convenor details -...

TRANSCRIPT

Page | 1

Introduction to the Law of International Finance

LALA121S7

Module Guide2015/16

LLM/MA Intensive Programmes

CONVENOR DETAILS

Dr Stephen Connelly (the Convenor)

School of LawBirkbeck, University of LondonMalet StreetLondon WC1E 7HX

Please use email to contact me if possible.

IMPORTANT DATES

Seminars start: Wednesday 16th March 2016

Seminars end: Tuesday 22nd March 2016

Deadline for agreement of coursework titles: Monday 9th May 2016

Coursework Submission Date: Monday 13th June 2016, 11.30am

If you are having any trouble meeting deadlines, please contact Dr Stewart Motha as soon as possible.

Page | 2

GENERAL INTRODUCTION TO THE COURSEWelcome to Introduction to International Finance Law. This is a core module for the LLM International Finance and Economic Law programme and an optional module for the LLM in International Economic Law, Justice and Development, and the LLM in Human Rights. The module aims to give an overview of the central issues affecting the relationship between international economic law, justice and development.

Introduction to the Law of International Finance (the Module) examines the financialisation of law that has taken place with increasing speed over the last 30 years. In so doing, the Module considers in some depth three areas in which traditional principles of law and equity have encountered and been suborned by the development of the international trade in debt and debt instruments. The wider theoretical aim of the module is the critical engagement with the ideas of ethics, norms and complexity within financial development, regulation and crisis. Students will be asked to explore the relationship between the concept of consciousness and the failure of financial regulation in the face of complex legal structures, and will be introduced to immanent critiques of finance in actu.

The primary legal focus of the Module will be English law-governed credit agreements in the form current in City of London practice, but given the international nature of the subject, due to the use of such English law-governed agreements in diverse jurisdictions globally, appropriate analysis of EU law and other national laws (particularly New York, Germany and France) will be undertaken at appropriate junctures. Students may be surprised to learn that an English law credit agreement for an English industrial corporation is not so very different in style from a loan agreement between, say, China and Costa Rica. By using the credit agreement as the anchor of the course, rather than international and somewhat abstract banking regulations, the Module attempts to offer a borrower perspective which links the more arcane aspects of the secondary market in debt to the more familiar and tangible context of industrial business, its directors and employees, and society as a whole. The Convenor contends that it is fundamental that the structure of financial relations be comprehended if one is to engage with the precise nature of ‘power’ at work during the current economic conjuncture.

Additionally, the Module is designed to bridge the gap between the formal understanding of the core principles of the English law of obligations, companies, and the tenets of equity, and the practise of these principles in ‘financial capitals’ across the World. For this purpose, the Module builds on students’ existing legal and socio-economic training to engage in a detailed analysis of credit facility agreements, guarantees, security agreements, intercreditor agreements and related primary and secondary finance documents, always emphasising the manner in which the economic demands of international finance ‘shape’ these agreements and in some instances strain legal doctrine to breaking point. We thus hope to illustrate the great tensions that lie at the heart of financialised law; tensions which were exposed by the 2008 Credit

Page | 3

Crunch. The analysis will look in particular at the idea of regulation and consciousness, examining how justice and ethics fall in the encounter between markets, states and regulatory capture.

The Module will be taught intensively from 16th March 2016 until 22nd March 2016 inclusive. There is set reading for each seminar, which is divided into essential and further reading. Students are expected to have studied the essential reading for each seminar and to be prepared to discuss that material in the light of the discussion questions for each seminar.

USE OF MOODLEPlease check regularly for updates, information and materials. Where possible the lecturers will draw your attention to new materials being placed on the sites, but it is considered to be your responsibility to stay informed and check regularly. If for any good reason you are unable to use Moodle and require assistance with obtaining the materials for the course please contact a member of the Administration Team at the Main Law School Office.

Essential reading for each seminar and assessment information will be placed on Moodle.

Page | 4

AIMS AND LEARNING OUTCOMESThe Module aims in general to introduce students to a critical examination of the law, regulations, institutions and practice of international finance, with particular emphasis on exploring the metaphysical assumptions supporting concepts of money, debt, guilt, finance, consciousness, normativity, and desire. In particular the Module’s aims are to:

• provide a critical genealogical background to the understanding of financial capitalism;• familiarise students with the concepts of money and finance capital;• give students a core working knowledge of current financial law practice and an understanding of

the relation between international secondary debt markets and credit agreements;• outline the relevance and contentious aspects of security and guarantees;• give students a working knowledge of complex international debt structures: syndication and

securitisation;• introduce students to the legal practical aspects of credit defaults, restructuring, transnational

insolvency and enforcement, and sovereign default; and• familiarise students with the problems of national and transnational financial regulation, with a

focus on banking supervision and the LIBOR scandal.

On successful completion of this module a student will be expected to be able to:

• apply their already acquired legal skills to the understanding of the central aspects of standard ‘London-form’ financial contracts in use in financial markets today;

• exhibit a general understanding of the common types of cross-border debt structures and be able to determine their morphology under credit default situations;

• discuss the relations between the ‘real’ economy, the world of private international finance, and international economic institutions; and

• critically discuss theories money, debt, guilt, finance, consciousness, normativity, and desire and their relation to socio-economic conditions in our financialised world, the activities of financiers, the failures of regulation, and financial crises.

Page | 5

ASSESSMENTThe course will be 100% assessed by a 4,000 word research essay. Students may either (a) choose a question from the list of sample research essay questions that appears below, or (b) develop their own essay question in consultation with me.

Where students elect to develop their own essay question in consultation with me, the question must be finalised by 9th May 2016. By this date, students must get my approval for a question that is not on the list of sample essay questions. Essays on questions other than those set out in the list of sample research essay questions may not be marked if students have not consulted with me as required in this paragraph.

For the purpose of writing this essay, students are expected to consult a range of primary and secondary materials.

The essay must be footnoted and all sources must be properly cited. Failure to observe this obligation may result in the loss of marks. Students are reminded that the failure to acknowledge sources relied upon may amount to academic misconduct. Proven academic misconduct carries potential penalties of greater severity than the loss of marks.

A case list and bibliography must be submitted with the essay showing all sources consulted. The remarks above in relation to academic misconduct are also pertinent to the obligation in this paragraph.

The word limit for the essay is 4000 words. This word limit includes discursive footnotes, but not footnotes that only contain a citation to source.

The case list and bibliography are not subject to the word limit. Where an essay exceeds the word length by more than 500 words then I retain the discretion to reduce the overall mark in proportion to the amount by which the word limit is exceeded.

Where the ability of a student to comply with the assessment requirements is compromised by illness or other adverse personal circumstance the matter should be brought to my attention or to the attention of the relevant course director as soon as the student is aware of it.

SAMPLE RESEARCH ESSAY TOPICS

1. “The advent of the Christian God as the maximal God yet achieved, thus also brought about the appearance of the greatest feeling of indebtedness. … [T]he possibility cannot be rejected out of hand that the complete and definitive victory of atheism might release humanity from the whole feeling of being indebted towards its beginnings, its causa prima.” Nietzsche (On the Genealogy of Morals, II §20)

Critically assess the theory of ‘primordial debt’ as an explanation of the role of indebtedness in the grounding of cities and maintaining social order.

Page | 6

2. Critically evaluate the contractual and statutory approaches to sovereign debt restructuring, and evaluate proposals for reform that take into account a wider range of social costs than the needs of creditors.

3. “A very significant portion of the social circulating capital…will thus periodically exist in the course of the annual turnover cycle in the form of capital set free. … This money capital that is set free…must play a significant role, as soon as the credit system has developed….” Marx Capital II pp.355-7.

Examine why Marx uses the language of self-liberation with respect to money capital, and how this classification of finance as sui juris might impact on attempts to regulate it.

4. “Without speculation there would be no business. Why the devil would I open my purse for you [Mme Caroline], just as I risk my fortune, if you didn’t promise fantastic pleasures…. The race begins, energies are released, the hurly-burly is such that, sweating as they do solely for personal gratification, people sometimes manage to produce children. … There is much filth, but without it the world would end.” Saccard in l’Argent by É. Zola

Critically assess theories which link finance capital with desire and/or life. Are such theories, despite their apparent radicalism, rather panegyrics for finance?

