copyright © 2010 by the american academy of actuaries 1 actuarial board for counseling and...

TRANSCRIPT

Copyright © 2010 by the American Academy of Actuaries

1

Actuarial Board for Counseling and Discipline

PROFESSIONALISM

IABA Annual MeetingAtlanta, Georgia

August 4, 2012

1

Copyright © 2010 by the American Academy of Actuaries

2

Actuarial Board for Counseling and Discipline

Codes of Professional Conduct

Candidates’ Code & Members’ Code

Robert J. Rietz FSA, MAAA, FCA, MSPATetteh Otuteye ACAS, MAAA

2

Copyright © 2010 by the American Academy of Actuaries

3

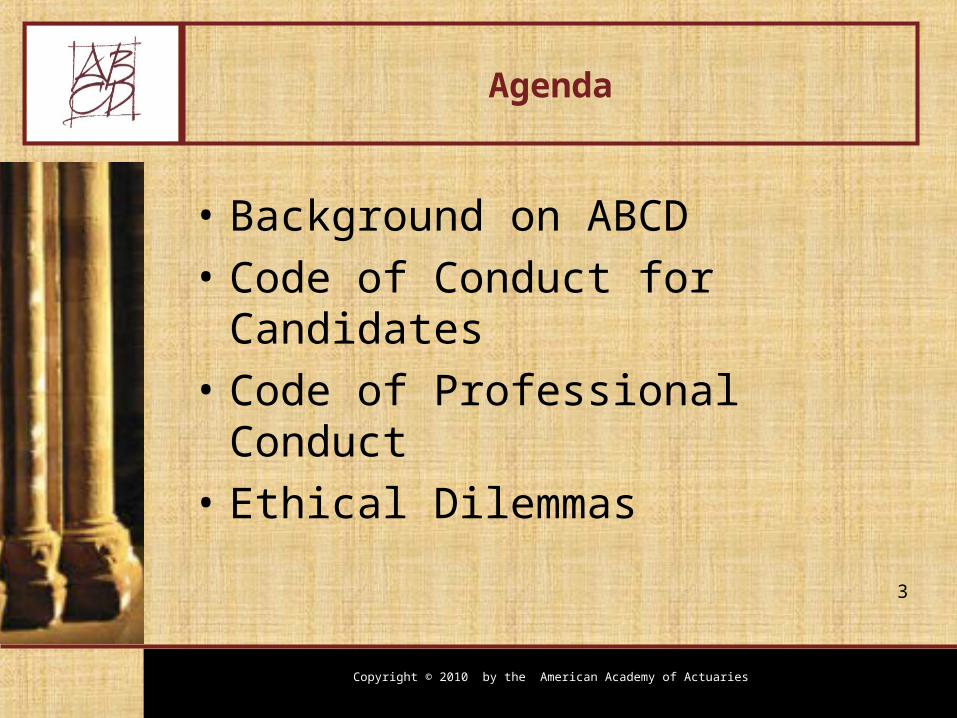

Agenda

• Background on ABCD

• Code of Conduct for Candidates

• Code of Professional Conduct

• Ethical Dilemmas

3

Copyright © 2010 by the American Academy of Actuaries

4

Actuarial Board for Counseling and Discipline

ABCD was established in 1991 by the U.S. actuarial organizations to– Investigate alleged violations of the

Code of Professional Conduct by members and recommend discipline

– Counsel (provide guidance to) members

– Mediate disputes between members and others.

4

Copyright © 2010 by the American Academy of Actuaries

5

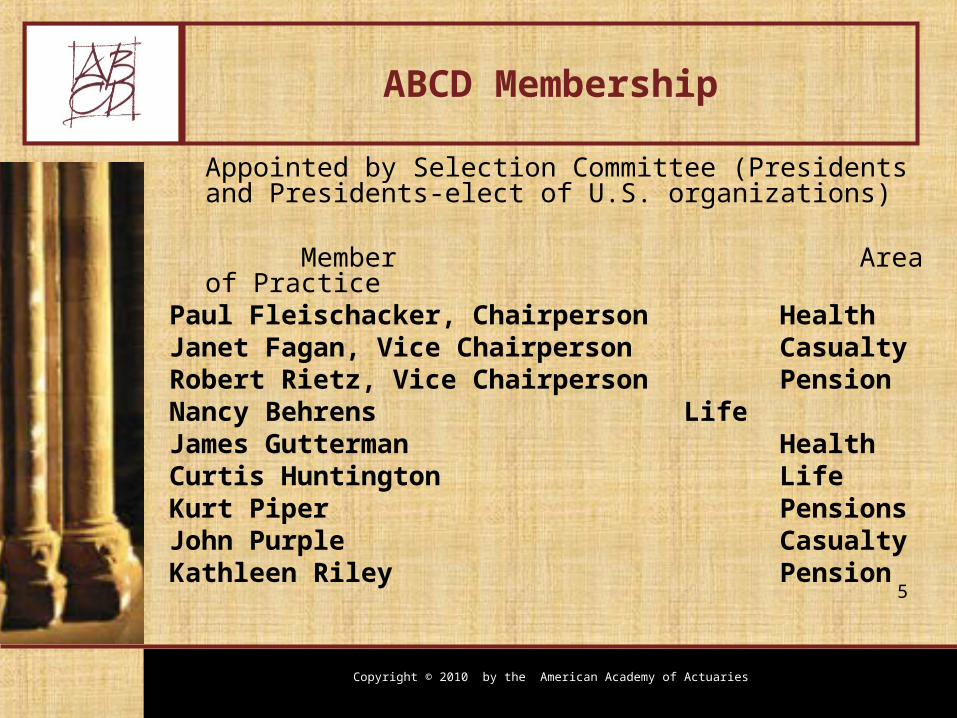

ABCD Membership

Appointed by Selection Committee (Presidents and Presidents-elect of U.S. organizations)

Member Area of PracticePaul Fleischacker, Chairperson HealthJanet Fagan, Vice Chairperson CasualtyRobert Rietz, Vice Chairperson PensionNancy Behrens LifeJames Gutterman HealthCurtis Huntington LifeKurt Piper PensionsJohn Purple CasualtyKathleen Riley Pension

