copyright © 2012 pearson prentice hall. all rights reserved. chapter 4 time value of money: valuing...

TRANSCRIPT

Copyright © 2012 Pearson Prentice Hall. All rights reserved.

Chapter 4

Time Value of Money: Valuing Cash Flow Streams

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-2

Chapter Outline

4.1 Valuing a Stream of Cash Flows4.2 Perpetuities4.3 Annuities4.4 Growing Cash Flows4.5 Solving for Variables Other Than Present Value or

Future Value

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-3

Learning Objectives

• Value a series of many cash flows• Value a perpetual series of regular cash flows called a

perpetuity• Value a common set of regular cash flows called an annuity• Value both perpetuities and annuities when the cash flows

grow at a constant rate• Compute the number of periods, cash flow, or rate of return

in a loan or investment

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-4

4.1 Valuing a Stream of Cash Flows

• Rules developed in Chapter 3:– Rule 1: Only values at the same point in time

can be compared or combined.– Rule 2: To calculate a cash flow’s future value,

we must compound it.– Rule 3: To calculate the present value of a

future cash flow, we must discount it.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-5

4.1 Valuing a Stream of Cash Flows

Applying the Rules of Valuing Cash Flows• Suppose we plan to save $1,000 today, and

$1,000 at the end of each of the next two years. • If we earn a fixed 10% interest rate on our

savings, how much will we have three years from today?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-6

4.1 Valuing a Stream of Cash Flows

• We can do this in several ways. • First, take the deposit at date 0 and move it

forward to date 1. • Combine those two amounts and move the

combined total forward to date 2.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-7

4.1 Valuing a Stream of Cash Flows

• Continuing in the same fashion, we can solve the problem as follows:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-8

4.1 Valuing a Stream of Cash Flows

• Another approach is to compute the future value in year 3 of each cash flow separately.

• Once all amounts are in year 3 dollars, combine them.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-9

4.1 Valuing a Stream of Cash Flows

• Consider a stream of cash flows: C0 at date 0, C1 at date 1, and so on, up to CN at date N.

• We compute the present value of this cash flow stream in two steps.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-10

4.1 Valuing a Stream of Cash Flows

• First, compute the present value of each cash flow.

• Then combine the present values.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-11

Example 4.1Present Value of a Stream of Cash Flows

Problem:• You have just graduated and need money to buy a new car. • Your rich Uncle Henry will lend you the money so long as

you agree to pay him back within four years.• You offer to pay him the rate of interest that he would

otherwise get by putting his money in a savings account.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-12

Example 4.1 Present Value of a Stream of Cash Flows (cont’d)

Problem:• Based on your earnings and living expenses, you think you

will be able to pay him $5000 in one year, and then $8000 each year for the next three years.

• If Uncle Henry would otherwise earn 6% per year on his savings, how much can you borrow from him?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-13

Example 4.1 Present Value of a Stream of Cash Flows (cont’d)

Solution:Plan:• The cash flows you can promise Uncle Henry are as follows:

• Uncle Henry should be willing to give you an amount equal to these payments in present value terms.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-14

Example 4.1 Present Value of a Stream of Cash Flows (cont’d)Plan:• We will:

– Solve the problem using equation 4.1– Verify our answer by calculating the future value of this

amount.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-15

Example 4.1 Present Value of a Stream of Cash Flows (cont’d)Execute:• We can calculate the PV as follows:

2 3 4

5000 8000 8000 8000

1.06 1.06 1.06 1.064716.98 7119.97 6716.95 6336.75

$24,890.65

PV

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-16

Example 4.1 Present Value of a Stream of Cash Flows (cont’d)Execute:• Now, suppose that Uncle Henry gives you the money, and

then deposits your payments in the bank each year.• How much will he have four years from now?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-17

Example 4.1 Present Value of a Stream of Cash Flows (cont’d)Execute:• We need to compute the future value of the annual

deposits. • One way is to compute the bank balance each year.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-18

Example 4.1 Present Value of a Stream of Cash Flows (cont’d)Execute:• To verify our answer, suppose your uncle kept his

$24,890.65 in the bank today earning 6% interest. • In four years he would have:

FV= $24,890.65×(1.06)4=$31,423.87 in 4 years

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-19

Example 4.1 Present Value of a Stream of Cash Flows (cont’d)Evaluate:• Thus, Uncle Henry should be willing to lend you $24,890.65

in exchange for your promised payments.• This amount is less than the total you will pay him ($5000+

$8000+$8000+$8000=$29,000) due to the time value of money.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-20

Example 4.1a Present Value of a Stream of Cash Flows

Problem:• You have just graduated and need money to pay

the deposit on an apartment.• Your rich aunt will lend you the money so long as

you agree to pay her back within six months.• You offer to pay her the rate of interest that she

would otherwise get by putting her money in a savings account.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-21

Example 4.1a Present Value of a Stream of Cash Flows (cont’d)Problem:• Based on your earnings and living expenses, you think you

will be able to pay her $70 next month, $85 in each of the next two months, and then $900 each month for months 4 through 6.

