copyright ©2003 south-western/thomson learning chapter 7 common stock: characteristics, valuation,...

TRANSCRIPT

Copyright ©2003 South-Western/Thomson Learning

Chapter 7Common Stock:

Characteristics, Valuation, and Issuance

Introduction

• This chapter describes the characteristics of common stock.

• It discusses the process for selling securities and the role of the investment banker.

• It develops the valuation models for common stock.

Common Stock

• Common stock (C/S) is the permanent long-term financing of a firm.

• Common Stock (C/S) represents the true residual ownership of a firm.

• Stockholders elect the board of directors.

Stock Quotations

• Table 7.1 shows selected stock quotations for stocks traded on the New York Stock Exchange.

TABLE 7.1 Selected Stock Quotations from the New York Stock Exchange

52 Weeks YTD%

CHG Hi Lo

Stock SYM DIV YLD%

PE Vol 100s

Last NET CHG

-15.8 49.88 32.64 DuPont DD 1.40 3.4 40 25369 40.70 +0.09 DuPont pfA 3.50 5.8 60 -0.05 DuPont pfB 4.50 5.9 76.25

Stock Quotations

• Beginning at the left-hand side, the second and third columns show the stock’s price range during the previous 52 weeks. For example, the per-share price of E. I. DuPont de Nemours & Company common stock ranged between $32.64 and $49.88.

• The column immediately to the right of the stock name shows the ticker symbol used to identify this stock on the exchange’s ticker tape, DD for DuPont.

Stock Quotations

• The next column shows the current annual dividend rate; for example, the DuPont Company’s current annual dividend rate is $1.40 per share of common stock. Dividends are normally paid in four quarterly installments throughout the year.

• The next column shows the dividend yield (percentage). For DuPont the figure is 3.4 (calculated as the annual dividend divided by the closing price, or $1.40/$40.70 = 3.4%).

Stock Quotations

• The price-to-earnings or P/E ratio (the closing price divided by the sum of the latest four quarters of earnings per share) is shown next. The P/E ratio (40) indicates how much investors are willing to pay for $1 of current earnings from the firm. Similarly, the P/E ratio will tend to be higher the more rapid the expected growth rate in future earnings.

• The next figure is the sales volume in hundreds of shares; on this day, 2,536,900 shares of DuPont common stock were traded.

Stock Quotations

• The next column lists the last or closing prices for the day.

• The final column shows the net change in price per share for the day, or the difference between this day’s last price and the last price on the previous business day (or the last day on which a trade took place). For the day, the common stock of DuPont gained 9 cents per share.

Stock Quotations

• When a company has preferred stock outstanding that is also traded on the New York exchange, the different classes of preferred stocks are listed in a separate table.

• As can be seen in Table 7.1, DuPont has two preferred stock issues (pfA and pfB that pay $3.50 and $4.50 per share respectively). Unlike common stock dividends, the preferred stock dividend rate normally will not change over the time the issue is outstanding.

Balance Sheet Accounts Associated With C/S

• Stockholders’ equity include both preferred stock (if any exists) and common stock. The total equity attributable to the common stock of a company is equal to the total stockholders’ equity less the preferred stock.

• In other words, the sum of the common stock account, contributed capital in excess of par value account, and retained earnings account equals the total common stockholders’ equity.

• Book value per share

Total common stockholders’ equity # of shares outstanding=

Rights of Common Stockholders

• Dividend rights

Stock holders have the right to share equally on a per-share basis in any distribution of corporate earnings in the form of dividends.

Rights of Common Stockholders

• Asset rights

In the event of a liquidation, stockholders have the right to assets that remain after the obligations to the government (taxes), employees, and debt holders have been satisfied.

Rights of Common Stockholders

• Preemptive rights

Stockholders may have the right to share proportionately in any new stock sold.

• Voting rights

Stockholders have the right to vote on stockholder matters, such as the selection of the board of directors.

