communisis plc – interim report 2011 · combined results demonstrate the strength of the msp...

TRANSCRIPT

Communisis plc – Interim Report 2011

C M

Y K

PMS ???

PMS ???

PMS ???

PMS ???

Non-print 1

Non-print 2

JOB LOCATION:

PRINERGY 3

Non-printingColours

COM111-InterimRep-11.indd 1 05/08/2011 14:52

Communisis plc – Interim Report 2011

2

Contents

BusIness RevIewFinancial and operational Highlights 3Chief executive’s Review 4Financial Performance Report 8

FInanCIal statementsConsolidated Income statement 11Consolidated statement of Comprehensive Income 12Consolidated Cash Flow statement 13Consolidated Balance sheet 14Consolidated statement of Changes in equity 15

notes to the Financial statements

1 segmental information 162 net finance costs 173 Income tax 174 earnings per share 175 Dividends paid and proposed 186 Cash generated from operations 197 acquisitions 198 Directors’ responsibility statement 199 Risks and uncertainties 2010 additional information 20

• operating profit before exceptional items increased by 27% to £3.6m (H1 2010 £2.8m)

• operating margin increased to 4.4% (H1 2010 3.3%)

• Change in mix of revenue and contribution between segments. Combined results demonstrate the strength of the msP proposition

• operating cash inflow before restructuring costs increased by £3.4m to £5.0m (H1 2010 £1.6m)

• Investments in business acquisitions of £6.8m increased net debt in H1 2011 to £23.6m (FY 2010 £15.8m)

• earnings per share up 17% at 1.85p (H1 2010 1.58p)

• Interim dividend 16% higher at 0.5p (H1 2010 0.43p)

FInanCIal HIgHlIgHts

COM111-InterimRep-11.indd 2 05/08/2011 14:52

Communisis plc – Interim Report 2011

3

FInanCIal anD oPeRatIonal HIgHlIgHts

• operating profit before exceptional items increased by 27% to £3.6m (H1 2010 £2.8m)

• operating margin increased to 4.4% (H1 2010 3.3%)

• Change in mix of revenue and contribution between segments. Combined results demonstrate the strength of the msP proposition

• operating cash inflow before restructuring costs increased by £3.4m to £5.0m (H1 2010 £1.6m)

• Investments in business acquisitions of £6.8m increased net debt in H1 2011 to £23.6m (FY 2010 £15.8m)

• earnings per share up 17% at 1.85p (H1 2010 1.58p)

• Interim dividend 16% higher at 0.5p (H1 2010 0.43p)

FInanCIal HIgHlIgHts

wInnIng new CustomeRs

• Procter & gamble – significant contract secured for marketing services at £10m revenue per annum, extending our footprint from the uK into several countries in mainland europe

• BBC tv licensing – Contract secured for four year term at £4.5m revenue per annum. Related acquisition of orchestra Bristol which has also brought other new customer opportunities

• virgin media, speedy Hire, Premium Credit, iReD and several mutual customers – other new wins across multiple sectors resulting from a strengthened sales and account management capability and growing customer receptiveness to the msP proposition

extenDIng ouR seRvICes

• Four-fold increase in customers taking our postal services offering; delivered in partnership with tnt

• major increase in access to credit data through an extended contract with equifax, leading to the launch of a new range of marketing products

tRansFoRmIng ouR DelIveRY CaPaBIlItIes

• second high-speed colour digital output platform, now fully operational

• Further investment in technology and new skills

• new london office opened incorporating data and creative services

• Consolidation of leicester logistics facility into newcastle completed. Further restructuring of Direct mail and central overhead functions planned for H2 2011

• overall number of sites will be reduced from 14 to 9 by the end of 2011

oPeRatIonal HIgHlIgHts

17% InCRease In eaRnIngs PeR sHaRe

27% InCRease In oPeRatIng PRoFIt BeFoRe exCePtIonals

16% InCRease In InteRIm DIvIDenD to 0.5p

COM111-InterimRep-11.indd 3 05/08/2011 14:52

Communisis plc – Interim Report 2011

4

New busINess wINs aCRoss multIple seCtoRs

CoNtINuINg INvestmeNt IN teChNology aNd skIlls

stRategy woRkINg aNd delIveRINg gRowth

we aRe makINg good pRogRess agaINst ouR plaNs to gRow aNd tRaNsfoRm the busINess aNd thIs CoNfIdeNCe Is RefleCted IN aN INCRease IN the INteRIm dIvIdeNd

ChIef exeCutIve’s RevIew

summaRy

It is encouraging to report that our results in the first half of 2011 were on target and considerably ahead of the same period last year. the marketing services sector is going through a period of rapid change and our model is proving appropriate and resilient. most importantly we can evidence further progress in the transformation of Communisis.

the board would like to thank each employee for the contribution they have made in delivering this strong performance.

what we do

Communisis is a leading marketing services provider (“msp”) which provides services that support its customers’ marketing programmes and transactional communications.

Communisis offers a broad range of services that can be delivered either separately or in combination to make its customers’ communications more targeted and more efficient and therefore more effective and more profitable.

the services include:• the overall development of integrated offline and online

marketing strategies;

• the acquisition, analysis and management of lifestyle and credit data, to generate target lists of prospects for marketing campaigns;

• the design, creation and management of customer content that is used to produce the documents that convey the marketing messages;

• the application of software tools to manage marketing campaigns on behalf of customers and to source materials;

• the production and distribution of highly personalised marketing and transactional documents; and

• the management of responses to marketing messages and the measurement of their effectiveness.

these services are managed through two strategic business units, Intelligence driven Communications (“IdC”) which is an integrated services business concentrated around the data, creative and digital marketing aspects of the msp proposition and specialist production and sourcing (“sps”) which focuses on product delivery.

the total addressable market for Communisis is primarily the direct marketing budget of large to medium-sized businesses that sit within the ftse 500 or the private equivalents of similar size. direct marketing remains one of the strongest forms of communication available to businesses because of its flexibility and the ease with which return on investment can be measured. we are investing in new capabilities in direct marketing that are trending positively, especially in digital media services.

ChIef exeCutIve’s RevIew

COM111-InterimRep-11.indd 4 08/08/2011 11:10

Communisis plc – Interim Report 2011

5

we aRe maKIng gooD PRogRess agaInst ouR Plans to gRow anD tRansFoRm tHe BusIness anD tHIs ConFIDenCe Is ReFleCteD In an InCRease In tHe InteRIm DIvIDenD

CHIeF exeCutIve’s RevIew

summaRY

It is encouraging to report that our results in the first half of 2011 were on target and considerably ahead of the same period last year. the marketing services sector is going through a period of rapid change and our model is proving appropriate and resilient. most importantly we can evidence further progress in the transformation of Communisis.

the Board would like to thank each employee for the contribution they have made in delivering this strong performance.

wHat we Do

Communisis is a leading marketing services Provider (“msP”) which provides services that support its customers’ marketing programmes and transactional communications.

Communisis offers a broad range of services that can be delivered either separately or in combination to make its customers’ communications more targeted and more efficient and therefore more effective and more profitable.

the services include:• the overall development of integrated offline and online

marketing strategies;

• the acquisition, analysis and management of lifestyle and credit data, to generate target lists of prospects for marketing campaigns;

• the design, creation and management of customer content that is used to produce the documents that convey the marketing messages;

• the application of software tools to manage marketing campaigns on behalf of customers and to source materials;

• the production and distribution of highly personalised marketing and transactional documents; and

• the management of responses to marketing messages and the measurement of their effectiveness.

these services are managed through two strategic business units, Intelligence Driven Communications (“IDC”) which is an integrated services business concentrated around the data, creative and digital marketing aspects of the msP proposition and specialist Production and sourcing (“sPs”) which focuses on product delivery.

the total addressable market for Communisis is primarily the direct marketing budget of large to medium-sized businesses that sit within the Ftse 500 or the private equivalents of similar size. Direct marketing remains one of the strongest forms of communication available to businesses because of its flexibility and the ease with which return on investment can be measured. we are investing in new capabilities in direct marketing that are trending positively, especially in digital media services.

asPIRatIon

our aspiration is to be the uK’s leading marketing services Provider with a growing customer-led international profile.

our aim is to improve profitability as measured by the margin of operating profit on sales so as to achieve double-digit returns over the medium term.

this will require investments in people, services and technology, both organically and by acquisition. we will also need to maintain our focus on winning higher margin services from both existing and new customers so as to continue to participate fully in the progressive migration of marketing and transactional communications from print to digital formats.

By continuing to make changes to our organisation and business processes, Communisis will have the right capabilities to satisfy our customers’ demands and an appropriate cost base from which to operate.

