commodity watch -...

TRANSCRIPT

COMMODITY WATCH

Bunzl Distribution Newsletter August 2015

Goodbye To All That From the print edition | The Economist

Published: August 22nd 2015

A decade of bingeing on raw materials

may leave an even longer hangover

IT WAS only a decade or so ago that Scot-

land was hit by the “Great Drain Robbery”,

the disappearance of 50 manhole covers

in Fife. It gave an inkling of the emergence

of a new era in commodity markets,

spurred by insatiable demand from China.

Scrap-metal prices – and so scrap-metal

thefts – soared. Africa was over-run by

Chinese engineers; Australia elected a

Mandarin-speaking prime minister; and

emerging markets from Argentina to Zam-

bia relished the rising values of their farm-

land and mines. The boom was fanned by

a weak American dollar, the currency in

which most stuff that comes out of the

ground is priced.

The gears have now gone into reverse. A

resurgent dollar has hammered commodity

prices: many have recently fallen below

their levels of a decade ago. That is a fate

not shared by other tradeable assets: not

since the late 1990s have commodity pric-

es been so weak compared with shares

(see chart 1). The American economy is

strengthening, but by no means enough to

encourage thieves to filch bronze bells

from Chinese temples to send as scrap to

the United States. The impact of its recov-

ery is

dwarfed by

slowing

demand in

China,

which still

consumes

about half

the world’s

metals

such as iron, aluminium, and zinc.

See Goodbye To All That on pg. 7

Contents

Resin

Aluminum

Paper and Pulp

Energy

Foreign Currency

2

4

4

5

6

Contact us

E-mail us with your comments

and suggestions.

Tetiana Tarasova

Bunzl Distribution

Our Goal is:

To show market trends that

affect Bunzl Distribution’s

final product cost.

To provide market and eco-

nomical data to internal

readers.

Prices Fall For Most Commodity

Resins By Frank Eposito | Plastic News

Published: September 3rd 2015

The Summer of 2015 began to fade in August – and it

took North American commodity resin prices down along

with it.

Average per-pound selling prices for polyethylene, polypro-

pylene, polystyrene, PVC and PET all fell in August. PE

saw the largest August drop with 5 cents, while PET prices

fell 4 cents. Next in line were PP and PS, each with a 2-

cent drop, while PVC prices ticked down 1 cent.

“Whenever oil prices move down sharply, most commodity

resins prices are bound to soon start moving downward, as

well,” said Phil Karig, managing director with the Mathelin

Bay Associates consulting firm in St. Louis. “In the case of

ethylene-affected resins [like PE and PVC], the recent eas-

ing of ethylene supply issues is also contributing to down-

ward pricing pressures. “Add in weaker export markets,

expectations for continued resin price declines … and a

growing unease over financial instability in China … and we

have all the ingredients for continued price declines in the

months ahead,” he added.

All of the pricing changes are reflected in the Sept. 7 print

edition of Plastics News. The lower polyethylene prices

were noted on PlasticsNews.com on Aug. 27, and the rest

of the changes on Sept. 3.

Lower feedstock costs played a role in sending North

American PE prices down. The decline effectively wipes out

a 5-cent hike that the market had seen in May. Prior to that

increase, regional PE prices fell a total of 16 cents between

October and April.

