controlling preview steps in the control process three types of control characteristics of effective...

TRANSCRIPT

Controlling

Preview

Steps in the Control Process

Three types of Control

Characteristics of Effective Control Systems

Financial Controls a. Financial Ratios used in Ratio Analysis b. Financial and Operating Budgets c. Nature of Budgeting Process

Assoc.Prof.Dr.B.G.Çetiner

Other nonfinancial Controls

Controlling

Definition of Controlling

Assoc.Prof.Dr.B.G.Çetiner

Compelling Events to Conform to Plans

Steps of Controlling

1. Establishing Standards

Planning

2. Measuring Actual Performance

3. Comparing Performance with Standards

4. Corrective Action

Controlling

Controlling

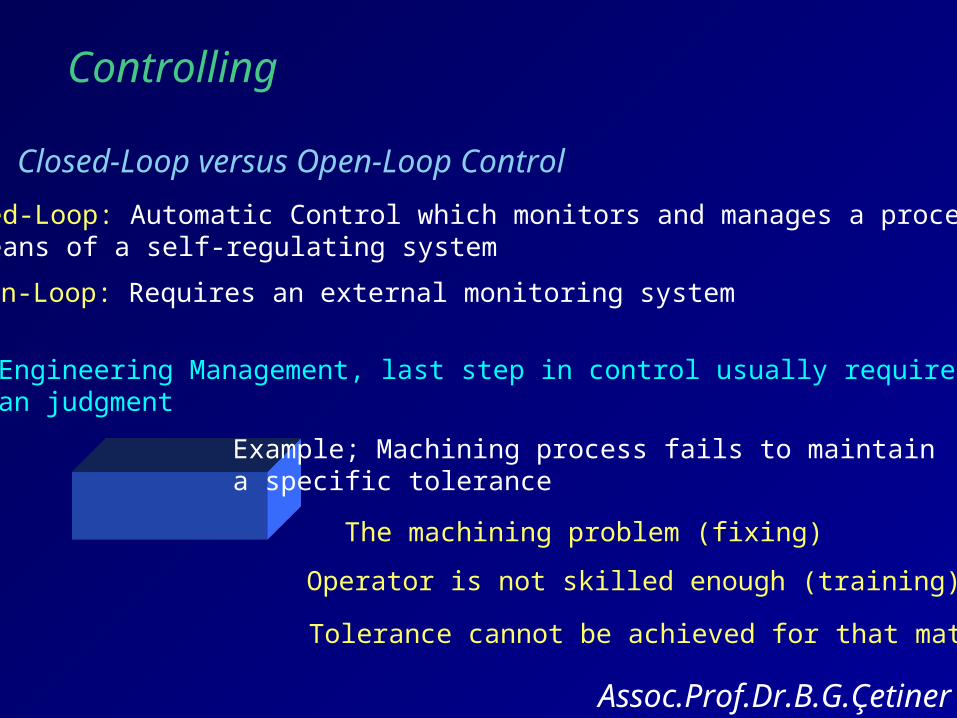

Closed-Loop versus Open-Loop Control

Assoc.Prof.Dr.B.G.Çetiner

Closed-Loop: Automatic Control which monitors and manages a process by means of a self-regulating system

Open-Loop: Requires an external monitoring system

In Engineering Management, last step in control usually requires Human judgment

Example; Machining process fails to maintain a specific tolerance

The machining problem (fixing)

Operator is not skilled enough (training)

Tolerance cannot be achieved for that material

Controlling

Three Perspectives on the Timing of Control

Assoc.Prof.Dr.B.G.Çetiner

Feedback Control: Thermostat example

Screening or concurrent control: Step-by-step control

Feedforward (or preliminary or steering control): Predict the impact of current actions or events on future outcomes and adjust the current decisions to meet the future goals

Controlling

Characteristics of Effective Control Systems

Assoc.Prof.Dr.B.G.Çetiner

Effective: Measure what needs to measured and controlled

Efficient: Economical and worth their cost

Timely: Enough time for corrective action

Flexible: should be adjustable to changing conditions

Understandable: should be easy to understand

Tailored: Deliver the information according to each level of manager

Highlight Deviations: Flag parameters deviating from planned values

Lead to corrective action: should incorporate means of corrective actions

Controlling

Delegation and Control

Assoc.Prof.Dr.B.G.Çetiner

In human aspects of organizing, we have seen delegating the authority.Delegation requires effective control systems.