PRogRess agaInst Plan

gRowtH we have continued to broaden and deepen our range of services in the first half of 2011 through our partnership with tnt for postal solutions, announced in april, and our agreement with equifax for data services, announced in may. In June we completed the acquisition of the trade and assets of orchestra Bristol, coupled with the novation of the BBC television licence contract with Proximity, to help build volume activity across our sPs service areas.

the latest marketing services contract with Procter & gamble, secured in July, will allow us to develop our international expertise and support network in europe. we also continue to invest in technology and deliver the innovative solutions that are demanded by our customers, evidenced by the installation in april of a second high-speed colour digital output platform.

we have invested further in sales and account management skills and processes to support our new business development and growth plans.

Cost ReDuCtIonImplementing efficiency and cost reduction programmes is an essential part of our drive for improved profitability. Following the successful completion of the first phase of our restructuring and organisational change project, announced in november 2010, we embarked on the second phase in July 2011 with the next stage in the restructuring of our Direct mail operations in leeds, further site consolidation and additional headcount reduction, including certain of the employees that recently transferred from orchestra Bristol.

the closure of the leicester warehouse and the transfer of its operations to our newcastle facility has now been successfully completed. earlier in the year we moved to newly refurbished offices in central london, vacating and consolidating those previously occupied in the City and in Richmond. In the second half of 2011 we will close our eastcote and Rickmansworth offices and

CHIeF exeCutIve’s RevIew

COM111-InterimRep-11.indd 5 05/08/2011 14:52

Communisis plc – Interim Report 2011

6

transfer the activities to newcastle and london. we also plan to vacate what is currently a separate Head office building in leeds and relocate the group functions to the main leeds Direct mail operating site. Cumulatively this consolidation will take Communisis from a 14 site structure at the end of 2010 to a 9 site structure by the end of 2011.

Results

operating profits before exceptional items for the first half of 2011 met our overall expectations at £3.6m: a 27% improvement on 2010 and reflected an increase in the operating margin on sales (excluding pass through) from 3.3% to 4.4%. within these operating results the mix of segmental contribution changed with IDC being £0.6m lower and sPs being £0.9m higher than in the comparable period in 2010 whilst corporate costs reduced by £0.5m.

we report our numbers across two segments, IDC and sPs, but optimise the benefit to customers by delivering a range of services that combine the capabilities of both segments to solve their problems. this means that the mix of services can vary considerably across customers and from one reporting period to another, as marketeers adjust their communications programmes at short notice based on market and competitor dynamics. this combined offering is a key strength of the marketing services Provider proposition.

the market within which we operate has, as we anticipated, been cautious in the first half of 2011 with some customers delaying more complex strategic decisions in favour of short-term tactical ones. this has played to the strengths of our sPs business which has both the scale and dynamic production environment to cope with short-term change. In IDC it is taking longer to close some new business opportunities due to lengthening customer decision processes. we expect this trend to reverse partially in the second half, supported and substantiated by the benefits of our recent contract win with Procter & gamble, and of the new products that have been developed through our partnership agreement with equifax.

as previously announced, the Company completed a bank re-financing in February 2011 securing committed facilities until august 2014.

IDC PeRFoRmanCe RevIew operating profits within IDC were £1.5m which was £0.6m lower than in the same period in 2010.

our data and creative service areas were challenged as a result of customers being more prudent with marketing spend and being attracted by frequent, heavy discounting in advertising and media channels in which we do not operate. nevertheless, these services, when offered in combination with services from other parts of our group, have had some notable successes. the establishment of an onsite creative team alongside our already present marketing team at Barclays, for example, and the integration of our data and digital output services at RBsi demonstrate our strength in integrated solutions and our ability to deliver those to the largest and most demanding of customers.

we believe that our ability to deliver large parts of a customer’s campaign management process, deploying a combination of data, creative and specialised output and sourcing services gives Communisis a major strategic advantage.

an example of a significant piece of new business resulting from this approach is the three year contract with everything everywhere, announced at the beginning of the year. the contract is worth about £10m in revenue per annum and has the Communisis team based at the customer’s premises with direct and ready access to our marketing campaign management systems and internal and external supplier base.

Procter & gamble was also attracted to this model which is applicable in any geography and not dependant on Communisis’ office locations. the resulting contract is worth approximately £10m in revenue per annum and sees us provide an outsourced campaign management service not only in the uK, but also in germany, austria, switzerland and Italy. this is a major win for Communisis and takes us back into the international arena as the result of a strong customer-led relationship.

the partnership agreement with equifax, which was signed in may has provided us with access to a considerable volume of credit data and has also allowed us to bring a range of new and compelling products to the market.

Communisis now consolidates 20 different sources of data every month, comprising 80 million records, enabling our customers to benefit from even greater data granularity, accuracy and breadth. this data helps them to target increasingly sophisticated consumers in a manner that generates better returns on marketing spend.

we continue to invest in our account management and sales activities, recruiting staff with strong marketing services backgrounds, and in developing marketing services software that is more integrated and relevant to the needs of our customers. an early success has seen tesco deploy this technology for more efficient management and distribution of point of sale material to its uK stores. In april we also signed a consultancy agreement with the postal market leader tnt, to enable us to provide cost and service benefits to customers from the integration of manufacturing and postal processes. the number of customers taking this service from us has increased from 6 to 27 since the beginning of the year.

sPs PeRFoRmanCe RevIew operating profits within sPs were £4.0m which was £0.9m better than in the same period in 2010.

Performance in Direct mail and statements improved in the first half of 2011. our ability to source and produce increasingly sophisticated and personalised communications in high volumes sets us apart from our competitors.

securing the BBC television licence contract in June together with the associated acquisition of the trade and assets of orchestra Bristol helps us access more customers and grow the business more quickly. orchestra Bristol is a marketing services business which is involved in data and specialist high-integrity output in both direct mail and transactional applications. the BBC contract, which has four years left to run, with an estimated annual revenue of £4.5m, covers the mailings involved in the issuance of television licences.

Further new tenders have recently been won for a range of production, sourcing and distribution services with virgin media, speedy Hire, Premium Credit, iReD and the mutual sector in general with six building societies recently returning as customers.

our growth strategy requires focused investment in new equipment that will allow us to deliver high-speed colour digital solutions in a common configuration across our two major sites in leeds and liverpool. the opportunity exists to migrate our customer base to a digital platform over time so that we can take full advantage of the benefits that this advanced technology offers. Currently we produce approximately six billion a4 pages annually, approaching 10% are already full-colour digital and we expect this to stand at more than 50% in three years time. In april we commissioned a second high-speed colour digital output platform in leeds, which has doubled our capacity for highly personalised, volume communications, in anticipation of these changing market requirements.

new business wins have more than offset both the anticipated and ongoing reduction in revenue due to falling volumes from existing customers, which for planning purposes we estimate at around 10% per annum on average across the various output services, and the recently announced loss of a Direct mail contract with HsBC. However, continuing overcapacity in the market has resulted in a price competitive environment, putting margins under pressure. to counter this we will be making savings in the more traditional areas, such as Direct mail, and in central overheads. this restructuring is part of the ongoing plan that was first announced in november 2010 to ensure that our business has the appropriate structure to deliver our future strategy.

COM111-InterimRep-11.indd 6 05/08/2011 14:52

Communisis plc – Interim Report 2011

7

an example of a significant piece of new business resulting from this approach is the three year contract with everything everywhere, announced at the beginning of the year. the contract is worth about £10m in revenue per annum and has the Communisis team based at the customer’s premises with direct and ready access to our marketing campaign management systems and internal and external supplier base.

Procter & gamble was also attracted to this model which is applicable in any geography and not dependant on Communisis’ office locations. the resulting contract is worth approximately £10m in revenue per annum and sees us provide an outsourced campaign management service not only in the uK, but also in germany, austria, switzerland and Italy. this is a major win for Communisis and takes us back into the international arena as the result of a strong customer-led relationship.

the partnership agreement with equifax, which was signed in may has provided us with access to a considerable volume of credit data and has also allowed us to bring a range of new and compelling products to the market.

Communisis now consolidates 20 different sources of data every month, comprising 80 million records, enabling our customers to benefit from even greater data granularity, accuracy and breadth. this data helps them to target increasingly sophisticated consumers in a manner that generates better returns on marketing spend.

we continue to invest in our account management and sales activities, recruiting staff with strong marketing services backgrounds, and in developing marketing services software that is more integrated and relevant to the needs of our customers. an early success has seen tesco deploy this technology for more efficient management and distribution of point of sale material to its uK stores. In april we also signed a consultancy agreement with the postal market leader tnt, to enable us to provide cost and service benefits to customers from the integration of manufacturing and postal processes. the number of customers taking this service from us has increased from 6 to 27 since the beginning of the year.

sPs PeRFoRmanCe RevIew operating profits within sPs were £4.0m which was £0.9m better than in the same period in 2010.

Performance in Direct mail and statements improved in the first half of 2011. our ability to source and produce increasingly sophisticated and personalised communications in high volumes sets us apart from our competitors.

securing the BBC television licence contract in June together with the associated acquisition of the trade and assets of orchestra Bristol helps us access more customers and grow the business more quickly. orchestra Bristol is a marketing services business which is involved in data and specialist high-integrity output in both direct mail and transactional applications. the BBC contract, which has four years left to run, with an estimated annual revenue of £4.5m, covers the mailings involved in the issuance of television licences.