See Prices Fall on pg. 8

2

Bunzl Distribution Newsletter | Commodity Watch August 2015

2

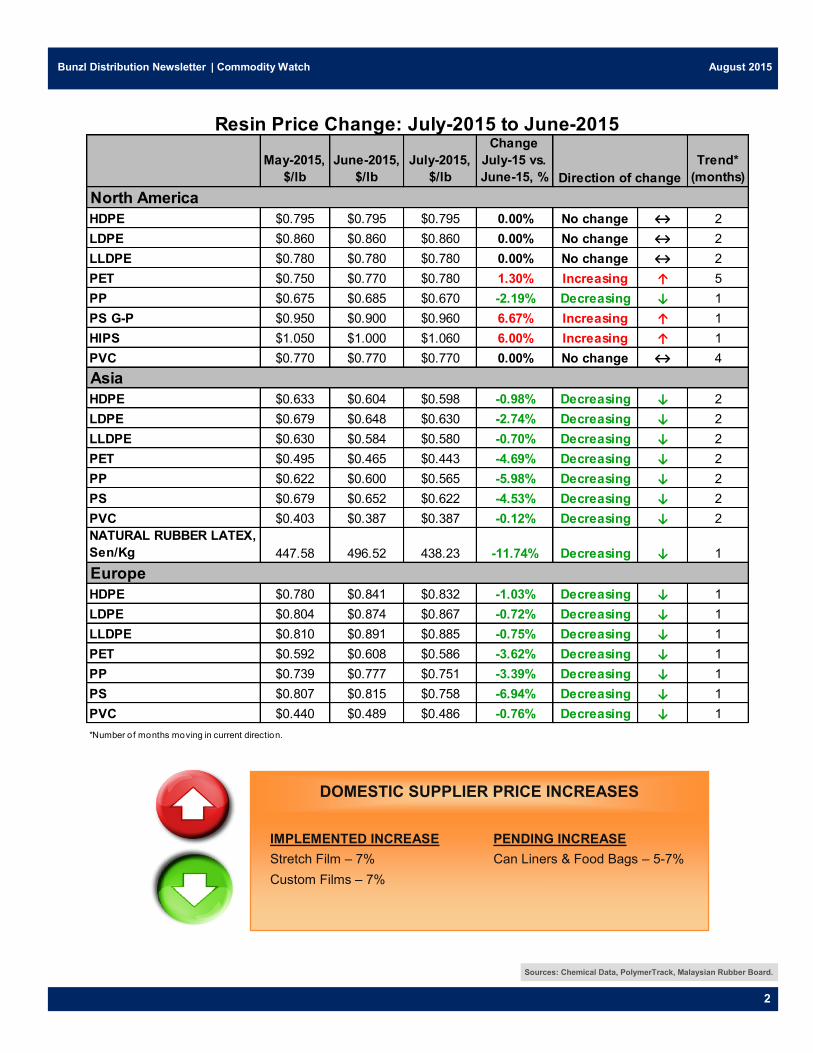

IMPLEMENTED INCREASE

Stretch Film – 7%

Custom Films – 7%

PENDING INCREASE

Can Liners & Food Bags – 5-7%

DOMESTIC SUPPLIER PRICE INCREASES

Sources: Chemical Data, PolymerTrack, Malaysian Rubber Board.

May-2015,

$/lb

June-2015,

$/lb

July-2015,

$/lb

Change

July-15 vs.

June-15, %

Trend*

(months)

HDPE $0.795 $0.795 $0.795 0.00% No change ↔ 2

LDPE $0.860 $0.860 $0.860 0.00% No change ↔ 2

LLDPE $0.780 $0.780 $0.780 0.00% No change ↔ 2

PET $0.750 $0.770 $0.780 1.30% Increasing ↑ 5

PP $0.675 $0.685 $0.670 -2.19% Decreasing ↓ 1

PS G-P $0.950 $0.900 $0.960 6.67% Increasing ↑ 1

HIPS $1.050 $1.000 $1.060 6.00% Increasing ↑ 1

PVC $0.770 $0.770 $0.770 0.00% No change ↔ 4

HDPE $0.633 $0.604 $0.598 -0.98% Decreasing ↓ 2

LDPE $0.679 $0.648 $0.630 -2.74% Decreasing ↓ 2

LLDPE $0.630 $0.584 $0.580 -0.70% Decreasing ↓ 2

PET $0.495 $0.465 $0.443 -4.69% Decreasing ↓ 2

PP $0.622 $0.600 $0.565 -5.98% Decreasing ↓ 2

PS $0.679 $0.652 $0.622 -4.53% Decreasing ↓ 2

PVC $0.403 $0.387 $0.387 -0.12% Decreasing ↓ 2

NATURAL RUBBER LATEX,

Sen/Kg 447.58 496.52 438.23 -11.74% Decreasing ↓ 1

HDPE $0.780 $0.841 $0.832 -1.03% Decreasing ↓ 1

LDPE $0.804 $0.874 $0.867 -0.72% Decreasing ↓ 1

LLDPE $0.810 $0.891 $0.885 -0.75% Decreasing ↓ 1

PET $0.592 $0.608 $0.586 -3.62% Decreasing ↓ 1

PP $0.739 $0.777 $0.751 -3.39% Decreasing ↓ 1

PS $0.807 $0.815 $0.758 -6.94% Decreasing ↓ 1

PVC $0.440 $0.489 $0.486 -0.76% Decreasing ↓ 1

Resin Price Change: July-2015 to June-2015

Direction of change

North America

Asia

Europe

*Number of months moving in current direction.

