commodity exchange

DESCRIPTION

commoditiesTRANSCRIPT

1.1 Introduction To Derivatives

The origin of derivatives can be traced back to the need of farmers to protect themselves against

fluctuations in the price of their crop. From the time of sowing to the time of crop harvest,

farmers would face price uncertainty. Through the use of simple derivative products, it was

possible for the farmer to partially or fully transfer price risks by locking-in asset prices. These

were simple contracts developed to meet the needs of farmers and were basically a means of

reducing risk.

A farmer who sowed his crop in June faced uncertainty over the price he would receive for his

harvest in September. In years of scarcity, he would probably obtain attractive prices. However,

during times of oversupply, he would have to dispose off his harvest at a very low price.

Clearly this meant that the farmer and his family were exposed to a high risk of price uncertainty.

On the other hand, a merchant with an ongoing requirement of grains too would face a price risk

that of having to pay exorbitant prices during scarcity, although favorable prices could be

obtained during periods of oversupply. Under such circumstances, it clearly made sense for the

farmer and the merchant to come together and enter into a contract whereby the price of the

grain to be delivered in September could be decided earlier. What they would then negotiate

happened to be a futures-type contract, which would enable both parties to eliminate the price

risk.

In 1848, the Chicago Board of Trade (CBOT) was established to bring farmers and merchants

together. A group of traders got together and created the `to-arrive' contract that permitted

farmers to lock in to price upfront and deliver the grain later. These to-arrive contracts proved

useful as a device for hedging and speculation on price changes. These were eventually

standardized, and in 1925 the first futures clearing house came into existence.

Today, derivative contracts exist on a variety of commodities such as corn, pepper, cotton,

wheat, silver, etc. Besides commodities, derivatives contracts also exist on a lot of financial

underlying like stocks, interest rate, exchange rate, etc.

Derivates can be defined as, "A derivative is a product whose value is derived from the value of

one or more underlying variables or assets in a contractual manner." The underlying asset can be

equity, forex, commodity or any other asset. As earlier stated, we saw that wheat farmers may

wish to sell their harvest at a future date to eliminate the risk of a change in prices by that date.

Such a transaction is an example of a derivative. The price of this derivative is driven by the spot

price of wheat which is the 'underlying' in this case.

The Forward Contracts (Regulation) Act, 1952, regulates the forward/ futures contracts in

commodities all over India. As per this Act, the Forward Markets Commission (FMC) continues

to have jurisdiction over commodity forward/ futures contracts. However, when derivatives

trading in securities was introduced in 2001, the term 'security' in the Securities Contracts

(Regulation) Act, 1956 (SC(R)A), was amended to include derivative contracts in securities.

Consequently, regulation of derivatives came under the purview of Securities Exchange Board

of India (SEBI). We thus have separate regulatory authorities for securities and commodity

derivative markets.

Derivatives are securities under the SC(R)A and hence the trading of derivatives is governed by

the regulatory framework under the SC(R)A. The Securities Contracts (Regulation) Act, 1956

defines 'derivative' to include -

1. A security derived from a debt instrument, share, loan whether secured or unsecured, risk

instrument or contract for differences or any other form of security.

2. A contract which derives its value from the prices, or index of prices, of underlying

securities.

1.1.2 Products, Participants And Functions

Derivative contracts are of different types. The most common ones are forwards, futures, options

and swaps. Participants who trade in the derivatives market can be classified under the following

three broad categories: hedgers, speculators, and arbitragers.

1. Hedgers: The farmer's example that we discussed about was a case of hedging. Hedgers

face risk associated with the price of an asset. They use the futures or options markets to

reduce or eliminate this risk.

2. Speculators: Speculators are participants who wish to bet on future movements in the

price of an asset. Futures and options contracts can give them leverage; that is, by

putting in small amounts of money upfront, they can take large positions on the market.

As a result of this leveraged speculative position, they increase the potential for large

gains as well as large losses.

3. Arbitragers: Arbitragers work at making profits by taking advantage of discrepancy

between prices of the same product across different markets. If, for example, they see

the futures price of an asset getting out of line with the cash price, they would take

offsetting positions in the two markets to lock in the profit.

1.1.3 Economic functions performed with the help of derivative market:

• Prices in an organized derivatives market reflect the perception of market participants

about the future and lead the prices of underlying to the perceived future level. The

prices of derivatives converge with the prices of the underlying at the expiration of the

derivative contract. Thus, derivatives help in discovery of future as well as current

prices.

• The derivatives market helps to transfer risks from those who have them but may not like

them to those who have an appetite for them.

• Derivatives, due to their inherent nature, are linked to the underlying cash markets.

• With the introduction of derivatives the underlying market witnesses higher trading

volumes, because of participation by more players who would not otherwise participate

for lack of an arrangement to transfer risk.

• Speculative traders shift to a more controlled environment of the derivatives market. In

the absence of an organized derivatives market, speculators trade in the underlying cash

markets. Margining, monitoring and surveillance of the activities of various participants

become extremely difficult in these kinds of mixed markets.

• An important incidental benefit that flows from derivatives trading is that it acts as a

catalyst for new entrepreneurial activity. Derivatives have a history of attracting many

bright, creative, well-educated people with an entrepreneurial attitude. They often

energize others to create new businesses, new products and new employment

opportunities, the benefit of which are immense.

• Derivatives markets help increase savings and investment in the long run. The transfer of

risk enables market participants to expand their volume of activity

1.1.4 Types of derivative markets

Derivatives markets can broadly be classified as commodity derivatives market and financial

derivatives markets. As the name suggest, commodity derivatives markets trade contracts are

those for which the underlying asset is a commodity. It can be an agricultural commodity like

wheat, soybeans, rapeseed, cotton, etc or precious metals like gold, silver, etc. or energy

products like crude oil, natural gas, coal, electricity etc. Financial derivatives markets trade

contracts have a financial asset or variable as the underlying. The more popular financial

derivatives are those which have equity, interest rates and exchange rates as the underlying. The

most commonly used derivatives contracts are forwards, futures and options.

Spot versus Forward Transaction

Every transaction has three components - trading, clearing and settlement. A buyer and seller

come together, negotiate and arrive at a price. This is trading. Clearing involves finding out the

net outstanding, that is exactly how much of goods and money the two should exchange. For

instance, A buys goods worth Rs.100 from B and sells goods worth Rs. 50 to B. On a net basis,

A has to pay Rs. 50 to B. Settlement is the actual process of exchanging money and goods.

Using the example of a forward contract, let us try to understand the difference between a spot

and derivatives contract.

In a spot transaction, the trading, clearing and settlement happens instantaneously, i.e. 'on the

spot'. Consider this example. On 1st January 2010, Aditya wants to buy some gold. The

goldsmith quotes Rs. 17,000 per 10 grams. They agree upon this price and Aditya buys 20 grams

of gold. He pays Rs.34,000, takes the gold and leaves. This is a spot transaction.

Now suppose, Aditya does not want to buy the gold on the 1st January, but wants to buy it a

month later. The goldsmith quotes Rs. 17,100 per 10 grams. They agree upon the 'forward' price

for 20 grams of gold that Aditya wants to buy and Aditya leaves. A month later, he pays the

goldsmith Rs. 34,200 and collects his gold. This is a forward contract, a contract by which two

parties irrevocably agree to settle a trade at a future date, for a stated price and quantity. No

money changes hands when the contract is signed. The exchange of money and the underlying

goods only happens at the future date as specified in the contract. In a forward contract, the

process of trading, clearing and settlement does not happen instantaneously. The trading happens

today, but the clearing and settlement happens at the end of the specified period.

A forward contract is the most basic derivative contract. We call it a derivative because it

derives value from the price of the asset underlying the contract, in this case- gold. If on the1st

of February, gold trades for Rs. 17,200 per 10 grams in the spot market, the contract becomes

more valuable to Aditya because it now enables him to buy gold at Rs.17,100 per 10 grams. If

however, the price of gold drops down to Rs. 16,900 per 10 grams he is worse off because as per

the terms of the contract, he is bound to pay Rs. 17,100 per 10 grams for the same gold. The

contract has now lost value from Adyta's point of view. Note that the value of the forward

contract to the goldsmith varies exactly in an opposite manner to its value for Aditya.

Exchange Traded Versus OTC Derivatives

Derivatives have probably been around for as long as people have been trading with one another.

Forward contracting dates back at least to the 12th century and may well have been around

before then. These contracts were typically OTC kind of contracts. Over the counter (OTC)

derivatives are privately negotiated contracts. Merchants entered into contracts with one another

for future delivery of specified amount of commodities at specified price. A primary motivation

for prearranging a buyer or seller for a stock of commodities in early forward contracts was to

lessen the possibility that large swings would inhibit marketing the commodity after a harvest

Later many of these contracts were standardized in terms of quantity and delivery dates and

began to trade on an exchange.

The OTC derivatives markets have the following features compared to exchange-traded

derivatives:

1. The management of counter-party (credit) risk is decentralized and located within

individual institutions.

2. There are no formal centralized limits on individual positions, leverage, or margining.

3. There are no formal rules for risk and burden-sharing.

4. There are no formal rules or mechanisms for ensuring market stability and integrity, and

for safeguarding the collective interests of market participants.

5. The OTC contracts are generally not regulated by a regulatory authority and the

exchange's self-regulatory organization, although they are affected indirectly by national

legal systems, banking supervision and market surveillance.

The derivatives markets have witnessed rather sharp growth over the last few years, which have

accompanied the modernization of commercial and investment banking and globalization of

financial activities. The recent developments in information technology have contributed to a

great extent to these developments. While both exchange-traded and OTC derivative contracts

offer many benefits, the former have rigid structures compared to the latter.

The largest OTC derivative market is the inter-bank foreign exchange market. Commodity

derivatives, the world over are typically exchange-traded and not OTC in nature.

1.1.5 Difference Between Commodity And Financial Derivatives

The basic concept of a derivative contract remains the same whether the underlying happens to

be a commodity or a financial asset. However, there are some features which are very peculiar to

commodity derivative markets. In the case of financial derivatives, most of these contracts are

cash settled. Since financial assets are not bulky, they do not need special facility for storage

even in case of physical settlement. On the other hand, due to the bulky nature of the underlying

assets, physical settlement in commodity derivatives creates the need for warehousing.

Similarly, the concept of varying quality of asset does not really exist as far as financial

underlying are concerned. However, in the case of commodities, the quality of the asset

underlying a contract can vary largely. This becomes an important issue to be managed. We

have a brief look at these issues.

Physical Settlement

Physical settlement involves the physical delivery of the underlying commodity, typically at an

accredited warehouse. The seller intending to make delivery would have to take the commodities

to the designated warehouse and the buyer intending to take delivery would have to go to the

designated warehouse and pick up the commodity. This may sound simple, but the physical

settlement of commodities is a complex process. The issues faced in physical settlement are

enormous. There are limits on storage facilities in different states. There are restrictions on

interstate movement of commodities. Besides state level octroi and duties have an impact on the

cost of movement of goods across locations. The process of taking physical delivery in

commodities is quite different from the process of taking physical delivery in financial assets.

Delivery notice period

Unlike in the case of equity futures, typically a seller of commodity futures has the option to

give notice of delivery. This option is given during a period identified as `delivery notice period'.

Assignment

Whenever delivery notices are given by the seller, the clearing house of the Exchange identifies

the buyer to whom this notice may be assigned. Exchanges follow different practices for the

assignment process.

Delivery

The procedure for buyer and seller regarding the physical settlement for different types of

contracts is clearly specified by the Exchange. The period available for the buyer to take

physical delivery is stipulated by the Exchange. Buyer or his authorized representative in the

presence of seller or his representative takes the physical stocks against the delivery order. Proof

of physical delivery having been effected is forwarded by the seller to the clearing house and the

invoice amount is credited to the seller's account.

The clearing house decides on the delivery order rate at which delivery will be settled. Delivery

rate depends on the spot rate of the underlying adjusted for discount/ premium for quality and

freight costs. The discount/ premium for quality and freight costs are published by the clearing

house before introduction of the contract. The most active spot market is normally taken as the

benchmark for deciding spot prices.

Warehousing

One of the main differences between financial and commodity derivative is the need for

warehousing. In case of most exchange-traded financial derivatives, all the positions are cash

settled. Cash settlement involves paying up the difference in prices between the time the contract

was entered into and the time the contract was closed. For instance, if a trader buys futures on a

stock at Rs.100 and on the day of expiration, the futures on that stock close at Rs.120, he does

not really have to buy the underlying stock. All he does is take the difference of Rs.20 in cash.

Similarly, the person who sold this futures contract at Rs.100 does not have to deliver the

underlying stock. All he has to do is pay up the loss of Rs.20 in cash.

In case of commodity derivatives however, there is a possibility of physical settlement. It means

that if the seller chooses to hand over the commodity instead of the difference in cash,

the buyer must take physical delivery of the underlying asset. This requires the Exchange to

make an arrangement with warehouses to handle the settlements. The efficacy of the

commodities settlements depends on the warehousing system available. Such warehouses have

to perform the following functions:

• Earmark separate storage areas as specified by the Exchange for storing commodities;

• Ensure proper grading of commodities before they are stored;

• Store commodities according to their grade specifications and validity period; and

• Ensure that necessary steps and precautions are taken to ensure that the quantity and

grade of commodity, as certified in the warehouse receipt, are maintained during the

storage period. This receipt can also be used as collateral for financing.

In India, NCDEX has accredited over 775 delivery centers which meet the requirements for the

physical holding of goods that are to be delivered on the platform. As future trading is delivery

based, it is necessary to create the logistics support for the same.

1.1.6 Quality of Underlying Assets

A derivatives contract is written on a given underlying. Variance in quality is not an issue in

case of financial derivatives as the physical attribute is missing. When the underlying asset is a

commodity, the quality of the underlying asset is of prime importance. There may be quite some

variation in the quality of what is available in the marketplace. When the asset is specified, it is

therefore important that the Exchange stipulate the grade or grades of the commodity that are

acceptable. Commodity derivatives demand good standards and quality assurance/ certification

procedures. A good grading system allows commodities to be traded by specification.

Trading in commodity derivatives also requires quality assurance and certifications from

specialized agencies. In India, for example, the Bureau of Indian Standards (BIS) under the

Department of Consumer Affairs specifies standards for processed agricultural commodities.

AGMARK, another certifying body under the Department of Agriculture and Cooperation,

specifies standards for basic agricultural commodities.

1.2 INTRODUCTION TO COMMODITY MARKET

The study of Indian derivatives markets in Money & Finance

would be incomplete without an account of the commodity derivatives

market in the country. In this paper we attempt to bring forth the nature

of information flows between futures and spot prices in the market for

commodity derivatives in India, taking into consideration the history of

commodity derivatives globally, and the importance of and problems

associated with commodity markets particularly in less mature economies.

In our previous studies on the Indian stock and futures markets

we have seen that the characteristics exhibited by the price index/

returns in these markets are more or less in agreement with or at least

lean towards what should be expected in a mature or efficient market.

Here we make an attempt to see whether price movements in the Indian

commodity derivatives market exhibit similar trends or not, particularly

as this market is less developed compared to the financial derivatives

markets, being constrained by its chequered history with many

policy reversals.

What is “Commodity”?

Any product that can be used for commerce or an article of commerce which is traded on an

authorized commodity exchange is known as commodity. The article should be movable of

value, something which is bought or sold and which is produced or used as the subject or barter

or sale. In short commodity includes all kinds of goods. Indian Forward Contracts (Regulation)

Act (FCRA), 1952 defines “goods” as “every kind of movable property other than actionable

claims, money and securities”.

In current situation, all goods and products of agricultural (including plantation), mineral and

fossil origin are allowed for commodity trading recognized under the FCRA. The national

commodity exchanges, recognized by the Central Government, permits commodities which

include precious (gold and silver) and non-ferrous metals, cereals and pulses, ginned and un-

ginned cotton, oilseeds, oils and oilcakes, raw jute and jute goods, sugar and gur, potatoes and

onions, coffee and tea, rubber and spices. Etc.

What is a commodity exchange?

A commodity exchange is an association or a company or any other body corporate organizing

futures trading in commodities for which license has been granted by regulating authority.

What is Commodity Future

A Commodity futures is an agreement between two parties to buy or sell a specified and

standardized quantity of a commodity at a certain time in future at a price agreed upon at the

time of entering into the contract on the commodity futures exchange. The need for a futures

market arises mainly due to the hedging function that it can perform. Commodity markets, like

any other financial instrument, involve risk associated with frequent price volatility. The loss

due to price volatility can be attributed to the following reasons:

Consumer Preferences: - In the short-term, their influence on price volatility is small since it is

a slow process permitting manufacturers, dealers and wholesalers to adjust their inventory in

advance.

Changes in supply: - They are abrupt and unpredictable bringing about wild fluctuations in

prices. This can especially noticed in agricultural commodities where the weather plays a major

role in affecting the fortunes of people involved in this industry. The futures market has evolved

to neutralize such risks through a mechanism; namely hedging.

The objectives of Commodity futures: -

Hedging with the objective of transferring risk related to the possession of physical assets

through any adverse moments in price. Liquidity and Price discovery to ensure base

minimum volume in trading of a commodity through market information and demand

supply factors that facilitates a regular and authentic price discovery mechanism.

Maintaining buffer stock and better allocation of resources as it augments reduction in

inventory requirement and thus the exposure to risks related with price fluctuation

declines. Resources can thus be diversified for investments.

Price stabilization along with balancing demand and supply position. Futures trading

leads to predictability in assessing the domestic prices, which maintains stability, thus

safeguarding against any short term adverse price movements. Liquidity in Contracts of

the commodities traded also ensures in maintaining the equilibrium between demand and

supply.

Flexibility, certainty and transparency in purchasing commodities facilitate bank

financing. Predictability in prices of commodity would lead to stability, which in turn

would eliminate the risks associated with running the business of trading commodities.

This would make funding easier and less stringent for banks to commodity market

players.

Benefits of Commodity Futures Markets:-

The primary objectives of any futures exchange are authentic price discovery and an efficient

price risk management. The beneficiaries include those who trade in the commodities being

offered in the exchange as well as those who have nothing to do with futures trading. It is

because of price discovery and risk management through the existence of futures exchanges that

a lot of businesses and services are able to function smoothly.

1. Price Discovery:-Based on inputs regarding specific market information, the demand

and supply equilibrium, weather forecasts, expert views and comments, inflation rates,

Government policies, market dynamics, hopes and fears, buyers and sellers conduct

trading at futures exchanges. This transforms in to continuous price discovery

mechanism. The execution of trade between buyers and sellers leads to assessment of fair

value of a particular commodity that is immediately disseminated on the trading terminal.

2. Price Risk Management: - Hedging is the most common method of price risk

management. It is strategy of offering price risk that is inherent in spot market by taking

an equal but opposite position in the futures market. Futures markets are used as a mode

by hedgers to protect their business from adverse price change. This could dent the

profitability of their business. Hedging benefits who are involved in trading of

commodities like farmers, processors, merchandisers, manufacturers, exporters,

importers etc.

3. Import- Export competitiveness: - The exporters can hedge their price risk and

improve their competitiveness by making use of futures market. A majority of traders

which are involved in physical trade internationally intend to buy forwards. The

purchases made from the physical market might expose them to the risk of price risk

resulting to losses. The existence of futures market would allow the exporters to hedge

their proposed purchase by temporarily substituting for actual purchase till the time is

ripe to buy in physical market. In the absence of futures market it will be meticulous,

time consuming and costly physical transactions.

4. Predictable Pricing: - The demand for certain commodities is highly price elastic. The

manufacturers have to ensure that the prices should be stable in order to protect their

market share with the free entry of imports. Futures contracts will enable predictability in

domestic prices. The manufacturers can, as a result, smooth out the influence of changes

in their input prices very easily. With no futures market, the manufacturer can be caught

between severe short-term price movements of oils and necessity to maintain price

stability, which could only be possible through sufficient financial reserves that could

otherwise be utilized for making other profitable investments.

5. Benefits for farmers/Agriculturalists: - Price instability has a direct bearing on farmers

in the absence of futures market. There would be no need to have large reserves to cover

against unfavorable price fluctuations. This would reduce the risk premiums associated

with the marketing or processing margins enabling more returns on produce. Storing

more and being more active in the markets. The price information accessible to the

farmers determines the extent to which traders/processors increase price to them. Since

one of the objectives of futures exchange is to make available these prices as far as

possible, it is very likely to benefit the farmers. Also, due to the time lag between

planning and production, the market-determined price information disseminated by

futures exchanges would be crucial for their production decisions.

6. Credit accessibility: - The absence of proper risk management tools would attract the

marketing and processing of commodities to high-risk exposure making it risky business

activity to fund. Even a small movement in prices can eat up a huge proportion of capital

owned by traders, at times making it virtually impossible to pay back the loan. There is a

high degree of reluctance among banks to fund commodity traders, especially those who

do not manage price risks. If in case they do, the interest rate is likely to be high and

terms and conditions very stringent. This posses a huge obstacle in the smooth

functioning and competition of commodities market. Hedging, which is possible through

futures markets, would cut down the discount rate in commodity lending.

7. Improved product quality: - The existence of warehouses for facilitating delivery with

grading facilities along with other related benefits provides a very strong reason to

upgrade and enhance the quality of the commodity to grade that is acceptable by the

exchange. It ensures uniform standardization of commodity trade, including the terms of

quality standard: the quality certificates that are issued by the exchange-certified

warehouses have the potential to become the norm for physical trade.

History of Evolution of commodity markets

Commodities future trading was evolved from need of assured continuous supply of seasonal

agricultural crops. The concept of organized trading in commodities evolved in Chicago, in

1848. But one can trace its roots in Japan. In Japan merchants used to store Rice in warehouses

for future use. To raise cash warehouse holders sold receipts against the stored rice. These were

known as “rice tickets”. Eventually, these rice tickets become accepted as a kind of commercial

currency. Latter on rules came in to being, to standardize the trading in rice tickets. In 19 th

century Chicago in United States had emerged as a major commercial hub. So that wheat

producers from Mid-west attracted here to sell their produce to dealers & distributors. Due to

lack of organized storage facilities, absence of uniform weighing & grading mechanisms

producers often confined to the mercy of dealers discretion. These situations lead to need of

establishing a common meeting place for farmers and dealers to transact in spot grain to deliver

wheat and receive cash in return.

Gradually sellers & buyers started making commitments to exchange the produce for cash in

future and thus contract for “futures trading” evolved. Whereby the producer would agree to sell

his produce to the buyer at a future delivery date at an agreed upon price. In this way producer

was aware of what price he would fetch for his produce and dealer would know about his cost

involved, in advance. This kind of agreement proved beneficial to both of them. As if dealer is

not interested in taking delivery of the produce, he could sell his contract to someone who needs

the same. Similarly producer who not intended to deliver his produce to dealer could pass on the

same responsibility to someone else. The price of such contract would dependent on the price

movements in the wheat market. Latter on by making some modifications these contracts

transformed in to an instrument to protect involved parties against adverse factors such as

unexpected price movements and unfavorable climatic factors. This promoted traders entry in

futures market, which had no intentions to buy or sell wheat but would purely speculate on price

movements in market to earn profit.

Trading of wheat in futures became very profitable which encouraged the entry of other

commodities in futures market. This created a platform for establishment of a body to regulate

and supervise these contracts. That’s why Chicago Board of Trade (CBOT) was established in

1848. In 1870 and 1880s the New York Coffee, Cotton and Produce Exchanges were born.

Agricultural commodities were mostly traded but as long as there are buyers and sellers, any

commodity can be traded. In 1872, a group of Manhattan dairy merchants got together to bring

chaotic condition in New York market to a system in terms of storage, pricing, and transfer of

agricultural products. In 1933, during the Great Depression, the Commodity Exchange, Inc. was

established in New York through the merger of four small exchanges – the National Metal

Exchange, the Rubber Exchange of New York, the National Raw Silk Exchange, and the New

York Hide Exchange.

The largest commodity exchange in USA is Chicago Board of Trade, The Chicago Mercantile

Exchange, the New York Mercantile Exchange, the New York Commodity Exchange and New

York Coffee, sugar and cocoa Exchange. Worldwide there are major futures trading exchanges

in over twenty countries including Canada, England, India, France, Singapore, Japan, Australia

and New Zealand.

History of Commodity Market in India:-

The Commodity Futures market in India dates back to more than a century. The first organized

futures market was established in 1875, under the name of ’Bombay Cotton Trade Association’

to trade in cotton derivative contracts. This was followed by institutions for futures trading in

oilseeds, food grains, etc. The futures market in India underwent rapid growth between the

period of First and Second World War. As a result, before the outbreak of the Second World

War, a large number of commodity exchanges trading futures contracts in several commodities

like cotton, groundnut, groundnut oil, raw jute, jute goods, castor seed, wheat, rice, sugar,

precious metals like gold and silver were flourishing throughout the country. In view of the

delicate supply situation of major commodities in the backdrop of war efforts mobilization,

futures trading came to be prohibited during the Second World War under the Defence of India

Act. After Independence, especially in the second half of the 1950s and first half of 1960s, the

commodity futures trading again picked up and there were thriving commodity markets.

However, in mid-1960s, commodity futures trading in most of the commodities was banned and

futures trading continued in two minor commodities, viz, pepper and turmeric.

The history of organized commodity derivatives in India goes back to the nineteenth century

when Cotton Trade Association started futures trading in 1875, about a decade after they started

in Chicago. Over the time datives market developed in several commodities in India. Following

Cotton, derivatives trading started in oilseed in Bombay (1900), raw jute and jute goods in

Calcutta (1912), Wheat in Hapur (1913) and Bullion in Bombay (1920).

However many feared that derivatives fuelled unnecessary speculation and were detrimental to

the healthy functioning of the market for the underlying commodities, resulting in to banning of

commodity options trading and cash settlement of commodities futures after independence in

1952. The parliament passed the Forward Contracts (Regulation) Act, 1952, which regulated

contracts in Commodities all over the India. The act prohibited options trading in Goods along

with cash settlement of forward trades, rendering a crushing blow to the commodity derivatives

market. Under the act only those associations/exchanges, which are granted reorganization from

the Government, are allowed to organize forward trading in regulated commodities. The act

envisages three tire regulations: (i) Exchange which organizes forward trading in commodities

can regulate trading on day-to-day basis; (ii) Forward Markets Commission provides regulatory

oversight under the powers delegated to it by the central Government. (iii) The Central

Government- Department of Consumer Affairs, Ministry of Consumer Affairs, Food and Public

Distribution- is the ultimate regulatory authority.

The commodities future market remained dismantled and remained dormant for about four

decades until the new millennium when the Government, in a complete change in a policy,

started actively encouraging commodity market. After Liberalization and Globalization in 1990,

the Government set up a committee (1993) to examine the role of futures trading. The

Committee (headed by Prof. K.N. Kabra) recommended allowing futures trading in 17

commodity groups. It also recommended strengthening Forward Markets Commission, and

certain amendments to Forward Contracts (Regulation) Act 1952, particularly allowing option

trading in goods and registration of brokers with Forward Markets Commission. The

Government accepted most of these recommendations and futures’ trading was permitted in all

recommended commodities. It is timely decision since internationally the commodity cycle is on

upswing and the next decade being touched as the decade of Commodities.

Commodity exchange in India plays an important role where the prices of any commodity are

not fixed, in an organized way. Earlier only the buyer of produce and its seller in the market

judged upon the prices. Others never had a say.

Today, commodity exchanges are purely speculative in nature. Before discovering the price,

they reach to the producers, end-users, and even the retail investors, at a grassroots level. It

brings a price transparency and risk management in the vital market. A big difference between a

typical auction, where a single auctioneer announces the bids and the Exchange is that people

are not only competing to buy but also to sell. By Exchange rules and by law, no one can bid

under a higher bid, and no one can offer to sell higher than someone else’s lower offer. That

keeps the market as efficient as possible, and keeps the traders on their toes to make sure no one

gets the purchase or sale before they do. Since 2002, the commodities future market in India has

experienced an unexpected boom in terms of modern exchanges, number of commodities

allowed for derivatives trading as well as the value of futures trading in commodities, which

crossed $ 1 trillion mark in 2006. Since 1952 till 2002 commodity datives market was virtually

non- existent, except some negligible activities on OTC basis.

In India there are 25 recognized future exchanges, of which there are three national level multi-

commodity exchanges. After a gap of almost three decades, Government of India has allowed

forward transactions in commodities through Online Commodity Exchanges, a modification of

traditional business known as Adhat and Vayda Vyapar to facilitate better risk coverage and

delivery of commodities. The three exchanges are: National Commodity & Derivatives

Exchange Limited (NCDEX) Mumbai, Multi Commodity Exchange of India Limited (MCX)

Mumbai and National Multi-Commodity Exchange of India Limited (NMCEIL)

Ahmedabad.There are other regional commodity exchanges situated in different parts of India.

1875 Bombay Cotton Trade Association

Between 1st and 2nd World war Rapid growth of futures markets

During 2nd World War Defence of India Act- Prohibited Futures trading in major Commodities owing to short supply.

1950s to mid-1960s Thriving Commodity futures markets

Mid 1960s to 1970s Banned Commodity Futures trading in most of the Commodities except two minor Commodities- Pepper and Turmeric.

1980s Revival of Futures trading in Potato, Castor Seed and Gur (Jaggery).

1992 Futures trading in Hessian permitted.

1999 Futures trading in various edible oilseeds complexes permitted.

2000 The National Agricultural Policy-recognized the positive role of forward and futures markets in price discovery and price risk management.

2001 Futures trading in Sugar permitted.

2003 Lifted prohibition on futures trading in all Commodities

Recognition to 3 National Commodity Electronic Exchanges MCX, NCDEX and NMCE.

2008 Commission issued guidelines on setting up of New National Multi Commodity Exchanges.

2009 Recognition to ICEX as 4th National Exchange

2010 Recognition to ACE as 5th National Exchange.

Notified “Iron Ore” under section 15 of the FCRA, 1952.

2012 Recognition to UCX as 6th National Exchange.

Legal framework for regulating commodity futures in India:-

The commodity futures traded in commodity exchanges are regulated by the Government under

the Forward Contracts Regulations Act, 1952 and the Rules framed there under. The regulator

for the commodities trading is the Forward Markets Commission, situated at Mumbai, which

comes under the Ministry of Consumer Affairs Food and Public Distribution

Forward Markets Commission (FMC):-

It is statutory institution set up in 1953 under Forward Contracts (Regulation) Act, 1952.

Commission consists of minimum two and maximum four members appointed by Central Govt.

Out of these members there is one nominated chairman. All the exchanges have been set up

under overall control of Forward Market Commission (FMC) of Government of India.

There are 21 Commodity Exchanges (15 Regional and 6 National Exchanges) regulating futures

trading in commodities under the purview of the Forward Markets Commission (FMC).

Forward Markets Commission (FMC) headquartered at Mumbai, is a regulatory authority for commodity futures market in India. It is a statutory body set up under Forward Contracts (Regulation) Act 1952.

The Commission functioned under the administrative control of the Ministry of Consumer Affairs, Food & Public Distribution, Department of Consumer Affairs, Government of India till 5th

September. Thereafter the Commission has been functioning under the Ministry of Finance, Department of Economic Affairs, Government of India.

The Act provides that the Commission shall consist of not less than two but not exceeding four members appointed by the Central Government, out of them one being nominated by the Central Government to be the Chairman of the Commission. Currently the Commission comprises of three members among whom Shri. Ramesh Abhishek, IAS is the Chairman, Dr. M. Mathisekaran, IES and Shri Nagendraa Parakh are the Members of the Commission.

Functions

The functions of the Forward Markets Commission are as follows:

(a) To advise the Central Government in respect of the recognition or the withdrawal of recognition from any association or in respect of any other matter arising out of the administration of the Forward Contracts (Regulation) Act 1952;

(b) To keep forward markets under observation and to take such action in relation to them, as it may consider necessary, in exercise of the powers assigned to it by or under the Act;

(c) To collect and whenever the Commission thinks it necessary, to publish information regarding the trading conditions in respect of goods to which any of the provisions of the Act is made applicable, including information regarding supply, demand and prices, and to submit to the Central Government, periodical reports on the working of forward markets relating to such goods;

(d) To make recommendations generally with a view to improving the organization and working of forward markets;

(e) To undertake the inspection of the books of accounts and other documents of any recognized association or registered association or any member of such association whenever it considers it necessary.

The country's commodity futures exchanges are divided majorly into two categories:

• National exchanges

• Regional exchanges

The six exchanges operating at the national level (as on ) are:

i) National Commodity and Derivatives Exchange of India Ltd. (NCDEX)

ii) National Multi Commodity Exchange of India Ltd. (NMCE)

iii) Multi Commodity Exchange of India Ltd. (MCX)

iv) Indian Commodity Exchange Ltd. (ICEX) which started trading operations on November

27, 2009

v) ACE Derivatives and Commodity Exchange

The leading regional exchange is the National Board of Trade (NBOT) located at Indore. There

are more than 15 regional commodity exchanges in India.

National Commodities & Derivatives Exchange Limited (NCDEX)

National Commodities & Derivatives Exchange Limited (NCDEX) promoted by ICICI Bank

Limited (ICICI Bank), Life Insurance Corporation of India (LIC), National Bank of Agriculture

and Rural Development (NABARD) and National Stock Exchange of India Limited (NSC).

Punjab National Bank (PNB), Credit Rating Information Service of India Limited (CRISIL),

Indian Farmers Fertilizer Cooperative Limited (IFFCO), Canara Bank and Goldman Sachs by

subscribing to the equity shares have joined the promoters as a share holder of exchange.

NCDEX is the only Commodity Exchange in the country promoted by national level institutions.

NCDEX is a public limited company incorporated on 23 April 2003. NCDEX is a national level

technology driven on line Commodity Exchange with an independent Board of Directors and

professionals not having any vested interest in Commodity Markets.

It is committed to provide a world class commodity exchange platform for market participants to

trade in a wide spectrum of commodity derivatives driven by best global practices,

professionalism and transparency.

NCDEX is regulated by Forward Markets Commission (FMC). NCDEX is also subjected to the

various laws of land like the Companies Act, Stamp Act, Contracts Act, Forward Contracts

Regulation Act and various other legislations.

NCDEX is located in Mumbai and offers facilities to its members in more than 550 centers

throughout India. NCDEX currently facilitates trading of 57 commodities.

Multi Commodity Exchange of India Limited (MCX)

Multi Commodity Exchange of India Limited (MCX) is an independent and de-mutulized

exchange with permanent reorganization from Government of India, having Head Quarter in

Mumbai. Key share holders of MCX are Financial Technologies (India) Limited, State Bank of

India, Union Bank of India, Corporation Bank of India, Bank of India and Canara Bank. MCX

facilitates online trading, clearing and settlement operations for commodity futures market

across the country. MCX started of trade in Nov 2003 and has built strategic alliance with

Bombay Bullion Association, Bombay Metal Exchange, Solvent Extractors Association of India,

pulses Importers Association and Shetkari Sanghatana.MCX deals with about 100 commodities.

National Multi Commodity Exchange of India Limited (NMCEIL)

National Multi Commodity Exchange of India Limited (NMCEIL) is the first de-mutualised

Electronic Multi Commodity Exchange in India. On 25 th July 2001 it was granted approval by

Government to organize trading in edible oil complex. It is being supported by Central

warehousing Corporation Limited, Gujarat State Agricultural Marketing Board and Neptune

Overseas Limited. It got reorganization in Oct 2002. NMCEIL Head Quarter is at Ahmedabad.

Some of the features of national and regional exchanges are listed below:

National Exchanges

• Compulsory online trading

• Transparent trading

• Exchanges to be de-mutualised

• Exchange recognized on permanent basis

• Multi commodity exchange

• Large expanding volumes

Regional Exchanges

• Online trading not compulsory

• De-mutualisation not mandatory

• Recognition given for fixed period after which it could be given for re regulation

• Generally, these are single commodity exchanges. Exchanges have to apply for trading

each commodity.

• Low volumes in niche markets

No Exchanges Main Commodities1.

Multi Commodity Exchange Of India Ltd,Mumbai.

Zinc,Nickel,Aluminum, cotton, Lead, Gold, Natural Gas, Copper , Silver, Crude Oil, Other Commodities

2.National Commodity & Derivatives Exchange Ltd, Mumbai

Turmeric,Jeera, Soya Oil, Kapas Khali, Mustard Seed, Dhaniya, Soya been, Rape Mustard seed, Chana.

3.National Multi Commodity Exchange Of india Ltd, Ahmedabad

Raw jute, Castor Seed, Rape/mustard Seed, Chana, Coffee Red bulk.

4. Mustard Seed, Natural Gas, Silver,

Indian commodity Exchange Ltd, New Delhi Soyabeen,Iron ores

5.Ace Derivatives and Commodity Exchange Ltd,Mumbai.

CPO, Castor, Cotton, Soya been, Resoyoil,

6.Universal commodity Exchange Ltd, Navi Mumbai.

Channa, Turmeric, Soyabeen, Rape Mustard Seed,

How Commodity market works?

There are two kinds of trades in commodities. The first is the spot trade, in which one pays cash

and carries away the goods. The second is futures trade. The underpinning for futures is the

warehouse receipt. A person deposits certain amount of say, good X in a ware house and gets a

warehouse receipt. Which allows him to ask for physical delivery of the good from the

warehouse. But someone trading in commodity futures need not necessarily posses such a

receipt to strike a deal. A person can buy or sale a commodity future on an exchange based on

his expectation of where the price will go. Futures have something called an expiry date, by

when the buyer or seller either closes (square off) his account or give/take delivery of the

commodity. The broker maintains an account of all dealing parties in which the daily profit or

loss due to changes in the futures price is recorded. Squiring off is done by taking an opposite

contract so that the net outstanding is nil.

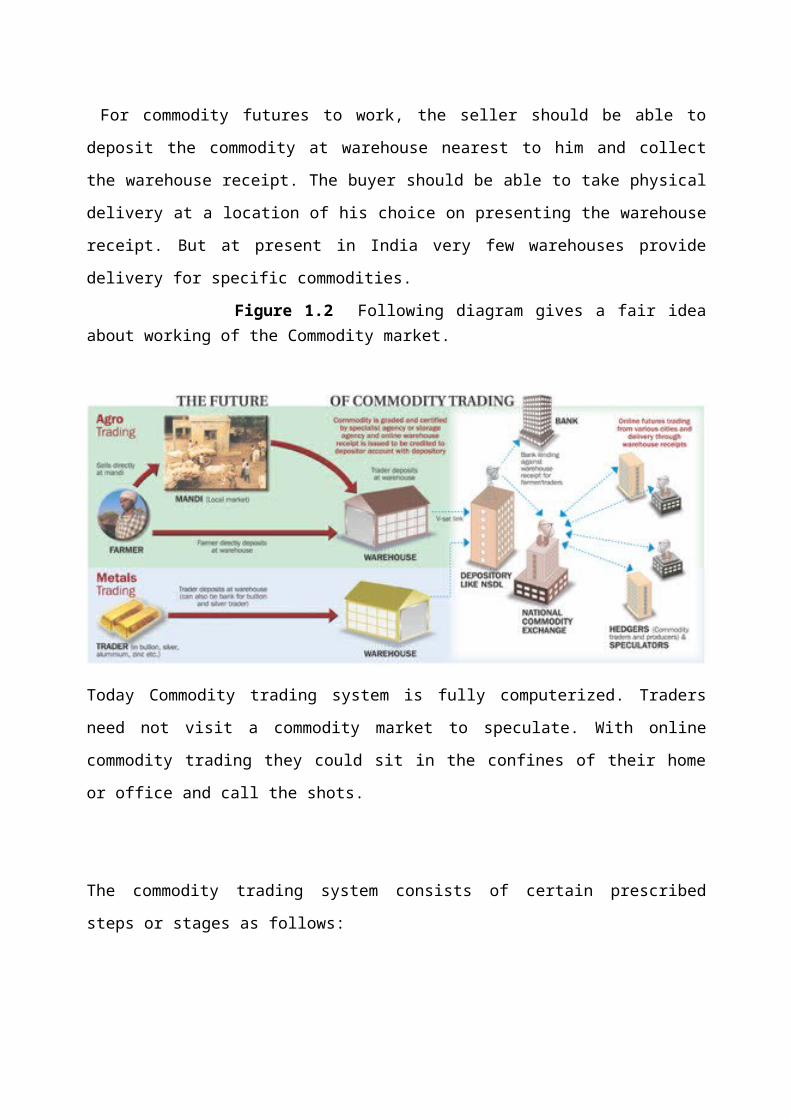

For commodity futures to work, the seller should be able to deposit the commodity at

warehouse nearest to him and collect the warehouse receipt. The buyer should be able to take

physical delivery at a location of his choice on presenting the warehouse receipt. But at present

in India very few warehouses provide delivery for specific commodities.

Figure 1.2 Following diagram gives a fair idea about working of the Commodity market.

Today Commodity trading system is fully computerized. Traders need not visit a commodity

market to speculate. With online commodity trading they could sit in the confines of their home

or office and call the shots.

The commodity trading system consists of certain prescribed steps or stages as follows:

I. Trading: - At this stage the following is the system implemented-

- Order receiving

- Execution

- Matching

- Reporting

- Surveillance

- Price limits

- Position limits

II. Clearing: - This stage has following system in place-

- Matching

- Registration

- Clearing

- Clearing limits

- Notation

- Margining

- Price limits

- Position limits

- Clearing house.

III. Settlement: - This stage has following system followed as follows-

- Marking to market

- Receipts and payments

- Reporting

- Delivery upon expiration or maturity.

How to invest in a Commodity Market?

With whom investor can transact a business?

An investor can transact a business with the approved clearing member of previously mentioned Commodity Exchanges. The investor can ask for the details from the Commodity Exchanges about the list of approved members.

What is Identity Proof?

When investor approaches Clearing Member, the member will ask for identity proof. For which Xerox copy of any one of the following can be given

a) PAN card Numberb) Driving Licensec) Vote IDd) Passport

What statements should be given for Bank Proof?

The front page of Bank Pass Book and a canceled cheque of a concerned bank. Otherwise the Bank Statement containing details can be given.

What are the particulars to be given for address proof?

In order to ascertain the address of investor, the clearing member will insist on Xerox copy of Ration card or the Pass Book/ Bank Statement where the address of investor is given.

What are the other forms to be signed by the investor?

The clearing member will ask the client to sign

a) Know your client formb) Risk Discloser Document

The above things are only procedure in character and the risk involved and only after understanding the business, he wants to transact business.

What aspects should be considered while selecting a commodity broker?

While selecting a commodity broker investor should ideally keep certain aspects in mind to ensure that they are not being missed in any which way. These factors include

Net worth of the broker of brokerage firm. The clientele. The number of franchises/branches. The market credibility. The references. The kind of service provided- back office functioning being most important. Credit facility. The research team. These are amongst the most important factors to calculate the credibility of commodity broker.

Broker:-

The Broker is essentially a person of firm that liaisons between individual traders and the commodity exchange. In other words the Commodity Broker is the member of Commodity Exchange, having direct connection with the exchange to carry out all trades legally. He is also known as the authorized dealer.

How to become a Commodity Trader/Broker of Commodity Exchange?

To become a commodity trader one needs to complete certain legal and binding obligations. There is routine process followed, which is stated by a unit of Government that lays

down the laws and acts with regards to commodity trading. A broker of Commodities is also required to meet certain obligations to gain such a membership in exchange.

To become a member of Commodity Exchange the broker of brokerage firm should have net worth amounting to Rs. 50 Lakh. This sum has been determined by Multi Commodity Exchange.

How to become a Member of Commodity Exchange?

To become member of Commodity Exchange the person should comply with the following Eligibility Criteria.

1. He should be Citizen of India.2. He should have completed 21 years of his age.3. He should be Graduate or having equivalent qualification.4. He should not be bankrupt.5. He has not been debarred from trading in Commodities by statutory/regulatory authority, There are following three types of Memberships of Commodity Exchanges.

Trading-cum-Clearing Member (TCM):-

A TCM is entitled to trade on his own account as well as on account of his clients, and clear and settle trades himself. A sole proprietor, Partnership firm, a joint Hindu Undivided Family (HUF), a corporate entity, a cooperative society, a public sector organization or any other Government or non-Government entity can become a TCM.

There are two types of TCM, TCM-1 and TCM-2. TCM-1 refers to transferable non-deposit based membership and TCM-2 refers to non-transferable deposit based membership.

A person desired to register as TCM is required to submit an application as per the format prescribed under the business rules, along with all enclosures, fee and other documents specified therein. He is required to go through interview by Membership Admission Committee and committee is also empowered to frame rules or criteria relating to selection or rejection of a member.

Institutional Trading-cum-clearing Member (ITCM):-

Only an Institution/ Corporate can be admitted by the Exchange as a member, conferring upon them the right to trade and clear through the clearing house of exchange as an Institutional Trading-cum-clearing Member (ITCM). The member may be allowed to make deals for himself

as well as on behalf of his clients and clear and settle such deals. ITCMs can also appoint sub-brokers, authorized persons and Trading Members who would be registered as trading members.

Professional Clearing Member (PCM):-

A PCM entitled to clear and settle trades executed by other members of the exchange. A corporate entity and an institution only can apply for PCM. The member would be allowed to clear and settle trades of such members of the Exchange who choose to clear and settle their trades through such PCM.

Current Scenario in Indian Commodity Market

Need of Commodity Derivatives for India:-

India is among top 5 producers of most of the Commodities, in addition to being a major

consumer of bullion and energy products. Agriculture contributes about 22% GDP of Indian

economy. It employees around 57% of the labor force on total of 163 million hectors of land

Agriculture sector is an important factor in achieving a GDP growth of 8-10%. All this indicates

that India can be promoted as a major centre for trading of commodity derivatives.

INITIATIVES OF THE COMMISSION IN 2013-14

Y Settlement Guarantee Fund: The Commission had issued guidelines regarding setting up of Settlement Guarantee Fund (SGF) in 2007. The SGF was operationalized in 2013 and the exchanges transferred ₹ 460.13 cr to SGF corpus as on 31/3/2014. This is a very important risk management initiative which has inspired much confidence among the market participants.

Y Corporate Governance: To strengthen corporate governance of the National Commodity Exchanges the Commission issued revised Guidelines to have a broad-based representation of all classes of shareholders on the Board of Directors of the Exchanges. This will improve Corporate Governance at the Exchanges and make Board of Directors more responsive and broad based, eliminating the dominance of non-institutional shareholders.

Y Strengthening of warehousing facilities: The Commission decided that all the

existing warehouses accredited by the Exchanges shall be registered with Warehousing Development and Regulatory Authority (WDRA) in a time-bound manner. This will strengthen the warehousing facility in the Commodity Futures market.

Y Risk Management Group: A Risk Management Group (RMG) was constituted to assist the Commission in formulating risk management policies and guidelines for Commodities Derivatives Market. RMG is chaired by Prof. J. R. Verma, IIM, Ahmedabad.

Y Incentives to hedgers: To reduce the cost of hedging, the Exchanges were directed to exempt the market participants, who have deposited certified goods against all the relevant futures contracts sold and earmarked for delivery, to the Exchange accredited warehouse, from paying initial, additional and special margins. Such participants will continue to remain exempted from payment of delivery margins. Besides, the Commission also permitted spread margin benefits to those having different month contracts of the same underlying commodity and to those having two contract variants having the same underlying commodity.

Y Margin Reporting: In order to regularly monitor the collection of margins by members and also provide a reasonable time to members for collection of margins from their

clients, the Commission on 14th March, 2014 revised its earlier instructions on short-collection/ non- collection of margins, so that the members will have time till ‘T+2’ working days to collect margins (except initial margins) from their clients and the Member shall report to the Exchange on T + 5 day the actual short collection/non collection of all margins from clients.

Y Approval of futures contracts on continuous basis: The Commission decided to grant continuous approval for trading in the futures contracts instead of the practice of giving permission for trading in futures contracts on yearly basis.

Y Consumer Protection- As a part of implementation of non-legislative recommendations of FSLRC, FMC adopted enhanced consumer protection measures which include requirement of professional diligence on the part of members and protection of consumers from unfair terms in financial contracts.

REGULATORY REFORMS UNDERTAKEN BY THE COMMISSION

1.1 Grant of Recognition / Renewal of Recognition to the association / recognized exchanges and grant of registration / renewal of registration to the recognized

exchanges.a) Renewal of Recognition to the Recognized Exchanges.

On recommendations of the Forward Markets Commission, the Government of India renewed the recognition of the following Associations / Exchanges:

Sr.No.

Name of the ExchangePeriod of renewal of Recognitionand the Commodities permitted

Date of issue ofNotification

1 Vijai Beopar Chamber Ltd,Muzaffarnagar

1st April, 2013 to 31st March,2014(Gur)

21st March ,2013

2 First Commodity Exchangeof India Ltd (FCEI), Kochi

1st June,2013 to 31st May, 2014(Coconut Oil and Copra)

13th June, 2013

a) Details of Grant/Renewal of Registration to the Recognized Exchanges.The Commission, in exercise of the powers conferred under Section 14(B) of the Forward Contracts (Regulation) Act, 1952, extended the period of registration of the following Associations / Exchanges, analogous to the period of recognition of the exchange:

Sr.No.

Name of the Exchange

Period of renewal of Registration and the Commodities permitted

Date of Issue of Registration1 Vijai Beopar Chamber Ltd,

Muzaffarnagar1st April, 2013 to 31st March,2014(Gur)

10th April, 2013

2 Bikaner Commodity Exchange Ltd, Bikaner

1st April 2013 to 31st March, 2014 (Guar Seed)

15th May, 2013

3 First Commodities Exchange of India Ltd., Kochi

1st June, 2013 to 31st May, 2014 (Coconut Oil and Copra)

28th June, 2013

a) The Commission also recommended to the Ministry to renew the recognition of thefollowing exchanges:

Sr. No. Name of the Exchange Commodities Period of Recognition

1 Surendranagar Cotton Oil & Oilseeds Association Ltd, Surendranagar

Kapas 1.04.2014 to 31.03.2019

a) Grant of permission for futures trading in Commodities:During the year, from 1st April 2013 to 31st March 2014, trading permission was granted to Multi Commodity Exchange of India (MCX), National Commodity Derivatives Exchange of

India, Mumbai (NCDEX), National Multi Commodity Exchange of India Ahmedabad, (NMCE), Indian Commodity Exchange Ltd., Mumbai (ICEX), ACE Commodity Exchange Ltd., Mumbai, (ACE) and Universal Commodity Exchange Ltd (UCX), Navi Mumbai as well as commodity specific Exchanges (Regional Exchanges). The Commodities vis-a-vis contracts permitted and the dates on which permission was issued are detailed in the Annexure-III and IV.

1.2 Revisions in margins

The Commission after reviewing the price volatility, volumes and open interest of Sugar and Wheat contracts, reduced the initial margin on Sugar and Wheat from 10% to 5% of the value of the contract or VaR based margin whichever is higher, with effect from 13th

May, 2013.

The Commission reviewed the price volatility, volumes and open interest in Chana, R/Mustard seed, Soybean and Refined Soya oil and reduced the initial margins in the aforesaid commodities from 10% to 5% of the value of the contract or VaR based margin whichever is higher with effect from 3rd July 2013.

In view of the current price volatility in the prices of Gold, Silver, Brent Crude Oil, Crude Oil and Natural Gas contracts, the Commission on 29th August, 2013 increased initial margin in respect of all the Gold contracts from existing level of 5% to 10% or VaR based margin whichever is higher. The Commission also imposed additional margin of 5% on all the Gold, Silver, Brent Crude Oil, Crude Oil and Natural Gas contracts. These margins were made effective from 2nd September, 2013.

As the price volatility in the contracts of Gold, Silver, Crude Oil, Brent Crude Oil, Natural gas, Aluminium, Copper, Lead, Nickel and Zinc subdued, the Commission on 4th

November, 2013 removed the additional margin of 5% on the said contracts.

The Commission on 12th February, 2014 conveyed its approval to the NCDEX Mumbai for withdrawal of the additional margin of 5% on long side and short side imposed by the Exchange on Castor seed contracts w.e.f. 14th February, 2014 due to subdued volatility in the prices.

In view of price volatility and other trading developments in the potato contracts at MCX , the Commission approved the proposal of MCX to impose an additional margin of 20% in March 2014 contract and 10% in April 2014 contract with effect from 13th February 2014.

Table 1.2 Commodity Futures Trade in India (Rs Lakhs Crores)

Category for April to MarchFY2013-14

Total 10144794.98

Bullion 4308937.82

Agro 1602401.96

Metals 1761359.89

Energy 2472095.31

According to Forward Markets Commission (FMC), the value of commodities traded from April

to march, 2013-14 was recorded at Rs 10144794.98 lakh crore in comparison to the value of

commodities traded from April to march FY 2012-13 was recorded at Rs 17046840.09 lakh

crore, suggesting decline in trading activity in 2013-14.

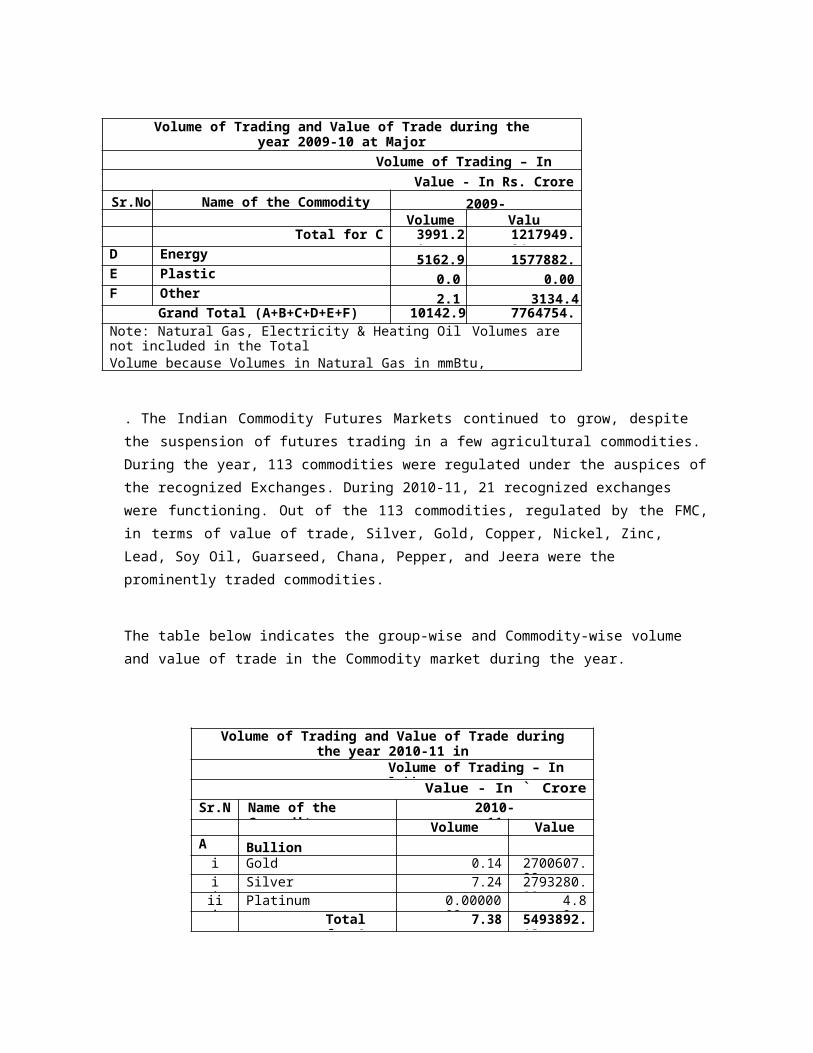

1 During 2009-10, forward trading was regulated in 109 commodities at 21 recognized exchanges. The break up of the total value of commodities traded stood as under-

• Bullion - Rs.31.64 lakh crore. (40.75%)• Base metals - Rs.18.02 lakh crore. (23.20%).• Energy products - Rs.15.78 lakh crore (20.32%)• Agricultural commodities-Rs.12.18 lakh crore (15.69%).

• Out of 21 recognized exchanges, Multi Commodity Exchange (MCX), Mumbai, National Commodity and Derivatives Exchange (NCDEX), Mumbai, National Multi Commodities Exchange, (NMCE), Ahmedabad, Indian Commodity Exchange, Ltd., Gurgon, National Board of Trade (NBOT), Indore, contributed 99.62% of the total value of the commodities traded during the year.

Volume of Trading and Value of Trade during the year 2009-10 at Major

CommoditiesVolume of Trading – In lakh tonne

Value - In Rs. Crore

Sr.No Name of the Commodity 2009-10Volume Value

A Bullioni Gold 0.126 1997801.0961

ii Silver 4.600 1165728.5591

iii Platinum 0.000 622.5880

Total for A 4.73 3164152.24B Metals other than Bullion

i Aluminium 57.38 53904.46

ii Copper 325.81 942590.17

iii Lead 244.50 240268.62

iv Nickel 33.79 284601.94

v Sponge Iron 0.00 0.00

vi Steel 35.94 8813.97

vii Tin 0.02 132.84

viii Zinc 284.48 271324.32Total for B 981.92 1801636.31

C Agricultural commoditiesi Chana/Gram 530.42 127950.47

ii Urad 0.00 0.00

iii Tur 0.00 0.00

iv Wheat 31.77 4015.01

v Rice 0.00 0.00

vi Maize 8.41 790.56vii Soy Oil 500.62 235605.92viii Mentha Oil 2.31 13173.04ix Guarseed 1226.69 283431.09x Guar Gum 59.46 29593.86

xi Potato 61.63 4575.74

xii Chillis 3.68 1998.17

xiii Jeera(Cuminseed) 26.50 33720.04

xiv Cordmom 0.28 2503.69

xv Pepper 19.61 27705.73

xvi Rubber 5.81 7123.20

xvii other agri 1514.02 445762.51

Volume of Trading and Value of Trade during the year 2009-10 at Major

CommoditiesVolume of Trading – In lakh tonne

Value - In Rs. Crore

Sr.No Name of the Commodity 2009-10Volume Value

Total for C 3991.21 1217949.04

D Energy 5162.95 1577882.06E Plastic 0.00 0.00F Other 2.12 3134.40

Grand Total (A+B+C+D+E+F) 10142.93 7764754.05Note: Natural Gas, Electricity & Heating Oil Volumes are not included in the TotalVolume because Volumes in Natural Gas in mmBtu, Electricity in MW & Heating Oil in USGLN at MCX, Mumbai.

. The Indian Commodity Futures Markets continued to grow, despite the suspension of futures trading in a few agricultural commodities. During the year, 113 commodities were regulated under the auspices of the recognized Exchanges. During 2010-11, 21 recognized exchanges were functioning. Out of the 113 commodities, regulated by the FMC, in terms of value of trade, Silver, Gold, Copper, Nickel, