copyright 2004 acnielsen shoppertrends 1 march 2004 shoppertrends 2004 romania

TRANSCRIPT

Copyright 2004 ACNielsenShopperTrends

1

March 2004

ShopperTrends 2004ShopperTrends 2004

RomaniaRomania

Copyright 2004 ACNielsenShopperTrends

2

Research ObjectivesResearch Objectives

Copyright 2004 ACNielsenShopperTrends

3

Research Objectives

• To provide retailers and manufacturers with a comprehensive overview of the Romanian retail environment

Understand the Romanian consumer: what they buy, when they shop, where they shop – and why

Identify the key factors driving shopper satisfaction and loyalty

What differentiates one retailer from another?

Store Equity: how strong is it, and what factors are driving it?

How do shoppers rate retailers on key drivers of satisfaction and loyalty?

Copyright 2004 ACNielsenShopperTrends

4

Research DesignResearch Design

Copyright 2004 ACNielsenShopperTrends

5

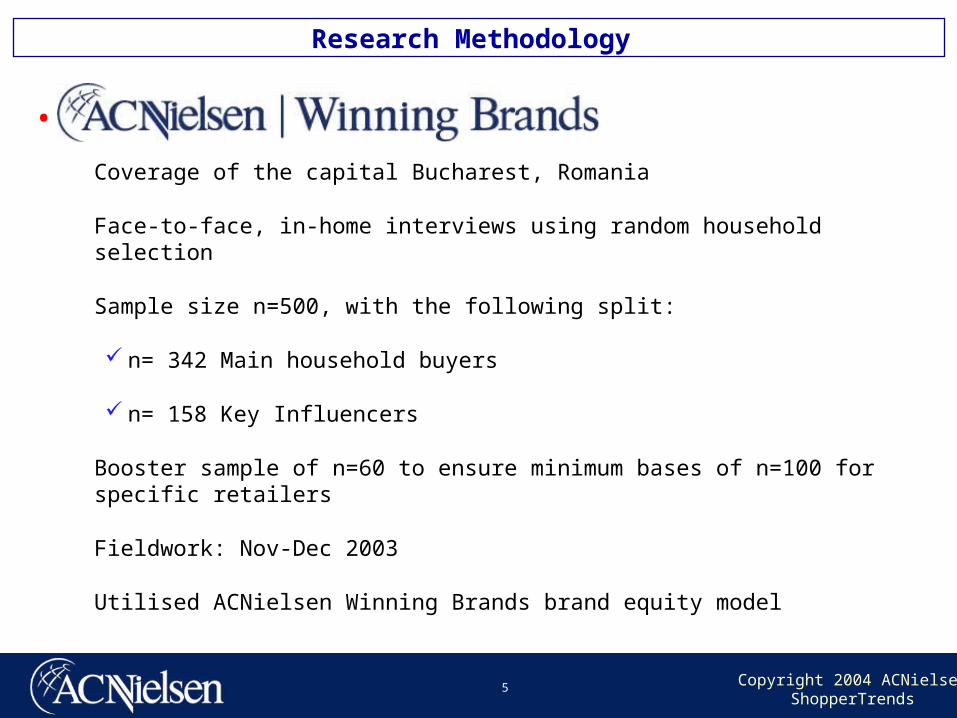

•

Coverage of the capital Bucharest, Romania

Face-to-face, in-home interviews using random household selection

Sample size n=500, with the following split:

n= 342 Main household buyers

n= 158 Key Influencers

Booster sample of n=60 to ensure minimum bases of n=100 for specific retailers

Fieldwork: Nov-Dec 2003

Utilised ACNielsen Winning Brands brand equity model

Research Methodology

Copyright 2004 ACNielsenShopperTrends

6

Economic Status Economic Status & Outlook& Outlook

Copyright 2004 ACNielsenShopperTrends

7

• Last 10 years have been a roller-coaster ride, but economy is now in better shape than ever. Growth is strong and possibly sustainable.

• Excellent results from food and beverage, FMCGs, consumer durables and IT.

• 80% of multi-national corporation country managers are cautiously optimistic, double the level of two years ago.

