competitor information sharing in joint ventures and...

TRANSCRIPT

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Competitor Information Sharing

in Joint Ventures and Mergers:

Minimizing Antitrust Risks Avoiding Gun-Jumping and Other Restraints on Competition

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, JANUARY 10, 2017

Karen Kazmerzak, Partner, Sidley Austin, Washington, D.C.

Mary Lehner, Partner, Freshfields Bruckhaus Deringer, Washington, D.C.

Meghan Rissmiller, Partner, Hogan Lovells, Washington, D.C.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-961-8499 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Coordination & Information Exchange in the Premerger Context Avoiding Gun Jumping

Mary Lehner

January 2017

Section

US Antitrust Laws Governing Premerger Engagement

1

Antitrust in the Premerger Context

Antitrust laws govern the pre-closing conduct of parties to

mergers, acquisitions, and joint ventures

• Merging firms have legitimate interest in engaging in certain forms of

coordination

• Merging firms must be careful to maintain separate identities and behave

in a competitive manner until closing

Antitrust risks in due diligence and integration planning are

manageable in every transaction

• To mitigate the antitrust risks from premerger coordination, parties must

implement and adhere to antitrust guidelines

• Parties that are existing or potential competitors or that are in a vertical

relationship (e.g., customer-supplier) should exercise particular caution

in due diligence and integration planning

7

Gun Jumping

What is Gun Jumping • Gun jumping occurs when parties to a transaction fail to remain

independent actors prior to closing

The premature consolidation of the parties’ businesses (premature

control); or

The exchange of information between competitors (information

exchange)

Two Contexts in Which Risks of Gun Jumping Arise

Due Diligence • Occurs prior to and until signing

• Purpose to value and assess the target and deal

Integration Planning • Until closing

• Purpose to plan for consolidated operations and facilitate realization of

synergies

8

Primary US Antitrust Laws

The Hart-Scott-Rodino Act (HSR Act) • Civil penalties (maximum $40,000/day); and

• Equitable relief

Section 1 of the Sherman Act “Every contract, combination in the form of trust or otherwise, or conspiracy, in restraint

of trade or commerce among the several States, or with foreign nations, is declared to

be illegal”

• Penalties (civil and criminal)

• Potential follow-on litigation with treble damages

Section 5 of the Federal Trade Commission Act (FTC Act) “Unfair methods of competition in or affecting commerce . . . are hereby declared

unlawful”

• Penalties include cease and desist orders and equitable relief

Restrictions on Conduct Continue Until Closing • Restrictions on information exchange and coordinated action under Section 1 and

Section 5 continue until closing, even if the HSR waiting period has expired or was

terminated

• The fact that the HSR waiting period has expired or was terminated may be relevant

to the question of competitive effects under the rule of reason

9

Section

Premature Control

2

Premature Control

The Delicate Balance of Control

• Prior to the expiration or termination of the HSR waiting period, the parties must

continue to compete with one another

Acquiring party generally should not exert control over the acquired party

• However, the acquiring party also needs to be comfortable that the value of the

acquired company is not materially diminished while the merger is being reviewed

• Tension often manifests in drafting and executing the terms of the merger

agreement

• Drafting a merger agreement that walks the line of avoiding control while still

protecting the interests of the acquiring company can be challenging

Agency Analysis

• The agencies will assess whether conduct has the effect of transferring beneficial

ownership of the target prior to the expiration or termination of the HSR waiting

period

• To do so, the agencies will consider whether sufficient indicia of beneficial

ownership have been transferred to the buyer such that the parties have effectively

consummated the transaction prior to the end of the HSR waiting period

11

Assessing Premature Control: Beneficial Ownership

The right to obtain the benefit of any increase in value or dividend

The risk of loss of value

The right to vote the stock or to determine who may vote the stock

The investment discretion (including the power to dispose of the stock

12

Indicia of beneficial ownership include:

Access to confidential information and control over key decision

Ability to reverse any key decision if the merger does not close

Whether the target’s key decisions were unilateral, mandated by the buyer, or something in between

Whether the buyer has tried to preempt attractive opportunities (e.g., hire key employees, appropriate proprietary know-how, negotiate with important customers)

Factors to assess whether sufficient

indicia have been transferred include:

Smithfield Foods / Premium Standard Farms (2010)

