congratulating chris floyd & the first national …...“your room” (your mental worldview)....

TRANSCRIPT

Extraordinary Banker® 1

BANK VALUATIONConcepts to

Influence How You Lead

THE 5 STEP Blueprint for

Winning Low- Cost Deposits

AVOID THESE Three Risky

Deposit Strategies

2019 BANK OF THE YEAR

WINNER

$19.97 | Issue No. 28

CONGRATULATING CHRIS FLOYD & THE FIRST NATIONAL BANK OF SYRACUSE TEAM

Full 2019 Banky™ Awards Winner’s List Inside

2 Extraordinary Banker®

LETTER FROM THE EDITORBy the time you hold this magazine in your hands, we’ll be six weeks from the end of 2019.

Think back to November of last year. You had big plans for 2019, I’m sure.

Have you achieved them?

I know one bank that checked off one very BIG goal just a few weeks ago.

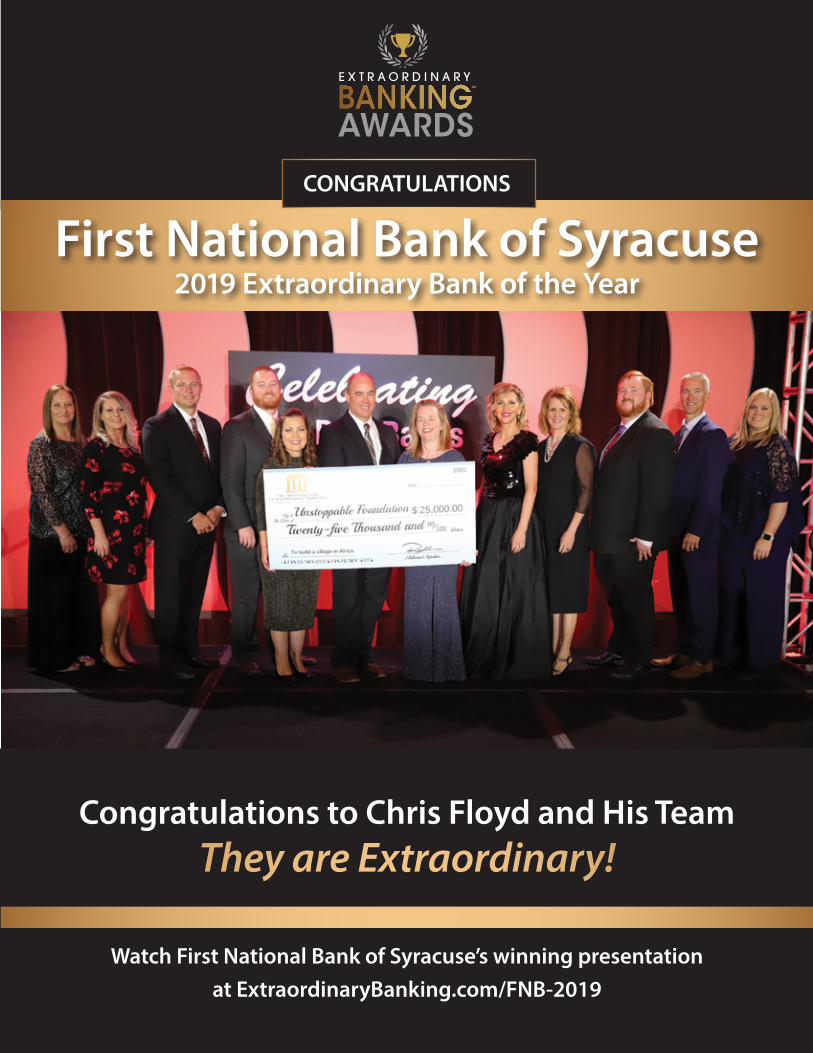

Please join me in congratulating Chris Floyd, CEO, and his team from First National Bank of Syracuse (Kansas): the 2019 Extraordinary Bank of the Year.

Chris’s team is used to big honors: They’ve been named to SNL’s Top 100 Banks Under $1 Billion, ranking as high as #2. And I know that being named Extraordinary Bank of the Year has been in Chris’s sights for several years. I’m excited that he and his team achieved it this year!

See First National Bank’s complete case study on Page 21.

New Headwinds Impacting Loan GrowthIn yet another installment of “The Economy Doesn’t Matter—There are Always Challenges,” I’ve been on the phone non-stop with bank CEOs who felt like they were knocking it out of the park hitting their loan closing goals–some saying they’re closing more deals than ever.

But … and it’s a big but … they’re barely eeking out three to five percent growth.

The cause: rapid payoffs by businesses, flush with cash, that are shedding debt.

This business certainly has a way of keeping us all humble.

We’ve been counseling with our member clients at my firm, The Emmerich Group®, to help them thrive, despite the challenge—and it’s working. Recently, I recorded a short audio and sent it to several hundred CEOs in my network.

If you missed it, you can listen online at ExtraordinaryBanking.com/PayOffIssue

Now’s the time to press hard toward the end of the year to be unstoppable in hitting all your goals.

To your success,

Roxanne EmmerichExecutive Editor

Extraordinary Banker® 3

TABLE OF CONTENTSE X T R AO R D I N A R Y

FOUNDER AND EDITORRoxanne Emmerich

CREATIVE DIRECTORSteve Gordon

GRAPHIC DESIGNPam Huber Designs

WRITERSJim Brennan, Roxanne Emmerich,Dale McGowan PhD, Z. Christopher Mercer, Joshua Siegel

PRODUCTION TEAMSophie Zollmann and Charles Kozierok

ADDRESSOne Liberty Corporate Center6625 West 78th Street, Suite 200Bloomington, MN 55439

TO ADVERTISE, CONTACTLeadership Avenue PressPhone: 952-737-6730Email: [email protected]

LETTERS TO THE EDITOREmail: [email protected]

Please include your mailing address and telephone number.

Key Trends Widening the Gap Between the Best Banks and the Commoditized Masses2019 Best Banks in America™ Super Conference RecapDale McGowan, PhD

Why These 3 Common Deposit Growth Strategies Put You at Risk NowPlus, the New Blueprint for Winning Low-Cost “Sticky” DepositsRoxanne Emmerich

How Can You Use Bank Valuation Concepts to Influence How You Think and Lead?Z. Christopher Mercer

Not Magic, Just Focus: How a Small Town Bank From Kansas Became One of the Best Banks in America™A Conversation with First National Bank of Syracuse CEO Chris Floyd

Are You Ready for the Next Recession?Joshua Siegel and Jim Brennan StoneCastle Partners, LLC

How to Escape Commodity-Ville: A Predictable “Franchise System” for Landing Large, Low-Cost Deposits in Any MarketRoxanne Emmerich

4

10

14

21

26

30© MMVI-MMXIX Leadership Avenue Press, LLC. All Rights Reserved.

4 Extraordinary Banker®CONTINUED on PAGE 6

always feel like I’m doing really well compared to my peers,

and then I come to this conference and realize how much work we still have to do.”

This is what many bank CEOs who attend the Super Conference say every single year—and especially this year.

The 6th annual conference, designed only for high-performing banks and those who want to get to the top and stay there, was based on the bestselling new book, Everything is Figureoutable.

We tackled banking’s biggest challenges, covering how to grow low-cost core deposits, command premium pricing while taking less risk, double profitable revenue per employee, and grow assets—all at a time when, despite hitting new loan volume numbers, payoffs are making it harder to have real asset growth. And for each topic, practical and proven answers and systems were openly shared.

When the elite, ambitious, results-oriented banks in America come together, there is a philosophy: Don’t

compete for pieces of the pie—grow the pie. They do it by sharing ideas that never get covered in other conferences but instead are held tight to the chests of the few who know how to break out.

If you missed the conference this year, here are a few highlights.

Mark Schaefer, author of Marketing Rebellion, star of one of America’s top five marketing blogs, and faculty member of the Rutgers School of Graduate Studies, taught us that we can no longer buy our way into new business with “advertising conversations.” Instead, we have to earn our way into real conversations with a new business approach that

appeals to “constant human truths.”There’s good news: You can probably cut 80 percent of your marketing budget and end up with better marketing. And there’s even better news: If you

learn a whole new type of marketing based on the principle that “the most human company wins,” you will easily capture the customers of competitors who continue to place ads and do direct product mailings. Only those who figure out how to humanize their marketing to build trust and relationships will stand a fighting chance.

Chris Mercer, CEO of Mercer Capital and author of Business Valuation and Valuing Financial Institutions, is arguably the foremost authority on bank valuations. He showed bank CEOs that what they thought they knew about creating franchise value for their banks may have been based on the wrong premise. He taught that bank valuations

go far beyond the traditional formulas. What really impacts valuations are such things as increasing customer and employee retention, your culture score, your client experience, cross-sales, and many other leading indicators. It was eye-opening for those who thought they understood how to determine the value of their bank or a bank they were considering

buying.

Dr. Ivan Misner, Chairman of the Board of Business Networking International (BNI), an organization

2019 BEST BANKS IN AMERICA™ SUPER CONFERENCE RECAP

KEY TRENDS WIDENING THE GAP BETWEEN THE BEST BANKS & THE COMMODITIZED MASSESBy Dale McGowan, PhD

“I

When the elite, ambitious, results-oriented banks in America come together, there is a philosophy:

Don’t compete for pieces of the pie—grow the pie.

Extraordinary Banker® 5

First National Bank of Syracuse 2019 Extraordinary Bank of the Year

Congratulations to Chris Floyd and His Team They are Extraordinary!

Watch First National Bank of Syracuse’s winning presentation at ExtraordinaryBanking.com/FNB-2019

CONGRATULATIONS

6 Extraordinary Banker®

with more than 9,000 chapters worldwide, shared concepts from his new bestseller, Who’s in Your Room? He explained the importance of having a “gatekeeper” who protects the key values you stand for and prevents people taking important real estate in your brain—such as the employee you had to fire who continues to harass you or speak negatively about you, the poor performer who caused you to lose confidence, or the untrustworthy person who caused you to become suspicious. These are all examples that demonstrate that when someone gets in, they never really leave “your room” (your mental worldview).

Roxanne Emmerich, CEO of The Emmerich Group®, founder of the Institute for Extraordinary Banking™, and editor of this magazine, has almost three decades of experience helping banks get to the top 5% percent of performance and stay there. She shared how to use a series of “franchise systems” that link together and are stage-appropriate to help everyone know how they tie to profit on a daily,

weekly, and monthly basis so they can move from normal to high performance. She shared a blueprint that has helped hundreds of banks catapult from average performance to top of peer status.