• Romania is taking one of the priority seats for business development for most clients (as growth slowed in the core CEE countries).

• Purchasing power is still low – average take-home pay is €100. But domestic demand boosted by FDI.

Business performance

Source: EIU

Copyright 2004 ACNielsenShopperTrends

8

• Continued pressure on profit margins.

• Companies now upgrading presence: spending more on advertising and brand-building, expanding out of Bucharest, expanding distribution.

• Competition will tighten in the next two years as more companies continue to invest in business development in Romania and as hypermarkets/supermarkets continue their expansion. Most major players will be on the market within a year.

Business outlook

Source: EIU

Copyright 2004 ACNielsenShopperTrends

9

Grocery Market Grocery Market PerformancePerformance

Copyright 2004 ACNielsenShopperTrends

10

High number of small stores reflective of fragmented structure Bucharest driving modern trade

Retail Structure Share by Channel Type 2003 (Food&Mixed excl. Kiosks)

56%

38%

6%

66%

31%

3%

65%

32%

2%

62%

35%

2%

86%

14%

0%

78%

21%

1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Czech Hungary Poland Slovakia Romania Bucharest

< 50 m2 51- 400 m2 Supermarkets (incl. Discounters)Source: ACNielsen

Copyright 2004 ACNielsenShopperTrends

11

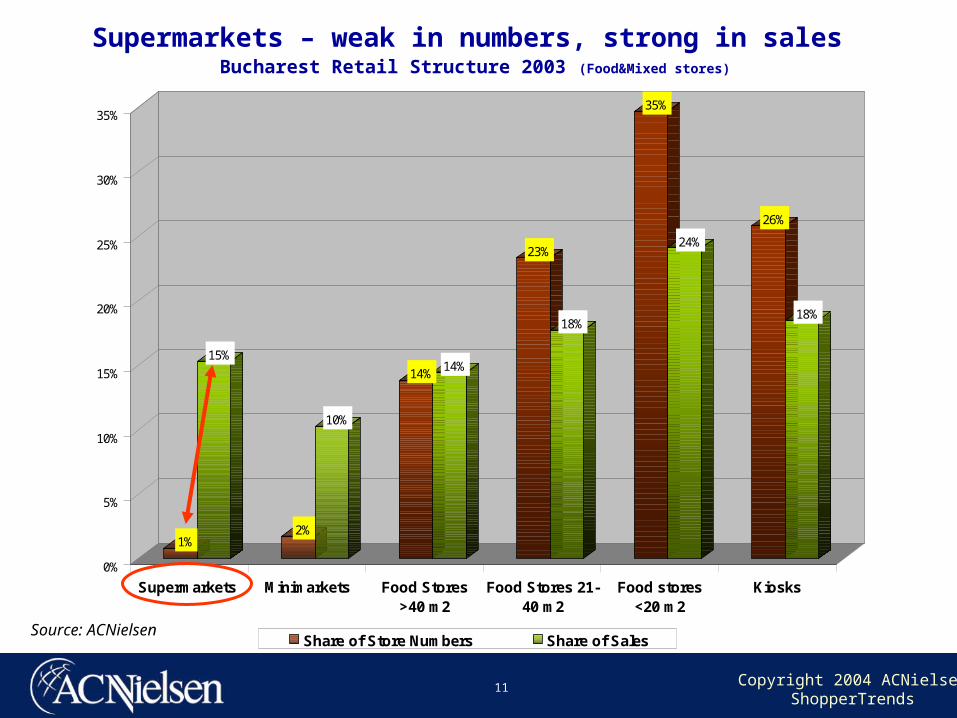

1%

15%

2%

10%

14%14%

23%

18%

35%

24%

26%

18%

0%

5%

10%

15%

20%

25%

30%

35%

Supermarkets Minimarkets Food Stores>40 m2

Food Stores 21-40 m2

Food stores<20 m2

Kiosks

Share of Store Numbers Share of Sales

Supermarkets – weak in numbers, strong in sales Bucharest Retail Structure 2003 (Food&Mixed stores)

