copyright 2008 the mcgraw-hill companies 18 extensions of demand and supply analysis

TRANSCRIPT

Copyright 2008 The McGraw-Hill Companies

18Extensions of Demand and Supply Analysis

Copyright 2008 The McGraw-Hill Companies

Chapter Objectives• Price Elasticity of Demand and

How It Can Be Applied• The Usefulness of the Total

Revenue Test for Price Elasticity of Demand

• Price Elasticity of Supply and How It Can Be Applied

• Cross Elasticity of Demand and Income Elasticity of Demand

• Consumer Surplus, Producer Surplus, and Efficiency Losses

Copyright 2008 The McGraw-Hill Companies

What is Elasticity?

• A term economists use to describe sensitivity or responsiveness: for example, how sensitive is quantity demanded to a change in price?

Copyright 2008 The McGraw-Hill Companies

The percentage change in quantity demanded divided by the percentage change in price

How do we measure the Price How do we measure the Price Elasticity of Demand?Elasticity of Demand?

Copyright 2008 The McGraw-Hill Companies

Price Elasticity of Demand• Price-Elasticity Coefficient

and FormulaPercentage Change in Quantity

Demanded of Product X

Percentage Change in Priceof Product X

Ed =

O 18.1

Copyright 2008 The McGraw-Hill Companies

Notes on Ed

• Ed negative, but ignore negative

• use of % change-not affected by units of measurement

Copyright 2008 The McGraw-Hill Companies

Classifying Ed

• Ed = 1 Unitary elasticity

• Ed > 1 Elastic demand

• Ed < 1 Inelastic demand

Copyright 2008 The McGraw-Hill Companies

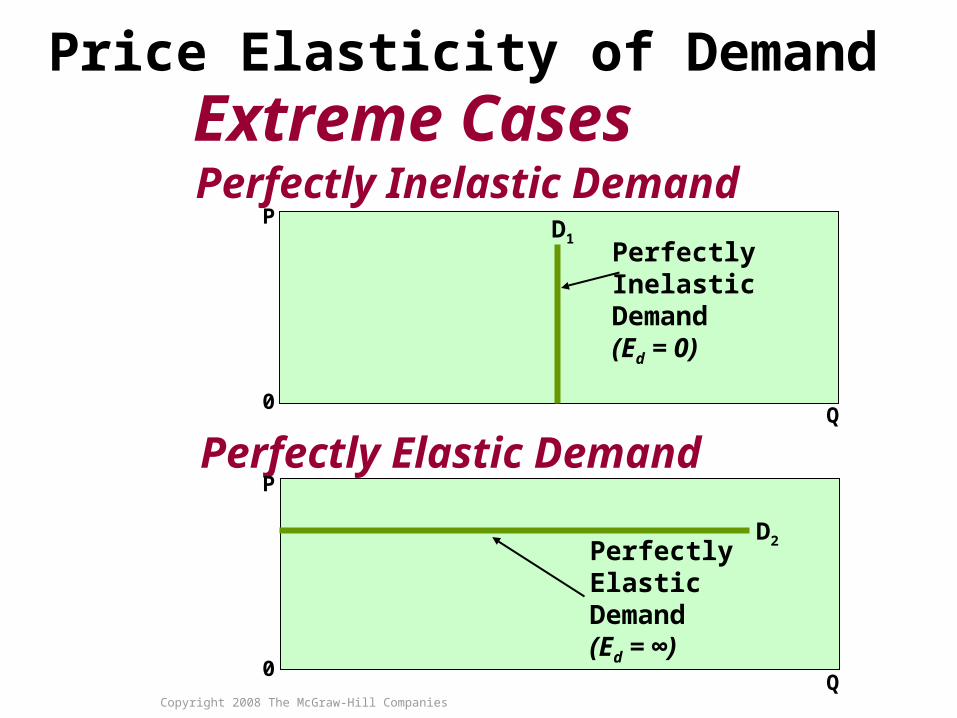

Extreme elasticities

• Ed = 0 Perfectly inelastic (vertical demand curve)

• Ed = Perfectly elastic (horizontal demand curve)

Copyright 2008 The McGraw-Hill Companies

Price Elasticity of DemandExtreme CasesPerfectly Inelastic Demand

Perfectly Elastic Demand0

P

Q

P

0Q

D1

D2

PerfectlyInelasticDemand(Ed = 0)

PerfectlyElasticDemand(Ed = ∞)

Copyright 2008 The McGraw-Hill Companies

Problem - When we move along a demand curve between two points, we get different answers to elasticity depending if we are moving up or down the demand curve

Calculating Elasticities

Copyright 2008 The McGraw-Hill Companies

If there is an If there is an increase increase from from 33 units to units to 55, what is the , what is the percentage increase?percentage increase?

