companies bill 2012 8th jan 2013-r

DESCRIPTION

BillTRANSCRIPT

PRESENTATION ON

COMPANIES BILL, 2012

WIRC OFINSTITUTE OF COST

ACCOUNTANTS OF INDIA

BY CS A SEKARB.COM, FCMA, ACS,LLB

BACKGROUND

• October 2011 - The Cabinet approved the proposal to make official amendments to the Companies Bill, 2011

• 14th December, 2011 – Companies Amendment Bill, 2011 introduced in the Lok Sabha, but was immediately referred to Standing Committee on Finance

• 26th June, 2012 – Standing Committee submitted its report to Speaker, Lok Sabha

• 13th August, 2012 – The report of standing committee laid before Lok Sabha and

• On 18th December, 2012 Based on standing committee report, amendments were proposed and finally the Companies Bill, 2012 was passed at 10.46 P .M. after discussions which lasted for about 3 hours.

HIGHLIGHTS OF THE COMPANIES BILL 2012 AS PASSED IN LOK SABHA

• 470 Clauses & 7 schedules as against 658 sections and 15 schedules in the existing Companies Act, 1956

• Bill divided into 29 chapters• New chapters on Registered Valuers, Government

Companies, Nidhis, NCLT and Special Courts• Bill empowers Central Government to make rules

through delegated legislation after having detailed consultative process

• Bill Provides for self – regulatory process but stringent compliance regime

WHAT LIES AHEAD• BILL IS REQUIRED TO BE PASSED BY RAJYA SABHA• AFTER BILL IS PASSED BY BOTH HOUSES (LOK SABHA HAVING

ALREADY PASSED IT), ASSENT OF PRESIDENT OF INDIA IS REQUIRED FOR COMPANIES BILL, 2012 TO BECOME AN ACT OF PARLIAMENT

• ONCE THE BILL BECOMES AN ACT CENTRAL GOVERNMENT WOULD NOTIFY THE DATE OF COMING INTO FORCE OF THE ACT AND ONLY FROM SUCH DATE THE PROVISIONS OF THE ACT WOULD COME INTO FORCE

• THE BILL PROVIDES THAT THE CENTRAL GOVERNMENT MAY PROVIDE FOR DIFFERENT DATES FOR DIFFERENT SECTIONS OF THE ACT TO COME INTO FORCE.

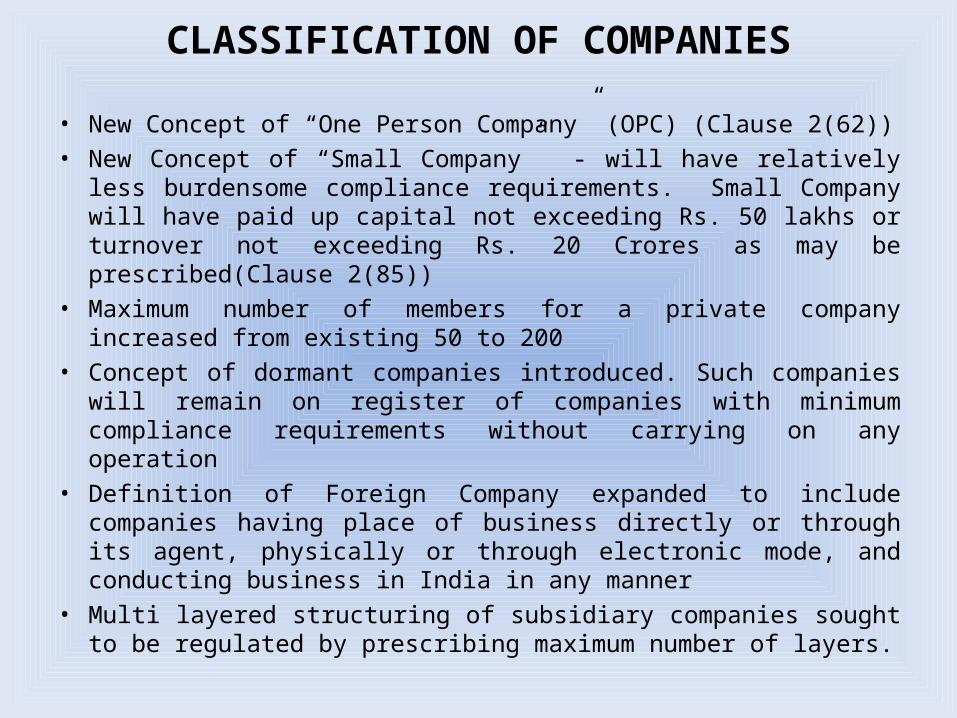

CLASSIFICATION OF COMPANIES

• New Concept of “One Person Company” (OPC) (Clause 2(62))• New Concept of “Small Company” - will have relatively less

burdensome compliance requirements. Small Company will have paid up capital not exceeding Rs. 50 lakhs or turnover not exceeding Rs. 20 Crores as may be prescribed(Clause 2(85))

• Maximum number of members for a private company increased from existing 50 to 200

• Concept of dormant companies introduced. Such companies will remain on register of companies with minimum compliance requirements without carrying on any operation

• Definition of Foreign Company expanded to include companies having place of business directly or through its agent, physically or through electronic mode, and conducting business in India in any manner

• Multi layered structuring of subsidiary companies sought to be regulated by prescribing maximum number of layers.

