compensation and workforce trends in the medical … by radford radford is part of aon hewitt, a...

TRANSCRIPT

Prepared by RadfordRadford is part of Aon Hewitt, a business unit of Aon plc.

Compensation and Workforce Trends in the Medical Device IndustryBoston, MAEd Speidel, PartnerRam Kumar, Director

RadfordProprietary & Confidential2

Today’s Topics

US Market and Employment Outlook Labor Trends Short-Term Incentive Practices Private and Public Long-Term Incentive Practices Executive Compensation and Governance Trends

RadfordProprietary & Confidential3

US Unemployment

The unemployment rate in Massachusetts has tracked below the national average for years and stands at 4.7% as of November 2015

Buoyed by the high volume of life sciences jobs, the state emerged strongly out of the recession and experienced solid job growth in recent years

Source: Economic Data, Federal Reserve Bank of St. Louis.

5.04.74.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Northeast Massachusetts US

RadfordProprietary & Confidential4

US Equity Market

High-performing life sciences stocks fell into bear territory in September 2015, and though the market has made a slight recovery, some stocks are still stumbling

Source: Yahoo! Finance.

0%

50%

100%

150%

200%

250%

300%

350%

1/2015 2/2015 3/2015 4/2015 5/2015 6/2015 7/2015 8/2015 9/2015 10/2015 11/2015

Dow Jones NASDAQ NASDAQ Healthcare

RadfordProprietary & Confidential5

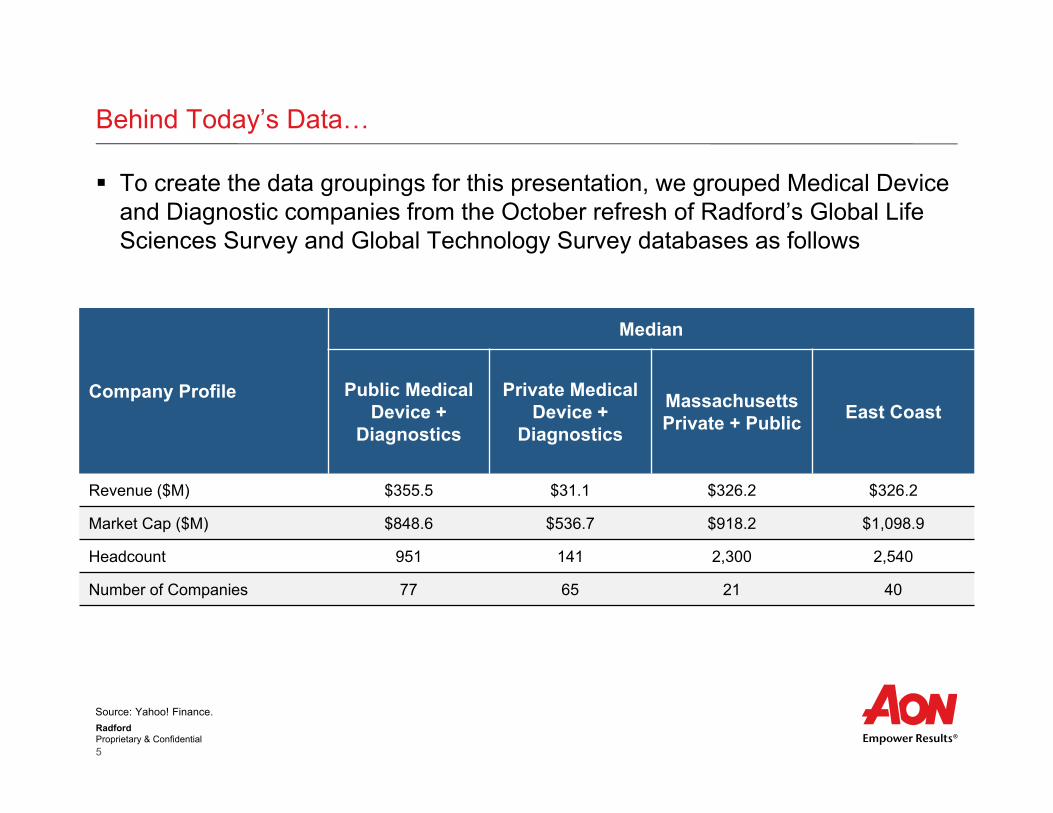

Behind Today’s Data…

To create the data groupings for this presentation, we grouped Medical Device and Diagnostic companies from the October refresh of Radford’s Global Life Sciences Survey and Global Technology Survey databases as follows

Source: Yahoo! Finance.

Company Profile

Median

Public Medical Device +

Diagnostics

Private Medical Device +

Diagnostics

Massachusetts Private + Public East Coast

Revenue ($M) $355.5 $31.1 $326.2 $326.2

Market Cap ($M) $848.6 $536.7 $918.2 $1,098.9

Headcount 951 141 2,300 2,540

Number of Companies 77 65 21 40

RadfordProprietary & Confidential6

The Medical Device Industry in the Spotlight

Johnson & Johnson to Slash 3000 Jobs in Medtech BizThe healthcare giant is continuing its restructuring of its medical device business by paying off approximately 3000 workers in its medical device unit over the next two years

Why Are Investors Running Away From Medical Devices?“Venture capital for device manufacturers has been drying up for a while…The slowdown in the rise of healthcare spending is also contributing to the drought in venture capital… [Further] the FDA is improving its performance, but the recent history of device failures still looms large, and has energized critics of the device industry.” (December 2015)

With Early Stage Investing Stifled, Things Look Grim for the Medical Device Industry“There’s a marked lack of investing in early stage companies – stifling tech growth in the entire medical device industry…The lack of funding in early stage investment comes from “an increasingly uncertain reimbursement climate, exacerbated by the repetitive nature of medtech innovation, and the resulting pressure for companies to find new ways to demonstrate the value of their products.” (October 2015)

RadfordProprietary & Confidential7

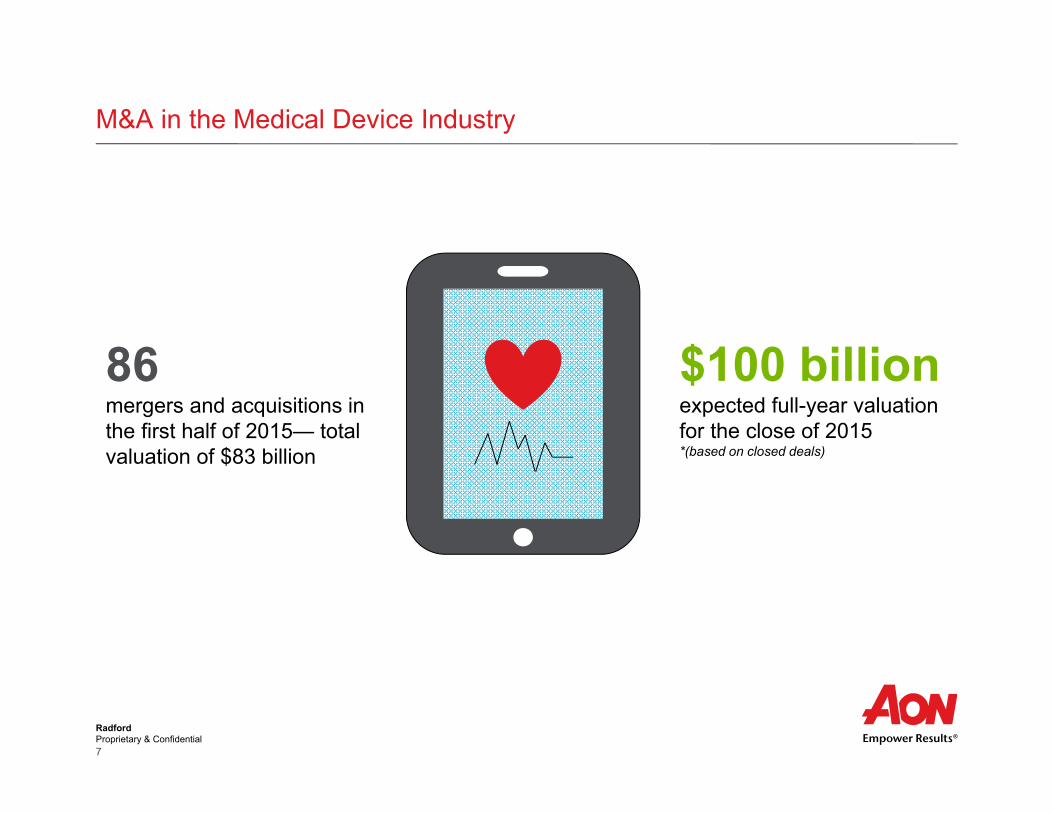

M&A in the Medical Device Industry

86mergers and acquisitions in the first half of 2015— total valuation of $83 billion

$100 billion expected full-year valuation for the close of 2015 *(based on closed deals)

RadfordProprietary & Confidential8

M&A in the Medical Device Industry

Just in the later months of 2015, the industry snagged the headlines below

Flextronics Expands Medical Design Capabilities With Acquisition Of Farm Design

Medtronic Smacks Down $110 Million Cash for Aircraft Medical

Technimark Acquires Leading Medical Component Manufacturer Ci Medical Technologies

Quest Diagnostics To Acquire Clinical Laboratory Partners' Outreach Laboratory Service Business In Connecticut

Medtronic CEO Ponders Over Sale of Some Covidien Assets Henry Schein Makes Second Purchase in Two Days

Ekso Bionics Acquires Gravity Balancing Arm Technology From Equipois Endologix Ponies Up $211 Million for TriVascular Tech

VC-Backed Kuros Biosurgery Merges with Cytos Biotech St. Jude Medical Completes Acquisition Of Thoratec

Galil Medical Extends Tender Offer Period To Acquire Perseon Johnson & Johnson Execs Hint at Possible M&A Drug or

Medical Device Deals Amid $10 Billion Share Buyback Move

Symmetry Medical Acquires Single-Use, Low Profile Retractor Product From Insightra Medical Inc. Progenics Makes $7 Million Bid for EXINI Diagnostics

RadfordProprietary & Confidential9

3% 2%26%

38% 40%50%

33%22%

48% 31%

60% 40%

45%57%

26% 31%10%

20% 19%

0%10%20%30%40%50%60%70%80%90%

100%

Public Private Massachusetts East Coast Q3 All US Med.Dev.

+ Diagnostics

Q2 All US Med.Dev.