2/3 = 66%

Copyright 2008 The McGraw-Hill Companies

If there is a If there is a decreasedecrease from from 55 units to units to 33, what is the percentage , what is the percentage

decrease?decrease?

2/5 = 40%

Copyright 2008 The McGraw-Hill Companies

One way to deal with this problem is to work with averages ...

Copyright 2008 The McGraw-Hill Companies

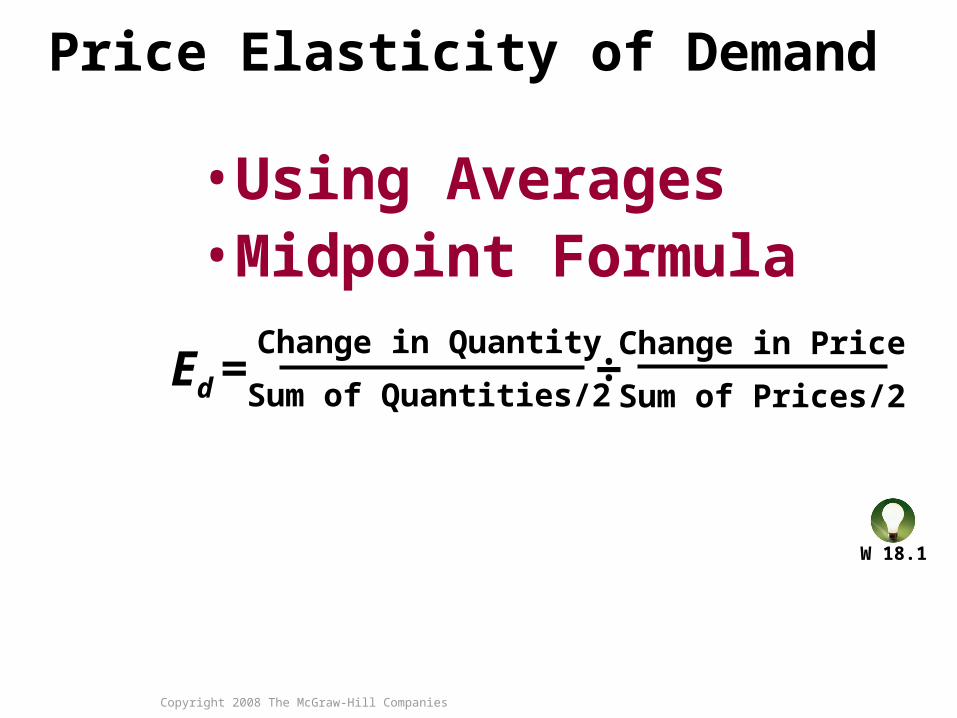

Price Elasticity of Demand

• Using Averages• Midpoint Formula

W 18.1

Change in QuantityEd = Sum of Quantities/2

÷Change in Price

Sum of Prices/2

Copyright 2008 The McGraw-Hill Companies

Practice: calculating Ed

• You usually buy 4 cd’s per month at a price of $14, but when the price rises to $18, you purchase only 3 per month. What is your elasticity of demand for cd’s over this range of prices?