REGISTERED OFFICE (CLAUSE 12)

• Every company must have a Registered Office address within 15 days of incorporation where it will receive notices, addresses and communications

• Within 30 days of incorporation, company has to furnish verification of the registered office in the prescribed manner to the Registrar

• In case of change of registered office address, company has to furnish to the Registrar verified in the prescribed manner, the details of the change of the registered office address.

• The requirements relating to verification of registered office address has already been introduced in the newly notified Form 18 under the existing Companies Act, 1956

ISSUE OF SECURITIES• The Bill governs the issue of all types of securities, not

only shares and debentures. • Contents of prospectus have been made more

detailed. • “Private Placement” can be made to not more than 50

shareholders. Any issue of securities to more than 50 shareholders shall be regarded as public offer and SEBI guidelines would apply to it.

• Return of allotment to be filed for issuance of all types of securities

• Companies cannot issue shares at discount other than as sweat equity.

DEPOSITS (CLAUSE 73)

• Approval of shareholders required• Credit Rating• Circular to be issued to members and file with the Registrar

within 30 days before the date of issue of circular• Provision for deposit insurance• Provision for creation of security in respect of interest and

creation of mortgage / charge on company’s properties and assets

• Rules to be framed in consultation with RBI by the CG• Provision for application to NCLT in the event of failure of

company to repay deposit or pay interest • Penal provisions for violation made extremely stringent

MORTGAGES AND CHARGES (CHAPTER VI)

• Responsibility to file particulars of charges created / modified within 30 days

• Registrar has power to extend the period up to 300 days on sufficient cause being shown

• Provision made for charge holder to file particulars of charges, if company does not file the same

• Company to file intimation of satisfaction of charges within 30 days.

• Registrar to send notice (14 days) to charge holder regarding satisfaction of charges if satisfaction document not signed by charge holder.

• Company to keep particulars of charges created, modified and satisfied at its registered office

E GOVERNANCEEnabling provisions for E Governance with respect to :-•Maintenance and inspection of documents in electronic form•Option of keeping of books of accounts in electronic form•financial statements to be placed on company’s website•Holding of board meetings through video conferencing/other electronic mode•Electronic Voting

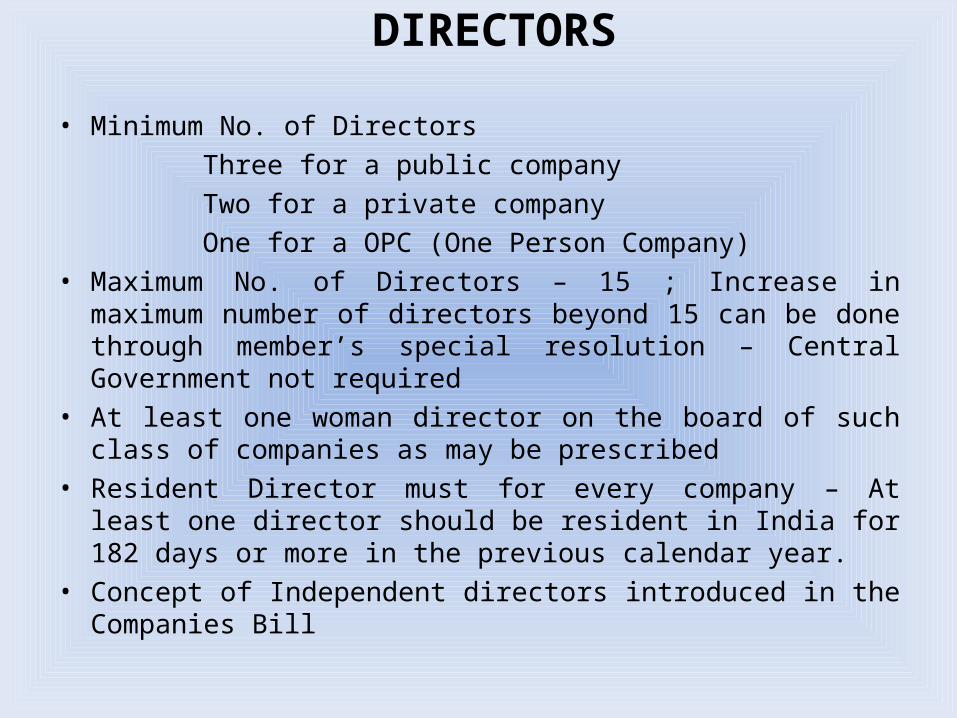

DIRECTORS

• Minimum No. of Directors Three for a public company Two for a private company One for a OPC (One Person Company)• Maximum No. of Directors – 15 ; Increase in maximum number of

directors beyond 15 can be done through member’s special resolution – Central Government not required

• At least one woman director on the board of such class of companies as may be prescribed

• Resident Director must for every company – At least one director should be resident in India for 182 days or more in the previous calendar year.

