copyright © 2015 pearson education, inc. publishing as prentice hall 22-1

TRANSCRIPT

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall22-1

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall22-2

Chapter 22

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Nearly 90% of all U.S. companies are family ownedGenerate 64% of the nation's GDPAccount for 63% of all employment and 78% of all job

creationPay 65% of all wages

Globally, family-owned businesses account for 70 to 90% of the world GDP

22-3

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Benefits of Family BusinessLong-term focusFaster decision makingAn entrepreneurial mindsetStrong commitment to their employeesLocal philanthropy

22-4

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

The Dark Side of Family BusinessThe stumbling block for most family companies is

management succession70% of first-generation businesses fail to survive

into the second generationOf those that do, only 13% make it to the third

generation, and just 3% survive to the fourth generation

Result: average life expectancy of a family business is 24 years

22-5

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-6

The World’s Oldest Family Businesses

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Why are the odds of succession so low? No management succession plan!

Most business founders intend to pass their companies on to their children

But... 47% had no written plan to describe what they

wanted to happen to their businesses when they leave

19% had not engaged in any kind of estate planning other than creating a will

22-7

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Characteristics of Successful Family BusinessesShared valuesShared powerTraditionA sense of stewardshipA willingness to learn and adaptBehaving like familiesStrong family support network

22-8

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-9

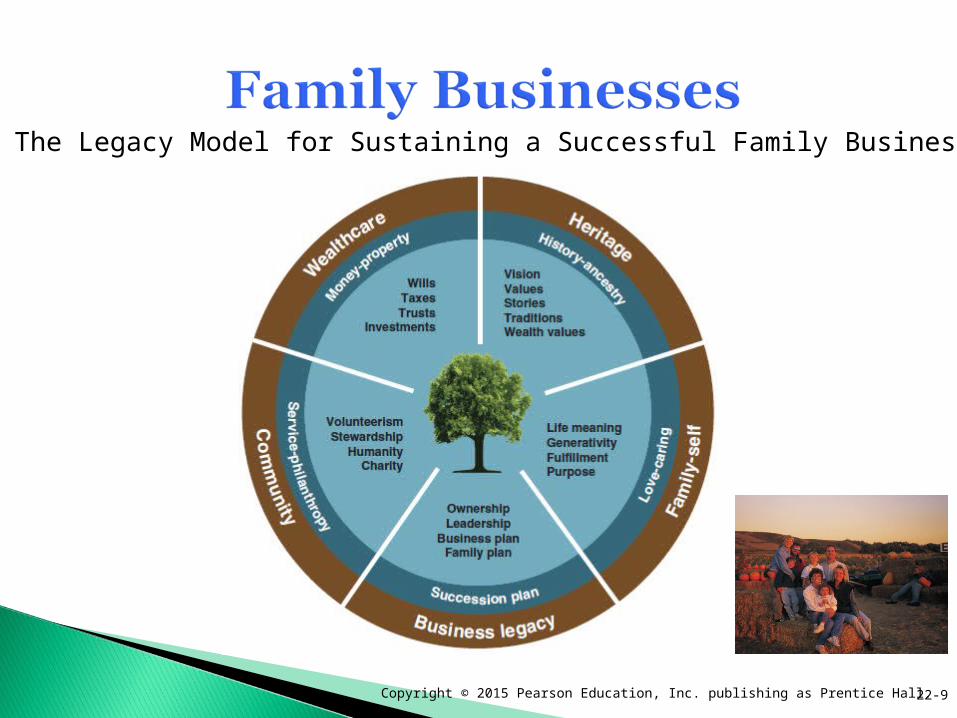

The Legacy Model for Sustaining a Successful Family Business

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-10

Plans for Passing on the Family Business

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

1. Selling to OutsidersStraight sale

2. Selling to InsidersCash plus a noteLeveraged buyouts (LBOs)Employee stock ownership plans (ESOPs)

22-11

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-12

Employee Stock Ownership Plans

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

1. Selling to OutsidersStraight sale

2. Selling to InsidersCash plus a noteLeveraged buyouts (LBOs)Employee stock ownership plans (ESOPs)

3. Transferring to the next generation of family members

22-13

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

By 2040, $10.4 trillion in wealth will be transferred from one generation to the next, much of it funneled through family businesses