Further new tenders have recently been won for a range of production, sourcing and distribution services with virgin media, speedy Hire, Premium Credit, iReD and the mutual sector in general with six building societies recently returning as customers.

our growth strategy requires focused investment in new equipment that will allow us to deliver high-speed colour digital solutions in a common configuration across our two major sites in leeds and liverpool. the opportunity exists to migrate our customer base to a digital platform over time so that we can take full advantage of the benefits that this advanced technology offers. Currently we produce approximately six billion a4 pages annually, approaching 10% are already full-colour digital and we expect this to stand at more than 50% in three years time. In april we commissioned a second high-speed colour digital output platform in leeds, which has doubled our capacity for highly personalised, volume communications, in anticipation of these changing market requirements.

new business wins have more than offset both the anticipated and ongoing reduction in revenue due to falling volumes from existing customers, which for planning purposes we estimate at around 10% per annum on average across the various output services, and the recently announced loss of a Direct mail contract with HsBC. However, continuing overcapacity in the market has resulted in a price competitive environment, putting margins under pressure. to counter this we will be making savings in the more traditional areas, such as Direct mail, and in central overheads. this restructuring is part of the ongoing plan that was first announced in november 2010 to ensure that our business has the appropriate structure to deliver our future strategy.

Communisis is a significant supplier of cheques to the uK market. as such, we welcome the recent decision by the Payments Council to remove the immediate uncertainty surrounding the future of cheques by announcing that it has withdrawn plans for closing cheque clearing in 2018 and that cheques as a primary payment mechanism will be continued for as long as needed. the Payments Council confirmed that it will focus on making all payments fit for the 21st century by encouraging innovation in new and existing types of payments. we have significant long term contracts for the production of cheques with the majority of our financial services customers and continue to work with all interested parties to investigate such alternative payment solutions. we are also extending our capability in security print to other areas, such as payslips, prescription forms and match tickets to offset any reducing demand for cheques whilst also continuing to manage the cost base to maintain margins.

outlooK

the Board is confident that Communisis has the right balance of risks and opportunities to meet its expectations for full year results in 2011. looking ahead, 2012 and onwards will benefit from the full year effects of our new business development successes, delivered from a progressively restructured cost base.

andy BlundellChief executive26 July 2011

CHIeF exeCutIve’s RevIew

a PaRtneRsHIP agReement wItH equIFax Has PRovIDeD us wItH aCCess to a ConsIDeRaBle volume oF CReDIt Data anD alloweD us to BRIng new PRoDuCts to maRKet

COM111-InterimRep-11.indd 7 05/08/2011 14:52

Communisis plc – Interim Report 2011

8

PRoFItaBIlItY

the table below is an extract from the Company’s segmental profit and loss account.

Profit and Loss Account Half year Half year £m ended ended 30 June 30 June 2011 2010

Turnover IDC 11.3 12.9sPs 71.3 72.2Pass through 15.2 13.0 97.8 98.1

Operating profit before exceptional items IDC 1.5 2.1sPs 4.0 3.1Corporate costs (1.9) (2.4)

3.6 2.8

Operating margin IDC 13.3% 16.3%sPs 5.6% 4.3%excluding pass through 4.4% 3.3%

exceptional items (0.3) –

Operating profit after exceptional items 3.3 2.8Finance costs (0.4) (1.0)

Profit before tax 2.9 1.8tax (charge) credit (0.4) 0.4

Profit after tax 2.5 2.2

Earnings per share Basic (p) 1.85 1.58adjusted (p) 1.71 0.96

operating profit before exceptional items increased 27% to £3.6m on turnover that was broadly unchanged on the prior year period. this was achieved in challenging market conditions in which we have been successful in winning new business and managing the cost base, especially in the sPs segment, so that the overall margin on sales (excluding pass through) has improved from 3.3% in 2010 to 4.4% in 2011.

tHe oveRall Result DemonstRates tHe stRengtH oF tHe maRKetIng seRvICes PRovIDeR PRoPosItIon

FInanCIal PeRFoRmanCe RePoRtFInanCIal

PeRFoRmanCe RePoRt

oPeRatIng PRoFIt BeFoRe exCePtIonals uP 27% t0 £3.6m

oPeRatIng maRgIn on sales InCReaseD to 4.4%

COM111-InterimRep-11.indd 8 05/08/2011 14:52

Communisis plc – Interim Report 2011

9

PRoFItaBIlItY

the table below is an extract from the Company’s segmental profit and loss account.

Profit and Loss Account Half year Half year £m ended ended 30 June 30 June 2011 2010

Turnover IDC 11.3 12.9sPs 71.3 72.2Pass through 15.2 13.0 97.8 98.1

Operating profit before exceptional items IDC 1.5 2.1sPs 4.0 3.1Corporate costs (1.9) (2.4)

3.6 2.8

Operating margin IDC 13.3% 16.3%sPs 5.6% 4.3%excluding pass through 4.4% 3.3%

exceptional items (0.3) –

Operating profit after exceptional items 3.3 2.8Finance costs (0.4) (1.0)

Profit before tax 2.9 1.8tax (charge) credit (0.4) 0.4

Profit after tax 2.5 2.2

Earnings per share Basic (p) 1.85 1.58adjusted (p) 1.71 0.96

operating profit before exceptional items increased 27% to £3.6m on turnover that was broadly unchanged on the prior year period. this was achieved in challenging market conditions in which we have been successful in winning new business and managing the cost base, especially in the sPs segment, so that the overall margin on sales (excluding pass through) has improved from 3.3% in 2010 to 4.4% in 2011.

FInanCIal PeRFoRmanCe RePoRt

the mix of revenues in the first half of 2011 has been different from that experienced in 2010 so that the relative contributions from the two segments has changed with IDC being £0.6m lower and sPs being £0.9m higher than in the comparable period in 2010. the strength of the business lies in our ability to deliver a range of tailored services either individually or in combination to meet the particular requirements of each customer and the value of this flexible approach is reflected in the overall results. Both segments, whether people-based or capital intensive, have a degree of operational gearing with certain costs being fixed in the short to medium-term. any changes in the level and mix of turnover therefore have an impact on profitability. this is reflected in the first half results for IDC as margins have fallen with the reduction in turnover. we expect these to improve in the second half as turnover recovers to the level achieved in the comparable period in 2010.

the strong sPs performance is expected to continue in the second half so that the relative contributions of the two segments should be comparable to those achieved in the first half. as in 2010 the operating results should be weighted to the second half of the year. Corporate costs, which are £0.5m lower than in the comparable period in 2010, should remain broadly constant between the first and second halves of 2011.

the acquisition of the trade and assets of the orchestra Bristol business just before the end of the half year is not expected to have a material impact on the operating result for the year. the benefits, notably from the BBC television licence contract, will flow in 2012 and beyond as the operations are fully integrated. Certain expenses associated with the transaction have been treated as exceptional costs in the first half.

the second phase of our restructuring programme together with the redundancies at orchestra Bristol that were announced in July 2011, are expected to result in an exceptional charge of £2.8m in the second half of 2011, at a cash cost of around £2m, and are estimated to result in annual savings in excess of £2m when fully implemented, a substantial part of which will be reinvested in new skills.

Included within finance costs for the first half is a credit of £0.4m, being the difference between the expected return and the expected interest cost on the pension fund assets and liabilities respectively (2010 charge of £0.3m).

FInanCIal PeRFoRmanCe RePoRt

COM111-InterimRep-11.indd 9 05/08/2011 14:52

Communisis plc – Interim Report 2011

10

the tax charge has been reduced from the standard rate of 26.5% to an effective rate of 14.9% following the favourable settlement of prior year group relief claims. the tax credit in 2010 resulted from the successful resolution of an outstanding tax issue in respect of a former subsidiary based in the usa and the write-back of the associated provisions.

overall profit after tax has increased by 15.9% to £2.5m (2010 £2.2m). Basic earnings per share have increased by a slightly higher 17%, due to a buy back of shares for the ltIP scheme. adjusted earnings per share have increased by 78%, principally due to the elimination of the exceptional tax credits in 2010.

the Company paid dividends of 1.29p per share in respect of 2010 and will pay an interim dividend of 0.5p per share for 2011, an increase of 16.3% on the prior year. the dividend will be paid on 26 september 2011 to shareholders on the register at the close of business on 26 august 2011.

CasH Flow anD net DeBt

the table below summarises the Company’s principal cash flows.

