes, debt does not affect firm value.firm value.

When there are corporate taxes, the firm When there are corporate taxes, the firm value is positively related to its debt --Debt value is positively related to its debt --Debt reduces the firm’s tax liabilityreduces the firm’s tax liability

With taxes, the sum of the debt plus the With taxes, the sum of the debt plus the equity of the levered firm is greater than the equity of the levered firm is greater than the equity of the unlevered firm.equity of the unlevered firm.

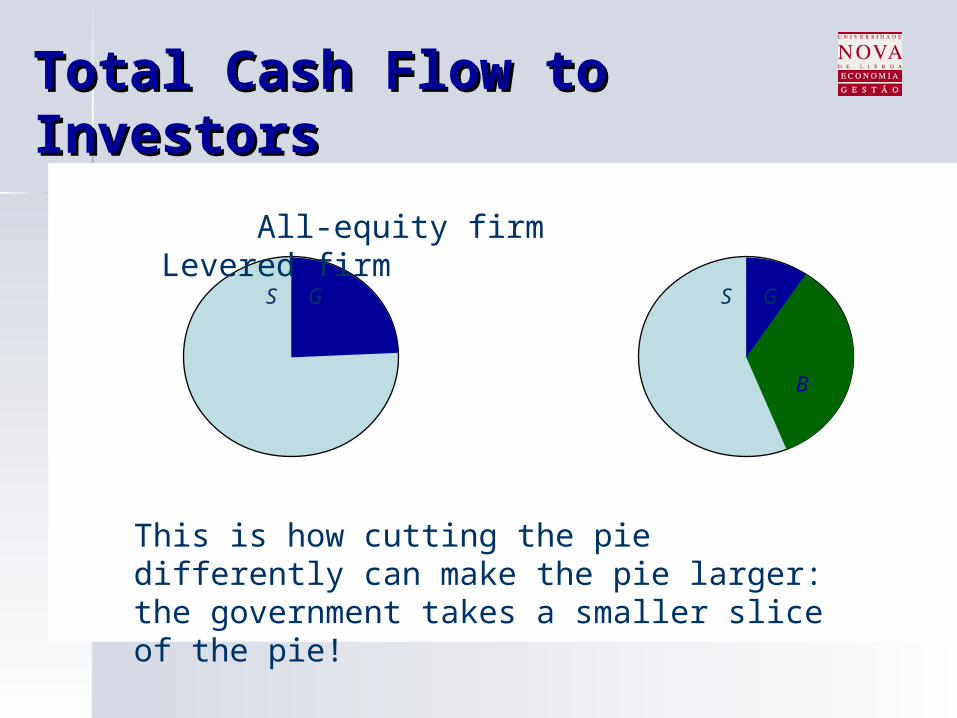

Total Cash Flow to InvestorsTotal Cash Flow to Investors

S G S G

B

All-equity firm Levered firm

This is how cutting the pie differently can make the pie larger: the government takes a smaller slice of the pie!

