conversation triggers

TRANSCRIPT

Ed Keller CEO, Keller Fay Group

Twitter.com/kellerfay

Emily Vanides VP Connections Research

& Analytics MediaVest

Conversation Triggers: Sparking Conversations with

Advertising & Media

Insert Photo

Insert Photo

June 13, 2011

Word of Mouth is Powerful

“The rewards of pursuing excellence in word-of-mouth are huge, and it can deliver a significant competitive edge few other

marketing approaches can match”

“It’s the most disruptive factor in marketing”

“Marketing-induced consumer-to-consumer word of mouth generates more than twice the sales of paid advertising”

2

McKinsey Quarterly, April, 2010

But What Sparks Conversation?

Many assume WOM is generated by great brand experiences – Highly satisfied customers become evangelists for brands.

However, marketing often sparks WOM, as well

– Half of conversations about brands refer to media/marketing.

To maximizing WOM, we need a clear sense of how marketing can most effectively “trigger” conversations.

– Which media, at what time of day, in what venues, and relating to what topics of conversation?

3

WOM is at the core of SMG’s approach to marketing communications

4

Simplifying human

understanding to deliver

meaningful brand experiences

Our framework for designing

experiences that matter

Ultimately, brands need to be a part of the conversation

We live in a networked world

The role of marketing is to be a spark in the communities where people live and play

We have to harness the power of people‟s shared purpose & voice – Weaving into the fabric that bonds people together

5

We must listen & understand the conversations and how we can trigger them

We looked to our partners at Keller Fay to provide new insights

5+ year partnership with SMG

Proven approach to WOM tracking and analysis – Inclusive of both online AND offline

International perspective

Successful and market-leading insights into the relationships between marketing and brand WOM – E.g. Super Bowl, Olympics, Cross-media studies, etc

6

Multiple Data Sources: TalkTrack®

TalkTrack® Methodology – TalkTrack® is a diary-based survey program that measures all forms of word of mouth (WOM) –

offline + online.

– Respondents keep a diary of conversations over a 24-hour period, and then take an online survey where they report on these conversations.

TalkTrack® US – A national syndicated program involving 36,000 consumers aged 13 to 69 annually.

– The majority of TalkTrack® US results presented in this analysis are derived from interviews collected during November 2009 to October 2010, and during this time a total of 36,622 respondents participated.

TalkTrack® Britain – Study was fielded online in May 2010.

– A total sample of 2,578 16 to 69 year olds participated in the first wave of this study.

TalkTrack® Australia – Study was fielded online in April – May 2010.

– A total sample of 2,829 16 to 69 year olds participated in this study.

7

Multiple Data Sources: IPA TouchPoints 3

Unique and original survey of 5,400 British adults aged 15+ – Information gathered through individual PDA diaries and self-completion

questionnaires.

The findings presented here focus on the diary portion of TP3.

The diary records information on a half hourly basis on the following:

– Location of respondent

– Who they were with

– What they were doing (consuming media, communicating, etc.)

– What media they were consuming

– Their mood

Research was conducted during September 2009 through February 2010.

8

Regardless of Market (or Category), Offline Conversations Dominate

9

US = 7% Britain = 7% Australia = 7%

US = 91% Britain = 92% Australia = 91%

Source: TalkTrack®: US, July 2009 – June 2010; Australia, April 2010, Britain, May 2010

How Brand Conversations Take Place

Presentation to Cover

What triggers WOM, according to consumers

Role of media/marketing in WOM

10

What Triggers WOM, According to Consumers

11

Base: Conversations (All WOM, n=17,653)

Source: Keller Fay Group‟s TalkTrack® Australia, April – May 2010

“Which one of the following comes closest to describing what

prompted or “sparked” the conversation? “

(TalkTrack® Australia)

“Something else” generally relates to “neutral” or

factual talk about brand experiences or purchase plans.

Important Differences in WOM Triggers by Category

12

Base: Conversations (Beauty & Personal Care, n=634; Beverages, n=1,390; Technology, n=1,368; Financial, n=1,003)

Note: Percentages will not add to 100% because “something else” is not shown. These figures are 32%, 46%, 27%, and 42%, respectively.