Cash flow statement Half year Half year Year £m ended ended ended 30 June 30 June 31 Dec 2011 2010 2010

Profit from operations before exceptional items 3.6 2.8 7.9Depreciation and other non-cash items 3.4 3.0 6.4Increase in working capital (3.6) (2.8) (2.4)additional pension fund contributions – – (2.9)Interest and tax – (1.4) (2.8)

Net cash inflow from operating activities 3.4 1.6 6.2net capital expenditure (2.2) (0.4) (2.1)Business acquisitions (6.8) – –Contract acquisition – – (1.8)Debt arrangement fees (0.8) – –Dividends (1.2) (0.6) (1.2)other movements (0.2) (0.1) (0.1)

(Increase) decrease in net debt (7.8) 0.5 1.0Opening net debt (15.8) (16.8) (16.8)Closing net debt (23.6) (16.3) (15.8)

net debt (23.6) (16.3) (15.8)Finance lease creditor (3.0) (3.2) (3.3)unamortised borrowing costs 0.7 0.3 – (25.9) (19.2) (19.1)

ConsolIDateD InCome statement

for the half year ended 30 June 2011: unaudited

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 Note £000 £000 £000

Revenue 1 97,800 98,131 193,166 Changes in inventories of finished goods and work in progress (360) 599 842 Raw materials and consumables used (51,549) (52,070) (99,793) employee benefits expense (26,169) (28,285) (54,779) other operating expenses (12,815) (12,273) (24,713) Depreciation and amortisation expense (3,341) (3,295) (6,863) exceptional items (227) – (309)

Profit from operations 1 3,339 2,807 7,551

Analysed as: Profit from operations before exceptional items 3,566 2,807 7,860 Pensions etv settlement gain – – 2,585 exceptional restructuring costs – – (2,894) acquisition and set up costs (227) – –

Profit from operations 3,339 2,807 7,551

Finance revenue 612 137 205 Finance costs before exceptional items (965) (1,182) (2,277) Recycling of cash flow hedge – – (401) accelerated amortisation of debt issue costs – – (161)

Finance costs (965) (1,182) (2,839)

total finance costs 2 (353) (1,045) (2,634)

Profit before taxation 2,986 1,762 4,917 Income tax (expense) / credit 3 (445) 430 (497)

Profit for the period attributable to equity holders of the parent 2,541 2,192 4,420

Earnings per share 4 on profit for the period attributable to equity holders and from continuing operations

– basic 1.85p 1.58p 3.20p – diluted 1.76p 1.52p 3.08p

Dividend per share 5 – paid 0.860p 0.430p 0.860p – proposed 0.500p 0.430p 0.860p

Dividends paid and proposed during the period were £1.2 million and £0.7 million respectively (30 June 2010 £0.6 million and £0.6 million respectively, 31 December 2010 £1.2 million and £1.2 million respectively).

the accompanying notes are an integral part of these Consolidated Financial statements.

all income and expenses relate to continuing operations.

operating cash inflow at £3.4m was £1.8m higher than in the equivalent period in 2010. strong cash management more than offset the £1.6m cash cost of the restructuring programme announced in november 2010 and included within working capital. tax receipts during the period covered the interest payments, contributing to the overall improvement.

we continue to invest in both the IDC and sPs segments with the investments being reflected largely in payroll costs in IDC and in capital equipment in sPs. our commitment to leading technology was evidenced by the acquisition of a second high-speed digital colour platform in april 2011 at a cost of about £2.2m. this was financed under an operating lease, effectively taking the aggregate level of capital expenditure for the first half to around £4.5m.

the final payment of £5.5m under the ai (now renamed Communisis Data Intelligence) earn-out arrangement together with the initial consideration for the orchestra Bristol business of £1.3m represent significant investments in the acquisitive part of our growth strategy.

the £7.8m increase in net debt to £23.6m effectively reflects the funding of our cost reduction activities and our continuing investments in the future growth of the business, both of which are expected to contribute to an increase in future operating margins.

nigel HowesFinance Director26 July 2011

ouR CommItment to leaDIng teCHnologY was evIDenCeD BY tHe aCquIsItIon oF a seConD HIgH-sPeeD DIgItal ColouR PlatFoRm In aPRIl 2011

COM111-InterimRep-11.indd 10 05/08/2011 14:52

Communisis plc – Interim Report 2011

11

ConsolIDateD InCome statement

for the half year ended 30 June 2011: unaudited

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 Note £000 £000 £000

Revenue 1 97,800 98,131 193,166 Changes in inventories of finished goods and work in progress (360) 599 842 Raw materials and consumables used (51,549) (52,070) (99,793) employee benefits expense (26,169) (28,285) (54,779) other operating expenses (12,815) (12,273) (24,713) Depreciation and amortisation expense (3,341) (3,295) (6,863) exceptional items (227) – (309)

Profit from operations 1 3,339 2,807 7,551

Analysed as: Profit from operations before exceptional items 3,566 2,807 7,860 Pensions etv settlement gain – – 2,585 exceptional restructuring costs – – (2,894) acquisition and set up costs (227) – –

Profit from operations 3,339 2,807 7,551

Finance revenue 612 137 205 Finance costs before exceptional items (965) (1,182) (2,277) Recycling of cash flow hedge – – (401) accelerated amortisation of debt issue costs – – (161)

Finance costs (965) (1,182) (2,839)

total finance costs 2 (353) (1,045) (2,634)

Profit before taxation 2,986 1,762 4,917 Income tax (expense) / credit 3 (445) 430 (497)

Profit for the period attributable to equity holders of the parent 2,541 2,192 4,420

Earnings per share 4 on profit for the period attributable to equity holders and from continuing operations

– basic 1.85p 1.58p 3.20p – diluted 1.76p 1.52p 3.08p

Dividend per share 5 – paid 0.860p 0.430p 0.860p – proposed 0.500p 0.430p 0.860p

Dividends paid and proposed during the period were £1.2 million and £0.7 million respectively (30 June 2010 £0.6 million and £0.6 million respectively, 31 December 2010 £1.2 million and £1.2 million respectively).

the accompanying notes are an integral part of these Consolidated Financial statements.

all income and expenses relate to continuing operations.

operating cash inflow at £3.4m was £1.8m higher than in the equivalent period in 2010. strong cash management more than offset the £1.6m cash cost of the restructuring programme announced in november 2010 and included within working capital. tax receipts during the period covered the interest payments, contributing to the overall improvement.

we continue to invest in both the IDC and sPs segments with the investments being reflected largely in payroll costs in IDC and in capital equipment in sPs. our commitment to leading technology was evidenced by the acquisition of a second high-speed digital colour platform in april 2011 at a cost of about £2.2m. this was financed under an operating lease, effectively taking the aggregate level of capital expenditure for the first half to around £4.5m.

the final payment of £5.5m under the ai (now renamed Communisis Data Intelligence) earn-out arrangement together with the initial consideration for the orchestra Bristol business of £1.3m represent significant investments in the acquisitive part of our growth strategy.

the £7.8m increase in net debt to £23.6m effectively reflects the funding of our cost reduction activities and our continuing investments in the future growth of the business, both of which are expected to contribute to an increase in future operating margins.

nigel HowesFinance Director26 July 2011

FInanCIal statements

COM111-InterimRep-11.indd 11 05/08/2011 14:52

Communisis plc – Interim Report 2011

12

ConsolIDateD CasH Flow statement

for the half year ended 30 June 2011: unaudited

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 Note £000 £000 £000

Cash flows from operating activities Cash generated from operations 6 3,371 3,052 9,052 Interest paid (848) (998) (1,919) Interest received 71 91 110 Income tax received / (paid) 801 (480) (1,021)

Net cash flows from operating activities 3,395 1,665 6,222

Cash flows from investing activities acquisition of subsidiary undertakings (6,839) – – Contract acquisition – – (1,820) Purchase of property, plant and equipment (1,884) (845) (2,125) Proceeds from the sale of property, plant and equipment 19 638 669 Purchase of intangible assets (313) (258) (639)

Net cash flows from investing activities (9,017) (465) (3,915)

Cash flows from financing activities

Purchase of own shares (197) – – new borrowings 42,000 3,000 13,000 Repayment of borrowings (29,000) (7,000) (30,000) Debt arrangement fees (790) – – Dividends paid 5 (1,190) (595) (1,190)

Net cash flows from financing activities 10,823 (4,595) (18,190)

Net increase / (decrease) in cash and cash equivalents 5,201 (3,395) (15,883) Cash and cash equivalents at 1 January 3,202 19,178 19,178 exchange rate effects 24 (126) (93)

Cash and cash equivalents at end of period 8,427 15,657 3,202

Cash and cash equivalents consist of: Cash and cash equivalents 8,427 15,657 3,202

the accompanying notes are an integral part of these Consolidated Financial statements.