• If your aunt would otherwise earn 6% per year on her savings, how much can you borrow from her?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-22

Example 4.1a Present Value of a Stream of Cash Flows (cont’d)

Solution:Plan:• The cash flows you can promise your aunt are as follows:

• She should be willing to give you an amount equal to these payments in present value terms.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-23

Example 4.1a Present Value of a Stream of Cash Flows (cont’d)Plan:• We will:

– Solve the problem using equation 4.1– Verify our answer by calculating the future value of this

amount.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-24

Example 4.1a Present Value of a Stream of Cash Flows (cont’d)

Execute:• We can calculate the PV as follows:

2 3 4 5 6

70 85 85 90 90 90

1.005 1.005 1.005 1.005 1.005 1.005$69.65 $84.16 $83.74 $88.22 $87.78 $87.35

$500.90

PV

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-25

Example 4.1a Present Value of a Stream of Cash Flows (cont’d)Execute:• Now, suppose that your aunt gives you the money, and then

deposits your payments in the bank each month.• How much will she have six months from now?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-26

Example 4.1a Present Value of a Stream of Cash Flows (cont’d)Execute:• We need to compute the future value of the monthly

deposits. • One way is to compute the bank balance each month.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-27

Example 4.1a Present Value of a Stream of Cash Flows (cont’d)

Execute:• To verify our answer, suppose your aunt kept her $500.90 in

the bank today earning 6% interest. • In six months she would have:

FV= $500.90×(1.005)6=$516.11 in 6 months

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-28

Example 4.1a Present Value of a Stream of Cash Flows (cont’d)Evaluate:• Thus, your aunt should be willing to lend you $500.90 in

exchange for your promised payments.• This amount is less than the total you will pay her ($70+

$85+$85+$90+$90+$90=$510) due to the time value of money.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-29

4.1 Valuing a Stream of Cash Flows

Using a Financial Calculator: Solving for Present and Future Values

• Financial calculators and spreadsheets have the formulas pre-programmed to quicken the process.

• There are five variables used most often:– N– PV– PMT– FV– I/Y

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-30

4.1 Valuing a Stream of Cash Flows

Example 1:• Suppose you plan to invest $20,000 in an account

paying 8% interest.• How much will you have in the account in 15

years?• To compute the solution, we enter the four

variables we know and solve for the one we want to determine, FV.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-31

4.1 Valuing a Stream of Cash Flows

Example 1:• For the HP-10BII or the TI-BAII Plus calculators:

– Enter 15 and press the N key.– Enter 8 and press the I/Y key (I/YR for the HP)– Enter -20,000 and press the PV key.– Enter 0 and press the PMT key.– Press the FV key (for the TI, press “CPT” and then “FV”).

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-32

4.1 Valuing a Stream of Cash Flows

Given: 15 8 -20,000 0

Solve for: 63,443

Excel Formula: = FV(0.08,15,0,-20000)

Notice that we entered PV (the amount we’re putting in to the bank) as a negative number and FV is shown as a positive number (the amount we take out of the bank).

It is important to enter the signs correctly to indicate the direction the funds are flowing.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-33

Example 4.2 Computing the Future Value

Problem:• Let’s revisit the savings plan we considered earlier. We plan

to save $1000 today and at the end of each of the next two years.

• At a fixed 10% interest rate, how much will we have in the bank three years from today?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-34

Example 4.2 Computing the Future Value (cont’d)

Solution:Plan:• We’ll start with the timeline for this savings plan:

• Let’s solve this in a different way than we did in the text, while still following the rules.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-35

Example 4.2 Computing the Future Value (cont’d)

Plan:• First we’ll compute the present value of the cash flows.• Then we’ll compute its value three years later (its future

value).

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-36

Example 4.2 Computing the Future Value (cont’d)

Execute:• There are several ways to calculate the present value of the

cash flows.• Here, we treat each cash flow separately an then combine

the present values.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-37

Example 4.2 Computing the Future Value (cont’d)

Execute:• Saving $2735.54 today is equivalent to saving $1000 per

year for three years. • Now let’s compute future value in year 3 of that $2735.54:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-38

Example 4.2 Computing the Future Value (cont’d)

Evaluate:• The answer of $3641 is precisely the same result we found

earlier.• As long as we apply the three rules of valuing cash flows, we

will always get the correct answer.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-39

4.2 Perpetuities

• The formulas we have developed so far allow us to compute the present or future value of any cash flow stream.

• Now we will consider two types of cash flow streams:– Perpetuities– Annuities

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-40

4.2 Perpetuities

Perpetuities– A perpetuity is a stream of equal cash flows

that occur at regular intervals and last forever. – Here is the timeline for a perpetuity:

– the first cash flow does not occur immediately; it arrives at the end of the first period

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-41

4.2 Perpetuities

• Using the formula for present value, the present value of a perpetuity with payment C and interest rate r is given by:

• Notice that all the cash flows are the same.• Also, the first cash flow starts at time 1.

2 3

C C C......

(1 r) (1 r) (1 r)PV=

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-42

4.2 Perpetuities

• Let’s derive a shortcut by creating our own perpetuity.

• Suppose you can invest $100 in a bank account paying 5% interest per year forever.

• At the end of the year you’ll have $105 in the bank – your original $100 plus $5 in interest.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-43

4.2 Perpetuities

• Suppose you withdraw the $5 and reinvest the $100 for another year.

• By doing this year after year, you can withdraw $5 every year in perpetuity:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-44

4.2 Perpetuities

• To generalize, suppose we invest an amount P at an interest rate r.

• Every year we can withdraw the interest we earned, C=r × P, leaving P in the bank.

• Because the cost to create the perpetuity is the investment of principal, P, the value of receiving C in perpetuity is the upfront cost, P.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-45

4.2 Perpetuities

PV (C in perpetuity)

C

r(Eq. 4.4)

Present Value of a Perpetuity

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-46

Example 4.3 Endowing a Perpetuity

Problem: • You want to endow an annual graduation party at your alma

mater. You want the event to be a memorable one, so you budget $30,000 per year forever for the party.