Copyright 2008 The McGraw-Hill Companies

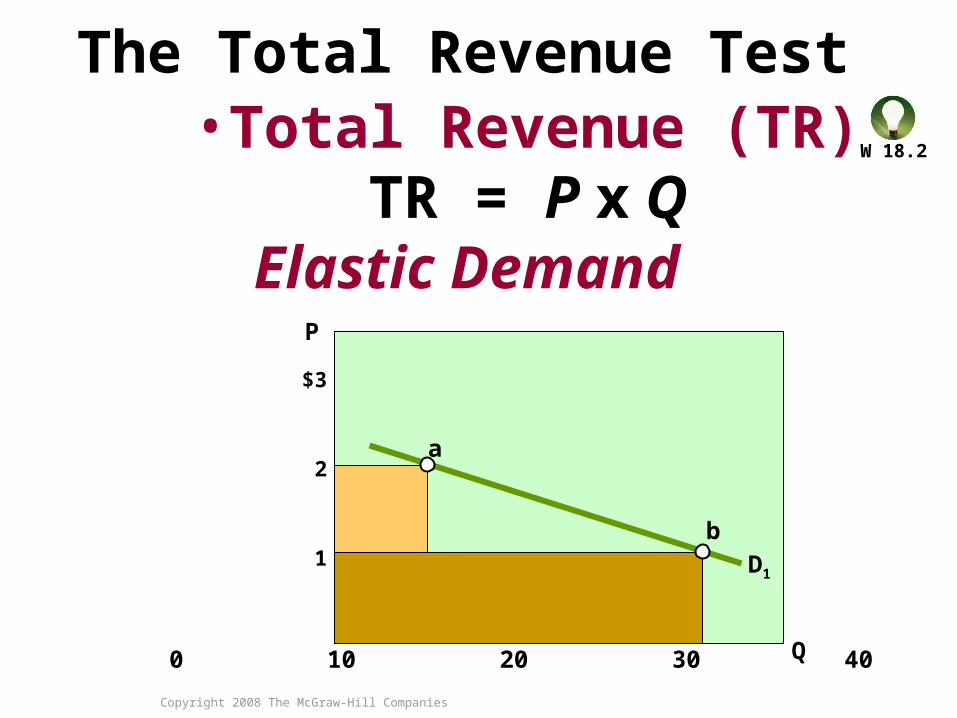

Elasticity and Total Revenue (TR)

• TR = PQ, price times quantity

• Ed = % change in Q

• % change in P

Copyright 2008 The McGraw-Hill Companies

Summary, elasticity, price changes, and total revenue

Ed = 1 Total revenue same

Total revenue same

Ed > 1 Total revenue falls Total revenue rises

Ed < 1 Total revenue rises Total revenue falls

Price increase

Price Decrease

Copyright 2008 The McGraw-Hill Companies

$3

2

1

0 10 20 30 40 Q

P

The Total Revenue Test• Total Revenue (TR) TR = P x Q Elastic Demand

a

b

D1

W 18.2

Copyright 2008 The McGraw-Hill Companies

$4

1

0 10 20 Q

P

The Total Revenue Test• Total Revenue (TR) TR = P x Q Inelastic Demand

c

d

D2

W 18.2

Copyright 2008 The McGraw-Hill Companies

$3

2

1

0 10 20 30 Q

P

The Total Revenue Test• Total Revenue (TR) TR = P x Q Unit-Elastic

e

fD3

W 18.2

Copyright 2008 The McGraw-Hill Companies

Elasticity on a Linear Demand Curve

1

2

3

4

5

6

7

8

8

7

6

5

4

3

2

1

5.00

2.60

1.57

1.00

0.64

0.38

0.20

$8,000

14,000

18,000

20,000

20,000

18,000

14,000

8,000

Elastic

Elastic

Elastic

Unit Elastic

Inelastic

Inelastic

Inelastic

(1)Total Quantity of

Tickets DemandedPer Week, Thousands

(2)Price Per Ticket

(3)Elasticity

Coefficient (Ed)

(4)Total Revenue

(1) X (2)

(5)Total-Revenue

Test

]]]]]]]

]]]]]]]

Price Elasticity of Demand for Movie Tickets as Measured by the ElasticityCoefficient and the Total-Revenue Test

Graphically…

G 18.1

Copyright 2008 The McGraw-Hill Companies

Price Elasticity and the Total-Revenue Curve

0 1 2 3 4 5 6 7 8

0 1 2 3 4 5 6 7 8

Quantity Demanded

Quantity Demanded

Pri

ceT

ota

l Rev

enu

e(T

ho

usa

nd

s o

f D

olla

rs)

$201816141210

8642

$87654321

a

bc

de

fg

h

ElasticEd > 1

Unit ElasticEd = 1

InelasticEd < 1

ElasticEd > 1

Unit ElasticEd = 1

InelasticEd < 1

D

TR

Copyright 2008 The McGraw-Hill Companies

Determinants of Price Elasticity of Demand

• Substitutability• Proportion of Income• Luxuries versus

Necessities• Time

Copyright 2008 The McGraw-Hill Companies

The more substitutes a good has, the more elastic demand for the product is.

