corporate expatriations – causes, consequences and future

TRANSCRIPT

Corporate Expatriations – Causes, Consequences and Future Developments

International Tax Institute

Wednesday, September 18, 2013

John J. Merrick Special Counsel to the Associate Chief Counsel (International)

Office of Associate Chief Counsel (International)

Lewis R. Steinberg Credit Suisse (USA) LLC

Willard Taylor

Adjunct Professor, New York University Law School

Corporate Expatriations

• We will address recent “expatriations” by U.S. corporations to Switzerland, Ireland, the U.K. and elsewhere • For example, the November 2012 acquisition of Cooper

Industries, an Irish company, by Eaton Corporation • Resulting in a new Irish corporation, Eaton Global, which will own

Eaton Corporation and Cooper Industries

• And the subsequent quite similar transactions involving Actavis Inc.’s acquisition of Warner Chilcott and Perrigo Company’s acquisition of Elan Corporation

1

Corporate Expatriations

• Several parts to our presentation • A short history of expatriations

• Why Ireland, Switzerland, the U.K., and the Netherlands?

• What do corporations do when they get there (e.g., post-inversion planning)?

• And are there risks?

• Possible legislative, treaty or regulatory responses

2

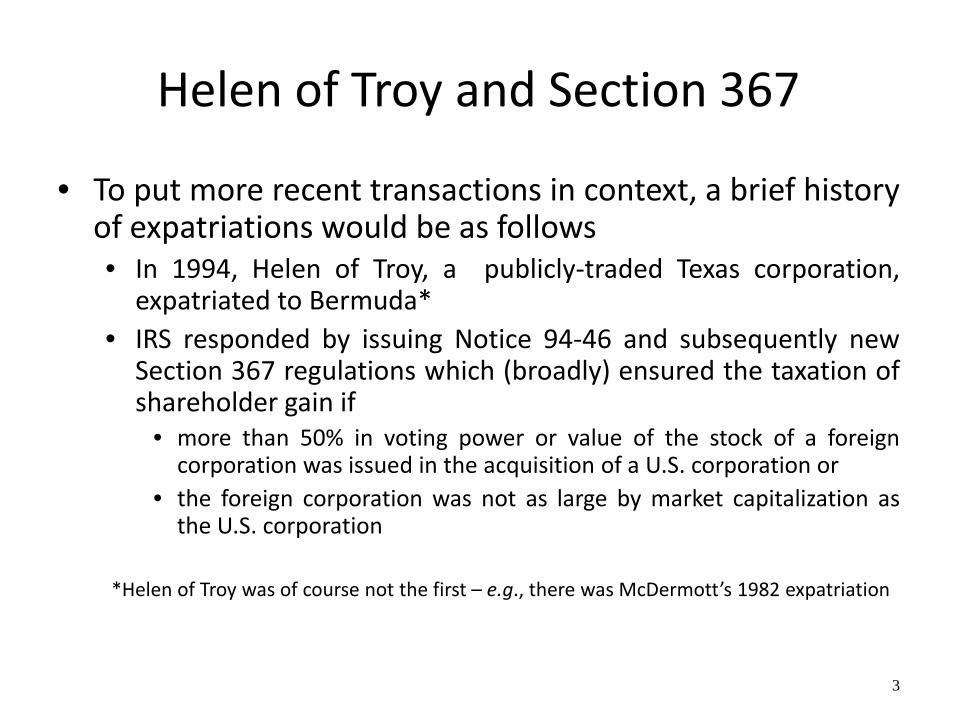

Helen of Troy and Section 367

• To put more recent transactions in context, a brief history of expatriations would be as follows • In 1994, Helen of Troy, a publicly-traded Texas corporation,

expatriated to Bermuda* • IRS responded by issuing Notice 94-46 and subsequently new

Section 367 regulations which (broadly) ensured the taxation of shareholder gain if

• more than 50% in voting power or value of the stock of a foreign corporation was issued in the acquisition of a U.S. corporation or

• the foreign corporation was not as large by market capitalization as the U.S. corporation

*Helen of Troy was of course not the first – e.g., there was McDermott’s 1982 expatriation