5

Copyright © 2010 by the American Academy of Actuaries

6

ABCD Processes

• Follow Article X of AAA bylaws and ABCD Rules of Procedure

• All ABCD inquiries, guidance and mediation confidential, unless– Actuary makes public or agrees to

publication– Court requires disclosure– Redacted, generic situation used for

educational purposes

6

Copyright © 2010 by the American Academy of Actuaries

7

An ABCD Inquiry

• Is a fact-finding effort, not an adversarial forum

• Examines whether or not an actuary materially violated the Code of Professional Conduct

• Does not administer discipline, but may recommend discipline to the actuary’s membership organizations

7

Copyright © 2010 by the American Academy of Actuaries

8

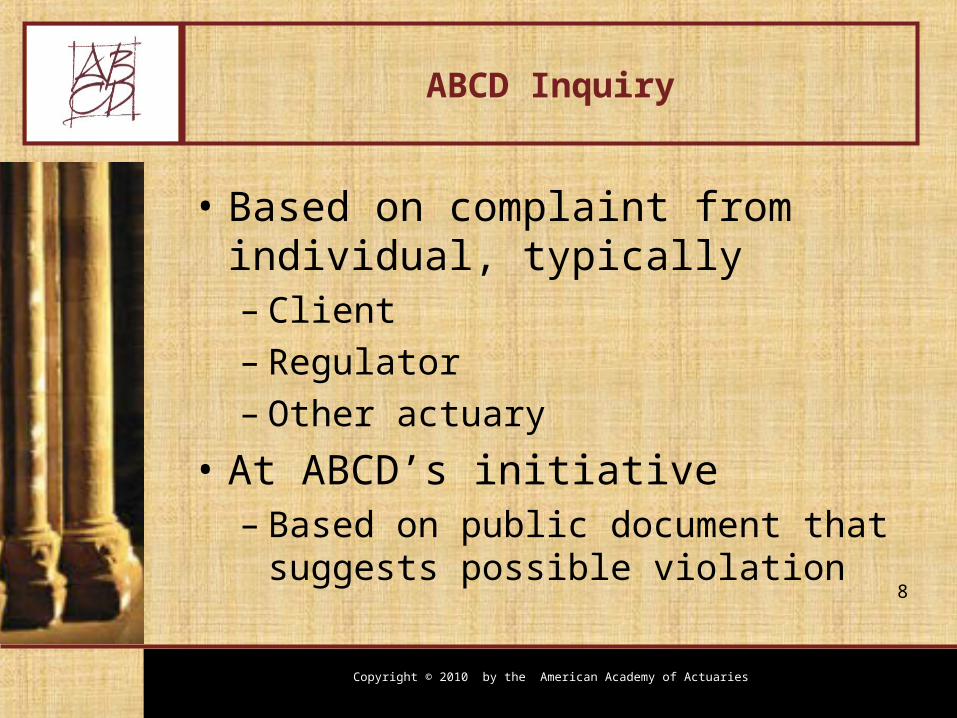

ABCD Inquiry

• Based on complaint from individual, typically– Client– Regulator– Other actuary

• At ABCD’s initiative– Based on public document that

suggests possible violation

8

Copyright © 2010 by the American Academy of Actuaries

9

Request for Guidance

Example RFG Topics• How do I know if I am qualified?• How can I become qualified?• How can I do a job that involves more than one area of

expertise?• How much can I rely on my supervisor?• How much can I rely on my staff?• How much documentation of my work should I save?

What if I leave my company?• When should I refuse an assignment?• When should I make a complaint about another actuary?• When is a violation of the Code material?• When is a violation of the Code resolved?

9

Copyright © 2010 by the American Academy of Actuaries

10

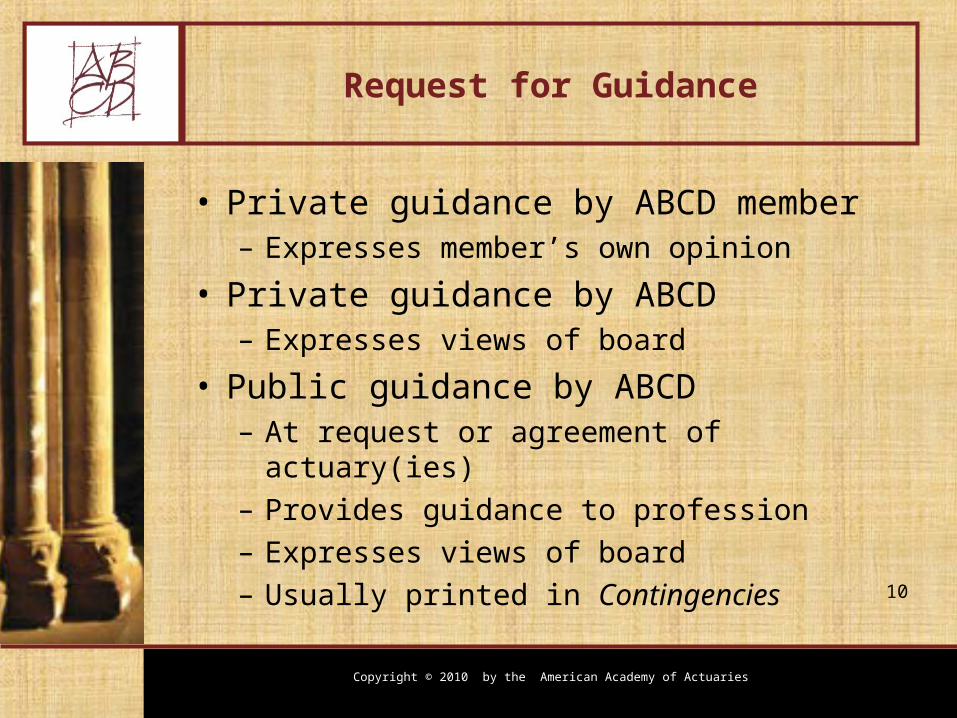

Request for Guidance

• Private guidance by ABCD member– Expresses member’s own opinion

• Private guidance by ABCD– Expresses views of board

• Public guidance by ABCD– At request or agreement of actuary(ies)– Provides guidance to profession– Expresses views of board– Usually printed in Contingencies

10

Copyright © 2010 by the American Academy of Actuaries

11

Mediation

• If all parties agree

• Facilitate resolution of issue without inquiry

11

Copyright © 2010 by the American Academy of Actuaries

12

2011 Caseload

• 55 Requests for Guidance

• 21 Discipline cases– 9 pension– 6 life– 5 casualty– 1 health– Evenly split between conduct and

practice

12

Copyright © 2010 by the American Academy of Actuaries

13

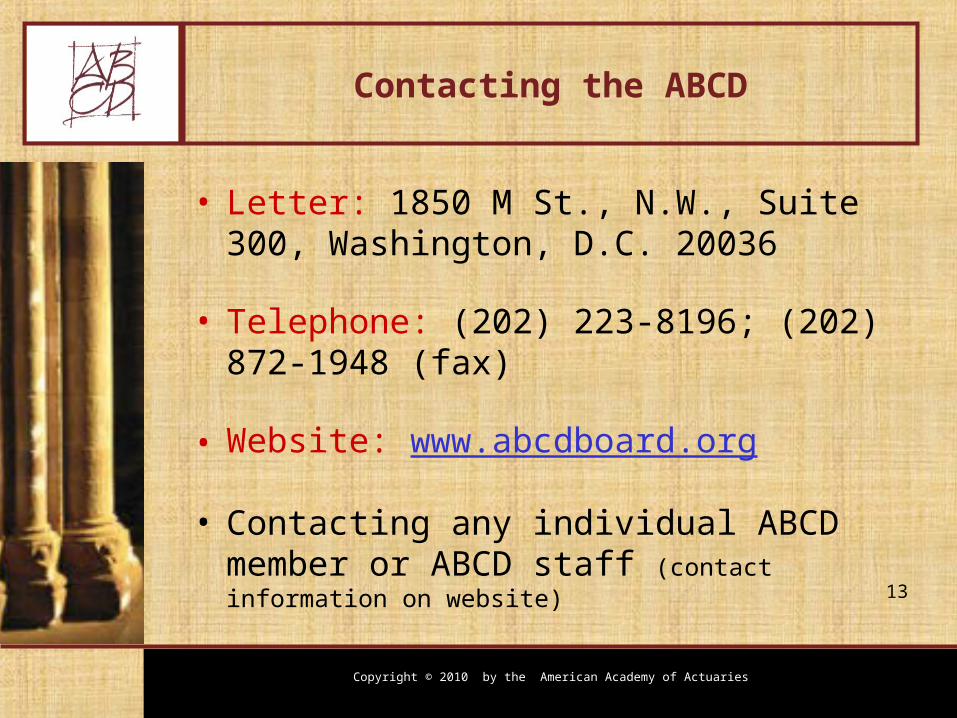

Contacting the ABCD

• Letter: 1850 M St., N.W., Suite 300, Washington, D.C. 20036

• Telephone: (202) 223-8196; (202) 872-1948 (fax)

• Website: www.abcdboard.org

• Contacting any individual ABCD member or ABCD staff (contact information on website)

13

Copyright © 2010 by the American Academy of Actuaries

14

Code of Conduct for Candidates

• Applicable to Actuarial Candidates

Defined as a person who has registered for or completed any SoA (or CAS) educational or evaluative activity, but is NOT a member (ASA, ACAS, CERA).

• Seven Rules

14

Copyright © 2010 by the American Academy of Actuaries

15

Code of Conduct for Candidates

• If performing actuarial work, client or employer is defined as the ‘Principal’

• ‘Actuarial Services’ are professional services provided to a Principal including rendering advice, recommendations, findings based on actuarial considerations.

15

Copyright © 2010 by the American Academy of Actuaries

16

Code of Conduct for Candidates

Effective 1 December 2008

• Rule 1: Act honestly, with integrity and competence, to uphold reputation of the profession.

• Rule 2: Not engage in any conduct involving dishonesty, fraud, deceit or commit any act reflecting adversely on profession.

16

Copyright © 2010 by the American Academy of Actuaries

17

Code of Conduct for Candidates

• Rule 3: Perform Actuarial Services with courtesy and professional respect and cooperate in Principal’s interest.

• Rule 4: Shall strictly comply [CAS: adhere] with [letter and spirit of – SoA only] Rules and Regulations.

17

Copyright © 2010 by the American Academy of Actuaries

18

Code of Conduct for Candidates

• Rule 5: Not authorized to use SoA/CAS membership designations until admitted by SoA/CAS.

• Rule 6: Not disclose any confidential information unless authorized by Principal or required by law, statute or regulation.

18

Copyright © 2010 by the American Academy of Actuaries

19

Code of Conduct for Candidates

• Rule 7: Respond promptly, truthfully and fully to any request for information and cooperate fully with appropriate disciplinary body.

19

Copyright © 2010 by the American Academy of Actuaries

20

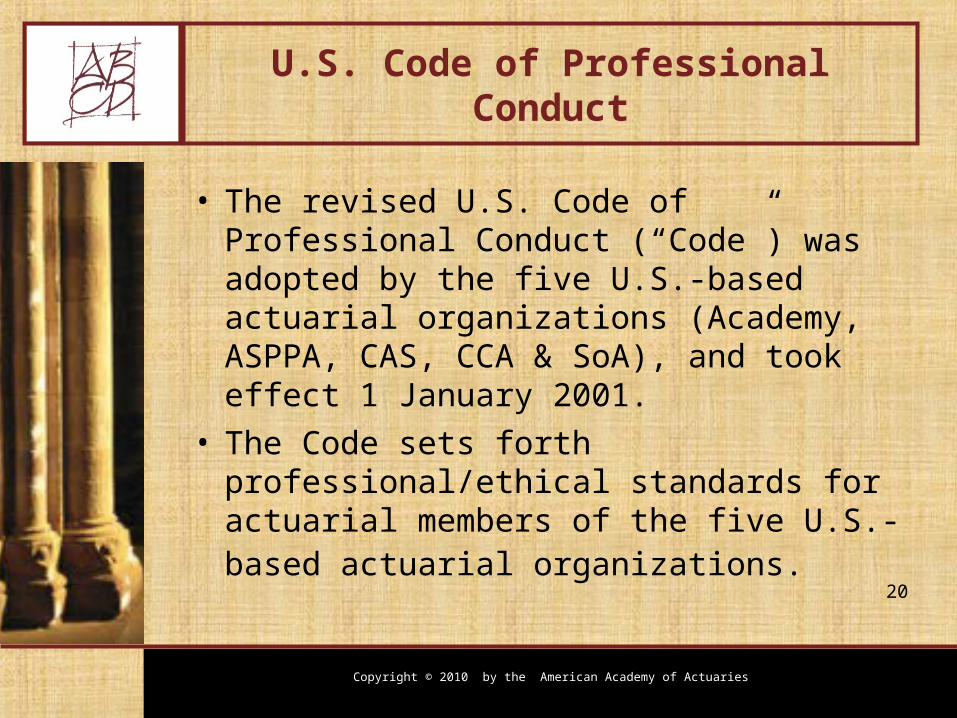

U.S. Code of Professional Conduct

• The revised U.S. Code of Professional Conduct (“Code”) was adopted by the five U.S.-based actuarial organizations (Academy, ASPPA, CAS, CCA & SoA), and took effect 1 January 2001.

• The Code sets forth professional/ethical standards for actuarial members of the five U.S.-based actuarial organizations.

20

Copyright © 2010 by the American Academy of Actuaries

21

U.S. Code of Professional Conduct

• The Code contains 14 Precepts, along with annotations providing further guidance on adhering to the Precepts.

• The Precepts are standards that must be followed by credentialed actuaries who are members of one of the U.S.-based organizations or whose member organizations require their members to follow the U.S. Code.

21

Copyright © 2010 by the American Academy of Actuaries

22

U.S. Code of Professional Conduct

• Precept 1 Professional Integrity:An actuary shall act honestly, with

integrity and competence, and in a manner to fulfill the profession’s responsibility to the public and to uphold the reputation of the actuarial profession

22

Copyright © 2010 by the American Academy of Actuaries

23

U.S. Code of Professional Conduct

• Precept 2 Qualification Standards:

An Actuary shall perform Actuarial Services only when the Actuary is qualified to do so on the basis of basic and continuing education and experience and only when the Actuary satisfies applicable qualification standards.

23

Copyright © 2010 by the American Academy of Actuaries

24

U.S. Code of Professional Conduct

• Precept 3 Standards of Practice

An Actuary shall ensure that Actuarial Services performed by or under the direction of the Actuary satisfy applicable standards of practice.

24

Copyright © 2010 by the American Academy of Actuaries

25

U.S. Code of Professional Conduct

• Precept 4 Communications

An Actuary who issues an Actuarial Communication shall take steps to ensure that is clear and appropriate to the circumstances and audience and satisfies applicable Standards of Practice.

25

Copyright © 2010 by the American Academy of Actuaries

26

U.S. Code of Professional Conduct

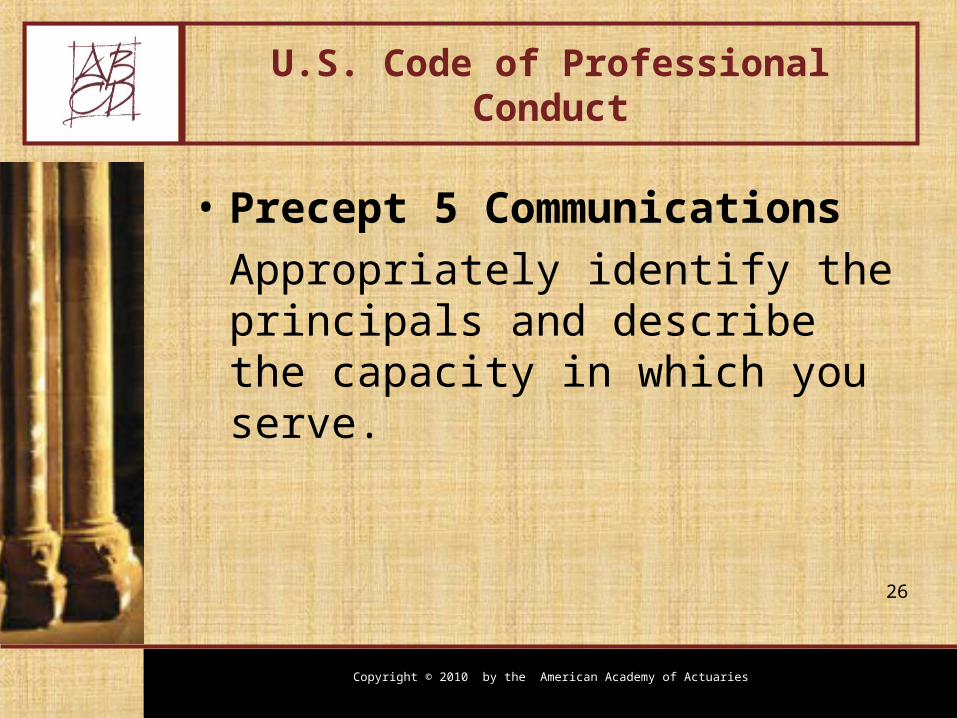

• Precept 5 Communications

Appropriately identify the principals and describe the capacity in which you serve.

26

Copyright © 2010 by the American Academy of Actuaries

27

U.S. Code of Professional Conduct

• Precept 6 Disclosure

Make appropriate and timely disclosure to present or prospective principals of sources of all direct and indirect material compensation you or your firm receives that relates to any assignment for that principal.