• Concept of Independent directors introduced in the Companies Bill

INDEPENDENT DIRECTOR• Independent director clearly defined in the Bill• At least one third of directors of a listed

company should be independent directors• Certain class or classes of public companies

will also have to appoint independent directors on the Board as may be prescribed by the Central Government

• Nominee director shall not be regarded as an independent director

• Independent director shall not be entitled to ESOP

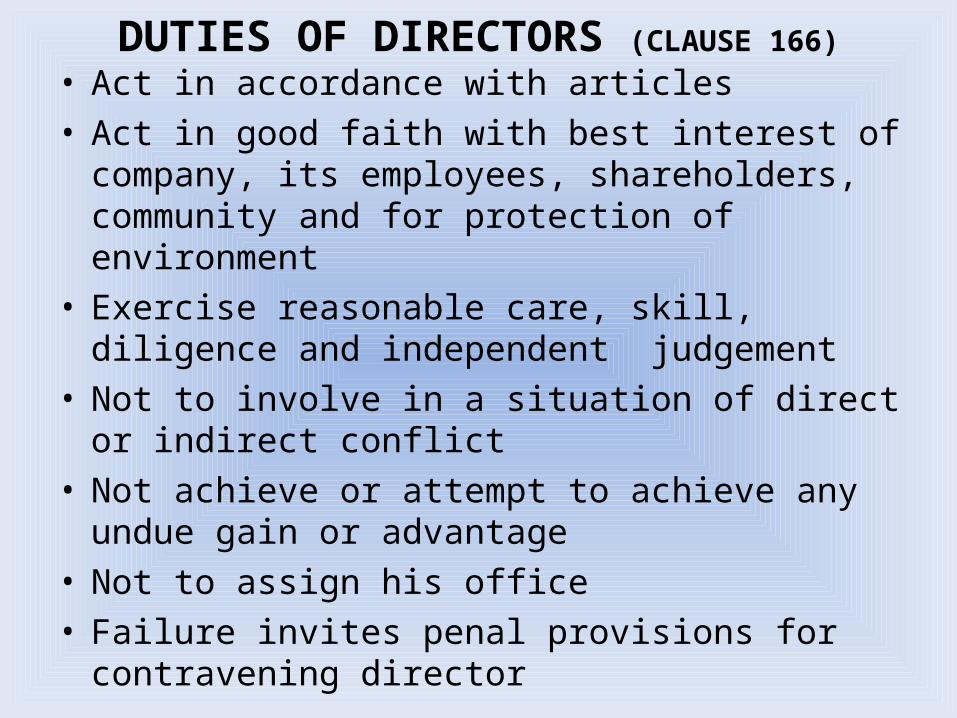

DUTIES OF DIRECTORS (CLAUSE 166)• Act in accordance with articles• Act in good faith with best interest of company, its

employees, shareholders, community and for protection of environment

• Exercise reasonable care, skill, diligence and independent judgement

• Not to involve in a situation of direct or indirect conflict

• Not achieve or attempt to achieve any undue gain or advantage

• Not to assign his office• Failure invites penal provisions for contravening

director

RESIGNATION OF DIRECTORS (CLAUSE 168)

• A director may resign by notice in writing. • Board to intimate Registrar about the

resignation and place the resignation before the general meeting of members

• Director concerned shall also forward a copy of the resignation along with the reasons to the Registrar within 30 days of his resignation

• The notice of resignation shall be effective from the date of its receipt by the company or if the notice mentions a date, then from such date whichever is later

