consumer awareness procedural manual - simah

TRANSCRIPT

Consumer AwarenessProcedural Manual

2nd Section

Copyright © 2021 SIMAH All Right Reserved

The Saudi Credit Bureau (SIMAH) has developed this procedural manual to publish it after the approval of Saudi Central Bank (SAMA). This Manual is intended to educate consumers about their rights guaranteed to them by the Credit Information Law and

its Implementing Regulations.

2nd Section Content

Copyright © 2021 SIMAH All Right Reserved

The Saudi Credit Bureau (SIMAH) has developed this procedural manual to publish it after the approval of Saudi Central Bank (SAMA). This Manual is intended to educate consumers about their rights guaranteed to them by the Credit Information Law and

its Implementing Regulations.

1st Section

1.1 Introduction1.2 Concepts 1.3 Definitions1.4 Regulations

2nd Section

2.1 Saudi Credit Bureau 2.2 Tasks2.3 Objectives2.4 Credit Report2.5 OfficeHours2.6 Supervision

3rd Section

3.1 Consumer Rights 3.2 Credit Principles3.3 SIMAHObligations3.4 Member’s Obligations

4th Section

4 Complaints and Disputes

Consumer Awareness Procedural Manual

4

Introduction

TheSaudiCentralBank(SAMA)istheregulator,supervisorandlicensorofthefinancial institutions

toworkintheKingdomofSaudiArabia(banksandfinancecompaniesincludingleasing,mortgage,

insurance, money exchange companies and credit information). In this context, SAMA monitors and

overseesthevariousproductsofferedtocustomersbyfinancialinstitutionsunderitssupervision.Since

the issuance of the its Article of Association in 1952 and Banking Control Law in 1966, SAMA has been

workingtoprotecttheinterestsoftheconsumersandmakesurethatfinancialinstitutionsdealwith

them with credibility and fair treatment.

Many countries and international bodies such as the G-20, the Financial Stability Board (FSB) and the

Organization for Economic Co-operation and Development (OECD) are considering amending and

issuing new standards in the area of consumer protection. Due to the growth and development of

the financial sector in Saudi Arabia, SAMAwill continue reviewing these developments and issue

appropriate regulatory directives to develop customer protection principles appropriately. SAMA aims

atensuringthattheconsumerwhodealswiththefinancialinstitutionsistreatedfairly,honestlyand

safely,andprovidedwithallnecessarytoolstoobtainfinancialserviceswitheaseandcomfort.Among

the most important rights are the credit rights which SAMA seeks to ensure to preserve in accordance

with the Credit Information Law issued by the Council of Ministers and the Implanting Regulations.

1.1

5

1st Section

The Concept of Saudi Credit Bureau (SIMAH)

This model demonstrates the importance of the credit information sharing and the role of SAMA in

regulatingandsupervisingtheactivitiesofSIMAHinSaudimarketandtomakesuretheycomplywith

the laws and regulations, such as Credit Information Law and Implanting Regulations. The credit infor-

mationbureaus,paymentsystemsfirmsandtheintermediaryfinancialsystemsareconsideredasthe

keyelementsinthefinancialinfrastructureofanycountry.Highqualityofthefinancialinfrastructure

affectsthegrowthandcontributionoftheprivatesectorwhichultimatelywillcontributetheconfi-

dence of lenders and investors and enable them to assess and manage risks.

TheSaudiCreditBureau(SIMAH)isconsideredtobeanimportantpillarofthefinancialinfrastructure

inchargeofprovidingnecessarycreditinformationtoenablebothborrowersandlendersalike.Having

an excellent credit report doesn’t guarantee approval, because lenders still consider other factors like

theconsumer’sincomeanddebt.However,agoodcreditreportincreasestheconsumer’schancesof

beingapprovedfornewcredit.CreditreportsprovidedbySIMAHhelplenderstoointhedecision-mak-

ing process to improve the ability to analyze consumers’ credit risks and assess the solvency of the

borrowers based on credit information.

Inaddition,SIMAH’sdata,demographic information,financialandnon-financial information,helps

to extrapolate the behavior of the consumer based on sophisticated mathematical models using these

data to support the lending decision, and risk management.

SIMAHbigdata,demographicinformation,financialandothervariablesavailableincreditreportshelp

lenders to extrapolate the borrower›s credit behaviors based on complex mathematical models that

use the variables and data of the credit report as key indispensable inputs to support lending decision

and risk management

Saudi Central Bank (SAMA)Regulation & Supervision

Paymnt Systems(SADAD, SAREEA)

Financial Institutions(Banks, financial

Companies)

Credit Reporting Bureau (SIMAH)

1.2

Consumer Awareness Procedural Manual

6

Definitions

The Credit Information Law (CIL) issued by the Royal Decree No. M/37 dated05/07/1429Hcorrespondingto08/07/2008.The Law

The Implementing Regulations (IR) of the Credit Information Law.Regulations

Saudi Central Bank (SAMA).Central Bank

Any consumer information or data related to his/her credittransactions.

