copyright ® 2005 global insight, inc. global insight’s industry outlook worldwide: winners and...

TRANSCRIPT

Copyright ® 2005 Global Insight, Inc.

Global Insight’s Industry Outlook Worldwide: Winners and Losers

Mark Killion, CFA

Managing DirectorWorld Industry Service

Global Insight

April 2005

2Copyright ® 2005 Global Insight, Inc.

Agenda – Global Outlook for Sector Activity

World Industry Service (WIS) provides sector data and benchmark forecasts for sales, growth, returns and risks

Globally consistent views, harmonized sector indicators Flexible benchmarks for each company’s own sector “peer group”, as well

as all the sectors that represent key markets for each company

Comparative sector performances, industry forecasts Which sectors enjoy the fastest growth? What geographies are driving sector activity?

Global Benchmarks of Production, Trade and Capital Sales Patterns, Profits Growth, Profit Margin Exports, Imports, Fixed Capital Expenditures

3Copyright ® 2005 Global Insight, Inc.

Introduction to the World Industry Service (WIS)

Unique set of global sector fundamental data, financial benchmarks, written reports, sector experts

Harmonized set of industries and indicators allow comparisons and aggregations across sectors and geography

71 industries and sub sectors that together comprise the entire economy; available for each of 70 countries/economies

Sales, Profits, Demand, Exports, Imports, CapEx, Prices

History since 1980 with forecasts 10+ years out

User friendly interface for navigation through choice of sector, country, indicator, time frame; all delivered via Web

Flexible metrics and reports for use in sales forecasting, credit risk management, corporate strategy, research

4Copyright ® 2005 Global Insight, Inc.

Global Sectors Analysts interact with Country Macroeconomic Experts

Sector Forecasts

Autos Energy Chemicals Construction Tourism Health Care Transport Communications Financial

Global Sector Expertise

Glo

bal M

acroeco

no

mic E

xpertise

World Industry Service• All Countries• All Sectors• Harmonized to Common Standard

World Industry Service• All Countries• All Sectors• Harmonized to Common Standard

U.S. MacroEconomics

U.S. MacroEconomics

Asia, Latin America, Rest of World

Macro Economics

Asia, Latin America, Rest of World

Macro Economics

West and EastEurope Macro

Economics

West and EastEurope Macro

Economics

WIS sector forecasts incorporate both the country and industry perspectives

5Copyright ® 2005 Global Insight, Inc.

Common Applications of WIS Available for Review

1) Custom Market Indexes Follow key customer performances, calculate market share, forecast sales for business segments and geographyhttp://www.globalinsight.com/Highlight/HighlightDetail133.htm

2) Sector Risk RatingManage risk exposure by tracking industry level changes in credit and operating risk, stress test portfolios with simulations and alternate “house view” scenarios http://www.globalinsight.com/Highlights/HighlightDetail1103.htm

3) Key Drivers for TechnologyUse Global Sector Activity and Spending as Key Drivers for technology sector forecasts, or research into industry structurehttp://www.globalinsight.com/Highlight/HighlightDetail133.htm

4) Stock Sector NavigatorSector earnings and capital expenditures are used to value financial securities such as stocks, bonds, loans, for investment research and portfolio managementhttp://www.globalinsight.com/Highlight/HighlightDetail1104.htm

Translating Economic Events into Implications for Global Sector Markets

6Copyright ® 2005 Global Insight, Inc.

-4

-2

0

2

4

6

8

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

An

nu

al G

row

th (

%)

Manufacturing Construction Services

Global Sector Growth PerformancesPercent Annual Growth of Real Value Added - World

Strong economic recovery since the down-turn in 2001, but slower relative growth in 2005-07 compared to 2004

Manufacturing sector played key role in both the down-turn and in the subsequent recovery

Service sector growth rates are more resilient in the face of economic volatility

Strong re-bound and steady forecast for construction

Outlook for Global Sector Markets

7Copyright ® 2005 Global Insight, Inc.

