commodity outlook: do fundamentals support continued …€¦ · commodity outlook: do fundamentals...

TRANSCRIPT

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

© 2017 IHS Markit. All Rights Reserved.

Commodity Outlook: Do Fundamentals Support Continued Growth?

6 February 2018 | Frankfurt, Germany

Katie Tamblin, Director, Pricing and Purchasing

+44 (0) 791 712 8457, [email protected]

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Contents

WEIVREVO TEKRAM YTIDOMMOC

RAW MATERIALS FOR BATTERIES: COBALT, LITHIUM

STEEL

PETROCHEMICALS: PLASTICS & POLYMERS

WAGES – EASTERN EUROPEAN OUTLOOK

RECOMMENDATIONS

Commodities/ Feb 2018

2

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

POLL QUESTION!

Presentation Name / Month 2017

3

How will December 2018 commodity prices compare to January

prices?

Higher

More or less the same

Lower

It depends

Access this poll on the event app!

https://api.cvent.com/polling/v1/api/polls/spxb0jyc

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

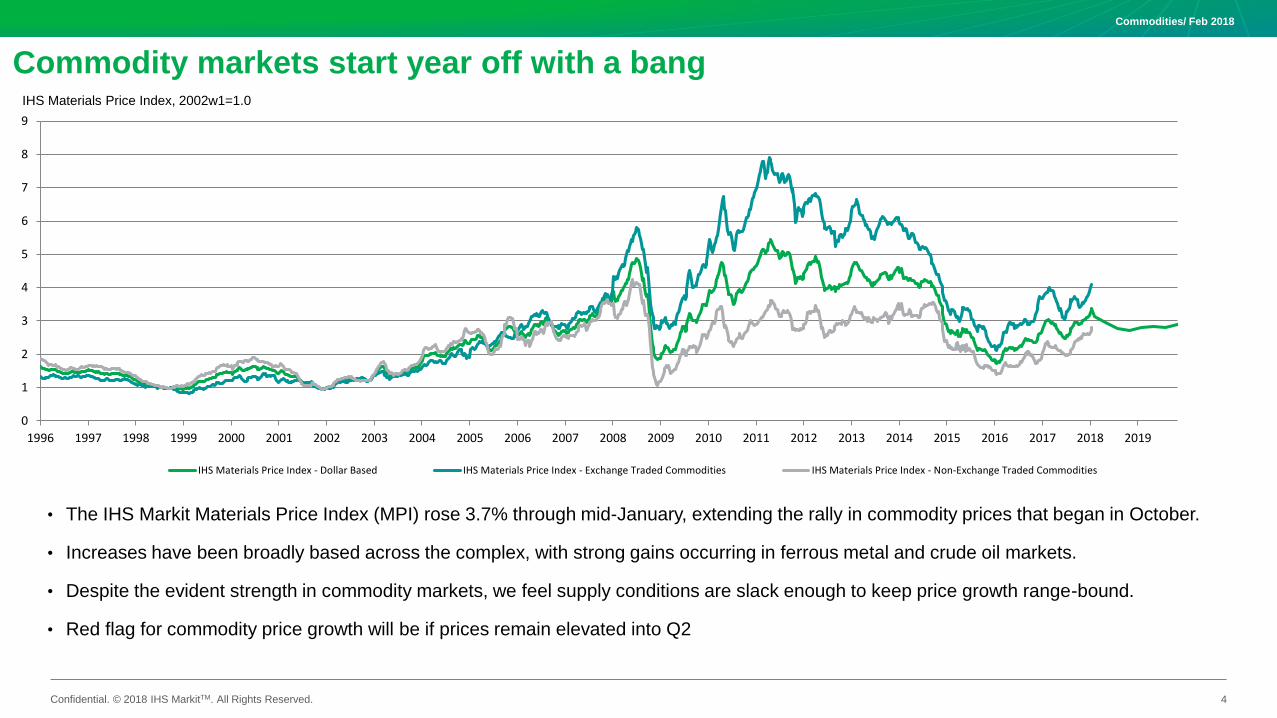

Commodity markets start year off with a bang

• The IHS Markit Materials Price Index (MPI) rose 3.7% through mid-January, extending the rally in commodity prices that began in October.

• Increases have been broadly based across the complex, with strong gains occurring in ferrous metal and crude oil markets.

• Despite the evident strength in commodity markets, we feel supply conditions are slack enough to keep price growth range-bound.

• Red flag for commodity price growth will be if prices remain elevated into Q2

4

0

1

2

3

4

5

6

7

8

9

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

IHS Materials Price Index - Dollar Based IHS Materials Price Index - Exchange Traded Commodities IHS Materials Price Index - Non-Exchange Traded Commodities