CreditInformation

A Saudi Credit information Bureau licensed to collect creditinformation and save it to share it with its members.

Saudi CreditBureau (SIMAH)

Any government or private entity which is party to a credit informa-tion exchange contract with at least one credit information bureau.Member

Any natural or corporate person engaging in credit transactions.Consumer

A report issued by credit bureaus containing consumer creditinformation.Credit Report

Credit information records maintained by government entities such as records of funds and banks offering government loans, judicial au-thorities, government committees, bankruptcy and insolvency records and the like.

Public Record

Any decision a member will take upon a consumer’s credit record against his/her interest.

Negativedecision

Any information provided by a member based on the consumer’s credit report against his / her interest.

NegativeInformation

Credit Information Dispute & Settlement Committee.The Committee

1.3

7

1st Section

Regulatory Framework

TheCreditInformationLawwasissuedbytheRoyalDecreeNo.M/37dated5/7/1429Hcorresponding

to08/07/2008upontheResolutionofCouncilofMinistersBo.188datedin4/7/1429H.ThisLawshall

be applied to companies, members and government and private entities maintaining credit informa-

tion in accordance with Article No. 3 of the Law. Implanting Regulations have also been issued ac-

cordingtotheCentralBank’sGovernorResolutionNo.1s/13709dated22/09/1432Hcorresponding

17/08/2011asacomplementarytotheLaw.InitsProvisions(2,3,4)ofArticle3,TheLawhasentrust-

ed to the Central Bank the task of licensing, supervising, regulating and controlling credit bureaus. You

canfindtheLawandRegulationsonSIMAHwebsitebyvisiting(SIMAHlinktoLaws+Regulations).

1.4

Consumer Awareness Procedural Manual

8

Saudi Credit Bureau (SIMAH)

SIMAHwasestablishedon2002andstarteditsoperationon14April2004asacreditinformationbureau licensed to collect and maintain credit information on consumers and provide the same to members upon request.

Tasks

SIMAHistaskedwithcollectingandmaintainingcreditinformationonconsumersandprovidingthesametomembersuponrequest.

Objectives

1. Providinganeffectivefinancialinfrastructurethatcanbereliedontoensuresustainableeconomicgrowth.

2. Contributingtosoundfinancial infrastructuretoensuregrowthandcontributionoftheprivatesectorsoastoriseconfidenceoflendersandinvestors,decreasetheiruncertaintiesandimprovetheir abilities to assess and manage risks.

3. Providing accurate credit information necessary to support borrower’s decision-making process to improve his/her ability in analyzing and evaluating the credit risk of the borrower’s solvency based on credit information.

4. Collecting and analyzing data, demographic information, financial and non-financial variablesto help lending institutions and related parties in extrapolating borrowers’ behaviors based on sophisticated mathematical models using available data to support the lending decision and risk management.

5. Reducing credit information asymmetries ; whereas information disparities between the lender and the borrower often lead to a high risk of lending and a high cost of borrowing due to the lending decision taken primarily based on the accuracy of the credit information.

6. Reducing the loan default rates, increasing collection ratios, as well as facilitating accessibility to financeatacostthatisrisk-basedpricingwithgreataccuracy.

7. Supporting the monetary policy and its instruments. Lenders’ ability to price risk in a dynamic, accurate and differentiated manner according to the likelihood of a borrower’s defaulting allows one of the most important monetary policy instruments ; namely interest rates, to directly affect economic behaviour such as borrowing, investment and consumption rates.

8. Upliftingcreditqualityandcreditexpansiontostimulateeconomicgrowth.

2.1

2.2

2.3

9

2nd Section

Credit Report

TheSaudiCreditBureau(SIMAH), intheprocessofevaluatingconsumers’creditworthinessandbyproviding credit reports, does not provide any opinion, decision and/or comment that would oblige any membertograntordenyanycreditfacilities.Onthisbasis,SIMAHhas,sinceitsfoundation,insertedthe following statement in each credit report issued “This information has been collated from various sourcesanddoesnotrepresenttheopinionofSIMAH.NoLiability(intortcontractorotherwisehow-soever) attaches to us with respect to the collation or supplying of the information or any use made of it and whether in relation to its accuracy or completeness or any other matter whatsoever “. The credit report includes information that helps to enhance risk management and to deliver the evaluation processfasterandmoreobjectively.SIMAHcollectscreditinformationembodiedoncreditreportsfrompublic records and from members.