Source: ACNielsen

Copyright 2004 ACNielsenShopperTrends

12

0

20

40

60

80

100

120

Czech Rep. Hungary Poland Slovakia Romania

No. supers/hypers per million population

With economy stronger, retailers such as Tesco, Auchan and Schwarz may extend further East beyond CEE

2003

Copyright 2004 ACNielsenShopperTrends

13

Source: ACNielsen

26.7% 28.2% 29.2% 30.0% 31.1% 31.5% 32.1% 33.3% 34.3% 34.9% 35.5% 36.0%

21.4% 21.8% 22.1% 22.3% 21.8% 22.7% 22.9% 23.0% 22.9% 23.1% 23.5% 23.3%9.4% 10.5% 11.5% 12.8% 13.6% 14.1% 14.6% 14.8% 14.9% 14.8% 14.6% 15.6%13.9% 12.8% 12.5% 11.0% 11.4% 10.8% 10.3% 10.4% 10.1% 9.8% 9.7% 8.4%28.7% 26.6% 24.8% 23.8% 22.0% 20.9% 20.0% 18.5% 17.9% 17.4% 16.7% 16.7%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Hypermarkets Large superM Discount Small SuperM Remaining

Europe: Polarization – Discounters & Hypermarkets were big share gainers in last decade

Share by Channel Type - Europe

Copyright 2004 ACNielsenShopperTrends

14

9,711

5,692

10,523

6,750

11,297

8,005

12,613

9,329

13,602

10,083

14,177

11,141

14,443

11,887

14,916

12,753

15,250

13,791

15,012

14,079

15,107

14,632

15,048

15,658

15,507

16,600

15,358

17,272

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004e

Hard Discount Stores

Soft Discount Stores

Europe: Discounters show steady growth in number of stores Hard Discounters accounted for 52% in 2003

No. of Discounter Stores in Europe

Source: ACNielsen

{32.650}

52%

48%

CountryDiscounter Stores 2003

Poland 1000Hungary 325Czech Rep. 245Romania 17 Lidl now in 14 European countries

Copyright 2004 ACNielsenShopperTrends

15

ACNielsen I ACNielsen I ShopperTrendsShopperTrends

DETAILED FINDINGSDETAILED FINDINGS

Copyright 2004 ACNielsenShopperTrends

16

Shopper ProfileShopper Profile

Copyright 2004 ACNielsenShopperTrends

17

33 18 23 26

32%

68%

Main Shopper Key Influencer

13%

87%

Females Males

Shopper Profile by Type & Gender & Age

Base: All respondents (n=500)

GENDER AGE

24 36 2911

15-24 yrs 25-34 yrs 35-49 yrs 50-65 yrs

58%42%

- Main shopping is strongly dominated by females- Males play quite an important role in influencing the shopping- Teenagers and Young Adults (15-24) constitute a significant force among the key influencers

Copyright 2004 ACNielsenShopperTrends

18

14%

26%

60%

Traditional shopper Modern shopper

Mixed shopper

Base: All respondents (n=500)

Shopper Profile by Trade Channel Type

- A good majority of shoppers shop at both modern and traditional trade stores without being loyal to a trade channel type.- Modern trade stores have a stronger foothold among shoppers loyal to a particular store type than traditional stores.

Definitions :

Modern shopper: Have shopped only at Modern

trade stores in past 4 weeks; OR spend most at a

Modern Trade store (i.e. 50% or more of their

grocery budget)

Traditional shopper: Have shopped only at

Traditional trade stores in past 4 weeks; OR spend

most at a Traditional trade store (i.e. 50% or more

of their grocery budget)

Mixed shopper: Have shopped at both Modern

and Traditional trade stores in past 4 weeks, and

spend less than 50% of grocery budget at most

often shopped store

Copyright 2004 ACNielsenShopperTrends

19

Trade Sector OverviewTrade Sector Overview

Copyright 2004 ACNielsenShopperTrends

20

Trade Sector Classification

Kiosks

Hypermarket

•Carrefour

•Cora

•Billa

•La Fourmi

•Mega Imag

e

•Gima

•Metro

•Selgros

Supermarket

Veggie Vendor/Fruit & Veggie

Shop

Open Markets

Convenience storesCash & Carry

Traditional grocery stores

Modern Trade

Traditional Trade

•XXL

DiscounterMinimarket

Copyright 2004 ACNielsenShopperTrends

21

Trade Sector RelationshipsTrade Sector Relationships

Modern Trade & Traditional Trade

Copyright 2004 ACNielsenShopperTrends

22

Trade Sector Relationships – Modern Trade

- Shoppers spend significantly more in supermarkets compared to other modern trade outlets.

HYPERMARKETS SUPERMARKETS MINIMARKETS

9

32

45

65

91

68

21

28

46

58

75

90

61

29

17

24

46

67

81

56

33

Base: All respondents (n=500)

Spend Most Money (%)

Use Regularly (P7D) (%)

Use P4W (%)

Occasionally Use (%)

Ever Used Past Year (%

)

Consider Using (%)

Non considerers (%)

Base: All respondents using less often than occasionally

CASH & CARRY

4

8

10

40

50

49

40

2

5

8

23

40

62

31

DISCOUNTERS

Number of stores 3 70 150 7 1

Copyright 2004 ACNielsenShopperTrends

23

Trade Sector Relationships – Traditional Trade

- Traditional trade channels have considerably higher percentage of regular and occasional visits than the Modern Trade, stemming from top-up shopping rather than main shopping, as well as purchase of Fresh Produce in the case of Open Markets and Bakeries

11

20

33

88

94

54

16

21

62

85

93

97

53

16

7

64

81

91

99

86

14

0

60

75

85

95

72

21

KIOSKS TRADITIONAL GROCERIES

OPEN MARKETS BAKERIES

Base: All respondents (n=500)

Spend Most Money (%)

Use Regularly (P7D) (%)

Use P4W (%)

Occasionally Use (%)

Ever Used Past Year (%)

Consider Using (%)

Non considerers (%)

Base: All respondents using less often than occasionally

Copyright 2004 ACNielsenShopperTrends

24

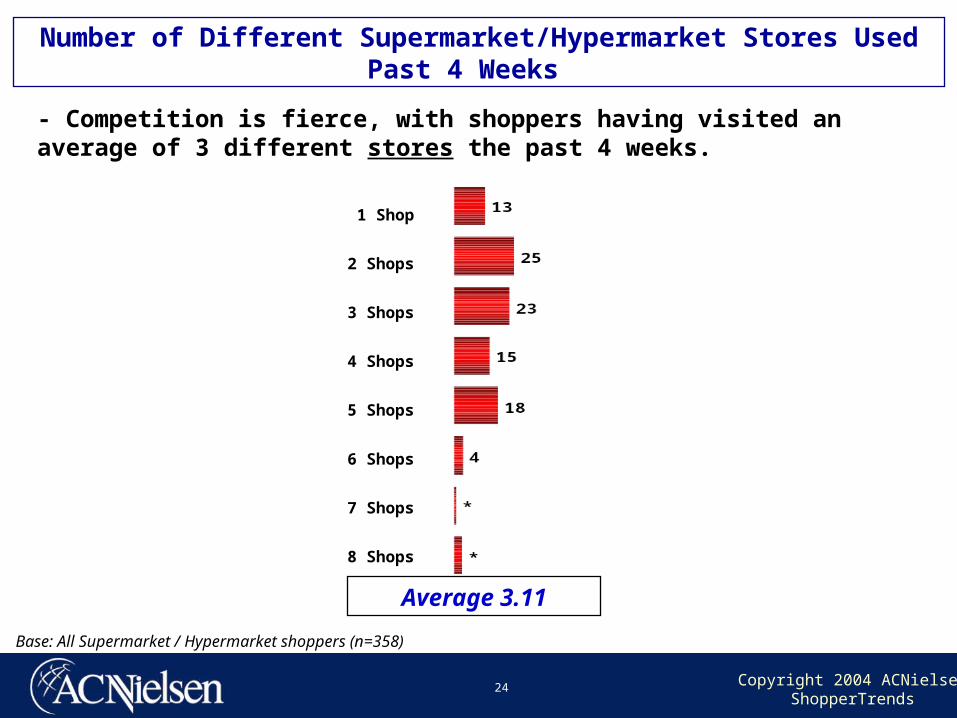

Base: All Supermarket / Hypermarket shoppers (n=358)

1 Shop

2 Shops

3 Shops

4 Shops

5 Shops

6 Shops

7 Shops

8 Shops

Average 3.11

Number of Different Supermarket/Hypermarket Stores Used Past 4 Weeks

- Competition is fierce, with shoppers having visited an average of 3 different stores the past 4 weeks.

Copyright 2004 ACNielsenShopperTrends

25

Key Product Category Key Product Category PurchasesPurchases

Copyright 2004 ACNielsenShopperTrends

26

Fresh Fruit & Vegetables* Fresh Meat/Chicken** Fresh Fish/Seafood***

Main Regular Source of Purchase for Fresh Food Items – Most Often Vs. Regular

Modern trade stores have strong competition from other trade types for Fresh Produce. Open Markets remain to dominate the purchasing of fresh fruits & vegetables.

* 1% do not buy Frui

t & Vegetables

** 2% do not buy Me

at or Chicken

*** 13% do not buy

Fresh Fish/Seafood

Copyright 2004 ACNielsenShopperTrends

27

Canned & packaged Frozen & Chilled Snacks &Food* Food** Confectionery***

Main Regular Source of Purchase for Packaged Food – Most Often Vs. Regular

Modern trade stores have strong competition from Kiosks and Confectioneries for Snacks and Confectioneries, while shoppers prefer hypers/supermarkets for packaged foods.

•* 17% do not

buy canned &

packed food

•** 20% do not

buy frozen &

chilled food

•*** 6% do not

buy snacks &

confectionery

Copyright 2004 ACNielsenShopperTrends

28

Winning B®ands™Winning B®ands™Equity ModelEquity Model

What is Store Equity Index

Store Relationship with Customers

Store Equity Indices for Hypermarkets/ s

upermarkets

Copyright 2004 ACNielsenShopperTrends

29

What is Store Equity IndexWhat is Store Equity Index

Copyright 2004 ACNielsenShopperTrends

30

How is it measured?By measuring the outcomes of Brand Equity

Factor AnalysisBrand Equity Index

(BEI)

3. Willing to pay price premium?

1. % Favorite brand1. % Favorite brand2. % Recommend 2. % Recommend

the brandthe brand

Brand (Store) Equity Index

Copyright 2004 ACNielsenShopperTrends

31

Factor AnalysisBrand Equity Index

(BEI)

ASSOCIATIONS

AWARENESSAWARENESSCONSIDERATIONCONSIDERATION

Brand (Store) Equity Index

How can it be managed?By managing the sources of Brand Equity

Copyright 2004 ACNielsenShopperTrends

32

The Winning Brands Model identifies the Key Drivers of Store Brand Equity

What people dowith stores

What people knowabout stores

PricePremium

Store Loyalty

StoreEquity Index

StoreEquity Index

Awareness

Consideration

Association A

Association B

Association C

Copyright 2004 ACNielsenShopperTrends

33

Building strong brand equity requires consistent brand strategy and investment

53%

33%

9%

5%

Less than 1.0

1.0 - 3.0

3.1 - 5.0

5.0 and above• Strong brand equity is the

exception;

only about 15% of brands

command a brand equity

score of more than 3.0

more than 30% are in the

range 1.0 - 3.0

• Majority of brands have an

equity score of less than 1.0

Source : ACNielsen|Winning Brands normative database of more than 1,500 brands

Strong brands

Brand Equity Index Norm

Copyright 2004 ACNielsenShopperTrends

34

- Carrefour has strong brand equity rating and can be considered as a strong brand.This is driven by strong awareness and high association ratings for value-for-money and wide product range.

Carrefour

Base: All Supermarket / Hypermarket shoppers (n=358)

4.6

2.01.7 1.6

1.4 1.4 1.4 1.31.1 1.1

B C D E F G H I J

Store Equity Indices – Supermarket / Hypermarket

Average across all chains = 1.92

Copyright 2004 ACNielsenShopperTrends

35

Store Associations :Store Associations :What drives Store EquityWhat drives Store Equity

Copyright 2004 ACNielsenShopperTrends

36

Recommenders (%)

Preferrers (%)

Dependables (%)

Regulars (%)

Considerers (%)

Trialists (%)

Aware (%)

Non considerers (%)

Too Hard to Get to (%)

Base: All Supermarket / Hypermarket shoppers (n=358)

45

44

27

64

87

82

98

1

23

8542

Carrefour

12

10

2

30

74

57

98

3

48

628

Chain A

Note: TOM = Top-of-Mind; TSA= Total Unaided Awareness; TA= Total Unaided & Aided

TOM TSA TA TOM TSA TA

Hypermarket Leverage

- Carrefour has the strongest consumer relationships at all levels of the consumer hierarchy

Chain B

3

3

1

16

42

40

79

12

19

323

Copyright 2004 ACNielsenShopperTrends

37

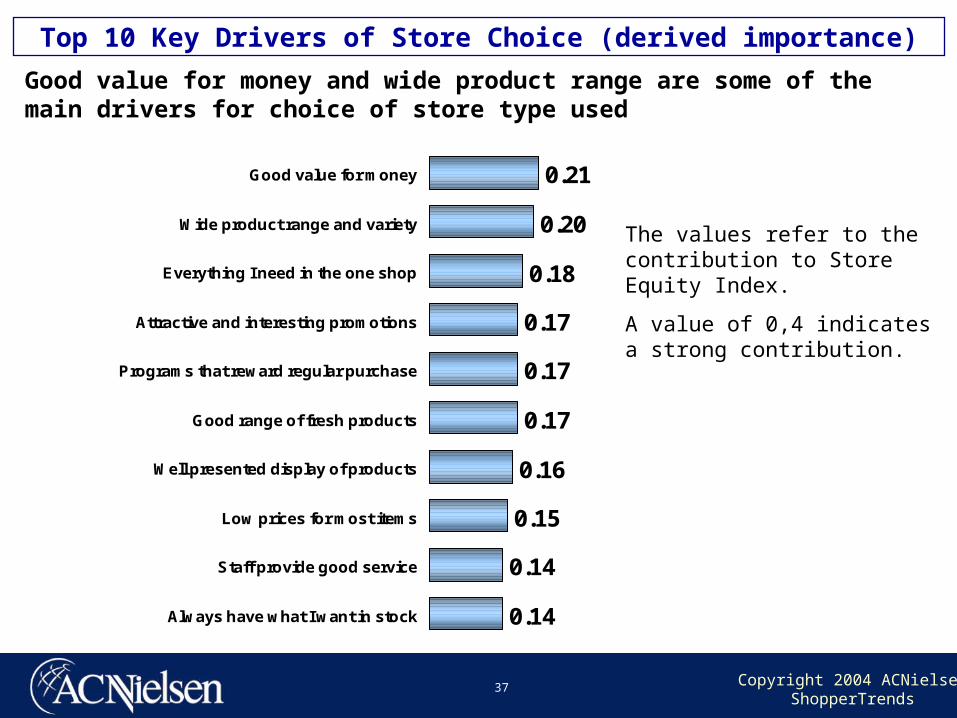

0.21

0.20

0.18

0.17

0.17

0.17

0.16

0.15

0.14

0.14

Good value for money

Wide product range and variety

Everything I need in the one shop

Attractive and interesting promotions

Programs that reward regular purchase

Good range of fresh products

Well presented display of products

Low prices for most items

Staff provide good service

Always have what I want in stock

Top 10 Key Drivers of Store Choice (derived importance)

Good value for money and wide product range are some of the main drivers for choice of store type used

The values refer to the contribution to Store Equity Index.

A value of 0,4 indicates a strong contribution.