-10

-5

0

5

10

15

20

25

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Transport Equip.

Chemicals &RefineriesComputers &Electronics

Manufacturing Leads the Current Expansion(%Growth in Inflation Adjusted Sector Sales for World Total)

-10

-5

0

5

10

15

20

25

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Banking &InsuranceCommunications

Wholsale & Retail

Key Manufacturing Sectors Key Services Sectors

Outlook for Global Sector Markets

8Copyright ® 2005 Global Insight, Inc.

-10

-5

0

5

10

15

20

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Motor Vehicles

Air Craft

Ships & RailEquipment

Transportation Equipment(%Growth in Inflation Adjusted Sector Sales for World Total)

-10

-5

0

5

10

15

20

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

Asia-Pacific

NAFTA

Western Europe

Transportation Equipment Sales Motor Vehicle Sales by Region

Outlook for Global Sector Markets

9Copyright ® 2005 Global Insight, Inc.

Strongest Volume Growth in Computers and Electronics

% in Aggregate Sales

Growth 2005 (%)

1 Office & Computing Machinery 1.16 10.94

2 Communications Equipment incl. Semiconductors 3.24 9.06

3 Computer Support and Software Services 1.86 6.43

4 Motor Cycles & Bicycles 0.11 6.29

5 Electrical Apparatus & Supplies 0.50 5.84

6 Synthetic Resins 0.60 5.69

7 Metal & Woodworking Machinery 0.21 5.01

8 Electrical Industrial Machinery 0.57 5.00

9 Small Electrical Appliances & Housewares 0.26 4.86

10 Drugs & Medicines 0.79 4.74

Top-Ten Real Growth PerformersBy Worldwide Growth Rate in Value Added (Real)

10

Copyright ® 2005 Global Insight, Inc.

Share in Total Sales (%)

Average Growth 2005-07 (%)

1 Drugs and Medicines 0.81 11.17

2 Aircraft and Aerospace 0.45 9.60

3 Educational Services 2.27 9.22

4 Health Services 4.45 8.93

5 Transport & Storage 4.31 8.43

6 Small Electrical Appliances and Housewares 0.21 8.36

7 Financial Institutions 3.75 8.18

8 Communication Equipment incl. Semiconductors 1.33 8.06

9 Computer Support and Software Services 1.96 8.03

10 Electrical Machinery 2.57 7.93

Top-Ten Revenue PerformersBy Growth Rate in Sales (Nominal US$)

Strongest Revenue Gains in Health Care and Services

11

Copyright ® 2005 Global Insight, Inc.

Ranking Sectors by the Outlook for Sales Growth

Share in Total Sales (%)

Average Growth 2005-07 (%)

10 Furniture and Fixtures 0.43 5.45

9 Paper and Products 0.86 4.68

8 Wholesale Trade 5.20 4.05

7 Agriculture, Hunting, Forestry & Fishing 3.21 3.29

6 Industrial Chemicals 1.64 3.09

5 Footwear (Excluding Rubber or Plastic) 0.10 3.06

4 Retail Trade 4.31 2.14

3 Petroleum Refineries 1.65 1.36

2 Primary Metals 1.93 -0.69

1 Mining and Quarrying 1.90 -2.09

Most Modest Performers By Growth Rate in Sales (Nominal US$)

12

Copyright ® 2005 Global Insight, Inc.

Public & Community Svs.

20%

Construction5%

Utilities2%

Manuf.20%

Mining & Quar.2%

Agric.4%

Financials24%

Communication,

Transportation

7%

Trade16%

s

Goods sector accounts for 32% of total world sales, manufacturing accounts for 20%

Financials’ 25% share dominate Services Sector

Community (public) services account for 20%

“Distributive Sectors” of Wholesale, Retail Trade account for 16%

How Big Are Sector Markets in the Global Economy?

Sector Percent Shares of Total World Sales

13

Copyright ® 2005 Global Insight, Inc.