According to Article 16 of Implementing Regulations, the credit report include information related to the creditworthiness of the consumer, such as:

1. Natural consumer’s name, I.D number, place of residency, current and previous work location, maritalstatus,educationalqualifications,andpersonaldata.

2. Juridical consumer’s name, commercial registration number, address, and any other relevant information.

3. All information on any existing or previous credit and any guarantees given to the consumer, hiscompliancewiththespecifieddates,andanydelayedordisputedpayments.

4. Any credit-based claim and resolutions that were issued

5. Any insolvency,bankruptcyor liquidationclaims institutedagainst theconsumerand judg-ments taken in this regard, name of liquidator or trustee of bankruptcy, assets or debtamounts, payment dates and liquidation charges and expenses.

6. Any bounced checks issued by the consumer, their values and dates, and actions taken toward them.

7. Claimsissuedfromofficial/competentauthoritiesthathefailedtosettle.

8. Numberandnamesofmemberswhoappliedfortheconsumer’screditreportsduringthepast2 years preceding the issuance date of the credit record, number of issued credit records and results thereof.

9. Any other information of credit nature that may affect the credit worthiness of the consumer.

2.4

2nd SectionConsumer Awareness Procedural Manual Consumer Awareness Procedural Manual

10

Consumer Credit Report

0 4 2 x x x x x17/11/202009:25:27

Page 1Out of 5

ID Number

Credit Report Summary

First Account Issue Date

Number of Active Credit Products

Total Limits

Total Outstanding Balances

Total Guaranteed Limits

Total Guaranteed Balances

Number of Defaulted Products

Total Outstanding Defaulted Balances

*******

*******

*******

*******

*******

*******

*******

*******

:

:

:

:

:

:

:

:

Active Products Summary

Product Type Creditor Account Number Installment Amount Credit Limit Outstanding

Balance As Of Date Payment Status

****** ****** ****** ****** ****** ****** ****** ******

****** ****** ****** ****** ****** ****** ****** ******

****** ****** ****** ****** ****** ****** ****** ******

****** ****** ****** ****** ****** ****** ****** ******

****** ****** ****** ****** ****** ****** ****** ******

****** ****** ****** ****** ****** ****** ****** ******

****** ****** ****** ****** ****** ****** ****** ******

******* ******* *******

******* ******* *******

******* ******* *******

******* ******* ******* *******

:

:

Credit Score

Simah Score - Powered By Fico

Scorecard

Score Contributing Factors

Personal Information

Customer Name : *******Gender : *******Marital Status : *******ID Number : *******ID Type : *******ID Expiry Date : *******Issuing Authority : *******Nationality : *******Date Of Birth : *******Mobile Number : *******Employment Sector : *******Employer Name : *******Occupation : *******Salary : *******City : *******Update Date : *******

Consumer Credit Report

0 4 2 x x x x x17/11/202009:25:27

Page 5Out of 5

ID Number

EmployeroccuptionDate Of EmploymentBasic SalaryTotal SalaryLast Reported

Employment Information

Employment Addresses:

:

:

:

:

:

:

:

:

:

:

:

:

:

:

:

:

:

:

:

Address TypeAddress Line 1Address Line 2P.O.BoxCity Postal CodeCountry

Building NoStreet NameDistrict NameCity NamePostal CodeAdditional NoUnit No

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

National Address

Disclaimer & Disclosure

Disclaimer: This information has been collated from various sources on a confidential basis and doesn,t represent the opinion of Saudi Credit Bureau (SIMAH). No Liability (in contract or otherwise whatsoever) attaches to SIMAH as a result of taking any investment and/or any other decision based on information provided.

Disclosure: SIMAH, a Closed Joint Stock Company, Capital SR 200,000,000 Paid in Full,C.R1010171047 Membership No 115731,Tel: 8003010046, P.O Box 8859 Riyadh,11492 National Address: Riyadh, Alshuhada, BLDG No. 2596,Unit No 1, Additional No.7347, Zip 13241. Under the Supervision and Regulation of SAMA with a License No. 37 / 2. www.simah.com

