compensation transparency and managerial opportunism: a study of supplemental retirement plans

TRANSCRIPT

Strategic Management JournalStrat. Mgmt. J., 30: 405–423 (2009)

Published online 1 December 2008 in Wiley InterScience (www.interscience.wiley.com) DOI: 10.1002/smj.737

Received 15 February 2008; Final revision received 15 September 2008

COMPENSATION TRANSPARENCY ANDMANAGERIAL OPPORTUNISM: A STUDYOF SUPPLEMENTAL RETIREMENT PLANS

PAUL KALYTA*Telfer School of Management, University of Ottawa, Ontario, Canada

Existing research on managerial compensation is based primarily on optimal contracting andmanagerial hegemony theories. Under the optimal contracting theory, observed compensationcontracts are optimally determined, aligning the interests of managers and shareholders. Underthe managerial hegemony theory, observed compensation contracts deviate from the optimumbecause top managers with power over boards are able to influence their own pay. I arguethat the impact of managerial power over boards on managerial pay, and hence the deviation ofcompensation contracts from the optimum, is contingent on the transparency of managerial com-pensation. Within this framework, I investigate the impact of supplemental executive retirementplans (SERPs)—historically the least transparent compensation component—on opportunisticdecision making. An empirical analysis based on a time series sample of CEOs of S&P/TSX60firms provides support of the compensation transparency theory. I find that SERP benefits areprimarily driven by variables proxying for CEO power over the board, whereas more transpar-ent compensation components are primarily driven by economic factors. The results also suggestthat CEOs whose SERPs are contingent on firm performance appear to reduce firm R&D expen-ditures as they approach retirement. Both findings provide important contributions to existingresearch on the impact of managerial compensation on opportunistic decisions. Copyright 2008 John Wiley & Sons, Ltd.

INTRODUCTION

The impact of managerial compensation on man-agerial decisions is an important multidisciplinaryresearch subject, with a significant body of the-oretical and empirical knowledge accumulated instrategic management, finance, accounting, humanresources, and labor economics literature. At theheart of the issue is the conflict of interests of cor-porate shareholders and managers and the propo-sition that compensation contracts may resolve or

Keywords: executive compensation; SERP; managerialopportunism; R&D*Correspondence to: Paul Kalyta, University of Ottawa, TelferSchool of Management, 45 Laurier Avenue East, Ottawa,Ontario, K1N 6N5, Canada. E-mail: [email protected]

alleviate the conflict (e.g., Berle and Means, 1932;Jensen and Meckling, 1976). When designed prop-erly, managerial compensation increases the like-lihood of managerial decisions in the best interestsof shareholders. When designed poorly, manage-rial compensation increases the likelihood of man-agerial opportunistic decisions at the expense ofshareholder value.

A distinct feature of observed managerial com-pensation contracts is the variety of remunera-tion options. However, the variety of choices onthe compensation menu is not fully reflected inacademic studies: while some compensation com-ponents are heavily researched, others are lefton the outskirts, often due to lack of publiclyavailable data, or high costs of data processing.

Copyright 2008 John Wiley & Sons, Ltd.

406 P. Kalyta

For instance, despite significant theoretical andempirical advancements in the understanding ofthe roles of ‘traditional’ pay components (suchas base salary, performance bonuses, and morerecently, stock option grants), the research onthe impact of supplemental executive retirementplans (hereafter, SERPs) on decision making isextremely limited at best. Although sizable, com-mon, and not uniformly distributed across man-agers (e.g., Sundaram and Yermack, 2007; Kalytaand Magnan, 2008), SERP benefits are typicallyignored in compensation research due to the histor-ically poor quality of disclosure and nontrivial datacollection. Even measures of total compensationused in professional articles and academic studiesrarely account for this component of managerialpay, underestimating the magnitude of compensa-tion and distorting comparisons among compensa-tion packages.

Because of the unique nature, structure, andregulatory environment of SERPs, exploring theimpact of SERP benefits on managerial decisionsallows making several important contributions tothe literature. In this study, I provide argumentsand evidence that the structure of SERP bene-fits and the quality of SERP disclosure may leadto managerial opportunism. Two prominent casesof managerial opportunism are considered: extrac-tion of rents and reduction in research and devel-opment (R&D) expenditures. In the first case, Iprovide arguments that the manager’s ability toextract rents has a negative association with thetransparency of compensation disclosure. Hence, Ipredict that the manager’s power over the boardhas a stronger association with less transparentpay schemes. Consistent with the prediction, theresults suggest that more transparent compensa-tion components (such as salaries, cash bonuses,and stock option grants) are driven primarily byeconomic variables, whereas SERP benefits—theleast transparent component of managerial com-pensation—are driven primarily by the manager’spower over the board. In the second case, I pro-vide arguments that the manager whose SERPis contingent on firm performance in preretire-ment years is incited to select projects with lowernet present values but higher current earnings toamplify his or her SERP benefits and maximizepersonal wealth. Consequently, I predict reduc-tions in R&D expenditures in final years prior tothe manager’s retirement when SERP benefits ofthe manager are contingent on firm performance

in these years. The empirical results support theprediction.

In addition to providing empirical evidence onthe impact of SERP benefits on managerial deci-sions, the study makes two significant theoreticalcontributions. First, it extends the literature on thenature and determinants of managerial compensa-tion. Most research in this area is based on optimalcontracting and managerial hegemony paradigms.Under the optimal contracting theory, observedcompensation contracts are optimally determined,aligning the interests of managers and sharehold-ers (e.g., Holmstrom, 1979, 1982; Grossman andHart, 1983). Under the managerial hegemony the-ory, observed compensation contracts deviate fromthe optimum, because managers with power overboards are able to increase their own pay (e.g.,Mace, 1971; Finkelstein and Hambrick, 1996;Bebchuk and Fried, 2004). I extend these theoreti-cal developments by applying the concept of com-pensation transparency and providing argumentsthat the impact of managerial power over boards onmanagerial pay, and hence the deviation of com-pensation contracts from the optimum, is contin-gent on the transparency of managerial compensa-tion. The compensation transparency theory makesan important connection between the two dominantcompensation paradigms, suggesting that the opti-mal contracting framework may be more appropri-ate when managerial compensation is transparent,whereas the managerial hegemony framework maybe more appropriate when managerial compensa-tion is opaque.

Second, the study makes an important contribu-tion to the literature on managerial opportunismin long-term projects. Theoretical developmentsin this research area suggest that the managerapproaching retirement would prefer projects withhighest current earnings to projects with high-est net present values (Smith and Watts, 1982).However, empirical results are mixed and incon-clusive: although several studies find some evi-dence of reductions in firm long-term expendituresas the chief executive officer (CEO) approachesretirement (Dechow and Sloan, 1991; Gibbons andMurphy, 1992), others find no such association(Murphy and Zimmerman, 1993; Cheng, 2004). Iextend the theoretical framework by introducing amoderating factor in the relationship between themanager’s horizon and opportunism and providingarguments that the manager’s incentives to reducelong-term expenditures depend on the structure

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

Compensation Transparency and Managerial Opportunism 407

of his or her SERP benefits. The latter proposi-tion implies, inter alia, that prior empirical testsmay not find patterns of reductions in long-termexpenditures in CEO preretirement years in gen-eral, when in fact such reductions do exist in somecases and do not exist in others, depending on thestructure of CEO compensation.

THEORETICAL DEVELOPMENT

SERPs

SERPs exist in many countries due to govern-mental regulations that limit the size of regulardefined benefit or defined contribution pensions.For instance, in the United States, the annual com-pensation used as a base for calculating regularpension benefits (hereafter, pensionable earnings)is capped at $230,000.1 Consider an executive whoretires in 2008 with a $1,000,000 preretirementbase salary, 30 years of pensionable service, and apension plan that calls for two percent of the pre-retirement base salary multiplied by the numberof years of pensionable service to be paid to theexecutive annually upon retirement. Because of thecap, the executive’s regular pension is limited to$138,000 ($230, 000 × 2% × 30) or 13.8 percentof his or her preretirement salary. Similar limita-tions on the size of regular pensions exist in theUnited Kingdom, Canada, France, and most otherdeveloped economies.

SERPs increase executive postretirement incomebeyond the regular pension. Under a SERP, thefirm makes ongoing payments to the retired exec-utive on top of the regular pension until his orher death or even until the death of the survivingspouse. A SERP is a noncontributory plan: it iscompletely funded by the employer (i.e., execu-tives do not have to save for their SERP benefitswhile working). In essence, SERP benefits are sim-ilar to a postretirement salary. SERP benefits arepaid to retired executives regardless of firm per-formance in the payout years and constitute a partof firm total pension obligations.

A qualitative analysis of executive compensationdisclosures in proxy statements reveals that in mostcases, firms use the following formula to calculate

1 Source: Sections 401(a)(17), 404(l), 408(k)(3)(C), and 408(k)(6)(D)(ii) of the Internal Revenue Code. Each year, the cap isslightly modified to reflect cost-of-living adjustments.

annual SERP benefits: a certain percentage (mul-tiplier) of uncapped pensionable earnings for eachyear of pensionable service to be paid annually to aretired executive. In other words, executives accu-mulate (‘earn’) SERP benefits while working, butreceive SERP benefits only after retirement. How-ever, despite similar accumulation-payout struc-tures, SERPs differ significantly across executives.For instance, in some cases, pensionable earningsare equal to the preretirement salary. In other cases,pensionable earnings also include annual perfor-mance bonuses, making SERP benefits contingenton firm performance in preretirement years. Thelength of the period over which pensionable earn-ings are determined also differs. In some cases,pensionable earnings are equal to the compensa-tion in the final year prior to retirement. In othercases, pensionable earnings are equal to an averageannual compensation over two or more years priorto retirement. Finally, SERPs differ significantlyin specific details: provision for survivor benefits,provision for early retirement, policy on inflationadjustment, policy on the multiplier size, policy onthe accumulation of years of credited service, andso on.

Until most recently, SERP benefits have beenoften referred to in the literature as hidden or‘stealth’ compensation due to poor quality ofSERP disclosure and lack of transparency (Mur-phy, 1999; Bebchuk and Fried, 2004). Accordingto North American executive compensation disclo-sure regulations implemented in 1992–1993 andin place until 2007–2009, firms had to disclosein annual proxy statements the existence of pen-sion plans for the five highest-paid executives aswell as the methods used to calculate the pen-sions. However, firms were not required to disclosedollar values of actual, projected, or accumulatedexecutive pensions and changes in these valuesfrom one year to another. Furthermore, the for-mat of SERP disclosure was not clearly prescribedleading to vague and cumbersome disclosures inmany cases. In contrast, firms were mandated todisclose dollar values for each ‘traditional’ paycomponent (i.e., base salary, performance bonus,etc.) and report them in straightforward compensa-tion tables. As a result, the transparency of SERPdisclosure was substantially inferior to the trans-parency of disclosure of other executive pay com-ponents. The following excerpt from BombardierInc.’s 2002 proxy statement illustrates a typical

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

408 P. Kalyta

SERP disclosure resulting from 1992–1993 dis-closure regulations.

Senior Officers, including the Named ExecutiveOfficers, participate in two non-contributorydefined benefit pension plans. Benefits payablefrom the basic plan correspond to 2% of averageearnings in the three continuous years of serviceduring which they were paid their highest salary(up to a maximum salary of $86,111) times thenumber of years of credited service.

Since January 1, 2001, the supplemental plan pro-vides (depending on the management level) foradditional benefits of 1.75% of average earningsin excess of $86,111 times the number of yearsof credited service or 2.25% or 2.50% of averageearnings times the number of years of credited ser-vice, less the pension payable from the basic planand any benefits payable from other pension plansof the Corporation. Benefits are reduced by 1/3 of1% for each month between the date of early retire-ment and the date of a participant’s 60th birthdayor, if earlier, the date at which the participant’s ageplus his years of credited service total 85. No ben-efits are payable from the supplemental plan if aparticipant has not completed five years of service

. . . . Upon the death of a participant, the spouse willbe entitled to a benefit equal to 60% of the ben-efit to which such participant was entitled. If theparticipant has no spouse at the time of retirement,the benefits will be paid, after death, to the desig-nated beneficiary until such time as 120 monthlyinstallments, in the aggregate, have been paid tothe participant and to the designated beneficiary.

All benefits payable from these plans are in addi-tion to government social security benefits. Onlybase salary is taken into consideration in calculat-ing pension benefits.

Years of credited service as at January 31, 2002for each of the Named Executive Officers here-after mentioned are: Robert E. Brown 15 years,Carroll L’Italien 8 years and 1 month, Louis Morin19 years and 4 months. (Bombardier Inc., 2002: 8)

The example clearly shows the lack of SERPtransparency. First, the firm did not disclose dollarvalues of executive pensions. Second, the infor-mation disclosed in the proxy statement was notsufficient to estimate these values. To estimate themagnitude of SERP compensation, one had to col-lect additional information about executives (age,marital status, age of spouse, historical compensa-tion) from other sources, make numerous actuarial

assumptions, and perform actuarial calculations: anontrivial, time-consuming, and costly task.2

As a result of nontransparent disclosure and highcost of data collection, for decades, SERP ben-efits have been omitted from measures of totalexecutive compensation employed in professionaland academic literature. Early exceptions are lim-ited to several publications based on unrepresen-tative samples from the 1960s and 1970s. Burgess(1963), Lewellen (1968), Masson (1971), andAntle and Smith (1985) estimate values of execu-tive pensions and incorporate pension increments(annual changes in accumulated pensions) intototal compensation alongside other compensationcomponents. None of these publications focusesspecifically on executive pensions. More recently,Bebchuk and Jackson (2005) provide a descrip-tive analysis of SERPs for two groups of CEOs ofStandard & Poor’s 500 firms: those already retiredand those expected to retire. The study finds thatSERP benefits are sizable and not uniformly dis-tributed across CEOs. The mean actuarial valueof CEO SERP at retirement is $15.1 million forCEOs already retired and $19.6 million for CEOsabout to retire. Using a sample of CEOs of For-tune 500 firms, Sundaram and Yermack (2007)also confirm that SERP benefits are common andsignificant. Seventy-eight percent of CEOs in thesample have SERP arrangements. The mean pen-sion increment is $0.9 million, which equals thebase salary and represents almost 40 percent oftotal CEO cash compensation. Kalyta and Magnan(2008) obtain similar statistics for a sample of thelargest Canadian firms.

Poorly disclosed SERP benefits provide a uniquecase to study the quality of compensation dis-closure and its impact on managerial decisions.Bebchuk and Fried (2004) argue that due to vaguedisclosure, SERPs may be used by powerful exec-utives to increase their own compensation off theradar screen of shareholders. Kalyta and Magnan(2008) provide preliminary evidence that SERPs

2 On 22 December, 2006, the Securities and Exchange Commis-sion (SEC) adopted new regulations on executive compensationdisclosure in the United States. The regulations taking effect in2007 and replacing the 1992 policies require firms to disclosemore details on executive pay. According to the new regulations,the firm must disclose not only the description of executive pen-sion plans but also the dollar values attached to them. Annualchanges in accumulated pensions must be included in summarycompensation tables alongside other executive compensationcomponents. In Canada, similar executive compensation disclo-sure regulations are to take effect in 2009.

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

Compensation Transparency and Managerial Opportunism 409

may be related to measures of CEO power. Thisstudy focuses on SERP benefits to provide furthertheoretical and empirical perspective on the role ofcompensation transparency in managerial oppor-tunistic behavior. Two prominent examples ofmanagerial opportunism are considered: the man-ager’s ability to increase his or her own compen-sation, and reductions in firm R&D expenditures.

Managerial opportunism

Rent extraction

Existing research on the nature of managerial com-pensation relies primarily on optimal contractingand managerial hegemony theories. The optimalcontracting theory suggests that managerial com-pensation is a tool that incites the manager to actin the best interest of shareholders, thereby allevi-ating the agency problem (e.g., Holmstrom, 1979,1982; Grossman and Hart, 1983). From the opti-mal contracting perspective, boards and compen-sation committees are assumed to design manage-rial compensation to maximize shareholder value.Hence, various economic factors (firm size, per-formance, etc.) are expected to be dominant inexplaining the variation in the level and structureof managerial pay.3

The managerial hegemony theory builds uponthe optimal contracting concepts, but relaxes theassumption that observed board and ownershipcharacteristics are value-maximizing for share-holders. It suggests that the manager with powerover the board of directors is able to increase his orher own compensation, which leads to rent extrac-tion (e.g., Zajac and Westphal, 1995, 1997; Finkel-stein and Hambrick, 1996; Bebchuk and Fried,2004). In this context, rent is defined as the dif-ference between the manager’s actual compensa-tion and the compensation that would have beenreceived under the optimal contracting scenario.According to the managerial hegemony theory, thevariation in the level and structure of managerialpay is explained not only by economic factors, butalso by the power of the manager over the board.The manager can influence actions or inactions ofboard members in a number of ways, most notablyvia active participation in director nomination andreappointment processes and via social ties with

3 The reader is referred to Hart and Holmstrom (1987) for acomprehensive overview of the optimal contracting literature.

directors (e.g., Mace, 1971; Vancil, 1987; Fredrick-son, Hambrick, and Baumrin, 1988). In the lattercase, the manager’s power may have an impact onall board members including de jure independentoutside directors.