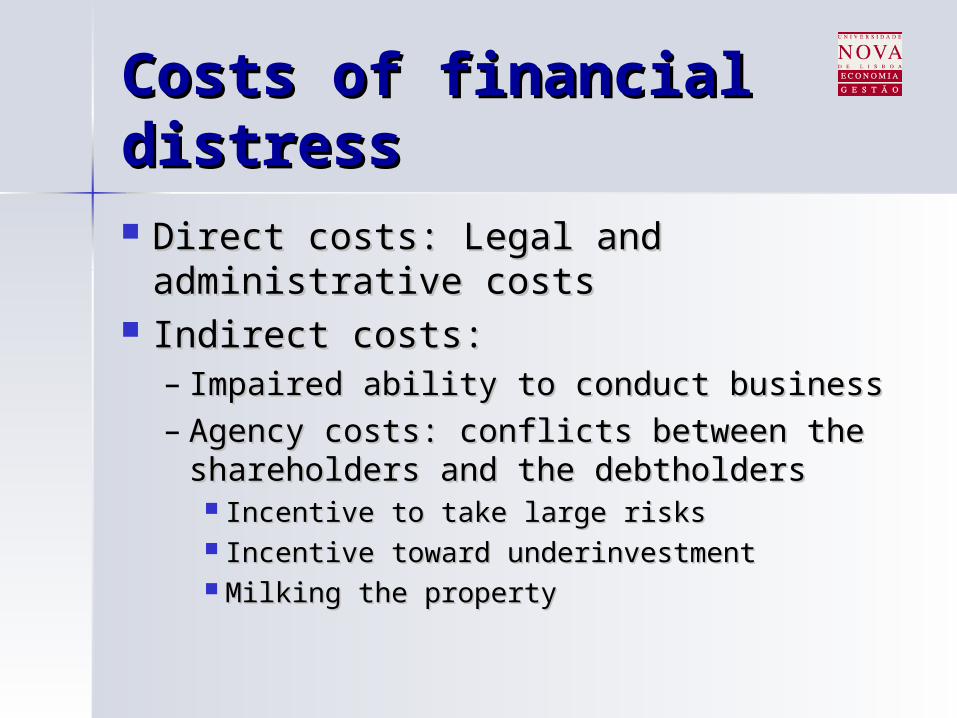

Costs of financial Costs of financial distressdistress Direct costs: Legal and Direct costs: Legal and

administrative costsadministrative costs Indirect costs:Indirect costs:

– Impaired ability to conduct businessImpaired ability to conduct business– Agency costs: conflicts between the Agency costs: conflicts between the

shareholders and the debtholdersshareholders and the debtholders Incentive to take large risksIncentive to take large risks Incentive toward underinvestmentIncentive toward underinvestment Milking the propertyMilking the property

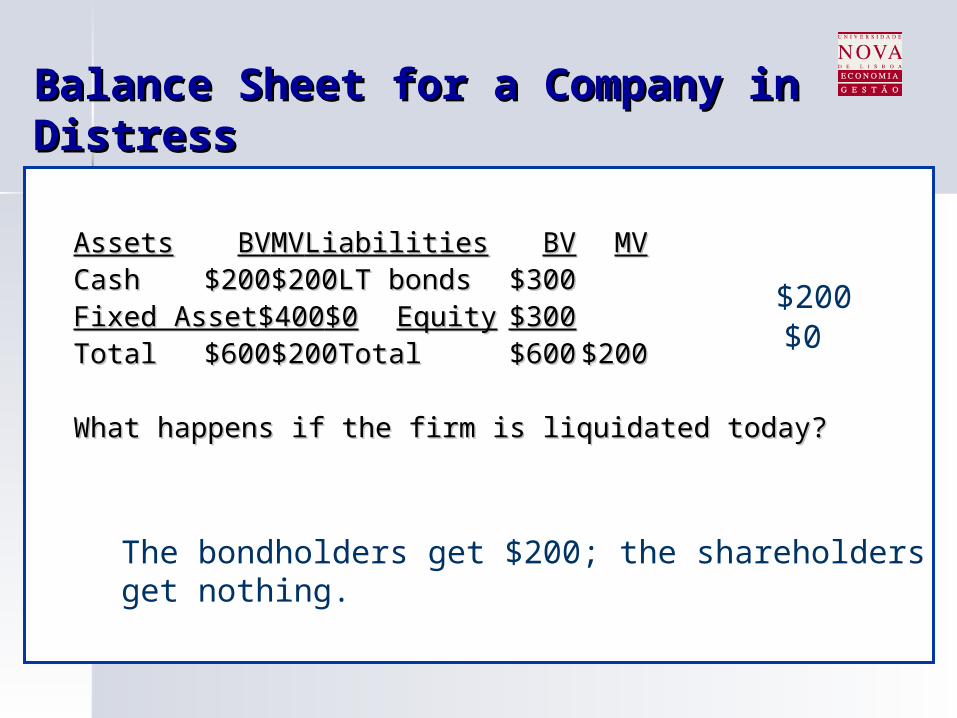

Balance Sheet for a Company in Balance Sheet for a Company in DistressDistress

AssetsAssets BVBV MVMV LiabilitiesLiabilities BVBV MVMVCashCash $200$200$200$200 LT bondsLT bonds$300$300Fixed AssetFixed Asset$400$400$0$0 EquityEquity $300$300TotalTotal $600$600$200$200 TotalTotal $600$600$200$200

What happens if the firm is liquidated today?What happens if the firm is liquidated today?

The bondholders get $200; the shareholders get nothing.