3

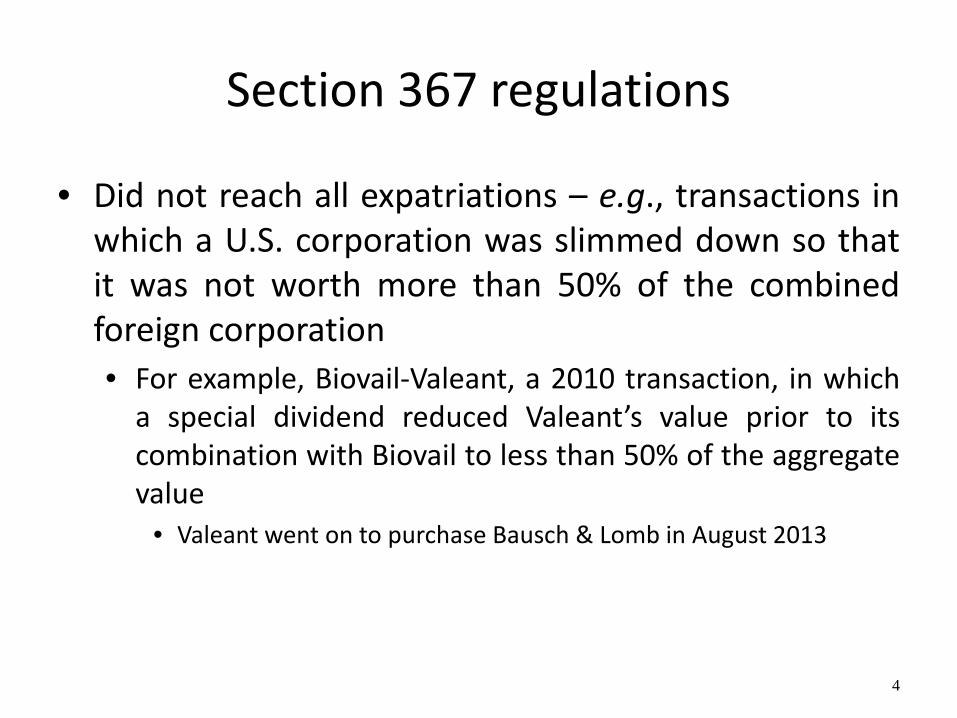

Section 367 regulations

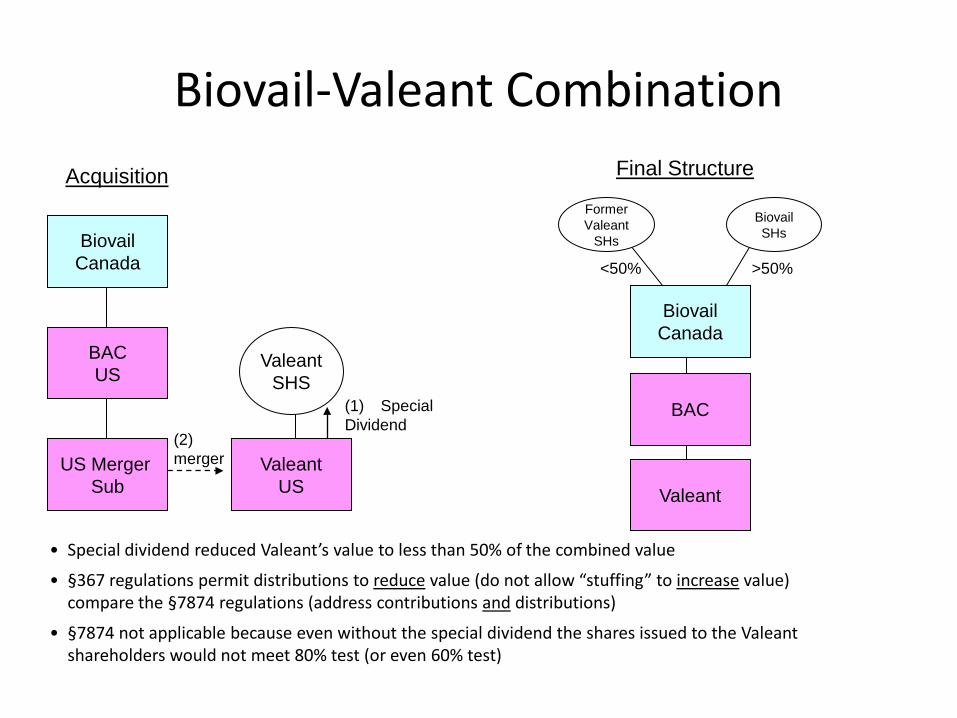

• Did not reach all expatriations – e.g., transactions in which a U.S. corporation was slimmed down so that it was not worth more than 50% of the combined foreign corporation • For example, Biovail-Valeant, a 2010 transaction, in which

a special dividend reduced Valeant’s value prior to its combination with Biovail to less than 50% of the aggregate value

• Valeant went on to purchase Bausch & Lomb in August 2013

4

Acquisition

Biovail Canada

BAC US

US Merger Sub

Valeant US

Valeant SHS

Final Structure

Biovail Canada

BAC

Valeant

Former Valeant

SHs

(2) merger

(1) Special Dividend

<50%

• Special dividend reduced Valeant’s value to less than 50% of the combined value

• §367 regulations permit distributions to reduce value (do not allow “stuffing” to increase value) compare the §7874 regulations (address contributions and distributions)

• §7874 not applicable because even without the special dividend the shares issued to the Valeant shareholders would not meet 80% test (or even 60% test)

Biovail-Valeant Combination

Biovail SHs

>50%

Helen of Troy and Section 367

• Some thought the new Section 367 regulations were misguided, since they did not address the corporate tax issues • The movement of intangibles and foreign subsidiaries out of the

former U.S. parent and the use of leverage to “strip” US earnings • But what could regulations do about that?

• And the Section 367 regulations did not stop expatriations, even when the result was the recognition of gain by shareholders • Specifically, there was a wave of expatriations in 1999-2002 (see the

slides at the end) • To Bermuda or the Cayman Islands, but with the new foreign parent resident

in the Barbados and, because publicly-traded, eligible for treaty benefits, including a 5% withholding tax on dividends

• Ability to stay in the S&P 500 may have helped – S&P regards Bermuda, the Cayman Islands and Barbados as “domiciles of

convenience”

6

Enactment of Section 7874

• This led to the enactment of Section 7874, effective for transactions after March 4, 2003, which • Disregards the expatriation if 80% or more in voting power or

value of the stock of the foreign corporation is acquired by the shareholders of the U.S. corporation, and

• Treats the foreign corporation as a “surrogate foreign corporation” if 60% or more, but less than 80%, of the voting power or value of the stock of the U.S. corporation is acquired

• And taxes the corporation on the “inversion gain” recognized in the next 10 years

• But in either case, not if the new corporation has “substantial business activities” in its country of incorporation or residence

7

Section 7874

• Section 7874 • Overrides all tax treaties

• “Nothing in…any…provision of law shall be construed as permitting an exemption, by reason of any treaty obligation of the United States heretofore or hereafter entered into, from the provisions of this section”

• Controversial effective date – at one point, would have applied to transactions after March 2, 2002, which would have captured some of the corporations that had expatriated

• If there is a “surrogate” foreign corporation, tax imposed at the capital gains rate on the value of stock options and other “specified” stock compensation of “insiders”

SC1:3359384v1 8

Section 7874

• Regulatory or other guidance under Section 7874 includes • Affiliate-owned and “hook” stock

• Publicly-traded foreign partnerships

• Acquisitions of multiple corporations

• Options and the like

• Indirect acquisitions of properties

• Stock of the foreign corporation sold for cash or the like in a transaction related to an inversion – Notice 2009-78

• “Substantial business activities” – as discussed hereafter

SC1:3359384v1 9

Off to Switzerland or Ireland

• Many of the corporations that moved to Bermuda and the Cayman Islands subsequently, in 2008-9, “re-domiciled” to Ireland or Switzerland • Limitation on benefits article of the U.S.-Barbados treaty was

revised so that it no longer gave treaty benefits to a Barbados resident corporation simply because it was traded in the U.S.

• Concerns about legislation introduced in 2007 that would, among other things

• Deny withholding tax reductions for U.S. source interest and royalties if a payment to the ultimate foreign parent would not have been covered by a treaty, or

• At least reduce the rate only to the rate of withholding that applied to the foreign parent, and

• Possibly change the definition of a U.S. corporation to include one that was managed and controlled here

SC1:3359384v1 10

After Section 7874

• Then, in 2011-13 • A series of transactions in which U.S. corporations

merged with smaller but existing Swiss or Irish companies, which • May overcome the 80% or more stock

ownership threshold, but • Will leave open the “surrogate foreign

corporation”, or inversion gain, issue if there are no “substantial business activities” in Switzerland or Ireland

11

After Section 7874

• And a few transactions in which U.S. corporations simply moved (without a merger partner) to the U.K. or the Netherlands • Concluding that they had substantial business activities

there • Such as Ensco International (2011) and Aon (2012) and Sara Lee’s

“coffee” subsidiary (2012)

• Expatriations tend to be oncentrated in specific industries • Pharmaceutical, insurance (and reinsurance) and oil field

services

SC1:3359384v1 12

After Section 7874

• The original, or June 2006, “substantial business activities” regulations had a facts-and-circumstances test and a “bright-line” 10% safe harbor – 10% was described in the preamble as a “reasonable threshold”

• Required that the new jurisdiction have at least 10% in number and compensation of employees, by value of tangible assets, and of sales