What do substitutes have to do with What do substitutes have to do with elasticity?elasticity?

Copyright 2008 The McGraw-Hill Companies

The lower the % of ones budget a good is, the less sensitive consumers are to a price change, thus the more inelastic the demand.

What does % of income a good makes What does % of income a good makes up have with elasticity?up have with elasticity?

Copyright 2008 The McGraw-Hill Companies

In general, luxuries have a more elastic demand, necessities a more inelastic demand.

What do luxuries vs. necessities What do luxuries vs. necessities have to do with elasticity?have to do with elasticity?

Copyright 2008 The McGraw-Hill Companies

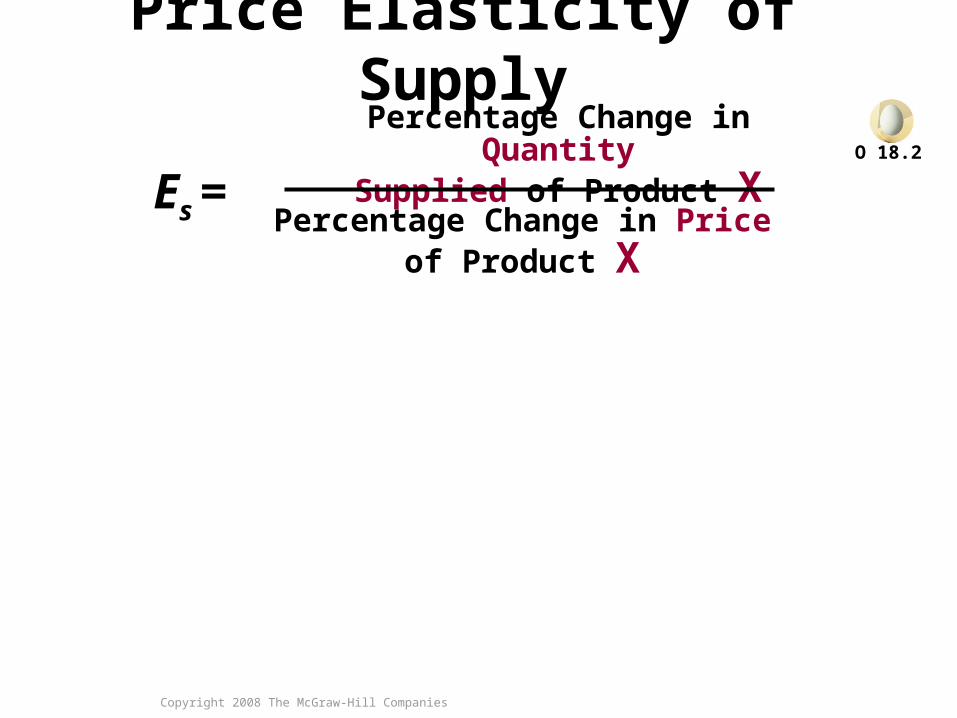

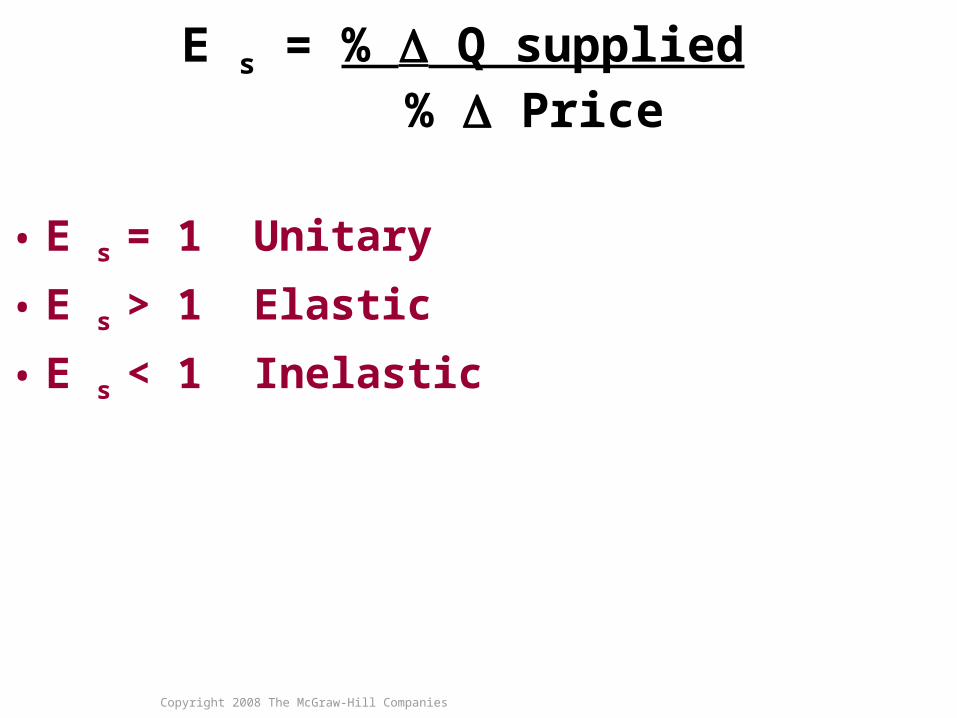

Price Elasticity of Supply

O 18.2

Percentage Change in QuantitySupplied of Product X

Percentage Change in Priceof Product X

Es =

Copyright 2008 The McGraw-Hill Companies

E s = % Q supplied % Price

• E s = 1 Unitary

• E s > 1 Elastic

• E s < 1 Inelastic

Copyright 2008 The McGraw-Hill Companies

Extreme cases of E s

• E s = 0, perfectly inelastic (vertical supply curve

• E s = , perfectly elastic (horizontal supply curve)

Copyright 2008 The McGraw-Hill Companies

Elasticity of Supply

• Time periods important: • Market period: vertical supply curve, too short of

a time to alter amount supplied• Short run: too short to change plant capacity but

can use existing capacity more or less intensively. Supply becomes somewhat more elastic

• Long run: long enough time for firms to change plant sizes, new firms to enter or leave, etc. making for more elastic supply

