comparing the current crisis to the great depression · causes, changes necessary to prevent...

TRANSCRIPT

Karl Aiginger

Comparing the Current Crisis to the

Great Depression

OECD - Nero ConferenceParis, September 21, 2009

H:user/aig/vortrag/OECD_crises_210909_short.ppt

1 23.09.2009

Great Depression (GD)

vs. Current Crisis (CC)

Comparison of the two crises with regard to two aspects

depth and length

policy reactions

Non goals:

causes, changes necessary to prevent further crises;

long-run effects on economic growth;

exit strategies;

missed chances, lessons forgotten;

regulatory changes, incentives, behavior.

2 23.09.2009

References for the other questions

Karl Aiginger: Causes, cures and consequences, WIFO WP No 341http://www.wifo.ac.at/aiginger/crisis/

Karl Aiginger: Strengthening the resilience, WIFO WP No 338(forthcoming in Intereconomics, October 2009) http://www.wifo.ac.at/aiginger/resilience/

Bernanke (2004), Eichengreen - O’Rourke (2009), Friedman-Schwartz (1963), Galbraith (1954), Hahn (2008), Kindleberger (1986), Krugman (2009), Mooslechner (2008), Romer (1991), Schulmeister (2009), Sim (2009), Tichy (2008), etc.

The understanding of the causes of the crisis is increasing –if not the weight for the individual reasons.

3 23.09.2009

Triggers, causes, amplifiers

Triggers: subprime loans (for the lingering phase)Lehman Brothers (for the showdown phase)

Causes:

Macroeconomic causes Surpluses and deficits, monetary policy US 2002ff

Inflated expectations about returns, asset prices

Shift from real economy to financial sector,

Microeconomic causes Short termism and overleveraging

Financial innovations: originate to distribute

Regulatory lenience and regulatory failure Belief in self regulation, circumvention of regulation

Competition policy uncritical merger, too big to fail,

Neglect of systemic risks,

Pro cyclicality of Basel 2 and accounting rules

Amplifiers: weakness in coordination, income distribution

Shortages food, raw materials, energy (bubbles, speculation).

4 23.09.2009

Motivation of the research questions

Some authors claim (Eichengreen – O’Rourke) that this crisis had been “as severe or stronger”

Whether policy made the difference and how policy should continue (2010/11)

Finally to learn whether further declines (“steps”) are probably in the short term; phases of hopes/despair.

5 23.09.2009

Methodology and data

Assumption: crisis is currently leveling off (as it looks for production in 09/09)

Methodology: own research, literature, stylized facts

Concentrating on industrialized countries

Data are incomplete, not fully comparable

Data sets are increasing daily

Project: WIFO Long-term database.

6 23.09.2009

Caveats and limits

Crisis is definitely not over as far as unemploymentis concerned

Policy is unknown for 2010

Fiscal consolidation strategies, regulatory reform

History warns us that crises can continue and may come back.

7 23.09.2009

Results I: in CC drop in activity much smaller

In this crisis - if it ends in 2009 - drop in activity was much smallerthan in the Great Recession

Specifically for GDP, employment, less for manufacturing, exports;for world output, industrialized countries, US, France, Germany

The drop in GDP and manufacturing is more synchronized;the Great Depression had two epicenters: Germany, Austria and USA

High growth in build-up period, GD volatile, CC smooth

Deflationary background and overcapacities in GD, scarcities of food, raw materials, energy in CC (incl. speculation).

8 23.09.2009

Results on depth in a nutshell: depth

1932/1929 vs. 2009

Great Depression Current Crisis

GDP - 10 % - 2 % (- 5%)

Manufacturing - 30 % -17 % (-19%)

Exports- 43 % - 18% (-30%)

Stock markets - 69 % - 48% (+33%)

Employment - 16 % - 3% (- 2%)

Unemployment 15 % (1932) 8% (2010)

Unemployment change + 12 PP + 3 PP (2010-2008)

Inflation - 14 % 0.5%

Data for world if existent, for subsets of mainly large industrial countries (GDP weighted) otherwise (in parenthesis quarterly data).

9 23.09.2009

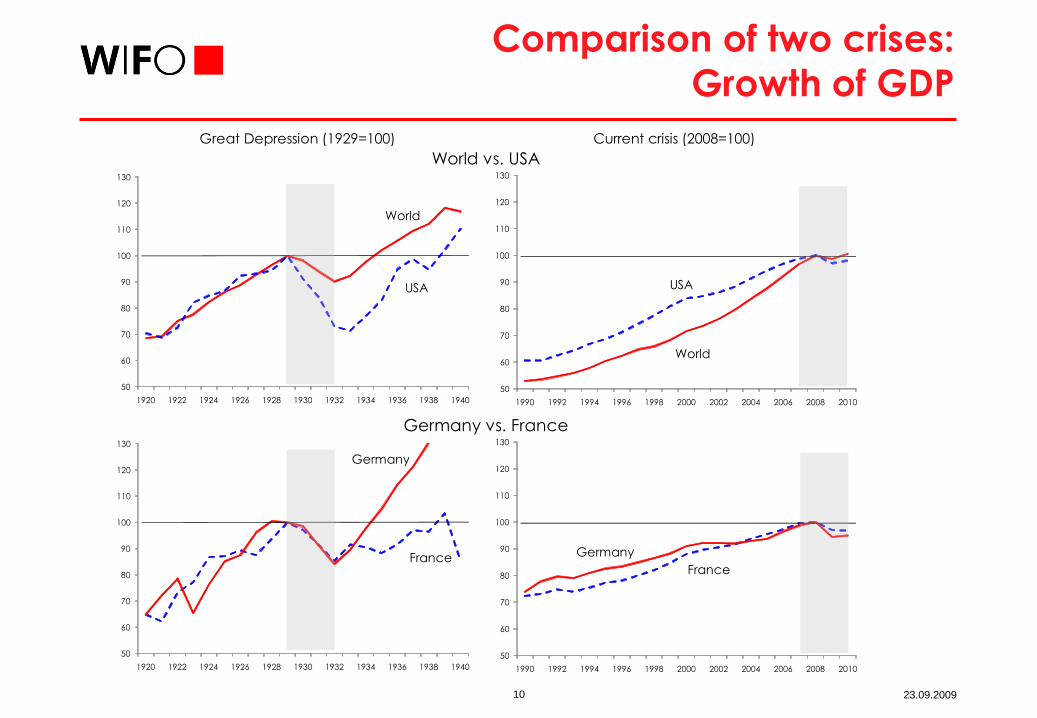

Comparison of two crises:

Growth of GDP

1929/1921 1932/1929 2008/2000

2009

forecast

Trough 2009/

peak 2008

Quarterly data

Austria 43.0 -19.8 17.3 -3.4 -4.4 1)

Germany 38.4 -15.8 9.8 -5.4 -6.7 2)

Belgium 33.4 -7.1 15.6 -3.5 -3.8 1)

Spain 34.2 -3.8 27.9 -3.2 -4.2 3)

France 61.0 -14.7 13.6 -3.0 -3.4 2)

Finland 55.7 -4.0 25.1 -4.7 -6.0 2)

Sweden 49.2 -4.3 20.9 -4.0 -6.4 3)

United Kingdom 28.5 -5.1 19.5 -3.8 -5.7 3)

USA 45.4 -27.0 19.0 -2.9 -3.9 1)

Japan 22.0 1.3 10.7 -5.3 -8.3 3)

World 44.7 -9.8 39.8 -1.3 -4.6 4)

Unweighted average over countries 41.1 -10.0 17.9 -3.9 -5.3

Standard deviation 12.2 8.9 5.8 0.9 1.6

Coefficient of variation 0.297 -0.886 0.325 -0.234 -0.301

Great Depression (1932) Current crisis (2007ff)

Annual data

Percentage change

Annual data

10 23.09.2009

Comparison of two crises:

Growth of GDP

1408.89715

1408.89715

Great Depression (1929=100) Current crisis (2008=100)

World vs. USA

Germany vs. France

50

60

70

80

90

100

110

120

130

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

World

USA

50

60

70

80

90

100

110

120

130

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

World

USA

50

60

70

80

90

100

110

120

130

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

France

Germany

50

60

70

80

90

100

110

120

130

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

France

Germany

11 23.09.2009

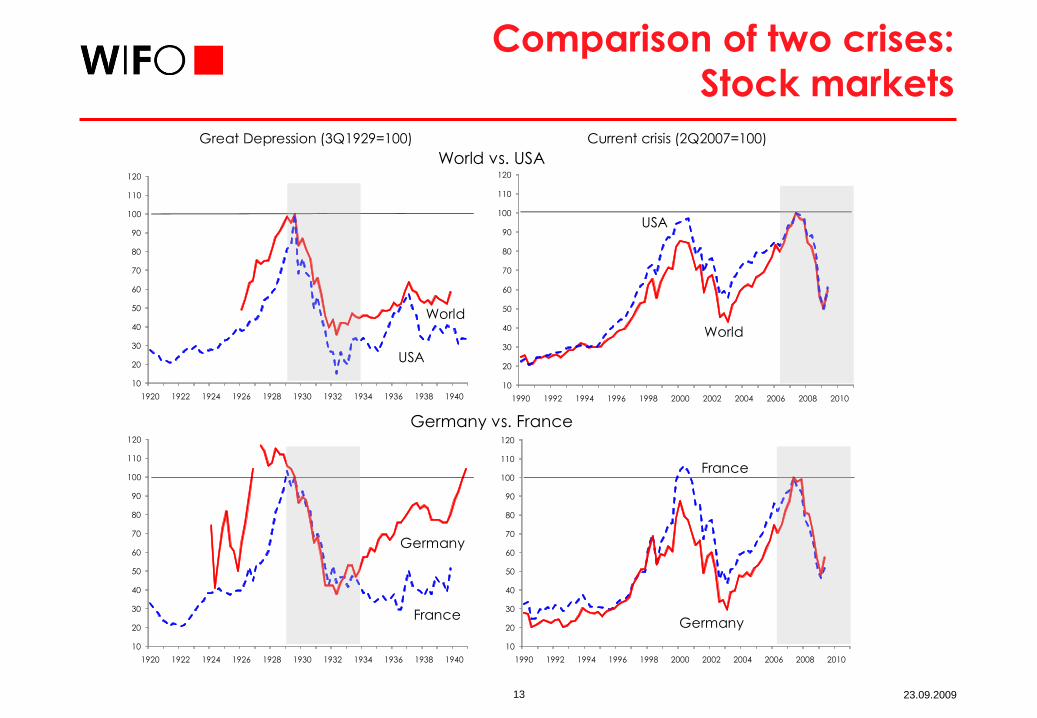

Results II: Stock market decline smaller in

CC, rebound definitely larger

GD: steep fall at the start, long recovery

70% (GDP weighted), US -84% (1929/1932)

CC: steepest part 08/2008 to 03/2009

Overall decline much smaller (44% vs. 69%; 4 big indices)

Rebound up to 33% (weighted), 45% unweighted (monthly)

Largest rebound in GD: +13% in world, 16% in US in 11/1929

Outsider Japan: now steeper than in GD (in Austria, too)

Steeper decline (than in GD) from 08/2008 to 03/2009Proportionate decline now for given period (17 month) smaller (Contrary to Eichengreen who started graphs in April 1929).

12 23.09.2009

Comparison of two crises:

Stock markets

Peak 1929/

trough 1921

Trough 1932/

peak 1929

Peak 2007/

trough 2003

Trough 2008/

peak 2007

August 2009/

trough 2009

Austria -45.6 318.6 -65.2 69.0

Germany -83.9 -62.1 237.7 -51.7 44.7

Belgium

Spain

France 335.3 -56.2 131.2 -53.6 36.7

Finland

Sweden

United Kingdom -49.3 191.1 -44.7 45.8

USA 377.9 -84.8 78.8 -50.0 30.7

Japan -34.2 127.5 -55.3 35.7

"World" -68.9 130.1 -47.7 32.7

Unweighted average over countries 209.8 -59.6 191.5 -53.0 45.4

Standard deviation 255.2 15.4 93.0 7.5 14.6

Coefficient of variation 1.217 -0.259 0.486 -0.142 0.321

Current crisis (2007ff)

Quarterly data; percentage change

Great Depression (1932)

13 23.09.2009

Comparison of two crises:

Stock markets

1408.89715

Great Depression (3Q1929=100) Current crisis (2Q2007=100)

World vs. USA

Germany vs. France

10

20

30

40

50

60

70

80

90

100

110

120

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

World

USA

10

20

30

40

50

60

70

80

90

100

110

120

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

USA

World

10

20

30

40

50

60

70

80

90

100

110

120

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Germany

France

10

20

30

40

50

60

70

80

90

100

110

120

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

France

Germany

14 23.09.2009

Results III: The decline was very steeper in

several months in the CC

Exports declined by 25% between 2Q/2008 and 1Q/2009

Manufacturing by 19% between 4Q/2007 and 2Q/2009

Starting with a comparison in some month in 2008, leaving out the lingering phase of CC (after burst of US housing and Lehmann) gave rise to message “as strong or stronger”

The Current Crisis had the potential to become a very deep and long depression.