– A safe harbor had been recommended by commentators, including the NYSBA Tax Section

• The safe harbor was eliminated in June 2009, leaving only the facts-and-circumstances test • Safe harbor could “apply to certain transactions that are inconsistent

with the purposes of section 7874”

13

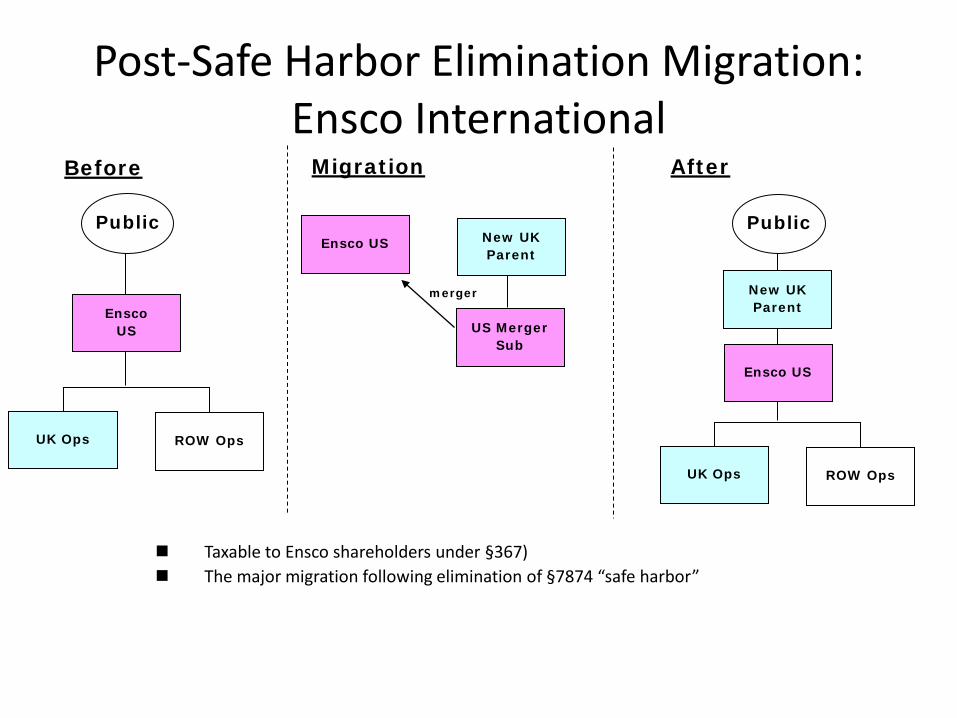

Post-Safe Harbor Elimination Migration: Ensco International

Before

Public

Ensco US

ROW Ops

Migration

Taxable to Ensco shareholders under §367) The major migration following elimination of §7874 “safe harbor”

UK Ops

After

New UK Parent

US Merger Sub

Ensco US Public

New UK Parent

ROW Ops UK Ops

Ensco US

merger

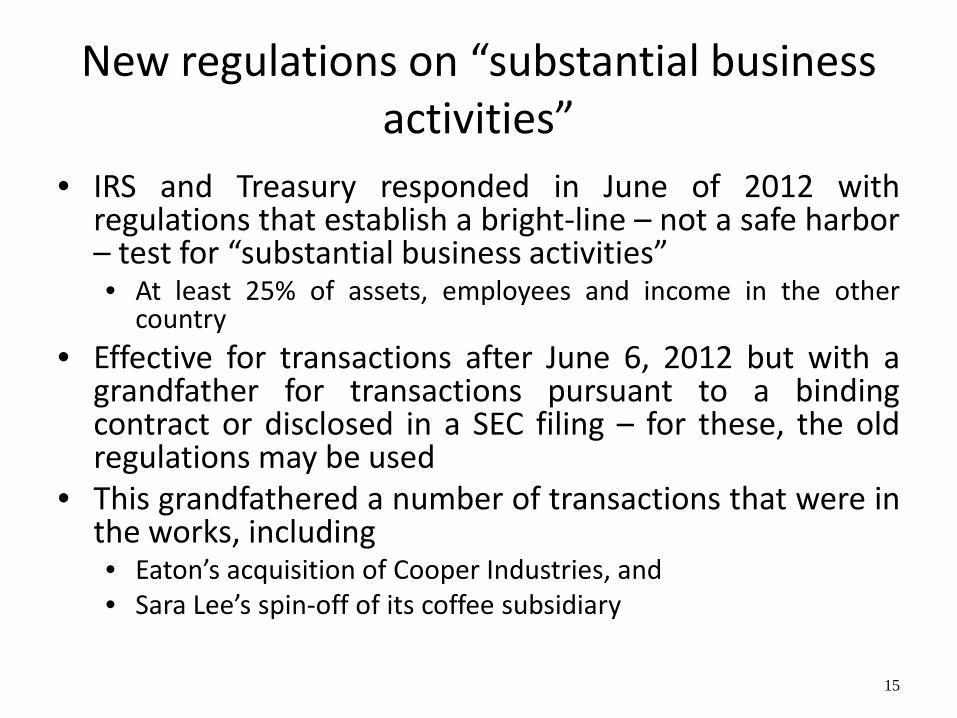

New regulations on “substantial business activities”

• IRS and Treasury responded in June of 2012 with regulations that establish a bright-line – not a safe harbor – test for “substantial business activities” • At least 25% of assets, employees and income in the other

country • Effective for transactions after June 6, 2012 but with a

grandfather for transactions pursuant to a binding contract or disclosed in a SEC filing – for these, the old regulations may be used

• This grandfathered a number of transactions that were in the works, including • Eaton’s acquisition of Cooper Industries, and • Sara Lee’s spin-off of its coffee subsidiary

15

SLC

Sara Lee Restructuring

Foreign Coffee business

Public

• Strong business purposes for splitting into two “pure play” companies under §355

Before (simplified)

US Meats business

Dutch CFC

US

US Coffee

Dutch CFC

US Coffee

Dutch CFC

Foreign Coffee business

(2)

(1)