27

Copyright © 2010 by the American Academy of Actuaries

28

U.S. Code of Professional Conduct

• Precept 7 Conflict of Interest

Do not perform actuarial services unless:1. your ability to act fairly is unimpaired;

2. you have disclosed conflict to all; AND

3. you secure agreement from all principals.

28

Copyright © 2010 by the American Academy of Actuaries

29

U.S. Code of Professional Conduct

• Precept 8 Control of Work Product

Take reasonable steps to ensure your services are not used to mislead other parties.

29

Copyright © 2010 by the American Academy of Actuaries

30

U.S. Code of Professional Conduct

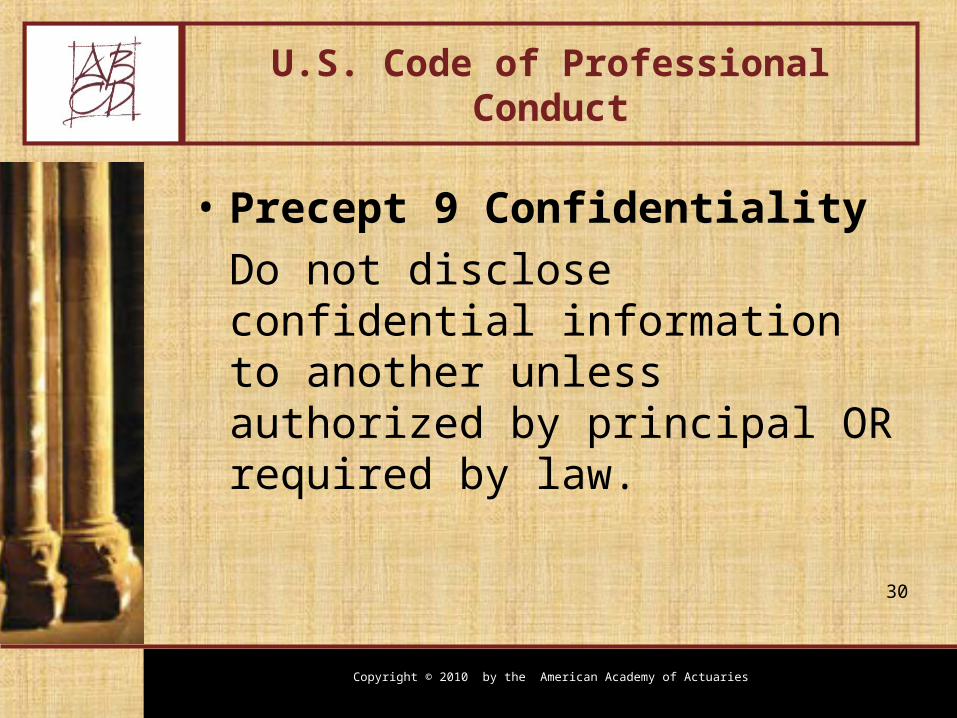

• Precept 9 Confidentiality

Do not disclose confidential information to another unless authorized by principal OR required by law.

30

Copyright © 2010 by the American Academy of Actuaries

31

U.S. Code of Professional Conduct

• Precept 10 Courtesy and Cooperation

Perform actuarial services with courtesy and professional respect and cooperate with others in the principal’s interest.

31

Copyright © 2010 by the American Academy of Actuaries

32

U.S. Code of Professional Conduct

• Precept 11 Advertising

Do not engage in advertising or business solicitation activities that are false or misleading.

32

Copyright © 2010 by the American Academy of Actuaries

33

U.S. Code of Professional Conduct

• Precept 12 Titles and Designations

Use membership titles and designations only in conformity with authorized practices.

33

Copyright © 2010 by the American Academy of Actuaries

34

U.S. Code of Professional Conduct

• Precept 13 Violations of the Code

If you know of an apparent, unresolved, material violation of the Code by another actuary and have attempted to resolve that violation through discussions that have been unsuccessful, you should disclose the violation to the ABCD.

34

Copyright © 2010 by the American Academy of Actuaries

35

U.S. Code of Professional Conduct

• Precept 14 Cooperation with ABCD

Respond promptly, truthfully and fully to requests from the ABCD subject to restrictions on confidentiality and those imposed by law.

35

Copyright © 2010 by the American Academy of Actuaries

36

A Sidenote on Integrity & Ethics

Precept 1 Professional Integrity:

An actuary shall act honestly, with integrity and competence, and in a manner to fulfill the profession’s responsibility to the public and to uphold the reputation of the actuarial profession

Rule 1: Act honestly, with integrity and competence, to uphold reputation of the profession.

36

Copyright © 2010 by the American Academy of Actuaries

37

A Sidenote on Integrity & Ethics

• Ethics is defined as moral principles that guide our behaviour

• Morals is defined as principles of right and wrong behaviour

• Moral behaviour also means to be concerned with, based on, or adhering to the code of behaviour that is considered right or acceptable in a particular society rather than legal rights and duties

• Three dominant moral philosophies

– Principled conscience

– Social conscience

– Rule compliance[Source: Oxford English Dictionary; Ethicability by Roger Steare; Tony Hewitt]

37

Copyright © 2010 by the American Academy of Actuaries

38

A Sidenote on Integrity & Ethics

You are pitching for a new client but your experience is lacking in one area. You are truthful because…

• Honesty is an important principle for me (Principled conscience)• If everyone lied, who could we trust? (Social conscience)• It would be fraud and I could be fired if found out later (Rule

Conscience)• All of the above?