You have to apply the rules for making the controls more effectiveafter delegating the authority.

Controlling

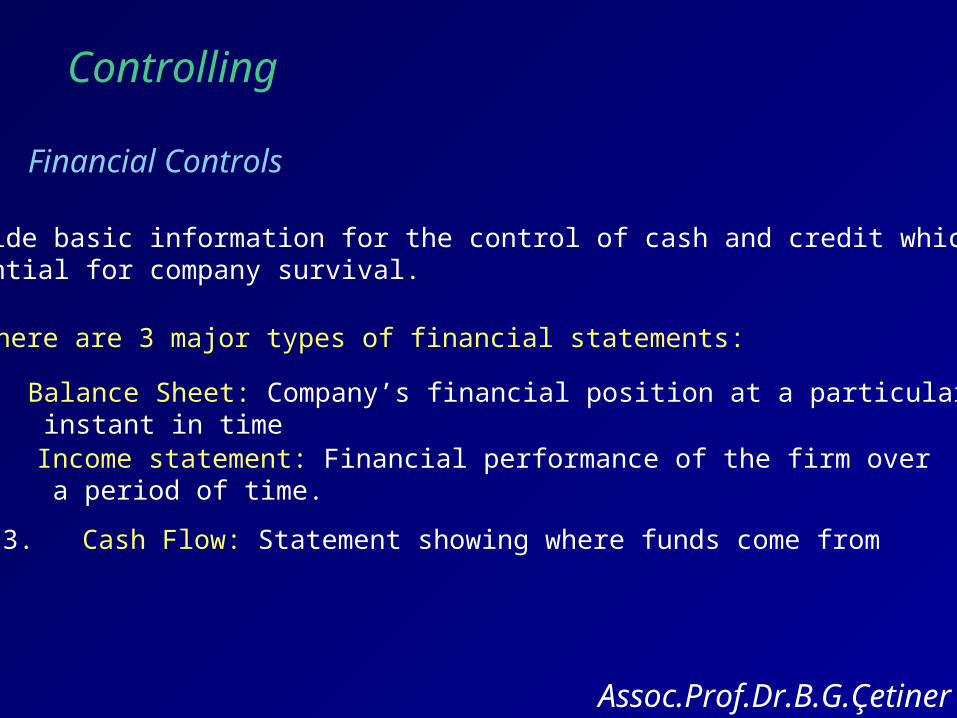

Financial Controls

Assoc.Prof.Dr.B.G.Çetiner

Provide basic information for the control of cash and credit which areessential for company survival.

There are 3 major types of financial statements:

1. Balance Sheet: Company’s financial position at a particular instant in time2. Income statement: Financial performance of the firm over a period of time.

3. Cash Flow: Statement showing where funds come from

Controlling Balance Sheet (EXAMPLE: Company X, December 2002)

Assoc.Prof.Dr.B.G.Çetiner

What company Owns

What company Owes

Controlling Statement of Income and Retained Earnings

Assoc.Prof.Dr.B.G.Çetiner

(EXAMPLE: Company X, End of 2002)