5. “The law of international finance is the new lex mercatoria in the sense that it exists independently of and is practically unbound by national legal regimes.” Critically discuss with reference to the tensions between international private financing structures and national laws (you may focus on your home jurisdiction).

6. “The capacity of finance institutions to require security, guarantees, and subordination, makes a mockery of states’ attempts to prefer other ‘stakeholders’ such as employees on insolvency of a business.”

Critically discuss, drawing on the contractual documentation discussed in the Module and examples reported in the financial press.

7. What are the rationales of regulation? With reference to the Global Financial Crisis, what are the key features and limits of a risk-based approach to regulation?

8. The basic principle of regulation—of requiring good behaviour—is against all common sense flawed. The sum total of good behaviours does not equal a well behaving financial system as the Global Financial Crisis powerfully proved.

Critically discuss with reference to the development of financial regulatory and bank supervisory regimes.

Page | 7

SUMMARY OF SEMINAR TOPICS

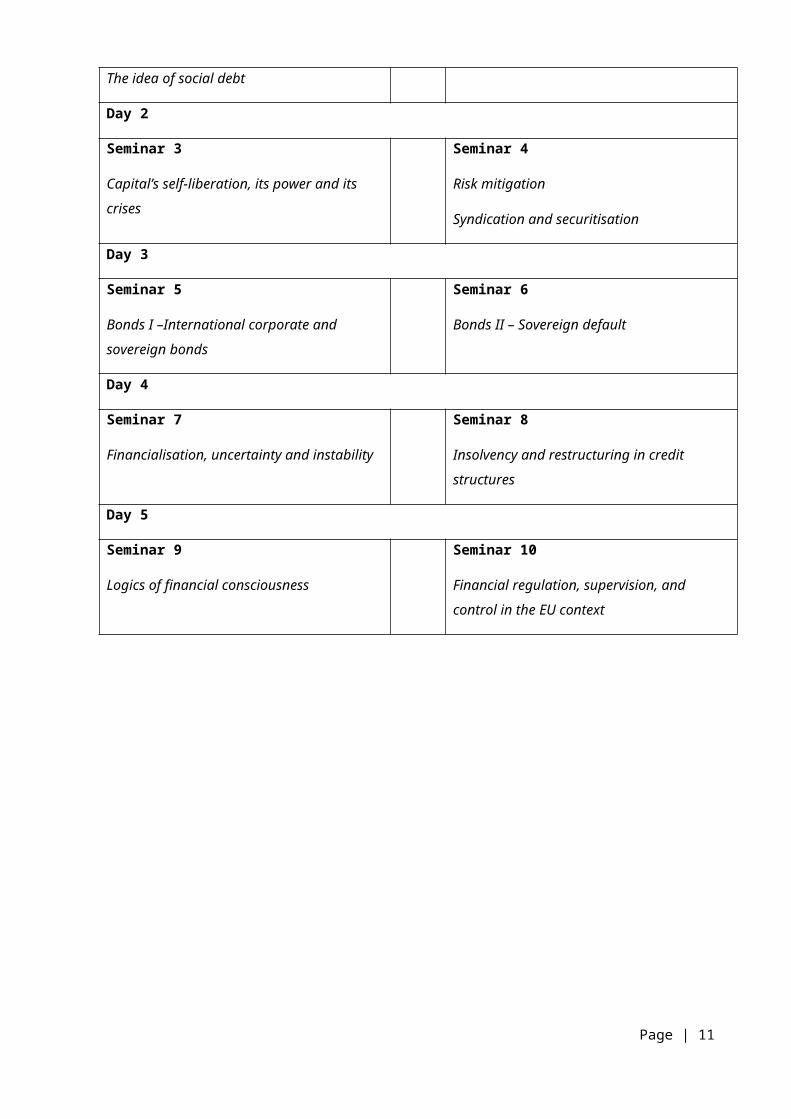

Break

Day 1

Seminar 1

Introduction

The idea of social debt

Seminar 2

The London ‘form’ of credit agreement

Day 2

Seminar 3

Capital’s self-liberation, its power and its crises

Seminar 4

Risk mitigation

Syndication and securitisation

Day 3

Seminar 5

Bonds I –International corporate and sovereign bonds

Seminar 6

Bonds II – Sovereign default

Day 4

Seminar 7

Financialisation, uncertainty and instability

Seminar 8

Insolvency and restructuring in credit structures

Day 5

Seminar 9

Logics of financial consciousness

Seminar 10

Financial regulation, supervision, and control in the EU context

Page | 8

SEMINAR TOPICS AND READING GUIDES

Page | 9

SEMINAR 1 – INTRODUCTION; THE IDEA OF SOCIAL DEBTINTRODUCTIONLet us begin with the following lengthy quotation from Graeber (2011:58-59):

‘The “primordial debt,” writes British sociologist Geoffrey Ingham “is that owed by the living to the continuity and durability of the society that secures their individual existence.” In this sense it is not just criminals who owe a “debt to society” – we are all, in a certain sense, guilty, even criminals.

For instance, Ingham notes that while there is no actual proof that money emerged in this way, “there is considerable etymological evidence”:

In all Indo-European languages, words for “debt” are synonymous with those for “sin” and “guilt”, illustrating the links between religion, payment and the mediation of the sacred and profane realms by “money”. For example, there is a connection between money (German Geld), indemnity or sacrifice (Old English Geild), tax (Gothic Gild) and, of course, guilt.’

In this first seminar, after our introductions, I would like us to explore the interrelations between debt, guilt, morality, discipline, and the symbolic and religious realms. However, in so doing I want you to consider whether the arguments adopted by Graeber and set out in the readings below provide an adequate explanation of the role of finance (and its law) in the world. In short, please consider the possibility that a distinction might be made between debt and finance; a distinction which does not necessarily absolve finance of the theological baggage which attaches to the debt concept, but which marks a transition from one to the other that has constituted our world.

As part of our examination we will consider the law relating to money, the way in which money is constituted as legal tender through debt and finance, and I will draw your attention to the current ideas about ‘money’ and money creation deployed in macroeconomics.

I hope in this first seminar to highlight the way in which the complexity of financial law is mirrored by the richness of its various purported metaphysical underpinnings, metaphysical ‘assumptions’ which tend to be occluded in traditional texts on this subject.

Page | 10

OBJECTIVES• To introduce ourselves and outline the aims of the Module.• To introduce the concepts of money, debt, capital, and finance, and consider certain theoretical

bases of these concepts, in particular:o the nominalist theory of money;

o the credit theory of money;

o the primordial debt theory of money.

DISCUSSION1. You will be asked to introduce yourselves and tell the rest of the class why you have chosen to do the

LLM in International Economic Law Justice and Development. Please be prepared to discuss your motivations for taking this module. I will also be interested to hear about your theoretical interests and inspirations.

2. Introduction to the main themes of the course:

2.1. the nature of debt and finance and its role in society;

2.2. finance structures and financial law;

2.3. instability and crisis, and their legal consequences;

2.4. financial ‘consciousness’ and regulation.

3. Questions for discussion of the introductory readings:

3.1. What is money? What is debt? How are the two related?

3.2. How does the idea of a primordial debt explain the inner nature of money? Is this conception too metaphysical? What objections might be raised against it?

3.3. Anselm of Canterbury (1033-1109) wrote:

“Hold it, therefore, as a most certain truth, that without satisfaction, i.e., without a willing payment of the debt, God cannot let the sinner go unpunished; nor can the sinner attain blessedness, even such as he had before he sinned; for were it so, man would not be restored even such as he was before sin.” (Cur Deus Homo I(XIX))

Having established this debt to God, Anselm introduces God-become-man:

“No man besides Him ever gave to God by dying what he would not at some time be compelled to lose; or ever paid, what he did not owe. But He, of his own accord, offered to the Father what He

Page | 11

would not have ever been compelled to lose; and He paid for the sinners what He did not owe for Himself.” (Id. II(XIX))

It thus seems that Jesus saves so he can bail out sinners. Nevertheless, the links between certain theological logics and primordial debt theories should not be overlooked, though the latter theories tend to argue that theology is first a product of economic primordial debts (in the form of the temple system). Critically discuss these linkages between money, debt, and the divine (which can be found in several religions e.g. the Rig Veda (cf. Graeber infra.)).