Steve Shapiro, columnist for Inc. magazine and past head of a 20,000-person unit at Accenture, shared how crucial innovation is to survival, why almost every bank gets innovation all wrong, and what to do instead.

On Tuesday night, the conference highlight Banky™ Awards involved

a red-carpet experience, presentations from the stage, and the top winner of the Los Angeles International Piano Competition demonstrating what mastery looks like. One thing that Banky™ Award winners share is the desire to hone their craft to the level of mastery.

During the Banky™ Awards program, over 45 banks were bestowed Banky™ Awards—recognized for outstanding performance, impact on their communities, and pulling ahead of other banks in both culture and customer service based on a culture survey and mystery shopping.

Category award winners inspired the audience by sharing the unique and impactful practices they have put in place to stand out in the five categories of service, culture, philanthropic impact, financial literacy, and enterprise. They highlighted their ability to run elite, high-performance banks. Several bank CEOs said they received two years’ worth of implementable ideas.

CONTINUED from PAGE 4

During the Banky™ Awards program, over 45 banks were bestowed

Banky™ Awards—recognized for outstanding

performance, impact on their communities, and pulling ahead of other

banks in both culture and customer service.

CONTINUED on PAGE 28

Extraordinary Banker® 7

1st Summit BankAmerican National Bank

American State Bank & Trust CompanyApex Bank

BAC Community BankThe Bank of Elk River

C&NCitizens Bank of Lafayette

Columbia BankCommunity State BankDecorah Bank & TrustDenver Savings Bank

F&M BankFarmers State Bank of Alto Pass

Farmers State Bank

The First Citizens National BankFirst International Bank & TrustFirst National Bank of Syracuse

First Service BankFirst Volunteer Bank

Franklin Savings BankGreater Community Bank

High Country BankHome State Bank

Hoosier Heartland State BankKennebec Federal Savings

Lead BankLegacy Bank

Libertyville Savings BankMarine Bank & Trust Company

NewBankNorthern BankPioneer Bank

PriorityOne BankRegent Bank

Richwood BankSecurity Bank (NE)Security Bank (TX)

Sterling Federal BankThomaston Savings Bank

TriStar BankUlster Savings Bank

The Victory BankVirginia Partners Bank

Vista Bank

Congratulations to the 2019

BANKY™ AWARD WINNERS

Recognizing the Best Banks in America™

Get advance notice when the 2020 Banky™ Nominations open, and join these elite banks and finally gain clear differentiation... you’ll be the talk of your market.

Get on the early-notification list now at BankyAwards.com/nominate

8 Extraordinary Banker®

FIRST INTERNATIONAL BANK AND TRUST

Extraordinary Banking Hall of Fame Inductee

Congratulations

Watch for a complete case study on First International Bank and Trust in the February 2020 issue of Extraordinary Banker® magazine

Congratulations to Peter Stenehjem and His Team

Extraordinary Banker® 9

Dan Diamond, MD Director of the Medical Triage Unit at the New Orleans Convention Center following Hurricane Katrina

Leadership Under Pressure We are all trying to get more done with fewer resources. Consequently, team members are at high risk to burnout and disengage. Dr. Dan Diamond equips leaders to make a difference when times are tough. Far from just motivational fluff, his rock-solid experience and trench-tested insights have been forged from the “front lines” of disasters around the globe. He was the Director of the Medical Triage Unit at the New Orleans Convention Center following Hurricane Katrina, led one of the first teams into Haiti after their devastating earthquake, and deployed to the Philippines following Typhoon Yolanda. He’s been seen on CNN, Anderson Cooper, and Larry King Live. This guy’s got something to say about getting your team engaged and succeeding, even in the most difficult situations.

Featuring Key Note Speaker

7TH ANNUAL THE BEST BANKS IN AMERICA™

SUPER CONFERENCEThe only conference for banks that want to

get to and stay in the top 5% of performance

*495 for each additional executive or board member you register.

Date

September 14-16, 2020

Location

Atlanta, GA

SUPER Early Bird Offer:

$695 for the first executive*Deadline is January 15th, 2020

Regular Price

$2,795

September 14-16, in beautiful Atlanta, Georgia.Register today at BestBanksinAmerica.com or call (952) 737-6700.

REGISTER NOW

“The content covered at the Super Conference is 10-20 years ahead of what we hear at other bank conferences—

we stopped going to most of those.

This program is at the core of the strategies that helped us achieve a 2.0 ROA. We would NEVER miss this conference.” — P. STEELE, CEO, First Volunteer Bank

Can I talk to you?”

“Sure.”

“You know when you said ‘deposits are easy’ before the coffee break? I looked around, and … well … it’s pretty obvious they don’t believe you.”

This was a bank CEO who had a mountain of evidence that growing deposits was hard because it had been hard for him—until, after years of struggling and thinking it couldn’t be done, his bank applied a different approach and grew low-cost sticky deposits quickly and easily. Now, this CEO was clear: Core deposit growth is easy if you have the right process.

Why These COMMON DEPOSIT GROWTH STRATEGIES Put You at RISK NowPlus, the New Blueprint for Winning Low-Cost “Sticky” Deposits By Roxanne Emmerich

Core deposit growth is easy if you have the right process.

3

10 Extraordinary Banker®

Extraordinary Banker® 11 CONTINUED on PAGE 12

In fact, his bank grew deposits 39 percent that year. His team simply had to stop doing what wasn’t working and find out what actually does work.

The belief that growing deposits is easy is not conventional wisdom. If you believe deposits are hard to find and keep, it’s not your fault: You’ve had that philosophy ingrained, and given the approaches that are now prescribed, it is hard to find evidence to the contrary.

The problem is that banks are continuing to use all the banking “tricks” they learned in graduate school when they need to play “catch up” with growing deposits. Advertising rates in the local paper. Offering CD specials. Creating incentive programs. Doing sales training. Firing the old SVP of Retail and hiring a new one.

No matter how sincere the attempts to implement those solutions, the basic processes to predictably and consistently grow core low-cost deposits remain elusive for many banks.

Let’s start by discovering why these seemingly reasonable strategies to predictably grow core deposits, or any deposits for that matter, continue to surprise most bank executives when they (of course) don’t work.

CD SPECIALSAds in the paper for CD specials attract a certain client: a person who will only invest with the best price and is willing to move for a few basis points. If you are later surprised at what happens when the money comes up for renewal and

the client runs to the most desperate competitor that is running their own ad at that time, you have a fundamental misunderstanding of basic human behavior: People rarely change and will predictably do again tomorrow exactly what they did today. Your ad will attract someone who will leave you for a better rate, so you have paid a considerable price only to be dumped.

A frightening thought is what kind of risk banks will have if they rely on this

strategy when there is a dramatic rate offer from American Express or Charles Schwab just when they most need funds—because that is when those firms will strategically decide to crush you and beat you when you’re down. When you most need funding is exactly when they most want those same deposits—and they have deeper pockets than you do as a community bank.

FIRING THE SVP OF RETAILThe next most common strategy banks deploy when they need to grow deposits faster is to fire the head of retail and replace that poor soul, hoping for a better result. Sadly, when that strategy is deployed, not only is that person’s life temporarily destroyed but, based on national statistics, the person you hired has less than

a 15% chance of keeping the job more than a year. That individual is set up to fail.

The problem is a team with “stuck energy”—inertia that makes it unwilling and unable to do the right activities. That stuck team now decides to slow-walk the new manager—they don’t want to make changes.

This unfortunate new manager has to confront the same fundamental issues as the last person who was set up to fail—not only a team that can’t or won’t engage in the needed behaviors but the bigger challenge of an executive team with strategies that start and end at “grow deposits.” There are no real defined strategies that have any chance of working, no integration of new strategies, advanced education, interwoven organizational development processes … nothing. So, the new head of retail quickly sees the future: When the numbers aren’t hit, he or she will be next on the chopping block.

WELL-INTENTIONED INCENTIVE PROGRAMSBut wait! There’s another solution that banks like to try: incentive programs. The corresponding adage is uttered by many a bank CEO without the slightest variation: “the behaviors follow the money.”

Again, it certainly sounds legitimate. And again, it just doesn’t work so well.

Think of it this way. If someone told you, “I’ll give you a million dollars to run a mile in under four minutes,” you’d be compelled. You’d be interested. You’d

The problem is that banks are continuing to use all the banking “tricks” they learned in graduate school when they need to play “catch up” with growing deposits.

Not only is that person’s life temporarily destroyed, but the person you hired has less than a 15% chance of keeping the job more than a year.

12 Extraordinary Banker®

CONTINUED from PAGE 11desire the money. You may or may not give it a sincere try, depending on how athletically inclined you are.

The problem is that there is so much more required than just a desire for the money: the mental toughness

for training, the stage-appropriate technique coaching, the supportive diet to optimize the body’s abilities, the training schedule with ever-advancing challenges that make sense based on readiness, and access to a team of experts as needed. Heck, even the selection of a person in the right age group who is the right size and has the

right body structure is fundamental. The list goes on.

Most banks’ incentive programs demoralize people more than they support them. It goes back to basic organizational development theory

about intrinsic rewards versus extrinsic rewards. Extrinsic rewards like money only work minimally and in the short term. Intrinsic rewards engage the whole person on an ongoing basis—long after the extra money stops providing the necessary change of behavior.

Repetition of these “fixes” that are considered conventional wisdom fail to deliver the necessary results. Sadly, most banks repeat them instead of challenging themselves to find out what really is working to grow deposits. The real question is whether you can afford to not find out exactly what the top deposit-attracting banks are doing that is working to attract all the deposits they need.

Extrinsic rewards like money only work minimally and in the short term. Intrinsic rewards engage the whole person on an ongoing basis—long after the extra money stops providing the necessary change of behavior.

I’ve talked with enough bank CEOs and boards to know that the question isn’t “Do you want more low-cost core deposits?” but, “WHEN would like

to start winning low-cost sticky deposits in a big way?”

If you’re like most of those CEOs and board members, the answer to that question is, emphatically, “YESTERDAY!”

That’s why we’ve created The Deposit Mastery™ Summit—the one-time special seminar just for ambitious, results-oriented bankers who are ready for a sustainable breakthrough in how they gather low-cost deposits. The Deposit Mastery™ Blueprint that has helped hundreds of banks catapult their deposit

gathering will be revealed at this new one-time seminar February 6-7, 2020 in sunny Orlando, Florida.

Get all the details and register yourself and your executive team atEmmerichFinancial.com/DepositSummit20

Roxanne Emmerich is the Founder of The Institute for Extraordinary Banking™, Editor of Extraordinary Banker® magazine, and CEO of The Emmerich Group®. For nearly 30 years she’s shaped the thinking and the results of The Best Banks in America™.