Type Type Type

More Than 180 Days Overdue

Deferred Payment

No Update provided

Vacation Deferred Payment

Payment Code Prescription Guide

1 - 30 Days Overdue

31 - 60 Days Overdue

Payment on time

61 - 90 Days Overdue Fully Paid

121 - 150 Days Overdue

151 - 180 Days Overdue

91 - 120 Days Overdue

No Transactions

Closed Product

Default Product

New Product

Copyright © 2021 SIMAH. ALL RIGHT RESERVED. B2CV.28

Consumer Credit Report

0 4 2 x x x x x17/11/202009:25:27

Page 3Out of 5

ID Number

Product Details

Payment Status For Last 24 Months

Sabb Personal Loan Active Product

Installment Start Date 1 : ****** Installment Amount : ******

Installment Start Date 2 : ****** Installment Amount : ******

Installment Start Date 3 : ****** Installment Amount : ******

Installment Start Date 4 : ****** Installment Amount : ******

Installment Start Date 5 : ****** Installment Amount : ******

Number Of Applicants Instalment Amount Last Amount Paid Last Payment Date Outstanding Balance

****** ****** ****** ****** ******

Percentage Allocation Applicant Limit Payment Status Past Due Amount Next Payment Date

****** ****** ****** ****** ******

Joint Applicant

Instalments Details ( In Case Of Installment Change )

Account Number Issue Date Credit Limit Number Of Installments Installment Amount Payment Frequency Expiry Date Type Of Guarantee

****** ****** ****** ****** ****** ****** ****** ******

Outstanding Balance Past Due Balance As Of Date Last Amount Paid Last Payment Date Next Payment Date Close Date Salary Assignment

****** ****** ****** ****** ****** ****** ****** ******

Balloon Payment Down PaymentDispensed Amount

Max Instalment Amount Finance Mode Product Status Average Instalment

Amount

****** ****** ****** ****** ****** ****** ******

Payment Status For Last 24 Months

Arab National Bank Credit Card Cloesed Product

Previous Enquiries

Amount Applied ForProduct TypeEnquiry NumberEnquirierEnquiry Date

******************************

******************************

Enforcement Courts Decisions

Resolution Date Resolution Number City Reported Date Claimed Amount Outstanding Balance Status Settlement Date

****** ****** ****** ****** ****** ****** ****** ******

Account Number Issue Date Credit Limit Number Of Installments Installment Amount Payment Frequency Expiry Date Type Of Guarantee

****** ****** ****** ****** ****** ****** ****** ******

Outstanding Balance Past Due Balance As Of Date Last Amount Paid Last Payment Date Next Payment Date Close Date Salary Assignment

****** ****** ****** ****** ****** ****** ****** ******

Balloon Payment Down PaymentDispensed Amount

Max Instalment Amount Finance Mode Product Status Average Instalment

Amount

****** ****** ****** ****** ****** ****** ******

Product: ****************

Product: ****************

Product Status: ****************

Product Status: ****************

2nd SectionConsumer Awareness Procedural Manual

11

2nd Section

2 5 2 x x x x0 4 2 x x x x x

Silver Report

17/11/201509:25:27

Page 1Out of 7

Enquiry Type: New ApplicationDisplay of Credit Facilities: Summary

Enquriy Number Member Reference Number

Funded

Non Funded

Credit Instrument Summary (000)

Grand Total $$$$$ $$$$$ $$$$$

Sub Total

Sub Total

$$$

$$$

$$$

$$$

$$$

$$$

Creditor Credit Limit Utilization Past Due Collateral Provided

Realtionship Age As of Date

Bank************

******************

******************

******************

******************

******************

******************

Creditor Credit Limit Utilization Past Due Collateral Provided Realtionship Age As of Date

Bank************

******************

******************

******************

******************

******************

******************

Demographic Information

Company Name

CR Number

Issuer

Issuer City

Expiry Date

Legal Type

Business Activity

*******

*******

*******

*******

*******

*******

*******

:

:

:

:

:

:

:

Previous Enquiries

AmountProduct TypeMember Reference Enquiry TypeEnquirierEnquiry Date

******************************************

******************************************

******************************************

******************************************

******************************************

******************************************

Facilities Summary Level 1 (000)

Creditor Approved Limit Global Limit Utilization Unutilized Balance Status Past Due Collateral Relationship

Age As Of Date

******************

******************

******************

******************

******************

******************

******************

******************

******************

******************

2 5 2 x x x x0 4 2 x x x x x

Silver Report

17/11/201509:25:27

Page 7Out of 7

Enquiry Type: New ApplicationDisplay of Credit Facilities: Summary

Enquriy Number Member Reference Number

Associated Narrative

Type Date Loaded Loded By text

******************

******************

******************

******************

!!

Disclaimer & Disclosure

Disclaimer: This information has been collated from various sources on a confidential basis and doesn,t represent the opinion of Saudi Credit Bureau (SIMAH). No Liability (in contract or otherwise whatsoever) attaches to SIMAH as a result of taking any investment and/or any other decision based on information provided.