For a smooth transition from one generation to the next, family businesses need a succession planAlthough 95% of small business owners

acknowledge the need for a succession plan, only one in eight actually has a written plan in place for leadership continuity

22-14

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-15

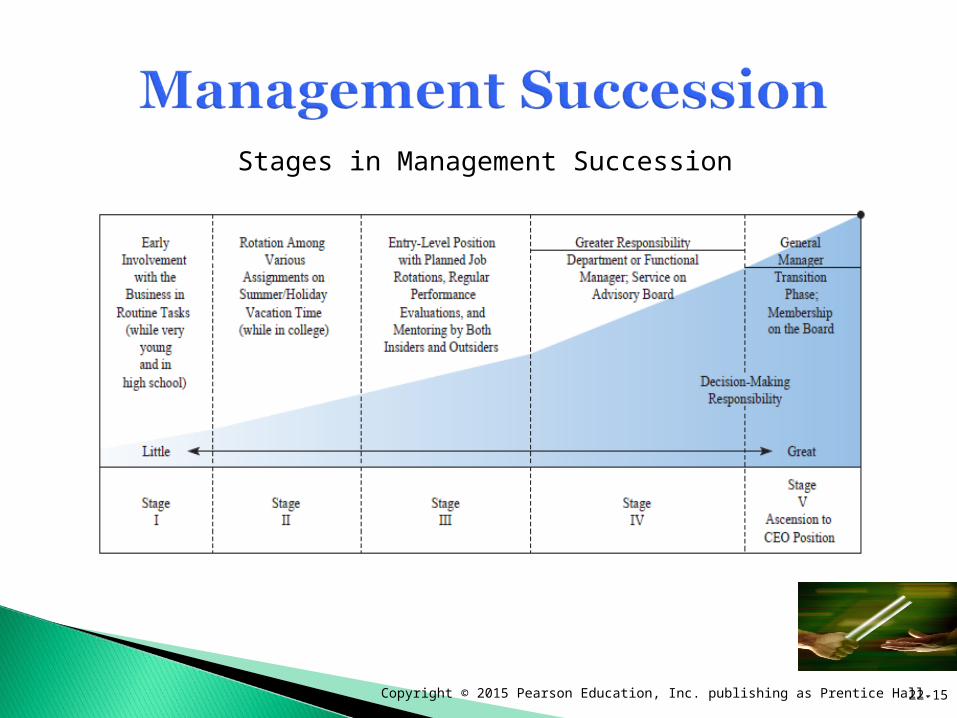

Stages in Management Succession

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Skills a successor needs:Financial abilitiesTechnical knowledgeNegotiating abilityLeadership qualitiesCommunication skillsJuggling skillsIntegrityCommitment to the business

22-16

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Families that are most committed to seeing their businesses survive from one generation to the next Believe that owning the business helps achieve

their families’ mission Are proud of the values on which their businesses

are built Believe that the business is contributing to society

and making it a better place to live Rely on management succession plans to assure

the continuity of the company

22-17

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Creating a succession plan:Step 1: Select the successor

Average tenure of a business founder: 25 yearsBut don’t postpone naming a successor! Make merit, skill, and ability the central focus Don’t assume that the successor must always come

from within the family Make it clear that children are not required to join

the family business Give family members the opportunity to work

outside the family business first

22-18

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Step 2: Create a survival kit for the successorInclude all of the company’s critical

documentsBrief the successor on the contents

22-19

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Step 3: Groom the successor A founder must be:

Patient Willing to accept mistakes Skillful at using mistakes to teach A cheerleader An effective communicator Capable of establishing reasonable

expectations Able to articulate the keys to the successor’s

performance

22-20

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Step 4: Promote an environment of trust and respect Empower the successor gradually Make the final transfer of power smooth

and coordinated Avoid meddling retiree syndrome!