• If the university earns 8% per year on its investments, and if the first party is in one year’s time, how much will you need to donate to endow the party?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-47

Solution:Plan:• The timeline of the cash flows you want to provide

is:

• This is a standard perpetuity of $30,000 per year. The funding you would need to give the university in perpetuity is the present value of this cash flow stream

Example 4.3 Endowing a Perpetuity (cont’d)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-48

Example 4.3 Endowing a Perpetuity (cont’d)

Execute:• From the formula for a perpetuity,

PV C / r $30, 000/0.08 $375,000 today

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-49

Example 4.3 Endowing a Perpetuity (cont’d)

Evaluate:• If you donate $375,000 today, and if the university invests it

at 8% per year forever, then the graduates will have $30,000 every year for their graduation party.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-50

Example 4.3a Endowing a Perpetuity

Problem: • You just won the lottery, and you want to endow a

professorship at your alma mater. • You are willing to donate $4 million of your winnings for this

purpose. • If the university earns 5% per year on its investments, and

the professor will be receiving her first payment in one year, how much will the endowment pay her each year?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-51

Solution:Plan:• The timeline of the cash flows you want to provide

is:

• This is a standard perpetuity. The amount she can withdraw each year and keep the principal intact is the cash flow when solving equation 4.4.

Example 4.3aEndowing a Perpetuity (cont’d)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-52

Example 4.3aEndowing a Perpetuity (cont’d)

Execute:• From the formula for a perpetuity,

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-53

Example 4.3a Endowing a Perpetuity (cont’d)

Evaluate:• If you donate $4,000,000 today, and if the university invests

it at 5% per year forever, then the chosen professor will receive $200,000 every year.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-54

4.3 Annuities

• Annuities – An annuity is a stream of N equal cash flows

paid at regular intervals.

– The difference between an annuity and a perpetuity is that an annuity ends after some fixed number of payments

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-55

4.3 Annuities

Present Value of An Annuity• Note that, just as with the perpetuity, we

assume the first payment takes place one period from today.

• To find a simpler formula, use the same approach as we did with a perpetuity: create your own annuity.

2 3 N

C C C C......

(1 r) (1 r) (1 r) (1 r)PV=

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-56

4.3 Annuities

• With an initial $100 investment at 5% interest, you can create a 20-year annuity of $5 per year, plus you will receive an extra $100 when you close the account at the end of 20 years:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-57Copyright © 2009 Pearson Prentice Hall. All rights reserved. 4-57

4.3 Annuities

• The Law of One Price tells us that because it only took an initial investment of $100 to create the cash flows on the timeline, the present value of these cash flows is $100:

$100 20 - year annuity of $5 per year $100 in 20 yearsPV( ) PV( )

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-58

4.3 Annuities

• Rearranging:

20

20 - year annuity of $5 per year $100 $100 in 20 years

$100$100 - $100 $37.69 $62.31

(1.05)

PV( ) PV( )

=

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-59

4.3 Annuities

• We usually want to know the PV as a function of C, r, and N.

• Since C can be written as $100(0.05)=$5, we can further re-arrange:

20 20

20

$5$5 $5 10.0520 - year annuity of $5 per year - 1

0.05 (1.05) 0.05 1.05

1 1$5 1

(0.05) 1.05

PV( )=

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-60

4.3 Annuities

• In general:

1 1(annuity of C for N periods with interest rate r) 1

(1 NPV C

r r)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-61

Example 4.4 Present Value of a Lottery Prize AnnuityProblem: • You are the lucky winner of the $30 million state lottery. • You can take your prize money either as (a) 30 payments of

$1 million per year (starting today), or (b) $15 million paid today.

• If the interest rate is 8%, which option should you take?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-62

Example 4.4 Present Value of a Lottery Prize Annuity (cont’d)Solution: Plan:• Option (a) provides $30 million in prize money but paid over

time. To evaluate it correctly, we must convert it to a present value. Here is the timeline:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-63

Example 4.4 Present Value of a Lottery Prize Annuity (cont’d)Plan (cont’d):• Because the first payment starts today, the last payment

will occur in 29 years (for a total of 30 payments). • The $1 million at date 0 is already stated in present value

terms, but we need to compute the present value of the remaining payments.

• Fortunately, this case looks like a 29-year annuity of $1 million per year, so we can use the annuity formula.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-64

Example 4.4 Present Value of a Lottery Prize Annuity (cont’d)Execute:• From the formula for an annuity,

PV( 29-year annuity of $1million) $1 million 1

0.081

1

1.0829

$1 million 11.16

$11.16 million today

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-65

Example 4.4 Present Value of a Lottery Prize Annuity (cont’d)Execute (cont’d):• Thus, the total present value of the cash flows is $1 million

+ $11.16 million = $12.16 million. In timeline form:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-66

Example 4.4 Present Value of a Lottery Prize Annuity (cont’d)Execute (cont’d): • Financial calculators or Excel can handle annuities easily—

just enter the cash flow in the annuity as the PMT:

Given: 29 8.0 1,000,000 0

Solve for: -11,158,406

Excel Formula: =PV(RATE,NPER, PMT, FV) = PV(0.08,29,1000000,0)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-67

Example 4.4 Present Value of a Lottery Prize Annuity (cont’d)

Evaluate:• The reason for the difference is the time value of money. • If you have the $15 million today, you can use $1 million

immediately and invest the remaining $14 million at an 8% interest rate.