Voting for the Board of Directors

• Majority voting – It requires more than 50 percent of the

votes to elect a director.– With majority voting, it is possible that a

group of stockholders with a minority viewpoint will have not representation on the board.

Voting for the Board of Directors

• Cumulative voting – Each share of stock represents as many

votes as there are directors to be elected.– For example, if a firm is electing seven

directors, a particular holder of 100 shares would have 700 votes and could cast all of them for one candidate, thereby increasing that candidate’s chances for being elected to the board.

– Shareholders may concentrate votes on a few candidates.

Voting for the Board of Directors

• Proxy– Shareholders can sign over their voting

rights to someone else.– Normally, a stockholders can expect to

receive a single proxy statement from the firm’s management requesting that stockholders follow management’s recommendations. In the rather unlikely event that another group of stockholders sends out its own proxy statement, a proxy fight is said to occur.

Voting for the Board of Directors

– Proxy fights are most common when a company is performing poorly or is in the midst of a takeover attempt.

Features of C/S

• C/S classes

• Stock splits

• Reverse stock splits

• Stock dividends

• Stock repurchases

Features of C/S: Common Stock Classes

• Occasionally, a firm may decide to create more than one class of common stock. The reason for this may be that the firm wishes to raise additional equity capital by selling a portion of the existing owners’ stock while maintaining control of the firm. This can be accomplished by creating a separate class of nonvoting stock.

• Typically, so-called Class A common stock is nonvoting, whereas Class B has voting rights; normally, the classes are otherwise equal.

Features of C/S: Stock Splits

• If management feels that the firm’s common stock should sell at a lower price to attract more purchasers, it can effect a stock split.

• Many investors believe stock splits are an indication of good financial health. The mere splitting of a stock, however, should not be taken in and of itself as evidence that the stock will necessarily perform well in the future.

• From an accounting standpoint, when a stock is split, its par value is changed accordingly. No changes occur in the firm’s account balance or capital structure.

Features of C/S: Reverse Stock Splits

• Reverse stock splits are stock splits in which the number of shares is decreased. They are used to bring low-priced shares up to more desirable trading levels.

• Many investors feel reverse stock splits indicate poor corporate health. For this reason, such splits are relatively uncommon.

Features of C/S: Stock Dividends

• A stock dividend is a dividend to stockholders that consists of additional shares of stock instead of cash.

• From an accounting (but not a cash flow) standpoint, stock dividends involve a transfer from the retained earnings account to the common stock and additional paid in capital accounts.

Features of C/S: Stock Repurchases

• From time to time, companies repurchase some of their own shares (known as treasury stock).

• A company may have a number of reasons for repurchasing its own stock as follows:

– Disposition of excess cash

– Financial restructuring

– Future corporate needs

– Reduction of takeover risk

Features of C/S: Stock Repurchases

• Disposition of excess cash. The company may want to dispose of excess cash that it has accumulated from operations or the sale of assets.

• Financial restructuring.

By issuing debt and using the proceeds to repurchase its common stock, the firm can alter its capital structure to gain the benefits of increased financial leverage.

Features of C/S: Stock Repurchases

• Future corporate needs. Stock can be repurchased for use in future acquisitions of other companies, stock option plans for executives, conversion of convertible securities, and the exercise of warrants.

• Reduction of takeover risk. Share repurchases can be used to increase the price of a firm’s stock and reduce a firm’s cash balance (or increase its debt proportion in the capital structure) and thereby reduce returns to investors who might be considering an acquisition of the firm.

C/S Advantages and Disadvantages

• Advantages– Flexible– Reduced financial leverage– Lower the firm’s weighted (average) cost of

capital

• Disadvantages– Diluted EPS – Expensive: high issuance costs associated

with common stock sold to the public

Investment Banking

• Long-range financial planning

• Timing of security issues

• Purchase of securities

• Marketing of securities

• Arrangement of private loans and leases

• Negotiation of mergers

How Are Securities Sold?

• Public cash offering– Selling securities through investment

bankers to the public– IPO’s Web site: http://www.ipo.com/

• Private or direct placement– Placing a security issue with one or more

large investors

How Are Securities Sold?