She can be reached at [email protected]

ABOUT THE AUTHOR

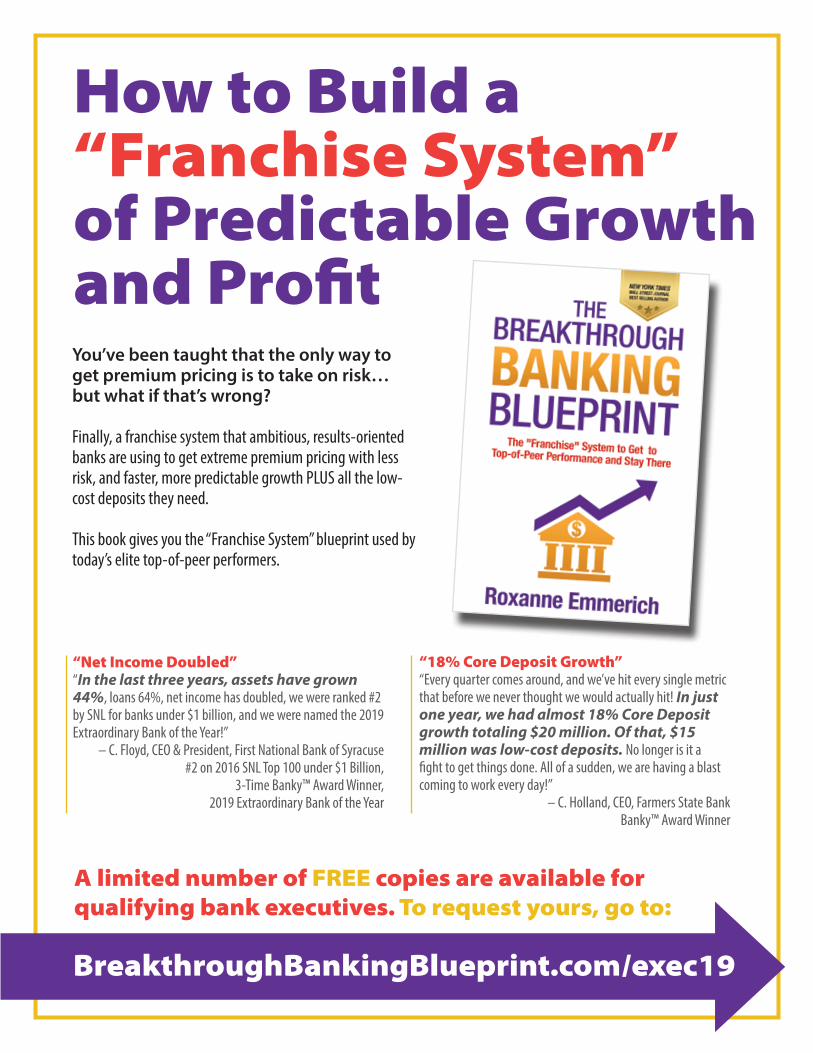

How to Build a “Franchise System” of Predictable Growth and Profit

“Net Income Doubled”“In the last three years, assets have grown 44%, loans 64%, net income has doubled, we were ranked #2 by SNL for banks under $1 billion, and we were named the 2019 Extraordinary Bank of the Year!”

– C. Floyd, CEO & President, First National Bank of Syracuse #2 on 2016 SNL Top 100 under $1 Billion,

3-Time Banky™ Award Winner, 2019 Extraordinary Bank of the Year

“18% Core Deposit Growth”“Every quarter comes around, and we’ve hit every single metric that before we never thought we would actually hit! In just one year, we had almost 18% Core Deposit growth totaling $20 million. Of that, $15 million was low-cost deposits. No longer is it a fight to get things done. All of a sudden, we are having a blast coming to work every day!”

– C. Holland, CEO, Farmers State BankBanky™ Award Winner

BreakthroughBankingBlueprint.com/exec19

A limited number of FREE copies are available for qualifying bank executives. To request yours, go to:

You’ve been taught that the only way to get premium pricing is to take on risk… but what if that’s wrong?

Finally, a franchise system that ambitious, results-oriented banks are using to get extreme premium pricing with less risk, and faster, more predictable growth PLUS all the low-cost deposits they need.

This book gives you the “Franchise System” blueprint used by today’s elite top-of-peer performers.

14 Extraordinary Banker®CONTINUED on PAGE 16

wners and managers of privately owned community banks tend to think about

running their banks effectively, of course. And then, there is an annual or occasional valuation of the bank for the ESOP, a repurchase of shares, some other transaction, or pure curiosity. It is my observation that many bankers don’t think about managing their banks with valuation concepts in mind. This short article may help bring valuation concepts and management concepts into better alignment for thinking about and leading your bank.

As complex as bank valuation can be, it can be summarized with only four terms.

This basic valuation equation summarizes a much more complex discounted cash flow analysis, but it is helpful for our discussion. The value of a bank, today, or V, is its Earnings

(technically, expected earnings), capitalized by a discount rate, R, minus the long-term expected Growth rate of Earnings, or G. The algebra in the equation at the top is fairly straightforward.

We learn three things (other things being equal, of course):

• Increase Earnings and Value will increase.

• Decrease Risk and Value will increase (it is in the denominator). Increasing Risk, on the other hand, will decrease the Value of a bank.

• Increase Growth and Value will increase.

We know these things almost intuitively, but the focus helps. To be clear how this all works, assume that Earnings are $10 per share, R is 15%, and G is 5%. The math is fairly simple. The Multiple developed is the typical price/earnings

multiple that we see in the markets for publicly traded banks.

If you want another quick valuation fact, there is a relationship between the Multiple and a bank’s return on equity (ROE). If, as in our example, the ROE is 15% and the Multiple is 10.0x, then the Price/Book Multiple will be 150% (10 x 15%). All bank leaders and shareholders are interested in their Price/Book Multiples!

So far, we have explained the basics of bank valuation in just over 300 words. Now let’s talk about how these concepts can influence how you think about your bank and, perhaps, how you lead it.

FOCUS ON EARNINGSBanks generate interest income on loans and other earning assets and pay interest on interest-bearing debt. In so doing, they generate a spread. They also generate fee and service income in a variety of forms. The question is: How can we influence Earnings in our day-to-day interactions with our banks?

At The Emmerich Group®, we learn the importance of cross-selling. Other than a score you can calculate, what is cross-selling? It is developing multiple relationships with the same customers. Why is this important? Let me provide a personal example.

I have banked with Commercial Bank & Trust Company, a community bank here in Memphis, for about 30 years. I have multiple personal accounts and my wife and children (now grown) have accounts. Commercial Bank has also been Mercer Capital’s banker for those same 30 years. It has provided financing for our ESOP’s purchase of half of our stock, multiple build-out loans when we have moved or expanded, and our seasonal line of credit.

HOW CAN YOU USE BANK VALUATION CONCEPTS TO INFLUENCE HOW YOU THINK AND LEAD?

VALUE =

Increase Earnings

Decrease Risk

Increase Growth

=

EarningsR - G

VALUE

VALUE =

MULTIPLE ==

VALUE ==

$10 per share15% - 5%

$10 per share x 10.0

$100 per share

1 / (15% - 5%)

10.0

OBy Z. Christopher Mercer

TM

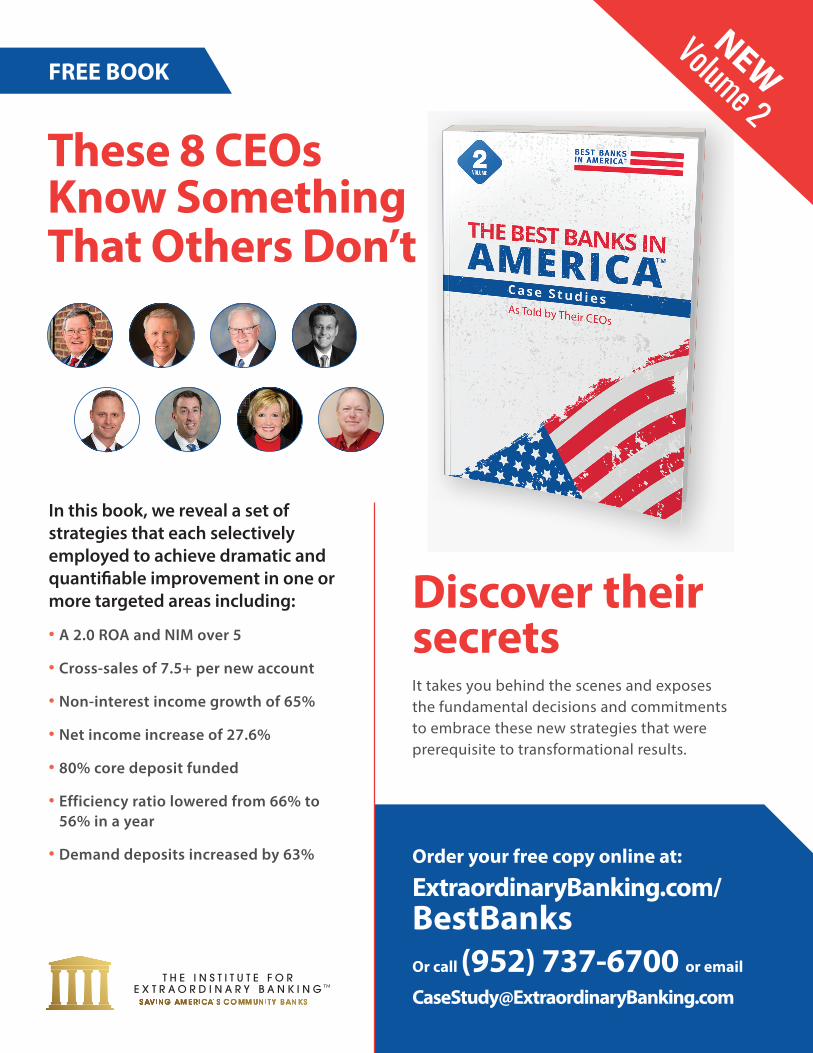

FREE BOOK

These 8 CEOs Know Something That Others Don’t

Discover their secretsIt takes you behind the scenes and exposes the fundamental decisions and commitments to embrace these new strategies that were prerequisite to transformational results.

Order your free copy online at:

ExtraordinaryBanking.com/BestBanksOr call (952) 737-6700 or email

In this book, we reveal a set of strategies that each selectively employed to achieve dramatic and quantifiable improvement in one or more targeted areas including:

• A 2.0 ROA and NIM over 5

• Cross-sales of 7.5+ per new account

• Non-interest income growth of 65%

• Net income increase of 27.6%

• 80% core deposit funded

• Efficiency ratio lowered from 66% to 56% in a year

• Demand deposits increased by 63%

NEW

TM

Volume 2

16 Extraordinary Banker®

CONTINUED from PAGE 14I don’t know if I’m a Top 100 Customer at Commercial Bank, but collectively, we probably are. I know that we get lots of attention from Mercer Capital’s banker, and she has taken care of numerous things for me over the years. They have worked hard to retain me and Mercer Capital as a customer for many years. They are not cheap, but the little bit more they might charge on loans or the little bit less they may pay on deposits have been worth it for many years.