Deal Overview

• In September 2006, Smithfield Foods announced the intention to acquire

Premium Standard

• The DOJ opened an investigation and issued a second request but

ultimately closed the investigation in May 2007 without challenging the

merger

DOJ Complaint

• In January 2010, Smithfield Food and Premium Standard Farms agreed

to a civil penalty of $900,000 for gun jumping before expiration of the

HSR Act waiting period

• The DOJ alleged that, in exercising operational control over Premium

Standard and acquiring and holding assets from the target’s hog

procurement contract, Smithfield prematurely acquired beneficial

ownership of a significant segment of Premium Standard’s business

operations

13

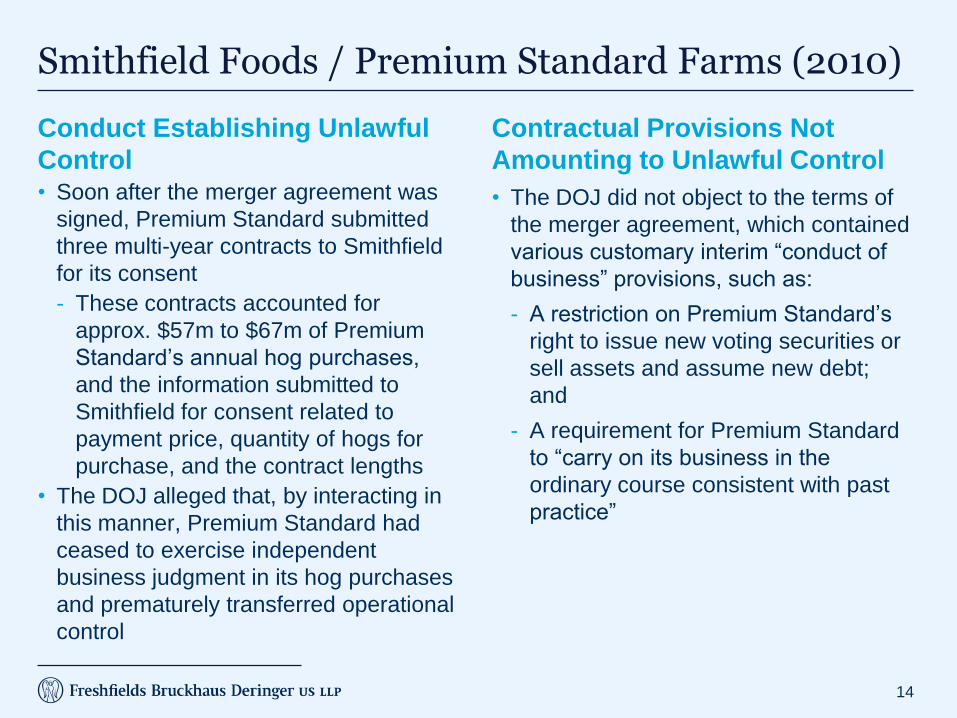

Smithfield Foods / Premium Standard Farms (2010)

Conduct Establishing Unlawful

Control • Soon after the merger agreement was

signed, Premium Standard submitted

three multi-year contracts to Smithfield

for its consent

These contracts accounted for

approx. $57m to $67m of Premium

Standard’s annual hog purchases,

and the information submitted to

Smithfield for consent related to

payment price, quantity of hogs for

purchase, and the contract lengths

• The DOJ alleged that, by interacting in

this manner, Premium Standard had

ceased to exercise independent

business judgment in its hog purchases

and prematurely transferred operational

control

Contractual Provisions Not

Amounting to Unlawful Control

• The DOJ did not object to the terms of

the merger agreement, which contained

various customary interim “conduct of

business” provisions, such as:

A restriction on Premium Standard’s

right to issue new voting securities or

sell assets and assume new debt;

and

A requirement for Premium Standard

to “carry on its business in the

ordinary course consistent with past

practice”

14

Flakeboard / SierraPine (2014)

Deal Overview • In January 2014, Flakeboard and SierraPine entered into an agreement

for Flakeboard to acquire SierraPine’s particleboard mills in Springfield,

OR and Martell, CA, and a medium-density fiberboard mill in Medford,

OR

• The parties filed HSR notifications in January 2014 and the DOJ issued

second requests; the waiting period expired in August 2014 after the

parties’ certified substantial compliance

DOJ Complaint • In November 2014, both parties agreed to pay $1.9 million in civil

penalties under the HSR Act and Flakeboard agreed to pay $1.15 million

in disgorgement, in order to resolve the alleged violations of Section 1 of

the Sherman Act and the HSR Act

• The Final Judgment further prohibited the parties from engaging in

certain agreements during the negotiation and interim periods of future

transactions

15

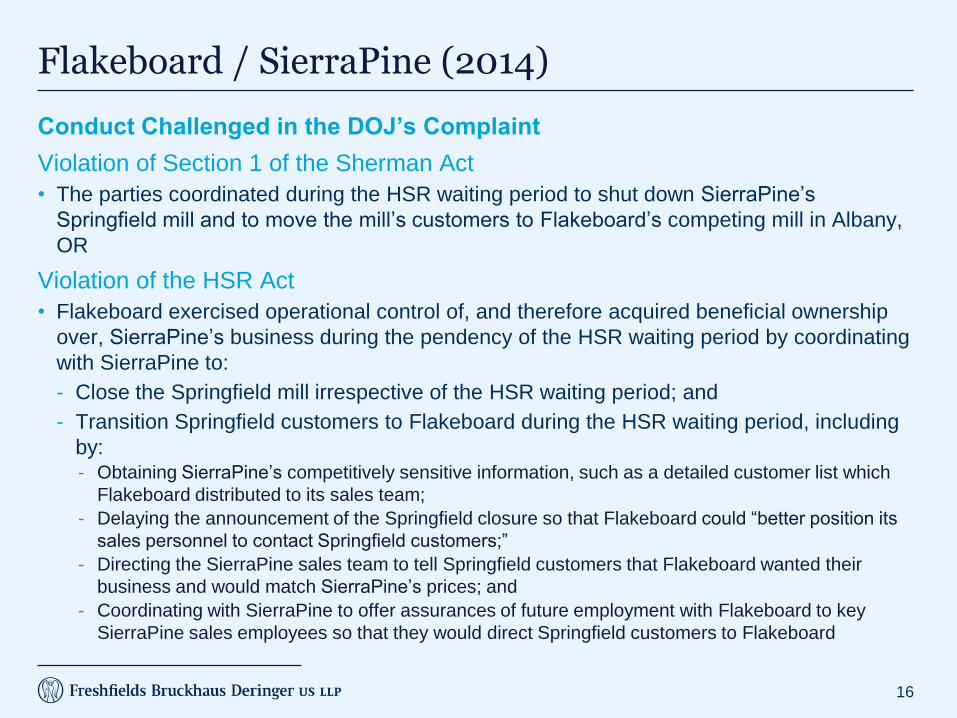

Flakeboard / SierraPine (2014)