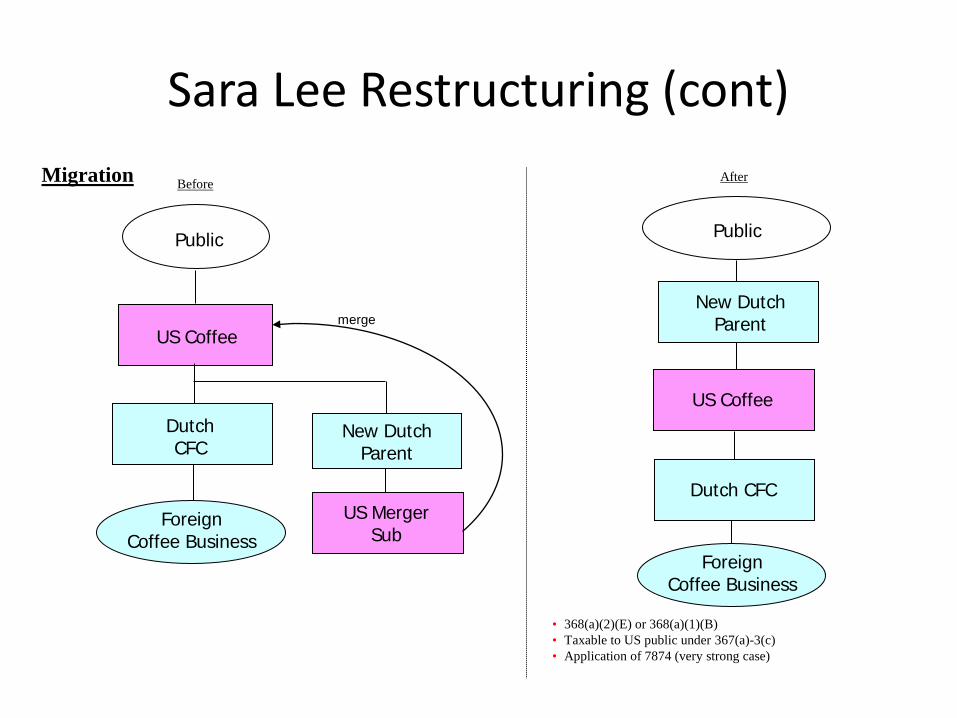

Sara Lee Restructuring (cont)

Foreign Coffee Business

US Coffee

US Coffee

New Dutch Parent

Public

• 368(a)(2)(E) or 368(a)(1)(B) • Taxable to US public under 367(a)-3(c) • Application of 7874 (very strong case)

Migration

Foreign Coffee Business

merge

Public

Before

Dutch CFC

Dutch CFC

After

US Merger Sub

New Dutch Parent

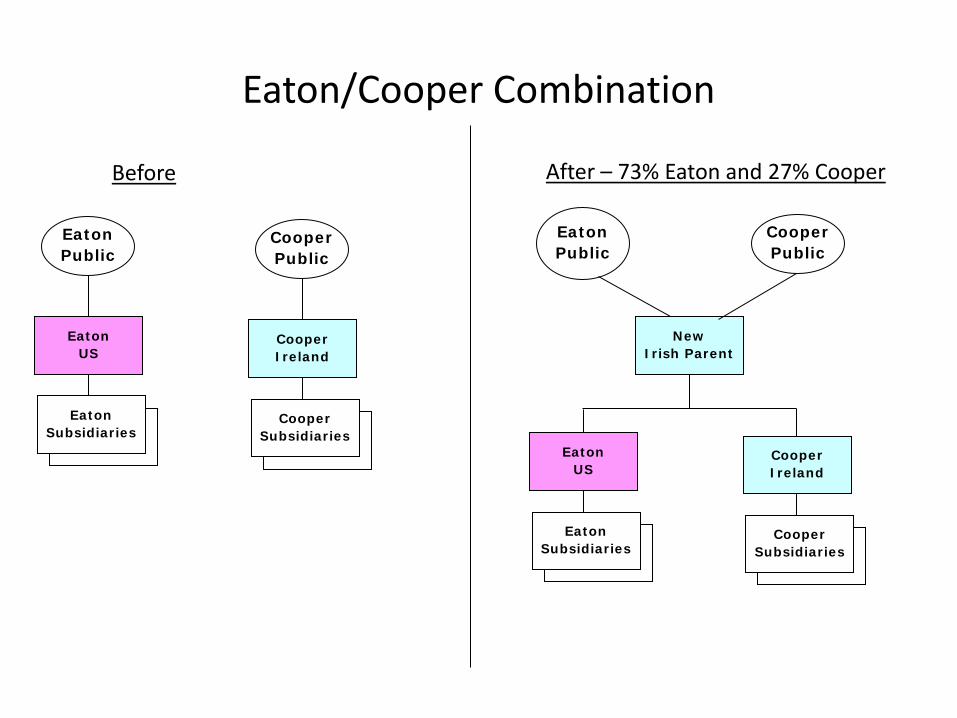

Eaton/Cooper Combination

Eaton Public

Eaton Subsidiaries

Eaton US

Before After – 73% Eaton and 27% Cooper

Cooper Public

Cooper Subsidiaries

Cooper Ireland

Eaton Public

Eaton Subsidiaries

Eaton US

Cooper Public

Cooper Subsidiaries

Cooper Ireland

New Irish Parent

Eaton/Cooper Combination

• Eaton/Cooper was grandfathered from the new “substantial business activities” regulations, but in any event did not satisfy the prior regulations’ fact-and-circumstances test

• From the proxy statement • “Based on the limited guidance available …Eaton currently

expects that [the substantial business activities] test will not be satisfied. As a result, Eaton and its U.S. affiliates could be limited in their ability to utilize their U.S. tax attributes to offset their inversion gain, if any.”

• “However, neither Eaton nor its U.S. affiliates expects to recognize any inversion gain as part of the transaction, nor do they currently intend to engage in any transaction in the near future that would generate inversion gain.”

19

Actavis and Perrigo

• No grandfather for recent transactions • Such as Actavis’ acquisition of Warner Chilcott and Perrigo

Company’s acquisition of Elan Corporation

• Both below the 80% threshold but resulting in more than 60% ownership by the US corporation’s shareholders

• 77% in the case of Actavis and 71% in the case of Elan

20

Why do U.S. corporations expatriate?

• Not all expatriations are tax motivated, but most anticipate post-transaction are reductions in financial statement tax rates • Is it just a vote-with-your feet step by corporations that are

frustrated with tax reform and the absence of a U.S. territorial or exemption system for taxing foreign income?

• Expatriation certainly elects into an exemption system if it is to a country that has such a system, as Ireland, Switzerland, the U.K. and the Netherlands do

• But it also gives the corporation the benefit of a tax treaty with the U.S. and ability through leverage and otherwise to “strip” the earnings of its U.S. operations