• This strategy will give you $14 million 8% = $1.12 million per year in perpetuity!

• Alternatively, you can spend $15 million – $11.16 million = $3.84 million today, and invest the remaining $11.16 million, which will still allow you to withdraw $1 million each year for the next 29 years before your account is depleted.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-68

Example 4.4a Present Value of an Annuity

Problem: • Your parents have made you an offer you can’t refuse. • They’re planning to give you part of your inheritance

early. • They’ve given you a choice. • They’ll pay you $10,000 per year for each of the next

seven years (beginning today) or they’ll give you their 2007 BMW M6 Convertible, which you can sell for $61,000 (guaranteed) today.

• If you can earn 7% annually on your investments, which should you choose?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-69

Example 4.4a Present Value of an Annuity (cont’d)

Solution: Plan:• Option (a) provides $10,000 paid over time. To evaluate it

correctly, we must convert it to a present value. Here is the timeline:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-70

Example 4.4a Present Value of an Annuity (cont’d)

Plan (cont’d):• The $10,000 at date 0 is already stated in present value

terms, but we need to compute the present value of the remaining payments.

• Fortunately, this case looks like a 6-year annuity of $10,000 per year, so we can use the annuity formula.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-71

Example 4.4a Present Value of an Annuity (cont’d)

Execute:• From the formula for a annuity,

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-72

Example 4.4a Present Value of an Annuity (cont’d)

Execute (cont’d):• Thus, the total present value of the cash flows is $10,000 +

$47,665. In timeline form:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-73

Example 4.4a Present Value of an Annuity (cont’d)

Execute (cont’d): • Financial calculators or Excel can handle annuities easily—

just enter the cash flow in the annuity as the PMT:

Given: 6 7 10000 0

Solve for: -47,665

Excel Formula: =PV(RATE,NPER, PMT, FV) = PV(0.07,6,10000,0)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-74

Example 4.4a Present Value of an Annuity (cont’d)

Evaluate:• Lucky you! • Even if you don’t want to keep it, the fact that you can sell it

for more than the annuity is worth means you’re better off taking the BMW.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-75

4.3 Annuities

(annuity) (1

11 (1 )

(1 )

1((1 ) 1)

N

NN

N

FV PV r)

Cr

r r

C rr

(Eq. 4.6)

Future Value of an Annuity

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-76

Example 4.5 Retirement Savings Plan Annuity

Problem: • Ellen is 35 years old, and she has decided it is time to plan

seriously for her retirement. • At the end of each year until she is 65, she will save

$10,000 in a retirement account. • If the account earns 10% per year, how much will Ellen have

saved at age 65?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-77

Example 4.5 Retirement Savings Plan Annuity (cont’d)

SolutionPlan:• As always, we begin with a timeline. In this case, it is helpful

to keep track of both the dates and Ellen’s age:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-78

Example 4.5 Retirement Savings Plan Annuity (cont’d)Plan (cont’d):• Ellen’s savings plan looks like an annuity of

$10,000 per year for 30 years. • (Hint: It is easy to become confused when you just

look at age, rather than at both dates and age. A common error is to think there are only 65-36= 29 payments. Writing down both dates and age avoids this problem.)

• To determine the amount Ellen will have in the bank at age 65, we’ll need to compute the future value of this annuity.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-79

Example 4.5 Retirement Savings Plan Annuity

Execute:

Using Financial calculators or Excel:

FV $10,000 1

0.10(1.1030 1)

$10,000 164.49

$1.645 million at age 65

Given: 30 10.0 0 -10,000

Solve for: -1,644,940

Excel Formula: =FV(RATE,NPER, PMT, PV) = FV(0.10,30,10000,0)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-80

Example 4.5 Retirement Savings Plan Annuity

Evaluate:• By investing $10,000 per year for 30 years (a total of

$300,000) and earning interest on those investments, the

compounding will allow her to retire with $1.645 million.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-81

Example 4.5a Retirement Savings Plan Annuity

Problem: • Adam is 25 years old, and he has decided it is time to plan

seriously for his retirement. • He will save $10,000 in a retirement account at the end of

each year until he is 45. • At that time, he will stop paying into the account, though he

does not plan to retire until he is 65. • If the account earns 10% per year, how much will Adam

have saved at age 65?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-82

Example 4.5aRetirement Savings Plan Annuity

SolutionPlan:• As always, we begin with a timeline. In this case, it is helpful

to keep track of both the dates and Adam’s age:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-83

Example 4.5aRetirement Savings Plan Annuity

• Adam’s savings plan looks like an annuity of $10,000 per year for 20 years.

• The money will then remain in the account until Adam is 65 – 20 more years.

• To determine the amount Adam will have in the bank at age 45, we’ll need to compute the future value of this annuity.

• Then we’ll compound the future value into the future 20 more years to see how much he’ll have at 65.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-84

Example 4.5a Retirement Savings Plan Annuity

Execute:

Using Financial calculators or Excel:

Given: 20 10.0 0 -10,000

Solve for: $572,750

Excel Formula: =FV(RATE,NPER, PMT, PV) = FV(0.10,20,10000,0)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-85

Example 4.5a Retirement Savings Plan Annuity

Execute:

Using Financial calculators or Excel:

Given: 20 10.0 -$572,750 0

Solve for: $3,853,175

Excel Formula: =FV(RATE,NPER, PMT, PV) = FV(0.10,20,0,-572750)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-86

Example 4.5a Retirement Savings Plan Annuity

Evaluate:• By investing $10,000 per year for 20 years (a total

of $200,000) and earning interest on those investments, the compounding will allow him to retire with $3.85 million.