+ Diagnostics

Freeze Selective Normal Aggressive

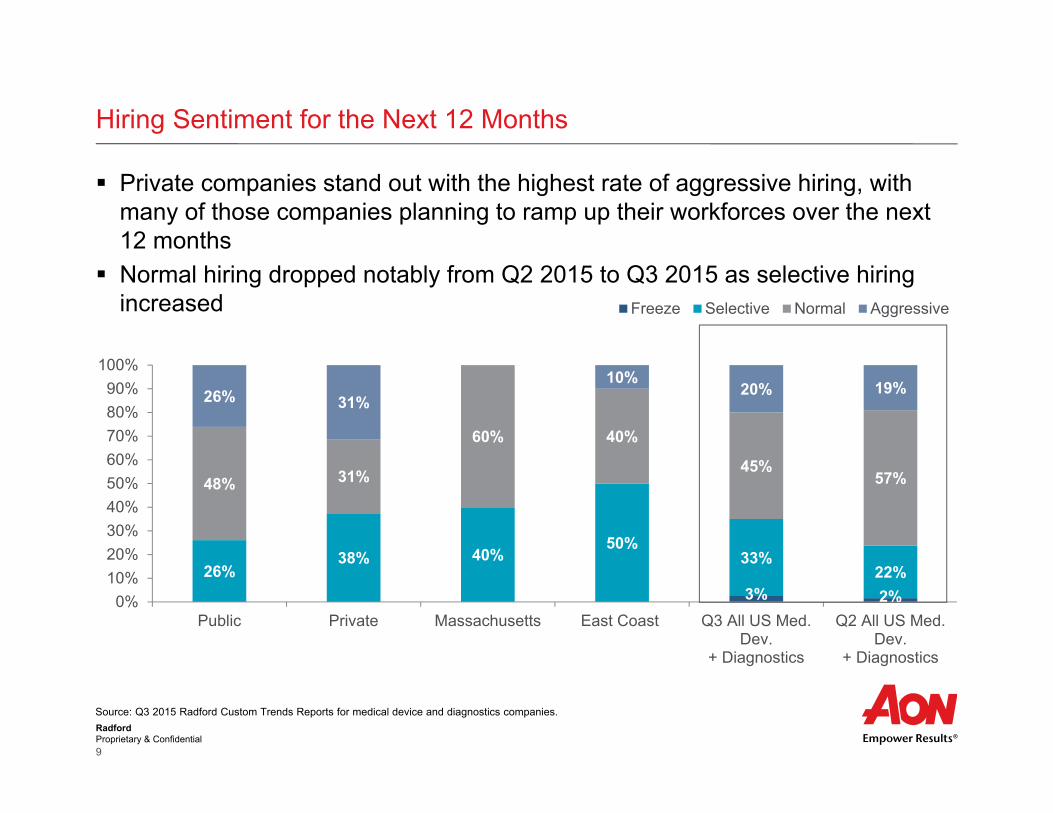

Hiring Sentiment for the Next 12 Months

Private companies stand out with the highest rate of aggressive hiring, with many of those companies planning to ramp up their workforces over the next 12 months

Normal hiring dropped notably from Q2 2015 to Q3 2015 as selective hiring increased

Source: Q3 2015 Radford Custom Trends Reports for medical device and diagnostics companies.

RadfordProprietary & Confidential10

Expected Workforce Changes for the Next 12 Months

Interestingly, medical device companies are hardly reporting expected decreases in headcount over the next 12 months

Private companies stand out among Massachusetts, the East Coast and the overall US industry, with 62% of companies planning to increase their workforces over the coming year

Industries &Regions Decrease

Stay The Same Size

Increase by up to

10%

Increase by morethan 10%

Unknown

Public 4% 35% 35% 17% 8%

Private -- 25% 31% 31% 13%

Massachusetts -- 40% 40% -- 20%

East Coast -- 50% 20% 20% 10%

All US Med. Dev. + Diagnostics -- 40% 23% 22% 15%

Source: Q3 2015 Radford Custom Trends Reports for medical device and diagnostics companies.

RadfordProprietary & Confidential11

Historical Turnover in the US Medical Device and Diagnostics Industry

Trailing 12-month voluntary turnover is rising slowly after a post-recession drop and may be stabilizing as we head into 2016

9.3% 9.8% 10.7%

5.9% 4.7%5.9%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

2013 2014 2015

Voluntary Turnover Involuntary Turnover

15.2% 14.5%16.6%

Source: Radford Trends Reports for medical device and diagnostics companies, Q3 2013, Q3 2014 and Q3 2015.

RadfordProprietary & Confidential12

Turnover

Turnover among private companies is considerably lower than turnover at public companies, however voluntary turnover among the group is relatively high, as many private companies indicate plans to ramp up workforce growth this year

11.4% 9.8% 10.4% 10.7%

5.9%

4.7%5.3% 5.9%

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%

Public Private Massachusetts East Coast

Voluntary Turnover Involuntary Turnover

17.3%

14.5%16.6%

Source: Q3 2015 Radford Custom Trends Reports for medical device and diagnostics companies.

15.7%

RadfordProprietary & Confidential13

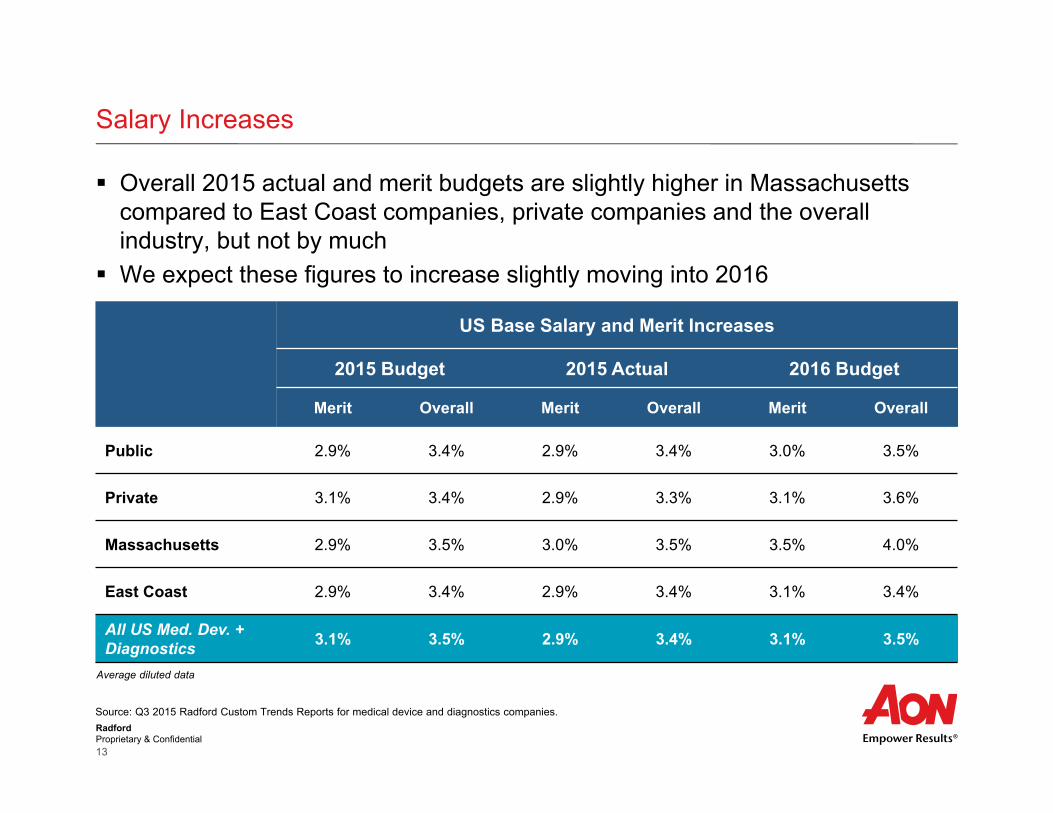

Salary Increases

Overall 2015 actual and merit budgets are slightly higher in Massachusetts compared to East Coast companies, private companies and the overall industry, but not by much

We expect these figures to increase slightly moving into 2016

US Base Salary and Merit Increases

2015 Budget 2015 Actual 2016 Budget

Merit Overall Merit Overall Merit Overall

Public 2.9% 3.4% 2.9% 3.4% 3.0% 3.5%

Private 3.1% 3.4% 2.9% 3.3% 3.1% 3.6%

Massachusetts 2.9% 3.5% 3.0% 3.5% 3.5% 4.0%

East Coast 2.9% 3.4% 2.9% 3.4% 3.1% 3.4%

All US Med. Dev. + Diagnostics 3.1% 3.5% 2.9% 3.4% 3.1% 3.5%

Average diluted data

Source: Q3 2015 Radford Custom Trends Reports for medical device and diagnostics companies.

RadfordProprietary & Confidential14

Short-Term Incentive Practices

RadfordProprietary & Confidential15

Types of Incentive Plans

Across all groupings, the majority of companies provide some form of cash incentive plan

Historically the medical device industry has stood out against other life sciences industries with higher rates of discretionary and cash profit sharing bonus plans

Metric Prevalence

Bonus Metric

Public Private MA East CoastAll US Med.

Dev. + Diagnostics

Companies with bonus/incentive compensation plan

95.8% 86.2% 100.0% 100.0% 89.3%

Types of Plans (% companies = of those with any plan)

Formal Bonus 96.7% 73.4% 94.1% 93.1% 83.8%

Discretionary Bonus 31.5% 44.4% 35.3% 41.4% 39.3%

Cash Profit Sharing 9.8% 5.8% -- 3.4% 6.0%

Source: Q3 2015 Radford Custom Practices Reports for medical device and diagnostics companies.

RadfordProprietary & Confidential16

Formal Bonus Plan Participation

Source: Q3 2015 Radford Custom Practices Reports for medical device and diagnostics companies.

% Employees Receiving Formal Bonus

Public Private MA East CoastAll US Med.

Dev. + Diagnostics

Percent of Employees in the US 64.5% 65.9% 65.2% 65.1% 65.2%

Percent of Employees Globally(includes US)