IHS Materials Price Index, 2002w1=1.0

Commodities/ Feb 2018

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

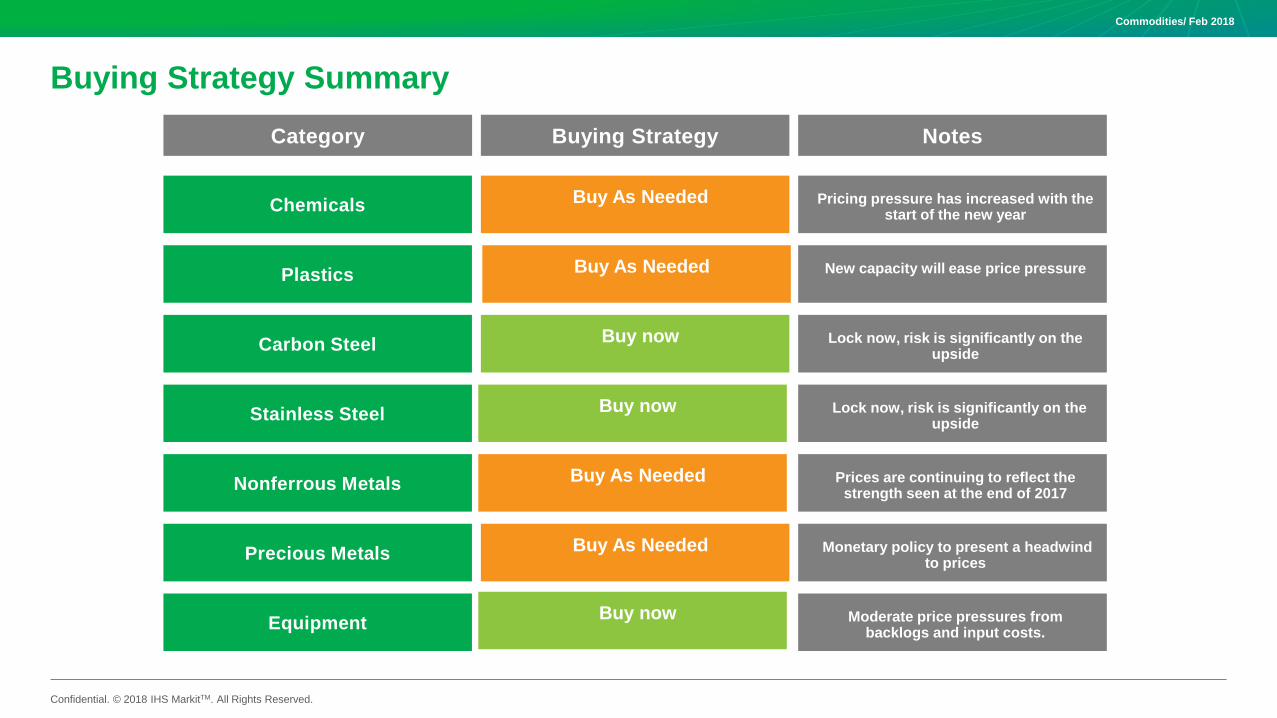

Buying Strategy Summary

Chemicals

Carbon Steel

Stainless Steel

Nonferrous Metals

Precious Metals

Category Buying Strategy Notes

Equipment

Plastics

Pricing pressure has increased with the start of the new year

New capacity will ease price pressure

Lock now, risk is significantly on the upside

Lock now, risk is significantly on the upside

Prices are continuing to reflect the strength seen at the end of 2017

Monetary policy to present a headwind to prices

Moderate price pressures from backlogs and input costs.

Buy As Needed

Buy now

Buy As Needed

Buy now

Buy As Needed

Buy As Needed

Buy now

Commodities/ Feb 2018

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

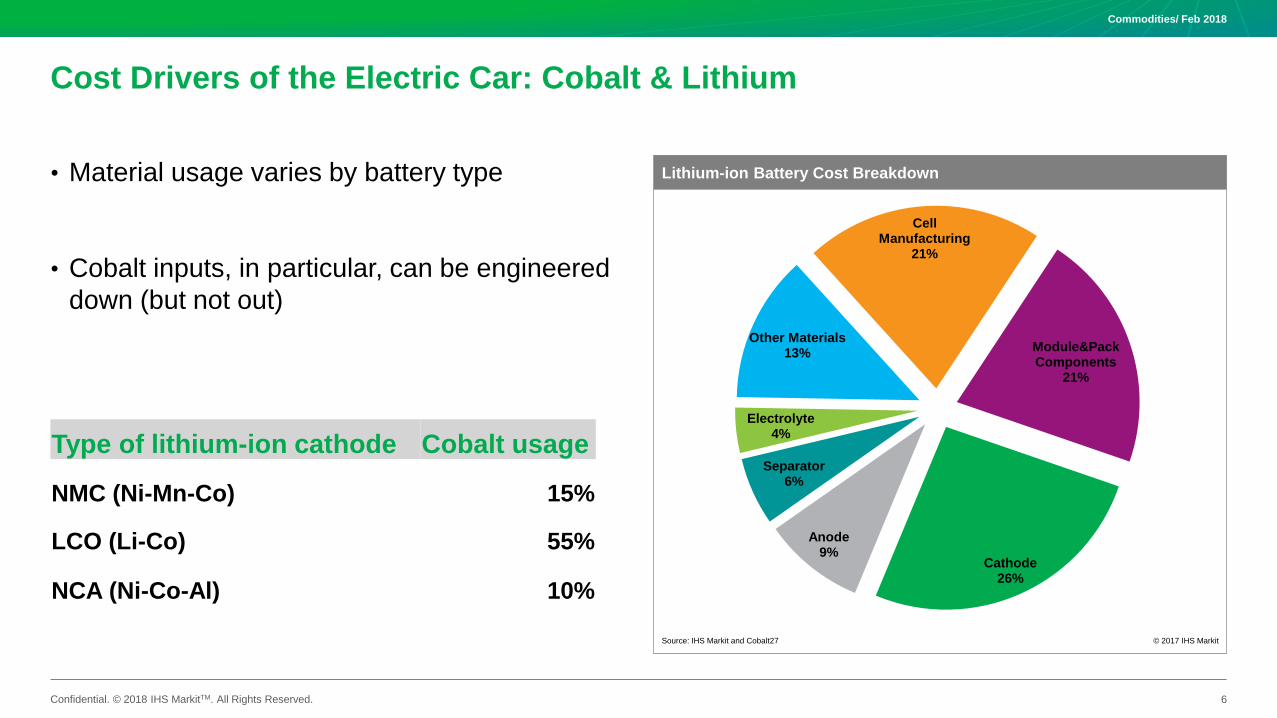

Cost Drivers of the Electric Car: Cobalt & Lithium

• Material usage varies by battery type

• Cobalt inputs, in particular, can be engineered

down (but not out)

Commodities/ Feb 2018

6

Cathode26%

Anode9%

Separator6%

Electrolyte4%

Other Materials13%

Cell Manufacturing

21%

Module&Pack Components

21%

Lithium-ion Battery Cost Breakdown

Source: IHS Markit and Cobalt27 © 2017 IHS Markit

Type of lithium-ion cathode Cobalt usage

NMC (Ni-Mn-Co) 15%

LCO (Li-Co) 55%

NCA (Ni-Co-Al) 10%

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

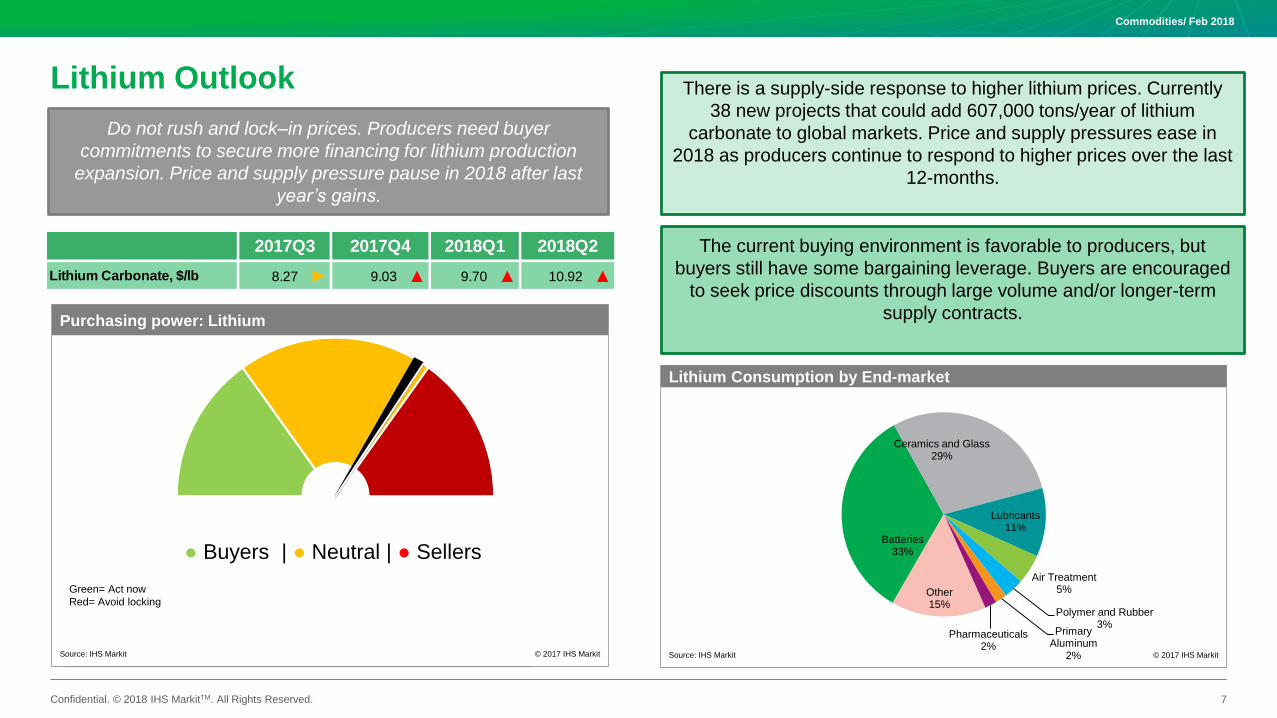

Lithium Outlook

7

The current buying environment is favorable to producers, but

buyers still have some bargaining leverage. Buyers are encouraged

to seek price discounts through large volume and/or longer-term

supply contracts.

There is a supply-side response to higher lithium prices. Currently

38 new projects that could add 607,000 tons/year of lithium

carbonate to global markets. Price and supply pressures ease in

2018 as producers continue to respond to higher prices over the last

12-months.

Do not rush and lock–in prices. Producers need buyer

commitments to secure more financing for lithium production

expansion. Price and supply pressure pause in 2018 after last

year’s gains.