21

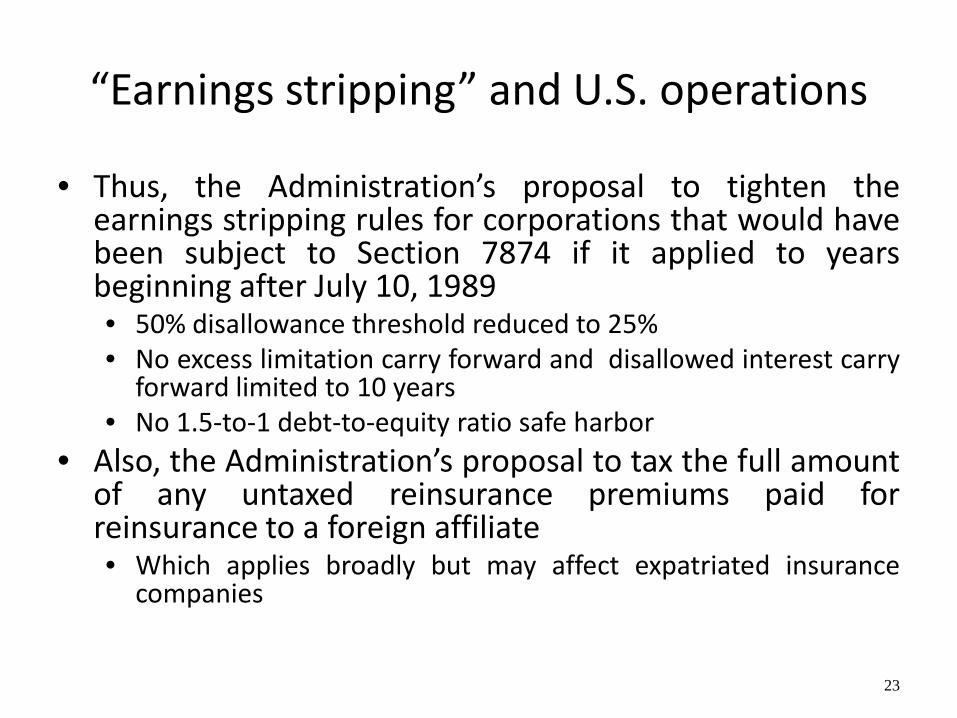

“Earnings stripping” and U.S. operations

• 2007 Treasury Department study of expatriations repeatedly made the earning stripping point • Concluding that data on inverted companies “strongly

suggest that these corporations are shifting substantially all of their income out of the United States, primarily through interest payments” (emphasis added)

• 2007 Congressional Research Service report for Congress made the same point

22

“Earnings stripping” and U.S. operations

• Thus, the Administration’s proposal to tighten the earnings stripping rules for corporations that would have been subject to Section 7874 if it applied to years beginning after July 10, 1989 • 50% disallowance threshold reduced to 25% • No excess limitation carry forward and disallowed interest carry

forward limited to 10 years • No 1.5-to-1 debt-to-equity ratio safe harbor

• Also, the Administration’s proposal to tax the full amount of any untaxed reinsurance premiums paid for reinsurance to a foreign affiliate • Which applies broadly but may affect expatriated insurance

companies

23

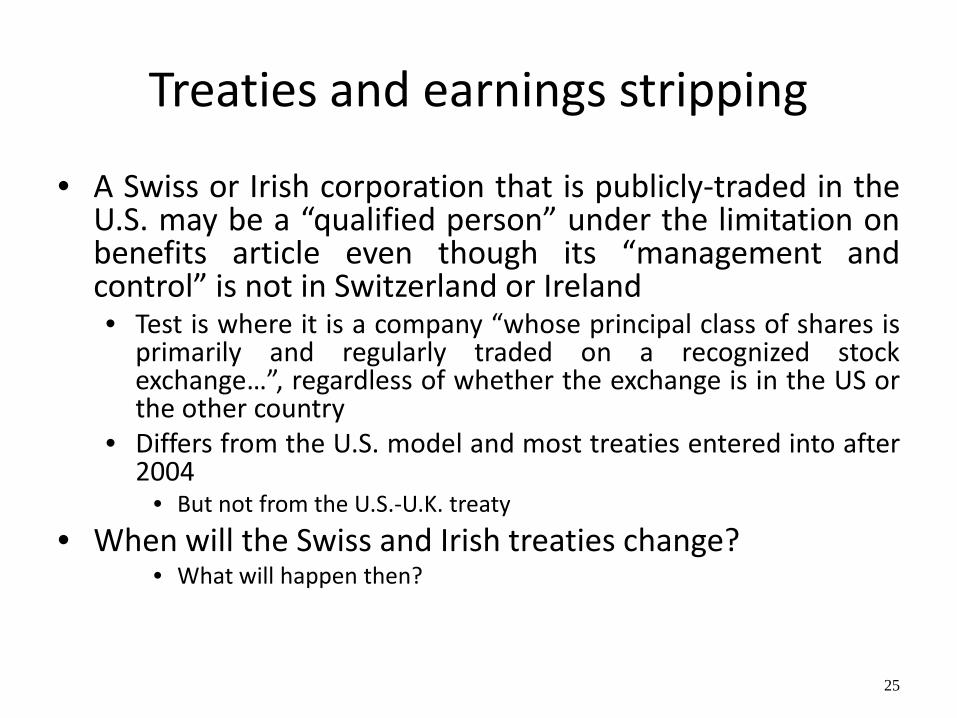

Treaties and earnings stripping

• Treaty benefits are why the original expatriated companies, although incorporated in Bermuda or the Cayman Islands, were often resident in Barbados • And one reason why, when the Barbados treaty changed at

the beginning of 2005, many left in 2008-2009 and moved to Switzerland and Ireland

• “Re-domiciling” to Ireland and Switzerland was also driven by a series of legislative proposals that would affect expatriated entities

24

Treaties and earnings stripping

• A Swiss or Irish corporation that is publicly-traded in the U.S. may be a “qualified person” under the limitation on benefits article even though its “management and control” is not in Switzerland or Ireland • Test is where it is a company “whose principal class of shares is

primarily and regularly traded on a recognized stock exchange…”, regardless of whether the exchange is in the US or the other country

• Differs from the U.S. model and most treaties entered into after 2004

• But not from the U.S.-U.K. treaty

• When will the Swiss and Irish treaties change? • What will happen then?