$200$0

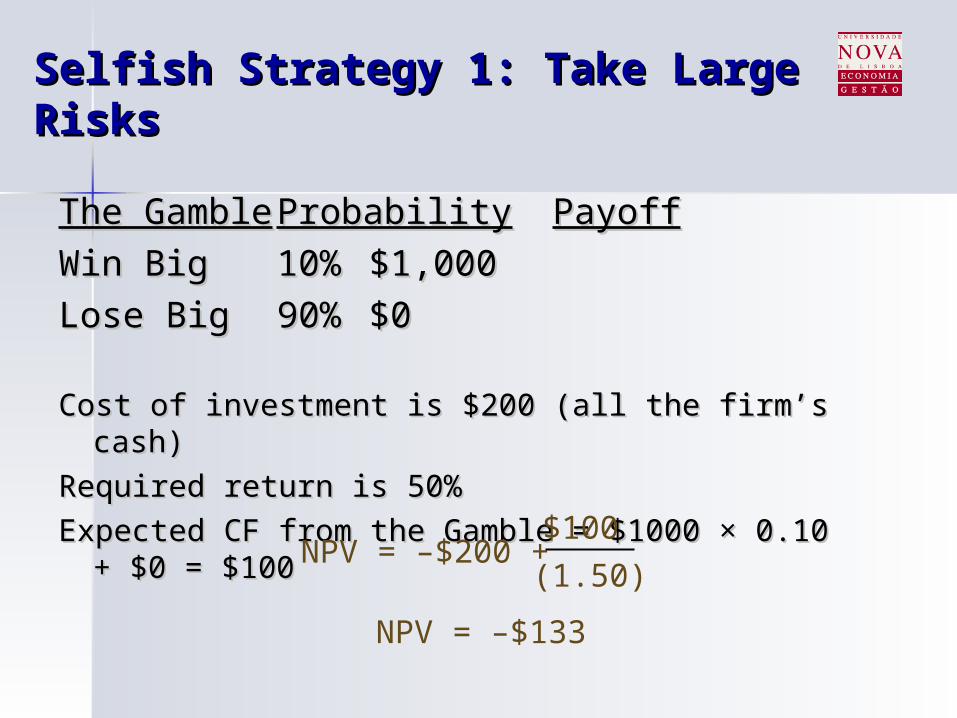

Selfish Strategy 1: Take Large RisksSelfish Strategy 1: Take Large Risks

The GambleThe Gamble ProbabilityProbabilityPayoffPayoff

Win BigWin Big 10%10%$1,000$1,000

Lose BigLose Big 90%90% $0$0

Cost of investment is $200 (all the firm’s cash)Cost of investment is $200 (all the firm’s cash)

Required return is 50%Required return is 50%

Expected CF from the Gamble = $1000 × 0.10 + Expected CF from the Gamble = $1000 × 0.10 + $0 = $100$0 = $100

NPV = –$200 + $100

(1.50)

NPV = –$133

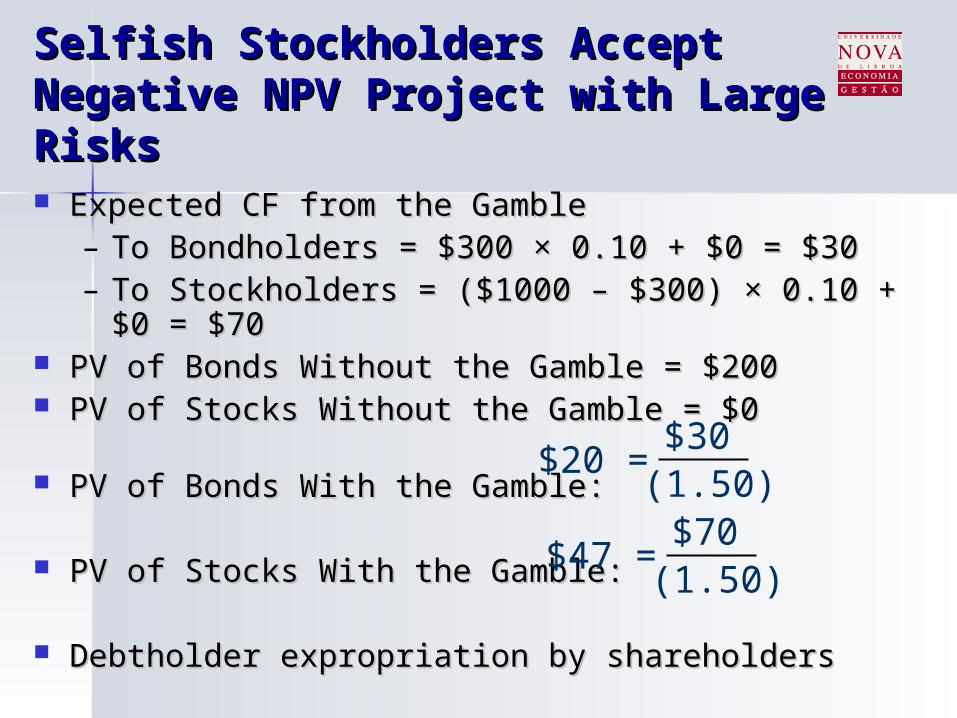

Selfish Stockholders Accept Selfish Stockholders Accept Negative NPV Project with Large Negative NPV Project with Large RisksRisks Expected CF from the GambleExpected CF from the Gamble