Normally, the extent of the manager’s powerover the board is constrained by mechanisms ofshareholder control. However, if the informationabout firm decisions or policies is not transpar-ent, shareholders may not be able to exercise thecontrol function effectively. Craighead, Magnan,and Thorne (2004) find that in the absence oftransparent compensation disclosure, firms withweak shareholder governance do not tightly linkexecutive compensation to performance. The resultsuggests that without adequate information, share-holders cannot monitor firm compensation prac-tices effectively. In this vein, Bebchuk and Fried(2004) suggest that SERP benefits make an attrac-tive choice for powerful CEOs to extract rents.Due to vague and nontransparent SERP disclosure,shareholder control over SERP benefits is likely tobe weak.

I extend Bebchuk and Fried’s (2004) argu-ment to other compensation forms and formalizeit into testable hypotheses. Based on the discus-sion above, rent extraction is expected to havea negative association with the transparency ofcompensation disclosure. In other words, CEOpower over the board is expected to have moreimpact on less transparent components of CEOpay. To test the prediction, I investigate the varia-tion in different components of CEO compensationexplained by CEO power over the board, therebyextending prior work on SERP determinants byKalyta and Magnan (2008). I define cash pay asthe most transparent compensation component. Idefine SERP benefits as the least transparent com-ponent. I define stock option grants as the mid-dle ground. Although most details on stock optiongrants are publicly available, stock option disclo-sures are not as transparent as straightforward cashpay disclosures. The following predictions are ana-lyzed:

Hypothesis 1: CEO power over the board ismore closely related to less transparent compo-nents of CEO pay.a) CEO power over the board is more closelyrelated to SERP benefits than to cash pay.

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

410 P. Kalyta

b) CEO power over the board is more closelyrelated to SERP benefits than to stock optiongrants.c) CEO power over the board is more closelyrelated to stock option grants than to cash pay.

R&D expenditures

Opportunism in R&D decisions marks one of themajor topics in the management research literature.One direction of research investigates whether firmR&D is influenced by the manager’s retirement.Smith and Watts (1982) suggest that when theanticipated tenure of the manager is shorter thanthe firm’s optimal investment horizon, the man-ager would prefer projects with lower net presentvalue but higher current earnings. The choice ofthe project with highest current earnings wouldmaximize the manager’s bonus compensation. Thecondition, commonly referred to as the horizonproblem, should be especially pronounced prior tothe manager’s retirement. In this case, the man-ager’s concern about the discipline from manage-rial labor markets becomes weaker or disappears(Gibbons and Murphy, 1992). Based on this logic,firm R&D expenditures are expected to decrease asthe manager approaches retirement. Dechow andSloan (1991) provide some empirical evidence thatthe final years prior to CEO retirement are charac-terized by reduced R&D and advertising expendi-tures. Gibbons and Murphy (1992) show that thegrowth rate of R&D intensity slows down as theCEO approaches retirement. However, later empir-ical studies find little or no association between thehorizon problem and firm long-term investments.According to Murphy and Zimmerman (1993),there is no evidence of managerial opportunismin R&D decisions when the CEO retires as part ofthe normal relay process—that is, when executivechange is an orderly and well-planned event (Van-cil, 1987). Similarly, Cheng (2004) finds no asso-ciation between CEO turnover and R&D expendi-tures.

To summarize, the empirical evidence on theimpact of the horizon problem on R&D expendi-tures is mixed and inconclusive. However, no priortheoretical or empirical study considers the impactof the manager’s retirement arrangements on his orher incentives to reduce R&D expenditures in finalpreretirement years. I suggest that some CEOs aresubstantially more incited to reduce R&D expendi-tures than others due to the structure of their SERP

benefits. To illustrate the point, I classify CEOsinto three groups according to their retirementarrangements: (1) CEOs without SERPs; (2) CEOswith SERPs in which pensionable earnings consistof base salary only and are therefore not directlycontingent on firm earnings; and (3) CEOs withSERP arrangements in which pensionable earningsconsist of base salary and performance bonus andare therefore directly contingent on firm earningsin SERP accumulation years via the bonus compo-nent. A short-term increase in firm earnings is mostbeneficial to a CEO from the third group: in thatcase, an increase in the performance bonus ampli-fies the value of the SERP and increases the pen-sion, thus providing the CEO and his or her fam-ily with monetary benefits that extend over manyyears, often until after the CEO’s death (due toSERP payouts to the surviving spouse). Since pen-sionable earnings are typically determined in thefinal several years prior to retirement, the impactof firm earnings on CEO SERP benefits should beespecially pronounced when such CEOs approachretirement.4 In other words, payoffs from projectswith higher current earnings are particularly sig-nificant for CEOs who approach retirement andwhose SERPs are performance-contingent. SuchCEOs have a strong motivation to reduce invest-ments in long-term projects and amplify their per-sonal wealth via supplemental retirement benefits.

In addition, as discussed earlier, SERPs arenot transparent and shareholder control over thisform of managerial compensation is expected tobe particularly weak. Consequently, any adverse

4 The following example illustrates the potential magnitude ofthe increase in SERP benefits. Consider a retiring CEO, with20 years of credited service, aged 60, whose annual pension is tobe determined by the product of cash compensation (base salaryplus annual bonus) in the last year prior to retirement, years ofcredited service, and a multiplier of two percent. If the salaryof the CEO in the last year prior to retirement is $1 million andthe bonus is $0, the CEO’s annual pension will be $0.4 million($1 million × 20 × 0.02) and the actuarial value of the CEO’sSERP will be $5.6 million, assuming the discount rate of 0.05and no surviving spouse. However, if the salary of the CEO inthe last year prior to retirement is $1 million and so is the bonus,the CEO’s annual pension and the actuarial value of SERP willbe $0.8 million and $11.2 million respectively. In other words,in the example above, $1 million of bonus compensation willactually increase the personal wealth of the CEO by the presentvalue equivalent of $6.6 million and will greatly contribute to theCEO’s retirement security, significantly narrowing down the gapbetween preretirement cash compensation and postretirementincome. Neither CEOs without SERPs nor CEOs with SERPswhere pensionable earnings consist of base salary only will enjoysuch significant increases in their wealth and retirement security.

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

Compensation Transparency and Managerial Opportunism 411

effects of CEO retirement arrangements on strate-gic decisions may not be easily detected by share-holder control mechanisms. This further increasesthe likelihood of opportunistic decisions, whenprojects with higher current earnings are selected atthe expense of long-term investments with highernet present values. Based on the incentive andtransparency arguments, I expect R&D expen-ditures to decrease as CEOs with performance-contingent SERPs approach retirement. Morespecifically, the likelihood of R&D decreasesshould be higher in the years when performance-based SERP benefits are determined (determina-tion years). In other words, if performance-basedSERP benefits of a given CEO are determinedbased on his or her compensation in the final n pre-retirement years, the likelihood of R&D decreasesin any of these years should be higher than (a) thelikelihood of R&D decreases in nondeterminationyears, and (b) the likelihood of R&D decreasesin determination years when SERP benefits arenot performance-based. Consequently, on average,R&D expenditures are expected to be lower whenCEOs with performance-contingent SERP benefitsare in their determination years. The following pre-diction is analyzed:

Hypothesis 2: Firm R&D expenditures are nega-tively related to the horizon problem when CEOSERP benefits are contingent on firm perfor-mance.

METHODOLOGY

Data

The sample of 60 firms that comprised the S&P/TSX60 Index in 1997 is used in the analysis. TheS&P/TSX60 Index consists of the largest publiclytraded firms listed on the Toronto Stock Exchange(TSX) as measured by market capitalization.5 A

5 See Kalyta and Magnan (2008) for the list of firms. Themajority of firms in the sample are cross-listed on the U.S.stock exchanges and all firms have a significant presence onthe U.S. consumer, capital, and labor markets. Because of ahigh level of economic integration between the United Statesand Canada, governance and compensation disclosure regimesin the two countries have been remarkably similar over time.Typically, regulatory decisions by the SEC have been quicklyfollowed by similar regulatory decisions by Canadian standardsetters. Several studies highlight other similarities between thetwo countries that are relevant to this study. Deshpande and Gol-har (1997) investigate human resources practices of U.S. and

focus on larger firms is essential to investigate therole of SERP benefits. Virtually all empirical stud-ies find that CEO cash compensation is positivelyassociated with firm size (e.g., Jensen and Mur-phy, 1990; Core, Holthausen, and Larcker, 1999).Higher cash compensation translates into a greaterdisproportion between pensionable earnings andregular pension. Consequently, SERP benefits areexpected to play a greater role for CEOs in largerfirms. As a result, the impact of CEO SERP ben-efits on managerial opportunism is expected to beespecially pronounced in such firms.