25

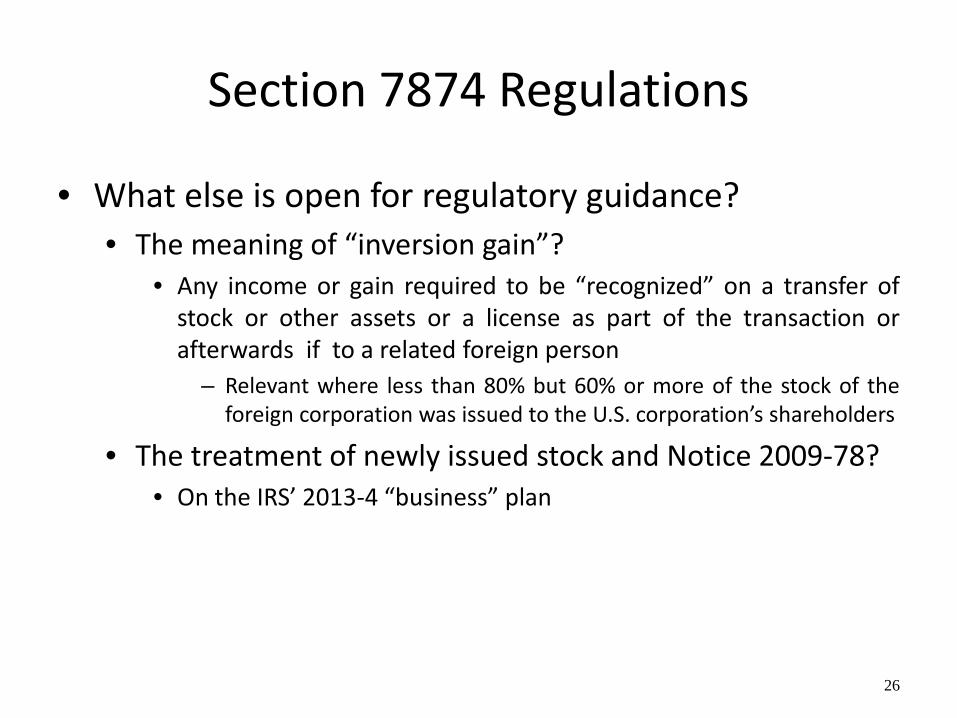

Section 7874 Regulations

• What else is open for regulatory guidance? • The meaning of “inversion gain”?

• Any income or gain required to be “recognized” on a transfer of stock or other assets or a license as part of the transaction or afterwards if to a related foreign person

– Relevant where less than 80% but 60% or more of the stock of the foreign corporation was issued to the U.S. corporation’s shareholders

• The treatment of newly issued stock and Notice 2009-78? • On the IRS’ 2013-4 “business” plan

26

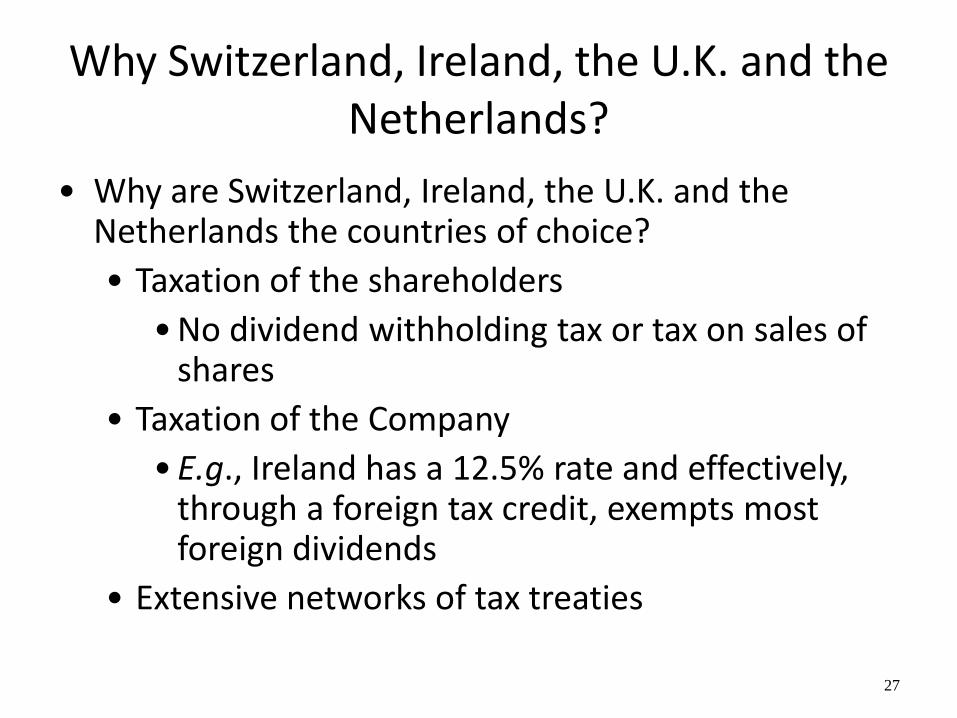

Why Switzerland, Ireland, the U.K. and the Netherlands?

• Why are Switzerland, Ireland, the U.K. and the Netherlands the countries of choice? • Taxation of the shareholders

•No dividend withholding tax or tax on sales of shares

• Taxation of the Company •E.g., Ireland has a 12.5% rate and effectively,

through a foreign tax credit, exempts most foreign dividends

• Extensive networks of tax treaties

27

What do they do when they get there?

• Post-Inversion planning • Replace the equity of the U.S. operations with debt –

euphemistically, “global cash management”* or “capital structure planning”

• De-controlling “controlled foreign corporations – euphemistically, “rationalizing foreign asset ownership”

• “Business restructuring”, “stripped-risk” distributors and other profit shifting steps

• Features of particular transactions – e.g., Eaton/Cooper was for U.S. tax purposes a purchase of Cooper’s assets

*See, e.g., The proxy statements for the Eaton/Cooper and Actavis/Warner Chilcott transactions – Irish incorporation “will result in significantly enhanced global cash management and flexibility….”

28

What do they do when they get there?

• Are there risks in post-inversion planning? Will the debt be respected? • Significant taxpayer victory with respect to debt created in

the ScottishPower’s post-acquisition restructuring of PacifiCorp*

• But • Ingersoll-Rand’s July 2013 10-Q -- “The most significant

adjustments proposed by the IRS [for 3 years under audit] involved treating the entire intercompany debt incurred in connection with the Company’s reincorporation in Bermuda as equity”

– which would result in about $455 million of withholding taxes plus penalties

* NA General Partnership v. Comm’r, 103 T.C.M. (CCH) 1016 (201

29

Are there risks in post-inversion planning?

• And, Tax Analysts (July 2, 2013) – “The IRS disallowed approximately $2.86 billion in interest …of [7] former US. subsidiaries of Tyco International Ltd. arising from intercompany debt,”

• asserting that substantially all of the debt should not be treated as debt for U.S. tax purposes

• Which could ultimately result in a disallowance of $6.6 billion in interest

30

Questions – What is the impact of the new regulations on expatriations?

• The new “substantial business activities” regulations may have slowed but did not stop expatriations • So long as foreign multinationals have tax advantages, will

the result be more tax-driven mergers of US companies with foreign companies?

• And will it be enough to find a merger partner entitled to 20+% of the equity?