3.4. Can we see a relation between debt and meaning or sense? Debts do not exist in nature in the broad sense of that word, but indebted people certainly sense the burden of debt. Could we say that debt is an expression of the sense or meaning of a human situation, and expression of subsisting power relations?

3.5. The following statement by Dicey & Morris (§36-001R) might be considered a general legal definition of the concept of monetary nominalism:

“A debt expressed in the currency of another country involves an obligation to pay the nominal amount of the debt in whatever is the legal tender at the time of payment according to the law of the country in whose currency the debt is expressed (lex monetae), irrespective of any fluctuations which may have occurred in the value of that currency in terms of sterling or any other currency, of gold, or of any commodities between the time when the debt was incurred and the time of payment.”

Critically assess how this concept might apply in times of crisis. What does this tell us about the nature of money and debt?

3.6. Why, when speaking of matters of credit, do we have different terms with different social registers e.g. debt, usury, finance…?

3.7. The word ‘finance’ derives from the Latin ‘finis’ meaning ‘end’. Why do you think this is?

3.8. Is it appropriate to interpret the Credit Crunch using the conceptual apparatus of ‘primordial debt’ (or its offshoots)?

READINGSInnes, J. ‘What is money?’ (1913) 30 Banking L. J. 377

______ ‘The credit theory of money’ (1914) 31 Banking L. J. 151

Théret, B ‘The Socio-Political Dimensions of the Currency: Implications for the Transition to the Euro’ (1999) 22 Journal of Consumer Policy 51-79

Page | 12

FURTHER READINGSAnselm of Canterbury, (1865) Cur Deus Homo (anon. trans.), Henry & Parker, London, I(XIX) ‘That man cannot be saved without satisfaction of sin’, I(XXIV) ‘That so long as man does not pay to God what he owes, he cannot be beatified’, and II(XIX) ‘How the life of Christ is paid to God for the sins of men’.

Aristotle, Politics, Bk.1(9) [1256b40-1258a18] in the Bollingen edition.

Deleuze, G. & Guattari, F. (1988) A thousand plateaus: capitalism & schizophrenia, Continuum, New York, Plateau 9 ‘1933: Micropolitics and segmentarity’

Graeber, D (2011) Debt: the first 5,000 years, Melville House, NY, Ch.3 ‘Primordial Debts’

Keynes, J.M., (1930) A Treatise on Money, Ch.1

Ingham, G. (1996) ‘Money as a social relation’ 54(4) Rev. Social Econ. 507-29

________ (1999) ‘Capitalism, money, and banking: a critique of recent historical sociology’ 5(1) Brit. J. Sociology 76-96

________ (2000) ‘“Babylonian madness”: on the historical and sociological origins of money’ in Smithin J. (ed.) What is money? Routledge, New York

________ (2004) The nature of money, Polity Press, Cambridge

Proctor, C. (2012) Mann on the legal aspect of money, OUP Oxford, Ch.1, Ch.9.

Nietzsche, F (1997) On the genealogy of morality, (Ansell-Pearson trans.) CUP, Cambridge, ‘Second Essay’

Simmel, G. (2004) The philosophy of money, Routledge, London

Spinoza, B. (2001) Ethics, (Parkinson trans.), with a focus on Part I starting with its Appendix and moving back.

Winkler, R. ‘I Owe You: Nietzsche, Mauss’ (2007) 38(1) J. Brit. Soc. Phen. 90

Page | 13

SEMINAR 2 – THE LONDON ‘FORM’ OF CREDIT AGREEMENT INTRODUCTIONIn the first seminar we discussed the relation between debt and money, and the relation between sense and debt. Now we are going to examine a significant interface between ‘debt money’ in general and individual indebtedness: the London form of credit agreement.

I think it very useful to regard the these sorts of contracts as machines which banks plug into sources of capital, and which transmit a flow of that capital to a borrow, and retransmit the capital plus margin (interest) back to the bank and thus the general supply of money/debt. Now nothing is physically flowing in the broad sense, but if we accept the proposal of regarding indebtedness as interposing sense into the human world – in the sense that social relations express something about power relations – then I would like to suggest that we regard the credit agreement as a kind of sense-machine which levies off the sources of capital and transmits it into circulation. In due course we will see that this transmission of flow has become a subsidiary function of the sense-machine, a bit like the steam engine was fixed in place to drive machinery, but soon set itself mobile and was primarily used to drive itself, but for the moment I want to focus on the transmission function.

The reason I have found this sense-machine notion useful in practice is that it holds in mind the idea, for the lawyer constructing it, that just any Heath-Robinson contraption will not do, the sense-machine has to be constructed in the manner appropriate for its functions, first of which in time is tapping into the money markets. Again by analogy, a three-pin plug might work in se, but it is useless when presented with a two-pin socket. My point here is that it is easy to regard the money markets as an homogenous mass of free-floating capital, but in fact this capital is extremely differentiated according to time and price. As to time, the availability of capital is subject to the condition that it be borrowed for a specific time (overnight, 1 day, 3, 6 months, 1, 2, 5, 10 years). This is not an inherent condition – in principle money can always be borrowed, but the market has developed certain ‘terms’ which are generally adhered to, to ease liquidity planning and so reduce cost, with the upshot that borrowing for unusual ‘terms’ comes at a premium. This also leads to the price differentiation – the cost of funds in the market varies every second, and while not by much in normal conditions, when one is speaking of credit agreements starting at €20,000,000, even minor variations can cost €1,000s. For this reason, our sense-machine should be constructed both to draw down capital, but also to withstand the shocks of power black-outs, brown-outs, or sudden surges.

For these reasons this ‘sense-machine’ has developed into a large and complicated piece of equipment. In this seminar I will help you to navigate your way through its mechanisms so that you can understand how the practice and conditions of finance have ‘formed’ this legal document.

Page | 14

OBJECTIVESTo understand why credit agreements take the form they do, by critically examining the context in which they are drafted and operate. In particular:

• to understand the relation between the money markets and the structure of credit agreements;

• to understand the broad classes of finance structures;• to see how disruptions in financial capitalism can feed through into the ‘real’ economy;• to encounter legal doctrine within the context of the practise of a complex legal document.

DISCUSSIONWith reference to teaching document (A) (the Agreement):

1. When the Agreement was signed, how much money did the borrowers receive?2. What is the difference between a term loan and a rollover loan? How does this relate to the

money markets? Why do you think they are treated differently in Clause 4.2(a) (Further conditions precedent)?

3. What are ICE LIBOR and EURIBOR? How do their fluctuations impact on the Agreement?4. During the Credit Crunch of 2008, it became difficult to assess what the LIBOR rate was. How does

the Agreement deal with this circumstance?5. Locate the Market Disruption clause of the Agreement (hint: in the Section marked ‘costs of

utilisation’). One of the banks would like to amend this to cover any notice given by any bank. Is this acceptable?

6. The Company does not want to pay Increased Costs to the banks just because the authorities require banks to comply with prudential standards such as capital adequacy. Advise the Company about its position.

7. What role do the financial covenants play? Are they important?8. Consider the following scenario and advise the Company:

The Company has issued corporate bonds. While its business status is healthy, businesses in its sector are struggling, and Moody’s (the rating agency) has downgraded all the bonds in that sector to B2. In addition, due to market disruption in the Eurozone, the lenders have increased the Margin payable by the Company, which (you admit) the lenders are entitled to do. The Finance Director tells you that due to these factors beyond the Company’s control, almost half of the Group’s earnings before interest, tax, depreciation and amortisation will be eaten up servicing interest payments. The FD believes, however, that the Company has nothing to worry about, as a big order is likely to come in in five months’ time.

Is the FD right not to be worried?

9. What do your conclusions from question 7 indicate about the linkages between financial crisis and the ‘real’ or industrial economy?

10. What is the significance if clause 24 (Changes to the Lenders)? Why is there a difference provided for between assignment and novation of rights?

11. What is the role of:

Page | 15

11.1. the Arrangers;11.2. the Facility Agent;11.3. the Security Agent.

12. The Facility Agent is Bornheimer AG, London Branch. What is a ‘branch’? Does this make legal sense? What problems do you foresee?

13. Under EU law the general position is that a jurisdiction clause which gives jurisdiction to a court in the EU where one of the parties to the relevant agreement is domiciled in the EU is required to meet the requirements of the Brussels I Regulation.