0

20

40

60

80

100S

ervi

ce

Go

od

s

Ag

ric.

Min

ing

Man

uf.

Uti

litie

s

Co

nst

ruc.

Tra

de

Co

m.&

Tra

n.

Fin

an.&

Bu

si.

Pu

blic

Ser

v.

OECD Share in World Total (Avg. 2000 - '05)OECD Share of Growth (from 2000 to '05)

OECD Countries’ Shares in Sector and Sector GrowthBased on Value Added in ’97 US$

Aggregate By ISIC One-Digit Sectors

14

Copyright ® 2005 Global Insight, Inc.

0

20

40

60

80

100S

ervi

ce

Goo

ds

Agr

ic.

Min

ing

Man

uf.

Util

ities

Con

stru

c.

Trad

e

Com

.&Tr

an.

Fina

n.&

Bus

i.

Pub

lic S

erv.

Sector Share (Avg. 2000 - '05)Share of Growth (from 2000 to '05)

Rest of the World (Non OECD) Shares in Sector and Sector GrowthBased on Value Added in ’97 US$

Aggregate By ISIC One-Digit Sectors

15

Copyright ® 2005 Global Insight, Inc.

Regional Shares of Global Manufacturing Sector Sales

($2.9 Trillion Year 2005)

India2%

U.S.20%

O ther17%

China13%

Korea3%

Taiwan2%

Japan13%

W. Europe30%

Role of Chinese Manufacturing in the World Economy

0

5

10

15

20

25

30

35

40

45

Share in Global Manufaturing Sector Sales

Regional Share of Global Growth in Manufacturing from 2000 to 2005

Regional Shares of Growth in Global Manufacturing Sector Sales

Source: GII World Industry ServiceSource: GII World Industry Service

16

Copyright ® 2005 Global Insight, Inc.

China Manufacturing Sector Sales

($2.9 Trillion Year 2005)

Basic Metals

12%

Machinery &

Equipment

37%

Food & Tobacco

10%

Textiles10%

Wood, Paper & Printing

4%

Chemicals

23%

Minerals4%

Role of Manufacturing Sector in the Chinese Economy

0

10

20

30

40

50

60

70

Manufacturing Value Added as Share of GDP, 2003

Manufacturing's Share of Total GDP Growth -- 2000 to 2005

Regional Shares of Manufacturing VA in GDP and Growth in GDP

Source: GII World Industry ServiceSource: GII World Industry Service

17

Copyright ® 2005 Global Insight, Inc.

0

50

100

150

200

250

300

China

India

Korea

Germ

any

France

U.S.

Bil

. U

S$

- Δ

fro

m 2

000

0

5

10

15

20

25

% A

nn

ual

Ch

ang

e si

nce

200

0

Increase during 2000 to 2004, $ Bil.(left)% annual growth (right)

Growth in Goods Imports in Selected Countries Change in Imports Since 2000

China recorded the largest growth in Goods imports for any country during 2000 to 2004

Growth in imports of US$ 245 Bill. Amounts to 23.6% annual average growth

Although increase in India’s imports were smaller in value, it was also very strong at 16% percent annual growth

18

Copyright ® 2005 Global Insight, Inc.

What is Role of Chinese Exports in World Trade?

Greater China Manufacturing Exports Percent Share of Total World Manufacturing Exports

0

2

4

6

8

10

12

14

1980 1990 1995 2000 2005

China* Hong Kong* Taiwan* Intra-Regional

* Export totals from China, Hong Kong and Taiwan exclude trade with each other. These are included in Intra-Regional.

Source: World Industry ServiceSource: World Industry Service

19

Copyright ® 2005 Global Insight, Inc.

What is Role of EU 15 Exports in World Trade?

EU 15 Manufacturing Exports Percent Share of Total World Manufacturing Exports

0

10

20

30

40

50

60

1980 1990 1995 2000 2005

EU 15 Rest of World* Intra-Regional

* Export totals from EU 15 Rest of World exclude trade with each other. These are included in Intra-Regional.