Disclosure: SIMAH, a Closed Joint Stock Company, Capital SR 200,000,000 Paid in Full,C.R1010171047 Membership No 115731,Tel: 8003010046, P.O Box 8859 Riyadh,11492 National Address: Riyadh, Alshuhada, BLDG No. 2596,Unit No 1, Additional No.7347, Zip 13241. Under the Supervision and Regula-tion of SAMA with a License No. 37 / 2. www.simah.com

Narratives

TextNarrative TypeReported Date

******************

******************

******************

Business Narratives

Member Narratives

!!

TextReported ByNarrative TypeReported Date

******************

******************

******************

******************

Copyright © 2021 SIMAH. ALL RIGHT RESERVED.V.9

2 5 2 x x x x0 4 2 x x x x x

Silver Report

17/11/201509:25:27

Page 2Out of 7

Enquiry Type: New ApplicationDisplay of Credit Facilities: Summary

Enquriy Number Member Reference Number

CREDITOR: ****************************

Credit Instrument Details

Limit Category Aggrregate Limit

****** ******

As of Date Issue Date Expiry Date Status

****** ****** ****** ******

As of Date Issue Date Expiry Date Status

****** ****** ****** ******

Last Amount Paid Next Due Date New Loan From Restructured Revolving Limit

****** ****** ****** ******

Last Amount Paid Next Due Date New Loan From Restructured Revolving Limit

Credit Instrument Number Product Type Credit Limit Utilized Amount

****** ****** ****** ******

Credit Instrument Number Product Type Credit Limit Utilized Amount

****** ****** ****** ******

Government Guaranteed Security Type Past Due Last Payment Date

****** ****** ****** ******

Government Guaranteed Security Type Past Due Last Payment Date

****** ****** ****** ******

Closed Date Tenure Instalment Amount Payment Frequency

****** ****** ****** ******

Closed Date Tenure Instalment Amount Payment Frequency

****** ****** ****** ******

Payment Code Shared Limit ID

****** ******

Last 24 Cycles

Project Name Project Owner Project Refernce

****** ****** ******

Credit Instrument Project

2 6 D0 43 81 5 M

Credit Instrument: 1

Credit Instrument: 2

Facilities Summary Level 2 (000)

Funded Non Funded

Creditor : ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ***** ******* ****** ******

Creditor : ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ***** ******* ****** ******

Creditor : ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ****** ***** ******* ****** ******

Credit Limit Cap Utilized Amount

Unutilized Balance Credit Limit Cap Utilized

AmountUnutilized Balance Limit

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

******

Shared Limit

Consumer Awareness Procedural Manual

12

Office Hours

SIMAH’sofficialworkinghoursfrom(8AM–4:30PM)(SundaytoThursday).

Supervision & Inspection

TheSaudiCentralBank(SAMA)issupervisingandinspectingtheSaudiCreditBureau(SIMAH)inac-cordance with Articles and Provisions stipulated in The Law and its Regulations.

2.5

2.6

Since 2002

Consumer Awareness Procedural Manual

14

Consumer Rights

SIMAHistakingtheresponsibilitytoraiseconsumersoftheircreditrightsthroughawarenessedu-cational programs (including this manual) according to Article 34 of the Regulations. in its educa-tionalprograms,SIMAHisobligedtoclarifythefollowing:

1. ThecreditreportisareportissuedbySIMAHthatcontainscreditinformationonconsum-ers.

2. Thecredit report reflects thecredithistoryof theconsumeruntil the lastupdateby themember.

3. AnIdentification(ID/passport/Iqama)mustbesubmittedbytheconsumertoSIMAHem-ployee before giving him/her any kind of service.

4. The credit reports of the consumer are history of their credit information and behaviors and do not give the member any decision to grant a facility or not.

5. The consumer has the right to know members who checked his/her credit report during the past 2 years preceding the issuance date of the credit report and their addresses.

6. SIMAH’smemberisobligedtoupdateconsumer’screditinformationonceaweekatleast.

7. SIMAH’smemberisobligedtoobtainconsumer’swrittenconsentuponmakinganinquiry.

8. SIMAH’smemberisobligedtoobtainconsumer’swrittenconsenttoprovidehis/hercreditinformationtoSIMAH.MembersshallnotprovideSIMAHwithincorrectdataoriftheyhavea believe that this data may be incorrect.

9. Theconsumerhastherighttoobtainhis/herfirstcreditreportfreeofcharge.

10. The consumer has the right to obtain his/her credit report free of charge if a member took a negative decision against him / her according to the Regulations.

11. The consumer has the right to obtain his/her credit report free of charge if he/she has e been rejected by a member.

12. The consumer has the right to obtain his/her credit report free of charge if he/she was a victim of any kind of fraud as long as he/she can prove it such as such as a proven manipu-lation of his /her personal information.