In Mme X v. Rothschild the French Cour de cassation ruled that the unilateral nature of a one-sided jurisdiction clause meant that it did not meet the requirements of the Regulation and was therefore entirely ineffective. Jurisdiction therefore fell to be determined by the fall-back rules in the Regulation as if there had been no jurisdiction clause. The Cour de cassation did not refer the point to the Court of Justice of the European Union. The decision in this particular case will, therefore, not be reviewed.

Review Clause 39 (Governing law) and suggest amendments in light of the above decision. How would you effect any amendments?

READINGSPlease familiarise yourself with, rather than read, the teaching document (A) Multicurrency credit facilities agreement between (amongst others) Phil Bell Group Limited as the Company, and Bornheimer AG, London Branch as Facility Agent.

FURTHER READINGSFinancial Services Authority Final Notice 122702 to Barclays Bank Plc dated 27 June 2012: http://www.fsa.gov.uk/static/pubs/final/barclays-jun12.pdf

Page | 16

SEMINAR 3 – CAPITAL’S SELF-LIBERATION, ITS POWER AND ITS CRISESINTRODUCTION

“where abstract individuality appears in its highest freedom and independence,

in its totality, there it follows that the being which is swerved away from, is all being.”

(Marx reading Seneca in his doctoral dissertation)

In this seminar we are going to explore an alternative interpretation of the role of finance with respect to money (and law) from that offered by the theories we examined in Seminar 1, which latter I am going crudely to lump together under the title ‘Primordial Debt Theories’ or PDTs for ease of reference. Now as we saw, all PDTs do something at once obvious and yet metaphysically imperceptible, in that the raise the status of the primordial debt to the level of Being in a Parmenidean sense – that is, nothing can be or be thought of without ultimate reference to the One Being. In the context on monetary politics as much as theology, we are immediately reminded of Nietzsche’s warning about the linkages between One debt and One guilt in the constituting of modern morality, and of the possibility that a theorisation of debt as primordial condemns every citizen, via the money form, to an irredeemable debt to the issuers of money, and consequently to a profound sense of belonging as indebtedness to a given authority. Furthermore, Being qua Being can be interpreted as Unlimited (apeiron) such that any deviation from its order is affirmed and brought within Being. While Parmenides made no such claim of his Being, which was Limited because it was compete and perfect, we have seen that the money form is both Limited on one face (the nominal value of the debt) and Unlimited on the other (the absolute power of the sovereign). The argument can then be made that all wealth accumulation is always already brought within the primordial debt, and consequently any dealings within any monetary system condemn everyone to participating in the inescapable unity of the Being-sovereign. One can see why some people are politico-philosophically driven to set up their own monetary systems (Système libre-échange in France), or to revert to barter, in order to avoid this consequence.

Page | 17

By utilising this categorical structure of {One substance/multiplicity of modes} PDTs immediately run into the problem of explaining Becoming, both metaphysically in terms of accounting for changes of Being (for only if Being is Limited is it properly complete, according to some Pre-Socratics), and practically, because we pointedly do not still utilise Roman sesterces, or might be citizens of a state that has acceded to the Eurozone. It seems that our ‘primordial debts’ are not that primordial at all, and that peoples come first and they create their monetary systems founded on state debt second. In Feuerbachian terms “man creates God in his own image”.

Yet we are not simply going to consider the case in which humans intentionally constitute monetary debt relations as a kind of debt. Rather, we will examine the particularly pertinent materialist theory of Marx whereby it is capital itself which frees itself from production to constitute the world in its own image. When you read the set texts, the first thing you need to be alive too is the difference that Marx is implicitly drawing between debt (usury, which he admits operated long before capitalism) and finance capitalism, which is specific to the capitalist mode of production itself. PDTs have criticised Marx (cf. Graeber (2011)) for falsely believing that the money form preceded debt in the constitution of economic relations, but to be fair to Marx, he is greatly interested not in debt as one might find in mercantilism or its spatial inverse the temple-market construct, but in the vast accumulation of capital in (associated) private hands which is repeatedly “thrown back” into the system in search of new profit, if necessary rearranging the system in order to achieve this. Marx would view the state monetary construct – the civil or bourgeois economy – as the highest example of Being i.e. a structure which endeavours to persist in its being; to remain the same. But in the wake of Hegel’s Begriff (concept), Marx is alive to the idea of Becoming, and the conception that bourgeois individuals might (r)evolve into social humans, and that civil states might (r)evolve into social becomings, of which capitalism is a dark precursor. As Harvey has maintained, Marx regards capital as not a thing but a process, a coming to be or becoming. If capital stops, it ceases to be capital; an extraordinary vision of what happened when the credit markets seized up in 2008.

OBJECTIVES• To familiarise ourselves with materialist theories of finance, as an alternative to the theories

discussed in Seminar 1.• To consider the reasons for Marx’s assertion that capital sets itself free.• To ascertain the power of finance capital.• To consider and critique the claim that finance capital engenders crises.

DISCUSSION1. Marx spends a long time proving, and being very enthusiastic about, his idea that capital sets itself

free. Engels, who edited this chapter, however seems completely unimpressed that Marx has shown something which to him, as a practising industrialist, is a commonplace – that capitalists accumulate a surplus. Why do you think Marx cared so much about this? [I will suggest my own interpretation in the seminar, drawing on the Further Readings, but the hermeneutic exercise will benefit from everyone’s background and input.]

2. Marx talks both about the way that finance can help reduce turnover times, and how space can be annihilated by time. It seems that capital can relativise time and space. Discuss the implications of such a thesis. Are there other theoretical movements which hold such a view?

3. By what mechanisms in the text does capital institute crises?Page | 18

4. Marx says that “the real barrier to capitalist production is capitalism itself” (Capital III p.250, 259). What might he mean by this?

5. Do you agree with the biocapitalist theory that production has been extended into consumption itself? How is profit derived in this way, and is this profit as ephemeral as the information gleaned by modern technology?

6. Biocapitalism as a theory is a fine example of TINAism (There Is No Alternative) from a left-perspective. In trying to critique capitalism it ends up weaving a glorious conspiracy theory in which nothing can escape a capitalism become ‘One’ or ‘Begriff’. Is this the ultimate form of ressentiment? Discuss.

READINGSMarx, K. (1978) Capital II, Penguin, London, Ch.15 ‘Effect of circulation time on the magnitude of capital advanced’ introductory section, and section 4 ‘Results’

______ (1981) Capital III, Penguin, London, Ch.21 ‘Interest-bearing capital’ and Ch.27 ‘The role of credit in capitalist production’.

FURTHER READINGSHarvey, D. (2011) The enigma of capital and the crises of capitalism, Ch.6 ‘The geography of it all’

Lefebvre, H. (1991) The production of space, Blackwell, Oxford

Marazzi, C (2011) The violence of financial capital, Semiotext(e), Los Angeles, ch.4 ‘The becoming-rest of profit’ pp.43-64.

Marx, K. ‘Differenz der demokritischen and epikureischen Naturphilosophie’ in (1990) Marx Engels Werke Bd.40 Schrifte bis 1844, pp.257-307.

Spinoza, B. (2001) Ethics, (Parkinson trans.), with a focus on Part II Props.7-13, Part III Prop.12 Scholium, and Part IV Props.37-39.

Weber, M. (1968) Economy and Society, California UP, Ch.9.6 ‘Distribution of Power: Class, Status, Party’

Page | 19

SEMINAR 4 – RISK MITIGATION SYNDICATION AND SECURITIZATIONPART A—RISK MITIGATIONINTRODUCTIONIn seminar 2 we examined how the credit agreement was a kind of sense-machine which needed to be constructed in such a way that it could be ‘plugged into’ the supply of finance capital on the money markets, thus permitting capital to flow from its place of accumulation to particular uses in the economy. In effervescent or booming market conditions, banks have been quite happy to proceed to lend using just such a sense-machine; that is, it is enough that there is some binding stipulation that the borrower repay capital and margin, without further risk mitigation mechanisms built into the sense-machine. Indeed, just before the Credit Crunch, banks all but dispensed with lawyers altogether, and began lending on the basis of fundable term sheets – literally 1-2 page documents specifying the parties, the loan amount and margin, and date of repayment, and the odd additional condition which the banks felt important. These were still binding contracts, but given the sums involved they did appear from a lawyer’s perspective to be close to lending billions off the “back of a fag packet”. Analysis of historic bubbles (such as the “South Sea Bubble”) unsurprisingly indicates similar tendencies in which the mania to throw money into the ring of investment was so great that investors all but dispensed with legal formality, scribbling the heads of agreement on coffee house napkins, scraps of paper, or whatever else came to hand.