The data includes nine years of observations:from 1997 to 2005. Since all the data on CEOSERP benefits must be manually collected fromproxy statements, using time series is crucial. First,SERP benefits are estimated based on historicalcash compensation. In other words, to calculatethe value of CEO SERP benefits at the end ofyear t , one needs to find out CEO cash com-pensation in years t , t − 1, . . ., t − n, where n

depends on the terms of the SERP. Second, ‘decod-ing’ SERP disclosures and estimating SERP valuesis an extremely time-consuming exercise: as illus-trated in the previous section, SERP disclosuresare often vague and cumbersome. Consequently,the incremental cost of gathering a cross-sectionalobservation substantially exceeds the incrementalcost of gathering a time series observation.

The remaining data is gathered as follows. Com-pensation, ownership, and board structure vari-ables are collected directly from proxy statements.When CEO and firm age are not disclosed incorporate reports, I retrieve them with Lexis-Nexis and Internet search engines. Death prob-ability tables are taken from Statistics Canadapublications (http://dsp-psd.tpsgc.gc.ca/Collection/Statcan/index-e.html). Financial data is collectedfrom Compustat. Missing observations are re-trieved from Report on Business Top 1000 (pub-lished by The Globe and Mail, a division of BellGlobemedia Publishing Inc.: Toronto, Canada) andcorporate financial statements. To account for infla-tion, all monetary values are converted into 2005dollars using historic Consumer Price Indices.

Canadian firms and find that compensation practices are similaracross countries. Beine and Coulombe (2005) suggest that U.S.and Canadian labor markets are highly integrated. Many otherstudies show various cultural, economic, and regulatory similar-ities between the United States and Canada (e.g., Mittoo, 1992;Doukas and Switzer, 2000).

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

412 P. Kalyta

Empirical models

Hypothesis 1

To test the rent extraction hypotheses, I regressCEO compensation components on variables thatproxy for CEO power over the board, controllingfor economic and other factors that may have animpact on compensation. Since panel data obser-vations are reasonably expected to be correlated,I use standard panel data models that accountfor CEO-specific and time-specific effects.6 I useannual cash compensation (salary plus bonus),value of annual stock option awards, and pensionincrement as alternative dependent variables.7 Pen-sion increment represents a present value equiva-lent of annual SERP compensation. As in the priorliterature, pension increment in year t is calculatedas the actuarially adjusted difference between thepresent value of the SERP in year t and the presentvalue of the SERP in year t − 1 (Sundaram andYermack, 2007; Kalyta and Magnan, 2008). Pen-sion increment in any given year is calculated inthree steps. In the first step, I estimate the valueof the annual pension already accumulated by theCEO according to the terms of his or her SERP.8 Inthe second step, I apply death probability tables tocalculate the present value of accumulated SERPbenefits. Finally, for any year t , I calculate CEOpension increment by subtracting the present valueof SERP benefits in year t − 1 from the presentvalue of SERP benefits in year t adjusted for one-year discount rate.9

According to the prediction, variables that proxyfor CEO power over the board should have more

6 Alternatively, I control for firm-specific or industry-specificrather than CEO-specific effects in all models. Results remainqualitatively unaffected.7 To compute the value of stock option grants, I use the modelproposed by Smith and Zimmerman (1976) for employee stockoptions: Maximum (0, Stock price at grant date − Present value[Exercise price + Future value {Dividend stream compounded atthe risk-free rate until option expiration}]). The model has beenextensively used in prior executive compensation studies (e.g.,Hemmer, 1993; Magnan and St-Onge, 1997; Craighead et al.,2004; Mahoney and Thorn, 2006).8 In several cases, firms voluntarily reported the accumulatedvalue of CEO annual pension. To ensure that actuarial assump-tions are homogeneous across observations, I use estimatedrather than reported values in such cases. A comparison ofdisclosed and estimated pension values shows high similaritybetween the two measures. I also perform all the analysis withreported pension values. Results remain qualitatively unaffected.9 The reader is referred to Sundaram and Yermack (2007) fordetailed methodology of pension increment estimation.

explanatory power in less transparent compensa-tion schemes. That is, CEO power is expected tohave more impact on CEO annual pension incre-ment than on other compensation components.Table 1 provides details on explanatory variablesused in the analysis. Consistent with prior lit-erature, I use a vector of variables rather thanone variable to proxy for CEO power over theboard (e.g., Zajac and Westphal, 1996; Conyon andHe, 2004; Adams, Almeida, and Ferreira, 2005).Such methodological construct reflects the viewthat the concept of managerial power is multidi-mensional and not easily observable (Finkelstein,1992; Adams et al., 2005). I use eight variables toproxy for CEO power over the board. Most of thevariables are standard in the compensation liter-ature. First, larger boards are more likely to havegreater coordination problems. Hence, CEO poweris expected to be positively related to the size of theboard. Second, inside directors are more likely tobe influenced by the CEO due to career concerns.Hence, CEO power is expected to be negativelyrelated to the proportion of outside directors on theboard. Third, owners of large stakes in the firm aremore likely to be vigilant in their monitoring role.Hence, CEO power is expected to be negativelyrelated to the presence of a large outside block-holder.10 Fourth, the CEO who performs the role ofthe board’s chairman has greater authority over theboard’s decisions. Hence, CEO power is expectedto be positively related to the CEO-chairman dual-ity. Fifth, ownership of a greater stake in the firmprovides additional motivation for outside direc-tors to act in the shareholders’ interest. Hence,CEO power is expected to be negatively relatedto the proportion of the firm’s shares held by out-side directors. Sixth, over time, the CEO is likelyto accumulate more authority over the board espe-cially if the board is an inexperienced one. Hence,CEO power is expected to be positively related toCEO tenure relative to average outside directors’tenure.

In two cases, effects of explanatory variablescannot be predicted. The CEO who served on theboard prior to taking the CEO office is likely to

10 Prior studies typically model blockholder presence as adichotomous variable equal to one if the firm has an outsideshareholder who owns at least five percent of its shares. I use a10 percent cutoff due to data availability issues: firms listed onthe TSX are not required to disclose shareholders who own lessthan 10 percent of their shares outstanding.

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

Compensation Transparency and Managerial Opportunism 413

Tabl

e1.

Exp

lana

tory

vari

able

sin

CE

Oco

mpe

nsat

ion

regr

essi

ons

Var

iabl

eD

escr

iptio

nE

xp.

sign

Sele

cted

liter

atur

e

CE

Opo

wer

vari

able

sB

OA

RD

Num

ber

ofdi

rect

ors

onth

ebo

ard

+Y

erm

ack

(199

6),

Cor

eet

al.

(199

9),

Gri

nste

inan

dH

riba

r(2

004)

,H

ean

dC

onyo

n(2

004)

,B

rick

,Pa

lmon

,an

dW

ald

(200

6),

Sund

aram

and

Yer

mac

k(2

007)

OU

TSI

DE

Prop

ortio

nof

outs

ide

dire

ctor

son

the

boar

d−

Lam

bert

,L

arck

er,

and

Wei

gelt

(199

3),

Meh

ran

(199

5),

Gri

nste

inan

dH

riba

r(2

004)

,H

ean

dC

onyo

n(2

004)

,B

rick

etal

.(2

006)

,Su

ndar

aman

dY

erm

ack

(200

7)B

LO

CK

1if

the

firm

has

anou

tsid

esh

areh

olde

rw

hoow

nsat

leas

t10

%of

itssh

ares

outs

tand

ing,

0ot

herw

ise

−M

ehra

n(1

995)

,C

ore

etal

.(1

999)

,C

raig

head

etal

.(2

004)

,G

hosh

and

Sirm

ans

(200

4),

He

and

Con

yon

(200

4)C

HA

IRM

AN

1if

CE

Ois

the

Cha

irm

anof

the

boar

d,0

othe

rwis

e+

Cor

eet

al.

(199

9),

Cye

rt,

Kan

g,an

dK

umar

(200

2),

Gho

shan

dSi

rman

s(2

004)

,G

rins

tein

and

Hri

bar

(200

4),

He

and

Con

yon

(200

4),

Bri

cket

al.

(200

6)O

WN

DIR

Prop

ortio

nof

firm

’ssh

ares

held

byan

aver

age

outs

ide

dire

ctor

−C

ore

(200

0),

Cye

rtet

al.

(200

2),

Gho

shan

dSi

rman

s(2

004)

,H

ean

dC

onyo

n(2

004)

TE

NU

RE

Ave

rage

tenu

reof

CE

Odi

vide

dby

aver

age

tenu

reof

outs

ide

dire

ctor

s+

Sing

han

dH

aria

nto

(198

9a.

