company presentation - helios towers · towers, ltd. (the “company”)or any of its affiliates or...

TRANSCRIPT

COMPANY PRESENTATION

8TH APRIL 2019

Website: www.heliostowers.com

LinkedIn: www.linkedin.com/company/helios-towers

Helios Towers | Private & Confidential

Disclaimer

2

No investment adviceThis Presentation does not constitute or form partof, and should not be construed as, an offer,invitation or inducement or recommendation topurchase or subscribe for any securities in HeliosTowers, Ltd. (the “Company”) or any of its affiliatesor subsidiaries (together the “Group”) in anyjurisdiction nor should it or any part of it form thebasis of, or be relied on in connection with, anycontract to purchase or subscribe for anysecurities of the Company or any member of itsgroup or with any other contract or commitmentwhatsoever.

Further, it should not be treated as givinginvestment, legal, accounting, regulatory, taxationor other advice and recipients should each maketheir own evaluation of the Company and of therelevance and adequacy of the informationcontained herein.

No warrantyNo representations or warranties, express orimplied are given in, or in respect of, thisPresentation. To the fullest extent permitted bylaw, in no circumstances will the Company, or anyof its respective subsidiaries, shareholders,affiliates, representatives, partners, directors,officers, employees, advisers or agents beresponsible or liable for any direct, indirect orconsequential loss, loss of profit, damages or costsarising from the use of this Presentation, itscontents (including the internal economicmodels), its omissions, reliance on the informationcontained within it, or on opinions communicatedin relation thereto or otherwise arising inconnection therewith. The information containedin this Presentation has not been independentlyverified.

Third party sourcesCertain statistical and other information about theCompany included in this Presentation is sourcedfrom publicly available third party sources. As suchit presents the views of those third parties, but maynot necessarily correspond to the views held bythe Company and the Company expresslydisclaims any responsibility for, or liability in respectof, such information.

Forward-looking statementsThis Presentation contains illustrative returns,projections, estimates and beliefs and similarinformation (together, “Forward LookingStatements”). The Forward Looking Statementscan be identified by the use of forward lookingterminology, including the terms “believes”,“estimates”, “anticipates”, “expects”, “intends”,“plans”, “may”, “will” or “should” or, in each case,their negative or other variations or comparableterminology.

The Forward Looking Statements are subject toinherent uncertainties and qualifications and arebased on numerous assumptions, in each casewhether or not identified in the Presentation. TheForward Looking Statements are provided forillustrative purposes only and are not intended toserve as, and must not be relied upon by anyinvestor as a guarantee, an assurance, aprediction or a definitive statement of fact orprobability.

Nothing in this Presentation should be construed asa profit forecast. Actual events and circumstancesare difficult or impossible to predict and will differfrom assumptions. Many actual events andcircumstances are beyond the control of theCompany. Some important factors that could

cause actual results to differ materially from thosein any Forward Looking Statements could includechanges in domestic and foreign business, market,financial, political and legal conditions. There canbe no assurance that any particular ForwardLooking Statements will be realised, and theperformance of the Company may be materiallyand adversely different from the Forward LookingStatements. The Forward Looking Statementsspeak only as of the date of this Presentation. TheCompany expressly disclaims any obligation orundertaking to release any updates or revisions toany Forward Looking Statements to reflect anychange in the Company’s expectations withregard thereto or any changes in events,conditions or circumstances on which anyForward Looking Statements are based.Accordingly, no reliance should be placed uponthe Forward Looking Statements.

Company Overview

Helios Towers | Private & Confidential

A Leading Sub-Saharan Independent TowerCo

4

Tower market share

Tanzania

Sites

3,701

DRC

Sites

1,773

Congo B

Sites

380

Sites

891

Ghana

5 countries

6,745 total sites

13,549 tenants

2.01x tenancy ratio

$359m Q4 2018 LQA(3)

22% CAGR FY 2015 – Q4 2018 (annualised)

81% of future contracted

revenues from Africa’s Big 5 MNOs(4)

Market Share(1)

66%

Market Share(1)

63%

Market Share(1)

49%

Market Share(1)

21%

Contracted revenues(2)

$3.1bn

$186m Q4 2018 LQA(3)

51% CAGR FY 2015 – Q4 2018

(annualised)

c.65% 2018 Adj. EBITDA in $/€

Lease-weighted average contract life remaining

8.1 years

Adj. EBITDA

Revenue

Source: Company as of 31 December 2018, except as otherwise indicated

(1) Hardiman Report, March 2019. Based on online, marketable sites(2) Refers to revenue contracted until 2035