15 23.09.2009

Results IV: Economic policy

made the difference

Recapitalization of banks, guarantees, support incl. nationalization

Monetary policy

Fiscal policy

International coordination

(Surprising) consensus of economists

Better institutions

Less protectionism – up to now.

16 23.09.2009

Result in a nutshell: policy variables

Great Depression Current Crisis

M1 -11 % (1932/1929) + 8% (2008/2007)

Discount Rates 4% (1930) 0.5 % (2009)

Budget deficit/GDP -2.5% (1932) - 9 % (2009)

There are many indicators on monetary/fiscal policy

– all show quicker, stronger reactions in CC.

17 23.09.2009

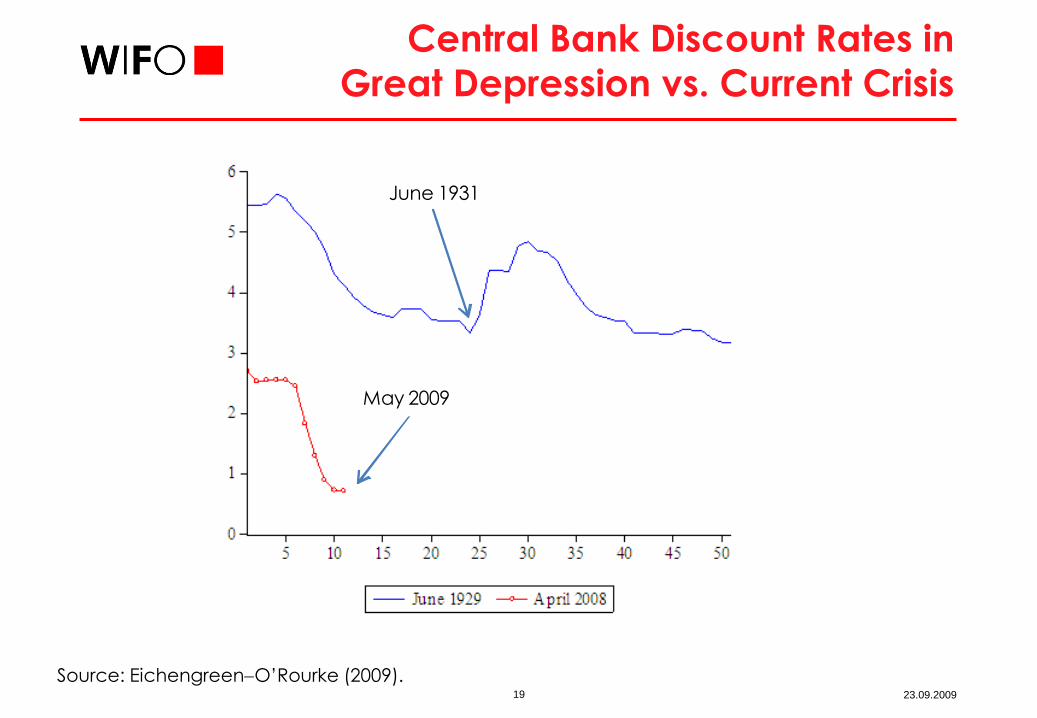

Monetary Policy

Great Depression

Increasing rate in 1928 to curb speculation

Reducing it slightly, increasing in some countries to prevent capital outflow

Asymmetric handling of gold standard

Imploding multipliers after bank runs and export decline.

18 23.09.2009

Monetary policy in GD vs. CC(Alternative)

Fed increased Rate in 1928 to curb stock market speculation

M1 flat in 1929/30 (18 countries), then -15% 1929/32

Gold standard, currency goal, asymmetric reaction

Decreasing multiplier, higher reserve requirements, bank runs and failures

Nominal discount rates reduced somewhat from 5.5 to less than 4

Deflation resulted in enormous (double digit) real rates!

Real wage increases (despite lower nominal / lower working hours)

From 1934/35 rapidly increasing M1, the more the less gold standard

Current Crisis

Discount rate 0,

Quantitative easing,

Unconventional operations.

19 23.09.2009

Central Bank Discount Rates in

Great Depression vs. Current Crisis

Source: Eichengreen-O’Rourke (2009).

June 1931

May 2009

20 23.09.2009

Comparison of two crises: inflation/

deflation (consumer prices)Great Depression (1932) Current crisis (2007ff)

1930 1931 1932 1932/1929 2008

2009

forcast

Percentage

price

change

Austria 0.0 -5.0 2.1 -3.0 3.2 1.1

Germany -4.0 -8.3 -11.4 -22.0 2.6 0.7

Belgium 1.2

Spain 1.4

France 1.0 -4.0 -9.3 -12.0 2.8 0.9

Finland 1.1

Sweden -3.6 -3.1 -1.3 -7.7 3.4 0.7

United Kingdom -4.0 -6.3 -2.2 -12.0 4.0 1.3

USA -2.9 -8.3 -10.4 -20.2 3.9 0.3

Japan -0.5

"World" 4) -2.2 -5.8 -6.9 -14.1 2.8 0.5

Unweighted average over countries -2.2 -5.8 -5.4 -12.8 3.3 1.0

Standard deviation 2.2 2.2 5.6 7.2 0.5 0.4

Coefficient of variation -0.975 -0.379 -1.043 -0.565 0.163 0.362

Change over previous year

Change over previous

year

21 23.09.2009

Money Supplies in

Great Depression vs. Current Crisis

Source: Eichengreen-O’Rourke (2009).

22 23.09.2009

Expansion of Central Banks’

balance sheets 2000/2009

Source: IMF (2009) using Bloomberg,Bank of Japan, Datastream, ECB.