ConsolIDateD statement oF ComPReHensIve InCome

for the half year ended 30 June 2011: unaudited

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Profit for the period 2,541 2,192 4,420

exchange differences on translation of foreign operations 12 (21) (10) adjustments in respect of prior years due to change in tax rate – – (175) actuarial gains / (losses) on defined benefit pension plans 1,444 (6,965) 2,230 Income tax thereon (375) 1,950 (602) gain / (loss) on cash flow hedges taken directly to equity 8 (195) (151) Income tax thereon (2) 55 42 Recycling of cash flow hedge – – 401 Income tax thereon – – (112)

Other comprehensive income / (loss) for the period, net of tax 1,087 (5,176) 1,623

Total comprehensive income / (loss) for the period, net of tax 3,628 (2,984) 6,043

attributable to: equity holders of the parent 3,628 (2,984) 6,043

the accompanying notes are an integral part of these Consolidated Financial statements.

evIDenCe oF stRategY ImPRovIng long-teRm PRosPeCts oF tHe BusIness:

COM111-InterimRep-11.indd 12 05/08/2011 14:52

Communisis plc – Interim Report 2011

13

ConsolIDateD CasH Flow statement

for the half year ended 30 June 2011: unaudited

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 Note £000 £000 £000

Cash flows from operating activities Cash generated from operations 6 3,371 3,052 9,052 Interest paid (848) (998) (1,919) Interest received 71 91 110 Income tax received / (paid) 801 (480) (1,021)

Net cash flows from operating activities 3,395 1,665 6,222

Cash flows from investing activities acquisition of subsidiary undertakings (6,839) – – Contract acquisition – – (1,820) Purchase of property, plant and equipment (1,884) (845) (2,125) Proceeds from the sale of property, plant and equipment 19 638 669 Purchase of intangible assets (313) (258) (639)

Net cash flows from investing activities (9,017) (465) (3,915)

Cash flows from financing activities

Purchase of own shares (197) – – new borrowings 42,000 3,000 13,000 Repayment of borrowings (29,000) (7,000) (30,000) Debt arrangement fees (790) – – Dividends paid 5 (1,190) (595) (1,190)

Net cash flows from financing activities 10,823 (4,595) (18,190)

Net increase / (decrease) in cash and cash equivalents 5,201 (3,395) (15,883) Cash and cash equivalents at 1 January 3,202 19,178 19,178 exchange rate effects 24 (126) (93)

Cash and cash equivalents at end of period 8,427 15,657 3,202

Cash and cash equivalents consist of: Cash and cash equivalents 8,427 15,657 3,202

the accompanying notes are an integral part of these Consolidated Financial statements.

ConsolIDateD statement oF ComPReHensIve InCome

for the half year ended 30 June 2011: unaudited

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Profit for the period 2,541 2,192 4,420

exchange differences on translation of foreign operations 12 (21) (10) adjustments in respect of prior years due to change in tax rate – – (175) actuarial gains / (losses) on defined benefit pension plans 1,444 (6,965) 2,230 Income tax thereon (375) 1,950 (602) gain / (loss) on cash flow hedges taken directly to equity 8 (195) (151) Income tax thereon (2) 55 42 Recycling of cash flow hedge – – 401 Income tax thereon – – (112)

Other comprehensive income / (loss) for the period, net of tax 1,087 (5,176) 1,623

Total comprehensive income / (loss) for the period, net of tax 3,628 (2,984) 6,043

attributable to: equity holders of the parent 3,628 (2,984) 6,043

the accompanying notes are an integral part of these Consolidated Financial statements.

FInanCIal statements

COM111-InterimRep-11.indd 13 05/08/2011 14:52

Communisis plc – Interim Report 2011

14

ConsolIDateD statement oF CHanges In equItY

for the half year ended 30 June 2011: unaudited

Capital Cumulative Issued Share merger ESOP redemption translation Retained Total capital premium reserve reserve reserve adjustment earnings equity £000 £000 £000 £000 £000 £000 £000 £000

As at 1 January 2011 34,651 22 11,427 (338) 1,375 (162) 86,523 133,498 Profit for the period – – – – – – 2,541 2,541 other comprehensive income – – – – – 12 1,075 1,087

Total comprehensive income – – – – – 12 3,616 3,628 employee share option schemes: – value of services provided – – – – – – 102 102 Purchase of own shares – – – (197) – – – (197) Dividends paid – – – – – – (1,190) (1,190)

As at 30 June 2011 34,651 22 11,427 (535) 1,375 (150) 89,051 135,841

As at 1 January 2010 34,651 22 11,427 (338) 1,375 (152) 81,283 128,268 Profit for the period – – – – – – 2,192 2,192 other comprehensive loss – – – – – (21) (5,155) (5,176)

Total comprehensive loss – – – – – (21) (2,963) (2,984) employee share option schemes: – value of services provided – – – – – – 195 195 Dividends paid – – – – – – (595) (595)

As at 30 June 2010 34,651 22 11,427 (338) 1,375 (173) 77,920 124,884

As at 1 January 2010 34,651 22 11,427 (338) 1,375 (152) 81,283 128,268 Profit for the year – – – – – – 4,420 4,420 other comprehensive loss – – – – – (10) 1,633 1,623

Total comprehensive loss – – – – – (10) 6,053 6,043 employee share option schemes: – value of services provided – – – – – – 377 377 Dividends paid – – – – – – (1,190) (1,190)

As at 31 December 2010 34,651 22 11,427 (338) 1,375 (162) 86,523 133,498

the accompanying notes are an integral part of these Consolidated Financial statements.

ConsolIDateD BalanCe sHeet

30 June 2011: unaudited

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

ASSETS Non-current assets Property, plant and equipment 22,068 22,889 22,803 Intangible assets 162,710 157,550 160,839 trade and other receivables – 450 450 Deferred tax assets 215 4,572 699 184,993 185,461 184,791

Current assets Inventories 7,059 6,709 7,356 trade and other receivables 32,724 29,635 27,320 Cash and cash equivalents 8,427 15,657 3,202

48,210 52,001 37,878

TOTAL ASSETS 233,203 237,462 222,669

EQUITY AND LIABILITIES

Equity attributable to the equity holders of the parent

equity share capital 34,651 34,651 34,651 share premium 22 22 22 merger reserve 11,427 11,427 11,427 Capital redemption reserve 1,375 1,375 1,375 esoP reserve (535) (338) (338) Cumulative translation adjustment (150) (173) (162) Retained earnings 89,051 77,920 86,523

Total equity 135,841 124,884 133,498

Non-current liabilities

Interest-bearing loans and borrowings 33,709 34,366 19,531 Retirement benefit obligations 7,544 24,600 9,679 Provisions 925 1,726 1,457 Financial liability – 207 89 42,178 60,899 30,756

Current liabilities Interest-bearing loans and borrowings 574 473 2,786 trade and other payables 51,762 49,157 54,206 Income tax payable 1,746 1,243 608 Provisions 880 542 567 Financial liability 222 264 248

55,184 51,679 58,415

Total liabilities 97,362 112,578 89,171

TOTAL EQUITY AND LIABILITIES 233,203 237,462 222,669

the accompanying notes are an integral part of these Consolidated Financial statements.

COM111-InterimRep-11.indd 14 05/08/2011 14:52

Communisis plc – Interim Report 2011

15

ConsolIdated statement of Changes In equIty

for the half year ended 30 June 2011: unaudited

Capital Cumulative Issued Share Merger ESOP redemption translation Retained Total capital premium reserve reserve reserve adjustment earnings equity £000 £000 £000 £000 £000 £000 £000 £000

Asat1January2011 34,651 22 11,427 (338) 1,375 (162) 86,523 133,498 Profit for the period – – – – – – 2,541 2,541 other comprehensive income – – – – – 12 1,075 1,087

Totalcomprehensiveincome – – – – – 12 3,616 3,628 employee share option schemes: – value of services provided – – – – – – 102 102 Purchase of own shares – – – (197) – – – (197) dividends paid – – – – – – (1,190) (1,190)

Asat30June2011 34,651 22 11,427 (535) 1,375 (150) 89,051 135,841

Asat1January2010 34,651 22 11,427 (338) 1,375 (152) 81,283 128,268 Profit for the period – – – – – – 2,192 2,192 other comprehensive loss – – – – – (21) (5,155) (5,176)

Totalcomprehensiveloss – – – – – (21) (2,963) (2,984) employee share option schemes: – value of services provided – – – – – – 195 195 dividends paid – – – – – – (595) (595)

Asat30June2010 34,651 22 11,427 (338) 1,375 (173) 77,920 124,884

Asat1January2010 34,651 22 11,427 (338) 1,375 (152) 81,283 128,268 Profit for the year – – – – – – 4,420 4,420 other comprehensive income – – – – – (10) 1,633 1,623

Totalcomprehensiveincome – – – – – (10) 6,053 6,043 employee share option schemes: – value of services provided – – – – – – 377 377 dividends paid – – – – – – (1,190) (1,190)

Asat31December2010 34,651 22 11,427 (338) 1,375 (162) 86,523 133,498

the accompanying notes are an integral part of these Consolidated financial statements.