(3) LQA = Last quarter annualised(4) Big 5 MNOs defined as: Airtel, MTN, Orange, Tigo, Vodafone/com

1 Company Overview

Attractive, Long-term Contracted Revenues

South Africa

As of January 2019

Helios Towers | Private & Confidential

42 50 60 63

83 85

126 127 133 138 148

164 168 176 181 186

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18

16 Consecutive Quarters of Adj. EBITDA(1) Growth

5

CAGR

FY 2015 – Q4 2018 LQA 51%

Group Annualised Adj. EBITDA ($m)

1 Company Overview

35% 35% 39% 38% 40% 40% 42% 47%46% 49%25% 27% 28% 28% 51% 52%

Margin

(1) “Adjusted EBITDA” is defined as earnings before interest, tax, depreciation and amortization adjusted for discontinued operations, other gains and losses, investment income, loss on disposal of PP&E, impairment of intangible assets and PP&E, deal costs relating to unsuccessful tower transactions or successful tower transactions that cannot be capitalized, and exceptional items. Exceptional items are material items that are considered exceptional in nature by management by virtue of their size and/or incidence. Annualised Adjusted EBITDA calculated as per the bond definition as the most recent fiscal quarter multiplied by 4. This is not a forecast of future results

Margin has more than doubled through top-line growth and implementation of business excellence strategy

>2x

Helios Towers | Private & Confidential

6

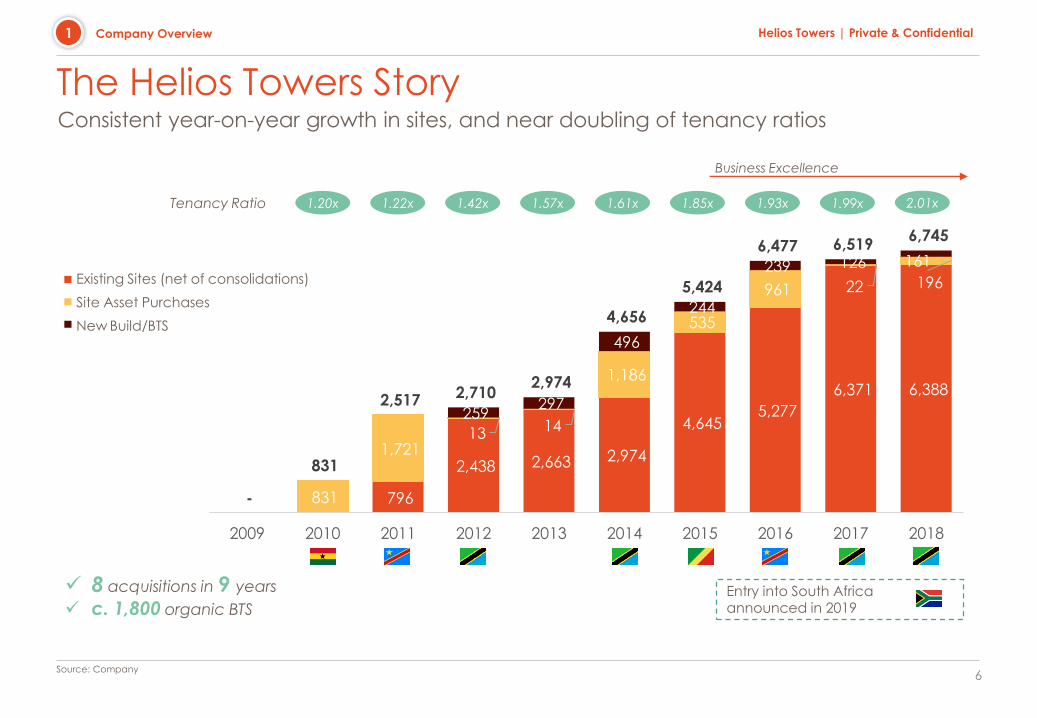

The Helios Towers Story

Source: Company

Existing Sites (net of consolidations)

Site Asset Purchases

New Build/BTS

Consistent year-on-year growth in sites, and near doubling of tenancy ratios

8 acquisitions in 9 years

c. 1,800 organic BTS

796

2,438 2,663 2,974

4,645 5,277

6,371 6,388

831

1,721 13 14

1,186

535

961 22 196

259 297

496

244

239 126 161

-

831

2,517 2,710 2,974

4,656

5,424

6,477 6,519 6,745

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1.20xTenancy Ratio 1.22x 1.42x 1.57x 1.61x 1.93x 1.99x1.85x

Business Excellence

2.01x

1 Company Overview

Entry into South Africa announced in 2019

Helios Towers | Private & Confidential

7

1 Company Overview

(1) United nations population prospects

(2) Hardiman report, March 2019(3) GSMA Intelligence, January 2019

Attractive Growth Indicators

c.30,000 towers in SA with only

c.10% owned and operated by

independent tower companies(2)

4G/

5G

3G and 4G widely available, increased

4G densification expected and to be

“5G ready”, with over 4 million 5Gconnections expected by 2023(3)

Multiple MNOs operating, including 2

of Africa’s “Big-5” MNOs

57 million population, forecast to

increase by 3 million over the next 5

years(1)

MTN Vodacom

TelkomCell C

c. 6,000 additional standard

PoS required by 2024(2)

Why HT has Entered South AfricaA high-growth market for HT – with attractive and diversifying dynamics

Favourable Structural Dynamics

1

2

3

1

2

3A leader in telecommunications innovation in Africa, providing the

opportunity to develop expertise in adjacent technologies which can

be leveraged in our four other markets

Helios Towers | Private & Confidential

8

1 Company Overview

How HT has Entered South Africa

Helios Towers South Africa (“HTSA”) created through Partnership with Vulatel

• Partnership with Vulatel announced January 2019 with HTSA majority owned by HT

• Vulatel management team made up of ex-Vodacom directors

• Level 2 B-BEE rating, 69% black owned and 45% black women owned

• Platform to expand HT product offering and geographical mix

• Announced acquisition of 13 fibre regeneration sites in April 2019

• HTSA announced first investment in SA through acquisition of SA Towers

• Pipeline of c.500 urban locations which are ready to be built or are in the process of

being permitted

• Expected to close Q2 2019

HTSA Acquires SA Towers

Creation of infrastructure platform to drive growth in South Africa

1

2

Helios Towers | Private & Confidential

9

1 Company Overview

Encouraging Recent Market Developments

Customers post +9% subs growth in Tanzania

in FY 18(1)

DRC customers report

+10% subs growth

in FY 18(2)

Felix Tshisekedi sworn

into office in DRC

24th January

+4.8%GDP growth in our

markets in 2018(3)

Africa Widely Identified as a Key Continent for Business Opportunities

Positive Political, Economic and Industry Dynamics

(1) Tanzania Communications Regulatory Authority

(2) GSMA estimates, 2018

(3) IMF 2018. Revenue-weighted average

Vodacom Airtel

Halotel

Tigo

Vodacom Airtel

Africell

Orange

Strategy

Helios Towers | Private & Confidential

11

HT Growth Strategy

(1) Hardiman Report, March 2019

(2) Company estimates of towers that can be acquired in HT’s markets as of 1 March 2019

(3) TowerXchange “TowerXchanges analysis of the Sub-Saharan African tower Industry”, July 2018

2 Strategy

Existing Markets Adjacent New TechnologiesNew Markets

Small Cells

Fibre Backhaul

Data Centres

• c.150k towers in Africa(3)

• c.58k towers owned by

independent TowerCos(3)

• What we look for:

Emerging market

Population of >10m

3+ operators

Stable and / or pegged currencies

Infrastructure gap

High subscriber growth

Low mobile penetration

Enhances group returns

Tanzania, DRC, Congo B and Ghana

South Africa

c.6,000 new standard PoS required by

2024(1)

Tower build program

Dark fibre

Edge data centres

Significant organic and acquired

EBITDA growth since 2015

c.12,000 new standard PoS required

by 2024 in established markets(1)

Potential opportunities to acquire

c.3,500 towers in existing markets(2)

54

106

146

178

33

19

31

1032

2015 Organic Acquired 2016 Organic Acquired 2017 Organic 2018

Strong platform for growth in new and existing markets

Helios Towers | Private & Confidential

Operational Strategy

12

“Congratulations for the good performance during May and June 2018”

Vodacom Congo, Chief Executive Officer

“We wish to understand and learn the principles so that we can share the

knowledge with other African Opcos”

Vodacom Tanzania, Chief Technology Officer

“We would like to learn from your operation and help us do what you do”

Viettel, Chief Technology Officer

“Aside from the performance I am equally impressed by your HSE”

Tigo Tanzania, Chief Technology Officer

Efficiency Improvements since 2015:

• 93% improvement in power service

delivery from Q4 15 to Q4 18(1)

• $46m reduction in capex between 2015

and 2018 on pricing alone

• 80% reduction in strategic suppliers from

60 to 12 between 2015 and Q4 18

• 38% productivity improvement with

employees per 100 towers reducing to

5.3 from 8.6(2)

• 45% reduction in office space(3)

Source:Company

(1) Q4 2018 average weekly downtime per tower compared to Q4 2015 average

(2) From December 2015 to December 2018

(3) Office space reduction in m2 in Tanzania, DRC and Congo B from December 2015 to December 2018

By the end

of 2018:

Of our staff will have

been trained in Lean Six Sigma

Driving Efficiency Improvements Customer Service Excellence FocusBuilding a Business Excellence Culture

Focus on developing local teams:

Trained in Six Sigma

by the end of 2019c.50%

c.35%

2 Strategy

Delivered significant achievements, with opportunities for further improvement

Markets

Helios Towers | Private & Confidential

6.7%

6.8%

6.9%

6.9%

6.9%

7.0%

7.2%

7.3%

8.2%

8.3%

Philippines

Tanzania

Senegal

Bhutan

Cambodia

Djibouti

Cote d'Ivoire

India

Ethiopia

Ghana

Why Africa?

14(1) ‘African cities surge to top of global growth league’ FT (11 September 2018)(2) World Bank 2018(3) UN Population Prospects 2018, projected % population change from 2018-2035 for cities with a current population over 2.5m

“Africa has become the world’s most

rapidly urbanising continent. From 2018 to 2035, the UN predicts that the world’s

10 fastest growing cities will be

African....Urbanisation is what helped

ignite the ‘Africa Rising’ narrative”Financial Times (2018)(1)

World Population Growth(1)

(Billion People)

Top 10 fastest growing economies in 2018(2)

(GDP)

3 Markets

96%

100%

103%

103%

104%

105%

108%

117%

121%

135%

Bamako, Mali

Port Harcourt, Nigeria

Kinshasa, DRC

Addis Ababa, Ethiopia

Antananarivo, Madagascar

Lusaka, Zambia

Abuja, Nigeria

Ouagadougou, Burkina Faso

Dar es Salaam, Tanzania

Kampala, Uganda

Top 10 fastest growing cities 2018 - 2035(3)

(Population)

2018 Population

1.3 Billion

2100 Population

4.5 Billion

Sustainable long-term growth

Helios Towers | Private & Confidential

Helios Towers’ Structural Growth OpportunityOur markets are expected to grow significantly in the coming years

38m(1)

new people in HT markets

8%(1)

increase in penetration

27m(1)

increase in people living in cities

67%(1)

below 30 years old

5.1%(2)

increase in GDP

51m(3) more

subscriptions across HT markets

Demand for Mobile

New technology

+4x(4)

increase in 4G connections

Data usage

+11x(5)

increase in data usage in SSA

Infrastructure demand

~18,000(3) new

standard PoS in HT markets

4G

(1) United Nations, World Population Prospects. 2018-2024E

(2) IMF, World Economic Outlook October 2018. 2017-2023E

(3) Hardiman report, March 2019. 2018-2024E

(4) GSMA Intelligence, March 2019. 2018-2024E

(5) Ericson Mobility Report, June 2018. 2017-2023E

+

Positive Macro Drivers

Low Telecom Penetration

High Equipment Growth

15

+ + +

+ +

3 Markets

Helios Towers | Private & Confidential

HT Markets Sub-Saharan Africa G7

Structurally Attractive Markets With Superior Growth

(1) United Nations Population Prospects, 2018 Revision. 2018-2023E

(2) United Nations Population Prospects, 2018 Revision. 2018

(3) IMF World Economic Outlook, October 201816

Macro

Strong GDP growth drives disposable income(3)

Real GDP Growth 2017-2023E

238m addressable population in HT’s marketsPopulation (m)(1)

Young Population with c.70% under 30(2)

0-30yrs

30+yrs

11%

3%

HT Markets G7

Favourable urbanisation trends(1)

Increase in urban population (2018-2024E) as % of population

+27 million will move to cities

5.1%

3.3%

1.6%

HT Markets Sub-Saharan Africa G7(revenue weighted)