62.9% 64.0% 63.5% 61.6% 63.2%

Across all groupings, most employees are receiving a formal bonus

RadfordProprietary & Confidential17

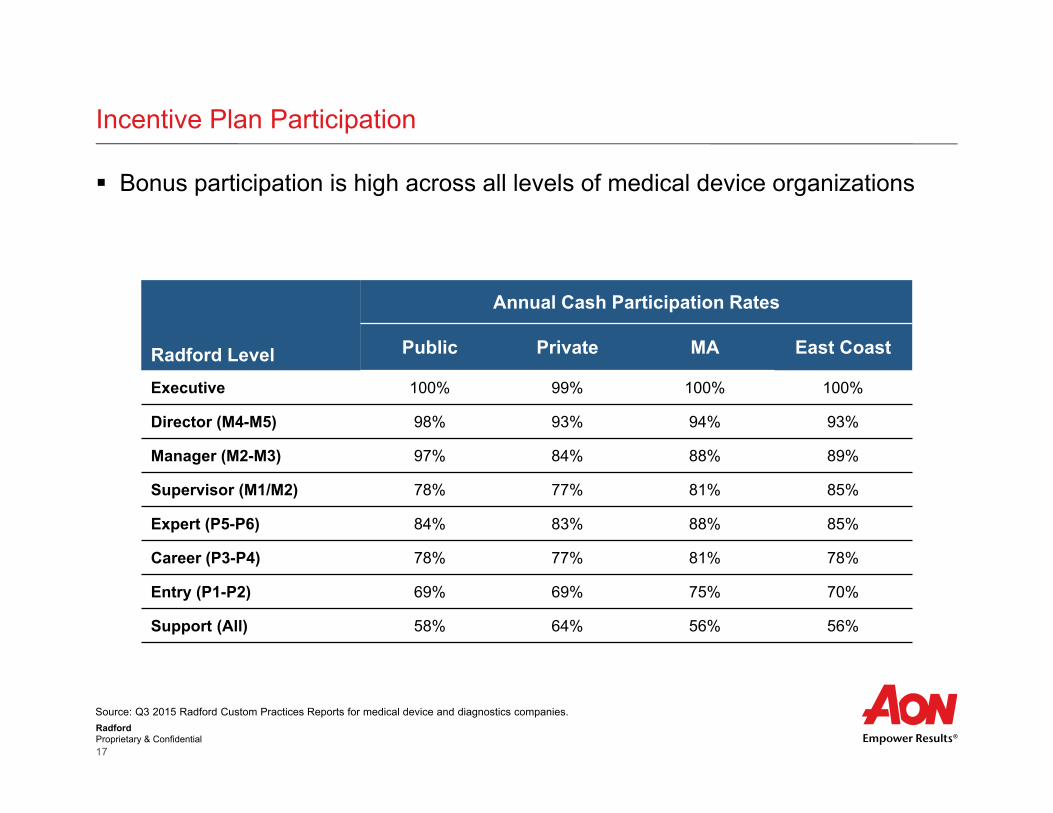

Incentive Plan Participation

Bonus participation is high across all levels of medical device organizations

Radford Level

Annual Cash Participation Rates

Public Private MA East Coast

Executive 100% 99% 100% 100%

Director (M4-M5) 98% 93% 94% 93%

Manager (M2-M3) 97% 84% 88% 89%

Supervisor (M1/M2) 78% 77% 81% 85%

Expert (P5-P6) 84% 83% 88% 85%

Career (P3-P4) 78% 77% 81% 78%

Entry (P1-P2) 69% 69% 75% 70%

Support (All) 58% 64% 56% 56%

Source: Q3 2015 Radford Custom Practices Reports for medical device and diagnostics companies.

RadfordProprietary & Confidential18

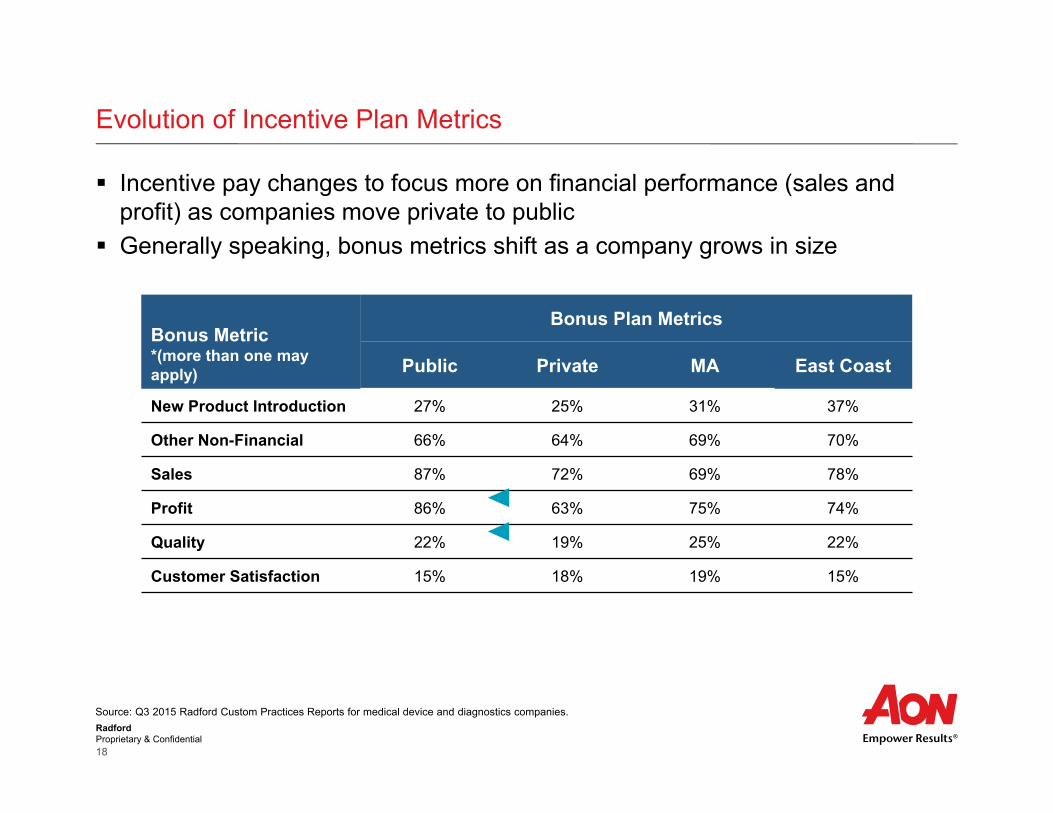

Evolution of Incentive Plan Metrics

Incentive pay changes to focus more on financial performance (sales and profit) as companies move private to public

Generally speaking, bonus metrics shift as a company grows in size

Bonus Metric*(more than one may apply)

Bonus Plan Metrics

Public Private MA East Coast

New Product Introduction 27% 25% 31% 37%

Other Non-Financial 66% 64% 69% 70%

Sales 87% 72% 69% 78%

Profit 86% 63% 75% 74%

Quality 22% 19% 25% 22%

Customer Satisfaction 15% 18% 19% 15%

Source: Q3 2015 Radford Custom Practices Reports for medical device and diagnostics companies.

RadfordProprietary & Confidential19

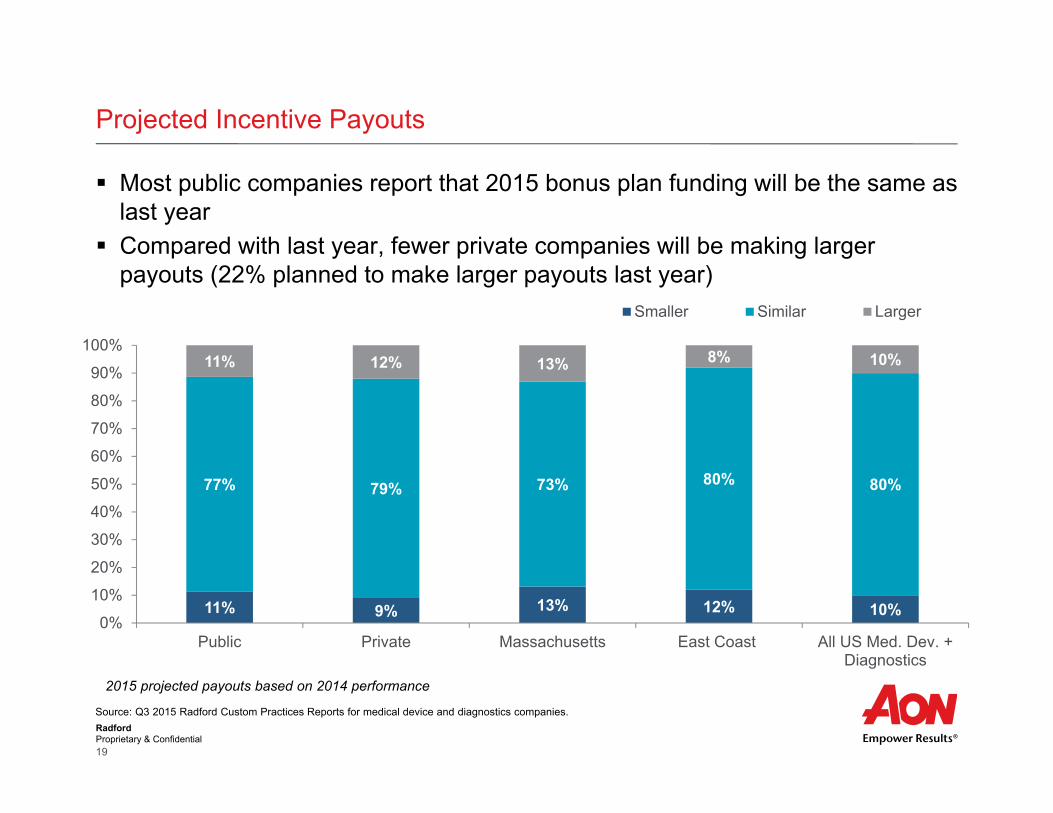

Most public companies report that 2015 bonus plan funding will be the same as last year

Compared with last year, fewer private companies will be making larger payouts (22% planned to make larger payouts last year)

Projected Incentive Payouts

2015 projected payouts based on 2014 performance

Source: Q3 2015 Radford Custom Practices Reports for medical device and diagnostics companies.

11% 9% 13% 12% 10%

77% 79% 73% 80% 80%

11% 12% 13% 8% 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Public Private Massachusetts East Coast All US Med. Dev. +Diagnostics

Smaller Similar Larger

RadfordProprietary & Confidential20

Private and PublicLong-Term Incentive Practices

RadfordProprietary & Confidential21

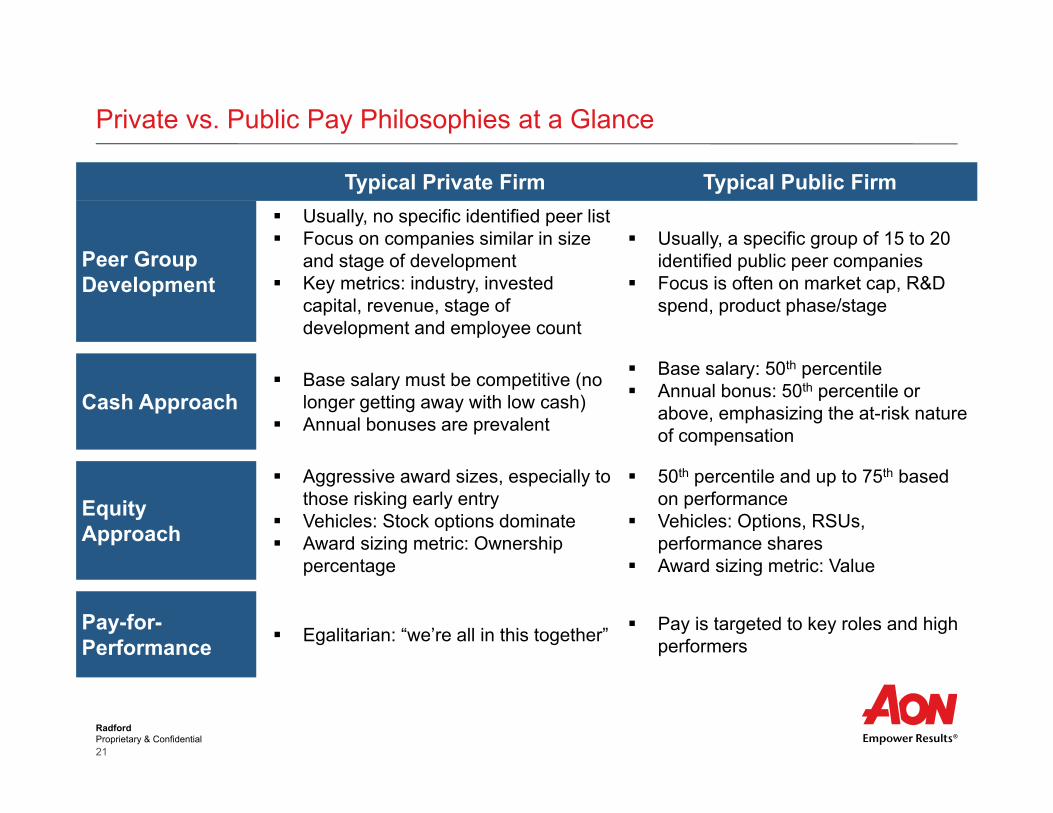

Private vs. Public Pay Philosophies at a Glance

Typical Private Firm Typical Public Firm

Peer Group Development

Usually, no specific identified peer list Focus on companies similar in size

and stage of development Key metrics: industry, invested

capital, revenue, stage of development and employee count

Usually, a specific group of 15 to 20 identified public peer companies

Focus is often on market cap, R&D spend, product phase/stage

Cash Approach Base salary must be competitive (no

longer getting away with low cash) Annual bonuses are prevalent

Base salary: 50th percentile Annual bonus: 50th percentile or

above, emphasizing the at-risk nature of compensation

Equity Approach

Aggressive award sizes, especially to those risking early entry

Vehicles: Stock options dominate Award sizing metric: Ownership

percentage

50th percentile and up to 75th based on performance

Vehicles: Options, RSUs, performance shares

Award sizing metric: Value

Pay-for-Performance Egalitarian: “we’re all in this together” Pay is targeted to key roles and high