22-21

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Step 5: Cope with the financial realities of estate and gift taxes Minimize the impact of estate and gift taxes

on family members and the business Only 41% of business owners have

created a comprehensive estate plan

22-22

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-23

Changes in the Estate and Gift Taxes

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Buy-Sell AgreementBuy-sell agreement: a contract that co-owners often

rely on to ensure the continuity of a businessLifetime giftingSetting up a trust

Trust: a contract between a grantor (the founder) and a trustee (generally a bank officer or an attorney) in which the grantor gives to the trustee legal title to assets which the trustee agrees to hold for the beneficiaries

22-24

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

TrustsRevocable trustIrrevocable trust

Bypass trustIrrevocable life insurance trustIrrevocable asset trustGrantor retained annuity trust (GRAT)Estate freezeFamily limited partnership

22-25

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Risk management takes a proactive approach to dealing with riskInsurance does not solve all risk problemsDealing with risk successfully requires

1. Risk avoidance2. Risk reduction3. Risk anticipation4. Risk transfer

Captive insurance

22-26

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Insurance: the transfer of risk from one entity (an individual, a group, or a business) to an insurance company

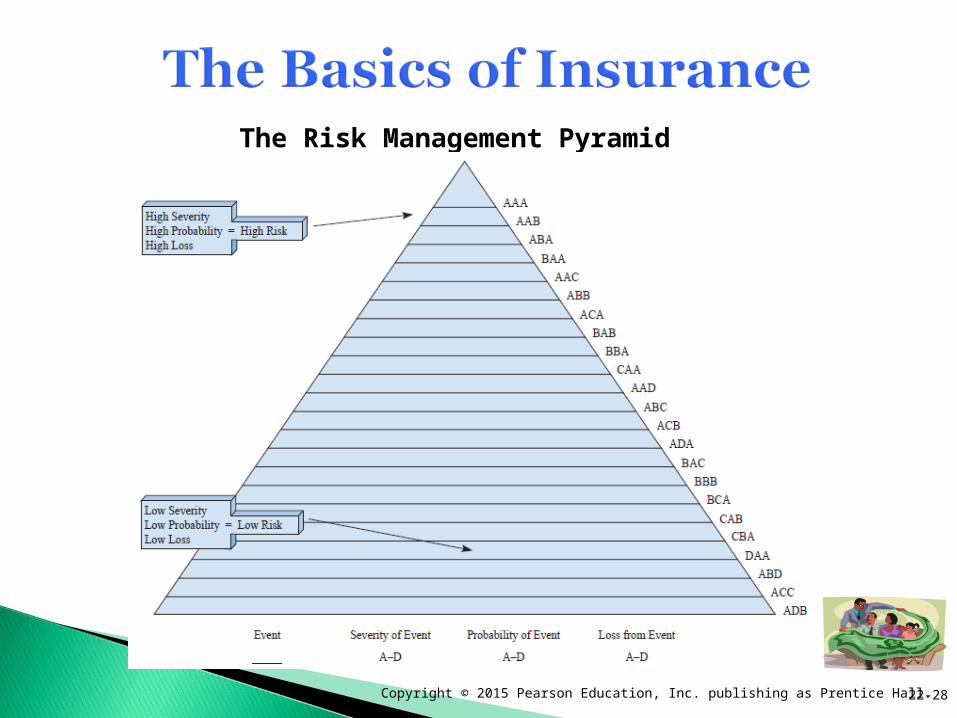

Decide how to allocate risk management dollarsRate primary risks based on:

SeverityProbabilityCost

22-27

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-28

The Risk Management Pyramid

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Types of InsuranceBuy a basic business owner’s policy Add additional coverage as needed

Four major categories:1. Property and casualty2. Extra expense coverage3. Business interruption4. Machinery and equipment

22-29

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Property and casualty insurance Covers tangible assets Buy a replacement cost policy Specific types include:

Property Surety Marine and inland marine Liability Business interruption Motor vehicle

22-30

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Life and disability insurance Life: protects families and business

against loss of income, security, or personal services that results from an individual’s untimely death

Disability: protects an individual in the event of unexpected and often very expensive disabilities

22-31

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Health insurance and workers’ compensation 56.8% of private sector employees get their

health insurance from their employers Patient Protection and Affordable Health Care

Act

22-32

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Health insurance and workers’ compensation 56.8% of private sector employees get their

health insurance from their employers Patient Protection and Affordable Health Care

Act Companies with 50 full-time equivalent

workers who work at least 30 hours a week must provide “minimum essential” and “affordable” health care coverage

22-33

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-34

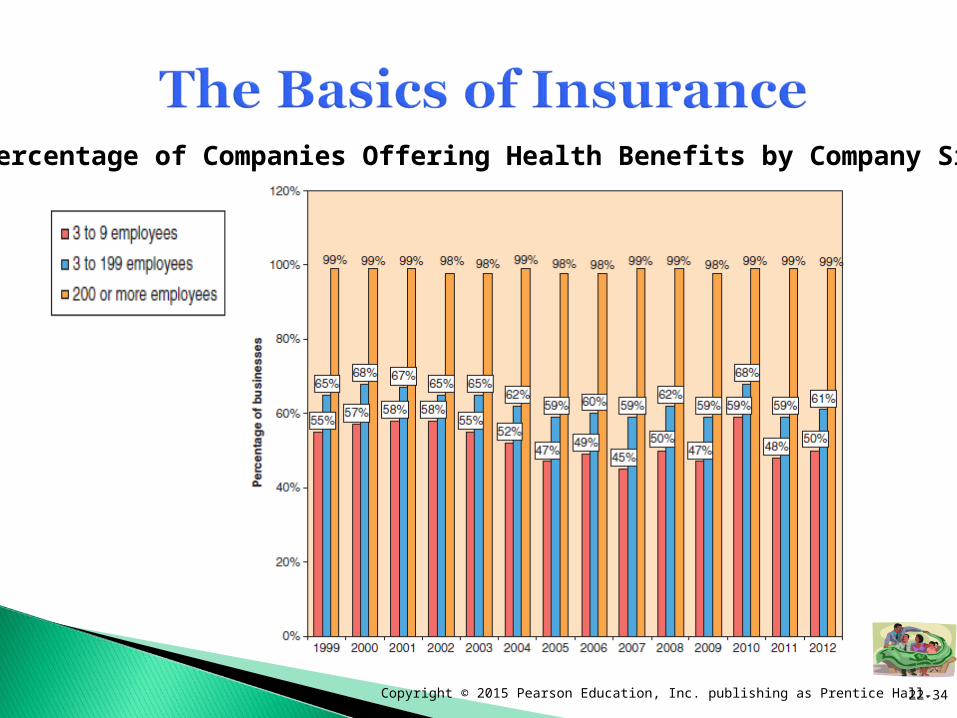

Percentage of Companies Offering Health Benefits by Company Size

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-35

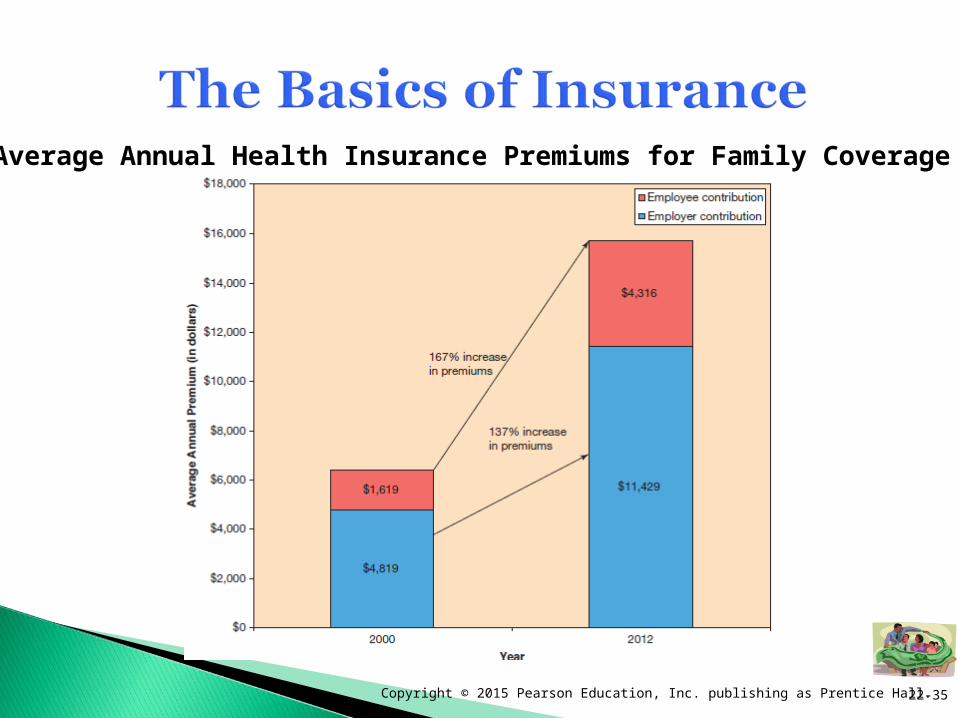

Average Annual Health Insurance Premiums for Family Coverage

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-36

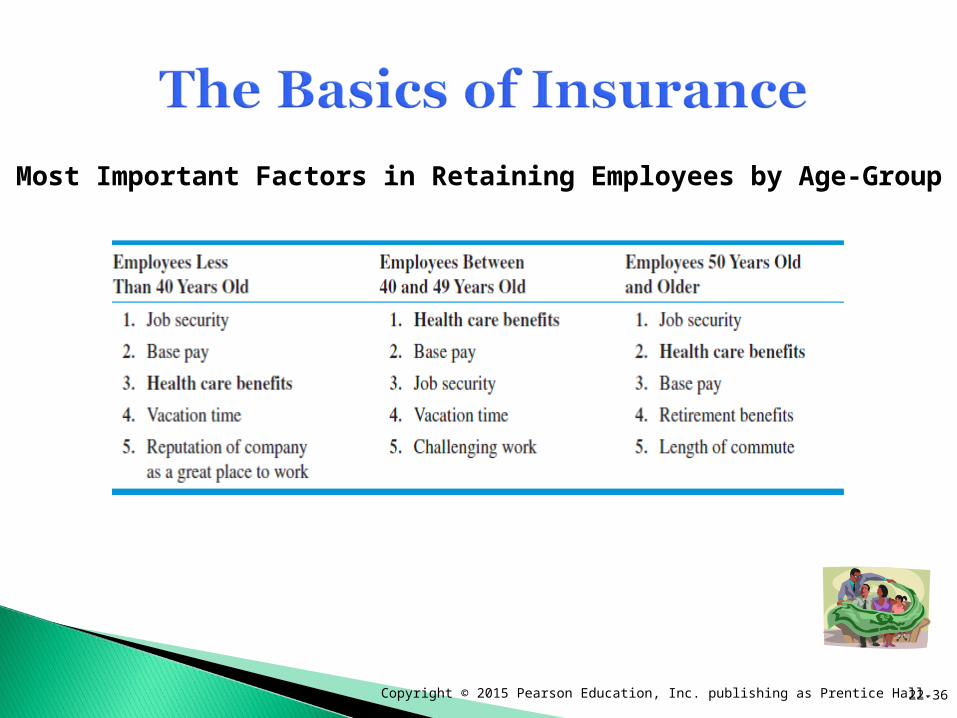

Most Important Factors in Retaining Employees by Age-Group

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

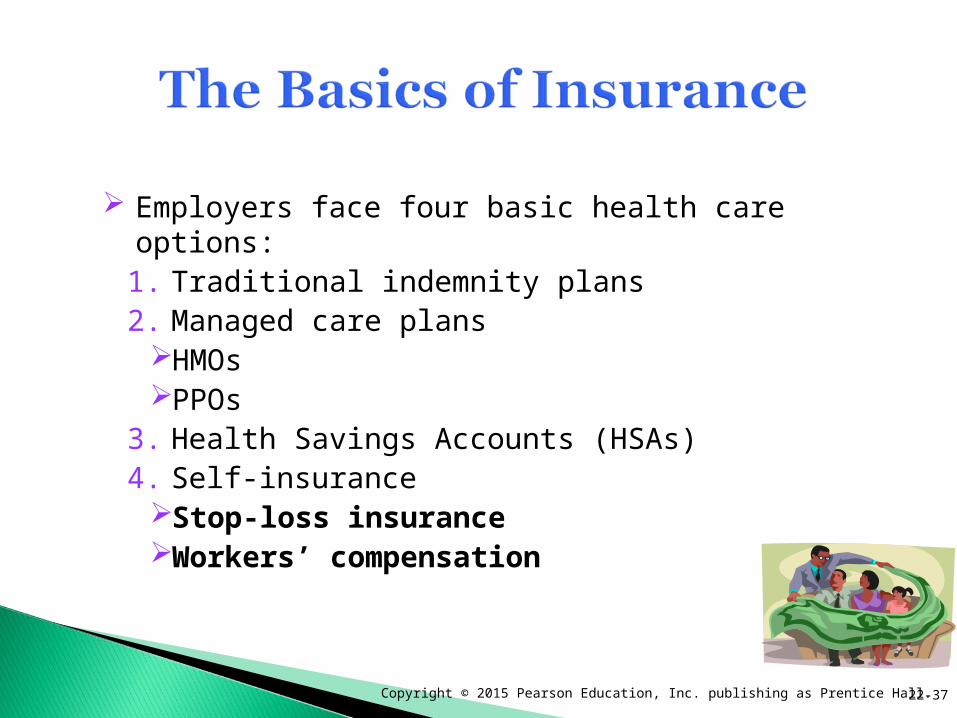

Employers face four basic health care options:1. Traditional indemnity plans2. Managed care plans

HMOsPPOs

3. Health Savings Accounts (HSAs)4. Self-insurance

Stop-loss insuranceWorkers’ compensation

22-37