Source: World Industry ServiceSource: World Industry Service

20

Copyright ® 2005 Global Insight, Inc.

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

Ch

an

ge

in S

ha

re

Taiwan South Korea China

1980-1989 1990-1999 2000-2009

Change in World Manufacturing Export Shares (Delta on the Shares: Share at End of Period less Share at Start of Period)

What is the Chinese Competitive Threat?

2005--2009: +2.0%

2000--2004: +2.9%

Source: World Industry ServiceSource: World Industry Service

21

Copyright ® 2005 Global Insight, Inc.

Cross Border Trade Still Growing in Importance for Sector Production

0

2

4

6

8

10

12

1990 1995 2000 2005 2010

Tri

l. U

S$

0

5

10

15

20

25

30

35

Shar

e in

%

Global Exports of All Goods (Tril. US$)

Exports as Share of Production (All Goods)

Manufacturing accounts for the largest share of merchandise exports

Of the $ 8.34 Trill. anticipated trade value, $7.54 Trill. Will be from the manufacturing sector

Agriculture and Mining provide $230 and $575 Bill. respectively

Rising trade intensity: While volume of Global exports continued to grow, share of exports in global production also continued to expand

22

Copyright ® 2005 Global Insight, Inc.

0

20

40

60

80

100

120

1995 2000 2005

China North Asia

Did the trade intensity increase over the past decade in China? Trade Intensity = (Export+Import)/Production

North Asia: High Technology Sector Trade Intensity in High-Tech in China

Source: World Industry ServiceSource: World Industry Service

23

Copyright ® 2005 Global Insight, Inc.

0

20

40

60

80

100

1995 2000 2005

India SAARC

Did the trade intensity increase over the past decade in India? Trade Intensity = (Export+Import)/Production

Source: World Industry ServiceSource: World Industry Service

SAARC: High Technology Sector Trade Intensity in High-Tech in India

24

Copyright ® 2005 Global Insight, Inc.

0

20

40

60

80

100

120

140

1995 2000 2005

Brazil Latin and Central America

Did the trade intensity increase over the past decade in Brazil? Trade Intensity = (Export+Import)/Production

Latin America: High Technology Sector Trade Intensity in High-Tech in Brazil

Source: World Industry ServiceSource: World Industry Service

25

Copyright ® 2005 Global Insight, Inc.

Comparing China’s Trade Shares with Other Countries

Source: World Industry ServiceSource: World Industry Service

0

10

20

30

40

50

60

Share of Export in Production (Sales)

Share of Imports in Consumption

Trade Shares of Metals & Construction Materials(World Production US$ 1.5 Trill. in 2005)

05

10

1520253035

404550

Share of Export in Production (Sales)

Share of Imports in Consumption

Trade Shares of Industrial Chemicals(World Production US$ 1.3 Trill. in 2005)

26

Copyright ® 2005 Global Insight, Inc.

Comparing China’s Trade Shares with Other Countries

Source: World Industry ServiceSource: World Industry Service

01020

3040506070

8090

100

Share of Export in Production (Sales)

Share of Imports in Consumption

Trade Shares of Communication Equip.(World Production US$ 1.04 Trill. in 2005)

0

10

20

30

40

50

60

Share of Export in Production (Sales)

Share of Imports in Consumption

Trade Shares of Motor Vehicles(World Production US$ 2.1 Trill. in 2005)

27

Copyright ® 2005 Global Insight, Inc.

What Is the Role of Capital Expenditures in Sector Activity?

0

2

4

6

8

1 0

1 2

1 4

1 6

TO

TA

L

No

n F

inan

cial

Fin

anci

als

En

erg

y

Mat

eria

ls

Ind

ust

rial

s

Co

ns.

Dis

cr.

Co

ns.