Copyright 2008 The McGraw-Hill Companies

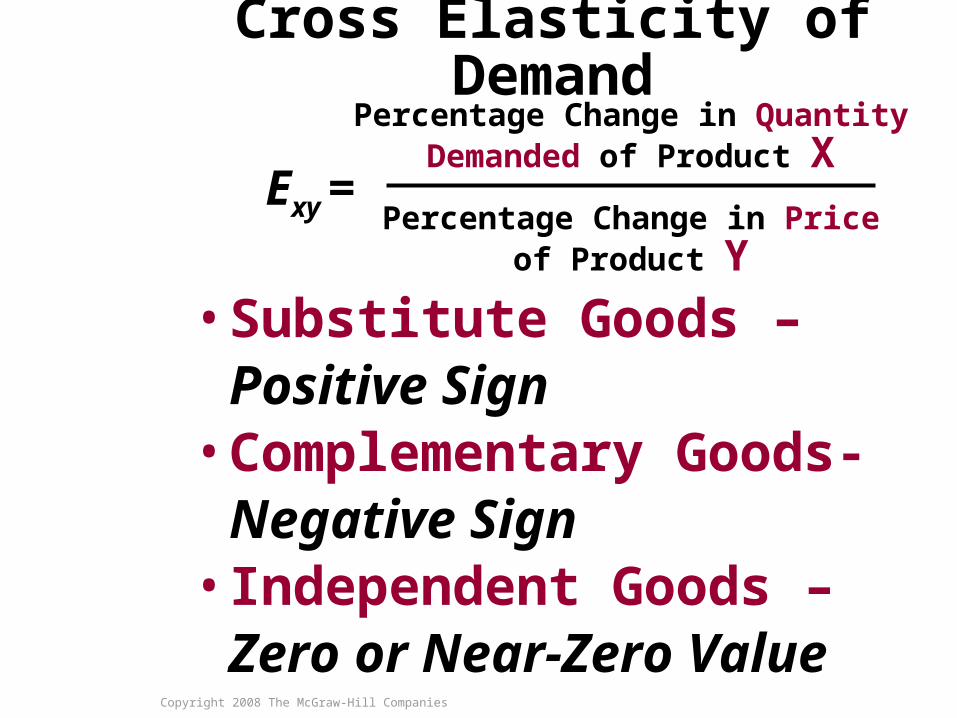

Cross Elasticity of Demand

• Substitute Goods – Positive Sign

• Complementary Goods- Negative Sign

• Independent Goods – Zero or Near-Zero Value

Percentage Change in QuantityDemanded of Product X

Percentage Change in Priceof Product Y

Exy =

Copyright 2008 The McGraw-Hill Companies

Income Elasticity of Demand

• Normal Goods – Positive

Sign

• Inferior Goods- Negative Sign

• Among normal goods, basic

necessities often have low income

elasticities, while luxuries have higher

income elasticities.

Percentage Change in QuantityDemanded

Percentage Change in IncomeEi =

Copyright 2008 The McGraw-Hill Companies

Elasticity of demand

• Applications:–Large Crop Yields–Excise Taxes–Decriminalization of Illegal Drugs