At the other extreme, just after the bubble bursts, lenders tend to rush to the law and demand the maximum protection conceivable before they lend (or enforce against sums already advanced). We will see more about this when we consider insolvency in financial law, but between these two extremes it is generally the case that lenders will demand some risk mitigation mechanisms in order to protect as much of their capital as possible if a borrower defaults. If we are realistic, however, we should note that most modern lenders are not just interested for their own part in mitigating risk, but, because they always have a view to distributing their assets (the credit advanced) to other investors, they are also interested in satisfying potential transferees of the asset that the asset is indeed a ‘safe investment’.

Potential transferees naturally will be primarily interested in the economic health and prospects of the borrower – they would rather just be repaid – but they are secondarily interested in risk mitigation, and in the seminar we will outline some of the classic methods of protecting capital advanced: namely security interests, guarantees, and subordination. Thus if we extend our sense-mechanical concept further, the

Page | 20

credit agreement must not only be constructed so as to appropriately plug into the power (potentia) of capital, but it must also be drafted such that it is able to draw down the authority (potestas) of written law, such that, when something goes wrong, the lender is able quickly to return to itself as much value as possible. This is an important feature of financial capitalism: as Andrew Mellon, the US Treasury Secretary during the Great Crash of 1929 and one of America's richest men, observed: in a crisis assets return to their rightful owners. As Keynes put it in greater detail:

“There is a multitude of real assets in the world which constitute our capital wealth – buildings, stocks of commodities, goods in course of manufacture and of transport, and so forth. The nominal owners of these assets, however, have not infrequently borrowed money in order to become possessed of them. To the corresponding extent the actual owners of wealth have claims, not on real assets, but on money. A considerable part of this ‘financing’ takes place through the banking system, which interposes its guarantee between its depositors who lend it money, and its borrowing customers to whom it loans money wherewith to finance the purchase of real assets. The interposition of this veil of money between the real asset and the wealth owner is a specially marked characteristic of the modern world.” (Essays in Persuasion (1932:169))

These quotations point us to an important underlying fact about risk mitigations which lawyers, obsessed as they are with the pomp of the court, might perhaps overlook. Lenders are not interested in courts, they do not want to go anywhere near one; they do not even want to have their right to real assets questioned. It is not a question of proving title to property; it is a question of being able with the minimum of time and effort to assume the property of the borrower in satisfaction of a liquidated debt claim. By way of simple example, if a mortgagor defaults, the mortgagee ideally wants to foreclose on the mortgaged land, evict any tenant, and realise its value (sell it), as quickly as possible. Against this demand for satisfaction, the credit agreement must also contend with the singular demands of the borrower (e.g. the security conditions on land should not prevent the use of the land), the particular demands of legal practicality (how does one enforce against an intangible asset like a brand name?), and the general demands of public policy (should immediate foreclosure be tolerated?). The corollary demand – that the lender is uninterested in assets which cannot be easily enforced against – does not follow however. This latter depends on the risk appetite of the lender: in the aftermath of the Credit Crunch I experienced many lenders who purported to take security which they were advised was unenforceable – but they took it nonetheless. Ask yourself why they might do this.

This seminar will attempt to place these issues within the context of the currently practised financial law.

In the further readings I have referred you to the EU Financial Collateral Directive 2002 (as amended by 2009/44/EC, the FCD) which somewhat cuts through the security principles we will discuss in this seminar. In essence FCD provides for rapid and non-formalistic enforcement procedures designed in part to limit contagion effects in the event of default by one of the parties to the arrangement. Member States may not make the creation, perfection, validity, enforceability or admissibility of a financial collateral arrangement dependent on the performance of any formal act. In addition, Member States must ensure that the collateral taker is able to realise financial collateral in one of the following manners:

• if it concerns financial instruments by sale or appropriation and by setting off their value against, or applying their value in discharge of, the relevant financial obligations;

Page | 21

• if it concerns cash by setting off the amount against or applying it in discharge of the relevant financial obligations;

• if it concerns a credit claim by sale or appropriation and by setting off their value against, or applying their value in discharge of, the relevant financial obligations.

• Appropriation is possible only if this has been agreed in the arrangement. The FCD defines:• Financial collateral arrangement: a collateral arrangement in the form of cash or financial

instruments, i.e. a title transfer of ownership or a security financial collateral arrangement.• Credit claims: pecuniary claims arising out of an agreement whereby a credit institution grants

credit in the form of a loan.

It is worth considering the policy pressures that led to the FCD being instituted, and the manner in which, within its financial domain, it attempts to brush aside national rules on security. I related matter is the doctrine of set-off and netting, which is quite baroque in its subtleties and a good indicator of the public policy attitude to debt and security in a given jurisdiction. For this, see Goode (2008) in the Further Readings below.

OBJECTIVES• To introduce the practice of granting security, guarantees, and accepting subordination in the

context of financial law.• To highlight major issues in the English and cross-border context.• To consider a case study regarding security in order to grant a ‘flavour’ of how legal issues and

international finance encounter each other (the critical legal theory idea of assessing the practise of law).

• This Seminar cannot possibly hope to treat of all the legal issues in sufficient detail – the law of security would require a module all of its own. It is designed to highlight the financial interface between law and practice.

DISCUSSIONWith reference to teaching documents (B) (and teaching document (A) to the extent relevant), consider the following questions:

1. What are the key practical considerations for a bank taking security?2. How does a company ‘organise’ property in a way that is different from, say, a natural person such

as Mr Bloggs? Think firstly about the way that a company holds as assets as a separate ‘stock’ from the providers of capital. Then think about how this is represented as a division between debt and equity. It has been argued that the key benefit of the company is this organisation of business property. Why do you think this is a benefit (think for example about liquidity and risk transformation)?

3. Consider the merits and problems of taking security over shares in Group companies as opposed to tangible corporate assets.

4. The Company already has a loan agreement with another bank which is based on the London form of credit agreement. What would you look for in this loan agreement to check whether or not there are any obstacles to the Company granting security?

Page | 22

5. Suppose that the security is for “all moneys” rather than the “Secured Liabilities”. Do you foresee any problems with this in non-common law jurisdictions?

6. The security is over a number of contracts and receivables. The Company does not want to give any notice of the security interest to the obligors/customers on the contracts because it wants to continue to operate the administration of the accounts with the obligors/customers itself. The obligors on the contracts are located in a number of other jurisdictions. In principle you are happy with this, but do you see any problems?

7. Why is the security granted as fixed and floating charges?8. The banks want to amend this agreement so that the debtor’s book debts are subject to a fixed

charge? Do you think this will work?9. If the banks are taking first security, why do they care to restrict the Company from granting lower

ranking security to third parties?10. Who is the Receiver referred to in document (B)?11. The banks are taking security granted by Group members based in multiple jurisdictions. The

banks’ agent, who has only ever worked in the English market before, wants to employ a trustee of the security, as this has worked well for him in the past. Do you see any trouble with this proposal?

12. One of the Company’s assets, an industrial lathe, is located in Germany. Is this security agreement valid with respect to it?

READINGSFamiliarise yourself (rather than read) with the structure of teaching document (B): Security Agreement.

FURTHER READINGSRe Spectrum Plus Ltd [2005] UKHL 41, [2005] 4 All ER 209 – a leading case on the problem of securing book debts.

EU Financial Collateral Directive 2002 [Directive 2002/47/EC of the European Parliament and of the Council of 6 June 2002 on financial collateral arrangements, as amended by 2009/44/EC]

Report from the Commission to the European Parliament and the Council Evaluation Report on the Financial Collateral Arrangements Directive (2002/47/EC) COM/2006/0833 final

Goode, R., (2008) Legal Problems of Credit and Security, Sweet & Maxwell, London – excellent though very detailed for the purposes of this Module.