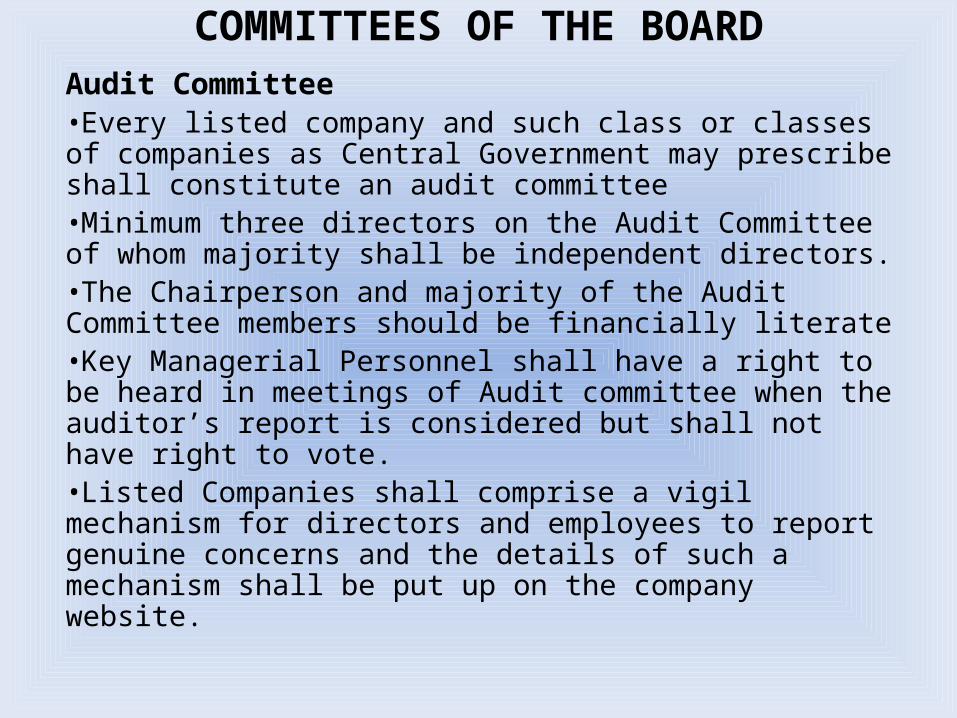

COMMITTEES OF THE BOARDAudit Committee•Every listed company and such class or classes of companies as Central Government may prescribe shall constitute an audit committee•Minimum three directors on the Audit Committee of whom majority shall be independent directors.•The Chairperson and majority of the Audit Committee members should be financially literate•Key Managerial Personnel shall have a right to be heard in meetings of Audit committee when the auditor’s report is considered but shall not have right to vote.•Listed Companies shall comprise a vigil mechanism for directors and employees to report genuine concerns and the details of such a mechanism shall be put up on the company website.

OTHER COMMITTEES OF THE BOARD

• Nomination and Remuneration Committee

• Stakeholder Relationship Committee• Corporate Social Responsibility (CSR)

Committee

CORPORATE SOCIAL RESPONSIBILITY (CLAUSE 135)

• Following Companies Shall constitute a CSR Committee: Net worth of rupees five hundred crore or more, or Turnover of rupees one thousand crore or more, or Net profit of rupees five crore or more • Committee to consist of at least three directors out of which

at least one should be independent director • Committee to formulate and recommend to the Board a CSR

policy indicating the activities to be undertaken (as specified in Schedule Vii) and recommend amount of expenditure to be incurred on these activities

• Board to ensure that at least 2% of the average net profits of last 3 years is spent by the company on CSR activities every financial year, else reasons for not spending to be specified in the Board’s report.

BOARD MEETINGS (CLAUSE 173)

• 7 Days Notice for a Board Meeting. Shorter notice subject to the condition that at least one independent director is present – otherwise decisions taken are final only if ratified by at least one independent director

• First Board meeting should be held within 30 days of incorporation

• Gap between two board meetings shall not be longer than 120 days

• Participation through video conferencing as per guidelines and rules prescribed will be permitted. C.G. may make rules providing for the items of business which can be transacted through video conferencing or other electronic mode.

• Certain relaxations for Small company and OPC

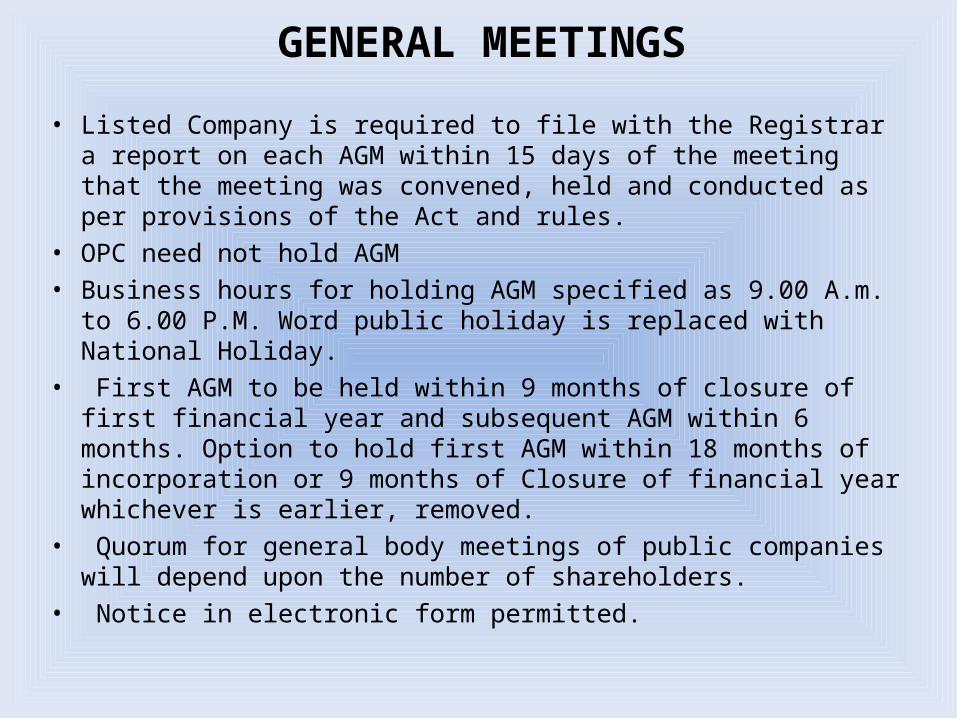

GENERAL MEETINGS

• Listed Company is required to file with the Registrar a report on each AGM within 15 days of the meeting that the meeting was convened, held and conducted as per provisions of the Act and rules.

• OPC need not hold AGM• Business hours for holding AGM specified as 9.00 A.m. to 6.00 P.M.

Word public holiday is replaced with National Holiday. • First AGM to be held within 9 months of closure of first financial

year and subsequent AGM within 6 months. Option to hold first AGM within 18 months of incorporation or 9 months of Closure of financial year whichever is earlier, removed.

• Quorum for general body meetings of public companies will depend upon the number of shareholders.

• Notice in electronic form permitted.

ELECTRONIC VOTING AND POSTAL BALLOT

• Voting by electronic means introduced ; Central Government may prescribe the class(es) of company(ies) and the manner in which a member may exercise right to vote (Clause 108)

• Central Government may prescribe Matters which have to be compulsorily transacted by way of

postal ballot Matters which may be transacted by way of postal ballot

other than items of ordinary business and where directors or auditors have a right to be heard (Clause 110)

SECRETARIAL STANDARDS (CLAUSE 118(10) READ WITH 205)

• Every company shall observe Secretarial Standards with respect to General and Board Meetings

• The Secretarial Standards shall be specified by the Institute of Company Secretaries of India and approved by the Central Government

• Duty of company secretary to ensure that company complies with the Secretarial Standards

• Beginning of a new era in which non financial standards are given importance.

KEY MANAGERIAL PERSONNEL (KMP) (Clause 203(1))

• Means CEO, CFO, Company Secretary, Whole time Director and such other officer as may be prescribed

• Such class of company or companies as may be prescribed shall have the following whole time managerial personnel :-– MD or CEO or Manager and in their absence a Whole Time

Director– Company Secretary

• The appointment of KMP shall be by a Board resolution which will outline the terms and conditions of the appointment

• The vacancy in the office of KMP shall be filled up within a period of six months from the date of such vacancy

MANAGERIAL REMUNERATION (CLAUSE 97)

• Ceiling of 11% on Net Profits for Managerial Remuneration continue to be applicable to Directors, Managing Director, Whole Time Director and Manager

• For Companies with no or inadequate profits, remuneration shall be payable in accordance with Schedule V, which provides a table containing maximum remuneration payable depending upon effective capital of the company

• Payment of remuneration not in accordance with Schedule V would require approval of the Central Government.

• Independent directors not entitled to Stock Options, but may get payment of fee and profit linked commission subject to limits in the Bill / rules

• Insurance Premium paid by company on behalf of its KMP for indemnifying them against any liability arising out of their duties shall not be treated as part of remuneration

FINANCIAL STATEMENTS (CLAUSE 129)

• The term financial statements is defined to include Balance Sheet, P&L, Cash Flow, statement of changes in equity and explanatory note forming part of these documents

• Financial year shall end on 31st March every year - Two years given for companies to change

• Financial statements shall comply with the notified accounting standards

• Holding Companies have to compulsorily consolidate the accounts of subsidiaries (Subsidiaries for the purpose include associate company and Joint venture company) and also place a statement of its subsidiaries before the members

• Central Government empowered to provide for consolidation of accounts and financial statements in such manner as may be prescribed

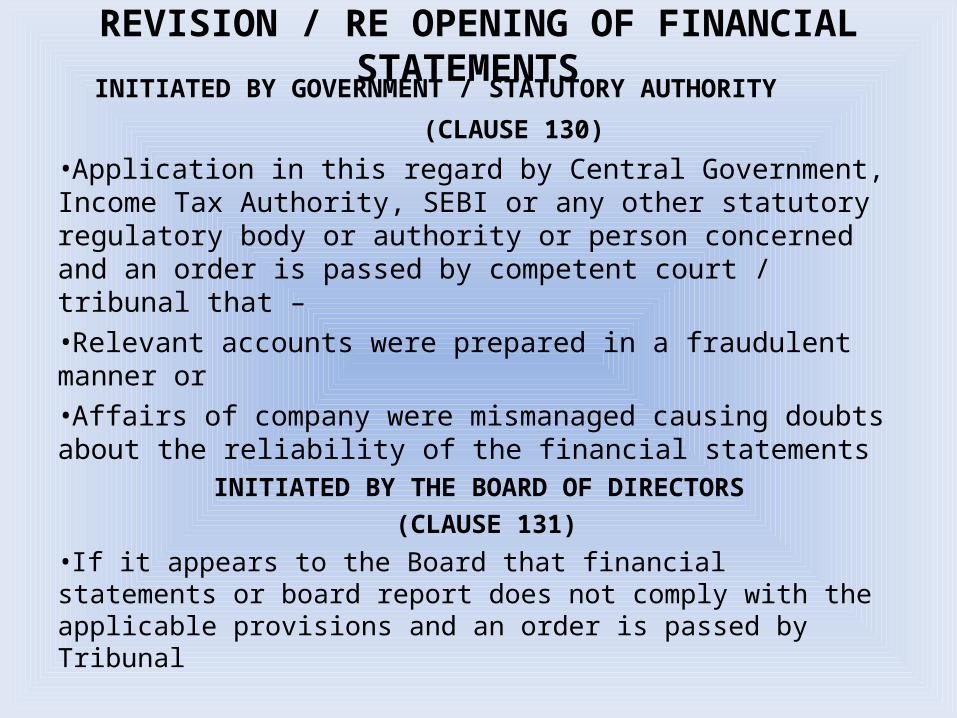

REVISION / RE OPENING OF FINANCIAL STATEMENTS INITIATED BY GOVERNMENT / STATUTORY AUTHORITY

(CLAUSE 130)