• Rights offering– Selling common stock to existing

stockholders

• Standby underwriting– Investment banker purchases shares not

sold to rights holder.

Public Cash Offering

• Normally, when a corporation wishes to issue new securities and sell them to the public, it makes an arrangement with an investment banker whereby the investment banker agrees to purchase the entire issue at a set price. This is called a firm commitment underwriting. The investment banker then resells the issue to the public at a higher price.

Public Cash Offering

• A negotiated underwriting is simply an arrangement between the issuing company and its investment bankers. Most large industrial corporations turn to investment bankers with whom they have had on going relationships.

Public Cash Offering

• In competitive bidding, the firm sells the securities to the underwriter (usually a group) that bids the highest price.

• Normally, a group of underwriters, called a purchasing syndicate, agrees to underwrite the issue in order to spread the risk.

Public Cash Offering

• An important part of the negotiations between the issuing firm and the investment banker is the determination of the security’s selling price.

• It is in the best interests of both the issuing firm and the underwriter to have the security “fair priced.”

Public Cash Offering

• If the security is underpriced, the issuing firm will not raise the amount of capital it could have, and the underwriter may lose a customer.

• If the security is overpriced, the underwriter may have difficulty selling the issue, and investors who discover that they paid too much may choose not to purchase the next issue offered by either the corporation or the underwriter.

Public Cash Offering

• Occasionally, with smaller company issues, the investment banker agrees to help market the issue on a “best efforts” basis rather than underwriting it.

• Under this type of arrangement, the investment banker has no further obligation to the issuing company if some of the securities cannot be sold.

Public Cash Offering

• The investment banker functions as a dealer in an underwriting situation and as a broker in a best-efforts situation.

• In a best-efforts offering, the investment banker does not assume the risk that the securities will not be sold at a favorable price.

Private Placements

• Many industrial companies choose to directly, or privately, place debt or preferred stock issues with one or more institutional investors instead of having them underwritten and sold to the public.

• In these cases, investment bankers who act on behalf of the issuing company receive a “finder’s fee” for finding a buyer and negotiating the terms of the agreement.

Private Placements: Advantage

• They can save on flotation costs by eliminating underwriting costs.

• They can avoid the time delays associated with the preparation of registration statements and with the waiting period.

• They can offer greater flexibility in the writing of the terms of the contract (called the indenture) between the borrower and the lender.

Private Placements: Disadvantage

• As a very general rule, interest rates for private placements are about one-eighth of a percentage point higher than they are for debt and preferred issues sold through underwriters.

Rights Offerings

• Firm may sell their common stock directly to their existing stockholders through the issuance of rights, which entitle the stockholders to purchase new shares of the firm’s stock at a subscription price below the market price.

Rights Offerings

• Rights offerings also are called privileged subscriptions.

• Each stockholder receives one right for each share owned.

Standby Underwritings

• In an arrangement called a standby underwriting, the investment banker agrees to purchase—at the subscription price—any shares that are not sold to rights holders. The investment banker then resells the shares.

• In a standby underwriting, the investment banker bears risk and is compensated by an underwriting fee.

Direct Issuance Costs

• An investment banker who agrees to underwrite a security issue assumes a certain amount of risk, and, in turn, requires compensation in the form of an underwriting discount or underwriting spread, computed as follows:

Underwriting spread

= Selling price to public – Proceeds to company

Direct Issuance Costs

• It is difficult to compare underwriting spreads for negotiated and competitive offerings because rarely are two offerings brought to market at the same time that differ only in the ways in which they are underwritten.

Direct Issuance Costs

• Other direct costs of security offerings include legal and accounting fees, taxes, the cost of registration with the Securities and Exchange Commission (SEC), and printing costs.

• Generally, direct issuance costs are higher for common stock than for preferred stock issues, and direct issuance costs of preferred stock are higher than those of debt issues.