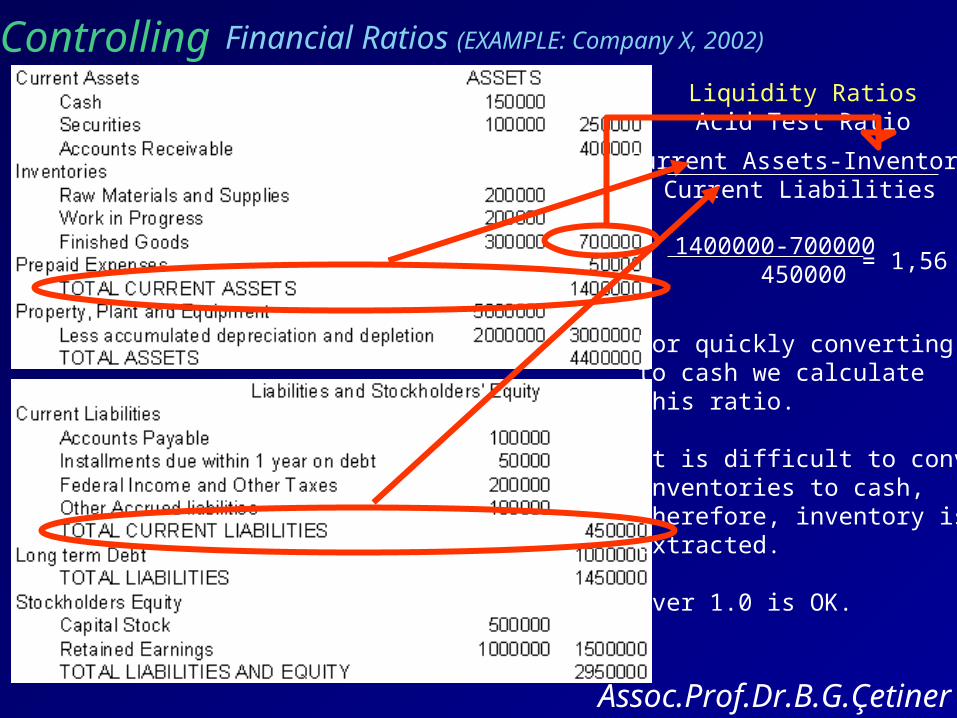

Controlling Financial Ratios (EXAMPLE: Company X, 2002)

Assoc.Prof.Dr.B.G.Çetiner

Liquidity RatiosCurrent Ratio

Current AssetsCurrent Liabilities

1400000450000

= 3,11

Measure the abilityto meet short-termobligations.

As minimum 2.0 is usedbut it varies. A current ratio of 10 shows assets are not usingefficiently.

Controlling Financial Ratios (EXAMPLE: Company X, 2002)

Assoc.Prof.Dr.B.G.Çetiner

Liquidity RatiosAcid Test Ratio

Current Assets-InventoryCurrent Liabilities

1400000-700000 450000

= 1,56

For quickly convertingto cash we calculatethis ratio.

It is difficult to convertinventories to cash,Therefore, inventory isextracted.

Over 1.0 is OK.

Controlling Financial Ratios (EXAMPLE: Company X, 2002)

Assoc.Prof.Dr.B.G.Çetiner

Leverage RatiosDebt-to-assets ratio

Total DebtTotal Assets

1450000 4400000

= 0,33

Relative importance ofstockholders and outside creditors as asource of enterprise’scapital.

Rate is dependent onthe industry.

Controlling Financial Ratios (EXAMPLE: Company X, 2002)