Copyright 2008 The McGraw-Hill Companies

Price Elasticity of Supply• Applications

– Antiques and Reproductions

– Volatile Gold Prices

Copyright 2008 The McGraw-Hill Companies

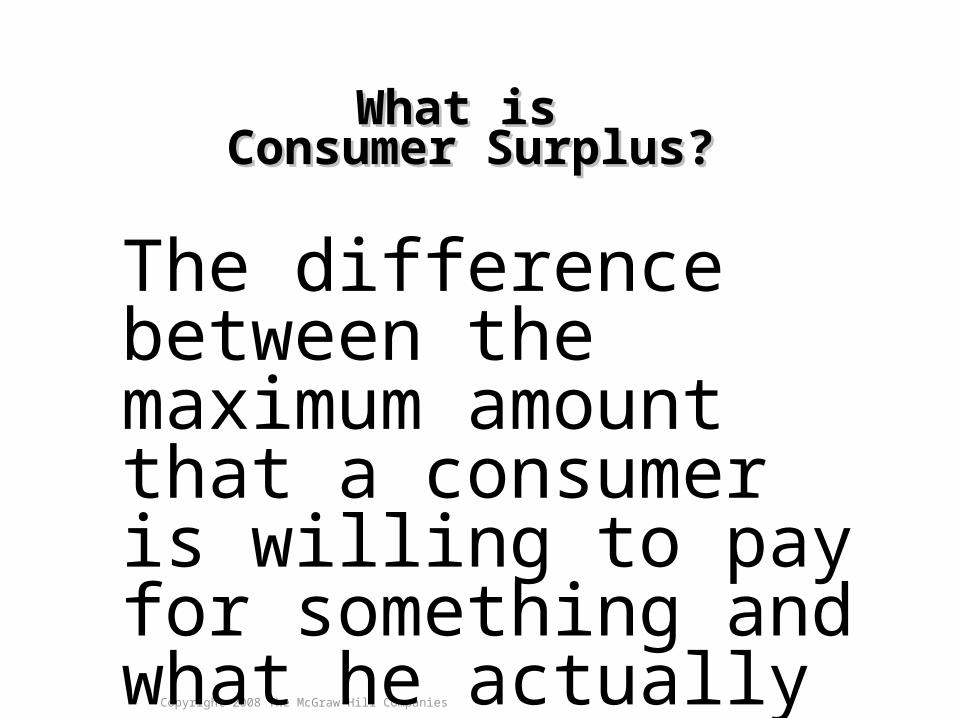

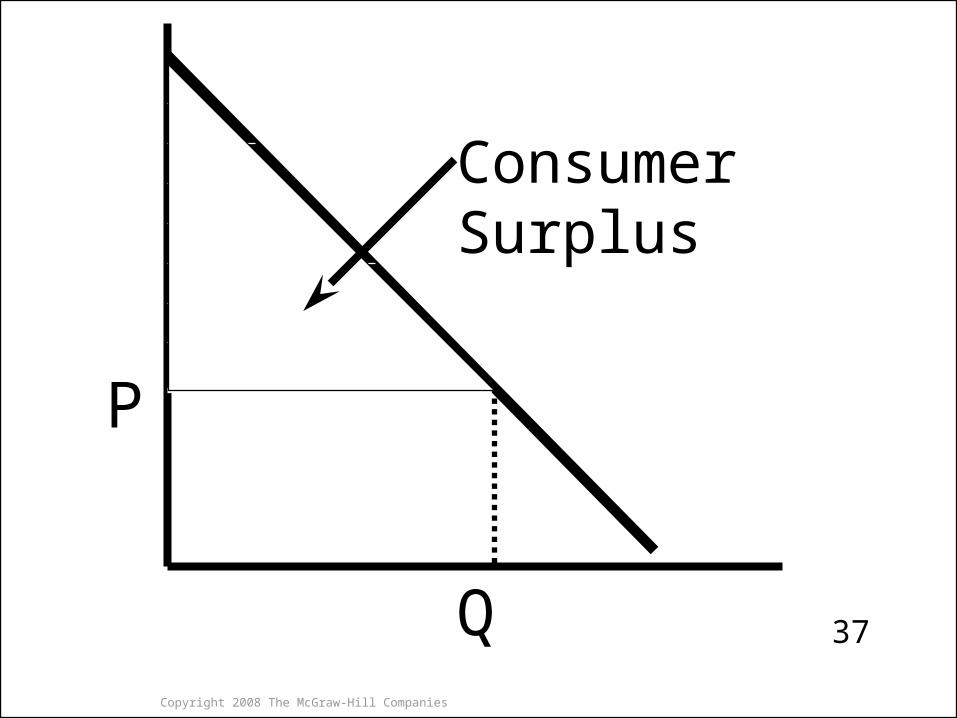

What is What is Consumer Surplus?Consumer Surplus?

The difference between the maximum amount that a consumer is willing to pay for something and what he actually pays

Copyright 2008 The McGraw-Hill Companies

Consumer SurplusConsumer Surplus

• Graphically, we approximate CS as the area under the demand curve but above the market price.

Copyright 2008 The McGraw-Hill Companies

P

Q

Consumer Surplus

37

Copyright 2008 The McGraw-Hill Companies

Consumer and Producer Surplus

Consumer Surplus

D

Pri

ce

(P

er B

ag

)

P1

Q1

Quantity (Bags)

ConsumerSurplus

Equilibrium Price = $8

O 18.3

Copyright 2008 The McGraw-Hill Companies

What happens to Consumer Surplus as Market Price changes?

• It increases when price falls and falls when prices increase

Copyright 2008 The McGraw-Hill Companies

Consumer and Producer Surplus

Producer Surplus

SP

ric

e (

Per

Ba

g)

P1

Q1

Quantity (Bags)

ProducerSurplus

Equilibrium Price = $8

Copyright 2008 The McGraw-Hill Companies

Producer Surplus• Producer surplus is the difference between