3

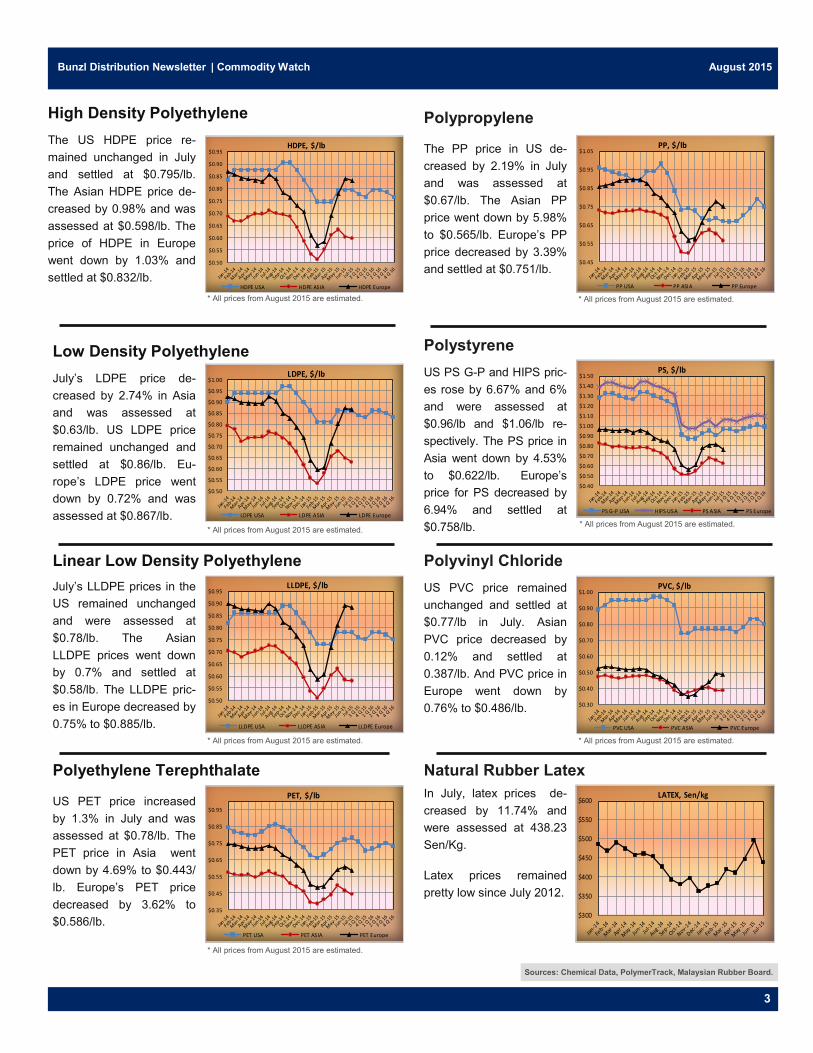

High Density Polyethylene

The US HDPE price re-

mained unchanged in July

and settled at $0.795/lb.

The Asian HDPE price de-

creased by 0.98% and was

assessed at $0.598/lb. The

price of HDPE in Europe

went down by 1.03% and

settled at $0.832/lb.

3

Low Density Polyethylene

July’s LDPE price de-

creased by 2.74% in Asia

and was assessed at

$0.63/lb. US LDPE price

remained unchanged and

settled at $0.86/lb. Eu-

rope’s LDPE price went

down by 0.72% and was

assessed at $0.867/lb.

Linear Low Density Polyethylene

July’s LLDPE prices in the

US remained unchanged

and were assessed at

$0.78/lb. The Asian

LLDPE prices went down

by 0.7% and settled at

$0.58/lb. The LLDPE pric-

es in Europe decreased by

0.75% to $0.885/lb.

Polyethylene Terephthalate

US PET price increased

by 1.3% in July and was

assessed at $0.78/lb. The

PET price in Asia went

down by 4.69% to $0.443/

lb. Europe’s PET price

decreased by 3.62% to

$0.586/lb.

Polypropylene

The PP price in US de-

creased by 2.19% in July

and was assessed at

$0.67/lb. The Asian PP

price went down by 5.98%

to $0.565/lb. Europe’s PP

price decreased by 3.39%

and settled at $0.751/lb.

Polystyrene

US PS G-P and HIPS pric-

es rose by 6.67% and 6%

and were assessed at

$0.96/lb and $1.06/lb re-

spectively. The PS price in

Asia went down by 4.53%

to $0.622/lb. Europe’s

price for PS decreased by

6.94% and settled at

$0.758/lb.

Polyvinyl Chloride

US PVC price remained

unchanged and settled at

$0.77/lb in July. Asian

PVC price decreased by

0.12% and settled at

0.387/lb. And PVC price in

Europe went down by

0.76% to $0.486/lb.

Natural Rubber Latex

In July, latex prices de-

creased by 11.74% and

were assessed at 438.23

Sen/Kg.

Latex prices remained

pretty low since July 2012.

Bunzl Distribution Newsletter | Commodity Watch August 2015

Sources: Chemical Data, PolymerTrack, Malaysian Rubber Board.

$0.50

$0.55

$0.60

$0.65

$0.70

$0.75

$0.80

$0.85

$0.90

$0.95HDPE, $/lb

HDPE USA HDPE ASIA HDPE Europe

* All prices from August 2015 are estimated.