TZ 60

DRC 85

CB 5GH 30

238

276

782

766

Population 2024E

1,064

1,241+2%CAGR

+3%CAGR

+0%CAGR

SA 58

67%

35%

33%

65%

HT Markets G7

3 Markets

Helios Towers | Private & Confidential

44 5838

635639

4499

104

2018 2024

Tanzania DRC Congo B Ghana South Africa

15% 17%

27%33%

48%

26% 29%

73%

Tan

zan

ia

DR

C

Co

ng

o B

Gh

an

a

So

uth

Afr

ica

Av

g H

T

Ma

rke

ts

Nig

eria

G7

43%

68%

36% 35%

19%

31%21% 6%

Tan

zan

ia

DR

C

Co

ng

o B

Gh

an

a

So

uth

Afr

ica

Av

g H

T

Ma

rke

ts

Nig

eria

G7

Structurally Attractive Markets With Superior Growth

(1) Hardiman Report, March 2019. Unique mobile subscribers 2018

(2) GSMA Intelligence, March 2019. Unique broadband subscribers 2018 17

+18,000 added PoS

(3) Point of Service or Operator Tenancy as opposed to Network PoS signifying different technology

equipment placed on a site by a single operator. Given multiple technologies, Network PoS can

considerably exceed equivalent PoS

(4) Hardiman Report March 2019. Company estimate for G7 based on subscriber growth

Underpenetrated mobile markets(1)

2018-2024E MNO PoS(3) Growth(4)

Telecoms

40% 37%

49%54%

67%

47% 49%

85%

Tan

zan

ia

DR

C

Co

ng

o B

Gh

an

a

So

uth

Afr

ica

Av

g H

T

Ma

rke

ts

Nig

eria

G7

Mobile broadband penetration is low(2)

Mobile subscription growth(1)

2018-2024E275

224

3% CAGR

CAGR2018-2024E: +9% +4% +2% +1%+5%

3 Markets

Helios Towers | Private & Confidential

2017 2018 2019 2020 2021 2022 2023

Sub-Saharan Africa North America China Western Europe

Mobile Operators Poised for African Data Boom

18(1) Ericsson Mobility Report, June 2018

(2) Company as of December 2018

Increased Mobile Data Consumption(1)

(2017 Indexed = 100)

c.11xIncrease in mobile data

traffic in SSA(2017 – 2023E)

c.6-8xIncrease in mobile data

traffic in China, North America and Western Europe

(2017 – 2023E)

3 Markets

4G Licence Awarded

Tanzania 2015

DRC 2018

Ghana 2016

Congo B 2016

South Africa 2012

+535Amendment

Colocations added since 2015(2)

Robust Business Model

Helios Towers | Private & Confidential

USD

62%

XAF/EUR

3%

LCY

35%USD

53%

XAF/EUR

4%

LCY

28%

Power

LCY

15%

Founded on Strong Contracts and Sustainable PricingBuilding Customer Relationships

(1) TCO = Total cost of ownership by MNO. Includes opex, maintenance capex and financing cost at 8%

(2) Based on FY 2018 results

(3) Airtel, MTN, Orange, Tigo, Vodafone/com

Long Tenure

Minimal cancellation rights

Automatic renewal clauses

Menu pricing for amendment revenue

Inflation and power price escalators

Take-or-pay commitments (colocation/BTS)

Strong Long-Term Contracts Sustainable Long-Term Pricing Strategy

Lea

se R

ate

Consideration per site

Higher Sustainability Lower Sustainability

Deal Range

Replacement cost

TCO

HT Deals:Lease Rate Discount to TCO(1)

~35%

20

4 Robust Business Model

FX and Inflation Protected(2) Strong Blue-Chip Client Base

Future Contracted Revenue by

Customer

Revenue

FX Mix

EBITDA

FX Mix

Africa's Big 5

MNOs

81%

Other

19%

(3)

57% Hard

Currency

65% Hard

Currency

Helios Towers | Private & Confidential

Historical Capex Investment Drives Future Cash Flow Expansion

(1) Excludes intangibles

(2) Non-discretionary capex is defined as maintenance and corporate capital expenditure

(3) Calculated as Adj. EBITDA – Tax paid –– Maintenance and Corporate capital expenditure

(4) Based on analysis of 5,874 sites, using TIA-222-H Standard For Antennas And The Supporting Structures For Antennas And Small Wind Turbines

Strong Unlevered Recurring Cash Flow(3)Low Non-Discretionary Capex Expected Going Forward

Capex(1) ($m)

16

72

123

158

2015 2016 2017 2018

($m)

21

Non-discretionary

capex(2) level of

$20-25m p.a.