1989

b),

Wad

e,O

’Rei

lly,

and

Cha

ndra

tat

(199

0),

Mai

n,O

’Rei

lly,

and

Wad

e(1

995)

INT

ER

NA

L1

ifC

EO

serv

edon

the

boar

dbe

fore

appo

intm

ent,

0ot

herw

ise

?B

rick

etal

.(2

006)

,Su

ndar

aman

dY

erm

ack

(200

7)

OW

NC

EO

Prop

ortio

nof

firm

shar

eshe

ldby

CE

O?

Meh

ran

(199

5),

Cor

eet

al.

(199

9),

Har

vey

and

Shri

eves

(200

1),

Gho

shan

dSi

rman

s(2

004)

,H

ean

dC

onyo

n(2

004)

,B

rick

etal

.(2

006)

OW

NC

EO

SQPr

opor

tion

offir

m’s

shar

eshe

ldby

CE

Osq

uare

d?

NA

Eco

nom

icva

riab

les

SIZ

EN

atur

allo

gari

thm

offir

mre

venu

e+

Cor

eet

al.

(199

9),

Mur

phy

(199

9),

Cra

ighe

adet

al.

(200

4),

Gri

nste

inan

dH

riba

r(2

004)

,B

rick

etal

.(2

006)

,Su

ndar

aman

dY

erm

ack

(200

7)P

ER

FO

RM

Ret

urn

onfir

mas

sets

+M

urph

y(1

999)

,C

raig

head

etal

.(2

004)

,G

rins

tein

and

Hri

bar

(200

4),

Bri

cket

al.

(200

6)L

EV

ER

AG

EFi

rmde

bt-t

o-eq

uity

ratio

+H

arve

yan

dSh

riev

es(2

001)

,C

raig

head

etal

.(2

004)

,G

hosh

and

Sirm

ans

(200

4),

Bri

cket

al.

(200

6),

Sund

aram

and

Yer

mac

k(2

007)

Oth

erva

riab

les

AG

EC

EO

Age

ofC

EO

+H

arve

yan

dSh

riev

es(2

001)

,H

ean

dC

onyo

n(2

004)

,B

rick

etal

.(2

006)

AG

EF

IRM

Yea

rssi

nce

foun

ding

ofth

efir

m+

Con

yon

and

He

(200

4),

Sund

aram

and

Yer

mac

k(2

007)

FIR

STY

R1

ifth

eye

aris

the

year

whe

nC

EO

ishi

red,

0ot

herw

ise

+/?

NA

LA

STY

R1

ifth

eye

aris

the

year

whe

nC

EO

retir

es,

0ot

herw

ise

+/?

NA

Not

e:Pr

edic

ted

effe

cts

ofF

IRST

YR

and

LA

STY

Rar

epo

sitiv

ew

hen

pens

ion

incr

emen

tis

used

asth

ede

pend

ent

vari

able

and

unsp

ecifi

edw

hen

cash

pay

and

stoc

kop

tion

gran

tsar

eus

edas

the

depe

nden

tva

riab

le.

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

414 P. Kalyta

have close ties with directors. However, the out-side CEO is likely to have less knowledge of thefirm than the inside one. Assuming risk aversion,the outside CEO would demand a premium fortaking the risk of running the firm. Consequently,the outside CEO would be more ‘expensive’ thanthe internal one. In other words, the impact ofCEO internality on CEO pay may take either side.Similarly, the effect of CEO ownership is unclear.Greater CEO stake in the firm may align his or herinterests with those of shareholders. Alternatively,it may signify CEO power, influence, and author-ity. Another possibility is a curvilinear relationshipbetween CEO ownership and compensation. Someprior studies suggest that the impact of owner-ship on managerial opportunism is described byan inverted U-shaped curve (e.g., Morck, Shleifer,and Vishny, 1988; Ghosh, Moon, and Tandon,2007). To control for possible nonlinearity, I con-sider CEO ownership squared as an additionalexplanatory factor. To the best of my knowledge,the variable has not been used in executive com-pensation studies before.

Control variables and their predicted effects onCEO pay are specified according to prior studies oncompensation determinants. The group of explana-tory economic variables includes proxies for firmsize (log revenue), performance (return on assets[ROA]), and leverage (debt-equity ratio).11 A pos-itive association of CEO compensation with thesefirm-level factors is well documented in the litera-ture. The last group includes other factors that mayhave an impact on CEO pay. I control for CEOage since one’s concerns about retirement benefitsare expected to grow as the retirement approaches.I also control for firm age. Sundaram and Yer-mack (2007) find a positive association betweenfirm age and the present value of CEO SERP ben-efits. Finally, I consider two dichotomous variablesthat correspond to the first and last years the CEOoccupies his or her position. Anecdotal evidencesuggests that firms grant additional years of cred-ited service to CEOs when they join the firm (asadditional incentive) or immediately prior to retire-ment (to close the gap between preretirement andpostretirement benefits). Hence, a positive relation-ship between the two variables and CEO pensionincrement is expected.

11 Using alternative proxies for firm size (log assets), perfor-mance (return on equity) and leverage (debt-to-assets) does notaffect results.

Hypothesis 2

To test the hypothesis of R&D reduction, I regressa measure of firm R&D expenditures on theinteraction between the horizon problem and theperformance-contingency of CEO SERP benefits.The model, which controls for CEO-specific andtime-specific fixed effects, is specified below:

R&Dt = β0 + β1HORIZONt

× PERFSERPt + β2HORIZONt

+ β3PERFSERPt + β4SIZEt

+ β5PERFORMt−1 + β6LEV ERAGEt

+ β7BLOCKt + β8AGECEOt

+ β9OWNCEOt + β10OWNCEOSQt

+ ε (1)

where t is the year indicator, R&D is firm R&Dexpenditure deflated by firm revenue and relativeto industry average, HORIZON is a dichotomousvariable equal to one if t is a year in whichCEO pensionable earnings are determined, PERF-SERP is a dichotomous variable equal to one ifCEO pensionable earnings are based on the per-formance bonus, and other variables are as definedin Table 1.

The HORIZON × PERFSERP interactioncan be interpreted as a dichotomous variable thattakes the value of one when the CEO is incitedto reduce R&D expenditures, and zero otherwise.According to Hypothesis 2, the β1 coefficient isexpected to be negative and significant. In otherwords, if CEO SERPs are performance-contingent,one would expect lower R&D expenditures in CEOfinal preretirement years, when CEO pension isdetermined.12 Following prior studies, I use a rel-ative measure of R&D expenditures to control forthe variation in R&D across industries and firmsof different sizes (e.g., Dechow and Sloan, 1991;

12 The model implies that the effect of firm performance on CEOcash bonus is greater than its effect on CEO salary: a reasonableassumption due to the very nature of the two pay components.Nonetheless, it is possible that in some cases, CEO cash bonusis a function of a measure over which the CEO has little orno control. It is also possible that CEO salary is increased as aresult of firm performance while CEO bonus is unaffected. Thetwo events are unlikely to be common and would bias againstthe results of the analysis.

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

Compensation Transparency and Managerial Opportunism 415

Barker and Mueller, 2002; Cheng, 2004).13 Indus-tries are defined by Standard Industrial Classifica-tion codes at the two-digit level.

I control for firm-level factors that may have animpact on R&D expenditures. First, I include thenatural logarithm of firm revenue in the model.Although the dependent variable takes firm sizeinto account, a significant association between sizeand R&D is still possible. Second, I consider firmpast performance.14 Prior studies find conflictingevidence on the association between past perfor-mance and R&D. Hundley, Jacobson, and Park(1996) suggest that firms tend to reduce R&Dspending when unprofitable. Barker and Mueller(2002) also find a positive association between firmpast performance and R&D. However, accordingto Hitt et al. (1991), the association between thetwo variables is negative. The latter result supportsthe argument that poor performance incites firmsto engage in innovation. Third, I control for firmleverage. Prior evidence suggests that firms withhigher levels of debt appear to be less focused onlong-term projects (e.g., Baysinger and Hoskisson,1989; Long and Ravenscraft, 1993). Consequently,R&D expenditures are expected to have a negativeassociation with leverage. Finally, some empiricalstudies find a positive association between institu-tional ownership and R&D (e.g., Hansen and Hill,1991; Barker and Mueller, 2002). The result is inline with the view that institutional investors focuson long-term rather than short-term performance.However, other studies suggest that the focus ofinstitutional investors varies and depends on thenature of institutions (e.g., Kochhar and David,1996; Hoskisson et al., 2002). Since the data onthe extent and structure of institutional ownershipis not publicly available for my sample, I use thepresence of blockholders—large and active exter-nal investors other than institutions—as a controlvariable in the R&D model, recognizing the limi-tations of this proxy.