23 23.09.2009

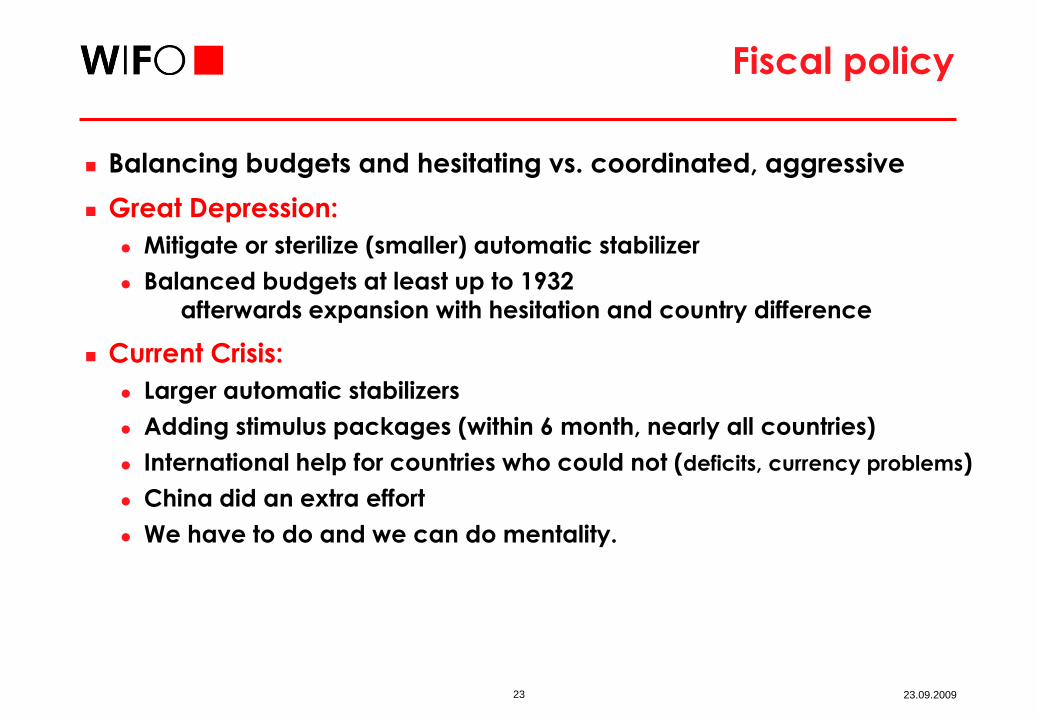

Fiscal policy

Balancing budgets and hesitating vs. coordinated, aggressive

Great Depression:

Mitigate or sterilize (smaller) automatic stabilizer

Balanced budgets at least up to 1932

afterwards expansion with hesitation and country difference

Current Crisis:

Larger automatic stabilizers

Adding stimulus packages (within 6 month, nearly all countries)

International help for countries who could not (deficits, currency problems)

China did an extra effort

We have to do and we can do mentality.

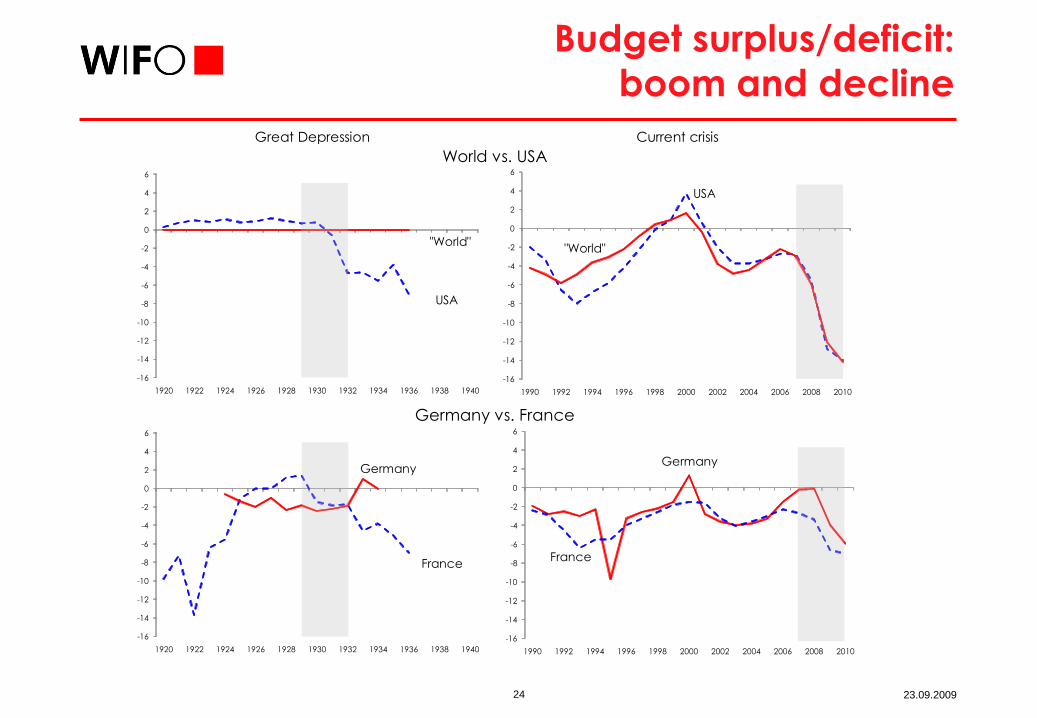

24 23.09.2009

Budget surplus/deficit:

boom and decline

1408.89715

1408.89715

Great Depression Current crisis

World vs. USA

Germany vs. France

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

France

Germany

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

Germany

France

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

USA

"World"

-16

-14

-12

-10

-8

-6

-4

-2

0

2

4

6

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

"World"

USA

25 23.09.2009

Government Budget Surpluses in the

Great Depression vs. Current Crisis

Source: Eichengreen-O’Rourke (2009).