Source: Keller Fay Group‟s TalkTrack® Australia, April – May 2010

What “Sparked” The Conversation Ranked by “All WOM” Results on Previous Slide

(TalkTrack® Australia)

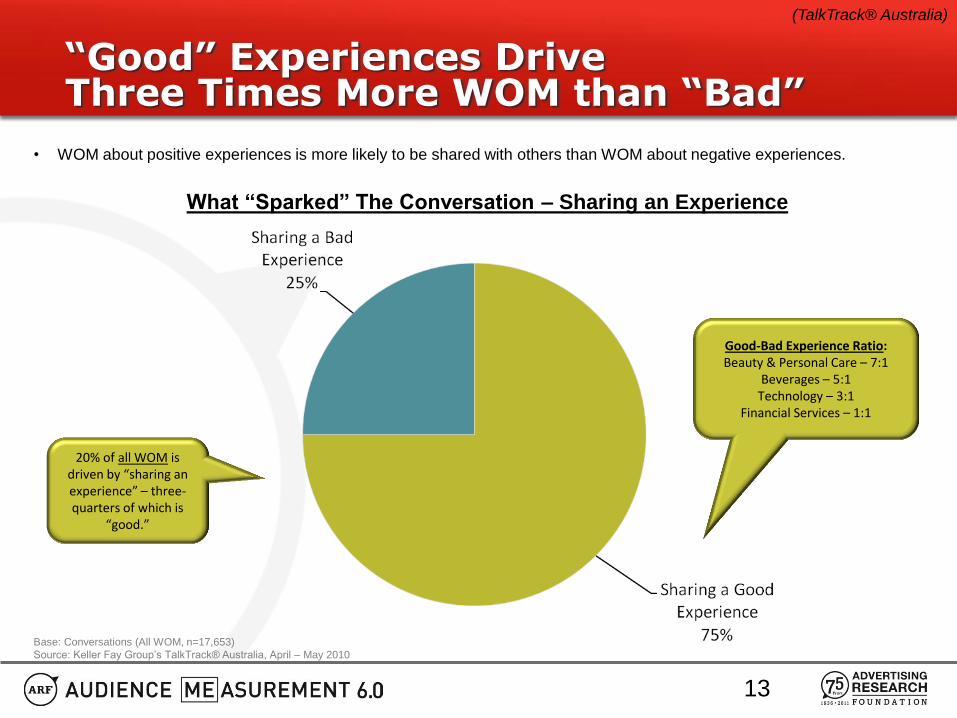

“Good” Experiences Drive Three Times More WOM than “Bad”

13

Base: Conversations (All WOM, n=17,653)

Source: Keller Fay Group‟s TalkTrack® Australia, April – May 2010

What “Sparked” The Conversation – Sharing an Experience

(TalkTrack® Australia)

20% of all WOM is driven by “sharing an experience” – three-quarters of which is

“good.”

Good-Bad Experience Ratio: Beauty & Personal Care – 7:1

Beverages – 5:1 Technology – 3:1

Financial Services – 1:1

• WOM about positive experiences is more likely to be shared with others than WOM about negative experiences.

Positive, Strong Emotions Trigger the Most WOM

14

Beauty & Personal Care Beverages

Topics Surfacing in Each Category Highly Likely Not Likely Highly Likely Not Likely

Superlative Brand Enthusiasm (Love, Excellent…) 10% 6% 11% 6%

General Brand Enthusiasm (Great, Good…) 15% 11% 11% 11%

General “Like” /Think Brand is OK 8% 7% 10% 11%

Brand Criticism (Terrible, Bad, Hate, Worst) 3% 5% 2% 5%

Brand Reputation (Positive) 6% 4% 2% 2%

Brand Works Well 14% 9% 17%* 11%*

Brand Does Not Work Well 3% 6% 3%* 3%*

Purchase Decision 10% 10% 15% 17%

“Need” The Brand 10% 7% 5% 5%

“Want” The Brand 1% 3% 5% 5%

Summary Table: WOM Topics Surfacing in Each Category by Pass-Along Likelihood

*For “Works Well” for beverages examined “tastes good” and brand hydrates, wakes me up, etc.

**For “Works Well” we examined “rate of return/earning interest” and positive feedback on customer service, since finance is a services oriented category. “Doesn‟t Work Well” is negative customer service.

***For “Cost” examined charges/fees/interest/rates positive and negative.

Note: Shading denotes statistical significance at the 90% confidence level.

Source: Keller Fay Group‟s TalkTrack®, October 2009 – September 2010

(TalkTrack® US)

Positive Emotions Also Key Trigger for Tech & Financial WOM

15

Technology Financial

Topics Surfacing in Each Category Highly Likely Not Likely Highly Likely Not Likely

Superlative Brand Enthusiasm (Love, Excellent…) 11% 5% 6% 3%

General Brand Enthusiasm (Great, Good…) 25% 18% 13% 7%

General “Like” /Think Brand is OK 5% 5% 2% 2%

Brand Criticism (Terrible, Bad, Hate, Worst) 7% 9% 14% 11%

Brand Reputation (Positive) 8% 3% 3% 1%

Brand Works Well 5% 2% 5%** 4%**

Brand Does Not Work Well 1% 3% 3%** 5%**

Purchase Decision 5% 6% N/A N/A

“Need” The Brand 2% 1% N/A N\/A

“Want” The Brand 6% 2% N/A N/A

Summary Table: WOM Topics Surfacing in Each Category by Pass-Along Likelihood

*For “Works Well” for beverages examined “tastes good” and brand hydrates, wakes me up, etc.

**For “Works Well” we examined “rate of return/earning interest” and positive feedback on customer service, since finance is a services oriented category. “Doesn‟t Work Well” is negative customer service.

***For “Cost” examined charges/fees/interest/rates positive and negative.

Note: Shading denotes statistical significance at the 90% confidence level.

Source: Keller Fay Group‟s TalkTrack®, October 2009 – September 2010

(TalkTrack® US)

Media Play a Big Role in Driving WOM

16

~ Half of consumer brand conversations

refer to marketing or media

…led by television (17%)

Internet (15%)

point of sale (9%)

newspapers (6%)

magazines (5%)

direct mail/email (5%)

Marketing and media are tools for encouraging WOM

(TalkTrack® US)

Source: Keller Fay Group‟s TalkTrack®, November 2009 – October 2010

Which Media that Trigger WOM? Plan by Category

All WOM Beauty & Personal

Care Beverages Technology

Financial Services

Brand Mentions Involving One or More References*

52% 59% 44% 55% 41%

Television 17% 15% 12% 13% 8%

Internet 15% 13% 8% 26% 19%

Point Of Sale 9% 14% 15% 12% 4%

Promotion 8% 18% 12% 6% 3%

Newspaper 6% 6% 5% 6% 5%

Direct Mail/E-Marketing 5% 5% 3% 5% 10%

Magazine 5% 9% 4% 6% 3%

Any Other Ad 3% 3% 3% 3% 3%

Radio 3% 3% 3% 3% 3%

Billboard 2% 2% 2% 2% 1%

17

Base: Brand Mentions (All WOM, n=170,380; Beauty, n=7,361; Technology, n=13,523; Beverages, n=17,822; Financial Services, n=8,324)

*Up to two media/marketing references can be selected so figures will not add to this total row.

Source: Keller Fay Group‟s TalkTrack®, November 2009 – October 2010

Media and Marketing References (% of WOM conversations citing media or marketing; top 3 references highlighted)

Magazines are disproportionately

referenced in beauty WOM.

(TalkTrack® US)

Introducing the Media Sociability Index™

Which media give advertisers the best access to consumers while they are in a conversational mode?

– Based on proximity of media use and conversation.

– TouchPoints3 (UK) is data source.

The Media Sociability Index™ reveals “highly sociable media.” – This is an index which compares „those consuming media and

communicating‟ with the average percentage of people communicating at any given half-hour interval over the course of the day.

18

Conversations Happen More Often at Times When Media are Being Consumed

19

Media Sociability Index*** = 141

• The baseline Media Sociability Index for conversations is 141 (based on 45% divided by 32%).

% of Total Adults Having

Conversations

During Each Half Hour

(Average Day*)

% of People Consuming Media

Who Are Simultaneously**

Conversing with Others Offline or

Online (Average Day)

All Forms of Conversation (Offline or Online)

(IPA TouchPoints 3)

*An average of the average percentage of offline./online or offline conversations during each half hour was taken to arrive at this figure.

**Same half hour

***Media Sociability Index compares „those consuming media & communicating‟ with the average percentage of people communicating during the day.

Source: IPA TouchPoints3

Internet & Radio are Highly Sociable, Coinciding Most with Conversations

20

*Same half hour

**Media Sociability Index compares the above results to the average percentage of people communicating overall (32%) or just offline (30%) over the

course of the day.

Source: IPA TouchPoints3

163 153 141 103 100

Boxed figures

represent Keller Fay‟s

Media Sociability

Index** metric

(IPA TouchPoints 3)

Large Variances in Times of Day People Socialize While Using Media

21

*Same half hour

**Midnight to 4AM excluded for print media due to low base sizes during these hours.

Source: IPA TouchPoints3

(IPA TouchPoints 3)

Workplace use drives the sociability of Internet use during

the morning hours.

Media Consumption at Work & School Enjoy Highest Sociability

22

*Same half hour

**Media Sociability Index compares the above results to the average percentage of people communicating overall (32%) across each day part.

Source: IPA TouchPoints3

141 225 219 131 128

Boxed figures

represent

Keller Fay‟s

Media

Sociability

Index** metric

The Percentage of People Consuming Media Who are Simultaneously* Conversing with Others Offline or Online – By Location (During Average Day – Monday through Sunday)

(IPA TouchPoints 3)

Digital Channels Related to Kids & Music Earn Highest Sociability Scores

23

Type of Digital Channel Watched % Communicating

with Others Media Sociability Index**

Children’s 73% 228

Music 54% 169

Home/DIY/Gardening 49% 153

Sport 48% 150

Reality 47% 147

News/Current Affairs 47% 147

Entertainment 46% 144

Shopping 44% 138

Game Show 41% 128

Movie 41% 128

Nature 39% 122

*Same half hour

**Media Sociability Index compares the above results to the average percentage of people communicating overall (32%) across each day part.

Source: IPA TouchPoints3

The Percentage of People Watching Digital TV Channels Who are Simultaneously* Conversing with Others Offline or Online

(During Average Day – Monday through Sunday)

(IPA TouchPoints 3)

Conclusions: Opportunities to Trigger WOM

24

Marketing and media play important roles in triggering WOM: – Consumers tell us media “triggers” WOM 20% of the time.

– Consumers report both conversing and consuming media during the same day parts.

– Consumers report nearly half their conversations contain a reference to content they found in marketing.

Conversations often happen close to the times when media are being consumed, providing marketers access to conversations.

– Early morning and early evening are especially good times to reach people who are consuming media and socializing.

Conclusions: Opportunities to Trigger WOM

25

TV & Internet are referenced in the largest volume of conversations, while point of sale & promotions play a key role in CPG WOM.

The Internet is possibly the most “sociable” of media, especially at work.

– Radio surprisingly effective at reaching people in social context.

– Television, especially programming/channels related to children, DIY, or sports, is effective in triggering conversations at home.

Positive experiences trigger more WOM than negative. – WOM containing stronger emotions tends to be the most viral.

– Positive talk related to product efficacy, such as “works well,” is also more likely to be shared with others.

Thank you!

Ed Keller, [email protected]

Facebook.com/kellerfay

Twitter.com/kellerfay

Emily Vanides

Insert Photo Insert Photo