Sta

ple

s

Hea

lth

Car

e

Tec

hn

olo

gy

Tel

eco

ms

Uti

liti

es

U S W e s t E u r o p e

0

0 . 5

1

1 . 5

2

2 . 5

3

3 . 5

4

4 . 5

5

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2

3

4

5

6

7

8

9

F in a n c ia l ( L H S ) N o n F in a n c ia l ( R H S )

CapEx Spending as % of Total SalesUnited States Vs Europe, (2003)

US CapEx Spending as % of Total SalesTotal for 446 US Corporations in the GICS

Sector Classification

Source: Worldscope Company Financial Statements & WIS CalculationsSource: Worldscope Company Financial Statements & WIS Calculations

28

Copyright ® 2005 Global Insight, Inc.

Ratio of Fixed CapEx to Sales(CapEx / Total Sales)

0

5

10

15

20

25

30

35

40

U.S. EU-15 Brazil India China

1995 2000 2005

0

2

4

6

8

10

12

U.S. EU-15 Brazil India China

1995 2000 2005

Service Sector (ISIC 6-9) Goods Sector (ISIC 1-3)

29

Copyright ® 2005 Global Insight, Inc.

What is the Return on Fixed CapEx Spending? (ROFIC)

0

2 0

4 0

6 0

8 0

1 0 0

1 2 0

1 4 0

1 6 0

1 8 0

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

0

5

1 0

1 5

2 0

2 5

3 0

3 5

4 0

4 5

F i n a n c i a l N o n F i n a n c i a l

US Corporate Sector: Return from Investment in Fixed Capital

Company Net Income / 3-year sum of Fixed Investments

5

10

15

2 0

2 5

3 0

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

∆ G D P / P r i v a t e F i x e d C a p E x

∆ G D P / C a p E x - - E q u i p m e n t & S o f t w a r e

US Macro Economy: Marginal Efficiency of Private Fixed Investment

∆ in GDP / 3-year sum of Fixed Investments

Source: US BEA, Worldscope Company Financial Statements & Source: US BEA, Worldscope Company Financial Statements & WIS CalculationsWIS Calculations

30

Copyright ® 2005 Global Insight, Inc.

Marginal Efficiency of Investment(∆ in GDP / Three-year sum of CapEx)

-5

0

5

10

15

20

25

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06

OECD LDC's

OECD and LDC’s U.S. and China

0

5

10

15

20

25

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06

US China

31

Copyright ® 2005 Global Insight, Inc.

Sector Return on Fixed Capital Spending(Operating Profits / Three-year sum of CapEx)

0

20

40

60

80

100

120

140

U.S

.

EU

-15

Bra

zil

Ind

ia

Ch

ina

1995 2000 2005

0

10

20

30

40

50

60

All

Goo

ds

Serv

ices

Fina

ncia

ls

Med

. Tch

1995 2000 2005

Aggregate ISIC: 1 to 9 China, by Sector

32

Copyright ® 2005 Global Insight, Inc.

Please Contact Us for a Personal Demonstration!

More Information?

Mark Killion, CFAManaging Director, World Industry [email protected]

Prem PremakumarApplications Manager, World Industry [email protected]

Copyright ® 2005 Global Insight, Inc.

Custom Market IndexesA Framework to Track and Forecast Company Sales

Prospects for Multiple Business Segments and Geographies

World Industry Service

34

Copyright ® 2005 Global Insight, Inc.

Global Insight’s World Industry Service (WIS) Provides Sector Benchmarks for Global Sales Forecasting

WIS provides a unique set of global sector data, financial benchmarks, and written reports, all delivered via Global Insight’s easy-to-use Web-based platform

Harmonized industries and indicators allow for consistency and comparisons across sectors and geography

User-friendly access facilitates navigation through a multi-dimensional choice of sector, country, indicator, and timeframe

The application of WIS featured here is the Custom Market Index (CMI) framework, which uses WIS sector data to aid in company sales forecasting and market planning

An ideal tool to forecast sales in several business segments and multiple countries/regions around the world

35

Copyright ® 2005 Global Insight, Inc.