the actual price a producer receives and the minimum acceptable price: approximated by the area below the actual price but above the supply curve.

Copyright 2008 The McGraw-Hill Companies

Consumer and Producer Surplus

Efficiency Revisited

D

SP

ric

e (

Per

Ba

g)

P1

Q1

Quantity (Bags)

ConsumerSurplus

ProducerSurplus

Equilibrium Price = $8

W 18.3

Copyright 2008 The McGraw-Hill Companies

Consumer and Producer Surplus

Efficiency Revisited

D

SP

ric

e (

Per

Ba

g)

P1

Q1

Quantity (Bags)

EfficiencyLosses

Q2 Q3

Efficiency Losses (Deadweight Losses)

Copyright 2008 The McGraw-Hill Companies

Elasticity and Pricing Power:Last

Word

Why Different Consumers Pay Different Prices

• All Buyers in a Highly Competitive Market Pay the Same Price Regardless of Their Elasticities

• Difficulty in Applying Different Prices

• Observe Differences in Group Elasticities– Business Travelers– Leisure Travelers– Discounting for Children– Different Net Prices for College

Tuition

Copyright 2008 The McGraw-Hill Companies

Key Terms• price elasticity of demand• midpoint formula• elastic demand• inelastic demand• unit elasticity• perfectly inelastic demand• perfectly elastic demand• total revenue test (TR)• total-revenue test

• price elasticity of supply• market period• short run• long run• cross-elasticity of demand• income elasticity of

demand• consumer surplus• producer surplus• efficiency losses

(deadweight losses)