$0.50

$0.55

$0.60

$0.65

$0.70

$0.75

$0.80

$0.85

$0.90

$0.95

$1.00LDPE, $/lb

LDPE USA LDPE ASIA LDPE Europe

* All prices from August 2015 are estimated.

$0.50

$0.55

$0.60

$0.65

$0.70

$0.75

$0.80

$0.85

$0.90

$0.95LLDPE, $/lb

LLDPE USA LLDPE ASIA LLDPE Europe

* All prices from August 2015 are estimated.

* All prices from August 2015 are estimated.

$0.45

$0.55

$0.65

$0.75

$0.85

$0.95

$1.05PP, $/lb

PP USA PP ASIA PP Europe

$300

$350

$400

$450

$500

$550

$600LATEX, Sen/kg

$0.35

$0.45

$0.55

$0.65

$0.75

$0.85

$0.95

PET, $/lb

PET USA PET ASIA PET Europe

* All prices from August 2015 are estimated.

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

$1.30

$1.40

$1.50PS, $/lb

PS G-P USA HIPS USA PS ASIA PS Europe

* All prices from August 2015 are estimated.

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

$0.90

$1.00PVC, $/lb

PVC USA PVC ASIA PVC Europe

* All prices from August 2015 are estimated.

ALUMINUM

Aluminum prices decreased by 5.4% in July.

Prices for Aluminum on the London Metal Exchange were assessed at

$1,594/mt in July.

4

PAPER AND PULP

Northern bleached softwood kraft prices remained unchanged in July and

were assessed at $980/ton.

The prices for 30# KRAFT UNBLEACHED BAG and 70# KRAFT UN-

BLEACHED SACK remained unchanged in July and settled at $1,175/ton

and $985/ton respectively.

Solid bleached sulphate prices remained unchanged and were assessed

at $1,155/ton in July.

Bunzl Distribution Newsletter | Commodity Watch August 2015

Sources: LME, P&P weekly.

$1,400

$1,500

$1,600

$1,700

$1,800

$1,900

$2,000

$2,100

$2,200ALUMINUM, $/ton

$900

$925

$950

$975

$1,000

$1,025

$1,050

$1,075

$1,100

$1,125

$1,150

$1,175

$1,200PAPER AND PULP, $/ton

NBSK SBS BOARD

30# KRAFT UN BLEACHED BAG 70# KRAFT UN BLEACHED SACK

*Tracking of Wastepaper pricing discontinued from January 2015.

May-2015,

$/ton

June-2015,

$/ton

July-2015,

$/ton

Change

July-15 vs.

June-15, %

Trend*

(months)

NBSK $980 $980 $960 -2.04% Decreasing ↓ 1

SBS BOARD $1,155 $1,155 $1,155 0.00% No change ↔ 6

30# KRAFT UNBLEACHED

BAG $1,175 $1,175 $1,175 0.00% No change ↔ 15

70# KRAFT UNBLEACHED

SACK $985 $985 $985 0.00% No change ↔ 15

*Number of months moving in current direction.

Paper and Pulp Price Change: July-2015 to June-2015

Direction of change

5

5

Bunzl Distribution Newsletter | Commodity Watch August 2015

Sources: U.S. Energy Information Administration (EIA).

ENERGY

North Sea Brent crude oil prices averaged $57/barrel (b)

in July, a $5/b decrease from June. Brent crude oil spot

prices fell further in early August, settling at $48/b on

August 7. The recent price declines reflect concerns

about lower economic growth in emerging markets, ex-

pectations of higher oil exports from Iran, and continuing

actual and expected growth in global inventories.

EIA forecasts that Brent crude oil prices will average

$54/b in 2015 and $59/b in 2016, $6/b and $8/b lower

than in last month's STEO, respectively. Forecast West

Texas Intermediate (WTI) crude oil prices in both 2015

and 2016 average $5/b less than the Brent price. The

current values of futures and options contracts for No-

vember 2015 delivery suggest the market expects WTI

prices to range from $34/b to $64/b (at the 95% confi-

dence interval) in November 2015.

On July 14, the P5+1 (the five permanent members of

the United Nations Security Council and Germany) and

Iran announced an agreement that could result in relief

from United States and European Union nuclear-related

sanctions (which include some oil-related sanctions). If

the agreement is implemented and sanctions relief oc-

curs, it will put additional Iranian oil supplies on a global

market that has already seen oil inventories rise signifi-

cantly over the past year. This forecast assumes sanc-

tions relief occurs in 2016, contributing to an annual av-

erage increase in Iranian crude oil production of 0.3 mil-

lion b/d from 2015 to 2016, with most of the increase

coming in the second half of 2016.