McEndrick, E. (2010) Goode on Commercial Law (4th ed.), Penguin, London, Part 4 ‘Secured Financing’ – a good practical introduction to security in a commercial context.

Page | 23

PART B—SYNDICATION AND SECURITISATIONINTRODUCTION

“For a machine constructed by man’s art is not a machine in each of its parts. … But natural machines, that is, living bodies,

are still machines to their least parts, to infinity.”

Leibniz, Monadology §64

We have deployed the concept of a contract as a kind of sense-machine which we construct and plug into various power sources to transmit effects. So we saw how the credit agreement is designed to plug into the money markets and draw off capital power (potentia) according to the timescales operating there, and we saw how the credit agreement achieves risk mitigation by attempting to draw down as much legal power (potestas) as possible should things go wrong. These have both been aspects of the machine which consider incoming power and the most efficient ways to draw it off, but now we are going to look at our sense-machine’s outputs. Our focus, however, is not on the obvious output of finance capital to the borrower’s use, but on an output of far greater interest to financial institutions: the claim to a borrower’s debt as the product of the sense-machine.

From this point of view, the capital advanced by the sense-machine becomes of almost secondary importance to the financial titles it produces. Why? Because once the capital is advanced it is tied up in the (industrial) production cycle, usually as plant and machinery, land, or raw materials, until such time as provided for in the repayment schedule as the borrower makes a profit and can repay the capital plus margin. In other words, the capital has got stuck, and when capital stops moving it ceases to be capital. But our sense-machine has developed a clever trick: though it cannot get the advanced capital moving while it is tied up in productive assets, it can get the claims to repayment and margin moving – it can sell these claims as products of the lending process, and use the proceeds of this sale to fund other loans to other borrowers, the claims to which it can sell on, with increasing velocity in ever increasing amounts. By way of example, a bank might lend £100 to Mr. X on the promise he repay £1 per month interest, repayment n of the principal sum in 12 months. Now for each of those 12 months the bank has the right to receive £1 and it is this ‘flow’ of £1s that is valuable and can be sold. Put enough such flows together and you can sell in quite an advantageous way. This in nuce is the ‘originate to distribute’ model that led in no small way to the Credit Crunch.

I really want to emphasise the way in which legal documentation has itself become a product here; a process we might call commodification. It is not particularly new that a legal document should become a commodity, for bank notes qua promissory note are the premier example of such a process. What is new, at least if we regard the last 30 years as recent, is that the evolution which has led IOUs declaring a promise to pay a sum endorsed on the face to become tradable as currency has been extended to legal documentation of such complexity that a whole industry has grown up of lawyers drafting the documents for credit parties and, importantly, of third parties who are paid to read these documents and assess their credit worthiness for the market. These latter are called rating agencies.

These structures are complicated for trained finance lawyers too, and mistakes and miscomprehension are not uncommon given the contradiction between legal complexity and the increasing velocity of capital circulation that drives these deals. In practise I have found the first stumbling block of many trainees is not

Page | 24

so much the volume of information involved, but the unawareness that these structures tend to operate on multiple ‘plateaux’, such that changes at one level may or may not produce changes at other levels, and that the borrowers at the bottom of a structure may be completely unaware that their debt has been transferred to a new entity, sliced up, sold to multiple institutions, which themselves may have used the claims in weird and wonderful ways. Financial law has in a certain manner become ‘baroque’ (cf. Deleuze (1986)), the folds of legal sense may be unfurled only to reveal countless other folds and complications in a seething ferment of sense. The ‘mechanical’ contract has been raised up by its internalisation of production in itself into a multiplicity of pleats of sense, and has become, after a certain fashion, ‘alchemical’.

OBJECTIVES• To introduce students to the financial structures known as syndication and securitisation and the

reasons for their development;• to review some typical legal documentation related to these structures, with a particular focus on

the contract known as an intercreditor agreement;• to highlight some of the key legal issues which affect these structures; and• to discuss these structures’ role in the Credit Crunch.

DISCUSSIONHere are some questions to guide our exploration of these complicated structures:

(I) Syndication1. What is loan syndication?2. Why did syndication develop?3. In what ways do syndicated credit agreements differ from the traditional bilateral loan agreement

between one bank and one borrower? Consider the effect of syndicate decision making and facility agency. Why would any bank transfer its right to make decisions in this way?

4. Can a borrower restrict who its lenders might be?5. Intercreditor agreements are normally kept secret as between the bank syndicate and its agents;

borrowers only rarely get to review this document. Discuss why and whether this is desirable. 6. Pay attention to the way that cash flows through a syndicated credit structure. What is a

waterfall? What happens when there are insufficient funds?7. What are the differences between participation, sub-participation, beneficial participation (via

trust), and synthetic participation (via a total return swap)?8. Discuss the legal aspects of the following scenario with particular focus on the legal relations

between the parties (you can assume the valuer’s work fell well short of the required standard):

Bornheimer Bank, London Branch lends €100m to Borrower which uses the entirety of the funds to purchase various English real estate. The loan is secured by first ranking mortgage against this real estate. A local valuer “Krank Fight” employed by Bornheimer values the land in aggregate at €150m. Bornheimer syndicates its loan in its entirety to Lenders, and remains as facility and security agent. Borrower defaults, Bornheimer enforces against the security, but, on realising its value, recovers only €75m for the Lenders. It is subsequently discovered that Krank Fight misvalued the real estate because some of the land was historically polluted

Page | 25

– a fact readily discoverable by the normal Envirocheck searches. The Lenders determine to sue Krank Fight for their losses.

(II) Securitisation9. What is securitisation? What are receivables?10. Why did securitisation develop?11. Explain the following jargon: ABS, CDO, RMBS, CMBS, SPV.12. What is the importance of a ‘true sale’ and its relation to capital adequacy?13. How might an originator achieve ‘credit enhancement’?14. What is tranching and how is it achieved?15. Consider the role of:

a. Credit rating agencies;b. Swap counterparties (interest swap with the SPV); andc. Monoline insurers

16. Discuss the legal aspects of the following scenario, based on real facts with particular focus on the liability of the rating agency:

NB. These facts are only indirectly linked to the securitisation structure but are based on a rare occurrence of some quite egregious facts ending up in a published court decision. They illustrate the distribute aspect of securitisation without the origination (the product relates to market indices, not specific receivables), but serve to emphasise the distributor-rating agency nexus and the liability of the rating agency (or lack thereof) with respect to investors.

These facts involve that now clichéd entity the "complex financial product" which no-one completely understood. A constant proportion debt obligation (the CPDO) had been developed by Tolomei Bank to track certain indices, with party and counterparty to the CPDO having to pay over a specific sum to the other as the indices fluctuated. Tolomei marketed the CPDO to Local Government Financial Services Pty ("LGFS"), who acted as a kind of investment broker (thus as agent) for various local councils.

Tolomei needed to obtain a AAA credit rating from a rating agency Bogstandard & Poorer (B&P) in order to satisfy the investment criteria of the local councils. When Tolomei approached B&P and asked them to rate the product, B&P initially decided to base their rating calculations on the assumption they had already used for a similar product that the volatility of the reference indices was 32%. On this basis they initially concluded that the CPDOs could not be rated AAA. A flurry of correspondence occurred in which Tolomei convinced B&P that the correct volatility assumption was 15% as this was the historic maximum volatility for the reference indices. This was simply false.

B&P accepted Tolomei’s representation as to volatility without verifying it, and proceeded to model the product on this basis. The CPDOs were granted AAA rating and B&P released a letter to Tolomei to accompany the financial prospectus stating that this indeed was its authorised rating.

The local councils purchased the CPDOs on LGFS' advice. From the beginning Tolomei began calculating the sums owed under the contracts by reference to its own models, which assumed

Page | 26

a 29% volatility. Very quickly the local councils began having to pay out large amounts of money. As market conditions became choppier approaching the Credit Crunch, the actual volatility of the indices was around 32%. The local councils sued B&P, LGFS, and Tolomei inter alia for misstatement and misrepresentation.

READINGSPlease skim through the teaching documents marked (C) and (D) which I have put up on Moodle, focusing on teaching document (C(i)) which is the intercreditor agreement.