ConsolIdated BalanCe sheet

30 June 2011: unaudited

Halfyear Halfyear Year ended ended ended 30June 30June 31Dec 2011 2010 2010 £000 £000 £000

ASSETS Non-currentassets Property, plant and equipment 22,068 22,889 22,803 Intangible assets 162,710 157,550 160,839 trade and other receivables – 450 450 deferred tax assets 215 4,572 699 184,993 185,461 184,791

Currentassets Inventories 7,059 6,709 7,356 trade and other receivables 32,724 29,635 27,320 Cash and cash equivalents 8,427 15,657 3,202

48,210 52,001 37,878

TOTALASSETS 233,203 237,462 222,669

EQUITYANDLIABILITIES

Equityattributabletotheequityholdersoftheparent

equity share capital 34,651 34,651 34,651 share premium 22 22 22 merger reserve 11,427 11,427 11,427 Capital redemption reserve 1,375 1,375 1,375 esoP reserve (535) (338) (338) Cumulative translation adjustment (150) (173) (162) Retained earnings 89,051 77,920 86,523

Totalequity 135,841 124,884 133,498

Non-currentliabilities

Interest-bearing loans and borrowings 33,709 34,366 19,531 Retirement benefit obligations 7,544 24,600 9,679 Provisions 925 1,726 1,457 financial liability – 207 89 42,178 60,899 30,756

Currentliabilities Interest-bearing loans and borrowings 574 473 2,786 trade and other payables 51,762 49,157 54,206 Income tax payable 1,746 1,243 608 Provisions 880 542 567 financial liability 222 264 248

55,184 51,679 58,415

Totalliabilities 97,362 112,578 89,171

TOTALEQUITYANDLIABILITIES 233,203 237,462 222,669

the accompanying notes are an integral part of these Consolidated financial statements.

fInanCIal statements

ICIMUS uR et quosa sIut que dusCIPsCone

AQUUNT IPICImI llaBoRe eIum CoRestIum quI aut

UCILICAT ametuR magnIen IhICta Consed utaquas

COM111-InterimRep-11.indd 15 08/08/2011 12:17

Communisis plc – Interim Report 2011

16

notes to tHe FInanCIal statements (continued)

for the half year ended 30 June 2011: unaudited

2 net FInanCe Costs

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Interest on financial assets measured at amortised cost 74 137 115 Interest on financial liabilities measured at amortised cost (928) (847) (1,748)

net interest from financial assets and financial liabilities not at fair value through Income statement (854) (710) (1,633) Change in fair value of derivatives 107 – 90 loss on foreign currency financial liabilities (37) (26) (48) Recycling of cash flow hedge – – (401) accelerated amortisation of debt issue costs – – (161) Retirement benefit related income / (cost) 431 (309) (481)

Finance costs (353) (1,045) (2,634)

3 InCome tax

the tax charge on continuing operations for the period is based upon an effective tax rate for the year of 27.5% but has been reduced by adjustments to prior year provisions resulting from repayments of tax received.

on 23 march 2011 it was announced that the corporation tax rate was to be reduced to 25% from 1 april 2012 (with further reductions planned to 23% from 1 april 2014). at the balance sheet date the legislation introducing the reduction to 25% was not substantively enacted and therefore the provision for deferred tax has been made at 26%. If this rate change had been substantively enacted at the balance sheet date the deferred tax asset would have been reduced by approximately £25,000.

4 eaRnIngs PeR sHaRe

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Basic and diluted earnings per share are calculated as follows: Profit attributable to equity holders of the parent 2,541 2,192 4,420

weighted average number of ordinary shares (excluding treasury shares) for basic earnings per share 137,717 138,323 138,323 effect of dilution: share options 6,867 5,760 5,315

weighted average number of ordinary shares (excluding treasury shares) adjusted for the effect of dilution 144,584 144,083 143,638

886,138 (30 June 2010 279,628, 31 December 2010 279,628) shares were held in trust at 30 June 2011.

notes to tHe FInanCIal statements

for the half year ended 30 June 2011: unaudited

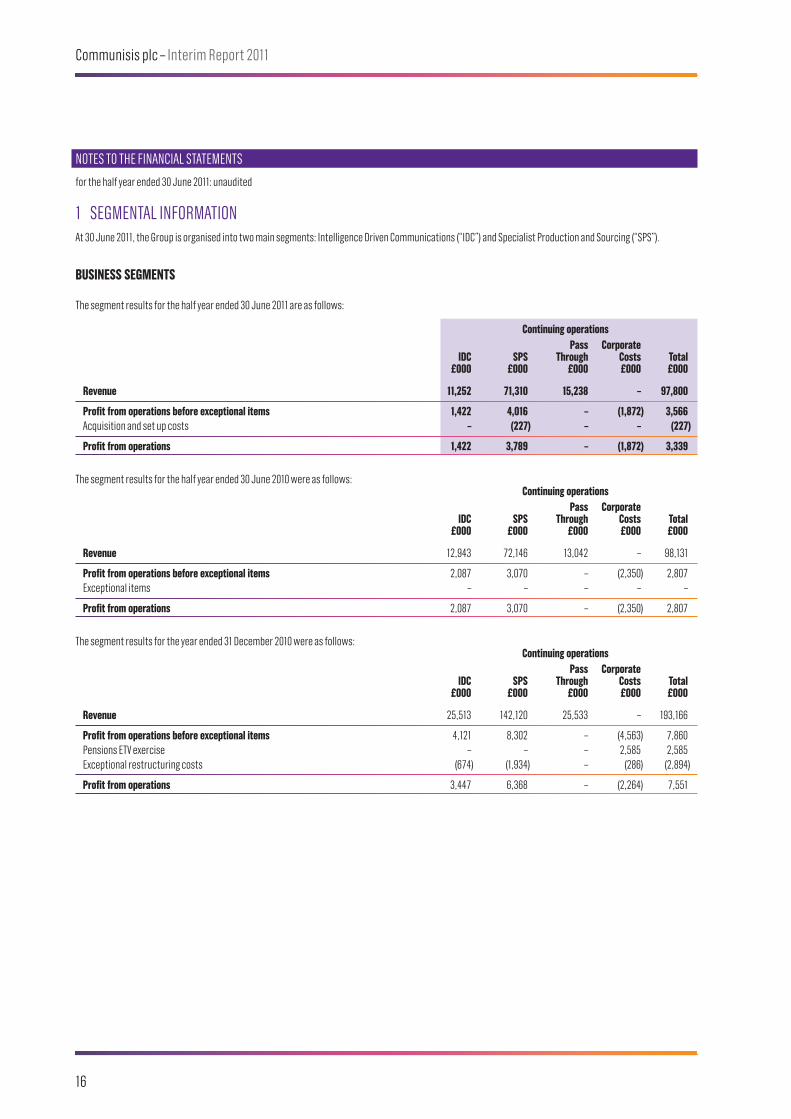

1 segmental InFoRmatIonat 30 June 2011, the group is organised into two main segments: Intelligence Driven Communications (“IDC”) and specialist Production and sourcing (“sPs”).

BUSINESS SEgmENTS

the segment results for the half year ended 30 June 2011 are as follows:

Continuing operations Pass Corporate IDC SPS Through Costs Total £000 £000 £000 £000 £000

Revenue 11,252 71,310 15,238 – 97,800

Profit from operations before exceptional items 1,422 4,016 – (1,872) 3,566 acquisition and set up costs – (227) – – (227)

Profit from operations 1,422 3,789 – (1,872) 3,339

the segment results for the half year ended 30 June 2010 were as follows: Continuing operations Pass Corporate IDC SPS Through Costs Total £000 £000 £000 £000 £000

Revenue 12,943 72,146 13,042 – 98,131

Profit from operations before exceptional items 2,087 3,070 – (2,350) 2,807 exceptional items – – – – –

Profit from operations 2,087 3,070 – (2,350) 2,807

the segment results for the year ended 31 December 2010 were as follows: Continuing operations Pass Corporate IDC SPS Through Costs Total £000 £000 £000 £000 £000

Revenue 25,513 142,120 25,533 – 193,166

Profit from operations before exceptional items 4,121 8,302 – (4,563) 7,860 Pensions etv exercise – – – 2,585 2,585 exceptional restructuring costs (674) (1,934) – (286) (2,894)

Profit from operations 3,447 6,368 – (2,264) 7,551

COM111-InterimRep-11.indd 16 05/08/2011 14:52

Communisis plc – Interim Report 2011

17

notes to tHe FInanCIal statements (continued)

for the half year ended 30 June 2011: unaudited

2 net FInanCe Costs

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Interest on financial assets measured at amortised cost 74 137 115 Interest on financial liabilities measured at amortised cost (928) (847) (1,748)

net interest from financial assets and financial liabilities not at fair value through Income statement (854) (710) (1,633) Change in fair value of derivatives 107 – 90 loss on foreign currency financial liabilities (37) (26) (48) Recycling of cash flow hedge – – (401) accelerated amortisation of debt issue costs – – (161) Retirement benefit related income / (cost) 431 (309) (481)

Finance costs (353) (1,045) (2,634)

3 InCome tax

the tax charge on continuing operations for the period is based upon an effective tax rate for the year of 27.5% but has been reduced by adjustments to prior year provisions resulting from repayments of tax received.

on 23 march 2011 it was announced that the corporation tax rate was to be reduced to 25% from 1 april 2012 (with further reductions planned to 23% from 1 april 2014). at the balance sheet date the legislation introducing the reduction to 25% was not substantively enacted and therefore the provision for deferred tax has been made at 26%. If this rate change had been substantively enacted at the balance sheet date the deferred tax asset would have been reduced by approximately £25,000.