Direct Issuance Costs

• One reason for this is the amount of risk of each type of issue involves. Common stocks usually involve more risk for underwriters than preferred stock, and preferred stock involves more risk for underwriters than debt.

Direct Issuance Costs

• Another reason is that investment bankers usually incur greater marketing expenses for common stock than for preferred stock or debt issues. Common stock is customarily sold to a large number of individual investors, whereas debt securities are frequently purchased by a much smaller number of institutional investors.

Direct Issuance Costs

• Low-quality debt issues tend to have higher percentage direct issuance costs than high-quality issues because underwriters bear more risk with low-quality issues and therefore require greater compensation.

Direct Issuance Costs

• Direct issuance costs tend to be a higher percentage of small issues, all other things being equal, because underwriters have various fixed expenses that are incurred regardless of the issue’s size.

Other Issuance Costs

• The cost of management time in preparing the offering.

• The cost of underpricing a new (initial) equity offering below the correct market value: Underpricing occurs because of the uncertainty associated with the value of initial public offering (IPO) and a desire to ensure that the offering is a success.

Other Issuance Costs

• The cost of stock price declines for stock offering by firms whose shares are already outstanding—so-called seasoned offerings. The announcement of new stock issues by a firm whose shares are already outstanding causes a price decline averaging about 3% for the outstanding shares.

Other Issuance Costs

• The cost of other incentives provided to the investment banker, including the overallotment or “Green Shoe” option. This option, often contained in underwriting contracts, gives the investment bankers the right to buy up to 15% more new shares than the initial offering amount at a price equal to the offering price.

Other Issuance Costs

• The green shoe option is designed to allow investment bankers to handle oversubscriptions. This option normally lasts for 30 days.

Registration Requirements

• SEC (Securities and Exchange Commission) act of 1933 & SEC exchange act of 1934

• Any interstate security issue over $1.5 million and having a maturity greater than 270 days is required to register issue with the SEC.

• Provide all buyers of the new security with a final copy of the prospectus

• Shelf registration• Check NYSE regulations

Global Equity Markets

• Multinational firms can take advantage of institutional differences from one country to another.

• Stock markets in United States, Japan, London, and Paris

• Nearly 24-hour per day trading of C/S

• Provide investors with opportunities to buy and sell shares any time they wish

• Global name and product recognition

Valuation of C/S

• Capitalized value of the stock’s expected stream of cash flow during holding period

Uncertain

Dividends Not constant

Expected to grow over time

Capital gain or loss

Valuation of C/S

• One-Period Dividend Valuation Model:

• Multiple-Period Dividend Valuation Model:

1 10 1 1e e

D PP

k k

1 20 1 2

...(1 ) (1 ) (1 ) (1 )

n nn n

e e e e

D PD DP

k k k k

Valuation of C/S: Example

• If Ohio Engineering Company common stock is expected to pay a $1.00 dividend and sell for $27.50 at the end of one period, what is the value of this stock to an investor who requires a 14 percent rate of return?

• P0 = $1.00(PVIF0.14, 1) + $27.50(PVIF0.14, 1)

= $1.00(0.877) + $27.50(0.877)

= $24.99

Valuation of C/S: Example

• Assume that the investor’s required rate of return is 14%. Dividends from the stock are expected to be $1 in the first year, $1 in the second year, $1 in the third year, $1.25 in the fourth year, and $1.25 in the fifth year. The expected selling price of the stock at the end of five year is $41. What is the value of this stock to the investor today (t = 0)?

Valuation of C/S: Example

• P0 = $1(PVIF0.14, 1) + $1(PVIF0.14, 2) + $1(PVIF0.14, 3) + $1.25(PVIF0.14, 4) + $1.25(PVIF0.14, 5) + $41(PVIF0.14, 5)

= $1(0.877) + $1(0.769) + $1(0.675) + $1.25(0.592) + $1.25(0.519) + $41(0.519)

= $24.99

Valuation of C/S

• A General Dividend Valuation Model:

• The value of a firm’s common stock to the investor is equal to the discounted present value of the expected future dividend stream.