Assoc.Prof.Dr.B.G.Çetiner

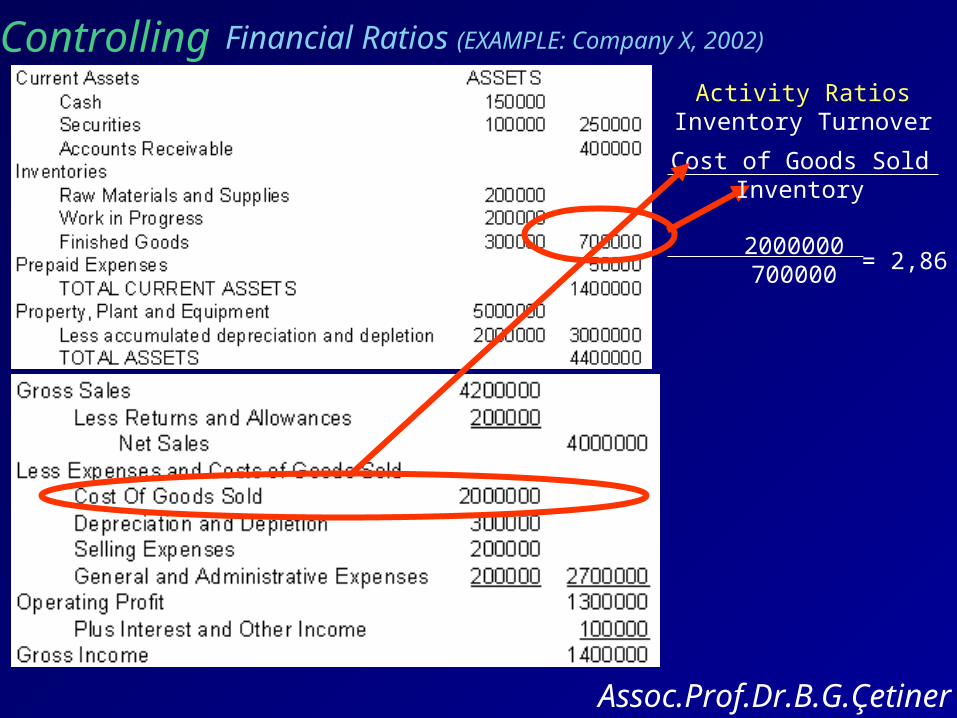

Activity RatiosInventory Turnover

Cost of Goods SoldInventory

2000000 700000

= 2,86

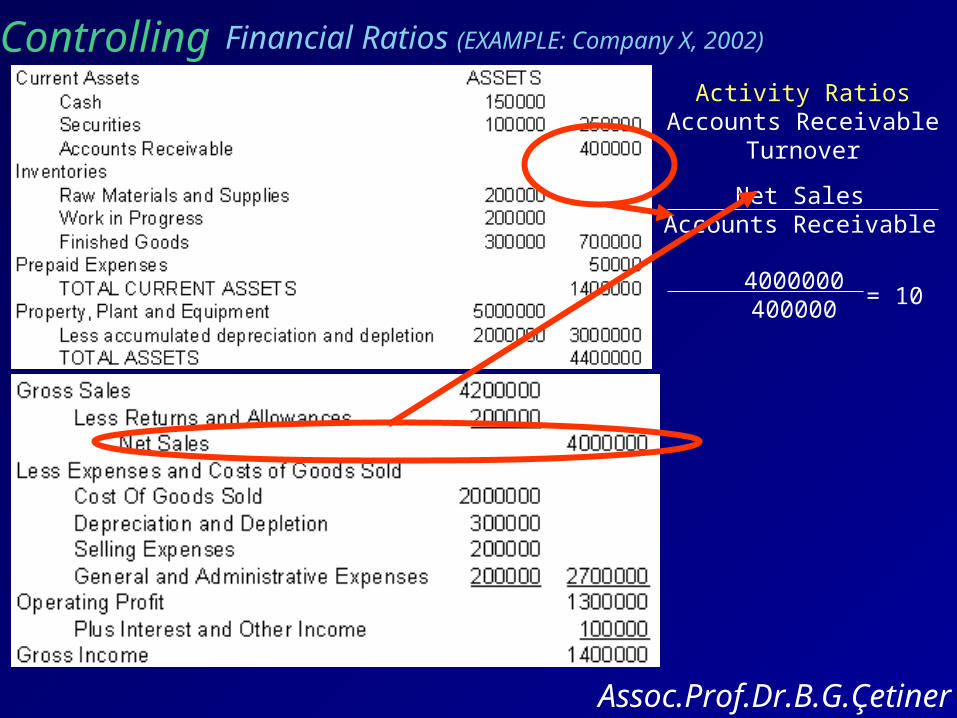

Controlling Financial Ratios (EXAMPLE: Company X, 2002)

Assoc.Prof.Dr.B.G.Çetiner

Activity RatiosAccounts Receivable

Turnover

Net SalesAccounts Receivable

4000000 400000

= 10

Controlling Financial Ratios (EXAMPLE: Company X, 2002)

Assoc.Prof.Dr.B.G.Çetiner

Activity RatiosAsset Turnover

Net SalesTotal Assets

4000000 4400000

= 0,91

Controlling Financial Ratios (EXAMPLE: Company X, 2002)