Where am I going to go? How many of your customers are happily in the position I am with Commercial Bank in Memphis?

Two other things to note quickly about Earnings. When you look at the bank, look at staffing levels around the bank and the work loads of employees. Are things reasonably balanced? Over- or under-staffing tends to decrease employee satisfaction and increase staff turnover, which can be an insidious drag on earnings if excessive. Good employees are expensive and hard to find, and when they leave, you lose important parts of your institutional memory and relationships.

In this short discussion of earnings, we have talked about customer retention, cross-selling, incremental pricing, Top 100 Customers, staffing levels and staffing work levels, and staff turnover. Know that when you focus on these things, and when your staff focuses on them, you are focusing on enhancing the Earnings and the Value of your bank.

RISKThe obvious issues regarding Risk relate to loan quality and maturity decisions and deposit maturity and pricing decisions. Let’s broaden the discussion to providing excellent service levels in every corner and department of your

bank. Good service keeps existing customers and attracts new ones. Reducing Risk in this fashion is also helpful for Earnings and Growth.

A high level of staff turnover can also increase the riskiness of your bank’s Earnings and its Value. Excessive turnover, as mentioned, is expensive. Its greatest cost, however, is not seen directly on your bank’s income statement: The real cost of turnover is in lost institutional memory and customer relationships. Turnover can increase the riskiness of your bank’s Earnings and diminish Growth prospects as well.

As you walk around your bank, look through the lens that evaluates risk. Does what you see tend, at the margin, to increase overall Risk or to decrease it?

GROWTHWe all want the balance sheet to grow, fee income to grow, and balance sheet relationships to remain within good ranges. Let’s look at Growth a bit more marginally. Every community bank is in one or more markets, and there is competition in nearly every market. To grow, you can, hopefully, grow with your markets. However, with Growth relatively slow in many community bank markets, that won’t provide the kind of Growth (and Value) you and your shareholders desire.

To grow, you will have to take some market share from your competitors. You can do that by vigorously cross-selling to existing customers and through customer retention. In turn, you do that by providing excellent service, the kind that people talk about, to attract new customers from other financial institutions. You can do that by developing a sales culture in the bank. And you can do that by making your bank an attractive place to work for great

employees while minimizing overall turnover and, hopefully, among your key employees.

WRAP-UPThe Value of your bank is a function of its future Earnings, its Risk, and its expected Growth. Bankers intuitively know this at the time of the annual appraisal (a great idea, by the way), and when they think about Value in planning meetings.

The idea presented in this article is to look at your bank through the lenses of Earnings, Risk, and Growth in your everyday movements about the bank and in your everyday interactions with your employees. The more you do this, and the more of your key leaders who do this, the easier it will be to build the Value of your bank. That is good for customers, your community, all employees, and, of course, your shareholders.

Z. Christopher Mercer is the Founder and CEO of Mercer Capital (MercerCapital.com). Chris is the author of eight books on valuation and a frequent speaker on valuation for banks. He has prepared, overseen, or contributed to hundreds of valuations for purposes related to tax, ESOPs, buy-sell agreements, and litigation, among others.

He can be reached at [email protected]

ABOUT THE AUTHOR

EarningsRisk

Growth

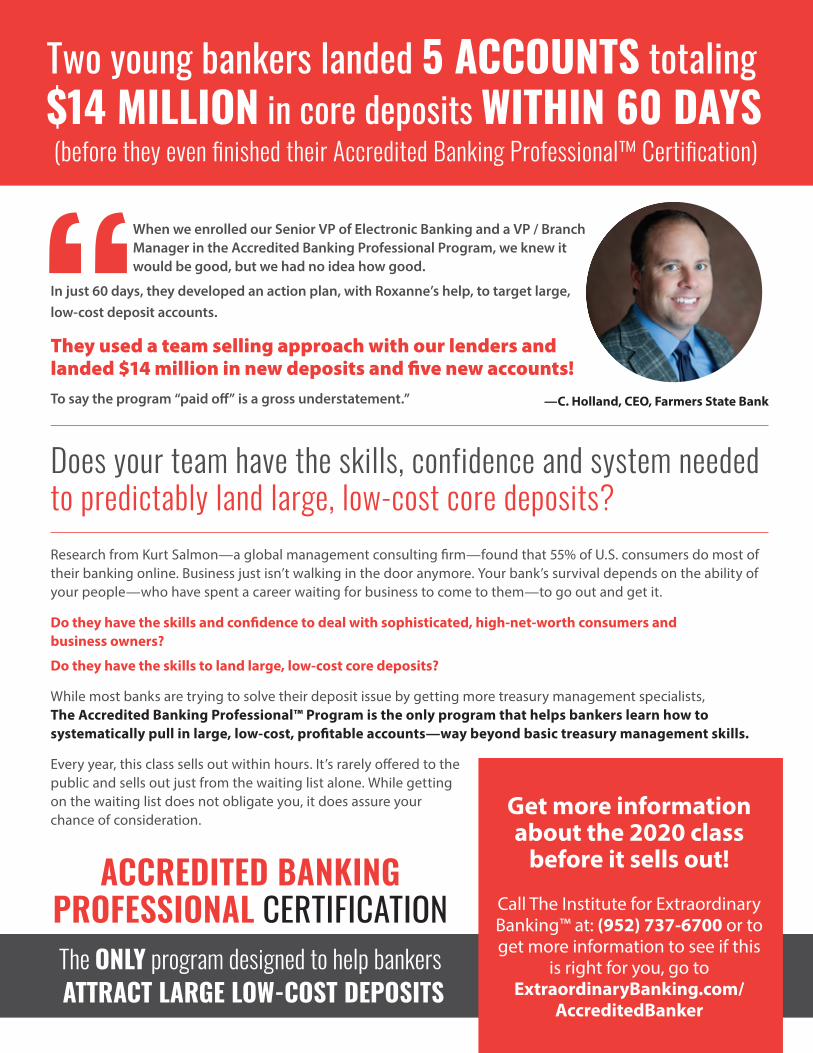

Two young bankers landed 5 ACCOUNTS totaling $14 MILLION in core deposits WITHIN 60 DAYS (before they even finished their Accredited Banking Professional™ Certification)

When we enrolled our Senior VP of Electronic Banking and a VP / Branch Manager in the Accredited Banking Professional Program, we knew it would be good, but we had no idea how good.

In just 60 days, they developed an action plan, with Roxanne’s help, to target large, low-cost deposit accounts.

They used a team selling approach with our lenders and landed $14 million in new deposits and five new accounts!To say the program “paid off” is a gross understatement.”

Get more information about the 2020 class

before it sells out!

Call The Institute for Extraordinary Banking™ at: (952) 737-6700 or to get more information to see if this

is right for you, go to ExtraordinaryBanking.com/

AccreditedBanker

Research from Kurt Salmon—a global management consulting firm—found that 55% of U.S. consumers do most of their banking online. Business just isn’t walking in the door anymore. Your bank’s survival depends on the ability of your people—who have spent a career waiting for business to come to them—to go out and get it.

Do they have the skills and confidence to deal with sophisticated, high-net-worth consumers and business owners?

Do they have the skills to land large, low-cost core deposits?

While most banks are trying to solve their deposit issue by getting more treasury management specialists, The Accredited Banking Professional™ Program is the only program that helps bankers learn how to systematically pull in large, low-cost, profitable accounts—way beyond basic treasury management skills.

Every year, this class sells out within hours. It’s rarely offered to the public and sells out just from the waiting list alone. While getting on the waiting list does not obligate you, it does assure your chance of consideration.

Does your team have the skills, confidence and system needed to predictably land large, low-cost core deposits?

ACCREDITED BANKING PROFESSIONAL CERTIFICATIONThe ONLY program designed to help bankers ATTRACT LARGE LOW-COST DEPOSITS

—C. Holland, CEO, Farmers State Bank

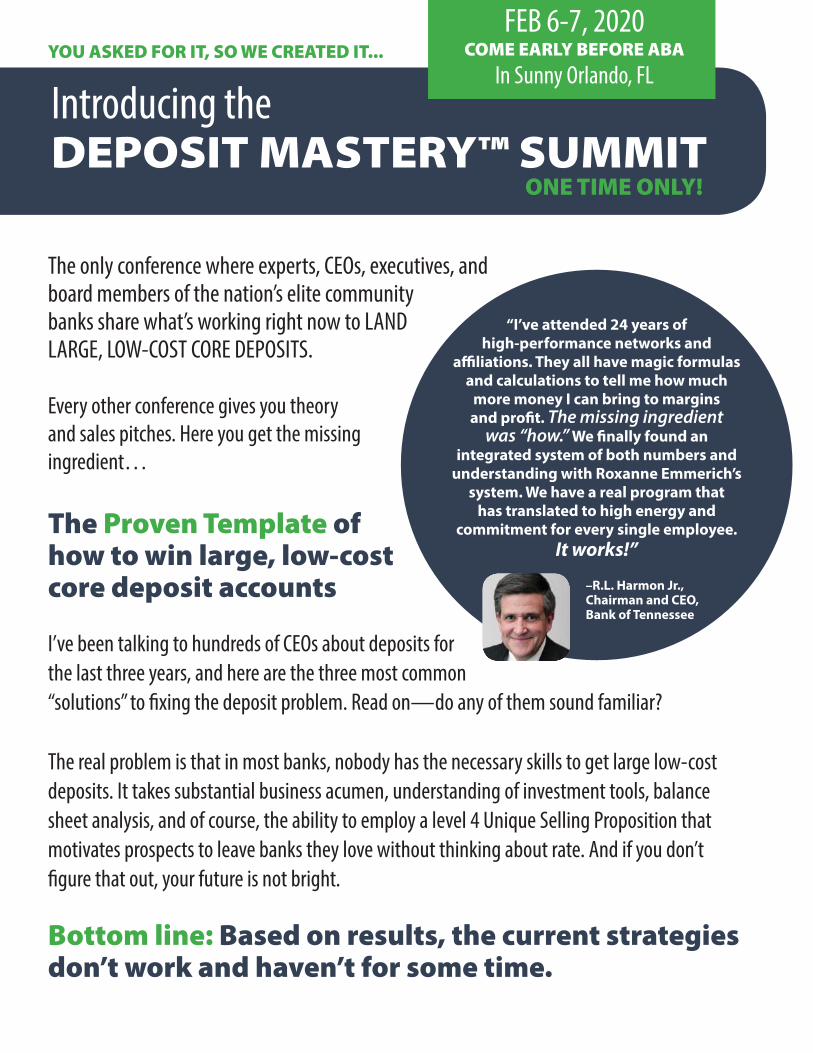

The only conference where experts, CEOs, executives, and board members of the nation’s elite community banks share what’s working right now to LAND LARGE, LOW-COST CORE DEPOSITS.