Purchasing power: Lithium

Source: IHS Markit © 2017 IHS Markit

● Buyers | ● Neutral | ● Sellers

Green= Act now

Red= Avoid locking

● Buyers | ● Neutral | ● SellersBatteries

33%

Ceramics and Glass29%

Lubricants11%

Air Treatment5%

Polymer and Rubber3%

Primary Aluminum

2%

Pharmaceuticals2%

Other15%

Lithium Consumption by End-market

Source: IHS Markit © 2017 IHS Markit

Lithium Carbonate, $/lb 8.27 ► 9.03 ▲ 9.70 ▲ 10.92 ▲

2017Q3 2017Q4 2018Q1 2018Q2

Commodities/ Feb 2018

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

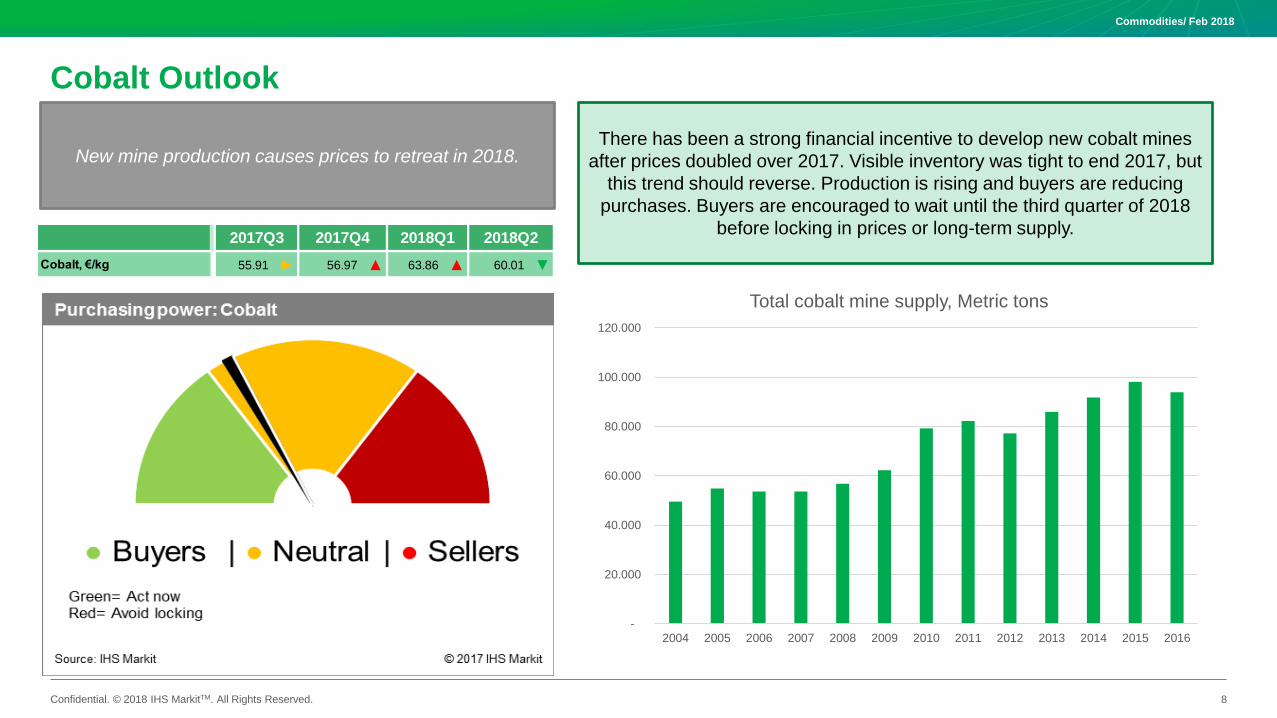

Cobalt Outlook

8

There has been a strong financial incentive to develop new cobalt mines

after prices doubled over 2017. Visible inventory was tight to end 2017, but

this trend should reverse. Production is rising and buyers are reducing

purchases. Buyers are encouraged to wait until the third quarter of 2018

before locking in prices or long-term supply.

New mine production causes prices to retreat in 2018.

-

20.000

40.000

60.000

80.000

100.000

120.000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Total cobalt mine supply, Metric tons

Cobalt, €/kg 55.91 ► 56.97 ▲ 63.86 ▲ 60.01 ▼

2017Q3 2017Q4 2018Q1 2018Q2

Commodities/ Feb 2018

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Traditional Raw Material Cost Drivers

Commodities/ Feb 2018

9

Confidential. © 2017 IHS MarkitTM. All Rights Reserved.