I also control for CEO-level factors that mayhave an impact on firm R&D expenditures. First, Iinclude CEO age in the model. Earlier studies sug-gest that executives become more conservative andrisk averse with age (e.g., Child, 1974; Hambrick

13 Alternatively, I use relative annual changes in R&D expendi-tures rather than relative R&D levels as the dependent variable.Results remain qualitatively unaffected.14 Using contemporaneous (PERFORMt ) rather than lagged(PERFORMt−1) performance does not affect the results.

and Mason, 1984). Barker and Mueller (2002),among others, find a negative association betweenCEO age and firm R&D spending. I also consider apotential impact of CEO ownership on firm R&D.May (1995) suggests that CEOs with significantstockholdings are more concerned about long-termfirm value. Barker and Mueller (2002) find a posi-tive association between CEO ownership and R&Dexpenditures. However, according to Ghosh et al.(2007), the relationship between the two variablesis nonlinear: R&D investments increase and thendecline as CEO ownership increases. To controlfor CEO ownership and potential nonlinearity, Iinclude the proportion of firm shares held by theCEO and its squared value in the model.

RESULTS

Since some firms from the 1997 S&P/TSX60Index were acquired during the 1998–2005 period,the initial sample contains 472 observations. Also,due to insufficient disclosure, I am unable to calcu-late pension increment in 28 CEO-years. Table 2provides key descriptive statistics (Panel A) andthe correlation matrix (Panel B). Results on thesize of CEO SERP benefits are similar to thosein Kalyta and Magnan (2008). The mean pen-sion increment is C$1.1 million.15 For compar-ison, the mean cash pay is C$1.8 million andthe mean value of annual stock option grants isC$2.4 million. Most other statistics and correlationcoefficients are also consistent with prior compen-sation and governance studies. Although many cor-relations are significant, none approaches a com-mon 0.70 criterion for multicolinearity.

To test Hypothesis 1, I regress the level of CEOcompensation components on CEO power, eco-nomic, and other variables specified in Table 1. Toaccount for possible outliers, all variables in theseand subsequent multivariate models are winsorizedat the one percent level.16 Results are reported inTable 3 (Panel A). A visual comparison of resultsin PENSION, CASH, and OPTIONS models sug-gests that the impact of CEO power on pensionincrements appears to be more substantial thanthe impact of CEO power on cash pay and stock

15 C$ denotes Canadian dollar. During the sample period(1997–2005), rates fluctuated between $0.63 and $0.86 for C$1.16 Winsorizing the data removes several extreme observations ineconomic variables. Results are not qualitatively affected if rawdata is used.

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

416 P. Kalyta

Tabl

e2.

Des

crip

tive

stat

istic

san

dco

rrel

atio

nsPa

nel

A.

Des

crip

tive

stat

istic

s

Var

iabl

eU

nits

Mea

nSt

.de

v

PE

NSI

ON

C$,

000

1,11

01,

585

CA

SHC

$,00

01,

815

1,86

6O

PT

ION

SC

$,00

02,

442

5,71

9H

OR

IZO

Nn/

a0.

394

0.49

0P

ER

FSE

RP

n/a

0.35

20.

396

R&

Dn/

a1.

077

0.25

2B

OA

RD

Dir

ecto

rs12

.63.

5O

UT

SID

En/

a0.

750

0.15

6B

LO

CK

n/a

0.49

40.

500

CH

AIR

MA

Nn/

a0.

273

0.44

6O

WN

DIR

n/a

0.00

130.

0072

TE

NU

RE

n/a

1.01

10.

986

INT

ER

NA

Ln/

a0.

560

0.48

9O

WN

CE

On/

a0.

0078

0.02

75O

WN

CE

OSQ

n/a

0.00

080.

0054

SIZ

En/

a15

.94

13.9

3P

ER

FO

RM

n/a

0.02

00.

137

LE

VE

RA

GE

n/a

0.76

50.

811

AG

EC

EO

Yea

rs54

.96.

7A

GE

FIR

MY

ears

72.4

56.0

FIR

STY

Rn/

a0.

181

0.38

0L

AST

YR

n/a

0.14

40.

352

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

Compensation Transparency and Managerial Opportunism 417

Pane

lB

.C

orre

latio

nm

atri

x

#V

aria

ble

AB

CD

∗E

∗F

GH

∗I∗

JK

L∗

MN

OP

QR

S∗

AP

EN

SIO

NB

CA

SH0.

19(0

.00)

CO

PT

ION

S0.

090.

11(0

.20)

(0.1

3)D

∗H

OR

IZO

N0.

360.

060.

07(0

.00)

(0.2

0)(0

.15)

E∗

PE

RF

SER

P0.

230.

030.

040.

46(0

.00)

(0.4

9)(0

.43)

(0.0

0)F

BO

AR

D0.

010.

11−0

.03

0.11

0.18

(0.8

3)(0

.05)

(0.6

0)(0

.04)

(0.0

0)G

OU

TSI

DE

−0.1

3−0

.07

−0.0

80.

080.

12−0

.04

(0.0

1)(0

.17)

(0.1

5)(0

.19)

(0.0

1)(0

.44)

H∗

BL

OC

K−0

.14

−0.0

30.

10−0

.10

−0.1

5−0

.17

−0.4

1(0

.03)

(0.5

6)(0

.09)

(0.0

0)(0

.00)

(0.2

2)(0

.00)

I∗C

HA

IRM

AN

0.22

−0.0

2−0

.06

0.18

0.29

0.25

0.10

−0.2

8(0

.00)

(0.7

6)(0

.28)

(0.0

0)(0

.00)

(0.0

0)(0

.06)

(0.0

0)J

OW

ND

IR0.

15−0

.10

−0.0

3−0

.10

−0.1

20.

050.

08−0

.22

−0.0

4(0

.01)

(0.0

6)(0

.54)

(0.0

5)(0

.02)

(0.3

8)(0

.20)

(0.0

0)(0

.49)

KT

EN

UR

E−0

.07

0.11

0.05

0.10

−0.0

4−0

.18

−0.1

40.

080.

210.

06(0

.25)

(0.0

4)(0

.31)

(0.0

3)(0

.45)

(0.0

0)(0

.01)

(0.1

1)(0

.00)

(0.2

3)L

∗IN

TE

RN

AL

−0.1

00.

09−0

.11

0.19

0.23

0.11

−0.0

9−0

.03

0.33

−0.1

6−0

.02

(0.1

1)(0

.14)

(0.0

4)(0

.00)

(0.0

0)(0

.06)

(0.1

2)(0

.51)

(0.0

0)(0

.02)

(0.7

4)M

OW

NC

EO

−0.0

30.

070.

140.

05−0

.09

0.13

−0.2

80.

02−0

.10

−0.0

50.

220.

13(0

.58)

(0.1

7)(0

.01)

(0.3

4)(0

.05)

(0.0

2)(0

.00)

(0.7

3)(0

.12)

(0.4

0)(0

.00)

(0.0

3)N

SIZ

E0.

150.

260.

190.

200.

310.

390.

16−0

.03

0.15

−0.2

2−0

.23

0.23

−0.1

8(0

.01)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.5

4)(0

.01)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

OP

ER

FO

RM

0.01

0.09

0.03

0.02

−0.0

70.

02−0

.02

0.10

−0.0

70.

030.

12−0

.06

0.07

−0.0

4(0

.84)

(0.1

0)(0

.50)

(0.7

1)(0

.16)

(0.7

4)(0

.71)

(0.0

6)(0

.15)

(0.6

0)(0

.02)

(0.2

2)(0

.19)

(0.4

9)P

LE

VE

RA

GE

−0.0

7−0

.10

−0.1

20.

080.

150.

530.

21−0

.28

0.28

−0.0

6−0

.12

0.11

−0.0

60.

27−0

.04

(0.2

3)(0

.05)

(0.0

1)(0

.13)

(0.0

0)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.32)

(0.0

2)(0

.05)

(0.3

0)(0

.00)

(0.4

9)Q

AG

EC

EO

−0.0

5−0

.01

0.07

0.22

0.19

−0.1

9−0

.00

0.04

0.39

0.05

0.23

0.28

−0.1

50.

060.

030.

07(0

.40)

(0.9

0)(0

.21)

(0.0

0)(0

.00)

(0.0

0)(0

.95)

(0.4

2)(0

.00)

(0.4

1)(0

.00)

(0.0

0)(0

.03)

(0.1

9)(0

.50)

(0.1

6)R

AG

EF

IRM

0.08

0.09

0.09

−0.0

30.