• Consider the Eaton/Cooper and other transactions (e.g., Perrigo/Elan, Actavis/Warner Chilcott and Argonaut/PXRE) where 60% or more but less than 80% of the stock was issued to shareholders of the U.S. corporation

SC1:3359384v1 31

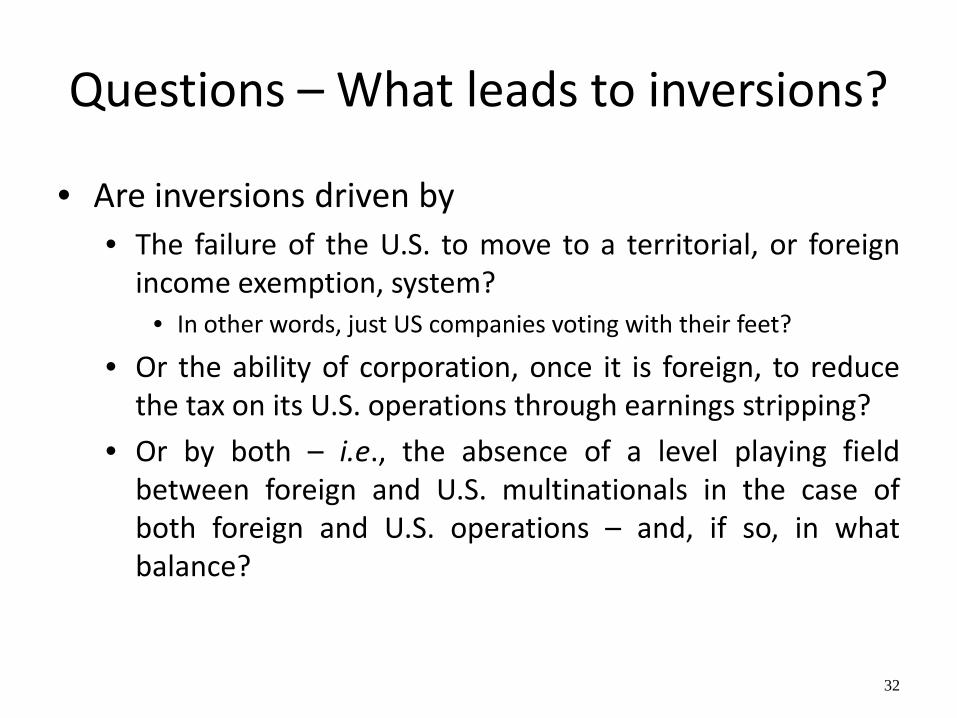

Questions – What leads to inversions?

• Are inversions driven by • The failure of the U.S. to move to a territorial, or foreign

income exemption, system? • In other words, just US companies voting with their feet?

• Or the ability of corporation, once it is foreign, to reduce the tax on its U.S. operations through earnings stripping?

• Or by both – i.e., the absence of a level playing field between foreign and U.S. multinationals in the case of both foreign and U.S. operations – and, if so, in what balance?

32

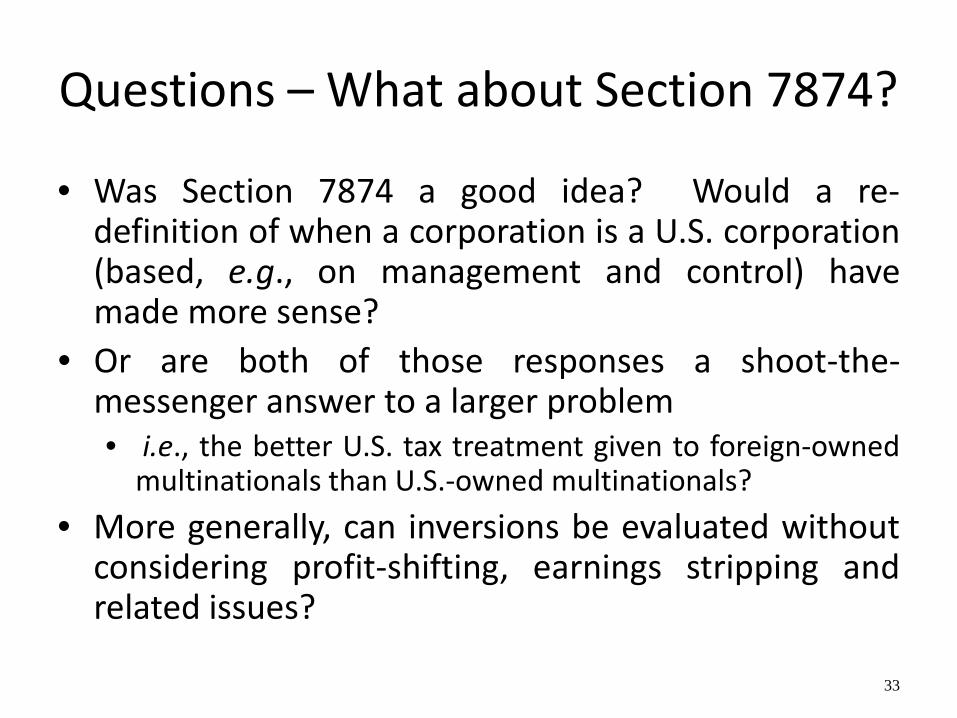

Questions – What about Section 7874?

• Was Section 7874 a good idea? Would a re-definition of when a corporation is a U.S. corporation (based, e.g., on management and control) have made more sense?

• Or are both of those responses a shoot-the-messenger answer to a larger problem • i.e., the better U.S. tax treatment given to foreign-owned

multinationals than U.S.-owned multinationals?

• More generally, can inversions be evaluated without considering profit-shifting, earnings stripping and related issues?

33

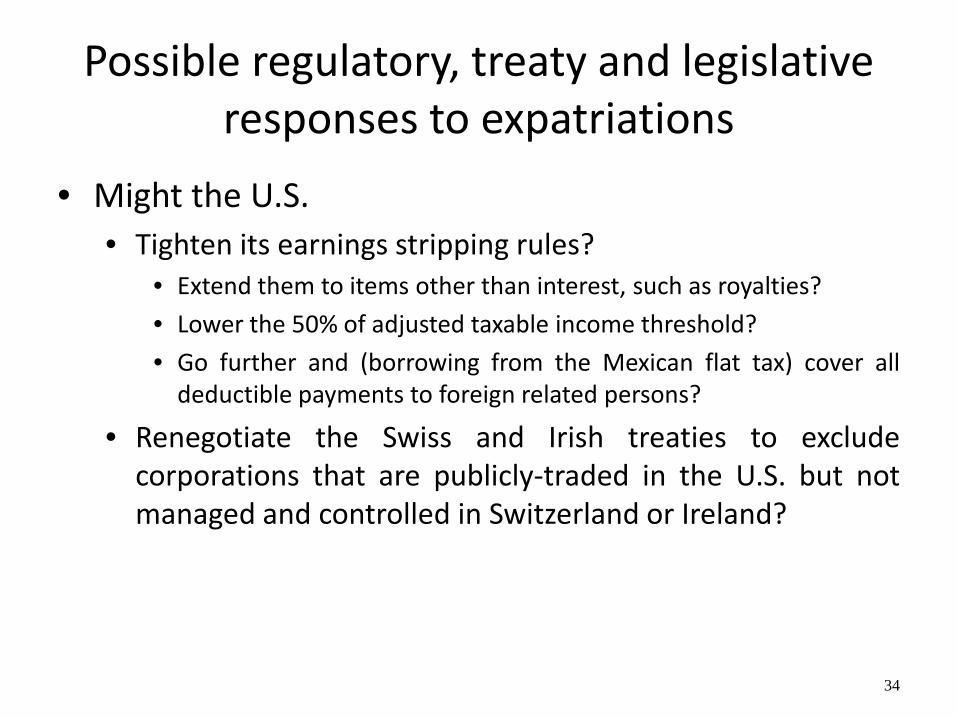

Possible regulatory, treaty and legislative responses to expatriations

• Might the U.S. • Tighten its earnings stripping rules?