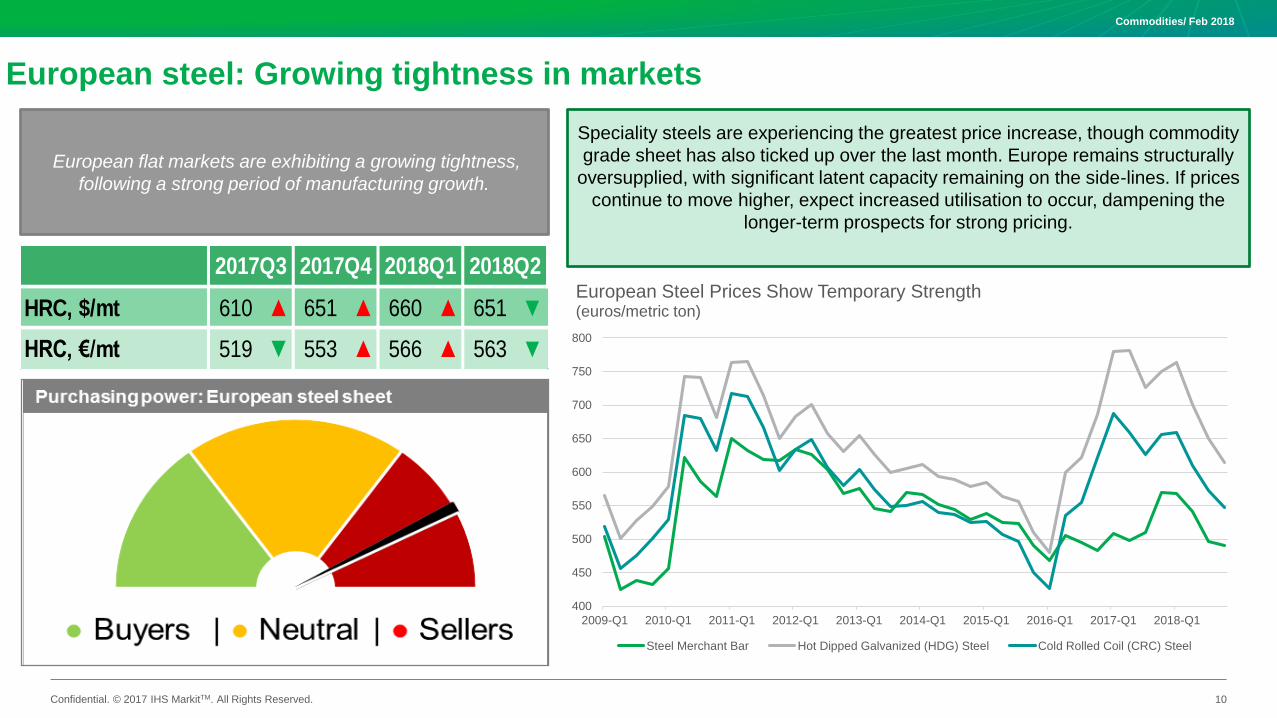

Speciality steels are experiencing the greatest price increase, though commodity

grade sheet has also ticked up over the last month. Europe remains structurally

oversupplied, with significant latent capacity remaining on the side-lines. If prices

continue to move higher, expect increased utilisation to occur, dampening the

longer-term prospects for strong pricing.

European steel: Growing tightness in markets

10

European flat markets are exhibiting a growing tightness,

following a strong period of manufacturing growth.

HRC, $/mt 610 ▲ 651 ▲ 660 ▲ 651 ▼

HRC, €/mt 519 ▼ 553 ▲ 566 ▲ 563 ▼

2017Q3 2017Q4 2018Q1 2018Q2

400

450

500

550

600

650

700

750

800

2009-Q1 2010-Q1 2011-Q1 2012-Q1 2013-Q1 2014-Q1 2015-Q1 2016-Q1 2017-Q1 2018-Q1

European Steel Prices Show Temporary Strength(euros/metric ton)

Steel Merchant Bar Hot Dipped Galvanized (HDG) Steel Cold Rolled Coil (CRC) Steel

Commodities/ Feb 2018

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

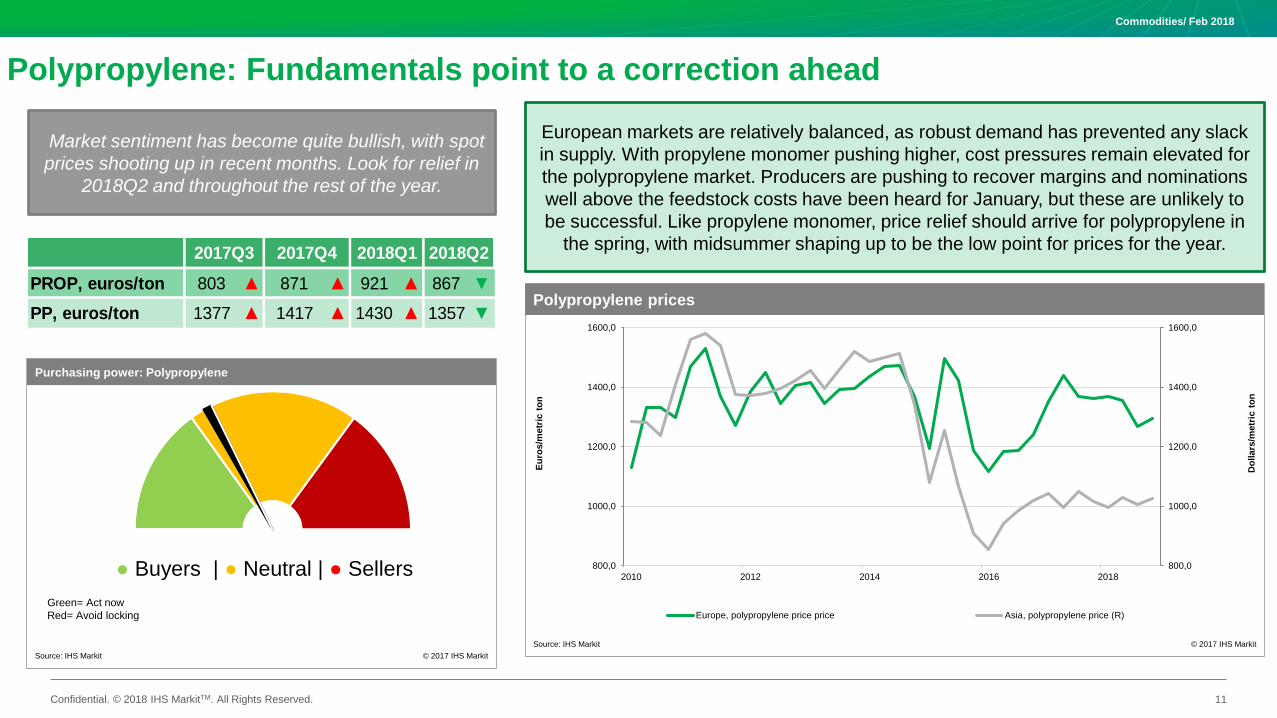

European markets are relatively balanced, as robust demand has prevented any slack

in supply. With propylene monomer pushing higher, cost pressures remain elevated for

the polypropylene market. Producers are pushing to recover margins and nominations

well above the feedstock costs have been heard for January, but these are unlikely to

be successful. Like propylene monomer, price relief should arrive for polypropylene in

the spring, with midsummer shaping up to be the low point for prices for the year.

Polypropylene: Fundamentals point to a correction ahead

11

Market sentiment has become quite bullish, with spot

prices shooting up in recent months. Look for relief in

2018Q2 and throughout the rest of the year.

PROP, euros/ton 803 ▲ 871 ▲ 921 ▲ 867 ▼

PP, euros/ton 1377 ▲ 1417 ▲ 1430 ▲ 1357 ▼

2017Q3 2017Q4 2018Q1 2018Q2

800,0

1000,0

1200,0

1400,0

1600,0

800,0

1000,0

1200,0

1400,0

1600,0

2010 2012 2014 2016 2018

Europe, polypropylene price price Asia, polypropylene price (R)

Polypropylene prices

Source: IHS Markit © 2017 IHS Markit

Eu

ros/m

etr

icto

n

Do

llars

/metr

ic t

on

Purchasing power: Polypropylene

Source: IHS Markit © 2017 IHS Markit

● Buyers | ● Neutral | ● Sellers

Green= Act now

Red= Avoid locking

Commodities/ Feb 2018

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

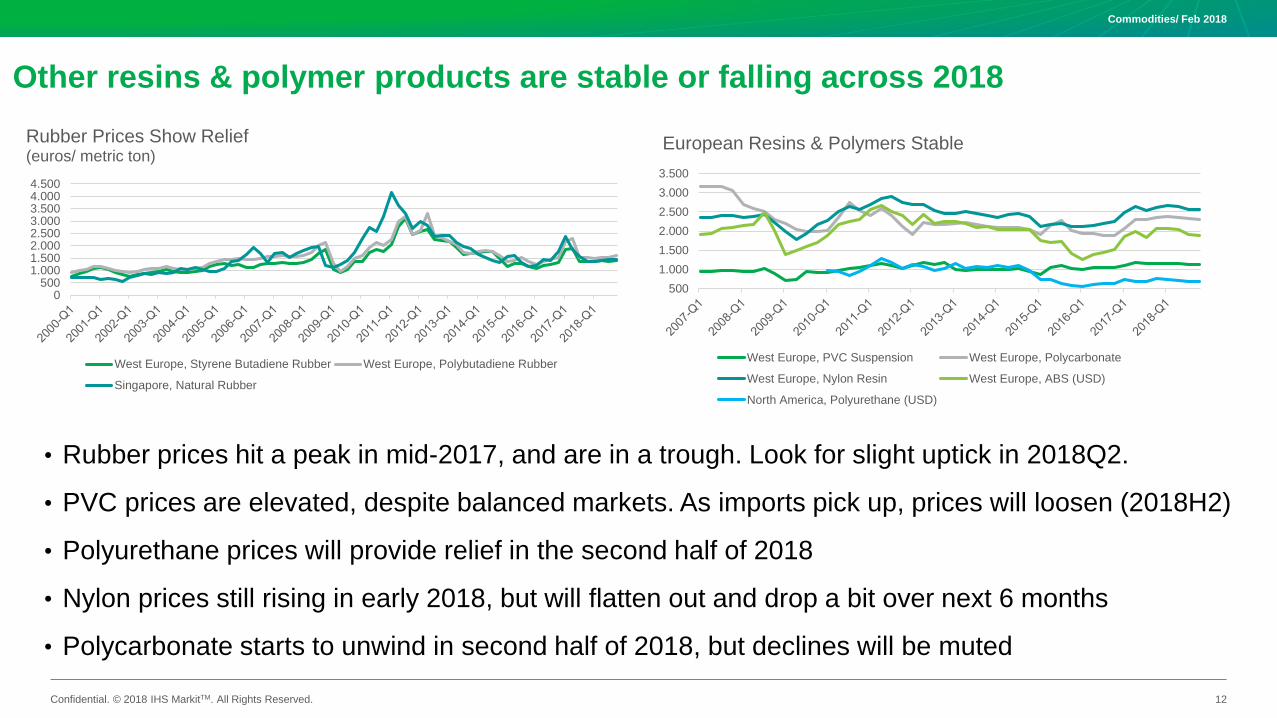

Other resins & polymer products are stable or falling across 2018

• Rubber prices hit a peak in mid-2017, and are in a trough. Look for slight uptick in 2018Q2.