070.

320.

35−0

.20

0.26

−0.1

0−0

.19

0.06

−0.1

90.

39−0

.06

0.37

0.05

(0.2

2)(0

.08)

(0.1

6)(0

.47)

(0.2

3)(0

.00)

(0.0

0)(0

.00)

(0.0

0)(0

.06)

(0.0

0)(0

.26)

(0.0

0)(0

.00)

(0.2

4)(0

.00)

(0.3

5)S∗

FIR

STY

R−0

.03

−0.0

40.

02−0

.22

−0.1

50.

02−0

.05

−0.0

2−0

.21

−0.0

1−0

.46

−0.0

5−0

.21

0.04

−0.0

8−0

.03

−0.2

00.

03(0

.56)

(0.4

1)(0

.75)

(0.0

0)(0

.00)

(0.7

2)(0

.32)

(0.7

5)(0

.00)

(0.7

8)(0

.00)

(0.3

4)(0

.00)

(0.4

0)(0

.12)

(0.5

2)(0

.00)

(0.5

9)T

∗L

AST

YR

0.19

0.08

−0.1

80.

210.

12−0

.04

−0.0

80.

020.

070.

03−0

.20

0.01

0.03

−0.0

2−0

.04

−0.0

00.

19−0

.03

−0.1

2(0

.00)

(0.1

2)(0

.01)

(0.0

0)(0

.02)

(0.3

9)(0

.11)

(0.7

1)(0

.19)

(0.6

2)(0

.00)

(0.7

9)(0

.61)

(0.6

3)(0

.40)

(0.9

7)(0

.00)

(0.6

2)(0

.01)

Not

e:P

EN

SIO

Nis

CE

Oan

nual

pens

ion

incr

emen

t,C

ASH

isC

EO

annu

alca

shco

mpe

nsat

ion,

OP

TIO

NS

isC

EO

stoc

kop

tion

gran

ts,

HO

RIZ

ON

isa

dum

my

vari

able

equa

lto

one

for

year

sin

whi

chC

EO

pens

iona

ble

earn

ings

are

dete

rmin

ed,

PE

RF

SER

Pis

adu

mm

yva

riab

leeq

ual

toon

eif

CE

Ope

nsio

nabl

eea

rnin

gsar

eba

sed

onth

epe

rfor

man

cebo

nus,

R&

Dis

firm

tota

lR

&D

expe

nditu

res

defla

ted

byfir

mre

venu

ean

dre

lativ

eto

indu

stry

aver

age.

Oth

erva

riab

les

are

defin

edin

Tabl

e1.

InPa

nel

B,

colu

mns

and

row

sw

ithSp

earm

anra

nkco

rrel

atio

nsar

ede

note

dw

ithan

aste

risk

(∗ );

othe

rwis

e,Pe

arso

nco

rrel

atio

nsar

ere

port

ed.

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

418 P. Kalyta

Table 3. Determinants of CEO compensationPanel A. Multivariate models of CEO compensation

Variable PENSION CASH OPTIONS %PENSION

CEO power variablesBOARD 1.3 13.7 −14.7 0.012OUTSIDE −1.280∗∗ −224.7 −121.2 −0.287∗∗

BLOCK −397.3∗∗∗ −60.2 48.5 −0.146∗∗

CHAIRMAN 761.9∗∗∗ −398.3 −204.0 0.194∗∗∗

OWNDIR 68.1 −94.7 −61.9 −0.355∗∗

TENURE −90.5 263.5 201.3 0.029INTERNAL −472.0∗∗ −85.4 −89.2 −0.060∗∗

OWNCEO 9.6 11.4 71.3∗∗ −0.002OWNCEOSQ −83.4 79.2 −55.6 −0.028

Partial R2 0.158 0.039 0.071 0.176

Economic variablesSIZE 178.8∗∗ 274.8∗∗∗ 220.2∗∗ 0.033∗∗

PERFORM 171.5 2,315.6∗∗ 440.9 −0.005LEVERAGE −299.2∗∗ −535.5∗∗∗ −353.1∗∗ −0.222

Partial R2 0.056 0.262 0.093 0.069

Other variablesAGECEO −15.2 −22.9 −0.4 0.003AGEFIRM 4.4 −3.3 −8.9 −0.001FIRSTYR −98.0 −14.6 −182.5 −0.025LASTYR 932.3∗∗∗ 143.7 −597.8∗∗ 0.086∗∗

Partial R2 0.095 0.025 0.086 0.088

SUMMARYTotal R2 0.309 0.326 0.250 0.333

% CEO power 51.1% 12.0% 28.4% 52.9%% Economic 18.1% 80.4% 37.2% 20.7%% Other 30.7% 7.7% 34.4% 26.4%

Panel B. Variation in CEO compensation explained by CEO power variables

Prediction Significance Difference

Partial R2 Partial R2/Total R2

PENSIONCEO power > CASHCEO power p < 0.01 0.119 0.391PENSIONCEO power > OPT IONSCEO power p < 0.01 0.087 0.227OPT IONSCEO power > CASHCEO power p < 0.05 0.032 0.164

Note: ∗∗∗ p < 0.01; ∗∗ p < 0.05. Models are estimated with Huber-White standard errors. Two-tailed tests are used. %PENSION isthe proportion of pension increment in total annual compensation. Coefficients on OWNDIR, OWNCEO, and OWNCEOSQ are scaledby 1,000. R2 percentages may not add to 100% due to rounding error.

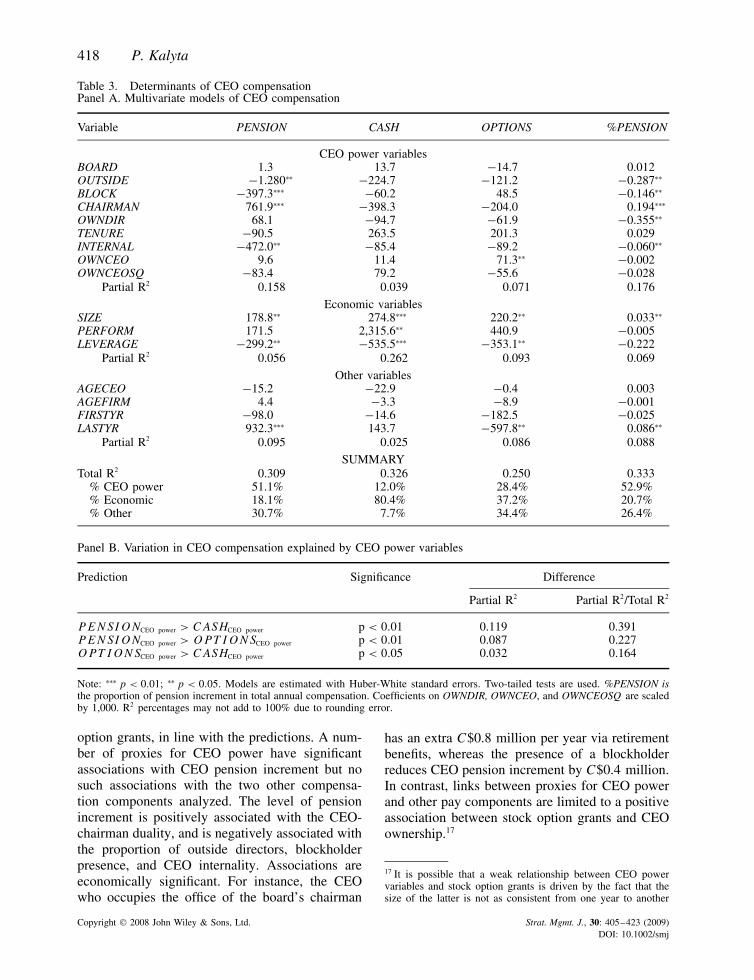

option grants, in line with the predictions. A num-ber of proxies for CEO power have significantassociations with CEO pension increment but nosuch associations with the two other compensa-tion components analyzed. The level of pensionincrement is positively associated with the CEO-chairman duality, and is negatively associated withthe proportion of outside directors, blockholderpresence, and CEO internality. Associations areeconomically significant. For instance, the CEOwho occupies the office of the board’s chairman

has an extra C$0.8 million per year via retirementbenefits, whereas the presence of a blockholderreduces CEO pension increment by C$0.4 million.In contrast, links between proxies for CEO powerand other pay components are limited to a positiveassociation between stock option grants and CEOownership.17

17 It is possible that a weak relationship between CEO powervariables and stock option grants is driven by the fact that thesize of the latter is not as consistent from one year to another