FURTHER READINGSThe following cases are particularly relevant to this seminar:

Australia

Bathurst Regional Council v Local Government Financial Services Pty Ltd and Others (No 5) [2012] Federal Court of Australia 1200

Esanda Finance Corporation v Peat Marwick Hungerfords [1997] HCA 8

England & Wales

BBL v Eagle Star [1995] 2 All ER 769, CA, reversed in part in [1997] AC 191, HL, where it was reported as South Australia Asset Management Co. v York Montague Ltd.

Caparo Industries plc v Dickman [1990] UKHL 2

Helmsley Acceptances v Lambert Smith Hampton [2010] EWCA Civ 356

Interallianz Finanz AG v Independent Insurance Company Ltd [1997] EGCS 91

European Commission

Rating Agencies page: http://ec.europa.eu/internal_market/rating-agencies/index_en.htm

Commission Delegated Regulation (EU) No 946/2012 of 12 July 2012 supplementing Regulation (EC) No 1060/2009 of the European Parliament and of the Council with regard to rules of procedure on fines imposed to credit rating agencies by the European Securities and Markets Authority, including rules on the right of defence and temporal provisions

United States (NY)

Ultramares Corporation v. Touche, 174 N.E. 441 (1932)

See also:

S. Jones ‘When Junk Was Gold’ , Financial Times (London), 17/10/ 2008, p. 16.

C. Gerner-Beuerle, ‘Underwriters, Auditors, and other Usual Suspects: Elements of Third Party Enforcement in US and European Securities Law’ (2009) 6 European Company and Financial Law Review 493- 499.

•

Page | 27

The following texts might be read as different takes on the relations between mechanism and the internalisation of mechanism in either a molecular unity or a multitude, depending on the philosophical perspective. They are very difficult texts and consequently quite appropriate to our subject matter.

Deleuze, G. (1986) The fold: Leibniz and the baroque, Athlone Press, London

Hegel, GWF. (1989) Science of Logic, The doctrine of the Notion, s.II ‘Objectivity’.

Page | 28

SEMINAR 5 – INTERNATIONAL CORPORATE AND SOVEREIGN BONDSINTRODUCTIONIn this seminar I will introduce international bond issues. Bonds can be thought of as very standard-form loans i.e. they are the same thing legally as parts of a loan under a credit facility agreement but they are so standardised that investors can exchange them readily on a like-for-like basis, the main variables of interest being the price of the bond and chances of it being repaid on maturity. It is a question liquidity: at one end of the spectrum you might have a highly negotiated and individual private equity loan to a corporation which requires lawyers to spend hours on due diligence before approving their client’s purchase, and at the other end, we have bonds which in principle should only require limited legal input: the investor need only consider micro- and macroeconomic factors.1 In between these two is the London form of credit facility agreement.

By international bonds I make an important distinction from domestic bonds. The difference has nothing to do with who issues the bonds—both corporations and states can issue international bonds and/or domestic bonds. The essential difference is that international bonds are denominated in a currency other than the issuer’s domestic currency, and commonly (but not necessarily) these bonds are traded on an international market. Bonds denominated in a foreign currency—such as Argentinian bonds denominated in US Dollars and traded in New York or London— are called Eurobonds. ‘Eurobonds’ has nothing to do with the Euro (the currency of the Eurozone) and is a term that developed in the 1970s. By contrasting example, were Argentina to issue peso-denominated bonds to Argentinian investors this would be a domestic bond issue.

The reason I will treat corporate and sovereign bonds together is historical—firstly, the techniques of bond issuance and dealing with defaults have been largely forged in the private sphere especially during the first wave of financialisation during the later nineteenth century, but primarily because corporate defaults are more common and more complicated than state defaults. Secondly, moral notions of debt and paying one’s way in the world have been transposed from the private sphere onto states, as the above quotation from Teddy Roosevelt indicates. You will of course be sensitive to the underlying tone of that ‘threat’; the moral symbolism is clothing for US policy instrumentalism towards Latin America in particular. We will look at this in the following seminar.

1 When debtors are at risk of default, however, the lawyers become heavily involved. Vulture funds may still wish to buy the bonds

Page | 29

For this seminar I am going to introduce the basic structures and relevant points of contest in bond issues and show some of the similarities between corporate and sovereign bond documentation, before bringing out some distinctions. We will then plunge more deeply into sovereign debt issues in preparation for our discussion of the law, socio-economics, and politics, of sovereign default.

As I say, we will run this seminar and the next together—the readings for this seminar are highly relevant to the next also.

READINGSBuckley, R. (2010) ‘The Bankruptcy of Nations: Let the Law Reflect Reality,’ 29(6) Banking and Financial Services Policy Report

International Law Association (2010) ‘State insolvency: Options for the Way Forward,’ Report of the ILA Sovereign Insolvency Study Group, ch.1-2.

Weidemeier, M. (2013) ‘Sovereign Debt after NML v Argentina,’ 8(2) Capital Markets Law Journal

Wong, Y (2012) Sovereign Finance and the Poverty of Nations: Odious Debt in International Law, Northamption Mass.: Edward Elgar, ch.2

FURTHER READINGSCross, K H (2011) ‘Investment Arbitration Panel Upholds Jurisdiction to Hear Mass Bondholder Claims Against Argentina,’ 15(30) American Society of Int’l Law (ASIL) Insights available at http://www.asil.org/insights/volume/15/issue/30/investment-arbitration-panel-upholds-jurisdiction-hear-mass-bondholder

Herman, B, Ocampo J, & Spiegel, S (2010) Overcoming Developing Country Debt Crises, Oxford: OUP ch.1 and 17

UNCTAD (2011) ‘Sovereign debt restructuring and international investment agreements,’ IIA Issues Note No.2

Philip R Wood (2007) International Loans, Bonds, Guarantees and Legal Opinions, London: Sweet & Maxwell – now slightly outdated discussion of the mechanics of bond issue.

Page | 30

SEMINAR 6 – SOVEREIGN DEFAULTINTRODUCTION

‘If a nation shows that it knows how to act with reasonable efficiency and decency in social and political matters, if it keeps order

and pays its obligations, it need fear no interference from the United States’

Pres. T Roosevelt, 20 May 1904

In the previous seminar I introduced bond finance and sovereign bonds—that is, bond finance that is used by states to fund their ongoing spending (known as gilts in the UK, and T-bills in the US). In fact, I say spending but a significant portion of gilt issuance takes place to refinance existing indebtedness. What this means is that a state may have to repay the principle on certain 10 year bonds on a given date. In order to find this money the state may well borrow it from private persons by issuing new bonds and it will try an ensure that this money is borrowed and available for use on the day the existing indebtedness is due, and that the new debt is on the same terms (or better) than the debt that is being repaid.

A major problem arises when the state cannot find new money to refinance its indebtedness, or, more likely, the terms of available refinancing are significantly worse than those of the existing debt. The principle term that varies, as we have seen, is the price (‘the yield’) which is the actual price the purchaser pays for the bond not necessarily the nominal price written on the bond. In a situation where a state is considered likely to not repay the debt it owes investors will only be prepared to invest at a significant discount to the nominal value of the debt. Such bonds are commonly called ‘junk,’ and more technically known as ‘high yield’. In such a situation a state may well have to issue vast amounts of debt to receive sufficient actual funds, a growth in indebtedness which very quickly becomes unsustainable. At this point the state is on the verge of bankruptcy.

The so-called bankruptcy of states, however, is legally incongruous. The fact that lawyers have applied the private law mechanisms of bankruptcy to a public entity should already indicate the problematic—a private bankrupt is rightly or wrongly deemed the sole cause of her own loss, is stripped of her non-essential assets, declared bankrupt, and then pushed to re-enter the market place. A state however, is almost never the sole author of its economic collapse, may only own ‘essential’ assets, contains very many innocents who may be severely affected by anything the state agrees to, and it is legally assumed (though it is a vexed question) that a state cannot actually be liquidated like, say, a corporation.2 The international politics of sovereign default drive this incongruity to extremes.

2 Ultimately it may always print coin to repay debts, and its principle asset (its territory) is likely to exceed liabilities.

Page | 31

The objective of this seminar is for you to discuss further the legal, economic and political issues raised in the previous seminar. We will explore in detail the landscape of international sovereign financing and the problems posed by the current international legal framework (or lack thereof) relating to sovereign debt restructuring.