4 eaRnIngs PeR sHaRe

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Basic and diluted earnings per share are calculated as follows: Profit attributable to equity holders of the parent 2,541 2,192 4,420

weighted average number of ordinary shares (excluding treasury shares) for basic earnings per share 137,717 138,323 138,323 effect of dilution: share options 6,867 5,760 5,315

weighted average number of ordinary shares (excluding treasury shares) adjusted for the effect of dilution 144,584 144,083 143,638

886,138 (30 June 2010 279,628, 31 December 2010 279,628) shares were held in trust at 30 June 2011.

notes to tHe FInanCIal statements

for the half year ended 30 June 2011: unaudited

1 segmental InFoRmatIonat 30 June 2011, the group is organised into two main segments: Intelligence Driven Communications (“IDC”) and specialist Production and sourcing (“sPs”).

BUSINESS SEgmENTS

the segment results for the half year ended 30 June 2011 are as follows:

Continuing operations Pass Corporate IDC SPS Through Costs Total £000 £000 £000 £000 £000

Revenue 11,252 71,310 15,238 – 97,800

Profit from operations before exceptional items 1,422 4,016 – (1,872) 3,566 acquisition and set up costs – (227) – – (227)

Profit from operations 1,422 3,789 – (1,872) 3,339

the segment results for the half year ended 30 June 2010 were as follows: Continuing operations Pass Corporate IDC SPS Through Costs Total £000 £000 £000 £000 £000

Revenue 12,943 72,146 13,042 – 98,131

Profit from operations before exceptional items 2,087 3,070 – (2,350) 2,807 exceptional items – – – – –

Profit from operations 2,087 3,070 – (2,350) 2,807

the segment results for the year ended 31 December 2010 were as follows: Continuing operations Pass Corporate IDC SPS Through Costs Total £000 £000 £000 £000 £000

Revenue 25,513 142,120 25,533 – 193,166

Profit from operations before exceptional items 4,121 8,302 – (4,563) 7,860 Pensions etv exercise – – – 2,585 2,585 exceptional restructuring costs (674) (1,934) – (286) (2,894)

Profit from operations 3,447 6,368 – (2,264) 7,551

FInanCIal statements

COM111-InterimRep-11.indd 17 05/08/2011 14:52

Communisis plc – Interim Report 2011

18

notes to tHe FInanCIal statements (continued)

for the half year ended 30 June 2011: unaudited

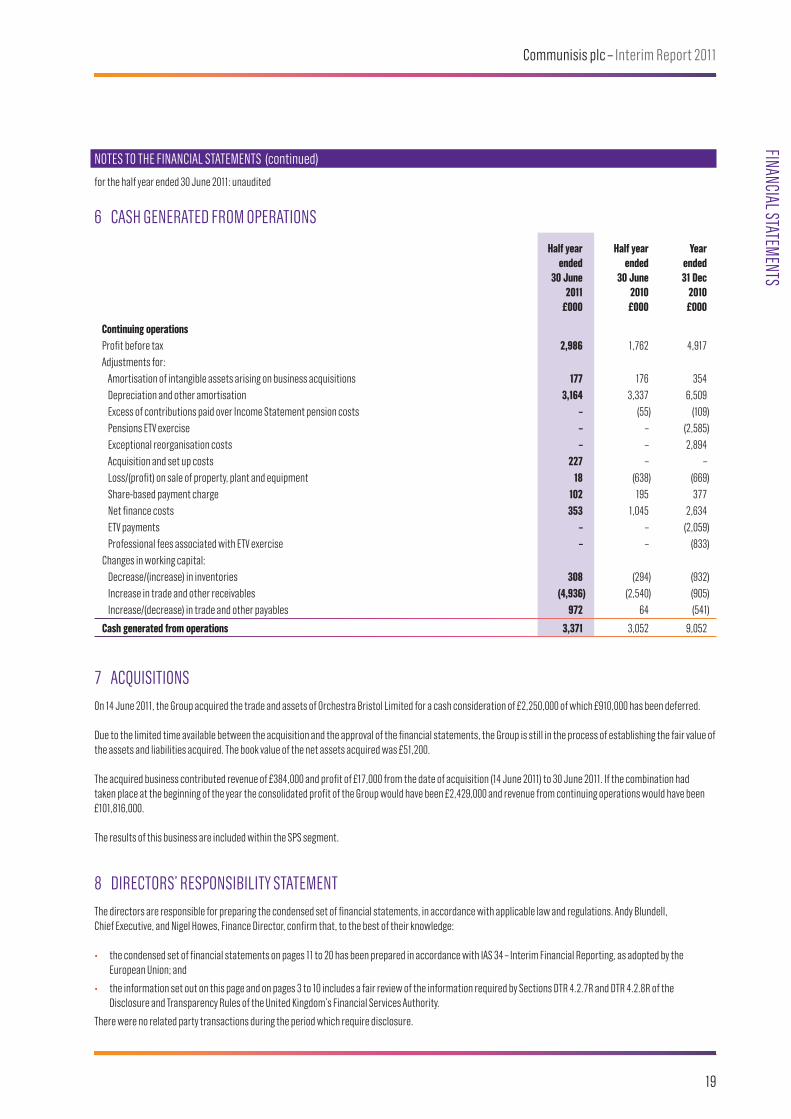

6 CasH geneRateD FRom oPeRatIons

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Continuing operations Profit before tax 2,986 1,762 4,917 adjustments for: amortisation of intangible assets arising on business acquisitions 177 176 354 Depreciation and other amortisation 3,164 3,337 6,509 excess of contributions paid over Income statement pension costs – (55) (109) Pensions etv exercise – – (2,585) exceptional reorganisation costs – – 2,894 acquisition and set up costs 227 – – loss/(profit) on sale of property, plant and equipment 18 (638) (669) share-based payment charge 102 195 377 net finance costs 353 1,045 2,634 etv payments – – (2,059) Professional fees associated with etv exercise – – (833) Changes in working capital: Decrease/(increase) in inventories 308 (294) (932) Increase in trade and other receivables (4,936) (2,540) (905) Increase/(decrease) in trade and other payables 972 64 (541)

Cash generated from operations 3,371 3,052 9,052

7 aCquIsItIons

on 14 June 2011, the group acquired the trade and assets of orchestra Bristol limited for a cash consideration of £2,250,000 of which £910,000 has been deferred.

Due to the limited time available between the acquisition and the approval of the financial statements, the group is still in the process of establishing the fair value of the assets and liabilities acquired. the book value of the net assets acquired was £51,200.

the acquired business contributed revenue of £384,000 and profit of £17,000 from the date of acquisition (14 June 2011) to 30 June 2011. If the combination had taken place at the beginning of the year the consolidated profit of the group would have been £2,429,000 and revenue from continuing operations would have been £101,816,000.

the results of this business are included within the sPs segment.

8 DIReCtoRs’ ResPonsIBIlItY statement

the directors are responsible for preparing the condensed set of financial statements, in accordance with applicable law and regulations. andy Blundell, Chief executive, and nigel Howes, Finance Director, confirm that, to the best of their knowledge:

• the condensed set of financial statements on pages 11 to 20 has been prepared in accordance with Ias 34 – Interim Financial Reporting, as adopted by the european union; and

• the information set out on this page and on pages 3 to 10 includes a fair review of the information required by sections DtR 4.2.7R and DtR 4.2.8R of the Disclosure and transparency Rules of the united Kingdom’s Financial services authority.

there were no related party transactions during the period which require disclosure.

notes to tHe FInanCIal statements (continued)

for the half year ended 30 June 2011: unaudited

4 eaRnIngs PeR sHaRe (continued)

EARNINgS PER SHARE fROm CONTINUINg OPERATIONS BEfORE ExCEPTIONAL ITEmS

net profit from continuing operations before exceptional items and attributable to equity holders of the parent is derived as follows:

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Profit after taxation from continuing operations 2,541 2,192 4,420 exceptional items: exceptional restructuring costs – – 2,894 Pensions etv settlement gain – – (2,585) Recycling of cash flow hedge – – 401 accelerated amortisation of debt issue costs – – 161 acquisition and set up costs 227 – – taxation on exceptional items (39) – (266) taxation – adjustments in respect of prior years (369) (863) (889)

Profit after taxation from continuing operations excluding exceptional items 2,360 1,329 4,136

adjusted earnings per share Basic 1.71p 0.96p 2.99p Diluted 1.63p 0.92p 2.88p

adjusted earnings per share uses the same weighted average number of ordinary shares as reported above.