• Note that the general dividend valuation model treats the stream of dividends as a perpetuity having no finite termination date.

01 1(1 ) (1 )

t tnt t n

t t ne e

D DP P

k k

Valuation of C/S

• As stated in Chapter 1, the primary goal of firms should be the maximization of shareholder wealth. The general dividend valuation model indicates that shareholder wealth, as measured by the value of the firm’s common stock, P0, is a function of the expected stream of future dividend payments and the investor’s required rate of return.

Valuation of C/S

• Thus, when making financial decisions that are consistent with the goal of maximizing shareholder wealth, management should be concerned with how these decisions affect both the expected future dividend stream and the discount rate that investors apply to the dividend stream. See Figure 7.3.

Applications of the General Dividend Valuation Model

• Zero growth– g = 0

• Constant growth dividend – ke > g– D1 = D0(1 + g)1 => Dt = D0(1 + g)t

• Nonconstant growth dividend

• Figure 7.4.

Zero Growth

• If a firm’s future dividend payments are expected to remain constant forever, the Dt in the general dividend valuation model can be replaced by a constant value D to yield the following:

01 (1 )t

t e e

D DP

k k

Zero Growth: Example

• Assume that the Mountainer Railroad common stock pays an annual dividend of $1.50 per share, which is expected to remain constant for the foreseeable future. What is the value of the stock to an investor who requires a 12 percent rate of return?

• P0 = $1.50/12%

= $12.50

Constant Growth

• If a firm’s future dividend payments per share are expected grow at a constant rate, g, per period forever, then the dividend at any future time period t can be forecast as follows: Dt = D0(1 + g)t where D0 is the dividend in the current period (t = 0).

Constant Growth

• Substituting for Dt in the general dividend valuation model yields the following:

• It is assumed that the required rate of return, ke, is greater than the dividend growth rate, g, in the constant growth valuation model.

0 10

1

1

(1 )

(1 )

t

tt e e

nn

e

D g DP

k k g

DP

k g

Constant Growth

• Note that in the the constant growth valuation model, the dividend value in the numerator is D1, that is, the dividend expected to be received one period from now. The model assumes that D0, the current dividend, has just been paid and does not enter the (forward-looking) valuation process.

Constant Growth

• The constant growth dividend valuation model can be used to illustrate the two forms of returns an investor can expect to receive from holding a common stock.

• The investor’s required rate of return is equal to the expected dividend yield, D1/P0, plus the price appreciation yield, g—the expected increase in dividends and, ultimately, in the price of the stock.

1 10

0e

e

D DP k g

k g P

Constant Growth: Example

• Suppose that Dividends for Eaton are expected to be $1.76 per share next year. According to estimates from Value Line and I/B/E/S, earnings and dividends are expected to grow at about 6.5 percent annually. To determine the value of a share of this stock an investor who requires a 12 percent rate of return, substituting $1.76 for D1, 6.5 percent for g, and 12 percent for ke in the constant growth model yields the following value for a share of Eaton’s common stock: P0 = $1.76/(12% 6.5%) = $32.00

Constant Growth: Example

• Thus, the investor’s 12 percent required rate of return consists of a 5.5 percent dividend yield (D1/P0 = $1.76/$32.00) plus a growth return of 6.5 percent annually.

Nonconstant Growth Dividend

• There is no single model or equation that can be applied when nonconstant growth is anticipated.

Nonconstant Growth Dividend

• In general the value of a stock that is expected to experience a nonconstant growth rate pattern of dividend can be calculated as follows:

P0 = (present value of expected dividends during period of nonconstant growth) + (present value of expected stock price at the end of the nonconstant growth period)