13. The consumer has the right to obtain his/her credit report free of charge if the report con-tains incorrect information.

3.1

15

3rd Section

14. The consumer has the right to obtain his/her credit report after modifying credit informa-tion upon submitting proven documents.

15. The consumer has the right to obtain his/her credit report at any time by paying the fees imposedbySIMAH,except forcasesmentionedabove.

16. Negative decision is any decision a member takes according to the credit report of a con-sumeragainsthis/herinterest.SIMAHshallnotinterfereinthedecision.

17. The consumer has the right to raise a dispute at any time about a negative decision or any credit information contained on his/her credit report.

18.Ifnegativeinformationisindisputebetweentheconsumerandthemember,themembershallnotifySIMAHthatthisinformationisindispute.

19. When a consumer complains about an incorrect or incomplete data in his/her credit report, SIMAHmustnotifyhim/heraboutinvestigationresults.

20.AmemberofSIMAHisobligedtonotifytheconsumerbyawrittennotificationupontakinganynegativedecisionbasedpartiallyorcompletelyonhis/hercreditreport.Thenotificationshall contain reasons of rejection, name, address and phone number of the credit bureau that provides data and a copy of the consumer’s credit report.

21. The consumer has the right to add a narrative in his/her credit report that shows his/her personal view on the information mentioned in his/her report.

22.Theconsumerhasnorighttoclaimforamodificationordeletionofanyoftheinformationinhis/hercreditreportwithoutsubmittingofficialdocumentstosupporthis/herclaimandto prove it.

23.TheconsumerhastherighttofileacasetoTheCommitteeifhe/sheisnotconvincedofinvestigationresultsprovidedbySIMAHorhis/herdispute is rejected.

24.SIMAHand itsmembersarecommitted tomaintainconfidentialityover thecredit infor-mation and data in their possession and to share them exclusively among each other and amongcreditbureaus.SIMAHanditsmembersareliablefortheiremployeesactsincaseof any violation of The Law or its Regulations.

25.AmemberofSIMAHmayaccepttheconsumer’sapplicationforanyfacilityevenifhe/sheis either in default or not.

Consumer Awareness Procedural Manual

16

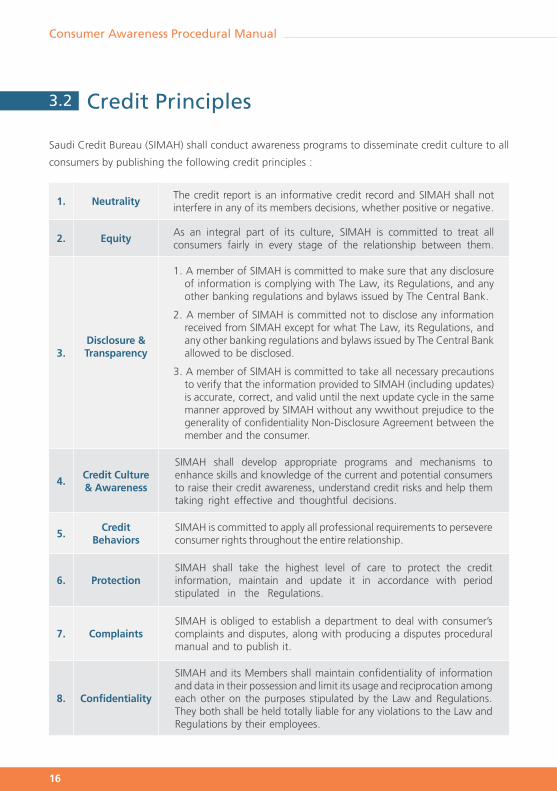

Credit Principles

SaudiCreditBureau(SIMAH)shallconductawarenessprogramstodisseminatecreditculturetoallconsumers by publishing the following credit principles :

1. Neutrality Thecredit report isan informativecredit recordandSIMAHshallnotinterfere in any of its members decisions, whether positive or negative.

2. Equity As an integral part of its culture, SIMAH is committed to treat allconsumers fairly in every stage of the relationship between them.

3.Disclosure & Transparency

1.AmemberofSIMAHiscommittedtomakesurethatanydisclosureof information is complying with The Law, its Regulations, and any other banking regulations and bylaws issued by The Central Bank.

2.AmemberofSIMAHiscommittednottodiscloseanyinformationreceivedfromSIMAHexceptforwhatTheLaw,itsRegulations,andany other banking regulations and bylaws issued by The Central Bank allowed to be disclosed.