• PVC prices are elevated, despite balanced markets. As imports pick up, prices will loosen (2018H2)

• Polyurethane prices will provide relief in the second half of 2018

• Nylon prices still rising in early 2018, but will flatten out and drop a bit over next 6 months

• Polycarbonate starts to unwind in second half of 2018, but declines will be muted

500

1.000

1.500

2.000

2.500

3.000

3.500

European Resins & Polymers Stable

West Europe, PVC Suspension West Europe, Polycarbonate

West Europe, Nylon Resin West Europe, ABS (USD)

North America, Polyurethane (USD)

0500

1.0001.5002.0002.5003.0003.5004.0004.500

Rubber Prices Show Relief(euros/ metric ton)

West Europe, Styrene Butadiene Rubber West Europe, Polybutadiene Rubber

Singapore, Natural Rubber

Commodities/ Feb 2018

12

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Investment tightens labor markets in Eastern Europe

Commodities/ Feb 2018

13

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

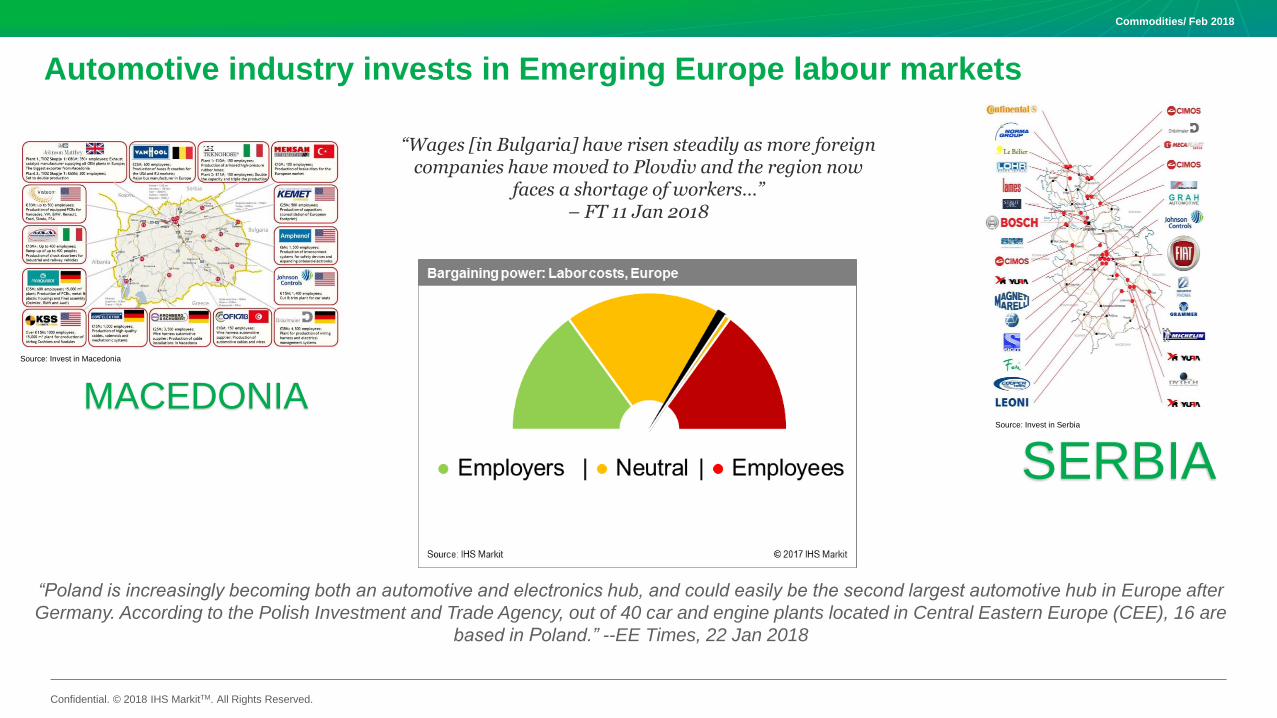

Automotive industry invests in Emerging Europe labour markets

Source: Invest in Macedonia

MACEDONIA

SERBIASource: Invest in Serbia

“Poland is increasingly becoming both an automotive and electronics hub, and could easily be the second largest automotive hub in Europe after

Germany. According to the Polish Investment and Trade Agency, out of 40 car and engine plants located in Central Eastern Europe (CEE), 16 are

based in Poland.” --EE Times, 22 Jan 2018

“Wages [in Bulgaria] have risen steadily as more foreign companies have moved to Plovdiv and the region now