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

Compensation Transparency and Managerial Opportunism 419

For in-depth analysis, I compare percentages ofvariance explained by CEO power factors in PEN-SION, CASH, and OPTIONS models. In the firststep, I divide all explanatory variables into threesets according to Table 1: CEO Power, Economic,and Other. In the second step, I run hierarchicalmultiple regressions for each of the three com-pensation components. This allows computing thesignificance of each added set of variables andthe proportion of variation in the dependent vari-able explained by a particular set. I find that theCEO Power set explains substantially more varia-tion in the level of pension increment than it doesin the level of cash pay and stock option grants.On average, CEO power over the board explains15.8 percent of the variation in the level of CEOpension increment, 7.1 percent of the variation inthe level of CEO stock option grants, and only3.9 percent of the variation in the level of CEOcash pay.18 In contrast, economic factors explain26.2 percent of the variation in the level of CEOcash pay, 9.3 percent of the variation in the levelof CEO stock option grants, and only 5.6 percentof the variation in the level of CEO pension incre-ment. A relative analysis of partial R2s providesadditional information. The set of CEO power vari-ables accounts for 51.1 percent of total R2 in thepension increment regression, 28.4 percent in thestock options regression, and 12.0 percent in thecash regression. In contrast, the set of economicvariables accounts for 80.4 percent of the total R2

in the cash regression, 37.2 percent in the stockoptions regression, and only 18.1 percent in thepension increment regression.19 Panel B of Table 3

as the size of other compensation components. In other words,the CEO may get a substantial stock option grant in year t ,but no grant at all in year t + 1. To assess this possibility,I conduct additional analysis, aggregating the value of stockoption grants over longer time periods (two, three, or five years),and regressing the resulted measure on explanatory variablesaveraged over the same period. The results remain qualitativelyunchanged. The proportion of each set of variables in totalR2 remains generally constant across models. The relationshipbetween CEO ownership and the value of stock option grantsremains significant when stock option grants are averaged overtwo or three years but becomes marginally significant (p < 0.10)when a five-year period is used. Other proxies for CEO powerremain statistically insignificant in explaining the variation inthe value of stock option grants.18 To ensure that results are robust to the choice of the order ofsets in the model, I run regressions for each possible hierarchy.Results remain qualitatively unchanged.19 Cash pay includes two components: base salary and annualbonus. It is possible that the determinants of the two cashcomponents differ, affecting the results in the CASH model.

summarizes the relationship between CEO powervariables and different compensation components.

To address the possibility that SERP benefits aresubstitutes for some other compensation compo-nent, I deflate pension increment by total compen-sation awarded to the CEO in a given year andinvestigate its determinants. The resulting variablecan be described as the proportion of nontrans-parent pay in the CEO compensation contract. Toperform arcsine root transformation of the depen-dent variable, I remove 22 observations in whichpension increment is negative.20 Results, reportedin the last column of Table 3 (Panel B), are similarto those reported in the PENSION model. Consis-tent with expectations, I find a significant impactof CEO power on the proportion of pension incre-ment in total CEO compensation. To summarize,the results provide support of Hypothesis 1, sug-gesting that less transparent compensation compo-nents are driven primarily by CEO power, whereasmore transparent CEO compensation componentsare driven primarily by economic variables.21

Descriptive statistics in Table 2 suggest thatperformance-contingent SERPs account for 35.2percent of observations in the sample. To testwhether the structure of CEO retirement benefits

To address the possibility, I estimate separate models for basesalary and cash bonus. The conclusions remain unaffected: bothcash pay components are primarily driven by economic factorsand have modest associations with CEO power.20 In contrast to other pay components, pension increment in agiven year can be negative. For instance, the firm may changeone or several SERP provisions in a way that reduces the valueof accumulated SERP benefits (e.g., decrease the multiplier).Removing observations with negative pension increments isnecessary to perform arcsine root transformation (e.g., Sokaland Rohlf, 1995; Zar, 1999) and estimate the model in whichthe dependent variable is the proportion of pension incrementin total CEO compensation. However, a potential downside isan overestimation of the proportion of pension increment intotal CEO compensation. To assess the degree of overestimation,I compare the average pay structure in the full sample withthe average pay structure in the reduced sample. Excludingobservations with negative pension increments overestimates theproportion of pension increment in total CEO compensation byless than one percent only and is not expected to affect theresults.21 I also perform factor analysis of CEO power variables to fur-ther triangulate the findings (unreported for brevity). I combineproxies for CEO power into one factor, estimate factor scores foreach observation, and run compensation regressions with CEOpower factor scores as the dependent variable, controlling foreconomic and other variables from Table 1. Despite insignificantfactor loadings in individual cases (consistent with the results inTable 3), CEO power factor scores are positive and significantin explaining pension increments. In contrast, I find no associ-ation between CEO power scores and other, more transparentcompensation components.

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

420 P. Kalyta

Table 4. Determinants of firm R&D expenditures

Variable Base sample Matched sample

HORIZON −0.028 −0.043 −0.081 −0.066PERFSERP −0.023 −0.021 −0.008 −0.029SIZE −0.026 −0.030 0.047 0.024PERFORM 0.148 0.120 0.133 0.095LEVERAGE −0.153∗∗ −0.180∗∗ −0.207∗∗∗ −0.220∗∗∗

BLOCK 0.179∗∗ 0.164∗∗ 0.206∗∗ 0.137∗∗

AGECEO −0.019 −0.038 −0.005 −0.020OWNCEO 0.015∗∗∗ 0.013∗∗∗ 0.008∗∗ 0.011∗∗

OWNCEOSQ −0.003 −0.003 0.003 0.002HORIZON × PERFSERP −0.201∗∗∗ −0.305∗∗∗

Adjusted R2 0.209 0.254 0.190 0.249R2 change 0.045∗∗∗ 0.059∗∗∗

n 472 472 332 332

Note: ∗∗∗ p < 0.01; ∗∗ p < 0.05. Models are estimated with Huber-White standard errors. Two-tailed tests are used. Coefficients onOWNCEO and OWNCEOSQ are scaled by 1,000.

affects firm R&D expenditures, Equation 1 is esti-mated. To enhance the reliability of the analysis,I use base sample and matched sample as twoalternatives.22 Results, reported in Table 4, pro-vide empirical support of Hypothesis 2. I findthat firms whose CEOs have short horizons andperformance-contingent SERPs (HORIZON ×PERFSERP = 1) are characterized by lowerR&D expenditures. Also, the inclusion of the inter-action term significantly increases the explanatorypower of the models. In contrast, when consid-ered separately, the horizon problem and SERPstructure have no significant association with firmR&D expenditures. In other words, consistent withprior literature (e.g., Cheng, 2004), I find no impactof CEO turnover on firm R&D in general. How-ever, I find that the association between the hori-zon problem and R&D expenditures is contingenton the structure of CEO SERP benefits. Firmsappear to reduce R&D expenditures when CEOswith performance-contingent SERPs are in theirdetermination years. The result is economicallysignificant: the coefficient on the interaction termsuggests that on average, the ratio of firm R&Dexpenditures relative to the industry mean is lowerby around 20 percent in these years. In contrast,there is no evidence of managerial opportunism inR&D decisions when CEO SERP benefits do not

22 In the latter case, observations with hypothesized reductionsin R&D (i.e., HORIZON × PERFSERP = 1) are matchedwith observations with no hypothesized reductions in R&D (i.e.,HORIZON × PERFSERP = 0) based on the two-digit SICcode, calendar year, and the closest ROA in the previous year.

depend on performance bonuses or when the CEOhas no SERP. The findings are consistent with theprediction that CEOs approaching retirement areincited to select projects with highest current earn-ings at the expense of long-term projects to amplifytheir retirement benefits.

CONCLUSIONS

I argue that shareholder control over poorly dis-closed SERP benefits is substantially weaker thanshareholder control over other, more transparentcompensation components, thus providing fertileground for managerial opportunism. I investigatethe role of SERP benefits in two prominent exam-ples of managerial opportunism: rent extractionand R&D reduction. Overall, the results supportthe predictions. Specifically, I find that the level ofCEO SERP benefits and the proportion of SERPbenefits in total CEO compensation are primarilydriven by variables proxying for CEO power overthe board. In contrast, more transparent compensa-tion components are primarily driven by economicfactors, including firm past performance, and havemodest associations with CEO power. The find-ing supports the prediction that CEOs with powerover boards are able to increase their own compen-sation via SERPs. It also suggests that the CEO’sability to exercise his or her power and extractrents via well-disclosed and transparent compen-sation components is limited. More generally, theassociation between managerial power and rent

Copyright 2008 John Wiley & Sons, Ltd. Strat. Mgmt. J., 30: 405–423 (2009)DOI: 10.1002/smj

Compensation Transparency and Managerial Opportunism 421

extraction appears to be contingent on the trans-parency of managerial compensation.