Copyright 2004 ACNielsenShopperTrends

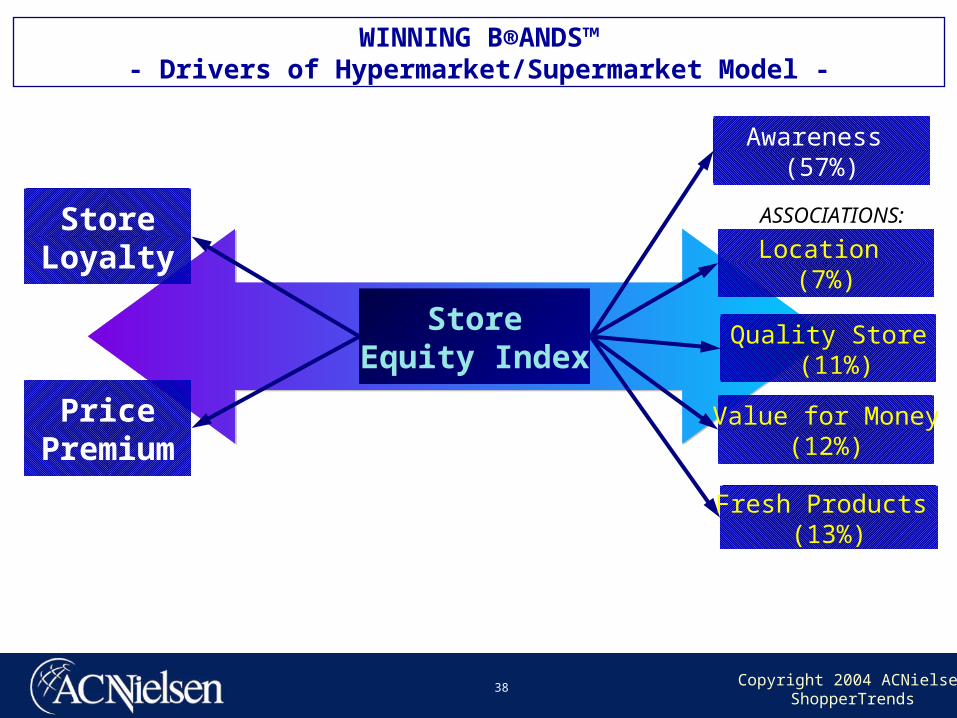

38

StoreEquity Index

StoreLoyalty

PricePremium

Location (7%)

Fresh Products (13%)

Value for Money(12%)

Awareness (57%)

Quality Store (11%)

WINNING B®ANDS™- Drivers of Hypermarket/Supermarket Model -

ASSOCIATIONS:

Copyright 2004 ACNielsenShopperTrends

39

Base: All Respondents

Associations as Drivers of Trade Types Visited in Past 4 Weeks

Drivers of Trade Types Visited P4W

Good range of fresh produce 0.17 High quality of fresh produce 0.11

Good value for money 0.21 Wide product range and variety 0.21 Everything I need in one shop 0.18 Low prices for most items 0.15 Always have what I want in stock 0.14 Ease of parking 0.13 Spacious 0.13 Well presented display of products 0.16 Staff provide good service 0.14 Better selection of high quality brands and

products 0.14 Modern, confortable store 0.12 Easy to find quickly what I need 0.12 Clean, hygienic store 0.08 Convenient to get to 0.08 Proximity to home 0.02

Location (7%)

Fresh Products (13%)

Value for Money(12%)

Quality Store (11%)

Copyright 2004 ACNielsenShopperTrends

40

Store Image AssociationsStore Image Associations

Copyright 2004 ACNielsenShopperTrends

41

Most Least

Brand Equity Differentiation

Base: All who rated particular hypermarket./supermarket

Performance = % top two boxes out of 5 scale

Top 6 Associations - Image Profile Analysis - Key Int’l Retailers Carrefour is more strongly associated with ‘attractive & interesting promotions’