38

Copyright © 2010 by the American Academy of Actuaries

39

A Sidenote on Integrity & Ethics

Integrity is the sum of all those principles that guide the way we live and behave with others:

– Prudence: wisdom, caution, good sense, mindfulness– Justice: fairness, impartiality, rights-and-duties– Fortitude: courage, guts, determination [fear/stubbornness]– Temperance: self-discipline, self-control, patience– Faith: trust, loyalty, commitment [betrayal/naivety]– Hope: cheerfulness, confidence, optimism– Love: honesty, openness, kindness– Excellence: doing our best, quality [mediocrity/perfectionism]– Respect: courtesy, respect, manners

[Source: Ethicability by Roger Steare]

39

Copyright © 2010 by the American Academy of Actuaries

40

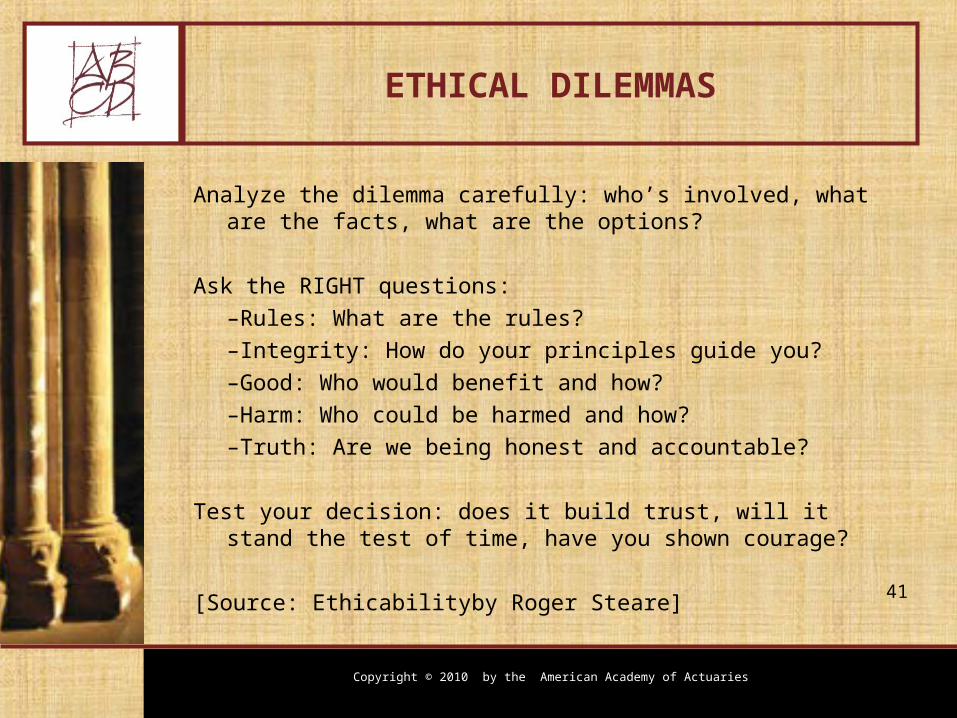

ETHICAL DILEMMAS

Case Studies

40

Copyright © 2010 by the American Academy of Actuaries

41

ETHICAL DILEMMAS

Analyze the dilemma carefully: who’s involved, what are the facts, what are the options?

Ask the RIGHT questions:

–Rules: What are the rules?

–Integrity: How do your principles guide you?

–Good: Who would benefit and how?

–Harm: Who could be harmed and how?

–Truth: Are we being honest and accountable?

Test your decision: does it build trust, will it stand the test of time, have you shown courage?

[Source: Ethicabilityby Roger Steare]

41

Copyright © 2010 by the American Academy of Actuaries

42

Case Study 1

You have prepared a proposal for a major government contract that could be worth $10 million over the next 5 years and, if you win it, would really establish your new firm (which is finding the going pretty tough).

42

Copyright © 2010 by the American Academy of Actuaries

43

Case Study 1

You are now flying to Washington to present to the selection panel, and cannot help noticing that two partners from a (rather sleepy) large professional services firm are sitting in the two seats in front of you. The seat beside you is vacant.

43

Copyright © 2010 by the American Academy of Actuaries

44

Case Study 1

You know who they are, but are pretty sure they don’t know who you are. They are discussing the same project that you are concerned with. They are your key competitor for the business, and if your firm is to survive, you have to win against them, and soon.

44

Copyright © 2010 by the American Academy of Actuaries

45

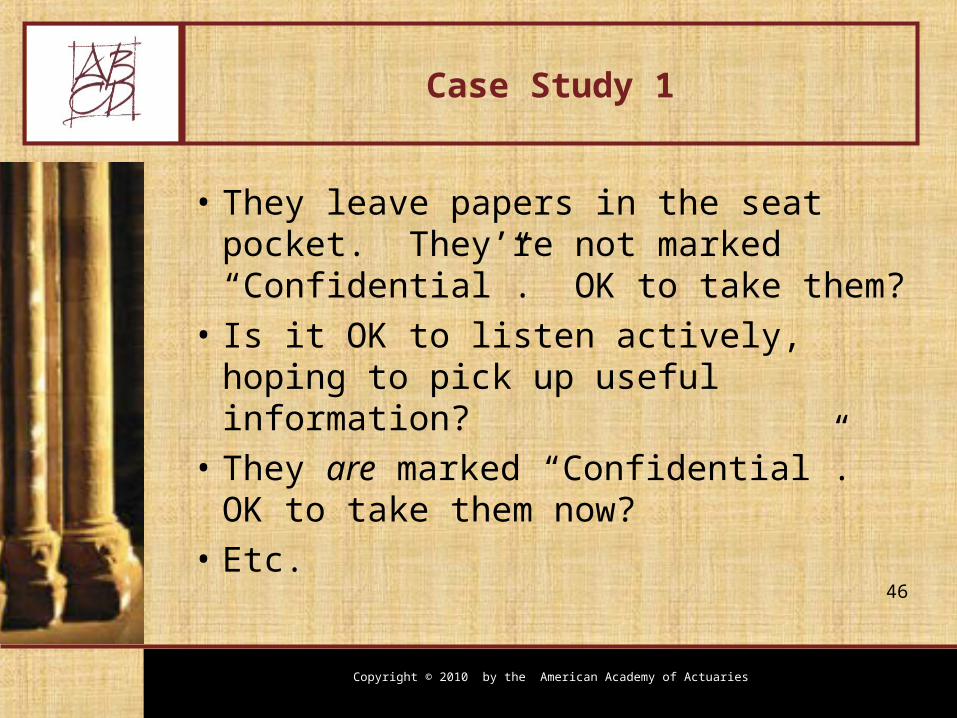

Case Study 1

Try to answer yes or no, and be prepared to give reasons.