U.S. regular gasoline monthly average retail prices aver-

aged $2.79/gallon (gal) in July, a decrease of 1 cent/gal

from June and 82 cents/gal lower than in July 2014. EIA

expects monthly average gasoline prices to decline from

their July level to an average of $2.11/gal during the

fourth quarter of 2015. EIA forecasts U.S. regular gaso-

line retail prices to average $2.41/gal for all of 2015.

EIA estimates total U.S. crude oil production declined by

100,000 barrels per day (b/d) in July compared with

June. Production is expected to continue decreasing

through mid-2016 before growth resumes late in 2016.

Projected U.S. crude oil production averages 9.4 million

b/d in 2015 and 9.0 million b/d in 2016, 0.1 million b/d

and 0.4 million b/d lower, respectively, than in July's

STEO.

Natural gas working inventories were 2,912 billion cubic

feet (Bcf) on July 31, which was 23% higher than a year

earlier and 2% higher than the previous five-year aver-

age (2010-14). EIA projects inventories will close the

injection season at the end of October at 3,867 Bcf,

which would be the second-highest end-of-October level

on record.

U.S. population-weighted cooling degree days through

the end of July were 14% more than in the same period

last year. The hotter temperatures contribute to an EIA

estimate that the typical residential electricity customer

will use 3,134 kilowatthours in the months of June, July,

and August this year, which is 4% more than during the

same period in 2014.

* All prices from August 2015 are estimated.