1929

2010 world2009

advanced

countries

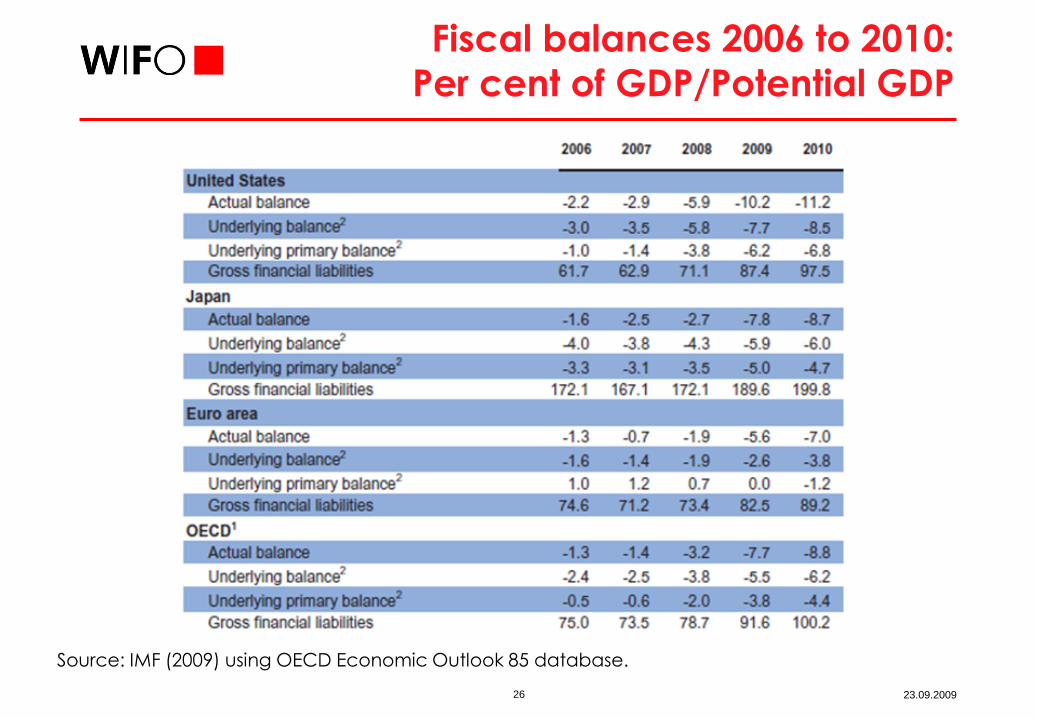

26 23.09.2009

Fiscal balances 2006 to 2010:

Per cent of GDP/Potential GDP

Source: IMF (2009) using OECD Economic Outlook 85 database.

27 23.09.2009

Is the Current Crisis over?

Burdens left

For production it could be over (decline stopped)

Not for unemployment

Lower growth expected in the medium term

Mega burdens to be tackled:

Consolidation of budgets without increasing taxes (too much)

Fighting unemployment while preparing for ageing society

Increasing economic growth while switching towards sustainability

Regulatory reforms without impairing financing of firms, consumers

Prudent governments and excellent

policy advice needed.

28 23.09.2009

Why there should be no further

steps of decline (we hope)?

Everything happened in the beginning Burst of bubbles, stock market decline, break down of exports,

bank failures

These problems occurred step by step during GD, as hopes of end

had come up

The policy reacted this time with force, determinedness, coordinated

In GD first un-decisive, partly restrictive as fiscal policy started to stabilize - money supply collapsed

Bank failures were unexpected, at least policy reaction and

repercussions

No deflation this time

No center periphery pattern - in the contrary: China, India restart the engine Surplus money (sovereign state funds) available for recapitalization

and reinvestment: Arab countries, Norway, Indonesia.

29 23.09.2009

Policy requirements to prevent

further steps similar to GD

Policy recommendation (learning from GD)

Refrain from early exit: fiscal policy, monetary policy, bank support

Keep reserve funds and task forces for critical situations

Minimize protectionism

Policy recommendations (learning from causes of CC)

Shift support from old structures (cash for clunkers) to future needs

Improve regulation and international coordination

Reduce imbalances in a consistent medium-run strategy

Will the consensus of economists last: if unemployment and fiscal deficits approach 10%? (in some countries, 7% in others).

30 23.09.2009

Summary I

The drop in activity was much smaller, the CC was shorter

The rebound of the stock market is larger and longer than during GD

The CC had the potential of a much greater crisis

Better institutions, higher globalization and synchronization potentialbut also multi polarity

Policy acted decisively, strong, early, partially coordinated

All policy lines were applied at the same time

Consensus of economists was surprisingly strong.

31 23.09.2009

Summary II

Further steps can not to be excluded -probability can be minimized by watchful policy

Exit phase very demanding

Long-run lessons not learned, long-run problems not attacked

The two crisis are siblings (not twins)who got different foster parents

How will the younger one behave in adolescence and as grown up (in adulthood).

32 23.09.2009

Karl Aiginger

Comparing the Current Crisis to the

Great Depression

OECD - Nero ConferenceParis, September 21, 2009

H:user/aig/vortrag/OECD_crises_210909_short.pptx

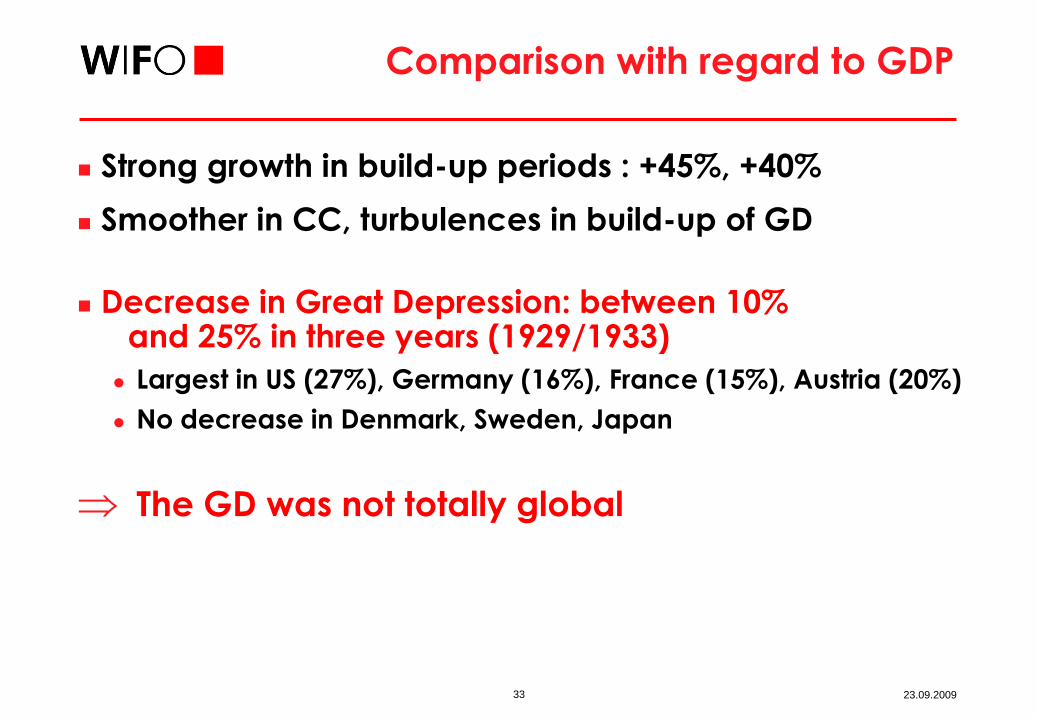

33 23.09.2009

Comparison with regard to GDP

Strong growth in build-up periods : +45%, +40%

Smoother in CC, turbulences in build-up of GD

Decrease in Great Depression: between 10% and 25% in three years (1929/1933)