– To Bondholders = $300 × 0.10 + $0 = $30To Bondholders = $300 × 0.10 + $0 = $30– To Stockholders = ($1000 – $300) × 0.10 + $0 = To Stockholders = ($1000 – $300) × 0.10 + $0 =

$70$70 PV of Bonds Without the Gamble = $200PV of Bonds Without the Gamble = $200 PV of Stocks Without the Gamble = $0PV of Stocks Without the Gamble = $0

PV of Bonds With the Gamble:PV of Bonds With the Gamble:

PV of Stocks With the Gamble:PV of Stocks With the Gamble:

Debtholder expropriation by shareholdersDebtholder expropriation by shareholders

$20 =$30

(1.50)

$47 =$70

(1.50)

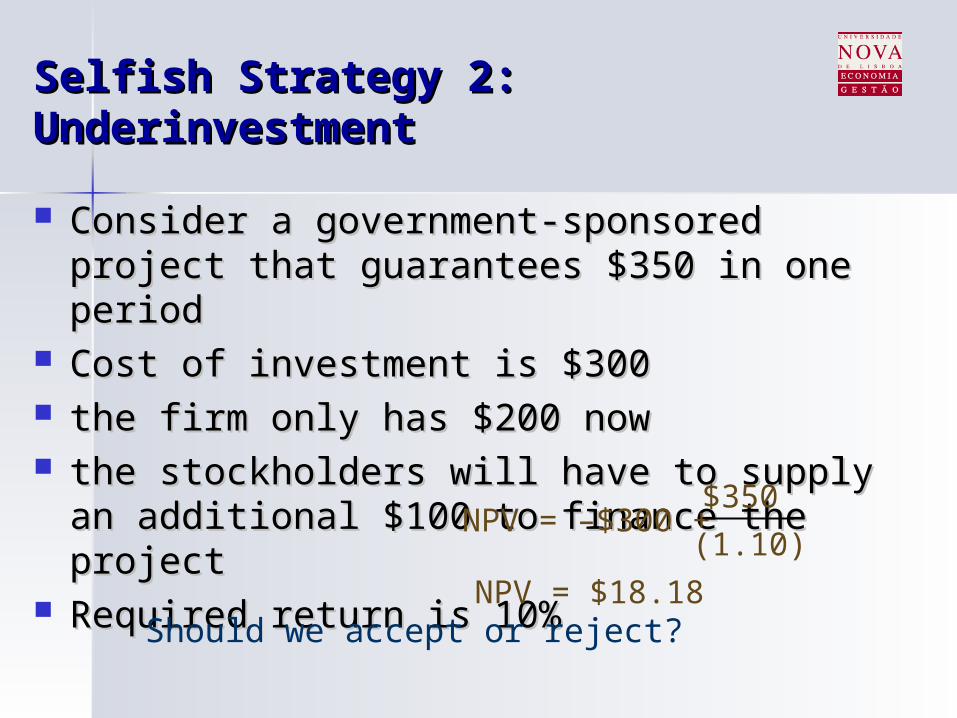

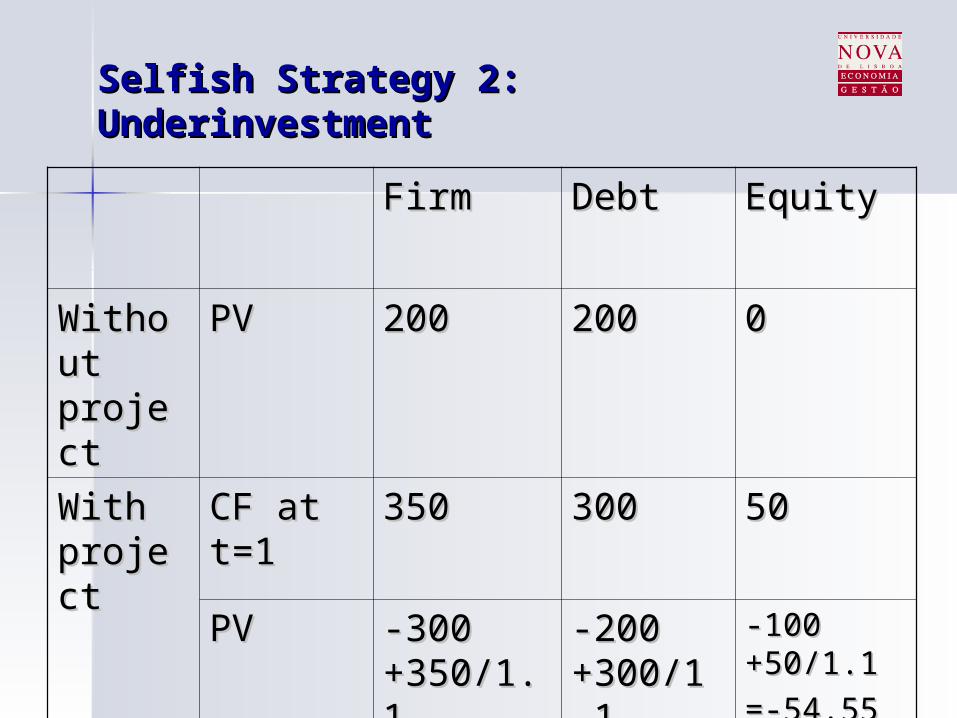

Selfish Strategy 2: UnderinvestmentSelfish Strategy 2: Underinvestment

Consider a government-sponsored project Consider a government-sponsored project that guarantees $350 in one periodthat guarantees $350 in one period

Cost of investment is $300 Cost of investment is $300 the firm only has $200 nowthe firm only has $200 now the stockholders will have to supply an the stockholders will have to supply an

additional $100 to finance the projectadditional $100 to finance the project Required return is 10%Required return is 10%

Should we accept or reject?

NPV = –$300 + $350

(1.10)

NPV = $18.18

Selfish Strategy 2: Selfish Strategy 2: underinvestmentunderinvestment