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

$5.5

$6.0

$6.5

Natural Gas, Dollars/Mil. BTUs

$40

$50

$60

$70

$80

$90

$100

$110

$120

Crude Oil, Dollars per BarrelCrude oil - Cushing OK WTI, $/barrel

$2.00

$2.25

$2.50

$2.75

$3.00

$3.25

$3.50

$3.75

$4.00

U.S. Regular-grade Retail Gasoline, Dollars per Gallon

Short-Term Energy Outlook

6

6

Bunzl Distribution Newsletter | Commodity Watch August 2015

Sources: http://www.x-rates.com/

http://www.oanda.com/currency/converter/

0.70

0.75

0.80

0.85

0.90

0.95Euro, per 1 USD

8,500

9,500

10,500

11,500

12,500

13,500

14,500Indonesian Rupiah, per 1 USD

31.50

32.00

32.50

33.00

33.50

34.00

34.50Thai Baht, per 1 USD

20,700

20,900

21,100

21,300

21,500

21,700

21,900Vietnamese Dong, per 1 USD

FOREIGN CURRENCY – Outlook

5.85

5.95

6.05

6.15

6.25

6.35

6.45Chinese Yuan, per 1 USD

2.95

3.05

3.15

3.25

3.35

3.45

3.55

3.65

3.75

3.85Malaysian Ringgit, per 1 USD

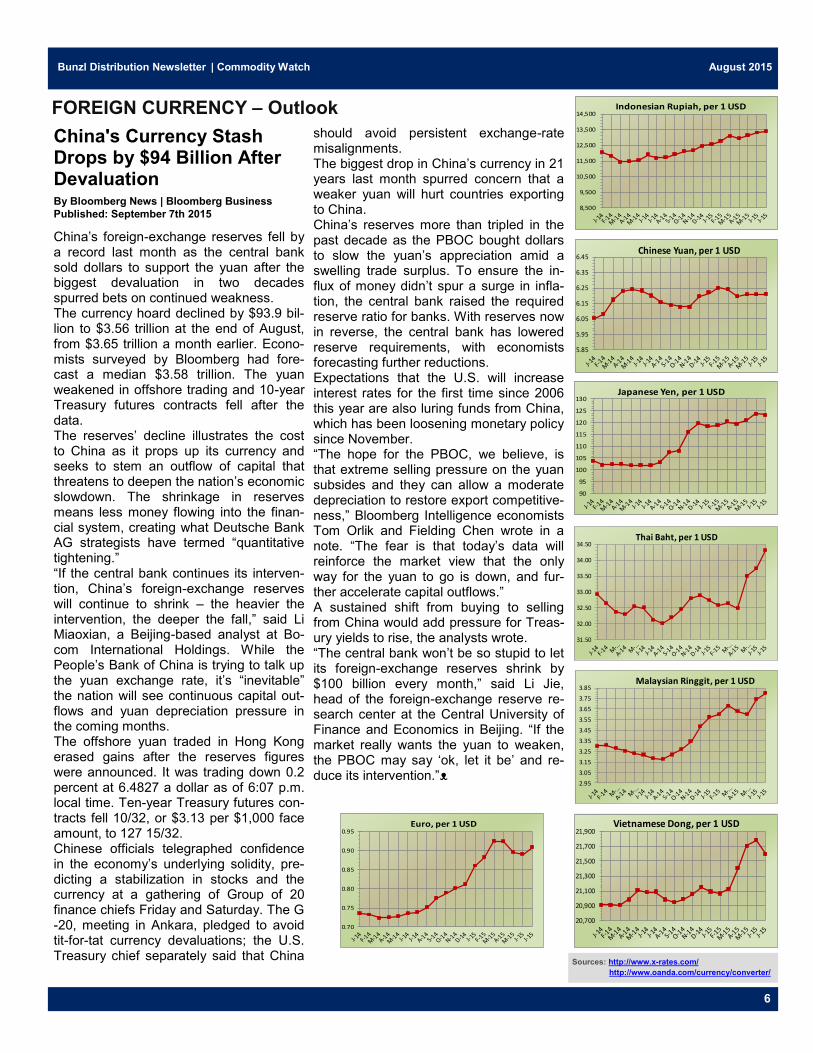

China's Currency Stash Drops by $94 Billion After Devaluation

By Bloomberg News | Bloomberg Business

Published: September 7th 2015

China’s foreign-exchange reserves fell by a record last month as the central bank sold dollars to support the yuan after the biggest devaluation in two decades spurred bets on continued weakness. The currency hoard declined by $93.9 bil-lion to $3.56 trillion at the end of August, from $3.65 trillion a month earlier. Econo-mists surveyed by Bloomberg had fore-cast a median $3.58 trillion. The yuan weakened in offshore trading and 10-year Treasury futures contracts fell after the data. The reserves’ decline illustrates the cost to China as it props up its currency and seeks to stem an outflow of capital that threatens to deepen the nation’s economic slowdown. The shrinkage in reserves means less money flowing into the finan-cial system, creating what Deutsche Bank AG strategists have termed “quantitative tightening.” “If the central bank continues its interven-tion, China’s foreign-exchange reserves will continue to shrink – the heavier the intervention, the deeper the fall,” said Li Miaoxian, a Beijing-based analyst at Bo-com International Holdings. While the People’s Bank of China is trying to talk up the yuan exchange rate, it’s “inevitable” the nation will see continuous capital out-flows and yuan depreciation pressure in the coming months. The offshore yuan traded in Hong Kong erased gains after the reserves figures were announced. It was trading down 0.2 percent at 6.4827 a dollar as of 6:07 p.m. local time. Ten-year Treasury futures con-tracts fell 10/32, or $3.13 per $1,000 face amount, to 127 15/32. Chinese officials telegraphed confidence in the economy’s underlying solidity, pre-dicting a stabilization in stocks and the currency at a gathering of Group of 20 finance chiefs Friday and Saturday. The G-20, meeting in Ankara, pledged to avoid tit-for-tat currency devaluations; the U.S. Treasury chief separately said that China

should avoid persistent exchange-rate misalignments. The biggest drop in China’s currency in 21 years last month spurred concern that a weaker yuan will hurt countries exporting to China. China’s reserves more than tripled in the past decade as the PBOC bought dollars to slow the yuan’s appreciation amid a swelling trade surplus. To ensure the in-flux of money didn’t spur a surge in infla-tion, the central bank raised the required reserve ratio for banks. With reserves now in reverse, the central bank has lowered reserve requirements, with economists forecasting further reductions. Expectations that the U.S. will increase interest rates for the first time since 2006 this year are also luring funds from China, which has been loosening monetary policy since November. “The hope for the PBOC, we believe, is that extreme selling pressure on the yuan subsides and they can allow a moderate depreciation to restore export competitive-ness,” Bloomberg Intelligence economists Tom Orlik and Fielding Chen wrote in a note. “The fear is that today’s data will reinforce the market view that the only way for the yuan to go is down, and fur-ther accelerate capital outflows.” A sustained shift from buying to selling from China would add pressure for Treas-ury yields to rise, the analysts wrote. “The central bank won’t be so stupid to let its foreign-exchange reserves shrink by $100 billion every month,” said Li Jie, head of the foreign-exchange reserve re-search center at the Central University of Finance and Economics in Beijing. “If the market really wants the yuan to weaken, the PBOC may say ‘ok, let it be’ and re-duce its intervention.”ᴥ

90

95

100

105

110

115

120

125

130Japanese Yen, per 1 USD

7

7

Bunzl Distribution Newsletter | Commodity Watch August 2015

Goodbye To All That Continued from pg. 1

The real curse for producers is over-supply in almost all

raw materials. Yet they continue to act as if they are

blithely unaware of it. Capital is still pouring into holes in

the ground, creating a hangover that may last at least a

decade. Jeff Currie of Goldman Sachs, a bank, says past

cycles suggest it can take up to 15 years to work through

the over-investment. “The world has just flip-flopped,” he

says.