Largest in US (27%), Germany (16%), France (15%), Austria (20%)

No decrease in Denmark, Sweden, Japan

The GD was not totally global

34 23.09.2009

Further results for GDP

Decrease in Current Crisis: about 5% in quarterly data (2Q2009/peak 2008)

Between 2% world, 4% US, 7% Germany, 8% Japan

More severe in Russia, Ukraine, Baltics, Turkey

Continued growth in Poland, China, India

This comparison overstates Current Crisis

(quarterly data vs. annual)

Much smaller decline in GDP

Less dispersion (for industrialized countries)

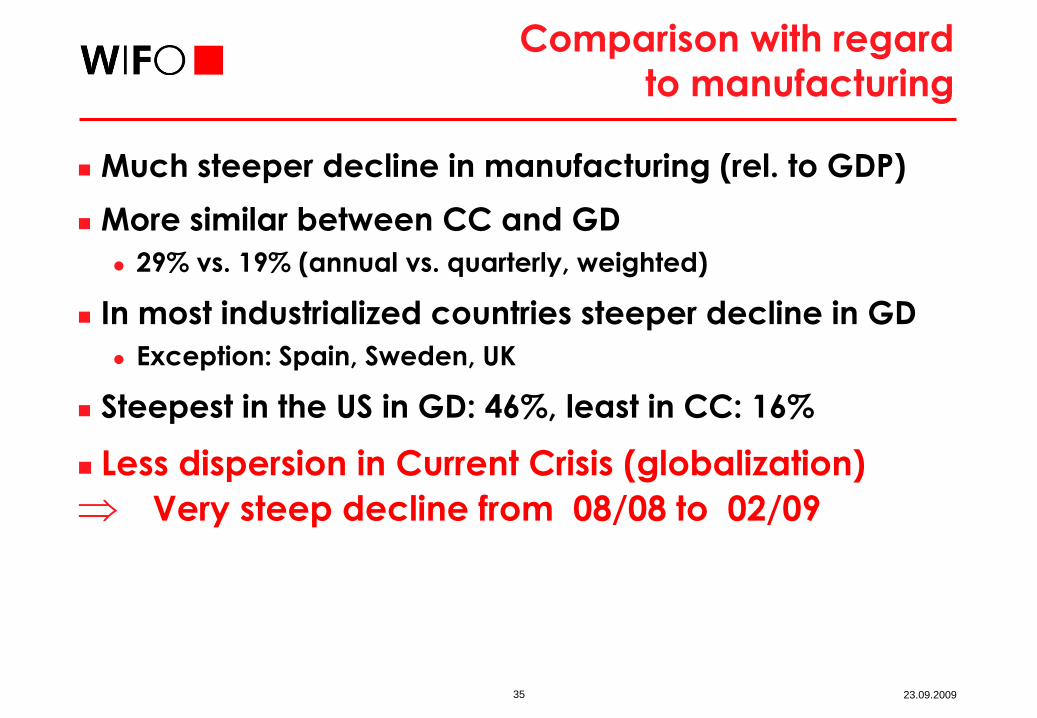

35 23.09.2009

Comparison with regard

to manufacturing

Much steeper decline in manufacturing (rel. to GDP)

More similar between CC and GD

29% vs. 19% (annual vs. quarterly, weighted)

In most industrialized countries steeper decline in GD

Exception: Spain, Sweden, UK

Steepest in the US in GD: 46%, least in CC: 16%

Less dispersion in Current Crisis (globalization)

Very steep decline from 08/08 to 02/09

36 23.09.2009

Comparison of two crises:

Industrial production

1929/1921 1932/1929 Peak/2000 Peak/1990

2009

forecast

2Q2009/

peak 2008

Quarterly data

Austria 52.1 -39.0 33.0 77.2 -15.3 -20.5

Germany 51.8 -41.2 21.2 33.5 -21.8 -24.3

Belgium 113.0 -36.5 12.3 29.8 -19.0 -16.9

Spain 48.1 -6.4 8.5 23.8 -22.7 -22.8

France 127.8 -26.0 2.4 13.4 -18.2 -24.6

Finland 134.6 -13.1 25.4 108.6 -24.3 -28.2

Sweden 94.1 -10.6 19.1 73.9 -22.3 -26.9

United Kingdom 57.3 -10.8 0.9 7.1 -12.9 -18.4

USA 87.9 -46.0 7.3 56.6 -13.0 -15.7

Japan 50.0 -2.6 8.9 4.7 -32.2 -32.1

"World" 72.2 -29.5 8.0 34.3 -16.5 -18.9

Unweighted average over countries 81.7 -23.2 13.9 42.9 -20.2 -23.0

Standard deviation 34.3 16.3 10.4 34.8 5.9 5.2

Coefficient of variation 0.420 -0.703 0.750 0.811 -0.290 -0.227

Great depression (1932) Current crisis (2007 ff)