Every other conference gives you theory and sales pitches. Here you get the missing ingredient…

The Proven Template of how to win large, low-cost core deposit accounts

Introducing theDEPOSIT MASTERY™ SUMMIT

I’ve been talking to hundreds of CEOs about deposits for the last three years, and here are the three most common “solutions” to fixing the deposit problem. Read on—do any of them sound familiar?

The real problem is that in most banks, nobody has the necessary skills to get large low-cost deposits. It takes substantial business acumen, understanding of investment tools, balance sheet analysis, and of course, the ability to employ a level 4 Unique Selling Proposition that motivates prospects to leave banks they love without thinking about rate. And if you don’t figure that out, your future is not bright.

Bottom line: Based on results, the current strategies don’t work and haven’t for some time.

“I’ve attended 24 years of high-performance networks and

affiliations. They all have magic formulas and calculations to tell me how much

more money I can bring to margins and profit. The missing ingredient

was “how.” We finally found an integrated system of both numbers and

understanding with Roxanne Emmerich’s system. We have a real program that

has translated to high energy and commitment for every single employee.

It works!”

FEB 6-7, 2020 COME EARLY BEFORE ABA

In Sunny Orlando, FL

–R.L. Harmon Jr., Chairman and CEO, Bank of Tennessee

YOU ASKED FOR IT, SO WE CREATED IT...

ONE TIME ONLY!

REGISTER NOW FOR “EARLY BIRD” ENROLLMENT Book by Dec. 12, 2019 and save $1,800 on the first executive or board member ticket you buy AND…

Get each additional executive/board member ticket for just $695 (Regular Retail Price is $2,795 per person.)

Because of registrations already booked, we only have seating available for an additional 71 that respond. It will sell out.

Go toEmmerichFinancial.com/

DepositSummit20or Call (952) 737-6730

between 8AM and 5PM Central, M-F

Step 3: Bring Extraordinary ValueINCREASED CORE DEPOSITS 31.1% PER YEAR AVERAGE

“In 2015, we increased average non-interest-bearing deposits by 23.7%. In 2016, we increased them by 31.5%. And in 2017, we increased average non-interest-bearing deposits by 38.2%.”—L. Harrison, President and CEO, Virginia Partners Bank / Maryland Partners Bank

Step 2: Prepare to Win Big Accounts26 OF OUR 29 BANKS ARE ABOVE CORE DEPOSIT TARGETS

“Our focus on the sales process has led to growth in our core deposits, adding significant value to our organization in the long run. Twenty-six of our twenty-nine banks are in excess of their target levels.”—M. Scheopner, CEO and President, Landmark National Bank

Step 1: Go Where the Money Is We landed $14 million in new deposits in just 60 days!

In just 60 days, two of our bankers developed an action plan, with Roxanne’s help, to target large, low-cost deposit accounts. They used a team selling approach with our lenders and landed $14 million in new deposits and five new accounts!—C. Holland, CEO, Farmers State Bank

“We not only met EVERY goal in ALL our

branches, but we exceeded many of our goals by 100 percent! Our entire organization acts like a

team! I can’t imagine any CEO who wouldn’t want this.”

—Chad Hoffman, President and CEO, Richwood Bank2015 Extraordinary Bank of the Year Award Winner

The Only Conference PROVEN to Show You How to Become a Top-Performing Bank

You’ve heard the dreaded “R” word in the news for months now. Will a recession come? Of course. Recessions always follow expansions. And when it comes, the bank in your market with a solid foundation of low-cost core deposits will be positioned to thrive. Banks that don’t get their deposit situation fixed now will be forced to change the signs out front and put someone else’s name up there.

The 2020 Deposit Mastery Summit Gives You the Blueprint for Landing Large, Low-Cost DepositsWe’ve worked with over 300 banks during the last 30 years. Those banks have implemented the blueprint we’ll be sharing with you at the Deposit Mastery Summit, and the results speak for themselves:

�4 out of 5 banks have increased their core deposits from between 12 and 33% in just one year

Over 70% doubled profitability within 36 months

98% doubled cross-sales to new accounts within 5 months

ONE TIME ONLY!

The real progress on the margin is on the deposit side. We have the second lowest cost of funds of any community bank in Utah. And even though rates have moved up, we’ve managed to keep customers.”

John JonesPresident and CEO, First National Bank of Layton

» NIM: 4.77 to 5.11» Efficiency Ratio: 66%

to 56% » ROA: From 1.78 to

2.66

Since 2015 we’ve gone from $6.2 million to $8.18 million in assets per employee. Our profitability has gone up from about $357,000 in the first half of 2015 to $1.1 million in the first half of 2018. Core deposits are up from $182 million to $263 million and assets have increased from $256 million to our current $422 million.”

Lloyd HarrisonPresident and CEO, Virginia Partners Bank

Non-interest bearing deposit growth:

One of the key phrases on our strategic plan is: ‘Do more with less.’ And we’ve done just that. That shows up in our culture scores, and it shows up in our productivity, based on the amount of assets under management per employee. And because we’re doing more with less, we have higher-paid people.

Nevin GrigsbyPresident, Farmers State Bank

» Net interest margin: Up 21 basis points

» Demand deposits: up 63%

» Up 34% in 2015

» Up 36.8% in 2016

» Up 26% in 2017

» Up 23% in 2018

We’ve got 10,000 customers, and they all deserve excellent service, of course. But knowing that those 100-150 best customers are providing over 100% of our net income means we need to focus on them and their health, and getting more people like them, has helped us survive the up and down cycles, which benefits everyone.”

Ben GrimstadPresident and CEO, Decorah Bank & Trust

» Asset growth: 39%» Core deposit growth: 49%» Non-interest income

improvement: 65%

THE BEST BANKS IN AMERICA™

BEGAN THEIR TRANFORMATION AT ANEMMERICH EVENT

Register today at BestBanksinAmerica.com or call (952) 737-6700.

Extraordinary Banker® 21

Roxanne: Chris and his bank just took home the 2019 Extraordinary Bank of the Year™ award at the Bankys, and he has quite a story. Can you tell us about some of the things you’ve accomplished over the last couple of years that you’re most excited about?

Chris: Well, winning the Banky™ Award is pretty cool. In going through the process of trying to win the award, you have to look back at what you did because it’s easy to get lost in the day to day of helping customers, but a lot of our customers helped us rebuild that history of service, which was really nice. They gave us some amazing stories about how our work has impacted their lives, and I thought: “Wow, we are making a difference.”

Roxanne: So many great stories there. I remember hearing about how you helped to mastermind a way to bring a large dairy into the market when you realized that there needed to be jobs created. You stepped in to help create a tremendous number of jobs.

SNL has acknowledged you as one of the top 100 US banks under $1 billion for two out of the last three years. I’m sure it’s been quite a journey to get to numbers like that. Many banks would aspire to those kinds of numbers. Can you tell me what things were like prior to you starting that journey?

Chris: We felt like we worked hard at it and tried to do everything we could, but we just never really got anywhere. We were stuck in the middle of the pack. The biggest change now is that our efforts

CONTINUED on PAGE 22

NOT MAGIC, JUST FOCUS” HOW A SMALL-TOWN BANK FROM KANSAS BECAME ONE OF THE BEST BANKS IN AMERICA

Roxanne Emmerich: I have the great honor today of introducing you to Chris Floyd, CEO of First National Bank of Syracuse. Chris is quite a rock star in the banking industry right now.

Chris Floyd: Thanks for that, Roxanne. Our bank was chartered in 1906 in Syracuse, Kansas, which is on the far western edge of the state, about 15 miles from Colorado. Over the years, we’ve ended up with five branches and four locations, mostly in pretty rural areas. Ag-focused for the most part, we have diversified over the years as well. We’re a family-owned bank trying to help people as we can.

We were stuck in the middle of the pack. The biggest change now is that our efforts are finally

showing up in the numbers, which is validating. -Chris Floyd

Chris Floyd and Roxanne Emmerich with the First National Bank Team

at the 2019 Banky™ Awards

A Conversation with First National Bank of Syracuse CEO Chris Floyd

22 Extraordinary Banker®

CONTINUED from PAGE 21are finally showing up in the numbers, which is validating.

Roxanne: So, working hard wasn’t the only formula. What are some of the systems or processes that were core to helping you create those numbers that skyrocketed?

Chris: We bought some branches in Garden City, which is kind of the hub in our area. Soon our assets doubled, and our employee count doubled. It was harder to manage than we expected. How we managed the bank had to change, all the way down to the frontline tellers. We had to do things differently. And once we had new systems in place, when we bought the next one in Ulysses, we simply dropped those proven systems into place.

Roxanne: Tell me a little bit about how you created the dramatic shift in your key metrics. You’ve had a pretty dramatic increase in core deposits. A lot of executives will say it can’t be done, so I’d like them have hope by hearing your story.

Chris: When we started, we were right at $200 million in assets. Today we’re $345 million and about to hit $360 million—that’s over a 70% increase. We used to think 3-5% was good growth. Well that’s really not growing—that’s just kind of keeping up. It’s better than some banks, but it really wasn’t what we needed or where we wanted it to be. In that same period, we’ve more

than doubled our loans. We’re trying to provide significant value for our customers and help them.

Roxanne: So, your net interest margin actually went up while you grew markedly and improved your credit quality—and you’re right in the middle of Farm Credit country. Whenever I hear bank CEOs say the words “Farm Credit,” the next words are always: “you just have to match their rates.” But you don’t match their rates at all. You manage to command premium pricing every single time. Tell me a little bit about how you’re pulling that off.

Chris: I’ve always figured that if we’re just a source of money, we’re just a commodity, and then we’re really not providing anything of value. A customer like that can get money anywhere, and we’re really not making a difference in people’s lives and not trying to impact them. So we set up several systems to help our customers be more profitable to start with. How can we help protect them from risk? Helping increase earnings, reducing expenses, and doing the analysis for them are things that a lot of times they don’t have the time or skill to do.

Roxanne: You’ve had a pretty remarkable shift in core deposits, which

is a critical number to be moving these days.

Chris: It’s really not magic—just a matter of focus. It has helped quite a bit to know that we’ve got to get the deposits when we get loans.

Roxanne: Culture is the hot word right now, although I don’t think a lot of bank executives really understand what bank culture means. Yours is not just a culture where people love to be at your bank, it’s also a culture where everybody knows how they tie to profit on a daily, weekly, monthly, and quarterly basis.

Chris: That’s one part that really changed quite a bit for us. When you mention culture, some people think of ping pong tables in the basement, goofy things like that to make the experience better. But there’s a way you can actually be highly productive, have a lot of fun, engage your employees, and let them be themselves as well.

It’s made a huge difference. And a lot of it really is set in our core values. I like talking about just being excellent. There can be a negative mindset about being good, so we want to be excellent. We encourage our employees to know everything that we do, from simple teller interactions to how we handle big,

We used to think 3-5% was good growth.

Well that’s really not growing—that’s just kind of keeping up. We’ve seen 70%

growth in 6 years. -Chris Floyd

Chris Floyd (L) with Roxanne Emmerich at the 2019

Banky™ Awards

Extraordinary Banker® 23 CONTINUED on PAGE 24

complex customers. We want to do the best we can. We’re not striving just to survive. And once we start with a mindset like that, then everybody’s like, okay, this is what we’ve got to do.

At the same time, you have to get the difference between just being nice and really holding people accountable, so we can get where we all want to be. Rooting out the bad behaviors that nobody likes in the workplace is always a work in progress.

Roxanne: Nothing warms my heart more than when I’m talking to one of your team members and they say something like: “We closed 37 of our top 100 prospects already this year, and it’s only June.” Everybody knows the few metrics that really matter. They know the ones that move the profit and growth needles while minimizing the risk to the organization.

Bank CEOs always tell me that before they embark on a journey like this, there is always some trepidation. What kind of things might have kept you from moving ahead in the beginning?

Chris: Part of it was selling the idea to the board of directors and senior management, especially around the word “culture.” They think it’s a lot of fluff. But this was action and usable tools. That’s the best part: I have a toolbox to grab a tool from if I need to fix something. It’s right there.

Roxanne: One of your guys told me that he was the “chief eye roller”

when you first started. Now his portfolio is four times the size it was just four years ago. He said he stopped eye rolling, which I thought was an adorable confession. I think every CEO knows that when they embark on something new that they know in their gut is the right thing, they’re going to have some chief eye rollers pulling back just as hard as they’re trying to push ahead. So, congratulations for continuing to push ahead and getting the rest of the eye rollers along on your team.

Now, tell me, what were the things that were most important in creating these admirable shifts of performance in almost every key metric?

Chris: After culture, probably the biggest tool we used was the Profit-Rich Sales™ process. Some people will call and say: “Hey, how are you really using this?” We just did whatever they told us to do and tried to follow the process. We’re not trying to outsmart ourselves thinking we can figure out a better way because it’s pretty well laid out, and it’s not rocket science. This is a proven process that will work—you just have to keep at it.

Roxanne: If you were talking to someone who was in the shoes that you were in when you first started your journey of transformation, what would you tell them?

Chris: Well, you’ve got to soul-search. Are you really committed to being extraordinary? Do you want to be one of the banks that survives? You talked about the hard trend of decline

That’s the best part: I have a toolbox to grab a tool from if I need to fix something.

It’s right there. -Chris Floyd

FIRST NATIONAL BANK OF SYRACUSE WINNING STATSFrom June 2013 to June 2019

• Total Assets (000) Start 199,728 End 345,284

• Total Loans (000) Start 139,723 End 279,350

• Total Deposits (000) Start 171,846 End 287,500

• Core Deposit (000) Start 112,400 End 219,370

• Net Income (000) Start $1,210 End $2,693

• 12-Month Total Profit (000) Start $2,533 End $5,245

• NIM Start 4.38 End 4.67

• Assets Per Employee Start 3.99 End 6.28

• ROA Start 1.19 End 1.56

• ROE Start 10.03 End 14.19

• Cross-Sales Start 2.2 End 8.12

24 Extraordinary Banker®

CONTINUED from PAGE 23

in banks. Ever since I started in banking, there has been a steady decrease in the number of banks in the country. That’s one thing that drives us every day: yes, we want to be one of the ones that are still here, not only surviving but thriving. You make that decision, then you go for it and figure it out, using a system to get yourself there.

Roxanne: One of the things I love about you, Chris, is you’re always celebrating the huge progress you’re making, and you have made staggering progress every single year in terms of profitability, net interest margin, growth in deposits, and growth in loans. And yet you’ve never said “good enough” or

“I guess we’ve got this all figured out.” You’re always, always, always seeking the next piece. As we’ve gone from 18,000 banks on our journey down the hard trend line toward 2,000, I’ve seen that the ones that are next to go out of business often thought they were having a good year because the economy was good. They’re not hungry to get to the next level, and before you know it, they’re gone.

You’ve become not just “bank smart,” but “leadership smart.” What’s your mantra right now?

Chris: We just have to have the mindset that nobody’s going to show up to help us. We’ve got to just figure it out and get moving. Complacency can destroy things pretty fast. If you’re not growing, eventually people will pass you by. It’s like we’ve ramped up the leadership skills of the entire bank. We have to grow and change all the time. How can

we do this better? How can I be better? How can every employee be better in every part of their job?

I remember reading the book Only the Paranoid Survive by Andrew Grove. He came to the U.S. from Hungary knowing that if you don’t fear for your life every day in business, you can get swallowed up fast. I figure I’m on a day-to-day contract, and I fight for that mindset in our bank. We fight to earn our customers every day, and nothing’s given to us.

Roxanne: Your customers are lucky to have you in your community. What you do to support your customers and community is legendary. As they say, the way to be successful is to help others be successful. You’ve done that in spades, and so has your team. Congratulations.

Chris: Thank you very much. We appreciate it.

Chris Floyd and his team began their transformation to become one of the Best Banks

in America™ at an Emmerich event. Your next opportunity is February 6-7, 2020

at The Deposit Mastery™ Summit.

Get all the details and register your executives at EmmerichFinancial.com/DepositSummit20

We’re not trying to outsmart ourselves thinking we can figure out a better way because it’s pretty

well laid out, and it’s not rocket science. This is a proven process that will work—you just have to keep at it. -Chris Floyd

I remember reading the book Only the Paranoid

Survive by Andrew Grove. He came to the

U.S. from Hungary knowing that if you

don’t fear for your life every day in business, you can get swallowed

up fast. I figure I’m on a day-to-day contract, and I fight for that mindset

in our bank. We fight to earn our customers every

day, and nothing’s given to us. -Chris Floyd

The CEO Roundtable Exclusively for High-Performing Banks

The Council™ roundtable is the only “home” for CEOs who choose to play at the highest level in the industry—to escape commoditization, be the acquirer (not the acquired), and

lead a team that wins at the game of banking.

“This is my Board of Advisors. My board doesn’t push me enough, challenge my ideas enough... I need to be around the real industry transformers. That’s why I come.”

THE COUNCIL™

“ I stopped going to most bank CEO conferences–they’re talking about things you taught us almost 20 years ago as if they are new ideas.” – P. Steele, CEO, First Volunteer Bank, Extraordinary Banking Hall of Fame Inductee

Download a prospectus and application atExtraordinaryBanking.com/Council

“ A great program to become a better executive and an even better program to become a greater human being.” – C. Holland, CEO,

Farmers State Bank of Alto Pass

26 Extraordinary Banker®

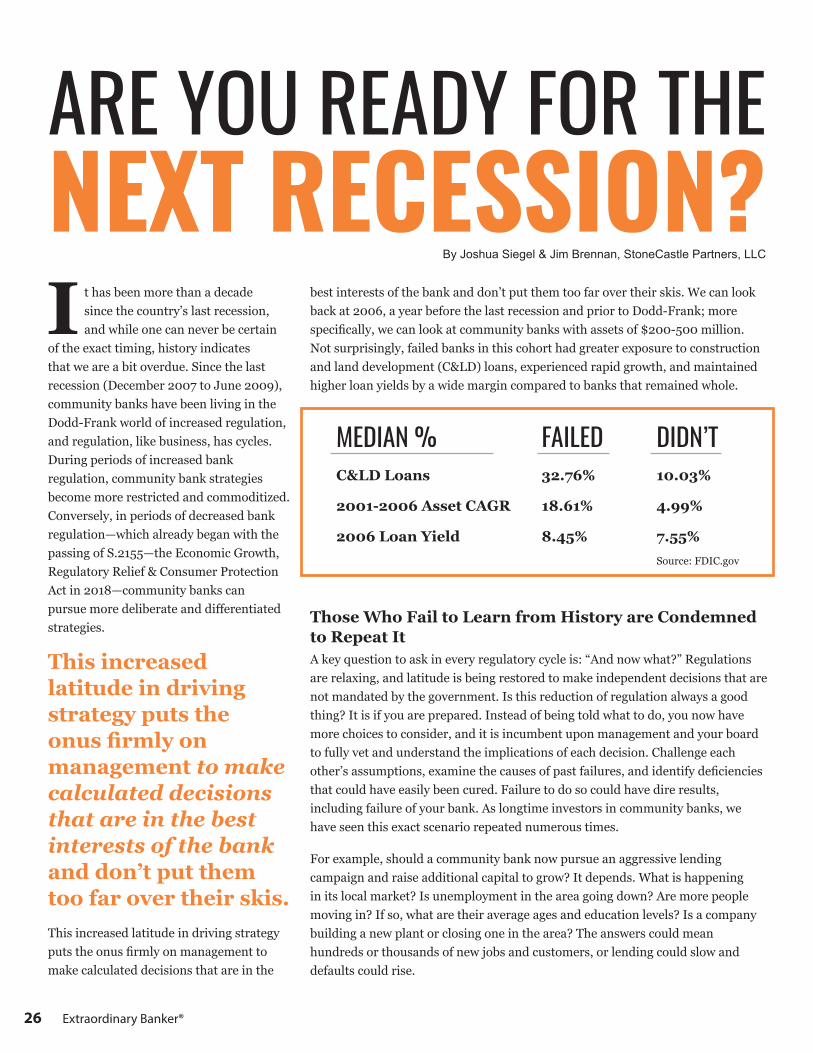

t has been more than a decade since the country’s last recession, and while one can never be certain

of the exact timing, history indicates that we are a bit overdue. Since the last recession (December 2007 to June 2009), community banks have been living in the Dodd-Frank world of increased regulation, and regulation, like business, has cycles. During periods of increased bank regulation, community bank strategies become more restricted and commoditized. Conversely, in periods of decreased bank regulation—which already began with the passing of S.2155—the Economic Growth, Regulatory Relief & Consumer Protection Act in 2018—community banks can pursue more deliberate and differentiated strategies.