• Extend them to items other than interest, such as royalties?

• Lower the 50% of adjusted taxable income threshold?

• Go further and (borrowing from the Mexican flat tax) cover all deductible payments to foreign related persons?

• Renegotiate the Swiss and Irish treaties to exclude corporations that are publicly-traded in the U.S. but not managed and controlled in Switzerland or Ireland?

34

Expatriated U.S. Corporations

35

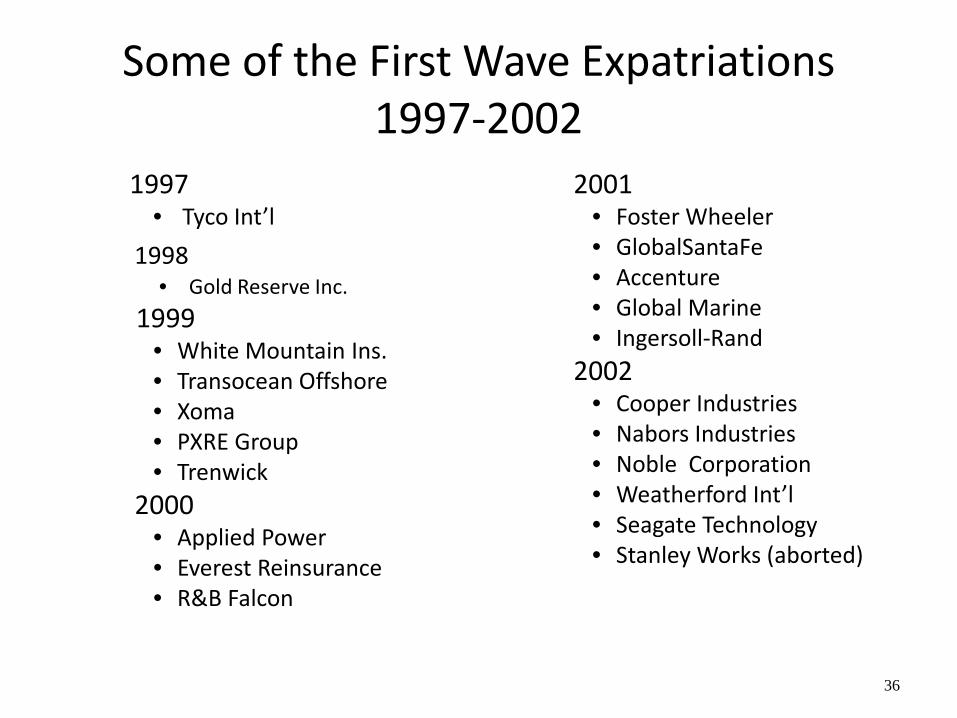

Some of the First Wave Expatriations 1997-2002

1997 • Tyco Int’l

1998 • Gold Reserve Inc.

1999 • White Mountain Ins. • Transocean Offshore • Xoma • PXRE Group • Trenwick

2000 • Applied Power • Everest Reinsurance • R&B Falcon

2001 • Foster Wheeler • GlobalSantaFe • Accenture • Global Marine • Ingersoll-Rand

2002 • Cooper Industries • Nabors Industries • Noble Corporation • Weatherford Int’l • Seagate Technology • Stanley Works (aborted)

36

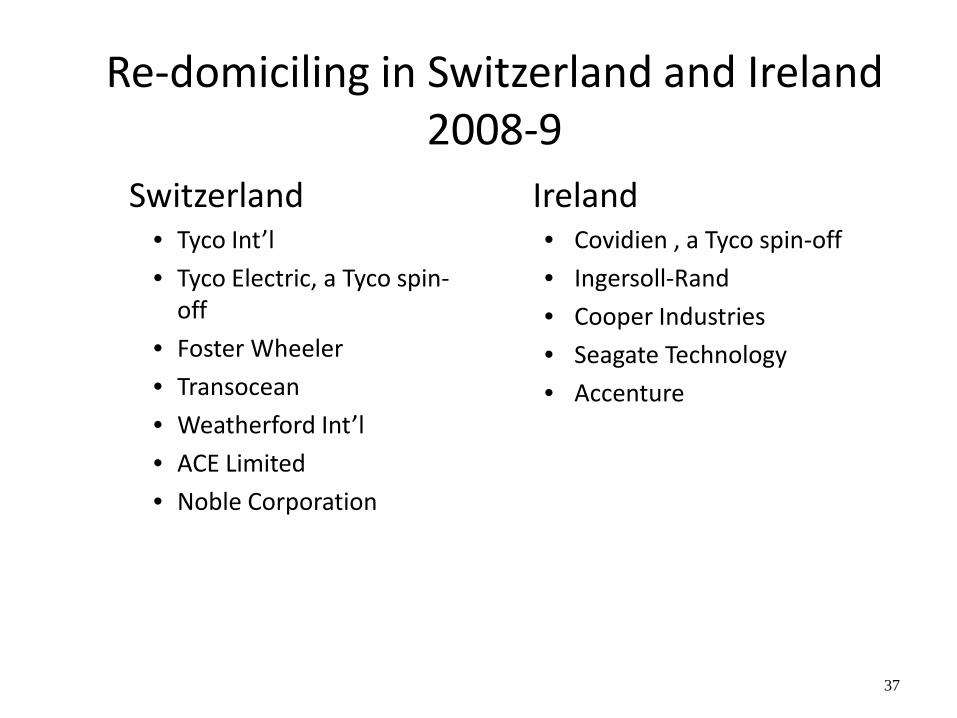

Re-domiciling in Switzerland and Ireland 2008-9

Switzerland • Tyco Int’l

• Tyco Electric, a Tyco spin-off

• Foster Wheeler

• Transocean

• Weatherford Int’l

• ACE Limited

• Noble Corporation

Ireland • Covidien , a Tyco spin-off

• Ingersoll-Rand

• Cooper Industries

• Seagate Technology

• Accenture

37

Some Recent Expatriation Transactions – 2009-13

• ENSCO U.K. • Eaton/Cooper Ireland • Pentair/Tyco spin off Switzerland • Aon Corporation U.K. • Jazz Pharmaceuticals/Azur Pharma Ireland • Alkermes /Elan Corp Ireland • Rowan Companies U.K. • DutchCo, a Sara Lee spin off The Netherlands • Global Indemnity Ireland • Valeant/Biovail Canada • Actavis/Warner Chilcott Ireland • Perrigo/Elan Ireland

38