Percentage change

Annual data

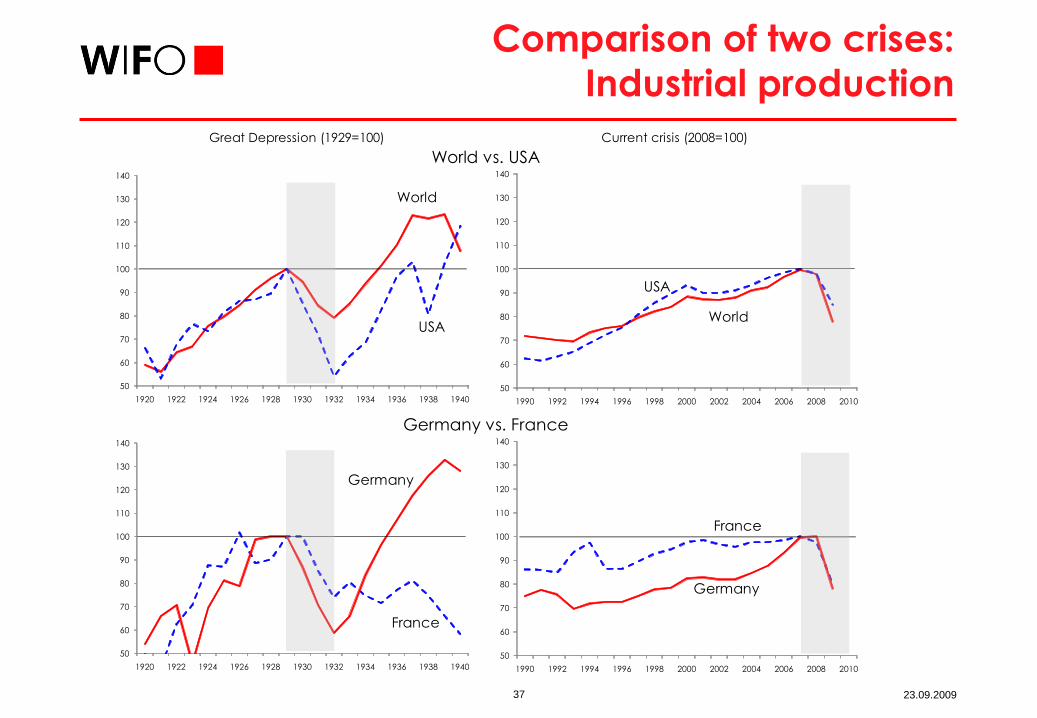

37 23.09.2009

Comparison of two crises:

Industrial production

1408.89715

1408.89715

Great Depression (1929=100) Current crisis (2008=100)

World vs. USA

Germany vs. France

50

60

70

80

90

100

110

120

130

140

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

World

USA

50

60

70

80

90

100

110

120

130

140

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

World

USA

50

60

70

80

90

100

110

120

130

140

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

France

Germany

50

60

70

80

90

100

110

120

130

140

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

France

Germany

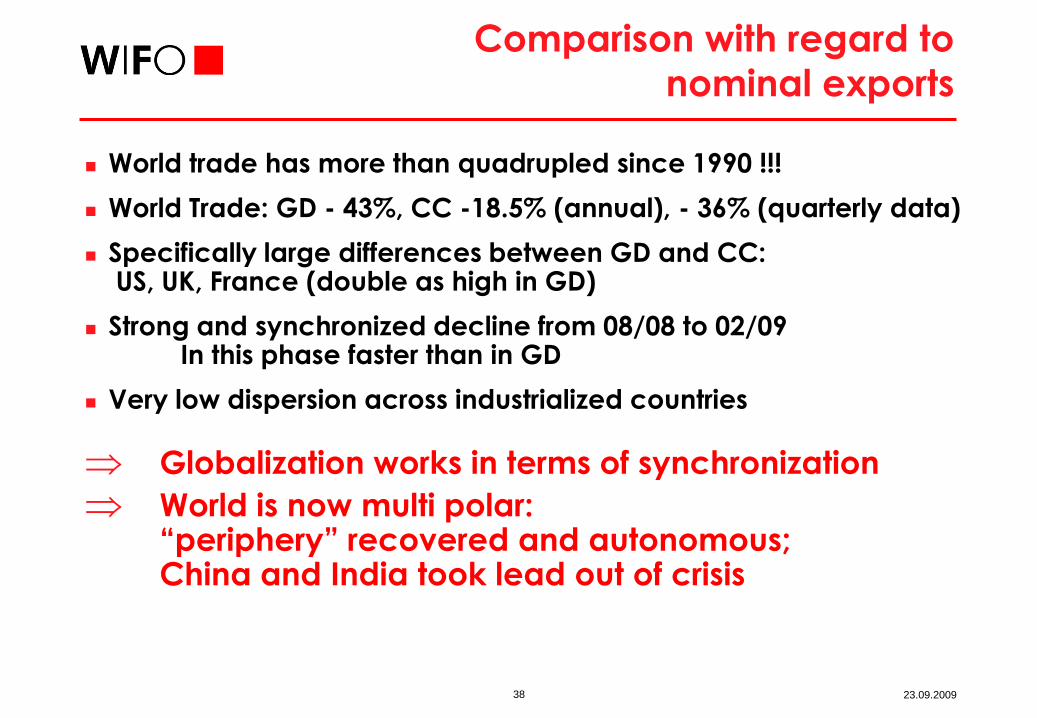

38 23.09.2009

Comparison with regard to

nominal exports

World trade has more than quadrupled since 1990 !!!

World Trade: GD - 43%, CC -18.5% (annual), - 36% (quarterly data)

Specifically large differences between GD and CC:US, UK, France (double as high in GD)

Strong and synchronized decline from 08/08 to 02/09In this phase faster than in GD

Very low dispersion across industrialized countries

Globalization works in terms of synchronization

World is now multi polar: “periphery” recovered and autonomous;China and India took lead out of crisis

39 23.09.2009

Comparison of two crises:

Nominal export growth

Great Depression (1932)

1929/1921 1932/1929 Peak/2000

2009

forecast

1Q2009/

peak 2008

Quarterly data

Austria 68.1 -41.0 68.6 -22.9 -26.2

Germany 45.3 -28.9 66.1 -21.0 -22.9

Belgium -24.2

Spain -25.7

France 153.6 -39.3 25.6 -21.1 -21.5

Finland -40.7

Sweden 65.2 -38.1 47.9 -30.0 -20.7

United Kingdom 3.6 -45.8 32.7 -19.8 -14.8

USA 17.3 -54.0 66.4 -10.6 -28.3

Japan

World 67.5 -43.3 150.0 -18.4 -30.0

Unweighted average over countries 58.8 -41.2 51.2 -20.9 -25.0

Standard deviation 53.0 8.4 18.8 6.2 7.1

Coefficient of variation 0.901 -0.203 0.367 -0.298 -0.282

Current crisis (2007ff)

Percentage change

Annual data

40 23.09.2009

Comparison of two crises:

Nominal export growth

1408.89715

1408.89715

Great Depression (1929=100) Current crisis (2008=100)