3.AmemberofSIMAHiscommittedtotakeallnecessaryprecautionstoverifythattheinformationprovidedtoSIMAH(includingupdates)is accurate, correct, and valid until the next update cycle in the same mannerapprovedbySIMAHwithoutanywwithoutprejudicetothegeneralityofconfidentialityNon-DisclosureAgreementbetweenthemember and the consumer.

4. Credit Culture & Awareness

SIMAH shall develop appropriate programs and mechanisms toenhance skills and knowledge of the current and potential consumers to raise their credit awareness, understand credit risks and help them taking right effective and thoughtful decisions.

5. CreditBehaviors

SIMAHiscommittedtoapplyallprofessionalrequirementstopersevereconsumer rights throughout the entire relationship.

6. ProtectionSIMAH shall take the highest level of care to protect the creditinformation, maintain and update it in accordance with period stipulated in the Regulations.

7. Complaints SIMAHisobligedtoestablishadepartmenttodealwithconsumer’scomplaints and disputes, along with producing a disputes procedural manual and to publish it.

8. Confidentiality

SIMAHanditsMembersshallmaintainconfidentialityofinformationand data in their possession and limit its usage and reciprocation among each other on the purposes stipulated by the Law and Regulations. They both shall be held totally liable for any violations to the Law and Regulations by their employees.

3.2

17

3rd Section

SIMAH’s Obligations

1. SIMAHshallbeobligedtosignmembershipagreementsapprovedbyTheCentralBankwithanyparty that wishes to obtain credit information, and provide such parties with credit reports on the consumer. Such agreements shall indicate rights and obligations of the parties. That party will be designated after signing the agreement as a “member”.

2. SIMAHmaydisclosetheconsumer’screditreportinthefollowingsituations:• Basedonthemember’srequestandconsentoftheenquiredconsumer;• Basedonarequestfromacompetentdisputesettlementauthority.• BasedonTheCentralBank’srequest.

3. SIMAHshallprepareregularrecordscontainingconsumers’namesandtheircharacteristicswheth-er natural or judicial, their addresses and work locations, nature of their businesses and their credit information.

4. SIMAHshallprepareregularrecordscontainingthenamesofmembersandcompaniestheyaretransacting with, whether they are sources of information or other companies governed by the Lawandits ImplementingRegulations,andtheagreementsandcontractsratifiedwitheachofthem as well as their periods and conditions.

5. SIMAHshalltakeallnecessarymeasuresandprecautionstoensuresafety,validity,accuracyandintegrityof informationobtainedaccordingtotheLawanditsRegulations.SIMAHshallcomplywith the following:• No information shall be collected from any party or source prior to signing a membership agreement

with that party.• No credit information shall be gathered from members unless such action is in compliance with

definedcriteriatoSIMAH,that includeadministrative,technicalandlegalrequirementsapprovedby The Central Bank.

• SIMAHiscommittedtomaintainconfidentialityovercreditinformationanddatainitspossessionand share them exclusively with members, other bureaus, other persons and other related parties in accordance with The Law and its Regulations.

• SIMAHshalltakethenecessaryactionstoensurethattherearereasonsforrequestinginformationby the member.

• SIMAHiscommittedtoinformthememberwithhisobligationsaccordingtotheLawanditsRegulations.

6. SIMAHshallestablishdataandinformationsecurityprotectioncontrolsfortheinformationithasor already possessed.

7. Priortotheissuanceofanycreditreport,SIMAHshall:• Verifytheidentityoftheapplicantandpurposeofsucharequest.• Obtain the member’s undertaking that the information will not be used except for the reasons

specified in the application.• Ensure accuracy, completeness and currency of the information it provides.

3.3

Consumer Awareness Procedural Manual

18

Member’s Obligations

The member shall:1. Obtaintheconsumer’sconsentuponenquiringabouthis/hercreditreportandobtainhis/her

consentforprovidingSIMAHwithhis/hercreditinformation

2. NotprovideSIMAHwithanyinformationabouttheconsumerifitknowsthatsuchinforma-tioncontainserrorsorsufficientlybelievesthatsuchinformationmaycontainincorrectdata.

3. NotfurnishSIMAHwithanyfalseinformationabouttheconsumerafteritreceivesanotifica-tion to that effect from the consumer.

4. Periodically update the consumer’s credit information.

5. ProvideSIMAH,inallcircumstances,withcorrectandcompletecreditinformationabouttheconsumer.

6. Usetheconsumer’sinformationreceivedfromtheSIMAHforlawfulpurposes.

7. InformSIMAH immediately about any closed credit accountsbasedon the consumer’s re-quest.

8. Notdivulge/discloseanyinformationreceivedfromSIMAHabouttheconsumer.

9. Develop records including the names and addresses of credit bureaus transacted with as well as the information provided to such bureaus.

10. In case the consumer’s information contains a dispute or complaint, the member shall not havetherighttoprovideSIMAHwithinformationontheconsumerwithoutnotifyingthemthat such information are under dispute or subject to complaint.

11. Verify the consumer’s information and correct or delete any contained errors.

12. ThememberwhoiscommittedbyamembershipagreementwithSIMAHmaynotdenypro-visionofcreditinformationrequiredbySIMAHordelaytheprovisionofsuchinformationtoSIMAHaccordingtothedefinedschedulesandagreedfrequencystipulatedinthemember-ship agreements.

13. The member shall not have the right to re-include any negative information that has been deletedormodifiedintheconsumer’screditreportwithoutaresolutionbyTheCommittee.

14. ThemembershallinformtheconsumerinwrittennotificationaboutanynegativeinformationitwillsendtoSIMAHclearlyandexplicitly.

15. In case the member has taken a negative decision toward the consumer for a cause that is partially or entirely due to any information included in his/her credit report, it shall notify the consumer with the negative information as well as the following information:

• Causes for taking such a negative decision ; and • Name, address and telephone number of the credit bureau from where it obtained the credit report.

3.4

19

1st Sectionالقسم الرابع

With You

FOR YOU

Consumer Awareness Procedural Manual

20

Disputes and Complaints

1. SIMAHshall establishadisputeandcomplaintsdepartment, createadisputeprocedure

manual for consumers and publish it after obtaining The Central Bank’s approval. This

manual should achieve the following:

• A full understanding of these procedures by the employee who deals with the con-sumers.

• Immediate and full investigation on any dispute.

• Keep a written disputes record and document any actions taken.

2. SIMAHshallwithin5workingdaysfromthedateofbeinginformedwiththecomplaint,in-

form the member who issued the objected information and mention all related information

as well as all evidence and documents submitted by the consumer, and give the member no

more than 10 working days to respond. If no response is received within 10 working days,

this will be taken as valid evidence for supporting the consumer’s claim.

3. SIMAHshalltakeanactionwithin7workingdaysfromthedateofreceivingthemember’s

response, or after 10 days without receiving any response from the member.

4. Once the investigation proves partial or complete validity of the claim, or it is proven that

theinformationcannotbeverified,SIMAHshallwithin2workingdaysremovetheobjected

information from the credit report or revise it, as the case may be.

5. SIMAHshallnothavetherighttodeleteorreviseanynegativeinformationintheconsum-

er’s credit report once it is proven to be accurate.

6. SIMAHshallnotifytheobjectorwiththeactionstakentoinvestigatehisobjectionwithinat

least 10 working days from the date of his/her objection.

4

21

4th Section

7. SIMAHiscommittedtonotifytheobjectorinwrittenwiththefindingoftheinvestigation

within at least 5 working days from the date of taking the decision in this regard, including

the following:

• A copy of the revised consumer’s credit report if the objection has proven to be valid.

• A Summary of the consumer’s rights according to The Law and its Regulations, if it is proven that the objection is invalid.

8. SIMAHshallreferineverycreditreportitissuesduringtheinvestigationperiodtotheob-

jection raised on any information contained in that report. If the investigation fails to settle

theobjection,SIMAHmay,ontherequestoftheobjector,undertakethefollowing:

• Refertotheobjectioninanysubsequentcreditreportrelatingtotheobjectorandin-cluding any objected information.

• Include in the credit report a clear summary of the actual facts of the projected infor-mation as viewed by the objector.

• Notify any party designated by the objector, which had obtained his credit report in the previous year of the objection regarding the submission of the objection if that report included any of the objected information.

9. Once any information contained in the objector’s credit report has been deleted or modi-

fied,SIMAHshallnotifysuchadeletionormodificationtoanypartydefinedbytheobjector

that may have obtained his/her credit report during the year preceding the objection, and

toalllicensedcreditinformationbureausthatarecontractedwiththeSIMAH.

10. The consumer may, if his /her objection is rejected, approach The Committee.

Contact Us 8003010046 [email protected] www.simah.com

Kingdom of Saudi ArabiaP.O.Box 8859 Riyadh 11492 | Toll Free No 8003010046

Email: [email protected] | Website: www.simah.com

Saudi Credit Bureau, SIMAH, a Closed Joint Stock Company, Capital SR 200,000,000 Paid in Full - C.R 1010171047- Membership No.115731, Toll Free No. 8003010046,Fax No. +966112188797 P.O Box 8859 Riyadh 11492- National Address: Riyadh, Al Shuhada, Building No. 2596, Unit No. 1, Additional No. 7347, Zip Code 13241.

Under the Supervision and Regulation of SAMA with a License No. 2 / 37. www.simah.com