faces a shortage of workers…” – FT 11 Jan 2018

Commodities/ Feb 2018

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

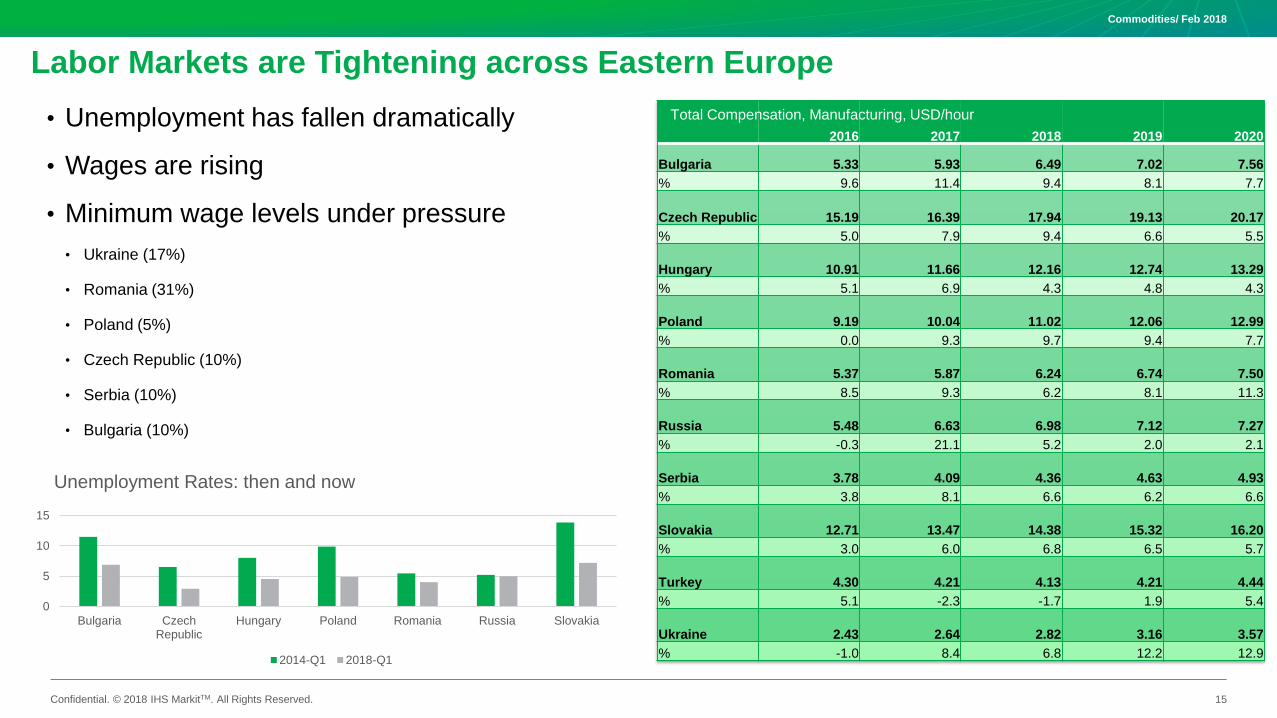

Labor Markets are Tightening across Eastern Europe

• Unemployment has fallen dramatically

• Wages are rising

• Minimum wage levels under pressure

• Ukraine (17%)

• Romania (31%)

• Poland (5%)

• Czech Republic (10%)

• Serbia (10%)

• Bulgaria (10%)

2016 2017 2018 2019 2020

Bulgaria 5.33 5.93 6.49 7.02 7.56

% 9.6 11.4 9.4 8.1 7.7

Czech Republic 15.19 16.39 17.94 19.13 20.17

% 5.0 7.9 9.4 6.6 5.5

Hungary 10.91 11.66 12.16 12.74 13.29

% 5.1 6.9 4.3 4.8 4.3

Poland 9.19 10.04 11.02 12.06 12.99

% 0.0 9.3 9.7 9.4 7.7

Romania 5.37 5.87 6.24 6.74 7.50

% 8.5 9.3 6.2 8.1 11.3

Russia 5.48 6.63 6.98 7.12 7.27

% -0.3 21.1 5.2 2.0 2.1

Serbia 3.78 4.09 4.36 4.63 4.93

% 3.8 8.1 6.6 6.2 6.6

Slovakia 12.71 13.47 14.38 15.32 16.20

% 3.0 6.0 6.8 6.5 5.7

Turkey 4.30 4.21 4.13 4.21 4.44

% 5.1 -2.3 -1.7 1.9 5.4

Ukraine 2.43 2.64 2.82 3.16 3.57

% -1.0 8.4 6.8 12.2 12.9

Commodities/ Feb 2018

15

0

5

10

15

Bulgaria CzechRepublic

Hungary Poland Romania Russia Slovakia

Unemployment Rates: then and now

2014-Q1 2018-Q1

Total Compensation, Manufacturing, USD/hour

Confidential. © 2018 IHS MarkitTM. All Rights Reserved.

Conclusions & Recommendations

Batteries

• Don’t3QlitnuylppustlaboCnikcol

• Lithium prices should retreat in 2018H2

Steel

• Lock in for the short term if possible; potential for

turmoil in European pricing

• Dollar weakness will provide some relief

Plastics & Polymers

• Capture declines in rubber

• Hold out for relief:

• Polypropylene PVC

• Polyurethane Polycarbonate

• But beware of upside risk & supply outages

Investing in Eastern Europe

• Labor market conditions can vary widely and have

large impact on investment costs

• Understand country-specific cost dynamics &

minimum wage pressures before making

investment or sourcing decisions

Commodities/ Feb 2018

16

IHS Markit Customer Care

Americas: +1 800 IHS CARE (+1 800 447 2273)

Europe, Middle East, and Africa: +44 (0) 1344 328 300

Asia and the Pacific Rim: +604 291 3600

Disclaimer

The information contained in this presentation is confidential. Any unauthorized use, disclosure, reproduction, or dissemination, in full or in part, in any media or by any means, without the prior written permission of IHS Markit Ltd. or any of its affiliates ("IHS Markit") is

strictly prohibited. IHS Markit owns all IHS Markit logos and trade names contained in this presentation that are subject to license. Opinions, statements, estimates, and projections in this presentation (including other media) are solely those of the individual author(s) at the

time of writing and do not necessarily reflect the opinions of IHS Markit. Neither IHS Markit nor the author(s) has any obligation to update this presentation in the event that any content, opinion, statement, estimate, or projection (collectively, "information") changes or

subsequently becomes inaccurate. IHS Markit makes no warranty, expressed or implied, as to the accuracy, completeness, or timeliness of any information in this presentation, and shall not in any way be liable to any recipient for any inaccuracies or omissions. Without

limiting the foregoing, IHS Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with

any information provided, or any course of action determined, by it or any third party, whether or not based on any information provided. The inclusion of a link to an external website by IHS Markit should not be understood to be an endorsement of that website or the site's

owners (or their products/services). IHS Markit is not responsible for either the content or output of external websites. Copyright © 2017, IHS MarkitTM. All rights reserved and all intellectual property rights are retained by IHS Markit.

Presentation Name / Month 2017

Questions?