Copyright 2004 ACNielsenShopperTrends

42

Shopper BehaviorShopper Behavior

Copyright 2004 ACNielsenShopperTrends

43

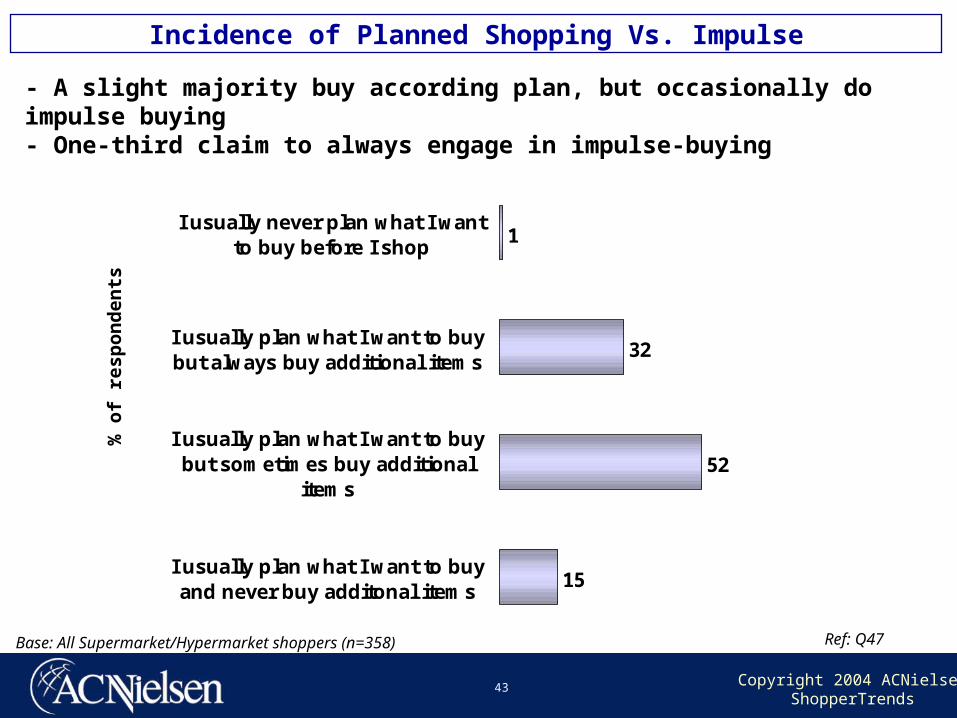

15

52

32

1

I usually plan what I want to buyand never buy additonal items

I usually plan what I want to buybut sometimes buy additional

items

I usually plan what I want to buybut always buy additional items

I usually never plan what I wantto buy before I shop

Ref: Q47

% o

f re

spo

nd

ents

Incidence of Planned Shopping Vs. Impulse

- A slight majority buy according plan, but occasionally do impulse buying- One-third claim to always engage in impulse-buying

Base: All Supermarket/Hypermarket shoppers (n=358)

Copyright 2004 ACNielsenShopperTrends

44

38%

45%

17%I love to keep ahead of what'shappening. I love trying new things. Ioften tell others about them

I usually keep up with what'shappening but I don't go out of myway to try every new thing

I don't generally waste my timetrying to keep up with new things. Iknow what I like and I don't have tokeep trying everything that's new

Ref: Q67

Level of Interest in New Things on the Market

A close majority could be labeled as innovators

Base: All Supermarket / Hypermarket shoppers (n=358)

Copyright 2004 ACNielsenShopperTrends

45

Summary

• Main shopping is strongly dominated by females

• Majority of shoppers shop at both modern and traditional trade stores

without being loyal to a trade channel type The incidence of shopping around among hypers/supers is high, implying low

loyalty levels

• Shoppers spend more in Supermarkets than in any other Modern Trade

type Supermarkets and Hypermarkets still have a challenge and opportunity in the

area of fresh fruits/vegetables vs Open Markets and Specialist outlets

• Store Equity Awareness is clearly a key driver Consideration is not a key driver of Store Equity, given the consistently high

acceptance levels for all stores In terms of Associations (attributes), fresh products, value-for-money and store

quality are similar in terms of importance for driving the Store Equity Each of the above associations are dependant on multiple factors as opposed to

a few key factors

Copyright 2004 ACNielsenShopperTrends

46

THANK YOU FOR YOUR ATTENTION!

Copyright 2004 ACNielsenShopperTrends

47

Building Better Brands