•Application in this regard by Central Government, Income Tax Authority, SEBI or any other statutory regulatory body or authority or person concerned and an order is passed by competent court / tribunal that –•Relevant accounts were prepared in a fraudulent manner or•Affairs of company were mismanaged causing doubts about the reliability of the financial statements

INITIATED BY THE BOARD OF DIRECTORS (CLAUSE 131)

•If it appears to the Board that financial statements or board report does not comply with the applicable provisions and an order is passed by Tribunal

NATIONAL FINANCIAL REPORTING AUTHORITY (CLAUSE 132)

• Central Government empowered to constitute a National Financial Reporting Authority (NFRA) to provide for matters relating to accounting and auditing standards.

• Functions of NFRA include :- Recommending of accounting and auditing policies and standards

for adoption by class of companies or their auditors Monitoring and enforcing compliance of accounting and auditing

standards Oversee quality of services rendered by professionals associated

with ensuring compliance of standards Perform such other functions as may be prescribed

RELATED PARTY TRANSACTIONS (CLAUSE 188)

Provisions for rotation of auditors and audit firms (Clause 139)

•Applicable to listed company and such class or class of companies as may be prescribed•An individual may be appointed up to a period of five years•An audit firm may be appointed for two terms of five consecutive years•After completion of the audit term the auditor (individual or firm) shall not again be re-appointed for a period of five years. The restriction also applies to audit firms having common partners•Members have a right to provide for rotation of audit partners and the audit team •Members also have right to appoint joint auditors•Existing company shall comply with these provisions within a period of 3 years from the commencement of this Act•Central Government empowered to frame rules relating to rotation of auditors

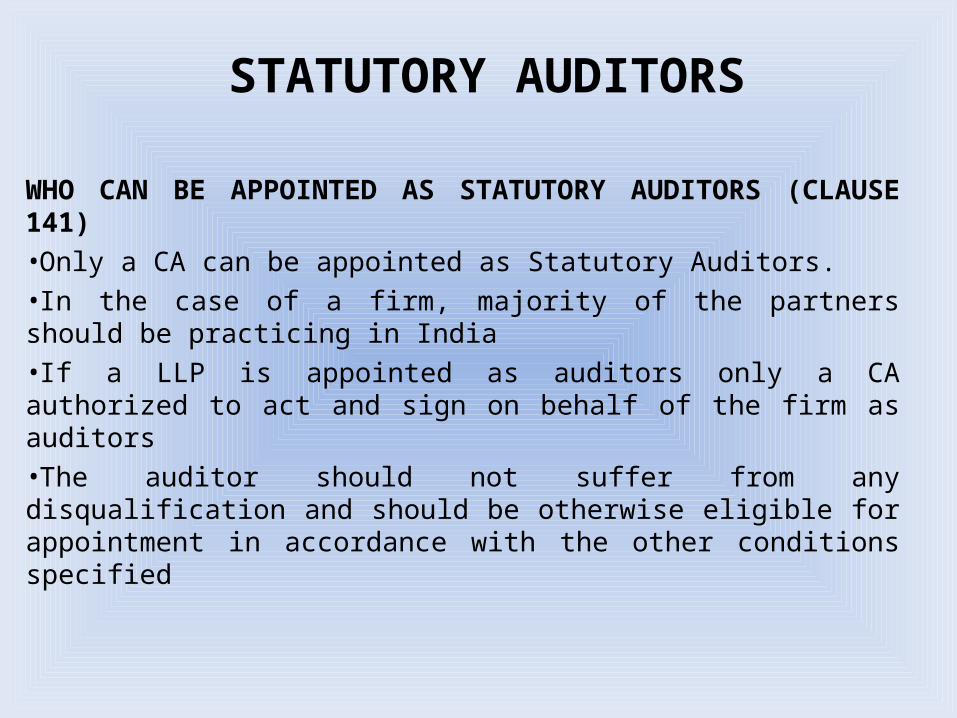

STATUTORY AUDITORS

WHO CAN BE APPOINTED AS STATUTORY AUDITORS (CLAUSE 141)•Only a CA can be appointed as Statutory Auditors. •In the case of a firm, majority of the partners should be practicing in India•If a LLP is appointed as auditors only a CA authorized to act and sign on behalf of the firm as auditors•The auditor should not suffer from any disqualification and should be otherwise eligible for appointment in accordance with the other conditions specified

STATUTORY AUDITORS (Continued)

Auditors not to provide certain specified services (Clause 144)

•An auditor may provide such other services as may be approved by Board or the Audit Committee but shall not provide the following services to the company, its subsidiary, or its holding company directly or indirectly :-