Conduct Challenged in the DOJ’s Complaint

Violation of Section 1 of the Sherman Act

• The parties coordinated during the HSR waiting period to shut down SierraPine’s

Springfield mill and to move the mill’s customers to Flakeboard’s competing mill in Albany,

OR

Violation of the HSR Act

• Flakeboard exercised operational control of, and therefore acquired beneficial ownership

over, SierraPine’s business during the pendency of the HSR waiting period by coordinating

with SierraPine to:

Close the Springfield mill irrespective of the HSR waiting period; and

Transition Springfield customers to Flakeboard during the HSR waiting period, including

by: Obtaining SierraPine’s competitively sensitive information, such as a detailed customer list which

Flakeboard distributed to its sales team;

Delaying the announcement of the Springfield closure so that Flakeboard could “better position its

sales personnel to contact Springfield customers;”

Directing the SierraPine sales team to tell Springfield customers that Flakeboard wanted their

business and would match SierraPine’s prices; and

Coordinating with SierraPine to offer assurances of future employment with Flakeboard to key

SierraPine sales employees so that they would direct Springfield customers to Flakeboard

16

Best Practices for Avoiding Premature Control

Premature Control in Merger Agreements

• Enforcement agencies recognize that an acquiring party has legitimate commercial and

practical interests, and will expect and allow reasonable post-signing covenants designed

to protect the target’s value

• Cause for concern arises where a purchase agreement:

Limits a target’s pre-closing conduct;

Inhibits the target’s ability to retain its competitive and operational independence; and/or

Effectively transfers operational control of the seller to the buyer

Best Practices

• Parties must carefully consider covenants in merger agreements that impose restrictions

on premerger conduct and/or require buyer approval to ensure that ordinary course

competition is not restricted

Negative covenants (e.g., providing the acquiring party a right to review high-threshold,

material assumption of liability) have legitimate purposes. But care should be exercised

in determining their scope and potential carve-outs

• No business integrations may begin until after clearance is obtained; parties cannot allow

for even the appearance or suggestion that parties have started to act as a single entity

• Clear guidelines should be issued early in the transaction process

17

Best Practices: Permissible Conduct

Conduct generally considered permissible by antitrust authorities:

• Agreements to operate in the “ordinary course of business” consistent with

past practices

• Certain restrictions on conduct that would cause a “material adverse change”

in the target’s business

• Joint conduct considered lawful independent of the proposed merger

• Joint marketing/advertisements that generally promote the transaction (with

appropriate guidelines and controls)

• Joint customer calls to discuss general benefits of the merger

• Disclosure of confidential business information related to competing products

in the context of litigation or settlement discussions (subject to a protective

order)

18

Best Practices: Prohibited Conduct

Conduct generally to be avoided:

• Agreements to exit certain businesses pending completion

• Agreements to “slow roll” (or delay negotiations) with certain customers

• Obtaining the other party’s pre-clearance for routine business decisions

• Coordinating business strategies, production, sales, distribution, or discount

policies

• Covenants in the merger agreement that entitle the buyer to review or approve

the seller’s ordinary course of business activities in areas in which the

companies compete

• Relocating staff to other party’s premises

• Joint bidding for contracts when the normal industry practice does not allow for

this activity

• Attending joint meetings with customers or other party’s internal meetings

• Discussion of post-merger conduct of either party in relation to sales/marketing

prospects or mutual customers

19

Section

Information Exchange

3

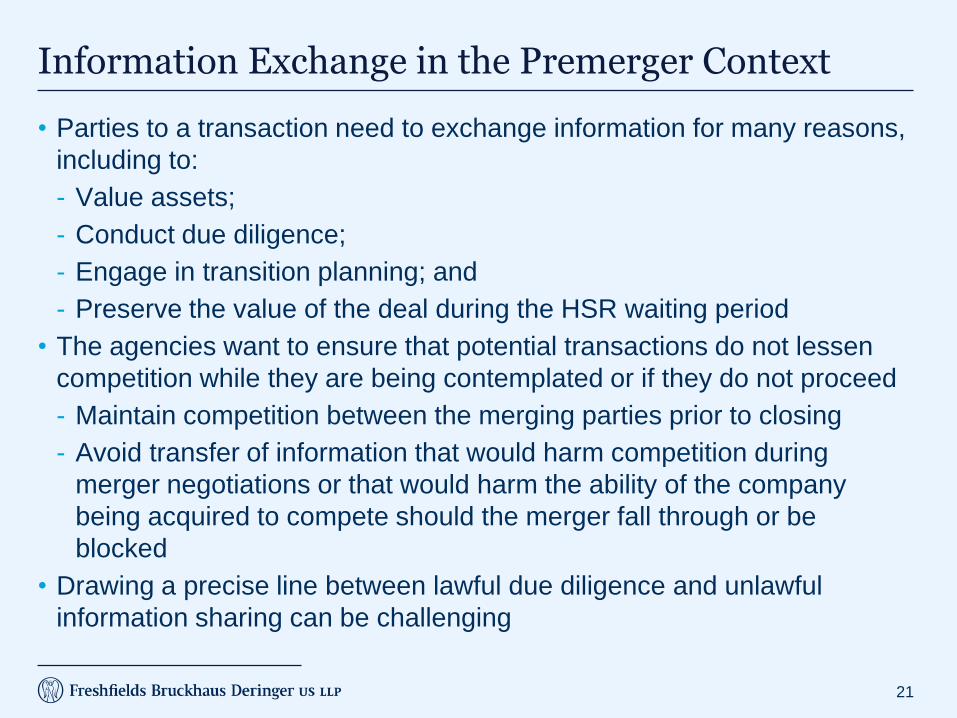

Information Exchange in the Premerger Context

• Parties to a transaction need to exchange information for many reasons,

including to:

Value assets;

Conduct due diligence;

Engage in transition planning; and

Preserve the value of the deal during the HSR waiting period

• The agencies want to ensure that potential transactions do not lessen

competition while they are being contemplated or if they do not proceed

Maintain competition between the merging parties prior to closing

Avoid transfer of information that would harm competition during

merger negotiations or that would harm the ability of the company

being acquired to compete should the merger fall through or be

blocked

• Drawing a precise line between lawful due diligence and unlawful

information sharing can be challenging

21

Risks of Information Exchange in The Premerger Context

Information Exchange in Due Diligence • Concern that the exchange of competitively sensitive information

between existing or potential competitors, or between parties in a vertical

relationship (e.g., customer-supplier), may lead to or facilitate collusion

• Risk of reducing competition before the transaction is consummated or if

the transaction is abandoned or blocked, e.g.,

• Basis to coordinate price, output, or some other competitively significant

terms during the premerger period; or

• If the transaction falls through, information could be used to coordinate

future conduct

• Risk of spillover effects

Information Exchange in Integration Planning • Similar risks as in due diligence

• Level and detail of information sharing will expand as parties progress

toward closing but risk associated with information exchange will

decrease as the parties satisfy conditions to closing

22

Information Exchange: Relative Risk Levels

Low Antitrust Risk

• Historical financial and

accounting information,

including balance sheets;

• Departmental or

functional budgets (not on

a product-line basis);

• Business descriptions;

• Lists of current products;

and

• Publicly available

information

Moderate Antitrust Risk

• Current strategic,

marketing, or business

plans or planning

documents;

• Future strategic initiatives,

including specific

customer targets and

entry or expansion plans

for plants or products;

• Prospective financial

information, including

budgets and projections,

as long as such materials

do not disclose the

parties’ explicit predictions

regarding future pricing or

significant costs; and

• General predictions of

market trends

Significant Antitrust Risk

• Customer-specific or

transaction-specific

confidential information,

including details or copies

of current customer

contracts

• Current or prospective

pricing on a specific

product or customer

basis; and

• Detailed production cost

information and/or

production schedules

23

Omnicare / UnitedHealth Group (7th Cir. January 2011)

Deal Overview • Omnicare is an institutional pharmacy that provides services to long-term care

(LTC) facilities; it negotiates contracts with health insurers who provide coverage

to senior citizens in those LTC facilities

• Senior citizens pay their premiums to health insurers; health insurers then

reimburse Omnicare at a pre-negotiated rate

• In 2005, two health insurers – UnitedHealth and PacifiCare – entered into

merger talks, conducted due diligence, signed a merger agreement, and

ultimately merged

• During due diligence, UnitedHealth and PacifiCare each negotiated separate

contracts with Omnicare

• Following the merger, UnitedHealth (the acquiring company) abandoned its

contract with Omnicare and joined PacifiCare’s more favorable contract

Omnicare Complaint • Omnicare sued, alleging a conspiracy (and fraudulent scheme) between

UnitedHealth and PacifiCare to coordinate their strategies for negotiating with

Omnicare prior to consummating their merger and to depress their

reimbursement rate

24

Omnicare / UnitedHealth Group (7th Cir. January 2011)

Court Decisions

• The US District Court for the Northern District of Illinois granted summary

judgment to UnitedHealth

• The US Court of Appeals for the 7th Circuit affirmed the judgment of the District

Court by finding that:

Early exchanges were restricted to aggregated pricing data, “sample regions,”

“high level review,” and “estimates”

Price information was shared among a limited number of high-level executives

(less likely to be involved in the negotiation with Omnicare)

Information shared outside the bounds of the Confidentiality Agreement,

without further evidence of concerted action, was not enough to support an

inference of conspiracy

Disclosed pricing information was “necessary to due diligence and was

performed in a reasonably sensitive manner”

Communications after signing and before closing focused on “long-term

strategic planning” and were always “with an eye towards integration of

services after the merger is completed”

Information exchange process was monitored by outside antitrust counsel

25

Best Practices on Information Sharing

Companies should consult with antitrust counsel to manage risks when obtaining information necessary for diligence and integration purposes

Careful planning and process documentation can reduce the risk of a successful allegation of improper information sharing

Companies should avoid exchanging any information beyond what is necessary for valuing the transaction and setting the stage for post-merger integration. Detailed, current competitive information presents the highest risk

Creating a limited due diligence team with personnel who are not responsible for pricing and marketing decisions is strongly advised

For necessary but extremely sensitive information, aggregation or using third-party vendors to review and summarize the information should be considered

26

Biography

27

Mary Lehner

Freshfields Bruckhaus Deringer

700 13th Street NW, 10th Floor, Washington DC 20005

T +1 202 777 4566

Mary focuses her practice on representing clients before the US Federal Trade

Commission, the Department of Justice Antitrust Division, and the State Attorneys

General on the antitrust aspects of M&A, joint ventures, distribution and intellectual

property arrangements, and other competitive conduct.

As part of a team with an expansive global network and client base, Mary has

extensive first-hand knowledge of the issues surrounding large-scale M&A and how

clients should consider large, multinational deals with multijurisdictional regulatory

considerations.

Before joining Freshfields, Mary served as an advisor to two FTC Chairs, providing

counsel on antitrust investigations, enforcement actions, domestic and international

policy initiatives, public relations, and congressional strategies. Prior to her post in

the Chairman’s office, Mary oversaw antitrust merger investigations as a lead

attorney in the FTC’s Bureau of Competition.

Mary actively participates in American Bar Association leadership, is a frequent

speaker at ABA programs, and is currently Vice Chair of the Antitrust Section’s

Corporate Counseling Committee. She received her JD from the University of

Chicago Law School and her BA from the College of William & Mary.

This material is provided by the international law firm Freshfields Bruckhaus Deringer LLP (a limited liability partnership organised under the law

of England and Wales) (the UK LLP) and the offices and associated entities of the UK LLP practising under the Freshfields Bruckhaus Deringer

name in a number of jurisdictions, and Freshfields Bruckhaus Deringer US LLP, together referred to in the material as ‘Freshfields’.

For regulatory information please refer to www.freshfields.com/support/legalnotice.

The UK LLP has offices or associated entities in Austria, Bahrain, Belgium, China, England, France, Germany, Hong Kong, Italy, Japan,

the Netherlands, Russia, Singapore, Spain, the United Arab Emirates and Vietnam. Freshfields Bruckhaus Deringer US LLP has offices

in New York City and Washington DC.

This material is for general information only and is not intended to provide legal advice.

© Freshfields Bruckhaus Deringer LLP 2014

Thank you

Information Sharing

Between Competitors:

Strafford CLE Webinar

Karen Kazmerzak

January 10, 2017

This Presentation

• Focus on legitimate collaborations among competitors

– Standards generally more permissive when arrangements do not involve competitors

• Excludes issues arising from cartels and naked restraints

– Important, but not today’s presentation

– Distinction from today’s issues sometimes blurs

SIDLEY AUSTIN LLP 30

Two Broad Families of Issues

• Pre-merger Conduct vs. Ongoing Conduct

– Pre-merger conduct: “Gun-jumping” before merger closing or JV formation

• Just addressed in Mary Lehner’s presentation

• “Information sharing / diligence” strand

• Distinct from “premature control” strand

– Ongoing conduct: Ancillary restraints and collateral effects in the context of ongoing

cooperation

• Examples on next slide

SIDLEY AUSTIN LLP 31

Ongoing Cooperation: Examples

• Joint ventures

– Where co-venturers compete with each other outside the venture

– Where a co-venturer competes with the venture

• Joint activity often not performed through entities

– Joint development arrangements

– Joint marketing and promotion

– Joint purchasing

• Standard-setting organizations

• Trade association data collection and dissemination

• Benchmarking

• Distribution by vertically integrated firms

– Where a manufacturer sells through independent distributors and through own

distribution arm

– Where a component manufacturer sells to independent downstream firms and transfers

in internal manufacturing operations

SIDLEY AUSTIN LLP 32

Main Legal Principles in US

• Information exchange as discussed here is subject to rule of reason treatment

• Certain content is riskier than other content

– Price information is riskier than cost and other non-price information

– Detailed information is riskier than aggregated information

• Multiplicity of sources

• Granularity of content

– Future information is riskier than stale information

SIDLEY AUSTIN LLP 33

Potemkin Village Exemptions

• Examples

– National Cooperative Research Act of 1984

– National Cooperative Research and Production Act of 1993

– Standards Development Organization Advancement Act of 2004

• Recurring patterns

– Justified by need to correct business misperception about application of antitrust

prohibitions to beneficial conduct

– Exempts conduct that was already lawful under rule of reason

– Carves out antitrust-exposed conduct from scope of exemption

SIDLEY AUSTIN LLP 34

Differences Emerging in Europe

• Increasingly more restrictive in application than standards in US

• Broadening interpretation of prohibitions on “restriction of competition by object”

– Capture disclosure of “intended future prices or quantities,” regardless of justifications or

effect

– Flexibility shown for historical information

– Some flexibility shown for certain classes of agreements such as R&D, joint production,

joint purchasing

• Frequent use of bright-line thresholds for safe harbors

– Reflection of systems based in civil code

– Thin patina of certainty and rigor

SIDLEY AUSTIN LLP 35

And Uncertainties Remain in US

• How to treat public disclosures?

– Valassis and analyst calls

– Airline Tariff Publishing and posted prices

• When are buffers required?

– Internal firewalls

– Third-party intermediaries

• How to treat intermediaries and agents?

• How is competitive effect to be assessed?

– Who has the burden of proving effect?

– How are benefits and adverse effects to be measured?

• What is required as to efficiencies?

– When must they be shown?

– By whom?

SIDLEY AUSTIN LLP 36

US Competitor Collaboration Guidelines

• FTC/DOJ Antitrust Guidelines for Competitor Collaborations, issued in 2000

– https://www.ftc.gov/sites/default/files/documents/public_events/joint-venture-hearings-

antitrust-guidelines-collaboration-among-competitors/ftcdojguidelines-2.pdf

• Tightrope walk between political calls for permissiveness and need to protect

against statements that undercut anti-cartel mission

• Result: grudging characterization of scope of legality

– See ABA comments on draft Competitor Collaboration Guidelines

• http://www.americanbar.org/groups/antitrust_law/resources/comments_reports_amicus_briefs/2000

_comments.htm

– Increasingly cited by courts

– Beginning to achieve mainstream acceptance, despite inaccuracy of analytical content

• Although some advocate for revisions

– See Summer 2016 issue of the ABA Antitrust Magazine (vol. 30, no. 3) dedicated to joint

ventures and the Competitor Collaboration Guidelines

SIDLEY AUSTIN LLP 37

US Health Care Statements

• FTC/DOJ Statements of Antitrust Enforcement Policy in Health Care, issued in

1996

– https://www.ftc.gov/sites/default/files/attachments/competition-policy-

guidance/statements_of_antitrust_enforcement_policy_in_health_care_august_1996.pdf

• Issued under intense political pressure, as Congress contemplated legislative

proposals that would have limited application of antitrust laws to the health care

sector

• Statements intended to provide “clarification” as to how the sector could operate

under mainstream antitrust principles

• Result: generally balanced and thoughtful guidance that has taken on a role as a

leading authority for the issues they address

– Most significant statements

• Statement 6: Provider Participation in Exchanges of Price and Cost Information

– Leading government statement to which trade associations and industry groups turn when

designing multi-member price and wage surveys

• Statement 7: Joint Purchasing Arrangements Among Health Care Providers

– Used across a number of industries to inform analysis of joint purchasing activities

SIDLEY AUSTIN LLP 38

Noteworthy US Supreme Court Decisions

• Leading historical Supreme Court cases on price information

– Maple Flooring (1925)

– Cement Manufacturers Protective Ass’n (1925)

– Container Corporation (1969)

– United States Gypsum (1978)

• Some other key Supreme Court cases on competitor arrangements

– National Society of Professional Engineers (1978)

– Broadcast Music (1979)

– Maricopa County Medical Society (1982)

– NCAA v. University of Oklahoma (1984)

– American Needle (2010)

SIDLEY AUSTIN LLP 39

Other Noteworthy US Authority

• Three lower court cases worth mention

– Addyston Pipe (6th Cir. 1898), aff’d (1899)

– United States v. Morgan (S.D.N.Y. 1953)

– United States v. Brown University (3d Cir. 1993)

• Major government policy statements

– Various business review letters

• DOJ: https://www.justice.gov/atr/business-review-letters-and-request-letters

• FTC: https://www.ftc.gov/tips-advice/competition-guidance/competition-advisory-opinions

SIDLEY AUSTIN LLP 40

Biography

SIDLEY AUSTIN LLP 41

Karen Kazmerzak, a former Federal Trade Commission

attorney, has a broad practice counseling clients regarding

antitrust matters involved in mergers and acquisitions and

concerning antitrust issues in licensing, distribution,

pricing, and competitor collaborations.

Karen represents clients seeking merger clearance from

the FTC and the U.S. Department of Justice, and clients

that are third-party market participants subpoenaed by the

government or that oppose an acquisition. Karen also

works closely with co-counsel and economists around the

world to develop the best global strategy for clients’

advocacy across several jurisdictions, including in the

United States.

KAREN KAZMERZAK Partner SIDLEY AUSTIN LLP 1501 K Street, N.W. Washington, DC 20005 +1 202 736 8068 [email protected] www.sidley.com

Beijing Chicago Houston New York Singapore

Boston Dallas London Palo Alto Sydney

Brussels Geneva Los Angeles San Francisco Tokyo

Century City Hong Kong Munich Shanghai Washington, D.C.

1,900 LAWYERS and 20 OFFICES

located in commercial, financial

and regulatory centers

around the world

Meghan E.F. Rissmiller Washington, DC

January 2017

Recent Developments

Information Sharing by Competitors

Hogan Lovells

• As recent events have demonstrated, the FTC and DOJ remain focused on curbing unlawful information exchanges among competitors.

• Since the last time our colleagues did this program, we have seen…

• Litigation

– In re AmeriGas & Blue Rhino (2015)

– United States v. DirecTV Group Holdings, LLC and AT&T, Inc. (2016)

• Guidance

– DOJ/FTC Guidance to HR Professionals (2016)

• Legislation

– Cybersecurity Information Sharing Act (2015)

Current events in information sharing

| 44

In re AmeriGas & Blue Rhino

United States v. DirecTV Group Holdings, LLC and AT&T, Inc.

Recent litigation

| 45

Hogan Lovells

• AmeriGas and Blue Rhino controlled approximately 80% of the market for wholesale propane exchange tanks.

• According to the FTC, AmeriGas and Blue Rhino illegally agreed to reduce the amount of propane in their tanks. This reduction from 17 lbs to 15 lbs per tank would result in a price increase.

• Walmart, which was a customer of both companies, resisted the reductions.

– Lowe’s accepted the fill reduction but only on the condition that all of Blue Rhino’s other customers (including Walmart) also accepted the reduction.

• AmeriGas and Blue Rhino secretly agreed that neither would deviate from the plan to reduce fill in negotiations with Walmart to ensure it accepted the reductions. This collusion was the basis of an FTC complaint.

In re AmeriGas & Blue Rhino (2015)

| 46

Hogan Lovells

• Information shared between executives at the two companies:

– After Walmart rejected Blue Rhino’s proposal to reduce fill levels, Blue Rhino decided to inform AmeriGas of its plans (believing the plan would only be effective if its competitors also agreed to reduce fill levels).

– Blue Rhino and AmeriGas communicated regarding the planned decrease and discussed the status of negotiations with Walmart.

– Coordinated emails using similar language to urge Walmart to accept the fill reductions.

• “No antitrust practitioner would counsel his or her client to engage in the direct competitor communications and concerted actions that are alleged to have occurred between Blue Rhino and AmeriGas.”

– Commissioner Wright, concurring

What information was shared?

| 47

Hogan Lovells

• FTC order bars companies from:

– Entering into any combination/conspiracy/agreement in restraint of trade.

– Communicating competitively sensitive nonpublic information to any competitor, or requesting, encouraging, or facilitating the communication of competitively sensitive nonpublic information from any competitor.

• Information sharing with competitors allowed if:

– Negotiating an agreement and information “is communicated only as reasonably necessary to negotiate and fulfill the terms” of a Propane Refilling Agreement (to refill tanks on behalf of a competitor);

– Reasonably necessary to engage in legally supervised due diligence for a potential sale, acquisition or joint venture; or

– Part of industry-wide information exchange provided data is at least 3 months old and comes from other firms, none of whose data accounts for more than 25% of the total data collected.

The FTC order

| 48

Hogan Lovells

• On November 2, 2016, the DOJ sued DirecTV Group Holdings (and AT&T, which acquired DirecTV in 2015) for its role in relation to a series of allegedly unlawful information exchanges.

• The DOJ alleges that DirecTV coordinated with AT&T, Cox Communications, and Charter Communications about the decision to carry the Dodgers Channel, which has exclusive rights to telecast locally almost all Dodgers games.

• The complaint claims DirecTV facilitated communications that reduced “each rival’s fear that competitors would carry the Dodgers Channel, thereby providing DirecTV and its competitors artificially enhanced bargaining leverage.”

United States v. DirecTV Group Holdings (2016)

| 49

Hogan Lovells

• Executives at each company are alleged to have engaged in regular communications regarding the status of their Dodgers Channel negotiations. The DOJ alleged the communications included:

– Texts and voice messages that improperly discussed non-public information about their content negotiations and future plans.

– Mutual assurances no company would launch the Dodgers Channel in the near term.

• According to the DOJ, such communications “corrupted the competitive process that should have resulted in each company making an independent decision on whether to carry the Dodgers Channel, subject to competitive pressures arising from independent decisions made by other, overlapping MVPDs.”

– Each company was “safer” because they had reason to believe they would not lose subscribers if they did not carry the Dodgers Channels with the knowledge that no one else intended to do so.

What information was shared?

| 50

Hogan Lovells

• The DOJ defined the relevant product market very narrowly—video distribution services in the Los Angeles area, of which local sports content is an important component.

– To observers, the relevant product market seems more like Dodgers games, which is what consumers are allegedly being denied. Consumers could still access other local sports content, such as Los Angeles Lakers games.

• Likewise, the relevant geographic market is defined very narrowly—the Cox and Charter Los Angeles service areas, only a slice of pay TV viewership in the greater Los Angeles metropolitan area.

• Additionally, the DOJ ignores the potential procompetitive effects that could have resulted from the information sharing.

– The MVPDs have argued that each acted independently and in the interests of their customers to reject the Dodgers Channel proposal because it was too high, saving customers money on their cable bill.

An unusual case

| 51

Hogan Lovells

• Although still pending, this litigation yields some early lessons.

• Information sharing among competitors is risky, particularly when the information is non-public and competitively sensitive (e.g., “current and forward-looking plans for product features on which they compete.”).

– As the DOJ explained, “[l]ike price, content carriage—and particularly local sports content carriage—is a crucial aspect of competition between video programming distributors to attract and retain subscribers. Just as a subscriber might switch away from a distributor in order to obtain a lower price, a subscriber might switch away from a distributor in order to watch programming that the subscriber’s current distributor does not offer.”

• The DOJ has demonstrated its willingness to bring a case to remedy what appears to be a very small harm—the inability of some Dodgers fans in the Los Angeles area to watch games.

Potential takeaways

| 52

DOJ/FTC Guidance to HR Professionals (2016)

Guidance

| 53

Hogan Lovells

• Issued October 2016

• “HR professionals should take steps to ensure that interactions with other employers competing with them for employees do not result in an unlawful agreement not to compete on terms of employment.”

• Although two companies may not compete in the same industry, they can still compete for a certain type of employee (an IT professional, e.g.), and thus be “competing employers” under this guidance.

DOJ/FTC Guidance to HR Professionals (2016)

| 54

Hogan Lovells

• The federal antitrust agencies have taken enforcement actions against employers that have agreed not to compete for employees.

• These types of agreements are illegal per se.

– Wage-fixing agreements (e.g., uniform bill-rate schedule set for nurses working for competitor hospitals)

– No-poaching agreements (e.g., agreement among competitors not to cold call each other’s employees)

• Potential consequences:

– Civil law suit (treble damages)

– Criminal prosecution

Per se unlawful agreements

| 55

Hogan Lovells

• “While agreements to share information are not per se illegal and therefore not prosecuted criminally, they may be subject to civil antitrust liability when they have, or are likely to have, an anticompetitive effect.”

• Even “periodic exchange of current wage information in an industry with few employees” could be circumstantial evidence of an implicit agreement not to compete on wages.

Agreements suggesting anticompetitive conduct

| 56

Hogan Lovells

• An information exchange may be lawful if:

– A neutral third party manages the exchange;

– The exchange involves information that is relatively old;

– The information is aggregated to protect the identity of the underlying sources; and

– Enough sources are aggregated to prevent competitors from linking particular data to an individual source.

• Merger-specific guidance:

– “In the course of determining whether to pursue a merger or acquisition, a buyer may need to obtain limited competitively sensitive information. Such information gathering may be lawful if it is in connection with a legitimate merger or acquisition proposal and appropriate precautions are taken.”

Strategies for lawful information exchanges

| 57

Cybersecurity Sharing Information Act of 2015

Legislation

| 58

Hogan Lovells

• A company may share with, or receive from, the federal government, state or local government, or other companies and private entities “cyber threat indicators” and “defensive measures” for a “cybersecurity purpose.”

– From the DOJ/DHS document, “Guidance to Assist Non-Federal Entities to Share Cyber Threat Indicators and Defensive Measures with Federal Entities under the Cybersecurity Information Sharing Act of 2015,” issued in June 2016.

• Statute follows from April 2014 FTC/DOJ joint policy statement on the sharing of cybersecurity information, which stated that properly designed cyber threat information sharing is not likely to raise antitrust concerns and can help secure the nation’s networks of information and resources.

Cybersecurity Sharing Information Act of 2015

| 59

Hogan Lovells

• When evaluating the antitrust risks of sharing cyber intelligence, the Agencies looked at three main factors:

– Cyber threat information sharing can improve efficiency and help secure our nation’s networks of information and resources.

– Cyber threat information typically is very technical in nature which is very different from the sharing of competitively sensitive information such as current or future prices and output or business plans.”

– Cyber threat information exchanges are unlikely to harm competition and is “unlikely in the abstract to increase the ability or incentive of participants to raise price or reduce output, quality, service, or innovation.”

Information exchanges under 2014 policy statement

| 60

Hogan Lovells

• DOJ Business review letter of October 2, 2014

– A proposed data-sharing platform intended to help prevent cyber attacks, will not face a Justice Department challenge.

– Assistant Attorney General William J. Baer observed:

– Antitrust law is “not an impediment to legitimate private-sector initiatives to share specific information about cyber incidents and mitigation techniques in order to defend against cyber attacks.”

– The system, “as proposed, would be unlikely to facilitate price or other competitive coordination,” he maintained.

– The proposed system is designed to address “shortfalls” in more traditional information sharing systems while still “operating within the framework set forth in the Department of Justice and Federal Trade Commission's Antitrust Policy Statement on Sharing of Cybersecurity Information.”

Implementation of the 2014 policy statement

| 61

Hogan Lovells

• Allows information exchange between private companies about cybersecurity threats while protecting them from liability:

– “No cause of action shall lie or be maintained in any court against any private entity, and such action shall be promptly dismissed” for the sharing or receipt of a cyber threat indicator or defensive measure conducted in accordance with this title. § 106(b).

• Contains an antitrust exemption:

– “It shall not be considered a violation of any provision of antitrust laws for 2 or more private entities to exchange or provide a cyber threat indicator, or assistance relating to the prevention, investigation, or mitigation of a cybersecurity threat, for cybersecurity purposes under this title.” § 104(e)(1)-(2).

– But see § 108(e) (“Nothing in this title shall be construed to permit price-fixing, allocating a market between competitors, monopolizing or attempting to monopolize a market, boycotting, or exchanges of price or cost information, customer lists, or information regarding future competitive planning.”).

2015 statute codifies 2014 policy statement

| 62

Social Media

Education

Areas of focus

T

Hogan Lovells

https://www.linkedin.com/in/meghan-rissmiller-4aa12650

J.D., Georgetown University Law Center, 2008 B.A., magna cum laude, The College of William & Mary, 2003

Merger Clearance Agency Investigations Antitrust and Competition Litigation Consumer Protection

202 637 4658

Meghan (Edwards-Ford) Rissmiller guides companies through the thicket of U.S. merger clearance. Whether before the U.S. Department of Justice Antitrust Division or the Federal Trade Commission, Meghan has the experience and know-how to help companies develop effective clearance strategies, particularly when the transaction is complex and the antitrust issues are challenging.

She also counsels clients on a range of non-merger antitrust, including joint ventures and information exchanges, and consumer protection issues and has litigated antitrust cases in federal court and administrative actions. She has particular knowledge of technology, media, and telecommunications; aerospace, defense, and government services; and automotive industries.

Meghan joined Hogan Lovells after clerking for the Honorable Jane R. Roth of the U.S. Court of Appeals for the Third Circuit. Prior to attending law school, Meghan spent two years as a national security analyst for a major U.S. defense contractor based in Virginia.

In addition to maintaining a rigorous legal practice, Meghan is active in the American Bar Association's section of antitrust law. She's a vice chair of the pricing committee and a former member of the editorial board of the Antitrust Source. She's a longstanding member of the law school and judicial clerk recruitment committee at Hogan Lovells and supports many of the firm's diversity and inclusion initiatives.

Partner, Hogan Lovells US LLP

Meghan E.F. Rissmiller

Biography

| 63

"Hogan Lovells" or the "firm" is an international legal practice that includes Hogan Lovells International LLP, Hogan Lovells US LLP and their affiliated businesses.

The word “partner” is used to describe a partner or member of Hogan Lovells International LLP, Hogan Lovells US LLP or

any of their affiliated entities or any employee or consultant with equivalent standing.. Certain individuals, who are designated as partners, but who are not members of Hogan Lovells International LLP, do not hold qualifications equivalent

to members.

For more information about Hogan Lovells, the partners and their qualifications, see www.hoganlovells.com.

Where case studies are included, results achieved do not guarantee similar outcomes for other clients. Attorney advertising. Images of people may feature current or former lawyers and employees at Hogan Lovells or models not

connected with the firm.

© Hogan Lovells 2016. All rights reserved

www.hoganlovells.com