The following exercise assumes you prepared the reading for the previous seminar and builds on it.

SEMINAR EXERCISEPlease read these articles (in your readings):

Elaine Moore ‘International Bankruptcy Back on the Agenda’ (Financial Times 29 October 2014); and

Jose Antonio Ocampo ‘The UN Takes the First Step to Debt Restructuring’ (Financial Times 29 October 2014),

and come prepared to debate the issues raised by the articles. In particular, you will be asked to discuss and explain the current regime for sovereign debt restructuring and debate the advantages and disadvantages of the contractual approach to sovereign debt restructuring versus the statutory approach to sovereign debt restructuring.

Seminar questions:

1. What is sovereign debt?

2. Why do countries get into debt? Is sovereign debt necessarily a bad thing?

3. What are the categories of sovereign debt and does it make a difference to their governing legal framework? Can excessive domestic debt lead to sovereign debt crisis?

4. What are the sources of sovereign finance today? What’s the difference between official and commercial debt?

5. What are the implications of imprudent sovereign borrowing and lending?

6. What is odious debt?

7. What happens when a sovereign state cannot repay its debt?

8. Considering examples from your own knowledge, how has international politics affected sovereign indebtedness, from colonialism to the Bretton Woods world order to today?

9. How is sovereign debt restructured? What is the current international framework for restructuring sovereign debt?

10. What are the differences between a contractual approach to sovereign debt restructuring and a statutory approach? Which is preferable for resolving sovereign debt crises?

11. How are human rights affected by sovereign debt restructuring and how might they be protected?

Page | 32

SEMINAR 7 – FINANCIALISATION, UNCERTAINTY AND INSTABILITYINTRODUCTION

“…in knowing nothing, [one] knows in a way that surpasses understanding.”Pseudo-Dionysius

During the early modern period natural philosophers developed the concept of the general equilibrium, though they used theological names for it, such as ‘divine immutability,’ infinite ‘power,’ ‘constancy.’ The basic concern of these thinkers was to reconcile the apparent change of the universe with the perfection of God, perfection being understood as completion. There was nothing God lacked and nothing God had not already ordained for the universe, and so the events of our world ought to be reconcilable with a set plan in the divine intellect. Some philosophers, such as Newton, continued to believe that God could miraculously intervene in the universe, but others, termed ‘Spinozists’ by their critics, followed the logic of divine perfection to its conclusion of a completely determined and perfectly ordered universe, in which change was explicable and indeed predictable through the development and application of natural laws.

Parallel to the idea of divine immutability came the idea of divine omniscience, which translated into a theory of knowledge which expressed the general equilibrium. While every finite thing in the equilibrium knew a certain amount about its world, its very finitude explained the partiality of its ignorance. Finitude was equated with ignorance, but on condition also that the whole as whole knew all of its parts and maintained the order. There was thus a limit case of knowledge which was ascribed to God.

In essence, the concept of general equilibrium might be regarded as the view that given a lawful physical system, any change in that system would be instantaneously compensated for by that system to preserve equilibrium. An easy example from statics would be an incompressible fluid – if you push one part of the fluid, the other parts will move out of the way, but the general volume of the fluid will not change. This general equilibrium view is more complicated than this however – it holds not only that the same extension (e.g. volume) will be maintained, but also that the same overall motions (and so forces) will be maintained i.e. we have a dynamic equilibrium. When the organisers of Davos’ World Economic Forum 2013 chose the epithet ‘Resilient dynamism’ I suggest this is what they imply – a system which changes in order to remain the same: a Being or One which subsists even as it appears to change.

This little excursion into some interesting metaphysics is important because the general equilibrium concept of classical physics was transposed readily into economics, unsurprisingly along with all the

Page | 33

theological deadweight too. We cannot blame C18-19th economists for seeking to apply successful physical methods to economic matters, provided they were open about it, especially because otherwise their task would have become impossible. Marx, for example, is completely explicit3 that he assumes a general equilibrium for methodological purposes (a) because he is critiquing his classical predecessors who implicitly assumed the same equilibrium, and (b) because if he did not hold certain things constant readers would not be able to see the ‘generality’ of the laws that Marx was able to derive about economic matters. This does not mean that Marx was not aware that economic systems did not (r)evolve; just that drawing the line between his self-proclaimed ‘scientific’ analysis and his metaphysical commitment to transformation of one’s world can be difficult, especially when Marx starts referring to ‘iron laws’ and ‘gravity asserting itself’. Others went further, with Adam Smith asserting that markets via the infamous ‘invisible hand’ would naturally move to their natural equilibrium state without the need for outside intervention (i.e. state regulation). To be fair to Smith, let’s quote him in full:

The natural price, therefore, is, as it were, the central price, to which the prices of all commodities are continually gravitating. Different accidents may sometimes keep them suspended a good deal above it, and sometimes force them down even somewhat below it. But whatever maybe the obstacles which hinder them from settling in this centre of repose and continuance, they are constantly tending towards it. The whole quantity of industry annually employed in order to bring any commodity to market, naturally suits itself in this manner to the effectual demand. It naturally aims at bringing always the precise quantity thither which may be sufficient to supply, and no more than supply, that demand. (Smith (1776), Vol. I, p. 65).

Consider how this taps into the idea of divine omniscience: the merchants are all parts of the market and as such they cannot know the status of the whole market know, nor in the future, but the whole market as such can be relied upon nevertheless to find its natural level, regulate itself, and ensure the greatest good possible. The deeper thought process implies that we do not need to know or worry about everything, and may pursue our individual desires, because the mind controlling the invisible hand is tending to us like the good shepherd. Incidentally, I cannot emphasise enough the gravitational analogy Smith is deploying and your need to critique that deployment to the extent that it is not mere metaphor but is actually, shall we say, ‘exerting its own force’ on Smith’s conceptualisation. Marx uses the gravity metaphor too (Capital I p.168).

The problem when applying iron laws to market behaviour is that even though certain laws do apply (let’s be clear about that), their predictive capacity collapses within moments. Actually Newton already knew this (a case of selective pilfering by economists). Newton had established the laws applicable when one body orbits another, and so naturally moved to consider the case of three bodies in an orbit. His mathematics established that with just three bodies apparently random behaviour ensured, with planets spinning out of orbit, or smashing into each other, and he could not find the law that explained this. Physicists and mathematicians have spent the following centuries investigating this ‘three-body problem’ and from it the subjects of non-linear dynamics and chaos theory were born.

Now if we consider a market, with all the variables involved, we start to guess that ‘resilient dynamism’ is a bit of a fairy story. Markets could do almost anything, including explode, and as we have seen this is what

3 Cf. e.g. Capital I p.708, Capital II p.1-2, Grundrisse p.89-100. Strictly the general equilibria are modified according to the components of the economy Marx is focusing on.

Page | 34

they do to the surprise of almost everyone, however well-schooled in the ‘science’ of economics. This surprise comes from a risk inherent in economic ‘scientism’, namely that once a beautiful law is established, deviations from this law are deemed aberrations to be ignored, or at best accounted for by special factors added in as ‘transaction costs’, ‘imperfect information’, or politically as ‘state meddling in the private sector’. Such an attitude is deeply unscientific; scientists ought (and do) jump at the strange and inexplicable, and try and make their theories account for them, rather than attempting the Sisyphean task of making the world fir their theories. Now, one thinker pertinent to our investigations of financial markets who embraced the problematic of instability and uncertainty is JM Keynes, whose ideas you will be reading through his interpreter Hyman Minsky. Keynes was not the first person to appreciate the difference between a lack of knowledge and a knowledge of nothing, but he puts it in quite concise terms drawing on his investigations into the theory of probability:

“By ‘uncertain’ knowledge, let me explain, I do not mean merely to distinguish what is known for certain from what is only probable. The game of roulette is not subject, in this sense, to uncertainty….The sense in which I am using the term is that in which the prospect of a European war is uncertain, or the price of cooper and the rate of interest twenty years hence…. About these matters there is no scientific basis on which to form any calculable probability whatever. We simply do not know. Nevertheless, the necessity for action and for decision compels us as practical men to do our best to overlook this awkward fact and to behave exactly as we should if we had behind us a good Benthamite calculation of [utility].” Keynes (1937) 51 Q. J. Econ. 213-214.