Accounting and Book Keeping

Internal Audit Financial Information System

Actuarial Services Investment Advisory Services

Investment Banking Services

Outsourced financial services

Management Consultancy Services

Other services as prescribed

• Stringent Penal Provisions for violation provided in Clause 147

DIRECTORS REPORT (CLAUSE 134)Extensive disclosures have been provided for. In addition to existing requirements, the following disclosures :-•Extract of Annual Return•Number of Board Meetings•A report of Remuneration Committee•Declaration of Independent directors•Particulars of loans, guarantees or investments made•Particulars of contracts or arrangements entered into•Details of CSR Initiatives•Statement indicating development and implementation of risk management policy•In the case of listed companies and companies having such paid up capital as may be prescribed, manner of performance evaluation of the Board Members•Comments on qualification or reservation made by CS in the Secretarial Audit Report

SECRETARIAL AUDIT (CLAUSE 204)

• Mandated for every listed company and a company belonging to such other class of companies as may be prescribed

• Expected to significantly enlarge scope for Practicing Company Secretary (PCS)

• Company to give all assistance and facilities to PCS

• Board to explain in full any qualification or observation or other remarks made in the PCS in his report.

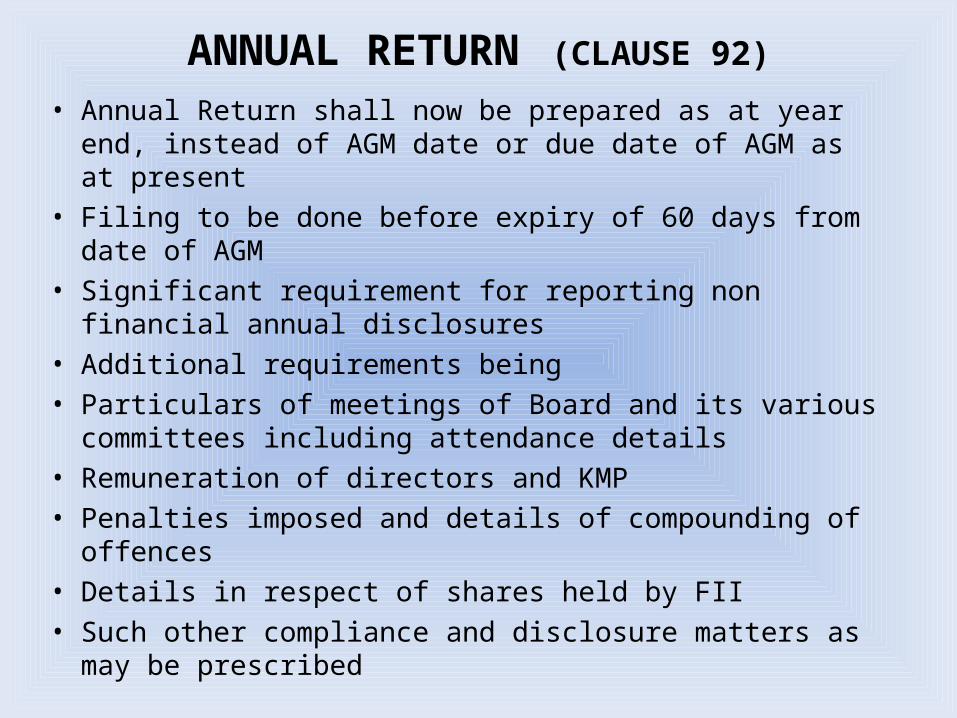

ANNUAL RETURN (CLAUSE 92)

• Annual Return shall now be prepared as at year end, instead of AGM date or due date of AGM as at present

• Filing to be done before expiry of 60 days from date of AGM• Significant requirement for reporting non financial annual

disclosures • Additional requirements being • Particulars of meetings of Board and its various committees

including attendance details• Remuneration of directors and KMP• Penalties imposed and details of compounding of offences• Details in respect of shares held by FII• Such other compliance and disclosure matters as may be

prescribed

CERTIFICATION / SIGNING OF ANNUAL RETURN (CLAUSE 92 CONTINUED)

• Certification of Annual Return is similar to the existing compliance certificate under Section 383A of the Companies Act

• Annual Return is required to be signed by a director and Company Secretary or where there is no Company Secretary by a Secretary in Whole Time Practice

• Annual Return is required to be certified by a Secretary in Whole Time Practice even if the same is signed by the Whole Time Secretary of the company in case of a listed company and such other companies having such paid up capital and turnover as may be prescribed.

INTERNAL AUDIT (CLAUSE 138)

• Appointment of Internal Auditor by certain class or classes of companies as may be prescribed

• Internal Auditor shall be either CA or CMA or such other professional as may be decided by the Board of Directors

• Central Government authorized to prescribe rules regarding intervals in which internal audit will be conducted and reported to the Board.