WIS Sectors Are the “Gear Box” that Connects

Macro and Companies!

WIS sector data represents a big “peer group” of all players that operate in each sector Data derived from company tax filings Includes public and private ownership Creates robust financial benchmarks Uses sector benchmarks to anticipate

likely company prospects

WIS Platform Drives Macro Performances through Sector Activity to Individual Company Performances

Macro

Policies Slate of

Demand Scenarios Prices and

Exchange Rates

Industry

Sources of Demand Purchases, COGS Consumer, B2B Markets Technology, Commercial

Linkages Trade, Competition, and

Profits

Company

Benchmark Global Sales Growth, Cost Structure, Risks

Market Share Competitive

Technology

36

Copyright ® 2005 Global Insight, Inc.

WIS provides comparative and consistent benchmarks of market size, growth, volatility, correlation, and structure

Use the WIS indicators and reports to understand demand conditions and structural changes in key customer markets

The Custom Market Index (CMI) framework facilitates the tracking, analysis, and forecasting of company sales prospects for multiple business segments and regions

Use WIS sector information as the basis for custom framework

Use company sales patterns to “weight” or tie sectors together into tailored market bundles

Produce a finely targeted and informed view of sales prospects

How to Use WIS Information in Sales Forecasting

Translate economic events into implications for key markets

37

Copyright ® 2005 Global Insight, Inc.

What is the Market Size of Key Global Sectors?—Examples of WIS Benchmark Indicators

WIS indicators show the size and composition of sector markets

Comparable measures are scalable to region and world totals

Ability to scan across sector groups and regions, then drill down to more granular market segments

Metrics allow custom definition of segments and geography

WIS Indicators Provide Robust Benchmarks of Sector Peer Groups

(Example of total world sales for the nine top sectors)Utility2%

Construction6%

Trade13%

Transport, Storage,

Communication Services

7%

Agriculture3%

Finance21%

Social Service17%

Mining2%

Manufacturing29%

38

Copyright ® 2005 Global Insight, Inc.

Drill Down from Top-Level Sectors to Sub-Industries, andShow Market Size Across Countries and Business Segments

13%

8%4%

75%

Ships & RailroadsMotor VehiclesAircraftOther

What is the Market Size of Key Global Sectors?—Examples of WIS Benchmark Indicators

25%

8%

21%8%

14%

19%

4%

U.S.

Canada & MexicoJapan

Other Asia

Germany

Other EuropeOther Emerging Markets

39

Copyright ® 2005 Global Insight, Inc.

Percent Growth in Inflation-Adjusted Sector Sales(World total from 70 economies)

-4

-2

0

2

4

6

8

10

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

All Sectors Manufacturing Sector Services Sectors

Sector Growth Rates are a key metric for sales forecasting

Identify and target the fastest-growing sectors, then determine the best geography for sales and production

CMI: Use custom definition of segments and geography to best represent and track a company’s own set of target market segments