performers

RadfordProprietary & Confidential22

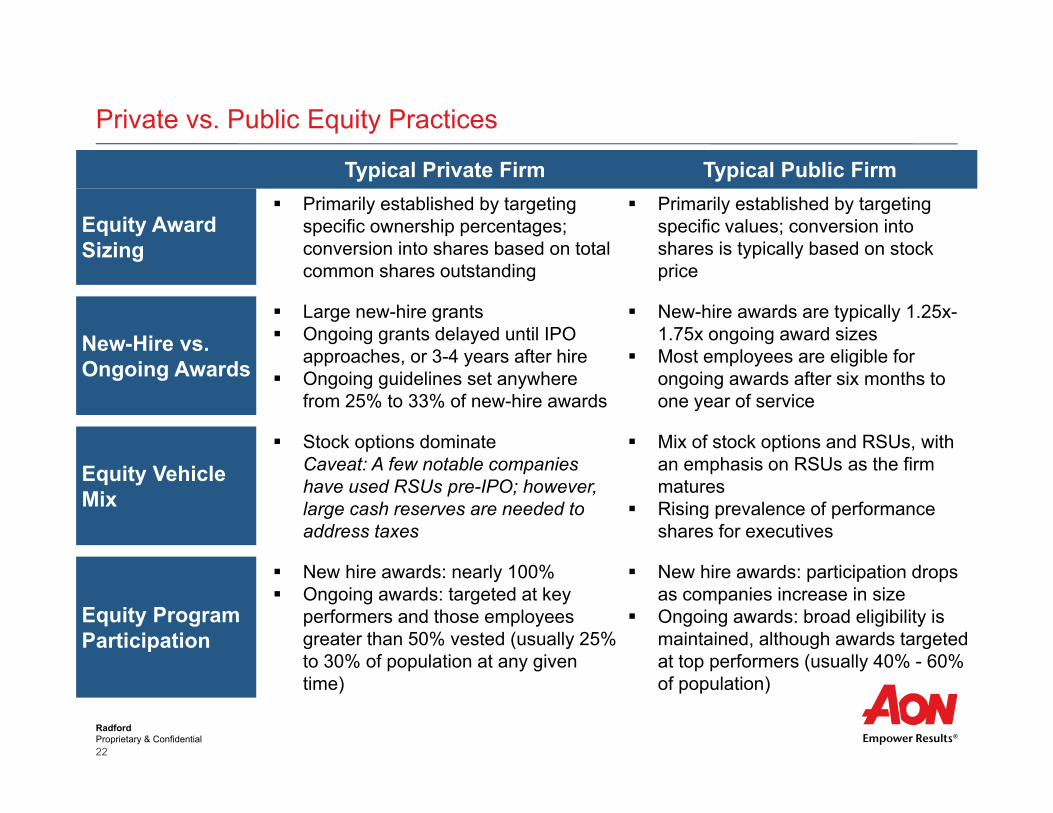

Private vs. Public Equity Practices

Typical Private Firm Typical Public Firm

Equity Award Sizing

Primarily established by targeting specific ownership percentages; conversion into shares based on total common shares outstanding

Primarily established by targeting specific values; conversion into shares is typically based on stock price

New-Hire vs. Ongoing Awards

Large new-hire grants Ongoing grants delayed until IPO

approaches, or 3-4 years after hire Ongoing guidelines set anywhere

from 25% to 33% of new-hire awards

New-hire awards are typically 1.25x-1.75x ongoing award sizes

Most employees are eligible for ongoing awards after six months to one year of service

Equity Vehicle Mix

Stock options dominateCaveat: A few notable companies have used RSUs pre-IPO; however, large cash reserves are needed to address taxes

Mix of stock options and RSUs, with an emphasis on RSUs as the firm matures

Rising prevalence of performance shares for executives

Equity Program Participation

New hire awards: nearly 100% Ongoing awards: targeted at key

performers and those employees greater than 50% vested (usually 25% to 30% of population at any given time)

New hire awards: participation drops as companies increase in size

Ongoing awards: broad eligibility is maintained, although awards targeted at top performers (usually 40% - 60% of population)

RadfordProprietary & Confidential23

Aligning Equity with Stage of Development

Long-Term Incentive Vehicles

Company Profile

Objectives and ImplicationsStartup/ Pre-IPO

Mid-Cap/ Growth Market

Mid-Cap/ Mature Market

Large Cap/Mature Market

Stock Options Only Stock options help employees focus on upside

potential, either stock price growth or company valuation growth

Restricted Shares/ Units Only

Restricted shares/units de-emphasize stock price growth in favor of employee retention and ownership

Stock Options and Restricted Shares/ Units

A mixed approach attempts to balance growth with retention, and typically involves different mixes for different employee levels

PerformanceShares/ Units

Performance shares allow companies to introduce targeted goals (beyond stock price growth) into their equity programs

Long-Term Cash Often used in conjunction with equity, long-term

cash allows for more diversity of performance goals, but requires an ability to set goals over multiple years

Relative Total Shareholder Return

The use of TSR metrics typically reflects alignment with the institutional investor perspective (i.e., portfolio performance) and requires a stable peer group

Emerging Practice Least Common PracticeMost Common Practice

RadfordProprietary & Confidential24

Focus on Individual Ownership

Private companies typically focus on employee ownership percentages as the best apples-to-apples point of comparison for delivering competitive equity packages

Employee Level

Median Individual Ownership by Level of Invested Capital

Under $40M $40M to $80M Over $80M

CEO 7.509% 4.293% 3.803%

Founder 8.623% 5.506% 4.195%

Non-Founder 7.127% 4.195% 3.082%

CFO 0.926% 0.639% 0.825%

Top HR Executive 0.351% 0.347% 0.309%

Vice President 0.688% 0.614% 0.548%

Director 0.254% 0.283% 0.075%

Manager 0.063% 0.120% 0.040%

Professional 0.027% 0.032% 0.012%

Support 0.006% 0.012% 0.005%

Source: Radford’s Pre-IPO/Venture-Backed Survey. Data shown are a roll-up of Radford levels taken at the median.

RadfordProprietary & Confidential25

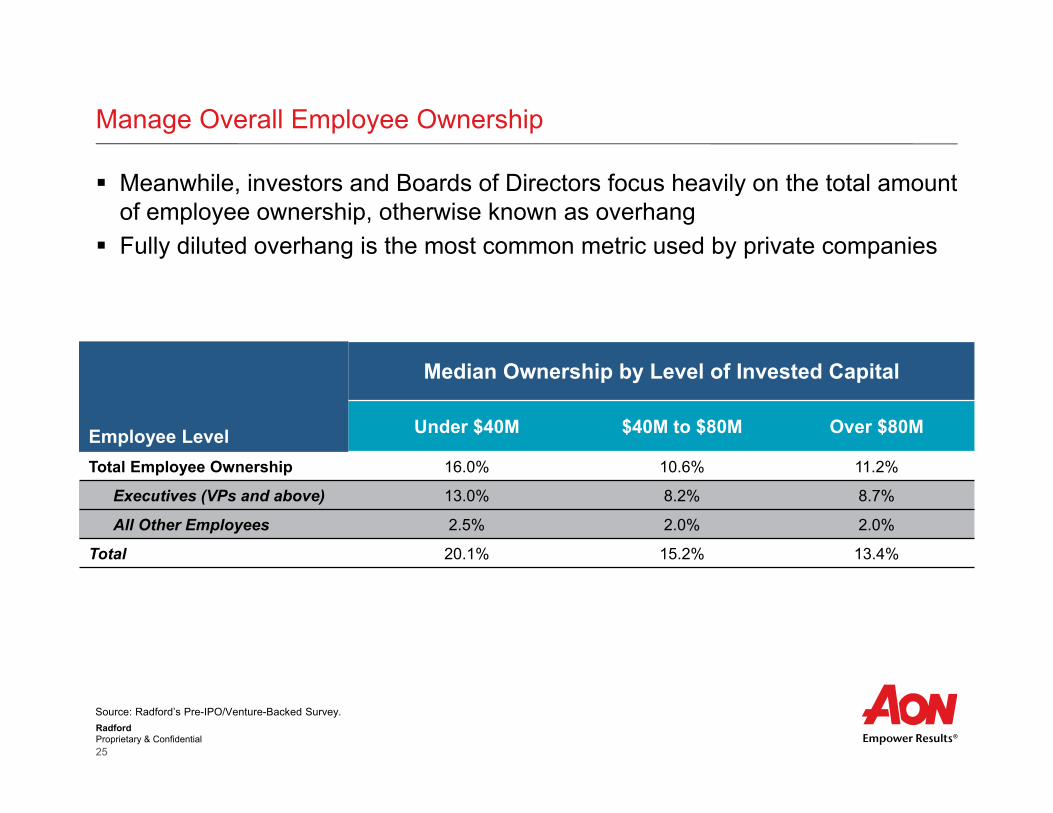

Manage Overall Employee Ownership

Meanwhile, investors and Boards of Directors focus heavily on the total amount of employee ownership, otherwise known as overhang

Fully diluted overhang is the most common metric used by private companies

Employee Level

Median Ownership by Level of Invested Capital

Under $40M $40M to $80M Over $80M

Total Employee Ownership 16.0% 10.6% 11.2%

Executives (VPs and above) 13.0% 8.2% 8.7%

All Other Employees 2.5% 2.0% 2.0%

Total 20.1% 15.2% 13.4%

Source: Radford’s Pre-IPO/Venture-Backed Survey.