This increased latitude in driving strategy puts the onus firmly on management to make calculated decisions that are in the best interests of the bank and don’t put them too far over their skis. This increased latitude in driving strategy puts the onus firmly on management to make calculated decisions that are in the

ARE YOU READY FOR THE NEXT RECESSION?

By Joshua Siegel & Jim Brennan, StoneCastle Partners, LLC

best interests of the bank and don’t put them too far over their skis. We can look back at 2006, a year before the last recession and prior to Dodd-Frank; more specifically, we can look at community banks with assets of $200-500 million. Not surprisingly, failed banks in this cohort had greater exposure to construction and land development (C&LD) loans, experienced rapid growth, and maintained higher loan yields by a wide margin compared to banks that remained whole.

Those Who Fail to Learn from History are Condemned to Repeat It A key question to ask in every regulatory cycle is: “And now what?” Regulations are relaxing, and latitude is being restored to make independent decisions that are not mandated by the government. Is this reduction of regulation always a good thing? It is if you are prepared. Instead of being told what to do, you now have more choices to consider, and it is incumbent upon management and your board to fully vet and understand the implications of each decision. Challenge each other’s assumptions, examine the causes of past failures, and identify deficiencies that could have easily been cured. Failure to do so could have dire results, including failure of your bank. As longtime investors in community banks, we have seen this exact scenario repeated numerous times.

For example, should a community bank now pursue an aggressive lending campaign and raise additional capital to grow? It depends. What is happening in its local market? Is unemployment in the area going down? Are more people moving in? If so, what are their average ages and education levels? Is a company building a new plant or closing one in the area? The answers could mean hundreds or thousands of new jobs and customers, or lending could slow and defaults could rise.

MEDIAN %C&LD Loans

2001-2006 Asset CAGR

2006 Loan Yield

FAILED32.76%

18.61%

8.45%

DIDN’T10.03%

4.99%

7.55%Source: FDIC.gov

I

Extraordinary Banker® 27

Preparing for All Scenarios Capital solves two primary issues: funding growth and withstanding periods of stress and credit losses. If your bank doesn’t raise enough capital to fund growth, you can quickly miss out on upswings in the area and lose local market share to competitors that thoughtfully raised capital to position their banks to better appeal to new clientele and future bank needs.

Alternatively, we have seen many banks fail because they underestimated the amount of capital needed to absorb losses. They argue, rather shortsightedly, that they don’t want to suffer the dilution of raising more capital, which is typically the first phase on the path to the ultimate dilution—failure—because 100 percent of nothing is still nothing.

We believe that a proven solution for smartly raising capital is the use of subordinated debt at the holding company and preferred stock (if available). While both carry a cost per annum, it is typically nominal compared to common equity and does not cause any dilution. Also, unlike dilutive common equity that cannot be redeemed, your bank can “undo” issuing subordinated debt or preferred stock since both have a call date to redeem the capital at 100 percent of face value.

There’s no such thing as too much capital during a recession, which is also the most difficult time to obtain it. Challenge each other. Discuss the uses of capital and how to deploy it for growth or use as dry powder in a market downturn. It has been just over a decade since the end of the last recession, so now is the time to discuss how your bank will be prepared. There’s no such thing as too much capital during a recession, which is also the most difficult time to obtain it. Subordinated debt currently remains available to community banks as an economically efficient way to address capital needs, including the pending changes from CECL.

Be prepared for the next recession. Give the past a closer look and consider the following:

1) Be extremely mindful when growing your construction loan book.2) Keep growth rates in check. If you decide to outgrow your peers, consider: a. If you want to grow faster than

local GDP, you need to take loans away from other banks by taking higher risks or accepting lower yields, both of which create risks for your bank.

b. M&A is often a safer growth strategy than significant organic growth, especially out-of-footprint expansion.

c. It’s always better to compromise on loan pricing than lending criteria.

d. Don’t stretch the amount or quality of capital to get there—during a recession, the more capital, the better.

3) Be cautious of chasing new lending strategies to increase loan yields. Marketplace lending and renewed interest in SBA lending can be an option, but consider all the risks attached to these programs, and ask yourself if you are truly being compensated for the added risk.

History tells us there will be another recession, and it may not be that far away. Listen to what it is saying.

About StoneCastle Partners Founded in 2003, StoneCastle Partners is one of America’s largest asset management firms dedicated to the U.S. banking sector and a recognized cash management leader for institutional investors. With over $20 billion in assets under management and advisement, StoneCastle Partners and its subsidiaries offer solutions that help address the needs of community banks as well as the investment community.

Notes & Disclosures The information contained in this article is for informational purposes and should not be construed as investment advice or an offer, solicitation, or recommendation to purchase any security. The views are as of the date of this article and are subject to change.

Connect with the Authors:

Joshua Siegel StoneCastle Partners, LLC 347-887-0303 [email protected]

Jim Brennan StoneCastle Partners, LLC 347-887-0326 [email protected]

28 Extraordinary Banker®

Three banks—Decorah Bank and Trust, Pioneer Bank, and First National Bank of Syracuse—competed as finalists for the Best Banks in America™ Extraordinary Bank of the Year designation. Each shared a story of breakthrough and told how they have taken their banks from success to significance.

This year’s three judges—Chris Mercer of Mercer Capital; Ken Derks, Managing Director of Equias Alliance; and James Brennan, Director of StoneCastle—balanced their votes with audience polling for the selection of the 2019 Extraordinary Bank of the Year designation.

First National Bank of Syracuse was this year’s award recipient. They received a sponsorship of $25,000 for a school in Africa as well as a Ford Escape wrapped in their branding to keep as a way to tell their story in their community for years to come. First International Bank and Trust was inducted into the Extraordinary Banking Hall of Fame. President Peter Stenehjem shared their entrepreneurial journey and how they have radically transformed their client experience that now regularly garners over 7 cross-sales on all new accounts.

A panel of bank CEOs— First National Bank of Syracuse CEO Chris Floyd, Farmers State Bank of Alto Pass CEO Charles Holland, and Citizens Bank of Lafayette CEO Peter Williston—shared what they were doing to grow deposits and garner

substantial NIM growth while decreasing risk. They also described how they keep their performance culture supporting breakthrough numbers to a level most banks never dream of—making it all real and doable for those in the audience.

The highlight was the “open space” forum—a structured way for bank executives to get their hardest questions answered fast by experts and other bank CEOs in a rapid-fire approach of “figure it out” meetings where best practices were shared and breakthrough thinking stimulated. Popular topics this year included how to build deep relationships with the digital-centric customer; how to improve communication with branches and team members; how to implement new technologies, such as rolling out a new core provider, without disrupting the bank’s productivity; and even how to attract new commercial lenders to a market where nobody wants to live.

Next year’s headliner keynote for the 2020 Best Banks in America™ Super Conference is Dan Diamond, MD, Director of the Medical Triage Unit at the New Orleans Convention Center following Hurricane Katrina. Dr.

Diamond led the charge of medical first responders into Haiti, Puerto Rico, and New Orleans after Katrina and will share his insights into why some people are unstoppable during challenging times while others demonstrate the worst of human nature.

Dan feels that Gallup has done a huge disservice to America by claiming that in order for people to be engaged, they need to first “have what they need” to do their job. In fact, engagement really is all about accomplishing things without the necessary resources—it’s about being able to get results regardless of circumstances.

Take advantage of early registration pricing for next year’s 7th Annual Best Banks in America™ Super Conference

now by going to

Bring your entire executive team and board.

Some CEOs believe they can’t afford the time away from the bank to attend. The real question is: Can you afford not to?

Dale McGowan, PhD is the author/editor of ten books and more than 700 articles on subjects from communications to business to parenting. He lives in Atlanta and teaches at Oglethorpe University.

ABOUT THE AUTHOR

CONTINUED from PAGE 6

BestBanksinAmerica.com

First National Bank of Syracuse was this year’s award recipient. They received a sponsorship of $25,000 for a school in Africa as well as a Ford Escape wrapped in their branding to keep as a way to tell their story in their community for years to come.

THEY LAUGHED WHEN I SAID WE’D GET NET INTEREST MARGIN OVER 5

“Our net interest margin is now over 5.0, an increase of over 40 basis points in the past year. Our three-year goal for net income was realized in the first year working with The Emmerich Group. We need to set our goals higher!”

Qualifying Bank Executives*, Request Your FREE Copy of

“THE NET INTEREST MARGIN SOLUTION”

*Qualification Criteria: To qualify for this valuable FREE copy of “The Net Interest Margin Solution,” you must be a senior vice president or higher in a community bank with assets of $150 million or more. If you meet these criteria, don’t wait. Discover how to finally get the pricing you deserve today!

Call: 952-737-6730 or visit:

NetInterestMarginSolution.com/EB

THEY’RE NOT LAUGHING NOW

C. Floyd, CEO/President | FNB Syracuse Ranked #2 bank under $1 billion by SNL

If your lenders are lined up outside your door saying, “We can do this deal if we match the rate,” you NEED this book!

30 Extraordinary Banker®CONTINUED on PAGE 32

ith BMO Harris, Wells Fargo, and TIAA Bank all offering rates from 1.9%

to 2.2% on money markets, we’re in a whole new kind of pressure cooker to get and keep low-cost deposits.

You can throw in the towel and match rates, or

run CD specials that skyrocket your cost

of funds.

Or you can master how to attract low-cost deposits by getting yourself out of the

commodity game once and for all.

I recently met with an executive

team whose CFO made a comment that still rings in my

ears: “Well, of course we have to match the rates—banking is a commodity.”

He declared it as definitively as many once said the world was flat.

Well, he’s right in a way, but consider this: Everything is a commodity game—until it’s not.

For example, coffee was a commodity until Starbucks came along, reinvented the category, and started charging not 10 percent more but 10 times more.

A Lexus 350 ES with a base price of $45,000 is essentially the same car as a $25,000 Toyota Camry, with perhaps an extra $1,000 cost of goods in gadgets.

Every smart business must figure out how to move itself out of the commodity pricing of its industry, and banking is not an exception.

The conventional wisdom has solutions for how to attract deposits:• You advertise rates in the paper.• You do promotional product

mailings.• You do “sales training.”• You match rates as people walk

in the door. • You create incentives for your

team to attract deposits. • You offer cash management.

If these are your strategies to compete when every bank is desperately and aggressively going after the same deposits, and it’s not working for you—you’re not alone. Each of these is failing for its own reasons.