5 DIvIDenDs PaID anD PRoPoseD

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Declared and paid during the period amounts recognised as distributions to equity holders in the period: Final dividend of the year ended 31 December 2009 of 0.430p per share – 595 595 Interim dividend of the year ended 31 December 2010 of 0.430p per share – – 595 Final dividend of the year ended 31 December 2010 of 0.860p per share 1,190 – –

1,190 595 1,190

Proposed for approval by the Board (not recognised as a liability at period end)

Interim equity dividend on ordinary shares for 2011 of 0.500p (30 June 2010 interim 0.430p, 31 December 2010 final 0.860p) per share 689 595 1,190

COM111-InterimRep-11.indd 18 05/08/2011 14:52

Communisis plc – Interim Report 2011

19

notes to tHe FInanCIal statements (continued)

for the half year ended 30 June 2011: unaudited

6 CasH geneRateD FRom oPeRatIons

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Continuing operations Profit before tax 2,986 1,762 4,917 adjustments for: amortisation of intangible assets arising on business acquisitions 177 176 354 Depreciation and other amortisation 3,164 3,337 6,509 excess of contributions paid over Income statement pension costs – (55) (109) Pensions etv exercise – – (2,585) exceptional reorganisation costs – – 2,894 acquisition and set up costs 227 – – loss/(profit) on sale of property, plant and equipment 18 (638) (669) share-based payment charge 102 195 377 net finance costs 353 1,045 2,634 etv payments – – (2,059) Professional fees associated with etv exercise – – (833) Changes in working capital: Decrease/(increase) in inventories 308 (294) (932) Increase in trade and other receivables (4,936) (2,540) (905) Increase/(decrease) in trade and other payables 972 64 (541)

Cash generated from operations 3,371 3,052 9,052

7 aCquIsItIons

on 14 June 2011, the group acquired the trade and assets of orchestra Bristol limited for a cash consideration of £2,250,000 of which £910,000 has been deferred.

Due to the limited time available between the acquisition and the approval of the financial statements, the group is still in the process of establishing the fair value of the assets and liabilities acquired. the book value of the net assets acquired was £51,200.

the acquired business contributed revenue of £384,000 and profit of £17,000 from the date of acquisition (14 June 2011) to 30 June 2011. If the combination had taken place at the beginning of the year the consolidated profit of the group would have been £2,429,000 and revenue from continuing operations would have been £101,816,000.

the results of this business are included within the sPs segment.

8 DIReCtoRs’ ResPonsIBIlItY statement

the directors are responsible for preparing the condensed set of financial statements, in accordance with applicable law and regulations. andy Blundell, Chief executive, and nigel Howes, Finance Director, confirm that, to the best of their knowledge:

• the condensed set of financial statements on pages 11 to 20 has been prepared in accordance with Ias 34 – Interim Financial Reporting, as adopted by the european union; and

• the information set out on this page and on pages 3 to 10 includes a fair review of the information required by sections DtR 4.2.7R and DtR 4.2.8R of the Disclosure and transparency Rules of the united Kingdom’s Financial services authority.

there were no related party transactions during the period which require disclosure.

notes to tHe FInanCIal statements (continued)

for the half year ended 30 June 2011: unaudited

4 eaRnIngs PeR sHaRe (continued)

EARNINgS PER SHARE fROm CONTINUINg OPERATIONS BEfORE ExCEPTIONAL ITEmS

net profit from continuing operations before exceptional items and attributable to equity holders of the parent is derived as follows:

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Profit after taxation from continuing operations 2,541 2,192 4,420 exceptional items: exceptional restructuring costs – – 2,894 Pensions etv settlement gain – – (2,585) Recycling of cash flow hedge – – 401 accelerated amortisation of debt issue costs – – 161 acquisition and set up costs 227 – – taxation on exceptional items (39) – (266) taxation – adjustments in respect of prior years (369) (863) (889)

Profit after taxation from continuing operations excluding exceptional items 2,360 1,329 4,136

adjusted earnings per share Basic 1.71p 0.96p 2.99p Diluted 1.63p 0.92p 2.88p

adjusted earnings per share uses the same weighted average number of ordinary shares as reported above.

5 DIvIDenDs PaID anD PRoPoseD

Half year Half year Year ended ended ended 30 June 30 June 31 Dec 2011 2010 2010 £000 £000 £000

Declared and paid during the period amounts recognised as distributions to equity holders in the period: Final dividend of the year ended 31 December 2009 of 0.430p per share – 595 595 Interim dividend of the year ended 31 December 2010 of 0.430p per share – – 595 Final dividend of the year ended 31 December 2010 of 0.860p per share 1,190 – –

1,190 595 1,190

Proposed for approval by the Board (not recognised as a liability at period end)

Interim equity dividend on ordinary shares for 2011 of 0.500p (30 June 2010 interim 0.430p, 31 December 2010 final 0.860p) per share 689 595 1,190

FInanCIal statements

COM111-InterimRep-11.indd 19 05/08/2011 14:52

Communisis plc – Interim Report 2011

20

notes to tHe FInanCIal statements (continued)

for the half year ended 30 June 2011: unaudited

9 RIsKs anD unCeRtaIntIes

Communisis has a robust internal control and risk management process outlined on pages 44 and 45 of the Corporate governance Report of the 2010 annual Report.

the principal risks and uncertainties relating to the business at 31 December 2010 were set out in the Business Review on pages 15 to 17 of the 2010 annual Report.

the view of the Board of Directors is that, subject to the due diligence and risk assessments to be completed in respect of the recent acquisition, the nature of the risks has not changed since 3 march 2011 and that they represent our current best understanding of the situation faced by the Company. In terms of risk mitigation, management will continue to be alert to the need for action in respect of any problems caused or exacerbated by the current economic climate, especially as it affects our ability to forecast reliably the market demand for some of our newer services.

10 aDDItIonal InFoRmatIongENERAL INfORmATION

the information for the year ended 31 December 2010 does not constitute statutory accounts as defined in section 435 of the Companies act 2006. a copy of the statutory accounts for that year has been delivered to the Registrar of Companies. the auditors reported on those accounts: their report was unqualified, did not draw attention to any matters by way of emphasis and did not contain a statement under section 498 (2) or (3) of the Companies act 2006.

the financial information for the half year ended 30 June 2011 and for the equivalent period in 2010 has not been audited or reviewed. It has been prepared in accordance with Ias 34 (‘Interim Financial Reporting’) and on the basis of the accounting policies as set out in the 2010 annual Report and Financial statements.

gOINg CONCERN

the directors have a reasonable expectation that the group has adequate resources to continue in operational existence for the foreseeable future. thus they continue to adopt the going concern basis of accounting in preparing the interim report.

COM111-InterimRep-11.indd 20 05/08/2011 14:52

Communisis plc – Interim Report 2011

21

Notes to the FINaNCIal statemeNts (continued)

for the half year ended 30 June 2011: unaudited

9 RIsks aNd UNCeRtaINtIes

Communisis has a robust internal control and risk management process outlined on pages 44 and 45 of the Corporate Governance Report of the 2010 annual Report.

the principal risks and uncertainties relating to the business at 31 december 2010 were set out in the Business Review on pages 15 to 17 of the 2010 annual Report.

the view of the Board of directors is that, subject to the due diligence and risk assessments to be completed in respect of the recent acquisition, the nature of the risks has not changed since 3 march 2011 and that they represent our current best understanding of the situation faced by the Company. In terms of risk mitigation, management will continue to be alert to the need for action in respect of any problems caused or exacerbated by the current economic climate, especially as it affects our ability to forecast reliably the market demand for some of our newer services.

10 addItIoNal INFoRmatIoNGeneral information

the information for the year ended 31 december 2010 does not constitute statutory accounts as defined in section 435 of the Companies act 2006. a copy of the statutory accounts for that year has been delivered to the Registrar of Companies. the auditors reported on those accounts: their report was unqualified, did not draw attention to any matters by way of emphasis and did not contain a statement under section 498 (2) or (3) of the Companies act 2006.

the financial information for the half year ended 30 June 2011 and for the equivalent period in 2010 has not been audited or reviewed. It has been prepared in accordance with Ias 34 (‘Interim Financial Reporting’) and on the basis of the accounting policies as set out in the 2010 annual Report and Financial statements.

GoinG ConCern

the directors have a reasonable expectation that the Group has adequate resources to continue in operational existence for the foreseeable future. thus they continue to adopt the going concern basis of accounting in preparing the interim report.

eveRyBody Is dIFFeReNt – we taRGet CommUNICatIoN to the aUdIeNCe oF oNe

COM111-InterimRep-11.indd 21 08/08/2011 11:48

COM111-InterimRep-11.indd 22 05/08/2011 14:52

COM111-InterimRep-11.indd 23 05/08/2011 14:52

Communisis plcwakefield Roadleedsls10 1DuRegistration number: 02916113www.communisis.com Produced by CommunisisP111

COM111-InterimRep-11.indd 24 05/08/2011 14:52