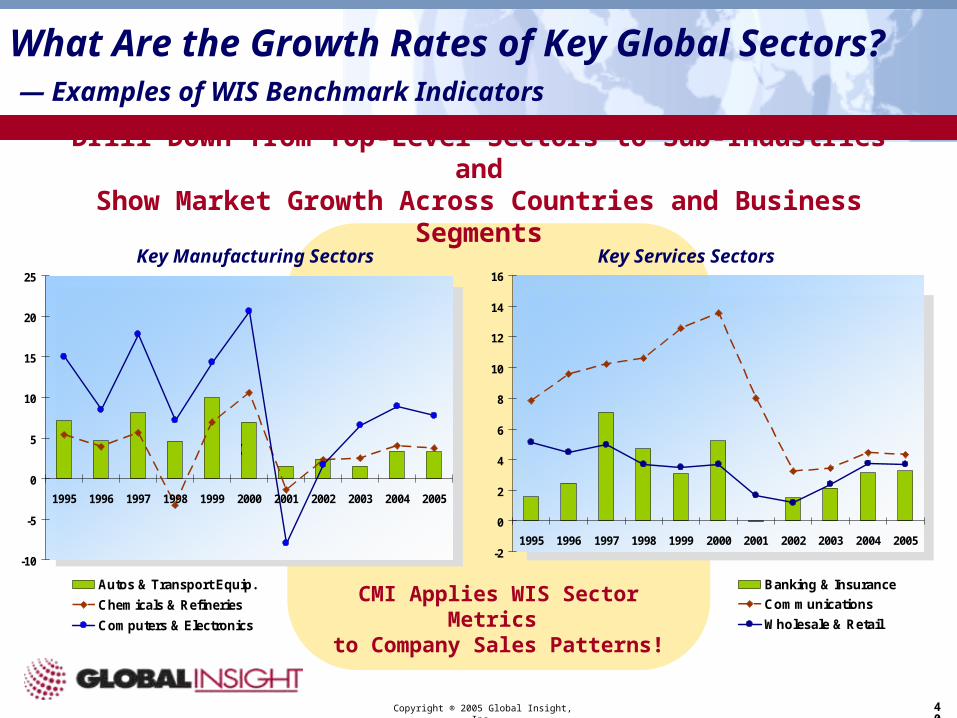

What Are the Growth Rates of Key Global Sectors?— Examples of WIS Benchmark Indicators

40

Copyright ® 2005 Global Insight, Inc.

-2

0

2

4

6

8

10

12

14

16

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Banking & Insurance

Communications

Wholesale & Retail

-10

-5

0

5

10

15

20

25

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Autos & Transport Equip.

Chemicals & Refineries

Computers & Electronics

(

Key Services SectorsKey Manufacturing Sectors

Drill Down from Top-Level Sectors to Sub-Industries andShow Market Growth Across Countries and Business Segments

What Are the Growth Rates of Key Global Sectors? — Examples of WIS Benchmark Indicators

CMI Applies WIS Sector Metrics to Company Sales Patterns!

41

Copyright ® 2005 Global Insight, Inc.

What Are Custom Market Indexes (CMI)?

Companies that operate in or sell into various sectors and several different countries are typically more difficult to track and forecast on a comparable basis across all business components

Also, the actual size of sectors and countries are naturally “weighted” by their actual US$ market size, but these natural “weights” may not be relevant for many companies

The importance of particular sectors to a client can be quite different than the importance of the same sectors to the macro economy

Solution: Create a tailored or Custom Market Index (CMI) that calibrates sector measures to an individual company and/or client business patterns

Provides a consistent framework that can be employed on a common basis across all business segments and regions

42

Copyright ® 2005 Global Insight, Inc.

Forecast sales growth, profits and margins, and market share Communication tool for Wall Street analysts to best illustrate

company performance relative to relevant markets Benchmarking, segmentation, and competitive analysis Corporate planning and strategy, resource management,

expansion, procurement, and competitive investment requirements Active risk management by sector and geographical dimensions

Global Insight’s Custom Market Indexes

Common Use of Custom Market Indexes

43

Copyright ® 2005 Global Insight, Inc.

Custom Market Indexes Take Several Forms

Global Insight’s Custom Market Indexes

1) Structural models provide strategic forecasts of company sales Sales forecasts are measured in US$ (or euro) for size, growth rates, and market

share calculations Flexible “slice and dice,” roll up across all business segments and regions

2) High-frequency models that feature turning point indicators Advantage is shorter time forecast horizons These models can only address segments selling to manufacturing sectors Forecasts are produced only in growth rate terms (not US$ size or market share)

3) Leading indicator models of inflection points Indexes whose known historical values have leading information for future company sales Identify turning points in growth without forecasts These models shows turning points only, not growth rates, market size, or market share

44

Copyright ® 2005 Global Insight, Inc.