FirmFirm DebtDebt EquityEquity

WithouWithout t projectproject

PVPV

With With projectproject

CF at CF at t=1t=1

PVPV

Selfish Strategy 2: UnderinvestmentSelfish Strategy 2: Underinvestment

FirmFirm DebtDebt EquityEquity

WithouWithout t projectproject

PVPV 200200 200200 00

With With projectproject

CF at CF at t=1t=1

350350 300300 5050

PVPV -300 -300 +350/1.+350/1.1 1 =18.18=18.18

-200 -200 +300/1.+300/1.1 1 =72.73=72.73

-100 -100 +50/1.1+50/1.1

=-54.55=-54.55

Selfish Strategy 3: Milking the PropertySelfish Strategy 3: Milking the Property

Liquidating dividendsLiquidating dividends Increase perquisites to Increase perquisites to

shareholders and/or managementshareholders and/or management

Protective CovenantsProtective Covenants

Agreements to protect bondholdersAgreements to protect bondholders Negative covenant: Negative covenant:

– Pay dividends beyond specified amount.Pay dividends beyond specified amount.– Sell more senior debt & amount of new Sell more senior debt & amount of new

debt is limited.debt is limited. Positive covenant: Positive covenant:

– Maintain good condition of assets.Maintain good condition of assets.– Provide audited financial information.Provide audited financial information.– Working capital requirement.Working capital requirement.