Nonconstant Growth Dividend: Example

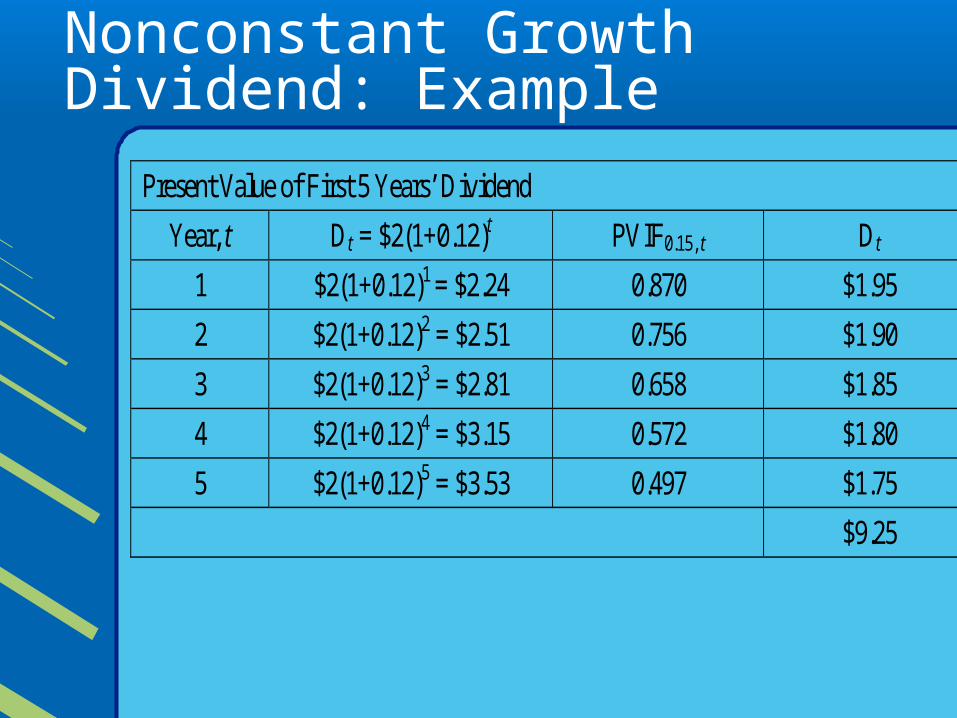

• Suppose an investor expects the earnings and common stock dividends of HILO Electronics to grow at a rate of 12% per annum for the next five years. Following the period of above-normal growth, dividends are expected to grow at the slower rate of 6% for the foreseeable future. The firm currently pays a dividend, D0, of $2 per share. What is the value of HILO common stock to an investor who requires a 15% rate of return?

Nonconstant Growth Dividend: Example

Present Value of First 5 Years’ Dividend

Year, t Dt = $2(1+0.12)t PVIF0.15, t Dt

1 $2(1+0.12)1 = $2.24 0.870 $1.95

2 $2(1+0.12)2 = $2.51 0.756 $1.90

3 $2(1+0.12)3 = $2.81 0.658 $1.85

4 $2(1+0.12)4 = $3.15 0.572 $1.80

5 $2(1+0.12)5 = $3.53 0.497 $1.75

$9.25

Nonconstant Growth Dividend: Example

6 65

2

6 5 2

5

Value of Stock at End of Year 5:

0.15 0.06

(1 ) $3.53(1 0.06) $3.74

$3.74$41.56

0.15 0.06

e

D DP

k g

D D g

p

Nonconstant Growth Dividend: Example

55 5 5

0.15, 55

0 5

Present Value of , PV( ) = (1 )

$41.56$41.56(PVIF )

(1 0.15)

$41.56(0.497) $20.66

Value of Common Stock:

PV(first 5 years' dividends) + PV( )

$9.25 $20.66 $29.91

e

PP P

k

P P

Sources of Analyst Growth Rate Forecasts

• Value Line Investment Survey– http://www.valueline.com/

• Institutional Brokers Estimate System– http://www.ibes.com/

• Zacks Earnings Estimates– http://www.zacks.com/

Valuing Small Firms

• Nature of business

• History of business

• Economic outlook

• Dividend paying

capacity

• Industry

• Earnings capacity

• Book value

• Financial condition

• Majority or minority

interest

• Voting or nonvoting

Valuation Web site: http://www.bearval.com/