• Even though he invested for 10 fewer years than Ellen did, Adam will end up with more than twice as much money because he’s starting his retirement plan ten years earlier than she will.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-87

4.4 Growing Cash Flows

• A growing perpetuity is a stream of cash flows that occur at regular intervals and grow at a constant rate forever.

• For example, a growing perpetuity with a first payment of $100 that grows at a rate of 3% has the following timeline:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-88

4.4 Growing Cash Flows

PV (growing perpetuity)

C

r g(Eq. 4.7)

Present Value of a Growing Perpetuity

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-89

Example 4.6 Endowing a Growing Perpetuity

Problem: • In Example 4.3, you planned to donate money to your alma

mater to fund an annual $30,000 graduation party. • Given an interest rate of 8% per year, the required donation

was the present value of PV=$30,000/0.08=$375,000. • Before accepting the money, however, the student

association has asked that you increase the donation to account for the effect of inflation on the cost of the party in future years.

• Although $30,000 is adequate for next year’s party, the students estimate that the party’s cost will rise by 4% per year thereafter.

• To satisfy their request, how much do you need to donate now?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-90

Example 4.6 Endowing a Growing Perpetuity (cont’d)Solution:Plan:• The cost of the party next year is $30,000, and the cost

then increases 4% per year forever. From the timeline, we recognize the form of a growing perpetuity and can value it that way.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-91

Example 4.6 Endowing a Growing Perpetuity (cont’d)Execute:• To finance the growing cost, you need to

provide the present value today of:

PV $30,000 / (0.08 0.04) $750,000 today

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-92

Example 4.6 Endowing a Growing Perpetuity (cont’d)Evaluate:• You need to double the size of your gift!

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-93

Example 4.6a Endowing a Growing Perpetuity

Problem: • In Example 4.3a, you planned to donate $4 million to your

alma mater to fund an endowed professorship. • Given an interest rate of 7% per year, the professor would

be able to collect $200,000 per year from your generosity. • The inflation rate is expected to be 2% per year. • How much can the professor be paid in the first year in

order to allow her annual salary to increase by 2% each year and keep the principal intact?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-94

Example 4.6a Endowing a Growing Perpetuity (cont’d)Solution:Plan:• The salary needs to increase 2% per year forever. From the

timeline, we recognize the form of a growing perpetuity and can value it that way.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-95

Example 4.6a Endowing a Growing Perpetuity (cont’d)

Evaluate:• She can only withdraw $120,000 in her first year.

• In the second year, her payment will be $120,000 X 1.02 = $122,400 and the payments will continue to increase each year.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-96

4.4 Growing Cash Flows

Present Value of a Growing Annuity• A growing annuity is a stream of N growing

cash flows, paid at regular intervals• It is a growing perpetuity that eventually

comes to an end.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-97

4.4 Growing Cash Flows

• The following timeline shows a growing annuity with initial cash flow C, growing at a rate of g every period until period N:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-98

4.4 Growing Cash Flows

• Present Value of a Growing Annuity:

N1 1

11

gPV= C

r - g r

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-99

Example 4.7Retirement Savings with a Growing AnnuityProblem: • In Example 4.5, Ellen considered saving $10,000 per year

for her retirement. Although $10,000 is the most she can save in the first year, she expects her salary to increase each year so that she will be able to increase her savings by 5% per year. With this plan, if she earns 10% per year on her savings, how much will Ellen have saved at age 65?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-100

Example 4.7Retirement Savings with a Growing Annuity (cont’d)

Solution:Plan: Her new savings plan is represented by the following timeline:

This example involves a 30-year growing annuity with a growth rate of 5% and an initial cash flow of $10,000. We can use Eq. 4.8 to solve for the present value of a growing annuity.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-101

Example 4.7Retirement Savings with a Growing Annuity (cont’d)

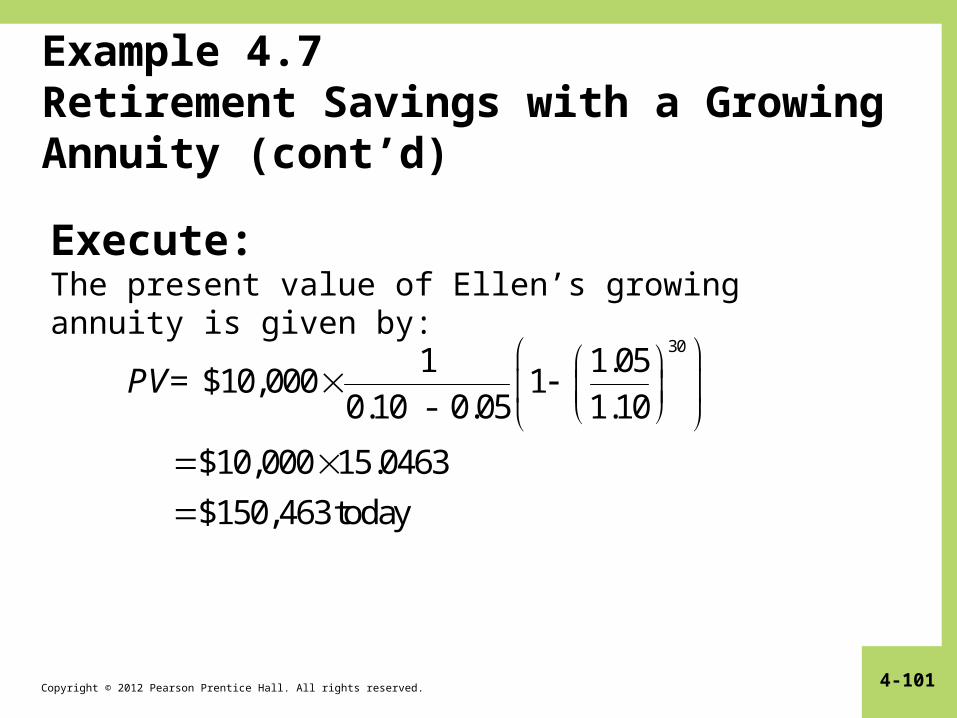

Execute: The present value of Ellen’s growing annuity is given by:

301 1.05

$10,000 10.10 - 0.05 1.10

$10,000 15.0463

$150,463today

PV=

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-102

Example 4.7Retirement Savings with a Growing Annuity (cont’d)

30$150,463 1.10

$2.625

FV=

million in 30 years

Execute: •Ellen’s proposed savings plan is equivalent to

having $150,463 in the bank today. To determine the amount she will have at age 65, we need to move this amount forward 30 years:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-103

Example 4.7Retirement Savings with a Growing Annuity (cont’d)

Evaluate: •Ellen will have saved $2.625 million at age 65 using

the new savings plan. This sum is almost $1 million more than she had without the additional annual increases in savings.

•Because she is increasing her savings amount each year and the interest on the cumulative increases continues to compound, her final savings is much greater.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-104

Example 4.7aRetirement Savings with a Growing AnnuityProblem: • In Example 4.5a, Adam considered saving $10,000 per year

for his retirement. Although $10,000 is the most he can save in the first year, he expects his salary to increase each year so that he will be able to increase his savings by 4% per year. With this plan, if he earns 10% per year on his savings, how much will Adam have saved at age 65?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-105

Example 4.7aRetirement Savings with a Growing Annuity (cont’d)

Solution:Plan: His new savings plan is represented by the following timeline:

This example involves a 20-year growing annuity with a growth rate of 4% and an initial cash flow of $10,000. We can use Eq. 4.8 to solve for the present value of a growing annuity.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-106

Example 4.7aRetirement Savings with a Growing Annuity (cont’d)

Execute: The present value of Adam’s growing annuity is given by:

201 1.04

$10,000 10.10 - 0.04 1.10

$10,000 11.2384

$112,384 today

PV=

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-107

Example 4.7aRetirement Savings with a Growing Annuity (cont’d)

40$112,384 1.10

$5,086,416

FV=

in 40 years

Execute: •Adam’s proposed savings plan is equivalent to

having $112,384 in the bank today. To determine the amount he will have at age 65, we need to move this amount forward 40 years:

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-108

Example 4.7aRetirement Savings with a Growing Annuity (cont’d)

Evaluate: •Adam will have saved $5.086 million at age 65

using the new savings plan. This sum is over $1 million more than he had without the additional annual increases in savings.

•Because he is increasing his savings amount each year and the interest on the cumulative increases continues to compound, his final savings is much greater.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-109

4.5 Solving for Variables Other Than Present Value or Future Value

• In some situations, we use the present and/or future values as inputs, and solve for the variable we are interested in.

• We examine several special cases in this section.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-110

4.5 Solving for Variables Other Than Present Value or Future Value

C P

1

r1

1

(1 r)N

(Eq. 4.8)

Solving for Cash Flows

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-111

Example 4.8Computing a Loan Payment

Problem: • Your firm plans to buy a warehouse for $100,000. • The bank offers you a 30-year loan with equal annual

payments and an interest rate of 8% per year. • The bank requires that your firm pay 20% of the purchase

price as a down payment, so you can borrow only $80,000. • What is the annual loan payment?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-112

Example 4.8Computing a Loan Payment (cont’d)

Solution:Plan:• We start with the timeline (from the bank’s

perspective):

• Using Eq. 4.8, we can solve for the loan payment, C, given N=30, r = 8% (0.08) and P=$80,000

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-113

Example 4.8Computing a Loan Payment (cont’d)

Execute:• Eq. 4.8 gives the payment (cash flow) as follows:

C P

1

r1

1

(1 r)N

80, 000

1

0.081

1

(1.08)30

$7106.19

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-114

Example 4.8Computing a Loan Payment (cont’d)

Execute (cont’d):• Using a financial calculator or Excel:

Given: 30 8.0 -80,000 0

Solve for: 7106.19

Excel Formula: =PMT(RATE,NPER, PV, FV) = PMT(0.08,30,-80000,0)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-115

Example 4.8Computing a Loan Payment (cont’d)

Evaluate:• Your firm will need to pay $7,106.19 each year to repay the

loan. • The bank is willing to accept these payments because the

PV of 30 annual payments of $7,106.19 at 8% interest rate per year is exactly equal to the $80,000 it is giving you today.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-116

Example 4.8aComputing a Loan Payment

Problem: • Suppose you accept your parents’ offer of a 2007 BMW M6

convertible, but that’s not the kind of car you want. • Instead, you sell the car for $61,000, spend $11,000 on a

used Corolla, and use the remaining $50,000 as a down payment for a house.

• The bank offers you a 30-year loan with equal monthly payments and an interest rate of 6% per year, and requires a 20% down payment.