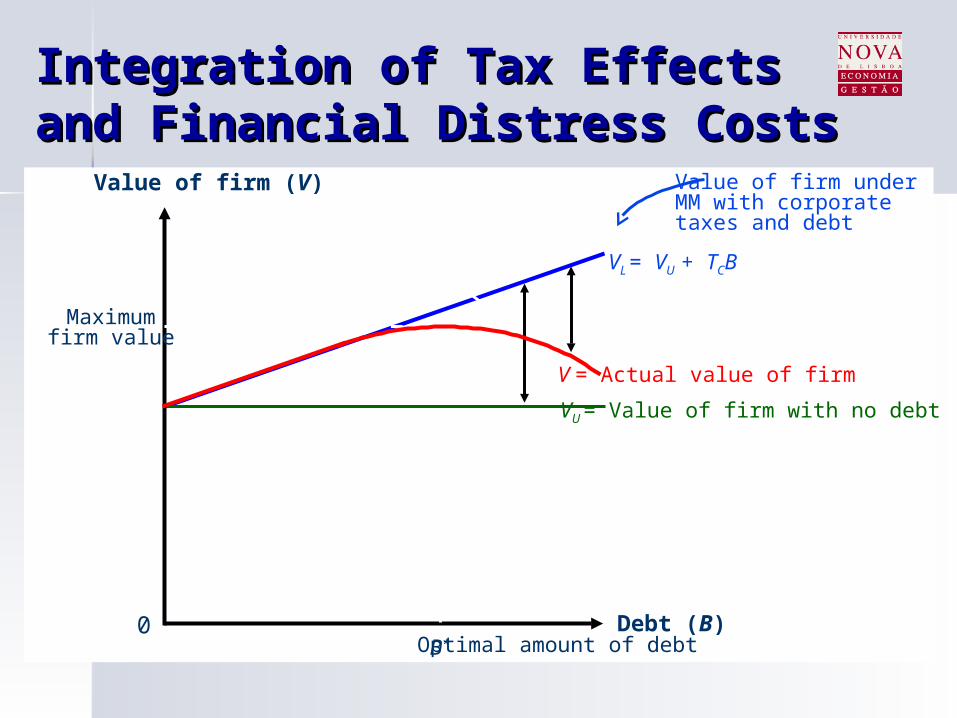

Integration of Tax EffectsIntegration of Tax Effectsand Financial Distress Costsand Financial Distress Costs

Debt (B)

Value of firm (V)

0

Present value of taxshield on debt

Present value offinancial distress costs

Value of firm underMM with corporatetaxes and debt

VL = VU + TCB

V = Actual value of firm

VU = Value of firm with no debt

B*

Maximumfirm value

Optimal amount of debt

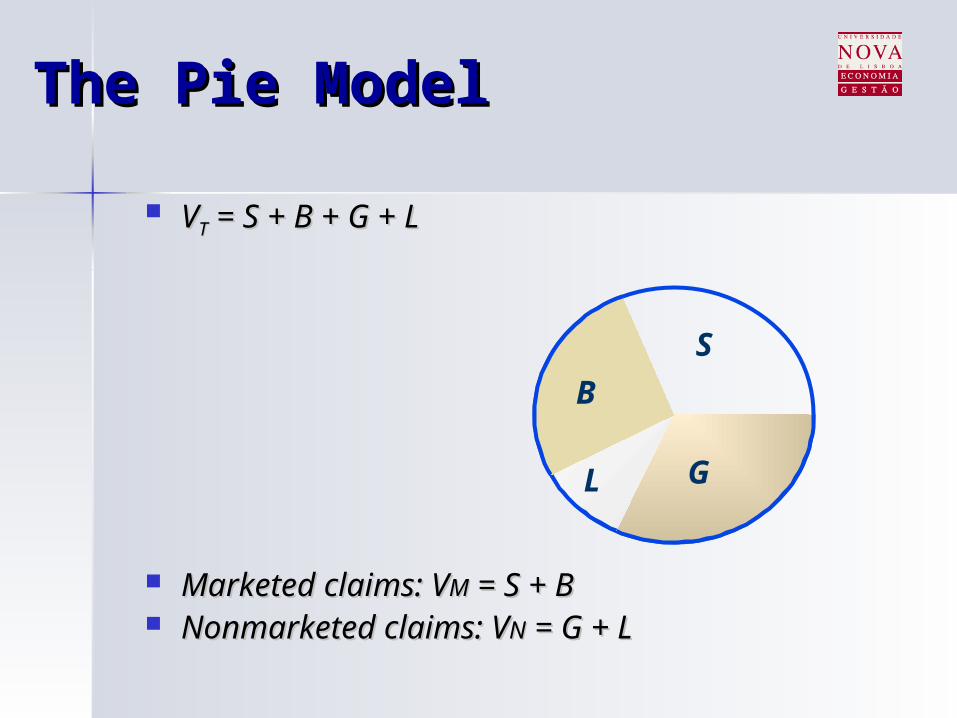

The Pie ModelThe Pie Model

VVTT = S + B + G + L = S + B + G + L

Marketed claims: VMarketed claims: VMM = S + B = S + B Nonmarketed claims: VNonmarketed claims: VNN = G + L = G + L

S

G

B

L

SignalingSignaling

The firm’s capital structure is The firm’s capital structure is optimized where the marginal subsidy optimized where the marginal subsidy to debt equals the marginal cost.to debt equals the marginal cost.

Investors view debt as a signal of firm Investors view debt as a signal of firm value.value.

A manager that takes on more debt A manager that takes on more debt than is optimal in order to fool than is optimal in order to fool investors will pay the cost in the long investors will pay the cost in the long run.run.