Autos, Trucks

Textiles Paper Chemicals

United States 7 3 4 16

West Europe 5 5 13 7

Asia 11 6 15 8

Shares of Company Sales from Geographical Regions and Client Industries Are Used to Create Custom Market Index

0

5

10

15

20

25

30

35

40

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

0

2

4

6

8

10

12

Company Actual Sales Growth (%, Left Scale)

Custom Market Index Growth (%, Right Scale)

Example of Company Custom Market Index—Structural Model Approach

Roll up sales from all segments and region to company totals; compare CMI to actual company sales performances

Use CMI over history to analyze and explain changes in market shares

Use CMI forecasts as unbiased market growth expectations

Cells show the percent shares of company sales that originate from clients in the listed sectors and regions

These shares are used as “weights” that are applied to WIS data to create the company’s actual, attainable custom market

45

Copyright ® 2005 Global Insight, Inc.

CMI for Brazil versus Brazilian GDP

(% change)

-4

-2

0

2

4

6

8

10

1991

1993

1995

1997

1999

2001

2003

2005

Brazil GDP

Custom Market Index for Brazil

CMI Is a Framework for Tracking Key Customer MarketsAcross Different Countries’ Business Segments

CMI for the Chemicals Business Segment

in Different Regions (%)

-3

-1

1

3

5

7

9

11

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Chemicals Segment CMI for North America

Chemicals Segment CMI for Asia

46

Copyright ® 2005 Global Insight, Inc.

Custom Market Index – Example of High Frequency Framework for Selling Into High Technology Sectors

Incorporate WIS high-frequency indicators for key technology and process industries

Use with company sales patterns to create Custom Market Index

Latest WIS data provide up-to-date snapshot of client markets

This version of CMI will forecast sales for a short time horizon (3-6 months), with statistical standard deviations around the forecasts

Focus on growth and inflection points in sales

Use Monthly/Quarterly Indicators to Track and Forecast Near-Term Growth in Sales

0

10

20

30

40

50

60

70

99 Q

1

99 Q

3

00 Q

1

00Q

3

01 Q

1

01 Q

2

01 Q

4

02 Q

2

02 Q

4

03 Q

2

03 Q

4

04 Q

2

04 Q

4

05 Q

2

05 Q

4

06 Q

2

06 Q

4

Plus One Std. Deviation

Segment Sales -- 3 Month Moving Average

Minus One Std. Deviation

History Forecast

47

Copyright ® 2005 Global Insight, Inc.

Custom Market Index – Example of Leading Indicator Based Forecast (Lead/Lag Relationships)

Nature and Length of the Lead/Lag Relationships Are Determined by the Data

US - $ Sales and Turning Point Index

0

2

4

6

8

10

12

14

16

18

1999

M1

2000

M1

2001

M1

2002

M1

2003

M1

2004

M1

Mo

nth

ly S

ales

$M

M 3

mm

a

94

96

98

100

102

104

106Sales 3mma

Index +8

Asia - $ Sales and Turning Point Index

6

7

8

9

10

11

12

13

Mo

nth

ly S

ales

$M

3m

ma

94

96

98

100

102

104

106

108

Ind

ex

Sales 3mma

Index +4

Use monthly/quarterly sector indicators to develop lead/lag relationships with sector indicators

Use high-frequency data for “leading indicators” of future sales Focus on metrics whose known values today anticipate future company sales trends Show likelihood of turning point in sales growth

48

Copyright ® 2005 Global Insight, Inc.

CMIs Deliver the Global Insight Advantage

Accurately forecast your business segment sales

Determine the strength and vulnerability of your markets

Improve your performance against competitors

Target resources toward most promising areas

Minimize the impact of exposure to business cycles

Minimize your risks as a lender or investor

Translate economic events into impacts on key markets

49

Copyright ® 2005 Global Insight, Inc.

Please contact us for a personal demonstration!

More Information?

Mark Killion, CFAManaging Director, World Industry [email protected]

Prem PremakumarApplications Manager, World Industry [email protected]