RadfordProprietary & Confidential26

Equity Receipt: Public Company Practice

Broad-based ownership remains common in the medical device industry so long as companies can manage dilution

Employee Level

Annual Equity Receipt RatesPublic MA East Coast

CEO 92% 83% 88%

VP 90% 93% 87%

Director (M4-M5) 84% 72% 82%

Manager (M2-M3) 42% 38% 55%

Supervisor (M1) 10% 13% 13%

Expert (P5-P6) 33% 15% 33%

Career (P3-P4) 14% 12% 19%

Entry (P1-P2) 4% 8% 8%

Support (All) 3% 1% 1%

Source: Radford Custom Global Long Term Incentive Reports for medical device and diagnostics companies.

RadfordProprietary & Confidential27

Equity Value: Public Company Practice

Equity values are heavily concentrated at the executive level, with values diminishing toward the lower levels of the organization

Massachusetts companies stand out with higher annual equity values over the overall East Coast, especially at the top levels of the organization

Employee Level

Annual Equity ValuePublic MA East Coast

CEO $2,040.3 $2,286.8 $1,657.6

VP $97.8 $152.9 $117.3

Director (M4-M5) $35.7 $57.7 $53.3

Manager (M2-M3) $16.2 $13.2 $13.3

Supervisor (M1) $10.1 $5.2 $5.0

Expert (P5-P6) $25.2 $26.6 $19.9

Career (P3-P4) $11.7 $6.5 $6.9

Entry (P1-P2) $7.2 $4.3 $4.3

Support (All) $6.7 $1.3 $1.3

Source: Radford Custom Global Long Term Incentive Reports for medical device and diagnostics companies.

RadfordProprietary & Confidential28

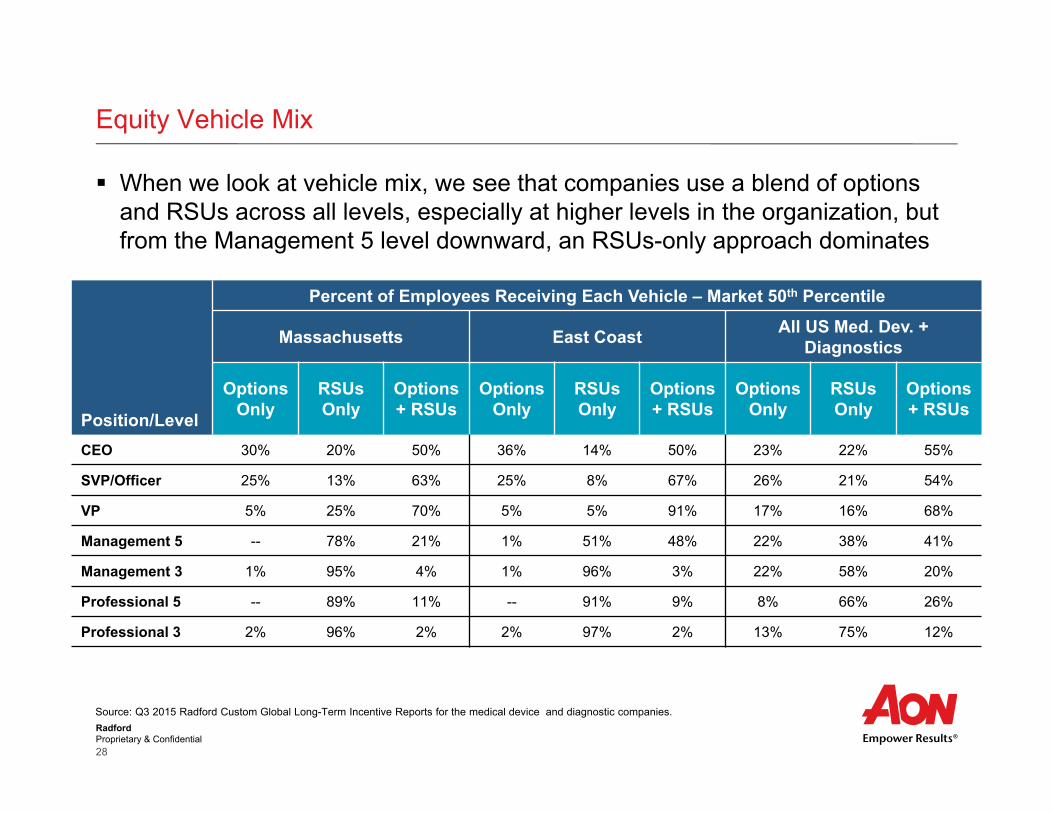

Equity Vehicle Mix

When we look at vehicle mix, we see that companies use a blend of options and RSUs across all levels, especially at higher levels in the organization, but from the Management 5 level downward, an RSUs-only approach dominates

Source: Q3 2015 Radford Custom Global Long-Term Incentive Reports for the medical device and diagnostic companies.

Position/Level

Percent of Employees Receiving Each Vehicle – Market 50th Percentile

Massachusetts East Coast All US Med. Dev. + Diagnostics

Options Only

RSUs Only

Options + RSUs

Options Only

RSUs Only

Options + RSUs

Options Only

RSUs Only

Options + RSUs

CEO 30% 20% 50% 36% 14% 50% 23% 22% 55%

SVP/Officer 25% 13% 63% 25% 8% 67% 26% 21% 54%

VP 5% 25% 70% 5% 5% 91% 17% 16% 68%

Management 5 -- 78% 21% 1% 51% 48% 22% 38% 41%

Management 3 1% 95% 4% 1% 96% 3% 22% 58% 20%

Professional 5 -- 89% 11% -- 91% 9% 8% 66% 26%

Professional 3 2% 96% 2% 2% 97% 2% 13% 75% 12%

RadfordProprietary & Confidential29

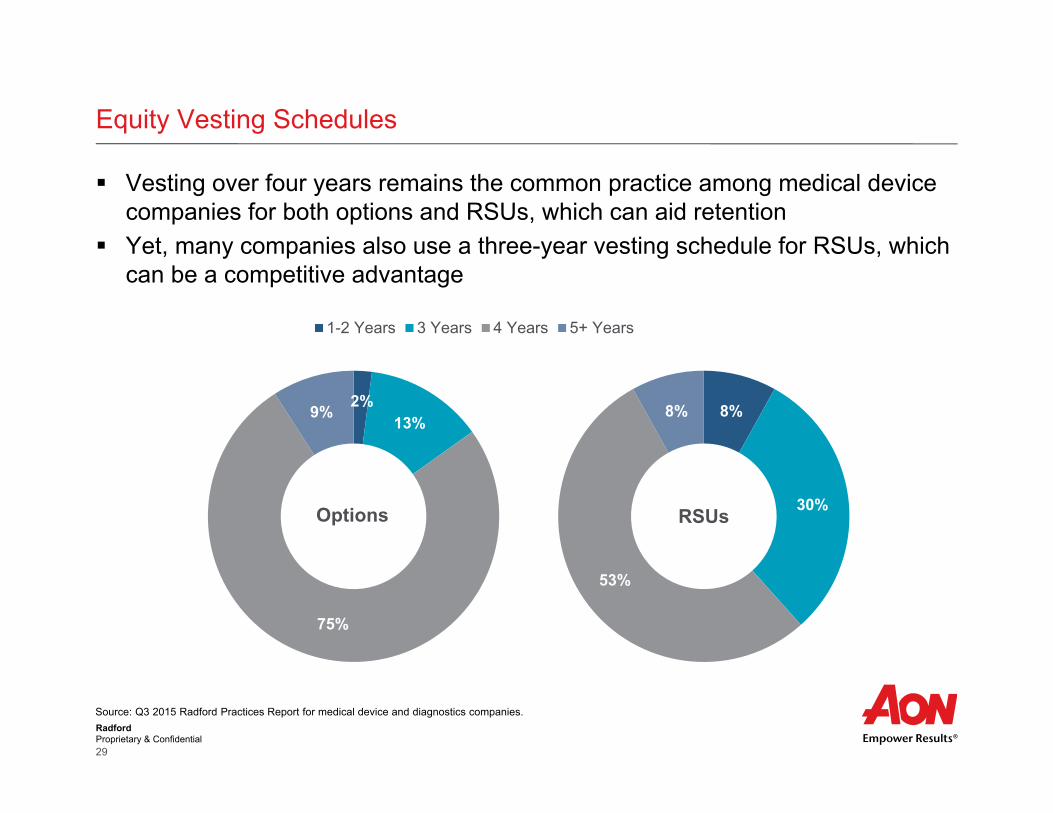

Equity Vesting Schedules

Vesting over four years remains the common practice among medical device companies for both options and RSUs, which can aid retention

Yet, many companies also use a three-year vesting schedule for RSUs, which can be a competitive advantage

8%

30%

53%

8%

RSUs

2%13%

75%

9%

Options

1-2 Years 3 Years 4 Years 5+ Years

Source: Q3 2015 Radford Practices Report for medical device and diagnostics companies.

RadfordProprietary & Confidential30

Burn Rates in the Medical Device Industry

Median last fiscal year (LFY) and 3-year gross burn rates are similar across the full US medical device industry

Relative to the East Coast and overall US medical device industry, Massachusetts medical device companies use the most equity

1.8%2.1%

3.2% 3.3%

4.4%4.9%

0%

1%

2%

3%

4%

5%

6%

LFY 3-Year Average

Gross Equity Burn Rate 25th 50th 75th

4.0%

3.2% 3.2%

0%

1%

2%

3%

4%

5%

Massachusetts East Coast All US Med. Dev +Diagnostics

Median LFY Burn Rate by Industry

Source: Radford proprietary database.

RadfordProprietary & Confidential31

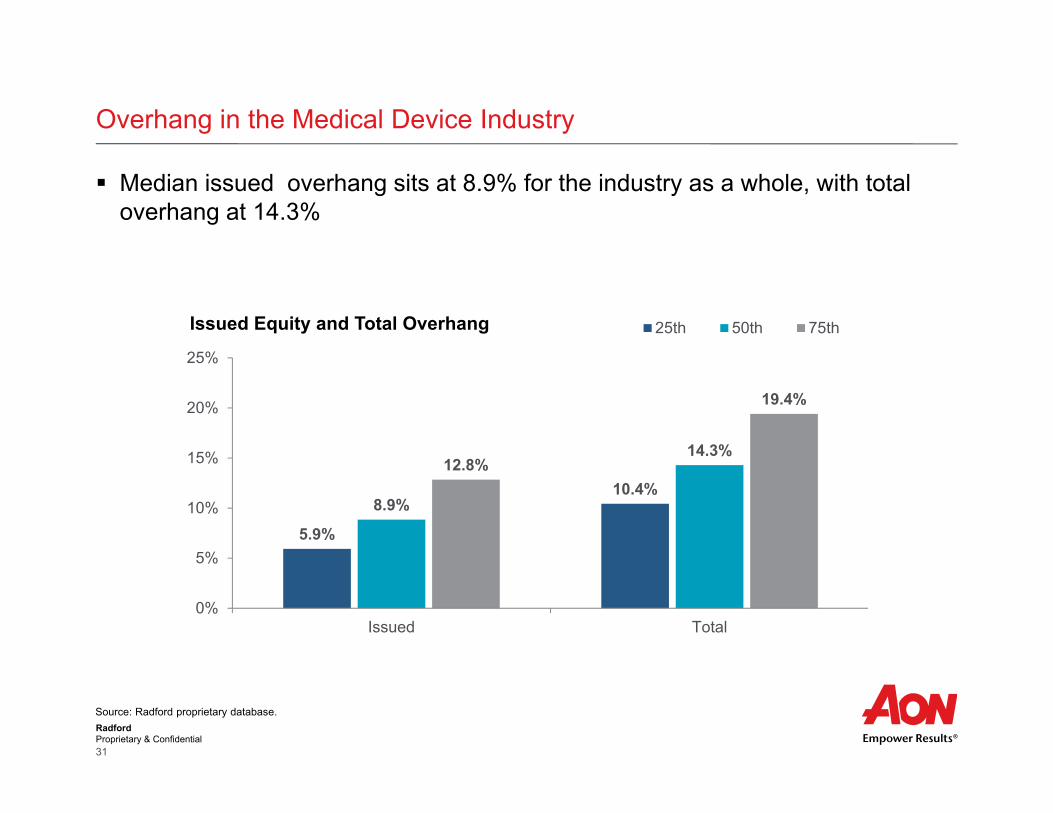

Overhang in the Medical Device Industry

Median issued overhang sits at 8.9% for the industry as a whole, with total overhang at 14.3%

5.9%

10.4%8.9%

14.3%12.8%

19.4%

0%

5%

10%

15%

20%

25%

Issued Total

Issued Equity and Total Overhang 25th 50th 75th

Source: Radford proprietary database.

RadfordProprietary & Confidential32

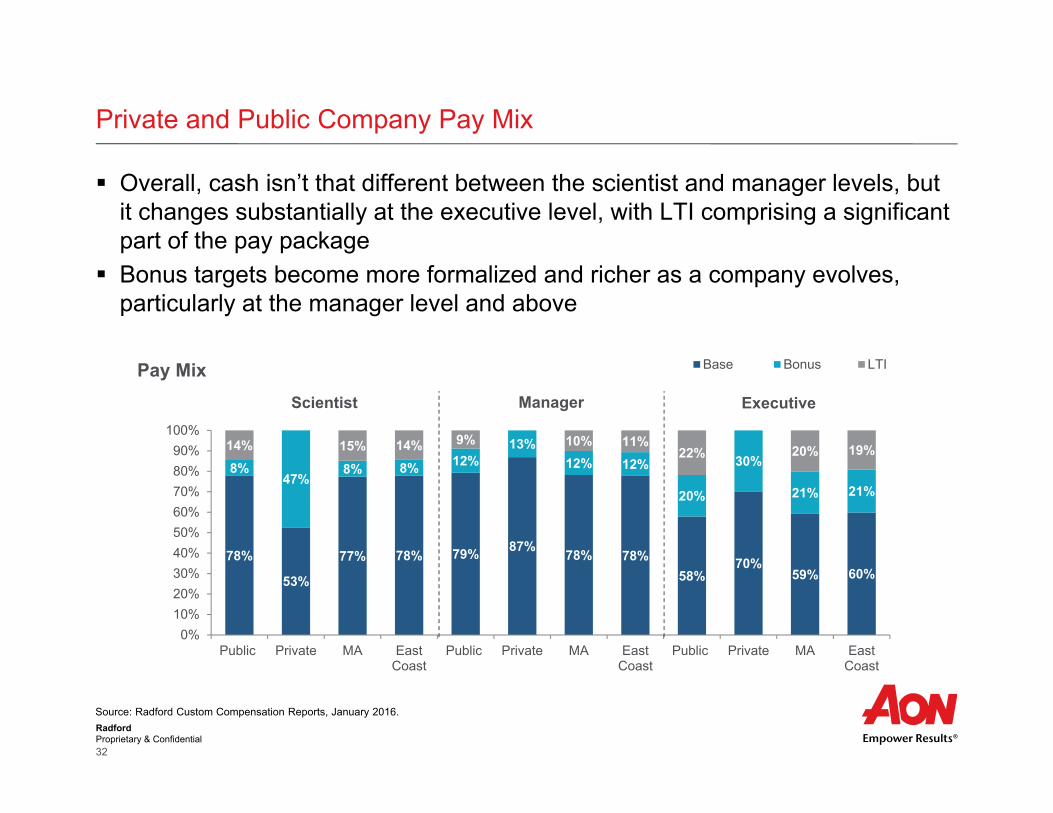

Private and Public Company Pay Mix

Overall, cash isn’t that different between the scientist and manager levels, but it changes substantially at the executive level, with LTI comprising a significant part of the pay package

Bonus targets become more formalized and richer as a company evolves, particularly at the manager level and above

Source: Radford Custom Compensation Reports, January 2016.

78%

53%

77% 78% 79% 87% 78% 78%58%

70%59% 60%

8%47%

8% 8% 12%13%

12% 12%

20%

30%

21% 21%

14% 15% 14% 9% 10% 11%22% 20% 19%

0%10%20%30%40%50%60%70%80%90%

100%

Public Private MA EastCoast

Public Private MA EastCoast

Public Private MA EastCoast

Pay Mix Base Bonus LTI

ExecutiveManagerScientist

RadfordProprietary & Confidential33

Executive Compensation

Unlike broad-based employees, executives are still willing to take a discount on cash for higher ownership

As companies move from private to public and become more established, CEO pay shifts: fixed pay typically gets higher, and long-term incentive values at the executive level become more meaningful as the company gains traction and as market capitalization values increase

Source: Radford Pre-IPO Venture-Backed Survey, Radford Custom Compensation Reports, January 2016.

CEO Public Private MA East Coast

Base Salary $604,135 $350,000 $600,000 $600,000

Target Total Cash $1,126,250 $412,250 $1,200,000 $1,175,000

Annual LTI Value $2,040,278 -- $2,792,350 $2,107,661

RadfordProprietary & Confidential34

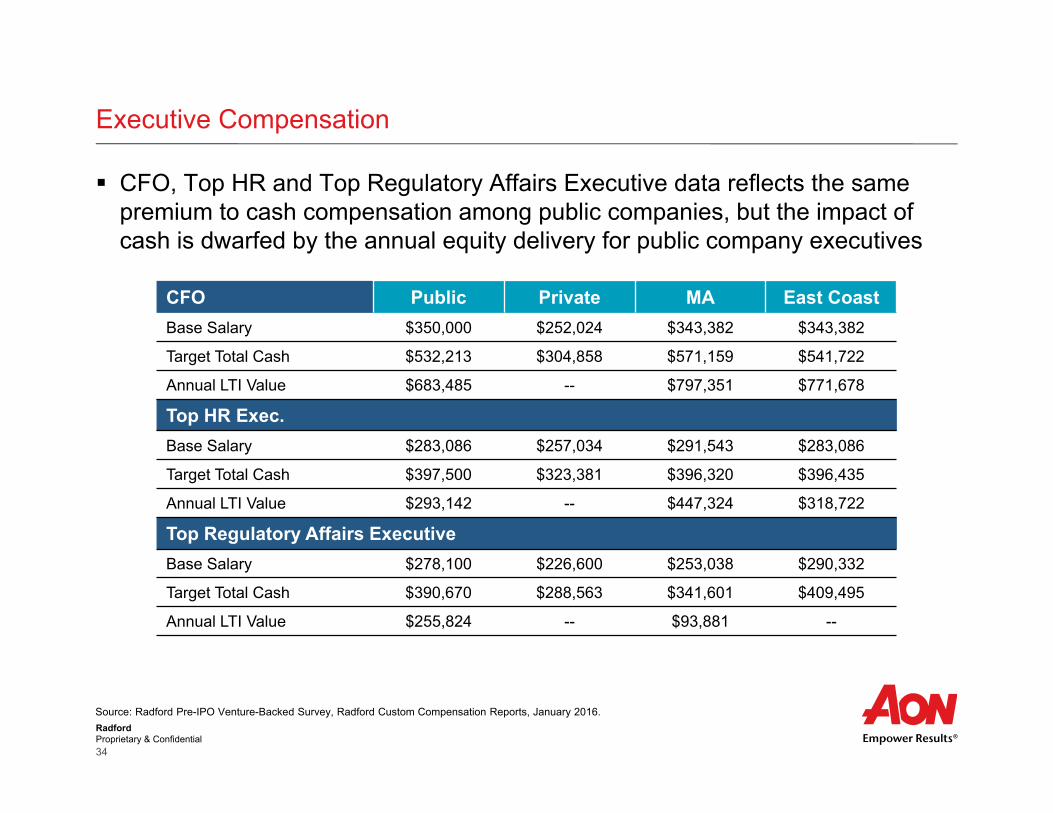

Executive Compensation

CFO, Top HR and Top Regulatory Affairs Executive data reflects the same premium to cash compensation among public companies, but the impact of cash is dwarfed by the annual equity delivery for public company executives

Source: Radford Pre-IPO Venture-Backed Survey, Radford Custom Compensation Reports, January 2016.

CFO Public Private MA East CoastBase Salary $350,000 $252,024 $343,382 $343,382

Target Total Cash $532,213 $304,858 $571,159 $541,722

Annual LTI Value $683,485 -- $797,351 $771,678

Top HR Exec.Base Salary $283,086 $257,034 $291,543 $283,086

Target Total Cash $397,500 $323,381 $396,320 $396,435

Annual LTI Value $293,142 -- $447,324 $318,722

Top Regulatory Affairs ExecutiveBase Salary $278,100 $226,600 $253,038 $290,332

Target Total Cash $390,670 $288,563 $341,601 $409,495

Annual LTI Value $255,824 -- $93,881 --

RadfordProprietary & Confidential35

Medical Device Professional IC Compensation

Source: Radford Pre-IPO Venture-Backed Survey, Radford Custom Compensation Reports, January 2016.

Development Engineer 4 Public Private MA East Coast

Base Salary $123,978 $90,140 $109,847 $109,847

Target Total Cash $140,369 $98,730 $119,732 $119,732

Annual LTI Value $70,166 -- $5,991 --

Scientist 3Base Salary $96,999 $105,000 $101,436 $97,344

Target Total Cash $105,600 $110,549 $112,750 $107,842

Annual LTI Value $18,040 -- $19,480 $18,040

At the Development Engineer 4 position, we see public companies stand out with high annual LTI values

For the Scientist 3 position, base pay is higher at private companies, and total target cash is considerably higher among companies located in Massachusetts

RadfordProprietary & Confidential36

Executive Compensation and Governance Trends

RadfordProprietary & Confidential37

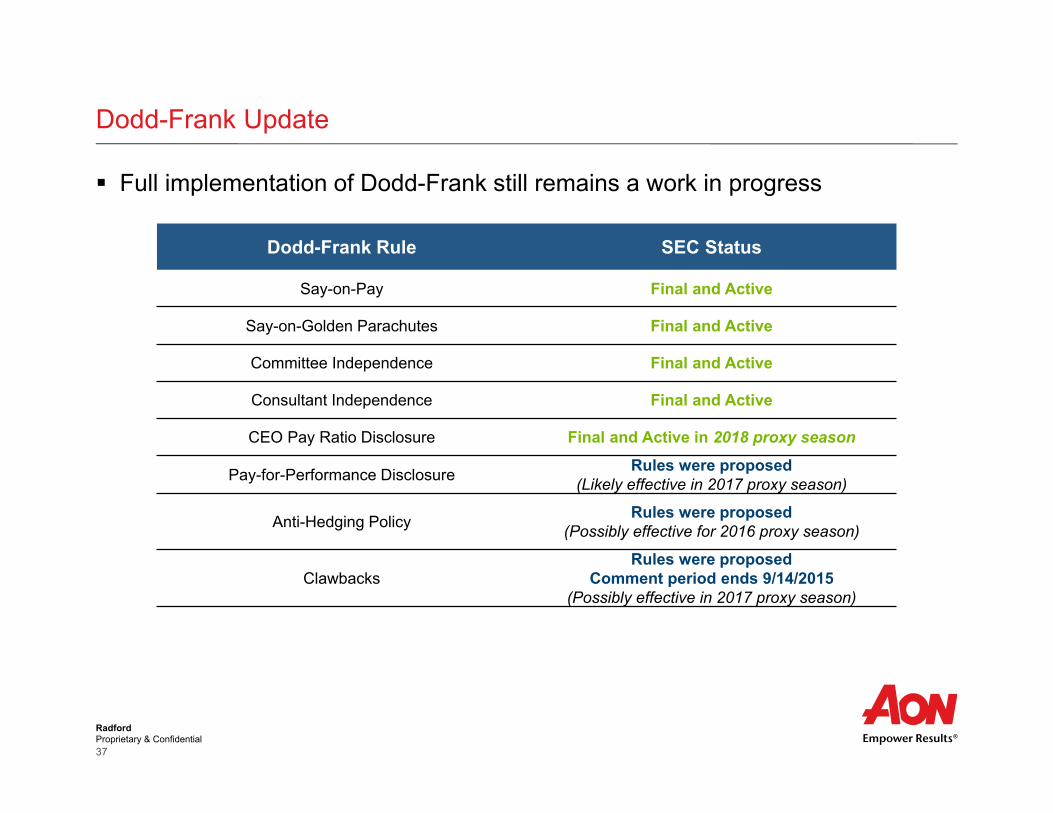

Full implementation of Dodd-Frank still remains a work in progress

Dodd-Frank Update

Dodd-Frank Rule SEC Status

Say-on-Pay Final and Active

Say-on-Golden Parachutes Final and Active

Committee Independence Final and Active

Consultant Independence Final and Active

CEO Pay Ratio Disclosure Final and Active in 2018 proxy season

Pay-for-Performance Disclosure Rules were proposed(Likely effective in 2017 proxy season)

Anti-Hedging Policy Rules were proposed(Possibly effective for 2016 proxy season)

ClawbacksRules were proposed

Comment period ends 9/14/2015(Possibly effective in 2017 proxy season)

RadfordProprietary & Confidential38

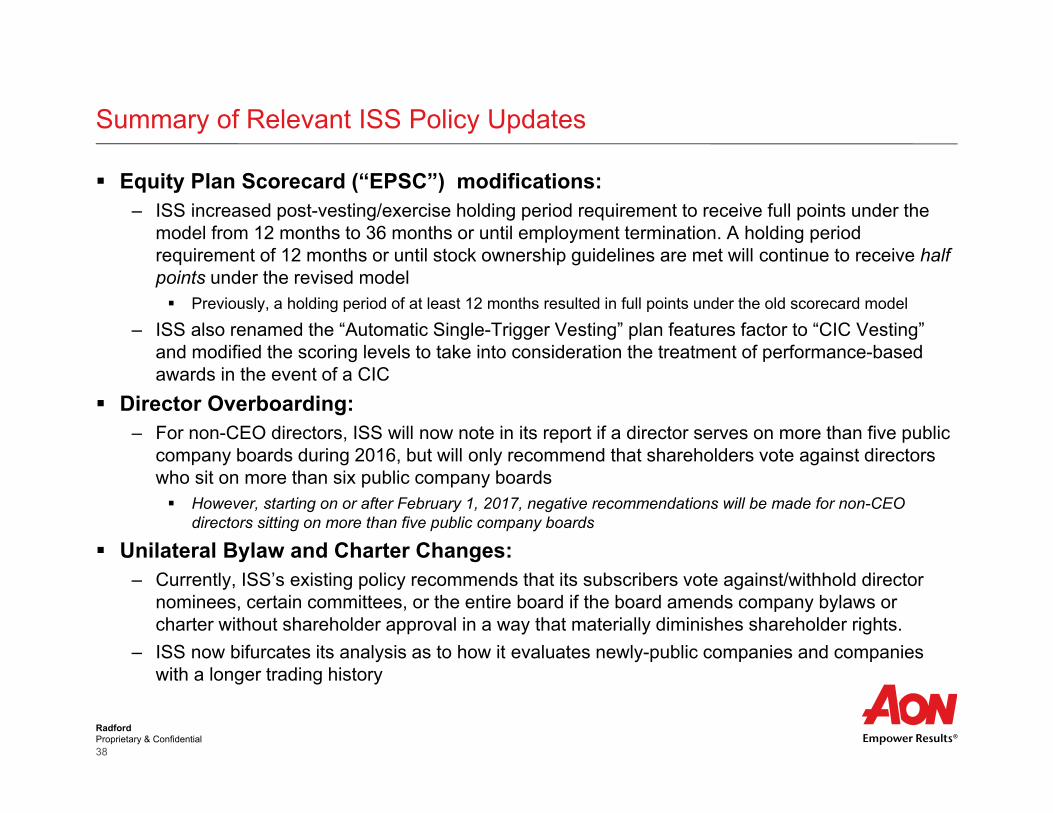

Equity Plan Scorecard (“EPSC”) modifications:– ISS increased post-vesting/exercise holding period requirement to receive full points under the

model from 12 months to 36 months or until employment termination. A holding period requirement of 12 months or until stock ownership guidelines are met will continue to receive half points under the revised model Previously, a holding period of at least 12 months resulted in full points under the old scorecard model

– ISS also renamed the “Automatic Single-Trigger Vesting” plan features factor to “CIC Vesting” and modified the scoring levels to take into consideration the treatment of performance-based awards in the event of a CIC

Director Overboarding:– For non-CEO directors, ISS will now note in its report if a director serves on more than five public

company boards during 2016, but will only recommend that shareholders vote against directors who sit on more than six public company boards However, starting on or after February 1, 2017, negative recommendations will be made for non-CEO

directors sitting on more than five public company boards

Unilateral Bylaw and Charter Changes:– Currently, ISS’s existing policy recommends that its subscribers vote against/withhold director

nominees, certain committees, or the entire board if the board amends company bylaws or charter without shareholder approval in a way that materially diminishes shareholder rights.

– ISS now bifurcates its analysis as to how it evaluates newly-public companies and companies with a longer trading history

Summary of Relevant ISS Policy Updates

RadfordProprietary & Confidential39

Possibly effective for proxy season 2016

Take Action: disclose whether your company permits employees (including officers) or directors to engage in hedging activities with respect to shares granted as part of compensation, as well as shares held directly or indirectly

– If some hedging activity is permitted, identify the categories of persons permitted to engage in hedging activities as well as the types of hedging activities that are permitted (or not permitted)

– Technically, these disclosures are required under Item 407 (Corporate Governance), and we would expect companies to provide this disclosure outside the CD&A Since hedging is one of the SEC’s “15 items” to be covered in the CD&A, the proposed rule

would allow companies to reference the Item 407 disclosure within the CD&A

Anti-Pledging

RadfordProprietary & Confidential40

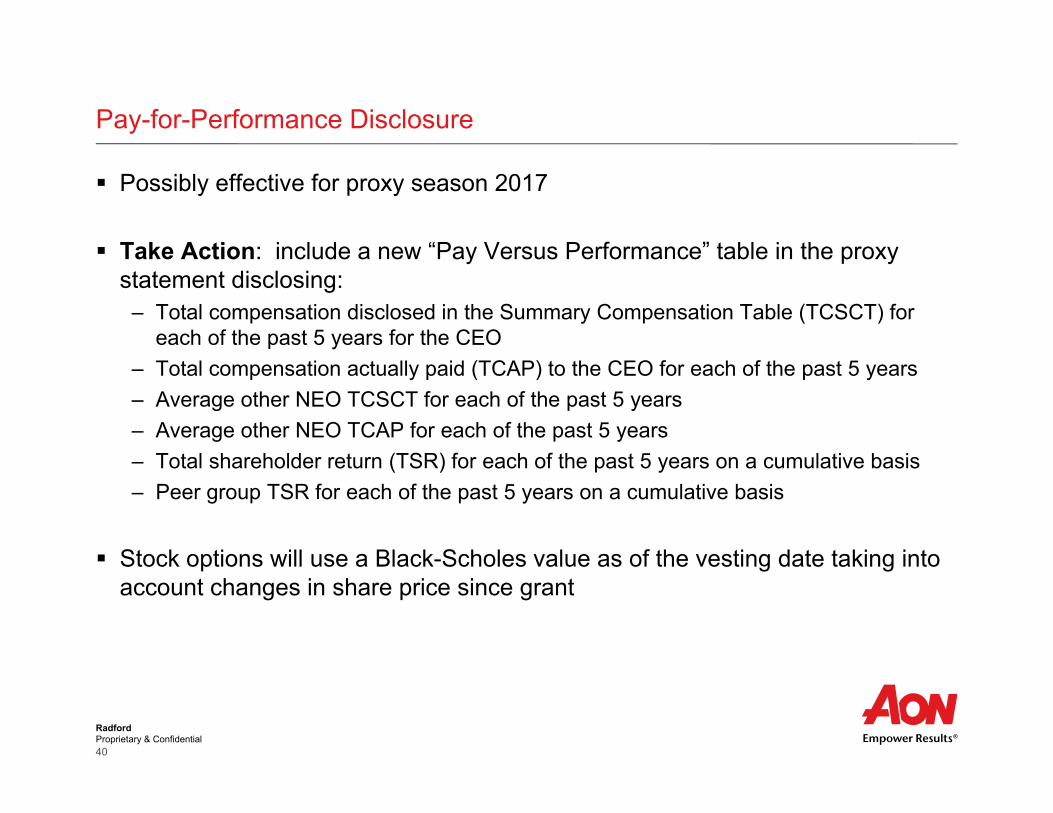

Possibly effective for proxy season 2017

Take Action: include a new “Pay Versus Performance” table in the proxy statement disclosing:

– Total compensation disclosed in the Summary Compensation Table (TCSCT) for each of the past 5 years for the CEO

– Total compensation actually paid (TCAP) to the CEO for each of the past 5 years– Average other NEO TCSCT for each of the past 5 years– Average other NEO TCAP for each of the past 5 years– Total shareholder return (TSR) for each of the past 5 years on a cumulative basis– Peer group TSR for each of the past 5 years on a cumulative basis

Stock options will use a Black-Scholes value as of the vesting date taking into account changes in share price since grant

Pay-for-Performance Disclosure

RadfordProprietary & Confidential41

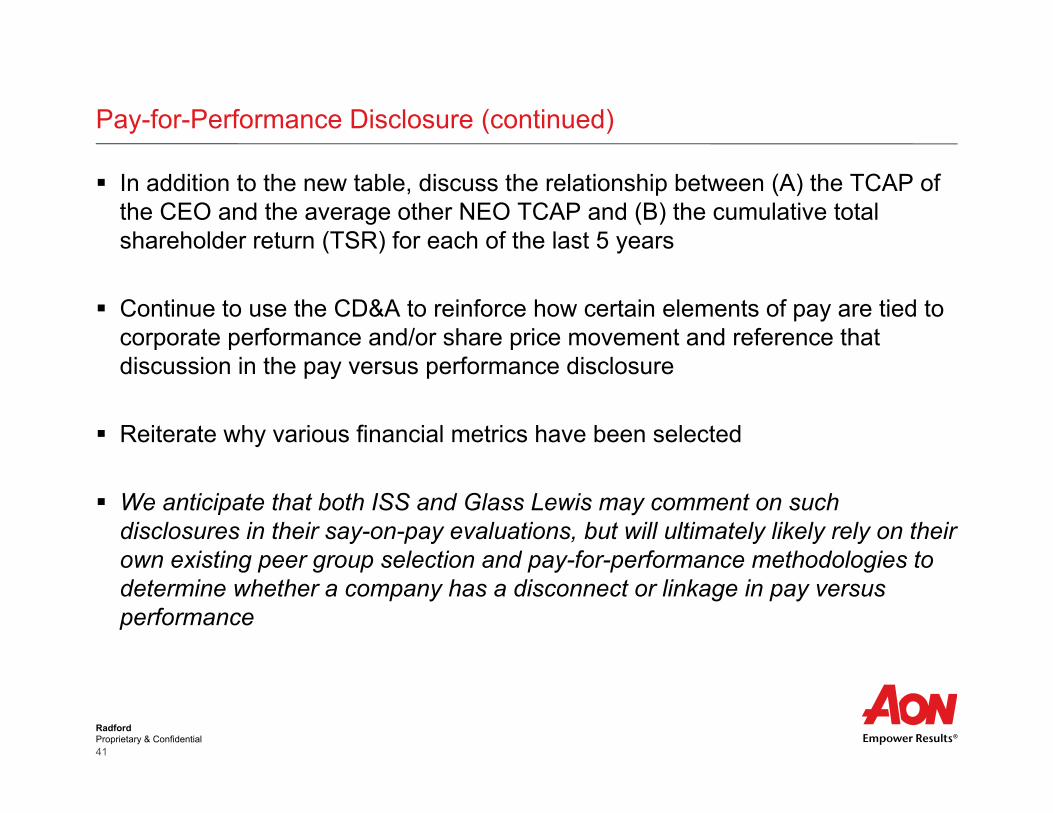

In addition to the new table, discuss the relationship between (A) the TCAP of the CEO and the average other NEO TCAP and (B) the cumulative total shareholder return (TSR) for each of the last 5 years

Continue to use the CD&A to reinforce how certain elements of pay are tied to corporate performance and/or share price movement and reference that discussion in the pay versus performance disclosure

Reiterate why various financial metrics have been selected

We anticipate that both ISS and Glass Lewis may comment on such disclosures in their say-on-pay evaluations, but will ultimately likely rely on their own existing peer group selection and pay-for-performance methodologies to determine whether a company has a disconnect or linkage in pay versus performance

Pay-for-Performance Disclosure (continued)

RadfordProprietary & Confidential42

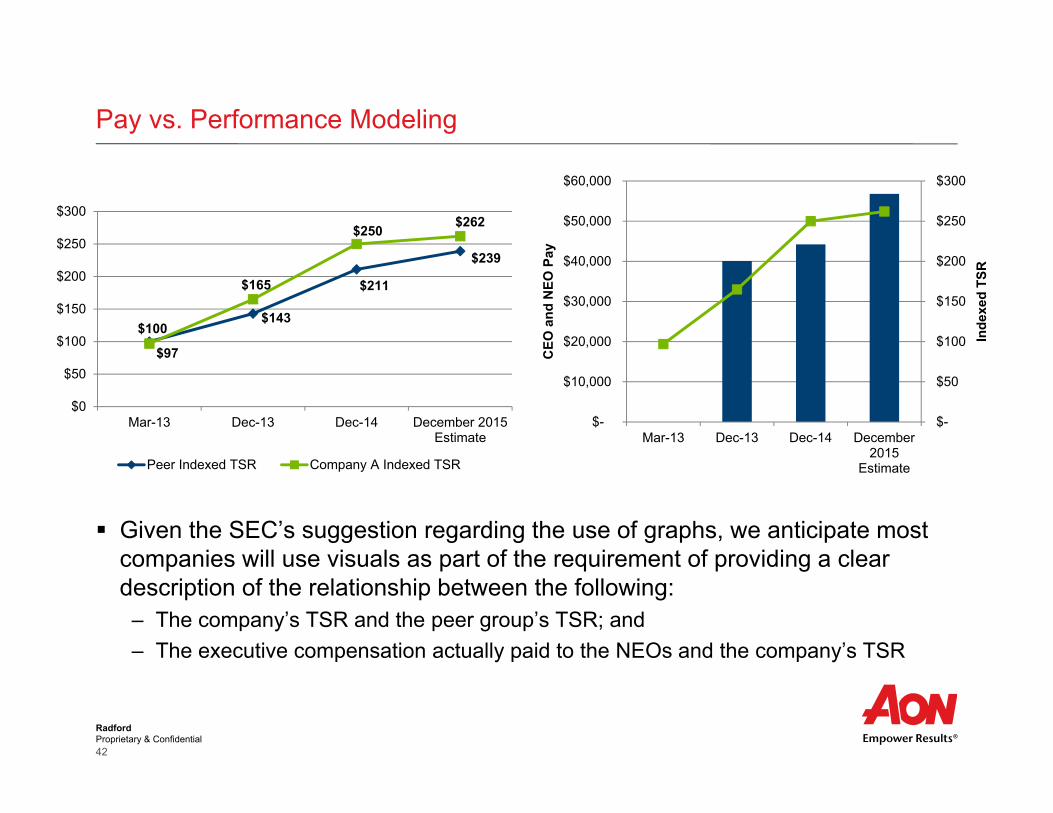

Given the SEC’s suggestion regarding the use of graphs, we anticipate most companies will use visuals as part of the requirement of providing a clear description of the relationship between the following:

– The company’s TSR and the peer group’s TSR; and – The executive compensation actually paid to the NEOs and the company’s TSR

Pay vs. Performance Modeling

$100 $143

$211

$239

$97

$165

$250 $262

$0

$50

$100

$150

$200

$250

$300

Mar-13 Dec-13 Dec-14 December 2015Estimate

Peer Indexed TSR Company A Indexed TSR

$-

$50

$100

$150

$200

$250

$300

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

Mar-13 Dec-13 Dec-14 December2015

Estimate

Inde

xed

TSR

CEO

and

NEO

Pay

RadfordProprietary & Confidential43

When will the clawback be triggered?– In event of a restatement without any requirement of misconduct or negligence of executives from

whom compensation is being recovered Applies to restatements compelled by error that is material to previously issued financial statements

From whom must compensation be recovered?– All executive officers with a policy-making role; anyone who met the definition of an executive

officer at any point during the incentive compensation’s performance period

What types of compensation are subject to the policy?– All incentive-based compensation, whether short-term or long-term– Based on any financial reporting measure or stock price/TSR– Equity awards are subject to clawback only to the extent the grant, vesting, or the amount of the

award earned is affected by the restated measure or related impact on stock or TSR– Time-based stock options and restricted stock are not incentive compensation subject to

clawback

Board discretion– No board discretion – recovery is compulsory, with the “excess” incentive compensation to be

recovered pro rata from all executive based on their share of the original overstated award

Clawback Overview

RadfordProprietary & Confidential44

We do not expect the policy to become effective earlier than the 2017 proxy season

Under the proposed rules, the listing exchanges must add a listing requirement for companies to adopt a clawback policy that minimally conforms to the SEC’s requirements:

– Clawback is triggered in the event of a restatement due to material non-compliance with GAAP reporting requirements (“no fault”)

– From the date the company is aware or should be aware that a restatement will be required, the company must look back to the 3 most recently completed fiscal years

– If the financial restatement affects the amounts originally determined to be earned under incentive pay programs, the company must clawback the excess compensation

– It is important to note that for life sciences companies, clinical / scientific milestones are not considered financial metrics and therefore plans or portions of plans related to these types of metrics cannot be subject to recoupment

Clawbacks

RadfordProprietary & Confidential45

The effective date for the CEO pay ratio is for fiscal years that begin on or after January 1, 2017 (for calendar-year filers, that would mean the first disclosure would occur in the 2018 proxy season)

Identifying the median employee is only required once every 3 years (provided the employee population has not changed in a way that would significantly affect the ratio (e.g., corporate mergers and acquisitions)

Median Employee can be identified using the employee population as of any date during the last 3 months of the fiscal year

– This includes any full-time, part-time, seasonal, or temporary worker employed by the registrant or any of its consolidated subsidiaries on that day

Nondiscriminatory benefit plans can be added to the numerator and denominator of the ratio

Optional narrative and supplemental ratios are permitted to provide helpful context

CEO Pay Ratio Rule

RadfordProprietary & Confidential46

Determining the CEO to worker pay ratio isn’t so simple…

The SEC has set forth several operational guidelines for determining the median employee, though companies must be sure to disclose and consistently apply the methodology of their choosing

CEO Pay Ratio Modeling

Median Employee Selection Methodology

Base Total Target Cash

Target Total Direct

Compensation

W-2(or int’l equiv.)

Wages

Median Employee Total Pay $95,000 $85,000 $100,000 $90,000

CEO Summary Comp Table Pay $10,500,000 $10,500,000 $10,500,000 $10,500,000

2015 Pay Ratio 11:1 12:1 11:1 12:1

RadfordProprietary & Confidential47

The final rules retained several operational guidelines that give employers flexibility

– Registrants may use (A) a methodology that uses reasonable estimates to identify the median and (B) reasonable estimates to calculate the annual total compensation or any elements of total compensation

– In determining the employees from which the median is identified, a registrant may use (A) its entire employee population or (B) statistical sampling or other reasonable methods

– A registrant may identify the median employee using (A) annual total compensation or (B) any other compensation measure that is consistently applied to all employees included in the calculation, such as amounts derived from the registrant’s payroll or tax records

– A registrant may annualize the total compensation for all permanent employees (other than those in temporary or seasonal positions) that were employed by the registrant for less than the full fiscal year

CEO Pay Ratio Rule

RadfordProprietary & Confidential48

Recently, we have seen increased scrutiny around director compensation, especially on equity awards

Because director compensation is typically set by the Compensation Committee, who also receives the compensation, some are alleging that the compensation constitutes a breach of fiduciary duty

A number of publicly traded companies have recently faced legal action around director compensation, causing many to consider implementing a concrete and meaningful limitation on grants to directors to be included in an equity plan and approved by shareholders

Companies should consider including a hard coded limit on annual equity awards to directors in the text of the next amendment to their plan; alternatively, a standalone policy could be put forth to shareholders for approval

Board of Director Compensation Litigation