Almost every bank is trying those old strategies that used to work and

HOW TO ESCAPE COMMODITY-VILLE: A Predictable “Franchise System” for Landing LARGE, LOW-COST DEPOSITS in Any Market

By Roxanne Emmerich

WEvery

smart business must figure out

how to move itself out of the commodity pricing of its industry, and banking is not

an exception.

Finally, the Answer to Banking’s Biggest Recurring Challenges

The Breakthrough Banking™ Webinar Series

“Roxanne showed us how to double our growth. We hit our loan growth goal for the year by the end of June… in our first year, with Roxanne Emmerich’s help! We’ve had employees in banking for 20 to 30 years who say they wish they’d started this program 20 years ago.”–Chris Floyd, CEO and President, First National Bank of Syracuse

• 2019 Extraordinary Bank of the Year • Named #2 Bank Under $1 Billion by SNL

Register now for this new monthly webinar series:

EmmerichFinancial.com/BreakthroughWebinar

Join Roxanne Emmerich and the CEOs of top-performing banks as they present profound and practical solutions to banking’s biggest challenges:

• Driving consistent loan growth (with A+ quality credits)

• Landing large, low-cost, sticky deposits

• Increasing Net Interest Margin with far less risk

• Cloning your 100 most profitable customers every year

• Aligning everyone in the bank to profit daily, weekly, and monthly

• Building a predictable success franchise system that just works

NEW!

32 Extraordinary Banker®

CONTINUED from PAGE 30wondering why they don’t seem to be working now.

If you’re trying these “tried and true” strategies and they’re not working, it’s not your fault. Sadly, very few banks seem to know what really works.

Yet some banks are growing core deposits at a record pace—all with some of the lowest deposit rates. What do they know that you need to discover quickly before it gets too hard to turn the ship around?

First, they understand that it’s not one thing. In fact, most “one things”—such as incentive pay, sales training, product mailings, and “specials”—don’t work individually and don’t work in combination, either.

The right system builds on the foundation of what really is working today: bringing exceptional value so far beyond “great service” that your clients will say they can’t afford to be without you.

The deposit attraction “franchise system” must be well thought out and must consider the following critical steps.

Step 1: Determine Who Is in the Small Group of Your Highly Desirable Prospects

Don’t fish the entire lake—fish in the fishing hole. There is a small group of people who have large deposits and consider many things to be more important than the rate on them. It’s a small group, but it is a mighty one.You need a system to find those people and businesses. With certainty and precision, you must identify that next group of Top 100 prospects.

Step 2: Lift Yourself Out of the Commodity Marketplace in the Minds of those Prospects

Once you know who has those large deposit accounts, you must figure out how to put yourself in a category of one—to have something of extreme value to those people that is offered by no one

else. It must be compelling enough that they can’t

afford to stay with a bank, credit

union, or mutual fund that pays more. That is the ticket. If you think it

can’t be done, you are correct

because you will not do what is

necessary to make it work. However, for those

curious enough to wonder how others are doing it, there is hope.

Step 3: Create a “Reputational Excellence” System to Build a Solid Relationship with Those Targeted Best Prospects Before You Ever Talk to Them

One of the worst mistakes banks make is the “officer call program,” which puts perfectly good humans in the position of losing all dignity because they were set up to look like salespeople—instead of professionals to be sought out and admired for their great insights and ability to make an impact.

One of the worst mistakes banks

make is the “officer call program,” which

puts perfectly good humans in the position

of losing all dignity because they were set

up to look like salespeople

CONTINUED on PAGE 34

If you think it can’t be done,

you are correct because you will not do what is necessary to make

it work. However, for those curious enough to wonder how others

are doing it, there is hope.

Extraordinary Banker® 33

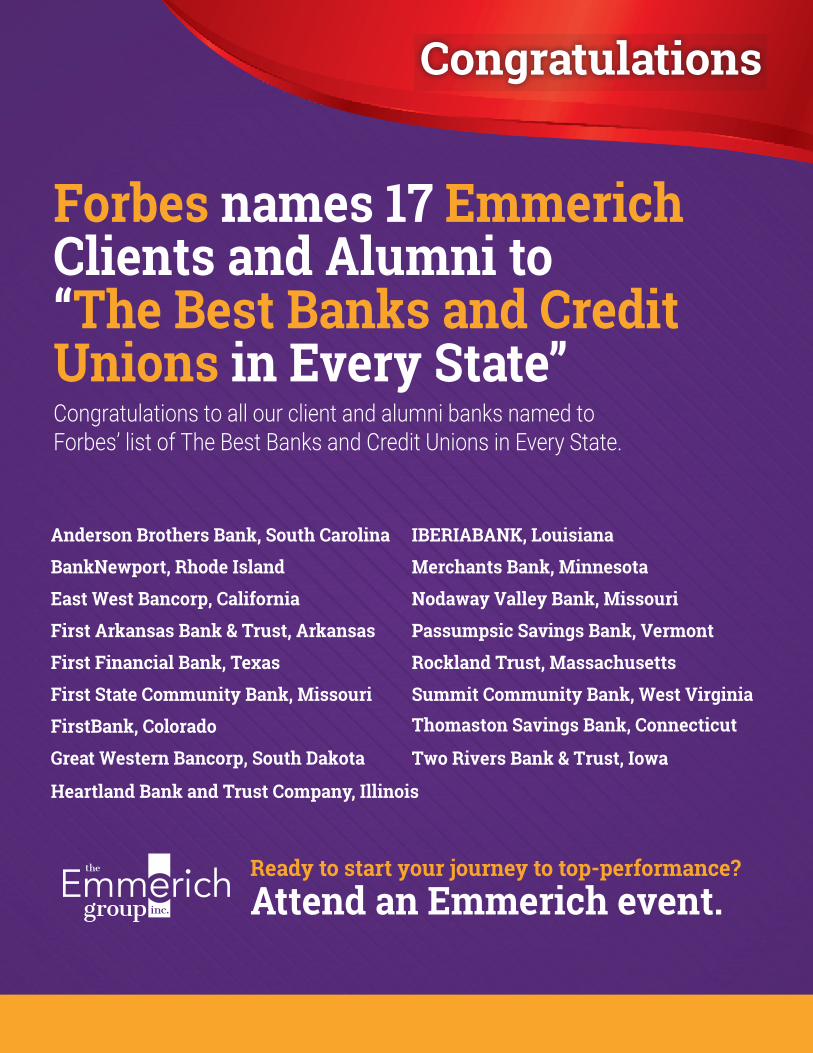

Forbes names 17 Emmerich Clients and Alumni to“The Best Banks and Credit Unions in Every State”Congratulations to all our client and alumni banks named to Forbes’ list of The Best Banks and Credit Unions in Every State.

Anderson Brothers Bank, South Carolina

BankNewport, Rhode Island

East West Bancorp, California

First Arkansas Bank & Trust, Arkansas

First Financial Bank, Texas

First State Community Bank, Missouri

FirstBank, Colorado

Great Western Bancorp, South Dakota

Heartland Bank and Trust Company, Illinois

Ready to start your journey to top-performance?

Attend an Emmerich event.

Congratulations

IBERIABANK, Louisiana

Merchants Bank, Minnesota

Nodaway Valley Bank, Missouri

Passumpsic Savings Bank, Vermont

Rockland Trust, Massachusetts

Summit Community Bank, West Virginia

Two Rivers Bank & Trust, Iowa

Thomaston Savings Bank, Connecticut

34 Extraordinary Banker®

As Mark Schaefer, one of today’s leading marketing minds, puts it in his book Marketing Rebellion: “The most human company wins.”

And as the late Zig Ziglar, who I listened to weekly in my formative career years, said so well: “The best way to get what you want is to help enough other people get what they want.”

It is only by obsessing over how to add value to each unique human in your small hit list of most desirable prospects that you can truly attract all their business without rate mattering hardly at all.

If you don’t believe that it can happen, that only means you haven’t made it happen yet. Only through an open mind can you fix a recurring issue.

Step 4: The Right “Smarketing” System

Have you done A/B split testing to determine the optimal way to bring in a $5 million business checking account without price being an issue and to know exactly how to get the highest close ratio? If not, then you need to learn from those who are enjoying a close rate of over 85 percent on prospects who, quite frankly, love their current banks and weren’t looking to change banking relationships.

Let’s face it: Those are the only people you want. They are the most likely to be loyal to you once you attract them away from their incumbent banks. And they aren’t even looking.

To grab their attention well enough for them to endure the pain of switching banks, the flow chart of the optimal system executed precisely should garner a close rate of over 85 percent. If your system doesn’t get that rate, you have the wrong system.

The problem with the wrong system is that if you don’t earn the respect of the affluent immediately and get them to switch within a week or two of the first meeting, they will kick you to the curb for wasting their time and not give you another chance for at least a decade. Remember, there aren’t that many highly desirable prospects with large balances who would consider investing funds with you at a lower rate. You can’t afford to experiment with these folks. You need the right system in place from the beginning.

Step 5: Expect and Inspect 100 Percent Compliance to the “Magnetic Deposit Attraction” System

Ego is the enemy of great results. You have an issue if people on your team chant to the new people around them: “Hey kid, don’t get too excited. I’ve been doing this for 30 years and hey, it works. Just do what I do.”

The issue is that those well-intended but ill-advised old-school lenders aren’t getting that 85 percent close rate and they continue to match rate on what they do close. So, although their system has “grown their portfolio,” it hasn’t grown it for maximum safety, premium pricing, and portfolio retention—the things that really matter to grow your franchise value.

Again, ego is the enemy. If you have people who won’t follow a system that works because they are unwilling to try, evangelizing instead that it can’t be done, they hold your entire organization hostage to operating well below your potential.

If you’re serious about pulling ahead of your competitors in attracting and

keeping low-cost deposits, attend the one-time

only special session I’ll be doing this

February: The Deposit Mastery™ Summit.

Bring your entire

executive team and

perhaps a few board members.

This is a strategic issue, and if your executive team

doesn’t understand the land, sea, and air integrated system, the shift of results would be minimal and not sustainable. That said, there will be many banks attending whose teams have doubled their core deposits in just a few short years—and are hungry for more.

Go to EmmerichFinancial.com/ DepositSummit20 now to determine who should attend with you.

The real question is: Can you afford not to attend?

Roxanne Emmerich is the Founder of The Institute for Extraordinary Banking™, Editor of Extraordinary Banker® magazine, and CEO of The Emmerich Group®. For nearly 30 years she’s shaped the thinking and the results of The Best Banks in America™.

She can be reached at [email protected]

ABOUT THE AUTHOR

CONTINUED from PAGE 32

Again, ego is the enemy.

If you have people who won’t follow a system that

works because they are unwilling to try...they hold

your entire organization hostage to operating

well below your potential.

FINALLY, THE BLUEPRINT

for High-Performance Banking