• A lot of very useful-sounding numbers are mentioned. Is it OK to take notes?

• It’s too much to write down. OK to turn on your tape recorder?

45

Copyright © 2010 by the American Academy of Actuaries

46

Case Study 1

• They leave papers in the seat pocket. They’re not marked “Confidential”. OK to take them?

• Is it OK to listen actively, hoping to pick up useful information?

• They are marked “Confidential”. OK to take them now?

• Etc.

46

Copyright © 2010 by the American Academy of Actuaries

47

Case Study 2

Charlie Schmidlap is a senior actuary in KantFin(US), the US subsidiary of a global firm called KantFinGroup

• KantFin sells financial reinsurance products to insurance clients

• Schmidlap is shocked to learn – off the record – from an auditor that:

– KantFin’s clients are being investigated for producing misleading financial statements

– The root cause of these misrepresentions appears to be KantFin’s products

47

Copyright © 2010 by the American Academy of Actuaries

48

Case Study 2

What would you do in Schmidlap’s position?

Why? Why not?

1. Nothing – off-the-record and so no need to get involved

2. Nothing – the issue belongs to clients and their auditors

3. Nothing – not an actuarial issue

4. Speak up internally to allow KantFin to address the issue

5. If KantFin fails to act, whistle-blow to the FCAS and the ABCD

6. Other?

48

Copyright © 2010 by the American Academy of Actuaries

49

Case Study 2

• Charlie decides to speak up internally.

• He learns that KantFin’s products involve two legs:

– each leg involves a genuine transfer of insurance risk

– each product is legally highly complex, but careful analysis of both legs shows it is obvious the net risk transfer is immaterial.

49

Copyright © 2010 by the American Academy of Actuaries

50

Case Study 2

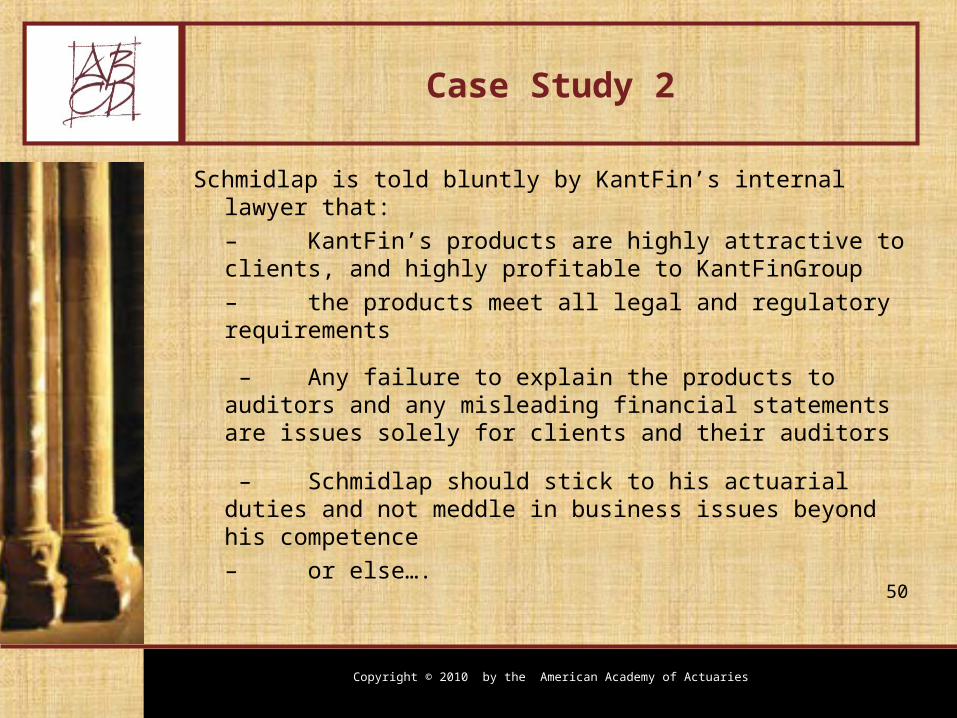

Schmidlap is told bluntly by KantFin’s internal lawyer that:

– KantFin’s products are highly attractive to clients, and highly profitable to KantFinGroup

– the products meet all legal and regulatory requirements

– Any failure to explain the products to auditors and any misleading financial statements are issues solely for clients and their auditors

– Schmidlap should stick to his actuarial duties and not meddle in business issues beyond his competence

– or else….

50

Copyright © 2010 by the American Academy of Actuaries

51

Case Study 2

You are an actuary also employed by KantFin(US).

Charlie consults you. What should you advise him?Why?

1. Do nothing – it is an issue for clients and their auditors

2. Just ensure carefully worded analytics disclaimers are in place

3. Find another job quietly

4. Use the confidential internal whistle-blowing facility to involve KantFin’s Ethics Board

5. Whistle-blow confidentially to the FCAS and the ABCD if action 4 fails

51

Copyright © 2010 by the American Academy of Actuaries

52

Case Study 2

Charlie does nothing?

What should you do? Why? Why Not?1. Nothing – it’s not your problem.

2. Nothing – it is an issue for clients and their auditors

3. Quietly find another job

4. Involve KantFin’s Ethics Board

5. Whistle-blow confidentially to the FCAS and the ABCD if action 4 fails

52

Copyright © 2010 by the American Academy of Actuaries

53

Case Study 3

1) Straight’n’Narrow Actuarial Consultants have been retained by Schmidlap Enterprises to advise on pension plan funding and accounting strategies and prepare their actuarial valuations starting with the 2012 plan year. You are a junior pension actuary working on this team and tasked with matching the prior actuary’s 2011 valuation results, as is customary when a new consulting firm takes over client work. The 2011 valuation has been finalized and the necessary filings submitted by the prior actuary. You find a problem with some of the funding results included in the 2011 valuation report and related schedule. You realize that fixing the error may require your client to amend the filing already made and may result in higher contribution requirements for funding and greater PBGC premiums (Pension Benefit Guarantee Corporation - pension insurance from the government).

What do you do?