Analysts point out that not all commodities act the same

way. Coal prices started falling in 2011; crude oil hung on

until mid-2014; agricultural prices hinge on the weather.

But a generalised whiff of fear about China’s economic

prospects has re-emerged in recent weeks, partly caused

by sliding stockmarkets and by the unexpected devalua-

tion of the yuan this month. So far this year, almost all ma-

jor commodities – energy, industrial metals and agriculture

– have fallen in a 10-20% range, a fairly homogenous per-

formance. What’s more, the supply glut is being fed by

three common factors. Cost-cutting has led producers to

think they can bear the pain of falling prices for longer.

Heavy hitters, whether OPEC princes or global miners,

still yearn to increase market share. And funding is still

available.

The cost cuts are part of a self-reinforcing downward spi-

ral. Outside America, cheap currencies vis-à-vis the dollar

have made domestic inputs, such as manpower, appear

less pricey. Ironically, cheaper energy and steel help, too.

In Australia, for example, Gina Rinehart, a mining tycoon,

uses low costs to justify opening a $13 billion mine in the

outback that is expected to produce 55m tonnes of iron

ore a year – as much as America’s annual output.

In the oil world, cost cuts have come from producers once

thought likely to be wiped out by falling oil prices: shale

producers. “Frackers” have slashed a third off their cost

bases, and continue to pump enough black stuff to de-

press prices. Lower costs may give them a false sense of

security about where prices will go: when crude prices

temporarily ticked higher in America this spring, the num-

ber of drilling rigs rose for the first time since December.

Shortly afterward prices fell again.

Among drilling titans, efforts to recoup market share from

fracking upstarts can appear counterproductive. Led by

Saudi Arabia, OPEC is pumping well above its 30m barrel-

a-day quota, helping push crude prices to below $47 a

barrel on August 19th, just about the lowest level since

March 2009. But if it intended to strangle American shale

producers, its plan has backfired, instead pushing frackers

to become more efficient. Meanwhile global miners such

as BHP Billiton and Rio Tinto have continued to increase

iron-ore production, despite plunging prices. Analysts say

they are trying to drive higher-cost competitors in China

and elsewhere out of business.

Funding avenues have not closed down, however. Tomás

Gutiérrez of Kallanish Commodities, an industry watcher,

notes that in China steel output has only recently peaked.

Yet rather than facing

bankruptcy, many

inefficient steel pro-

ducers are limping

along thanks to local-

government support.

Their surpluses are

exported, adding to

the pressure on glob-

al steel prices (see

chart 2).

In the oil industry Goldman’s Mr Currie says that, unusual-

ly, high-cost output, such as Canada’s tar sands, is owned

by oil majors with strong balance-sheets. Though they

have cut spending, it may take longer to shut down entire

projects.

Eventually stresses will manifest themselves more violent-

ly. Small shale producers may find themselves in a pickle

unless prices stop falling. Deutsche Bank notes that ener-

gy companies account for about one in six of America’s

high-yield borrowers. It believes American crude prices

below $55 a barrel may push them into financial distress.

OPEC has its own invalids, such as Venezuela, Nigeria

and Libya.

But the latest leg down in crude prices may not yet have

run its course. Saudi Arabia, the all-important swing pro-

ducer of the cartel, is deaf to talk of a cutback. Earlier this

month it raised $5 billion to offset flagging oil income.

America’s summer driving season is ending. If an Iran nu-

clear deal is ratified by America’s Congress next month,

8

8

Bunzl Distribution Newsletter | Commodity Watch August 2015

Goodbye To All That Continued from pg. 7

once-embargoed oil will start flowing. Glencore, an Anglo-

Swiss miner and commodities trader, reported whopping

losses on August 19th. Its boss, Ivan Glasenberg, has

railed against rivals unwilling to throttle back production

and decried “prices that are still not making any sense”.

If these are daunting headwinds, they are not unusual.

When prices fall far enough for long enough, output does

eventually decline, as it started to do with nickel last year.

In the meantime, big mining and oil firms will take over

smaller ones and shut down their weakest assets. Then

another decades-long cycle can start.ᴥ

Prices Fall Continued from pg. 1

North American PE makers now have taken the almost

unprecedented step of advising their customers that prices

are expected to decline by 4 cents per pound in Septem-

ber. Market sources said this likely is an attempt to stop

prices from falling even farther in light of recent stock mar-

ket volatility, which has threatened to destabilize global

economies.

Oil prices remain a global price-setter for PE, even though

most PE made in North America is derived from natural

gas. West Texas Intermediate oil prices were above $45

per barrel on Aug. 1, but were near $39 per barrel by the

end of the month, for a drop of about 13 percent. Prices

since then have rebounded to above $46 in late trading

Sept. 2.

