confidential 2013 1 a payments approach to checking revenue compliant fees consumers willingly pay

TRANSCRIPT

1Confidential

2013

A Payments Approach to Checking Revenue

Compliant Fees Consumers Willingly Pay

2Confidential

Contents

• Introduction• A Payments Approach to DDA Revenues• Your Revenue Opportunities• Engagement

3Confidential

Introduction

• 2012 – Present, President and CEO – R.C. Giltner Services, Inc.

4Confidential

A Payments Approach to DDA Revenues

Service Charges on Deposits Banks < $10 Billion, 2009 - 2012

While service charges on deposits are falling, “payments” providers like PayPal are growing revenues over 20% annually.

Source: FDIC, PayPal, in millions

PayPal Revenues2009 - 2012

Confidential 5

A Payments Approach to DDA Revenues

The “payments” revenue strategy is exploding.

Scan & Pay

6Confidential

A “payments” approach to segmenting and pricing transaction services is winning relationships and earning fees consumers willingly pay.

– Financial institutions focus on “accounts,” which still provide settlement, but their value is at the bottom of the pack in the hierarchy of consumer payment methods, venues and management.

– Payment providers create value by focusing on the use, context and experience of specific payments, such as where the payment occurs or the context of before or after the payment.

– Use, context and experience segmentation of individual payments drives new revenue and value that can be added to any account.

A Payments Approach to DDA Revenues

7Confidential

Consumers pay more for products and services according to use, context and experience.

Large $1.6969% more

Grande $2.10

110% More

A Payments Approach to DDA Revenues

Confidential

Segmentation of “payment” revenues within or across all accounts as a add-on services can be focused on 1) NSF revenue, 2) interchange and debit payments and 3) small dollar loans.

8

$38 BillionPawn/Other $3 B

Sub Prime CC $4BPayDay Ln $8B

Late Fees On Bills $23 B

Non Credit ScoreSmall Dollar Loan

Revenues

Source: 2012 FDIC, Fair Issacs, CFSI, Our Analysis

A Payments Approach to DDA Revenues

With BankAccount

$32 Billion

3Interchange(net) $10 B

2

FI Service Charges$44 Billion

$31 Billion

Bank NSF/OD Fee Revenues

1

9Confidential

Your Revenue OpportunitiesYour near-term revenue opportunities in applying the payments segmentation paradigm can grow revenues 39%.

A. Tiered NSF Fees – 10%, 90 days

B. Prepaid Check Card/Fresh Start – 8%

C. Salutary Small Dollar Loan – 21%

10Confidential

# of NSFs Last 12 Mo. Accounts % of Total Items

0 76,650 73% - 1 8,400 8% 6,427

2-5 7,350 7% 20,160 6-10 6,300 6% 40,320 11-20 2,100 2% 41,889 21-30 1,248 1% 33,600 31-40 726 1% 30,240 41-50 1,050 1% 23,520 50+ 1,628 2% 141,120

Total 105,000 100% 336,000

10+ overdrafts fee users pay $1,100 a year in fees; 7% of accounts; want items paid; low per item price sensitivity.

Heavy NSFer

Poor Service

1-5 items a year pay $105 a year in fees,15% of accounts;

6-10 items 6% of accounts.

Rare NSFer

22% of accounts <650 credit score15% of accounts>650 and convenience loan oriented

Non NSF Liquidity Borrower

No Service

Sample FIGood

Service

Bank ServiceKey Segments

35 % No Liquidity Use

We focus first on segmenting the key existing revenue sources, overdraft and liquidity services.

Your Revenue Opportunities

11Confidential 11

Tiered NSF fees according to the context of total NSFs presented by the consumer annually maximizes customer service, revenue and regulatory management.

Your Tiered Pricing Estimate

Sample Competitive Market

Fifth Third $37Chase $35BBVA Compass $38Wells Fargo $35Fulton Bancshares $39

# of NSFs Last 12 Mo. Accounts % of Total Items % of Total $ 29.00

Tiered Revenue

Projected Revenue

Tiered Fee 0 12,070 71% - 0% -$

1-2 1,700 10% 2,975 5% 87,763$ 19.00$ 56,525$ 3-5 1,020 6% 4,165 7% 122,868$ 25.00$ 104,125$ 74% Lower 6-9 680 4% 5,355 9% 157,973$ 29.00$ 155,295$ cost

10-19 510 3% 7,735 13% 228,183$ 35.00$ 270,725$ 20-29 255 2% 7,140 12% 210,630$ 35.00$ 249,900$ 26% Competitive30-39 238 1% 5,950 10% 175,525$ 35.00$ 208,250$ Rate40+ 238 1% 26,180 44% 772,310$ 35.00$ 916,300$

Total 17,000 100% 59,500 100% 1,755,250$ 1,961,120$ Increase 205,870$

Revenue @

29.50

Your Revenue Opportunities – Tiered NSF Fees

12Confidential

Consumer Accounts Presenting NSFs

NSF Items Accounts % Items % Items/Acct Balance $ of Dep/Mo. # of

Dep/Mo. Opt In Fees@$25 vs Annual Dep

1-2 NSF 434 45% 569 6% 1.3 12,742$ 11,739$ 3.7 2% 0.0%3-5 NSFs 214 22% 828 9% 3.9 3,130$ 9,306$ 5.4 2% 0.1%

Subtotal 648 67% 1,397 16% 2.2 9,568$ 10,523$ 4.5 2% 0.0%6-9 NSFs 119 12% 860 10% 7.2 4,067$ 13,899$ 7.1 6% 0.1%10-19 NSFs 88 9% 1,193 13% 13.6 2,963$ 11,998$ 6.9 1% 0.2%20-29 NSFs 46 5% 1,090 12% 23.7 2,690$ 10,729$ 7.5 4% 0.5%30-39 NSFs 18 2% 620 7% 34.4 2,821$ 13,670$ 7.6 0% 0.5%40+ NSFs 44 5% 3,681 42% 83.7 11,998$ 33,751$ 8.7 0% 0.5%

Totals 963 100% 8,841 100% 9.2 7,941$ 12,205$ 5.5 2% 0.2%

We recommend monitoring accounts with 10 or more NSFs, but with monthly deposits averaging less than $20k or where annual NSF/OD fees are more than 3% of annual deposits a year for removal or limitation of use of from overdraft programs.

Consumer accounts reflect rising deposit amounts and frequency with increased NSF/OD usage, and overdraft fees consistently below 1% of annual deposits.

Sample Client – 5,000 Accounts

Your Revenue Opportunities – Tiered NSF Fees

13Confidential

Prepaid is now promoted as an alternative to checking accounts.– Big retailer promotion is

driving consumer interest.– 87% of prepaid card users

have a checking account.

You cancreate a checkingaccount toserve asa prepaidcompanionaccount.

Your Revenue Opportunities – Checking Companion Card

14Confidential

No Chex

PrePaid Check Card $5.95/mo.

Current Accounts As Priced

No Overdraft/Return Check Charges $14.95/mo.

87% of prepaid card users have a checking account. Providing a companion card and services by segment drives better service and revenues.

Chex Systems (Fresh Start)

5.95/mo.

12.95/mo.

$19.95 mo.$13.95/mo.

Your Revenue Opportunities – Segment Expansion

15Confidential

Small dollar loans can be delivered with automated underwriting and online automation with SEO marketing with no outward facing customer data. You serve and win customers who can repay with no credit score required.

Proprietary Checking Based Small Dollar Loan Program

Your Revenue Opportunities – Small Dollar Loans

16Confidential

Using deposits and net account balances is an alternative way for underwriting loans, similar to Guidance by the OCC (OCC-2013-0005), FDIC (6714-01-P) and CFPB, FIs can define customer ability to repay without credit scores.Underwriting Matrix

Age Under Six Months: No Loan Limit Age Six Months or More and: Last 6 Mo. Ending Balance

Dep Last 35 Days Dep Last 180 Days Avg Ending Balance Loan Limit =<$500 <$3,000 <$50 0$500<$750 $3000<$4,500 >$50<$75 200$ $750 - $1,500 $4,500<$9,000 $50 < $75 350$ $1,500 - $2,500 >$9,000<$15,000 >$75<$100 500$ $2,500 - $3,000 >$15,000<$18,000 >$100<$125 750$ >$3,000 >$18,000 >$125 1,000$

Your Revenue Opportunities – Small Dollar Loans

17Confidential

Underwriting Justifies Loans for 67% of FI Accounts <650 Credit Score

Nearly Half of Small Dollar Loan Users Have Credit Scores >650

– <650 credit score54%

– >650 credit score46%

Source: FI Client

Loan Available %

$1,000 15%

$750 9%

$500 19%

$350 23%

$0 33%

Total 100%

Source: Our Client Analysis

Your Revenue Opportunities – Small Dollar Loans

18Confidential

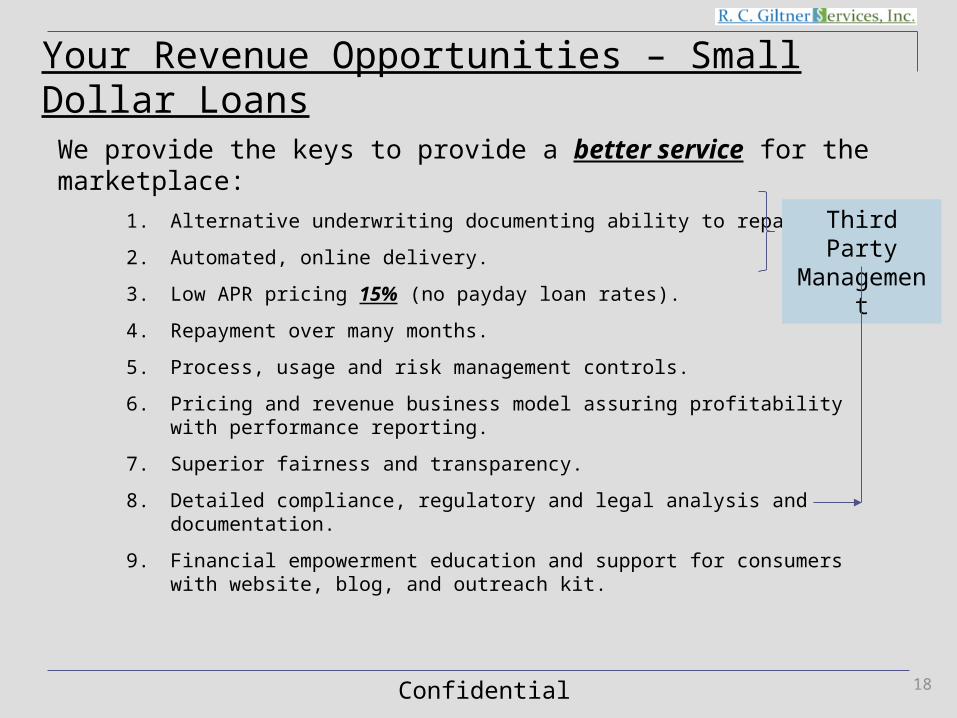

We provide the keys to provide a better service for the marketplace:

1. Alternative underwriting documenting ability to repay.

2. Automated, online delivery.

3. Low APR pricing 15% (no payday loan rates).

4. Repayment over many months.

5. Process, usage and risk management controls.

6. Pricing and revenue business model assuring profitability with performance reporting.

7. Superior fairness and transparency.

8. Detailed compliance, regulatory and legal analysis and documentation.

9. Financial empowerment education and support for consumers with website, blog, and outreach kit.

Third Party Management

Your Revenue Opportunities – Small Dollar Loans

19Confidential

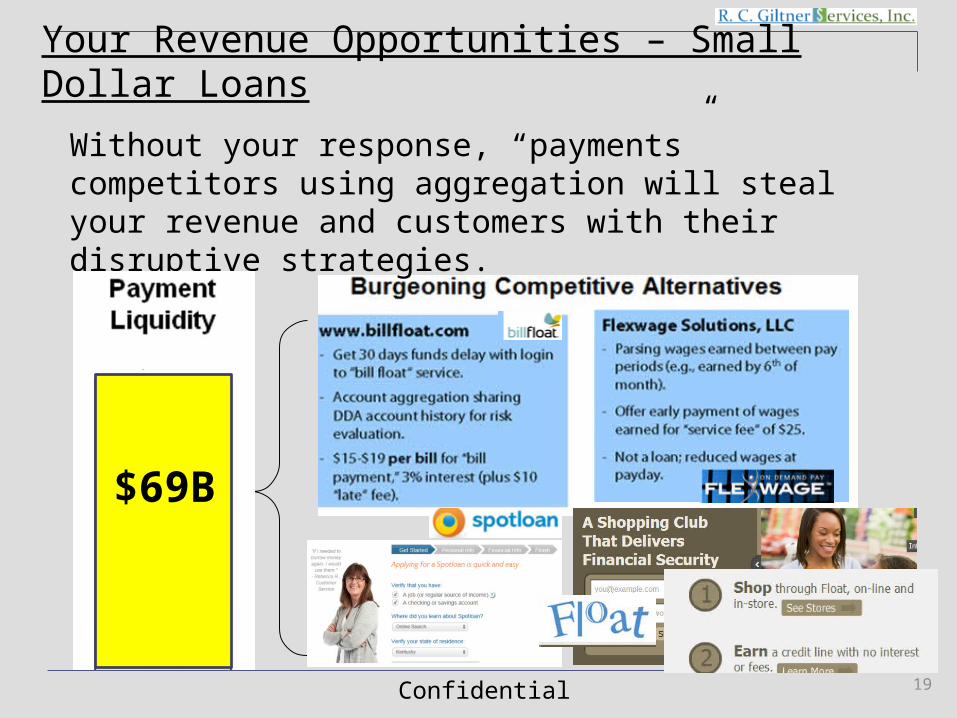

Without your response, “payments” competitors using aggregation will steal your revenue and customers with their disruptive strategies.

$69B

Your Revenue Opportunities – Small Dollar Loans

20Confidential

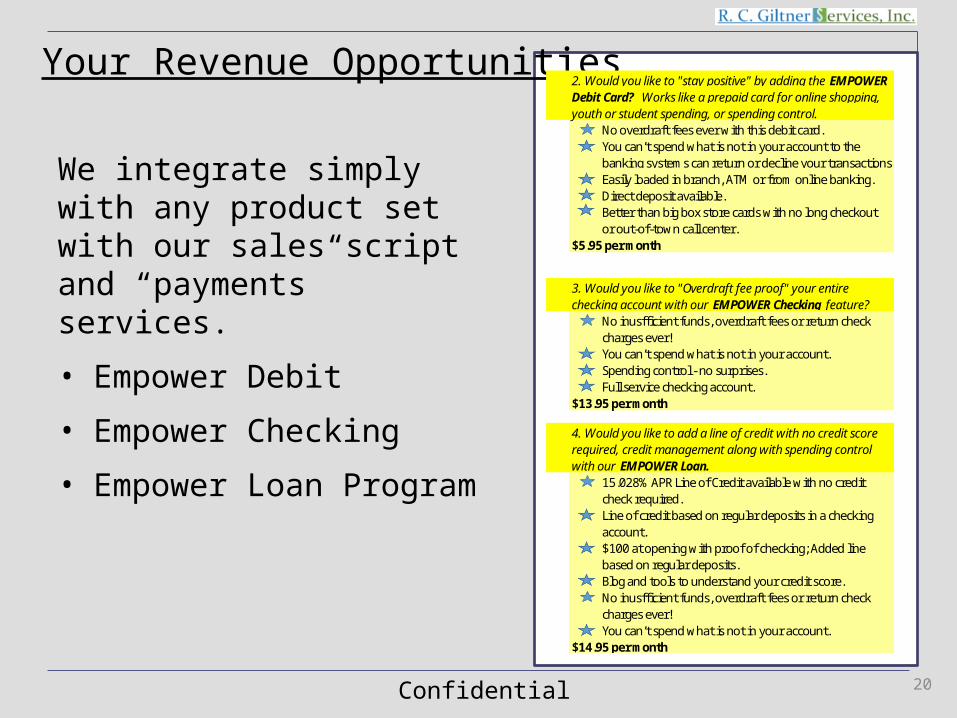

We integrate simply with any product set with our sales script and “payments” services.

• Empower Debit

• Empower Checking

• Empower Loan Program

Your Revenue Opportunities 2. Would you like to "stay positive" by adding the EMPOWERDebit Card? Works like a prepaid card for online shopping,youth or student spending, or spending control.

No overdraft fees ever with this debit card.You can’t spend what is not in your account to the banking systems can return or decline your transactions.Easily loaded in branch, ATM or from online banking.Direct deposit available.Better than big box store cards with no long checkoutor out-of-town call center.

$5.95 per month

3. Would you like to "Overdraft fee proof" your entirechecking account with our EMPOWER Checking feature?

No inusfficient funds, overdraft fees or return checkcharges ever!You can’t spend what is not in your account.Spending control - no surprises.Full service checking account.

$13.95 per month

4. Would you like to add a line of credit with no credit scorerequired, credit management along with spending controlwith our EMPOWER Loan.

15.028% APR Line of Credit available with no creditcheck required.Line of credit based on regular deposits in a checkingaccount. $100 at opening with proof of checking; Added line based on regular deposits.Blog and tools to understand your credit score.No inusfficient funds, overdraft fees or return checkcharges ever!You can’t spend what is not in your account.

$14.95 per month

21Confidential

Next Steps

Let us share the detailed pro forma of the revenue benefits we can bring to you.

A Payments Approach to Checking Revenue

Compliant Fees Consumers Willingly Pay