53

Copyright © 2010 by the American Academy of Actuaries

54

Case Study 3

2) Now assume you perform additional analysis and realize the error is immaterial and a correction will have negligible impact on funding requirements for 2011 and onwards. Now what?

3) Now, pretend your company was responsible for last year’s reports. The actuary responsible is no longer at your company and correcting the error will have a material impact.

a) Do nothing – the person responsible is gone, the work was peer reviewed – it’s no longer your problem. Pretend you didn’t see it.

b) Notify the client immediately

c) Other?

54

Copyright © 2010 by the American Academy of Actuaries

55

Case Study 3

4) You are friends with the client’s actuary, and she informs you confidentially that management is aware of the numbers, and that they have chosen to maintain those numbers because it resulted in lower contribution requirements for the client. The client is going through some financial difficulty, and revising their numbers and communicating higher contribution requirements would put your company at a significant risk of losing the client.

What do you do?

55

Copyright © 2010 by the American Academy of Actuaries

56

Case Study 3

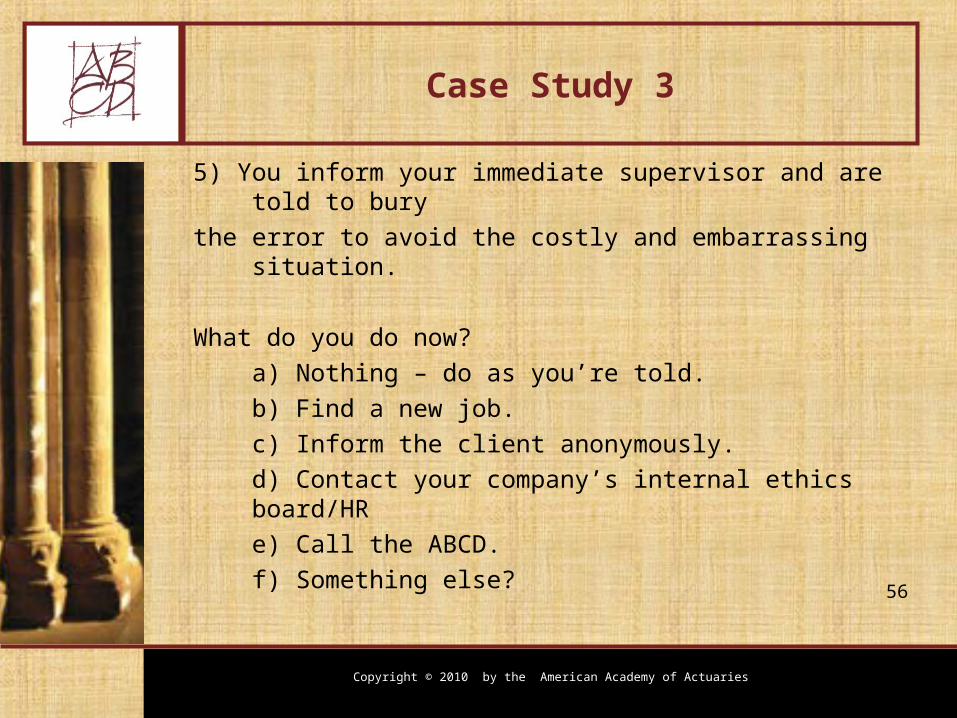

5) You inform your immediate supervisor and are told to bury

the error to avoid the costly and embarrassing situation.

What do you do now?

a) Nothing – do as you’re told.

b) Find a new job.

c) Inform the client anonymously.

d) Contact your company’s internal ethics board/HR

e) Call the ABCD.

f) Something else?

56

Copyright © 2010 by the American Academy of Actuaries

57

Case Study 4

You are a P&C actuary working for CashMoney reinsurance brokers. You meet an underwriter at an insurance conference who happens to work for a client whose business your firm is trying to win. After a few too many mojitos, he whips out his blackberry, and before you can avert your gaze, he shows you the details of the best quote they’ve received from a rival brokerage firm.

You return to work with these numbers floating around your head. What do you do with this information?

a) Keep it to yourself – you shouldn’t know, so pretend you don’t.

b) Try to forget the details and do your own most thorough analysis.

c) Disclose this information to the lead actuary and broker on the team.

d) Other?

57

Copyright © 2010 by the American Academy of Actuaries

58

Case Study 4

Assume you have done your own thorough analysis and determined rates that you believe are unbiased. Your numbers are significantly higher than your competitors’ numbers.

What do you do?

a) Nothing – your best estimate is all that matters.

b) Tweak your trend assumptions and loss development selections downwards to get a more competitive rate: these are highly judgmental and you have some wiggle room.

c) Other?

58

Copyright © 2010 by the American Academy of Actuaries

59

Case Study 4

The account manager (who is not an actuary) asks if you have any insights (perhaps from other analyses or from other actuaries in the company, etc.) as to how competitive your rates will be.

What do you do?

a) Inform him of the existing quote – let him know you doubt you will win the business because the client is price sensitive and your best quote is too high.

b) Tell him you have no idea – that’s his job.

c) Lie.

d) Other?

59

Copyright © 2010 by the American Academy of Actuaries

60

Case Study 4

You opt to tell the account manager about the competitor’s pricing. He wants you to modify your estimates even further than you already have to support a lower rate that he can use to negotiate with the reinsurance market to beat your competitor’s rates.

What do you do?

a) Do what you’re told – getting on his bad side isn’t a good career move.

b) Refuse, and start polishing your resume.

c) Other?

60

Copyright © 2010 by the American Academy of Actuaries

61

Actuarial Board for Counseling and Discipline

QUESTIONS?

61

Copyright © 2010 by the American Academy of Actuaries

62

Actuarial Board for Counseling and Discipline

THANK YOU !

62

Copyright © 2010 by the American Academy of Actuaries

63

Contacting the ABCD

• Letter: 1850 M St., N.W., Suite 300, Washington, D.C. 20036

• Telephone: (202) 223-8196; (202) 872-1948 (fax)

• Website: www.abcdboard.org

• Contacting any individual ABCD member or ABCD staff (contact information on website)

63