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-38

Most Dangerous Jobs in the U.S.: Number of Fatal Work Injuries per 100,000 FTE Workers

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Liability insuranceProtects a business against losses resulting from

accidents or injuries people suffer on the company’s property and from its products or services and from damage the company causes to others’ property Professional liability insurance (errors and

omissions coverage) Employment practice liability (EPL) insurance Cyber liability insurance

22-39

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-40

Number of Employment Charges Filed with EEOC

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

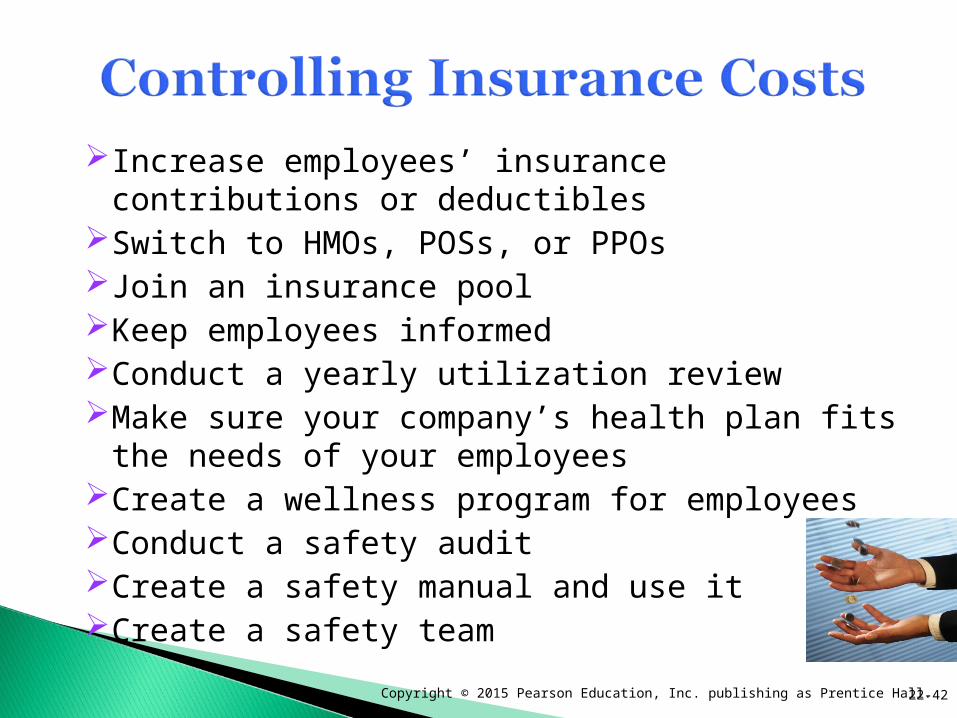

Pursue a loss-control programIncrease your policies' deductiblesWork with a qualified professional insurance broker or

agentFind a broker or agent who understands your needs Find insurance companies that want small companies’

businessUtilize the resources of your insurance company Conduct a periodic insurance auditCompile employment policies into a handbook for

employees

22-41

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall.

Increase employees’ insurance contributions or deductibles

Switch to HMOs, POSs, or PPOsJoin an insurance poolKeep employees informedConduct a yearly utilization reviewMake sure your company’s health plan fits the needs of

your employees Create a wellness program for employeesConduct a safety auditCreate a safety manual and use itCreate a safety team

22-42

Copyright © 2015 Pearson Education, Inc. publishing as Prentice Hall. 22-43