• How much can you borrow, and what will be the payment on the loan?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-117

Example 4.8aComputing a Loan Payment (cont’d)

Solution:Plan:• To calculate the amount we can borrow, we need to find out

what amount $50,000 is 20% of:$50,000 = .2 X Value

Value = $50,000/.2 = $250,000 • Because you’ll be putting $50,000 down, your loan amount

will be $250,000 - $50,000 = $200,000.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-118

Example 4.8aComputing a Loan Payment (cont’d)

Solution:Plan:• We start with the timeline:

• Note, we need to use the monthly interest rate. Since the quoted rate is an APR, we can just divide the annual rate by 12:

r = .06/12 = .005

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-119

Example 4.8aComputing a Loan Payment (cont’d)

Execute:• Eq. 4.8 gives the payment (cash flow) as follows:

= $1,199.10

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-120

Example 4.8aComputing a Loan Payment (cont’d)

Execute (cont’d):• Using a financial calculator or Excel:

Given: 360 0.5 200,000 0

Solve for: -1199.10

Excel Formula: =PMT(RATE,NPER, PV, FV) = PMT(0.005,360,200000,0)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-121

4.5 Solving for Variables Other Than Present Value or Future Value

• Rate of Return – The rate of return is the rate at which the

present value of the benefits exactly offsets the cost.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-122

4.5 Solving for Variables Other Than Present Value or Future Value

• Suppose you have an investment opportunity that requires a $1000 investment today and will pay $2000 in six years.

• What interest rate, r, would you need so that the present value of what you get is exactly equal to the present value of what you give up?

6

20001000

(1 r)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-123

4.5 Solving for Variables Other Than Present Value or Future Value

• Rearranging:

6

1

6

1000 (1 r) 2000

20001 r

1000

1.1225,or

r 12.25%

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-124

4.5 Solving for Variables Other Than Present Value or Future Value

• Suppose your firm needs to purchase a new forklift.

• The dealer gives you two options:– A price for the forklift if you pay cash ($40,000)– The annual payments if you take out a loan

from the dealer (no money down and four annual payments of $15,000).

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-125

4.5 Solving for Variables Other Than Present Value or Future Value

• Setting the present value of the cash flows equal to zero requires that the present value of the payments equals the purchase price:

• The solution for r is the interest rate charged by the dealer, which you can compare to the rate charged by your bank.

4

1 140,000 15,000 1

r (1 r)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-126

4.5 Solving for Variables Other Than Present Value or Future Value

• There is no simple way to solve for the interest rate.

• The only way to solve this equation is to guess at values for r until you find the right one.

• An easier solution is to use a financial calculator or a spreadsheet.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-127

4.5 Solving for Variables Other Than Present Value or Future Value

Given: 4 40,000 -15,000 0

Solve for: 18.45

Excel Formula: =RATE(NPER,PMT,PV,FV)=Rate(4,-25000,40000,0)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-128

Example 4.9 Computing the Rate of Return with a Financial Calculator

Problem: • Let’s return to the lottery example (Example 4.4). • How high of a rate of return do you need to earn investing

on your own in order to prefer the $15 million payout?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-129

Example 4.9 Computing the Rate of Return with a Financial Calculator

Solution:Plan:• We need to solve for the rate of return that makes

the two offers equivalent. • Anything above that rate of return would make

the present value of the annuity lower than the $15 million lump sum payment and

• anything below that rate of return would make it greater than the $15 million.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-130

Example 4.9 Computing the Rate of Return with a Financial Calculator

Execute:

The rate equating the two options is 5.72%.

Given: 29 -14,000,000 1,000,000 0

Solve for: 5.72

Excel Formula: =RATE(NPER, PMT, PV,FV) = RATE(29,1000000,‑14000000,0)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-131

Example 4.9 Computing the Rate of Return with a Financial Calculator

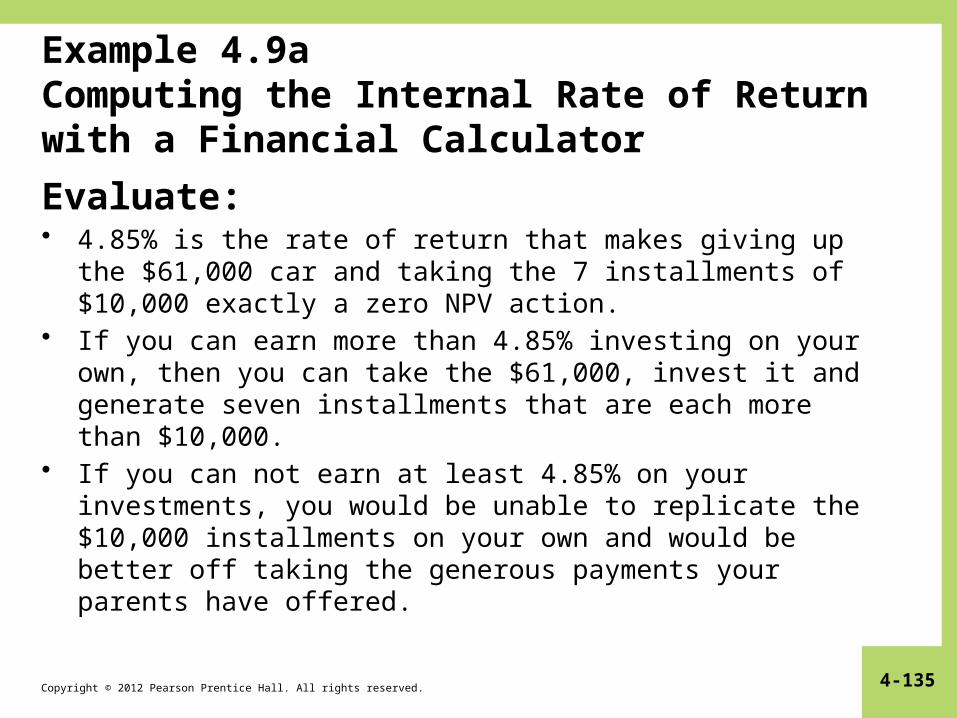

Evaluate:• 5.72% is the rate of return that makes giving up the $15

million payment and taking the 30 installments of $1 million exactly a zero NPV action.