Abundant supplies of PE also played a role in the 5-cent

price drop, according to Mike Burns, a PE market analyst

with Resin Technology Inc. in Fort Worth, Texas.

“There are no supply issues for polyethylene or ethylene,”

Burns said in a phone interview. “You can almost say that

globally.”

PE demand remains solid

PE demand growth in the U.S. and Canada remained solid

through July, according to the American Chemistry Council

in Washington. High density PE sales in the region were up

almost 6 percent in that seven-month period, with domestic

growth of 2 percent boosted by a gain of almost 29 percent

in export sales.

For low density PE, seven-month sales ticked up almost 2

percent, with 3.5 percent domestic growth hampered by a

loss of more than 4 percent in export sales. The linear low

density PE market fared better, with sales up almost 6 per-

cent in that time frame. Domestic LLDPE growth of almost

7 percent was softened by growth of only 2 percent in the

export market.

The August PP decline averaged 2 cents per pound, alt-

hough that amount could vary, depending on how much of

a decrease buyers saw in July. The two-month July-August

dip totaled 3 cents per pound. Some saw that move in 1.5-

cent increments, others saw 1 cent in July and 2 in August,

or vice versa.

The August PP drop was the second straight month prices

for the material have fallen and the third decline in four

months. Regional PP prices now are down a net of 17

cents per pound so far in 2015.

At the same time, PP makers in the region have been able

to increase their profit margins by about 10 cents per

pound in 2015. They’ve done so by lowering prices by less

than the amounts that propylene monomer feedstock pric-

es have fallen. By comparison, producers only gained 1

cent in margin per year in 2013 and 2014.

Tight PP supplies

They’ve been able to take that step because of tight sup-

plies of PP in the region, according to Scott Newell, a PP

market analyst with RTI. “Operating rates [for PP] are as

high as we’ve seen in many years,” he said by phone.

“They’re above 92 percent for the year and in these last

couple of months have been close to 95 percent. Supply is

tight, and when you add in some production issues and

other dynamics, things can get pinched here and there.”

North American PP growth was solid in the first seven

months of 2015, growing 5.3 percent. A 5.9 percent do-

mestic growth rate was dampened by a 10 percent slide in

export sales.

Regional PS prices tumbled an average of 2 cents per

pound in August. Some buyers reported 3 cent drops, but 2

seemed to be the market average and is being shown on

this week’s Plastics News resin pricing chart. That drop

came only a month after prices rose 6 cents, prompted by

higher prices for benzene feedstock.

9

9

Bunzl Distribution Newsletter | Commodity Watch August 2015

Prices Fall For Most Commodity

Resins Continued from pg. 8

Benzene prices for August, however, fell about 8 percent

to $2.80 per gallon, sending PS resin prices down as well.

Regional PS prices now are down a net of 4 cents per

pound in 2015.

PS suppliers announce decreases

The region’s three major PS makers had pre-announced

price decreases for August. The market apparently was

able to hold to the 2-cent drops announced by Americas

Styrenics and Styrolution instead of the 3-cent decline of-

fered by Total Petrochemicals.

North American PS sales through July essentially were flat

vs. the year-ago period. Sales into the market’s leading

food packaging/food service sector grew 2 percent in those

seven months.

For PVC, prices ticked down an average of 1 cent per

pound as seasonal construction activity began to slow in

the region. Prior to that decline, prices for the material had

been flat for four consecutive months. The 1-cent August

drop now has regional PVC prices right back where they

started on Jan. 1.

U.S./Canadian PVC sales essentially were flat through

July, as a gain of almost 3 percent in export sales was

canceled out by a decline of almost 2 percent for sales into

the domestic market. Sales into PVC’s flagship rigid pipe

and tubing market also were essentially flat for the seven-

month period.

PET bottle resin’s 4-cent August drop wiped out a 3-cent

hike that some buyers saw in June and others saw in July.

In August, some buyers reported a 5-cent price drop, but 4

seemed to the number seen by most buyers and is being

shown on this week’s PN chart.

For the year, North American PET prices now are up a net

of 2 cents per pound. The market continues to struggle

with lower consumption of carbonated soft drinks and with

increased use of thinner water bottles that use less PET

per unit.ᴥ

Copyright © 2013 Bunzl Distribution USA, Inc. All rights reserved. This document is the property of Bunzl and its affiliated companies, and is intended only for the person(s) or entity to which it is ad-dressed and may contain confidential and/or privileged information. It may not be reproduced, distributed or otherwise made available to other parties without the explicit written approval of Bunzl and its

legal department. Information has been obtained from sources believed reliable. However, because of the possibility of human or mechanical error by sources, Bunzl or others, Bunzl does not guarantee the accuracy, adequacy or completeness of any such information and is not responsible for any errors or omissions or for results obtained from use of such information.