Assoc.Prof.Dr.B.G.Çetiner

Profitability RatiosProfit Margin

Net IncomeNet Sales

1050000 4000000

= 26,3%

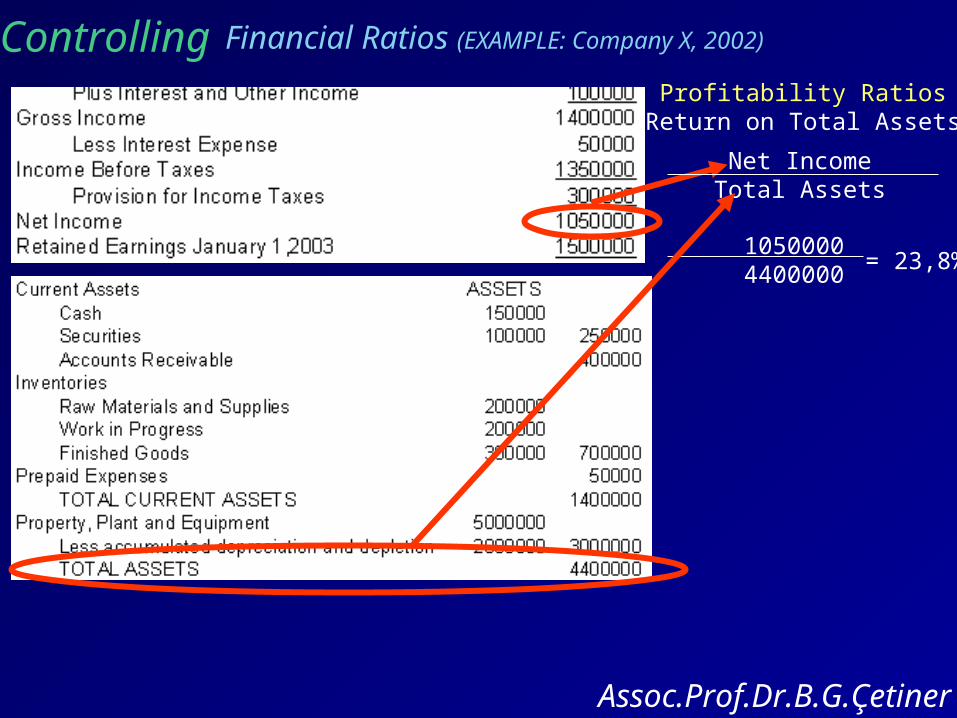

Controlling Financial Ratios (EXAMPLE: Company X, 2002)

Assoc.Prof.Dr.B.G.Çetiner

Profitability RatiosReturn on Total Assets

Net IncomeTotal Assets

1050000 4400000

= 23,8%

Controlling

Assoc.Prof.Dr.B.G.Çetiner

BudgetsPlans for the future allocation and use of resources over a fixed period of time.

Financial BudgetsPlanning of cash for the coming period and how thecompany intends to use it.

Three Types of Financial Budgets1.Cash Budgets: Estimate future revenues and expenditure and their timing during budgeting period

2.Capital Expenditure Budgets: Describes future investments in plant and equipment

3.Balance Sheet Budget: Uses the first two estimates to predict what balance sheet look like at the end of budgeting period

Controlling

Assoc.Prof.Dr.B.G.Çetiner

BudgetsPlans for the future allocation and use of resources over a fixed period of time.

There are responsibility centers in organizations.

Cost Center: Primary financial concern is control of costs

Revenue Center (Sales or Marketing): The manager has revenue targets to meet

Profit Centers: For manipulating costs to increase profit.

Operating budgets can be created like expense budget, revenue budget and profit budget.

Controlling

Assoc.Prof.Dr.B.G.Çetiner

Budgeting ProcessBudgets can be prepared by a central group and imposedon everyone by top management (top-down approach).This does not take the advantage of information from lower management.

Alternatively, budgets can be prepared in responsibilitycenters. They tend to be inflated and doesn’t consider uppermanagement goals and objectives.

Controlling

Assoc.Prof.Dr.B.G.Çetiner

Audits of Financial DataAudits are investigations of an organization’s activitiesto verify their correctness and identify any need forimprovement.

External Audits: required at least once a year for publiclyheld organization by independent companies

Internal Auditing Staff: They spend their times in auditing several units of organization

Controlling

Assoc.Prof.Dr.B.G.Çetiner

Non-financial Controls

Human Resource Control: Seen in Human Aspects oforganizing (Chapter 6)

Management Audit: By answering some questions about management such as planning, organizing andstaffing, directing, control, resource planning and control

Human Resource Accounting: Investments in acquiringpeople and in extensive training

Social Control: Building an organizational culture andcontrolling.