• If you could earn more than 5.72% investing on your own, then you could take the $15 million, invest it and generate thirty installments that are each more than $1 million.

• If you could not earn at least 5.72% on your investments, you would be unable to replicate the $1 million installments on your own and would be better off taking the installment plan.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-132

Example 4.9a Computing the Internal Rate of Return with a Financial Calculator

Problem: • Let’s return to the BMW example (Example 4.4a). • What rate of return would make you indifferent

between the car and the $10,000 per year payout (even if the car is your favorite color and has HD radio)?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-133

Example 4.9a Computing the Internal Rate of Return with a Financial Calculator

Solution:Plan:• We need to solve for the rate of return that makes

the two offers equivalent. • Anything above that rate of return would make

the present value of the annuity lower than the $61,000 car and

• anything below that rate of return would make it greater than the $61,000.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-134

Example 4.9a Computing the Internal Rate of Return with a Financial Calculator

Execute:

The rate equating the two options is 4.85%.

Given: 6 -51,000 10,000 0

Solve for: 4.85%

Excel Formula: =RATE(NPER, PMT, PV,FV) = RATE(6,10000,‑61000,0)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-135

Example 4.9a Computing the Internal Rate of Return with a Financial Calculator

Evaluate:• 4.85% is the rate of return that makes giving up the

$61,000 car and taking the 7 installments of $10,000 exactly a zero NPV action.

• If you can earn more than 4.85% investing on your own, then you can take the $61,000, invest it and generate seven installments that are each more than $10,000.

• If you can not earn at least 4.85% on your investments, you would be unable to replicate the $10,000 installments on your own and would be better off taking the generous payments your parents have offered.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-136

4.6 Solving for Variables Other Than Present Value or Future Value

• Solving for the Number of Periods – In addition to solving for cash flows or the

interest rate, we can solve for the amount of time it will take a sum of money to grow to a known value.

– In this case, the interest rate, present value, and future value are all known.

– We need to compute how long it will take for the present value to grow to the future value.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-137

Example 4.10 Solving for the Number of Periods in a Savings Plan

Problem: • Let’s return to saving for a down payment on a

house. • Imagine that some time has passed and you have

$10,050 saved already, and you can now afford to save $5,000 per year at the end of each year.

• Also, interest rates have increased so that you now earn 7.25% per year on your savings.

• How long will it take you to get to your goal of $60,000?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-138

Example 4.10 Solving for the Number of Periods in a Savings Plan

Solution:Plan:• The timeline for this problem is

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-139

Example 4.10 Solving for the Number of Periods in a Savings Plan

Plan (cont’d):• We need to find N so that the future value of our current

savings plus the future value of our planned additional savings (which is an annuity) equals our desired amount.

• There are two contributors to the future value: the initial lump sum $10,050 that will continue to earn interest, and the annuity contributions of $5,000 per year that will earn interest as they are contributed.

• Thus, we need to find the future value of the lump sum plus the future value of the annuity

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-140

Example 4.10 Solving for the Number of Periods in a Savings Plan

Execute:

Given: 7.25 -10,050 -5,000 60,000

Solve for: 7

Excel Formula: =NPER(RATE,PMT, PV, FV) = NPER(0.0725,‑5000,‑10050,60000)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-141

Example 4.10 Solving for the Number of Periods in a Savings Plan

Evaluate:• It will take seven years to save the down payment.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-142

Example 4.10a Solving for the Number of Periods in a Savings Plan

Problem: • Let’s return to Ellen and Adam. • Suppose Ellen decides she will continue working

until she has as much at retirement as her brother, Adam, will have when he retires.

• She will continue to contribute $10,000 each year to her retirement account.

• How much longer will she need to work to tie the competition with her brother?

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-143

Example 4.10a Solving for the Number of Periods in a Savings Plan

Solution:Plan:• The timeline for this problem is

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-144

Example 4.10a Solving for the Number of Periods in a Savings Plan

Plan (cont’d):• We need to find N so that the FV of the $1,645,000 she’ll

have at age 65 plus the $10,000 she’ll contribute each year is equal to $3,850,000.

• Remember, she’s earning 10% on her investments.

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-145

Example 4.10a Solving for the Number of Periods in a Savings Plan

Execute:

Given: 10 -1645000 -10,000 3850000

Solve for: 8.57

Excel Formula: =NPER(RATE,PMT, PV, FV) = NPER(0.10,‑10000,‑1645000,3850000)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-146

Example 4.10a Solving for the Number of Periods in a Savings Plan

Evaluate:• Ellen will have to work until she’s 73 ½ years old. • (Here’s hoping she really loves her job!)

Copyright © 2012 Pearson Prentice Hall. All rights reserved. 4-147

Chapter Quiz

1. How do you calculate the present value of a cash flow stream?

2. What is the intuition behind the fact that an infinite stream of cash flows has a finite present value?

3. What are some examples of annuities?

4. What is the difference between an annuity and a perpetuity?

5. What is an example of a growing perpetuity?

6. How do you calculate the cash flow of an annuity?

7. How do you calculate the rate of return on an investment?