COST ACCOUNTS AND COST AUDIT (CLAUSE 148)

• Scope for maintenance of cost accounts enlarged to include companies engaged in provision of such services as may be prescribed

• Central Government empowered to direct cost audit for such class of companies as it considers necessary

• Central Government while issuing directions for cost audit shall prescribe the criteria of “Turnover” or “Net Worth”

• The Audit shall be conducted by a Cost Accountant in Practice to be appointed by the Board of Directors

• Remuneration of cost auditors to be determined by members

• Central Government approval for appointment of cost auditors not required

INSPECTION, ENQUIRY AND INVESTIGATION• Existing provisions strengthened• New Clause 221 provides for investigation into the affairs

of the company on reference by Central Government or complaint by specified no. of members or creditorsthat transfer or disposal of funds, properties or assets is

likely to take place, which is prejudicial to the interests of the company , then Tribunal may consider such cases and is empowered to order freezing of such transfer, removal or disposal of assets for a period of three years.

• New Clause 228 provides for inspection and investigation shall also mutatis mutandis apply to inspection or investigation of foreign companies

CLASS ACTION SUIT

• New Proviso enabling specified number of members or Depositors• to file application before Tribunal , if they are of

the opinion that management or control of the affairs of the company are being conducted in a manner prejudicial to the interests of the company / members / creditors

• Order passed by Tribunal on such application shall be binding on the company and all its members and depositors.

SERIOUS FRAUD INVESTIGATION OFFICE (SFIO)

• Statutory status proposed for SFIO• Investigation report of SFIO shall be treated as a

report filed by police officer• SFIO shall power to arrest in respect of certain

offences of the Bill which attract the punishment for fraud

• Stringent penal provisions for fraud related offences• Fraud shall have meaning as defined in Clause 447

COMPROMISE AND ARRANGEMENTS

• Matters relating to Mergers and Amalgamation will now be with National Company Law Tribunal (Tribunal) before whom CA/CMA/CS can appear in addition to advocates as authorized representatives

• Simplified procedure for amalgamation involving • Holding / subsidiary companies• Two Small Companies• Prescribed class of such other companies• without having to apply before Tribunal, if the scheme is approved

by members and creditors and no objection is received from Central Government, Registrar and Official Liquidator

• Merger and Amalgamations now possible involving companies registered in India and those registered abroad subject to rules prescribed by Central Government in consultation with RBI

COMPROMISE AND ARRANGEMENTS (continued)

• Objection to compromise / arrangement can be made by persons having at least 10% of shareholding or 5% of total outstanding debt as per latest audited financials

• Notice of meeting to consider scheme to be sent to Central Government, Income Tax Authorities and Registrar

• Notice of meeting to be sent also to SEBI, Stock Exchanges , RBI, Official Liquidator, Competition Commission of India and other sector regulators or authorities who are affected by the proposed scheme

• Representations from the above mentioned authorities to be received within 30 days, otherwise, it will be presumed they have no objection

• Mandatory to send valuation report to all the aforementioned authorities, as applicable in case of mergers and amalgamations

• Accounting treatment should comply with prescribed accounting standards and auditor’s certificate to be filed with Tribunal.

RESTRUCTURING AND LIQUIDATION

• The entire rehabilitation and liquidation process has been made time bound (Clause 254)

• Winding up is to be resorted only when revival is not feasible

• Tribunal is empowered to appoint an interim administrator or a Company Administrator from the panel of CA / CMA / CS

• Company Administrator to prepare a scheme of revival and rehabilitation

• If revival scheme is not approved, Tribunal shall order for winding up

RESTRUCTURING AND LIQUIDATION (continued)

COMPANY LIQUIDATORS•The Tribunal may appoint Provisional Liquidator of the company till the making of the Winding up order (Clause 273)•Provisional Liquidator or the Company Liquidator, as the case may be shall be appointed from a panel of CS, CA, CMA, Advocates or firms or bodies corporate having these professionals as may be notified by the Central Government (Clause 275)•The Company Liquidator may with the sanction of Tribunal appoint one or more professionals to assist him in the performance of his duties and functions (Clause 291)

COMPANY LAW TRIBUNAL AND APPELLATE TRIBUNAL

• Clause 408 provides for constitution of a National Company Law Tribunal and such number of technical and judicial members as Central Government may deem it necessary

• Clause 410 provides for constitution of an Appellate Tribunal consisting of a Chairperson and such number of members not exceeding eleven as deemed fit by the Central Government for hearing appeals against orders of the Tribunal

• Clause 419 provides for constitution of such number of benches as may be specified by the Central Government

• Clause 422 provides for expeditious disposal of all matters referred to Tribunal and Appellate Tribunal within 3 months of their reference. Also provides for reasons to be recorded in writing if matter cannot be disposed of within 3 months and may extend up to a further period of 90 days

CONSTITUTION OF SPECIAL COURTS

• Central Government empowered to establish special courts in consultation with the Chief Justice of High Court within whose jurisdiction the judge is to be appointed.

• All offences under this Act shall be tried by the Special Court established for the area in which the registered office of the company is in relation to which the offence is committed and if there are more special courts than one for such area, by such one of them as may be specified in this behalf by the High Court concerned

• Special Court would have the liberty to try summary proceedings for offences punishable with imprisonment for a term not exceeding three years. But sentence for imprisonment cannot exceed a term of one year.

OPPORTUNITIES FOR PROFESSIONALS

SKYIS

THE LIMIT

Thank You