4

4 Robust Business Model

Maintenance & Corporate Upgrade Growth Acquisitions

19%

4%

27%

50%

At capacity

+1 tenancy

+2 tenancies

+3 tenancies

An Attractive Asset Base, Ready for Future Tenants

Available capacity to accommodate up

to c. 4.1x tenancy ratio(4)

81% of sites with capacity, lease-up ready and colocation

demand can be accommodated with minimal

incremental capex

2016 2017 2018 2019

281

171

119 100

(excl. SA)

Wrap-up

Helios Towers | Private & Confidential

43%

68%

36% 35%19%

Tan

zan

ia

DR

C

Co

ng

o B

Gh

an

a

So

uth

Afr

ica

Wrap-up

Invested to ensure lease-up ready in all markets

81% sites ready for new tenants

Capacity of 4.1x on tenancies today

In-market expansion options New Markets optionsAdjacent Service options

Prepared for Growth4

Source: Company as of 31 December 2018

(1) Source: Hardiman Report, March 2019

+18,000 added PoS

2018-2024 MNO PoS Growth(1)

Robust Business Model with Strong Recurring Cash Flows

6

Long-Term Contracts

Sustainable Pricing Strategy

FX and Inflation Protected

Diversified Blue Chip Client Base

Sole Independent TowerCo in 3 out of 5 markets

66% 63%

49% 21%

#1 #1

#1

1

Tanzania DRC

Congo B Ghana

HT market share (excl. South Africa)

77%Urban

23

Exposure to Large High Growth Markets

Population Growth

Young Population

Urbanisation

GDP Growth

Business Excellence Driving Margins Higher

5

Localised workforce

2 High Telecoms Infrastructure Growth

3

5 Wrap-up

Delivering growth and quality for our stakeholders

Appendix

Helios Towers | Private & Confidential

25

Leading Values, Ethics and HSE

Source: Company(1) Estimated annualised CO2 savings as of December 2018(2) 2018 average monthly KM driven compared to FY 16 average monthly KM driven

Training and code of conduct extends to suppliers

Global Whistleblower Hotline in place

Ethics

Health & Safety Environment

Values

Comprehensive suite of policies aligned with international best practice

Group-wide strategy to positively monitor and improve our contribution to the environment

“Do The Right Thing”

430 solar solutions, 640 hybrid sites and

400 grid connections installed, saving over

5,000 tonnes in CO2 emissions per year(1)

330K km monthly reduction in site travel,

resulting in 48K litres fuel being saved(2)

Group program for training and reinforcing our value;

6 Appendix

Helios Towers | Private & Confidential

Straight-Forward Revenue Model

26

• Adding new tenant to an existing tower

• Existing customer adds additional equipment

• Grow tower portfolio through acquisitions (sale & leaseback) or organically (build-to-suit)

Tower with 1 tenantColocation: Multiple

Tenancies

Amendment: Equipment

AdditionAcquire and Build Towers

• MNOs place own active equipment on HT towers

80%-90% Adj. EBITDA margin flow through(1)

1 2 3 4

(1) Based on management estimates

6 Appendix

Helios Towers | Private & Confidential

Previously at: • Hutchison Telecom

• BeMobile

• Strong management

team with extensive

experience came

together in 2015

• Demonstrating a

track record of

margin growth

• Establishing world-

class capabilities

within the

organisation

27

Philippe LoridonCEO HT Tanzania

• Joined 2012

Helen EbertChief Legal Officer

• Joined 2018

Roy CursleyDirector of Delivery

and Technology

• Joined 2015

Colin GastonDirector of

Special Projects

• Joined 2015

Tom GreenwoodChief Financial Officer

• Joined 2010

Alex LeighChief Commercial

Officer

• Joined 2012

Jeffrey

SchumacherCEO HT Ghana, HT

Congo Brazzaville &

HT South Africa

• Joined 2011

Nick SummersDirector of Sustainability

and Organisational

Development

• Joined 2010

Léon-Paul O.

ManyaCEO HT DRC

• Joined 2011

Kash PandyaChief Executive

Officer

• Joined 2015

Strong Executive Team

Previously at: • Tigo

• Dimension Data

Previously at: • Soros Fund

Management

Previously at: • Schlumberger

• Aggreko

Previously at: • Aggreko

Previously at: • Vodafone

Previously at: • Linklaters

• Freshfields

Previously at: • Rothschild

• UBS

Previously at: • PwC

Previously at: • Johnston Group

• Aggreko

6 Appendix