World vs. USA

Germany vs. France

20

40

60

80

100

120

140

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

World

USA

20

40

60

80

100

120

140

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

World

USA

20

40

60

80

100

120

140

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

France

Germany

20

40

60

80

100

120

140

1920 1922 1924 1926 1928 1930 1932 1934 1936 1938 1940

France

Germany

41 23.09.2009

Stock Market Decline

GD: steep fall at the start, long recovery

70% (GDP weighted), US -84% (1929/1932)

CC: steepest part 08/2008 to 03/2009

Overall decline much smaller (44% vs. 69%; 4 big indices)

Rebound up to 33% (weighted), 45% unweighted (monthly)

Largest rebound in GD: +13% in world, 16% in US in 11/1929

Outsider Japan: now steeper than in GD (in Austria, too)

Steeper decline (than in GD) from 08/2008 to 03/2009Proportionate decline now for given period (17 month) smaller (Contrary to Eichengreen who started graphs in April 1929)

42 23.09.2009

Unemployment rate, employment,

income level

Unemployment rose from 3% (1929) to 12% (1932; world) in GD

From 3% to 24% (USA)

From 9% to 30% (Germany)

From 12% to 25% (Austria)

CC: from 5% to 7% (2009), maybe surpassing 10% in US, EU 2010/11

Employment decreased by 16% (World, US: -18%, DE: -29%) in GD

And is expected to decrease by 2% to 3% in CC 2009

Employment doubled since GD, +8% since 2000

Income (real, PPP) is 8 to 10fold of 1929 at the start of the crisis

43 23.09.2009

Fiscal policy in GD

Surplus or small deficits in 1929

Deficit of 0.5% (1930), 1% (1931), 3% (1932), and then finally more (data for general government)

This looks to be much less than automatic stabilizers(at least up to 1931)

Governments (and states) tried to keep deficits low,

raised taxes

Restraints due to currency stabilization,

gold standard, memories of war debt and hyperinflation

44 23.09.2009

Fiscal policy in CC

Starting from -2.7% in US, -0.7% in EU, -5.5% in UK (2008)

Allowed automatic stabilizers to work

And added stimulus packages as of 4-5% of GDP (08/10)

At the start (2008/09) larger part were automatic stabilizers,

but intention to allow and to amplify them was clear from the start

Larger multipliers today

Political will to increase public demand/decrease taxes

(Nearly) all countries in (loosely) coordinated effort

45 23.09.2009

Fiscal policy: Interpretation

Great Depression:

1929-1931 Attempts to mitigate (smaller) automatic stabilizers

to balance budget, secure currency

prevent money/gold outflow

small deficits or even surpluses

from 1932 on more active (USA, France)

non coordinated internationally

Current Crisis:

different starting level in US, EU, UK

all allowed automatic stabilizers to work

additional stimulus packages

coordinated

46 23.09.2009

Complementary policies

in the Current Crisis

Fiscal/monetary intersection in CC

Guarantees of deposits

Recapitalization of banks

State ownership (partly, temporary) from banks to car firms

Similar guarantees of deposits recapitalization also in GD, but late, eclectic, uncoordinated (no ex ante funds and rules)

Employment policy: short-term working programs

Protectionism: strong verbal opposition

Opposition and mitigation where it occurred

Soft protectionism and “buy national” clauses exist

and may become more frequent (US tires etc.)

47 23.09.2009

The Current Crisis had the potential

of a Great Depression

Decline of manufacturing (and exports) for several months similar

“Fast start” of CC – at least after it was transmitted to real sector in 2008

Short length (at least for production and given if it is over in 2009)

Soft start in GD (slower transmission of stock crash in less globalized world); cycle had leveled off before

The final difference was in the length of the depression, not the speed at the beginning

48 23.09.2009

What made the difference?

Differences in institutions:

Lower share of manufacturing, larger public sector

New institutions (IMF, G20, World Bank), new coordination will

No gold standard, no competitive devaluations, Euro members sheltered

Difference in policy

All strands of policy worked together (with national differences)

Economists had a clear message: you can and should do somethingHalf of the economists did restrain from their usual advice

or were sidelined ;

OECD adopted a proactive approachit

Politicians of all large countries wanted pro active

policy at any costs, within or outside of existing rules

49 23.09.2009

Is the Current Crisis over?

Burdens left

For production it could be over (decline stopped)

Not for unemployment

Lower growth expected in the medium term

Mega burdens to be tackled:

Consolidation of budgets without increasing taxes (too much)

Fighting unemployment while preparing for ageing society

Increasing economic growth while switching towards sustainability

Regulatory reforms without impairing financing of firms, consumers

Prudent governments and excellent

policy advice needed

50 23.09.2009

Why there should be no further

steps of decline (we hope)?

Everything happened in the beginning Burst of bubbles, stock market decline, break down of exports,

bank failures

These problems occurred step by step during GD, as hopes of end

had come up

The policy reacted this time with force, determinedness, coordinated

In GD first un-decisive, partly restrictive as fiscal policy started to stabilize - money supply collapsed

Bank failures were unexpected, at least policy reaction and

repercussions

No deflation this time

No center periphery pattern - in the contrary: China, India restart the engine Surplus money (sovereign state funds) available for recapitalization

and reinvestment: Arab countries, Norway, Indonesia

51 23.09.2009

Policy requirements to prevent

further steps similar to GD

Policy recommendation (learning from GD)

Refrain from early exit: fiscal policy, monetary policy, bank support

Keep reserve funds and task forces for critical situations

Minimize protectionism

Policy recommendations (learning from causes of CC)

Shift support from old structures (cash for clunkers) to future needs

Improve regulation and international coordination

Reduce imbalances in a consistent medium-run strategy

Will the consensus of economists last: if unemployment and fiscal deficits approach 10%? (in some countries, 7% in others)

52 23.09.2009

Summary over stylized facts I

Given that policy decline has leveled off in summer 2009

The drop in GDP has been much smaller than in GD

Definitely for world output (-10% vs. -1% to -2%)

Specifically for all USA, France, Germany

Not for Japan, and some countries less affected in GD

53 23.09.2009

Summary over stylized facts II

Difference GD-CC is less in manufacturing and for exports

but still smaller drop for most industrialized countries

Stock market decline has been less for big stock exchanges

Effect on unemployment (up to now and including forecasts

2010/11) much smaller, the same holds for employment loss

Difference is not so much in the speed of decline,

but in the length, therefore the results depend on

the recurrence of the crisis or not

Prudent policy can prevent the recurrence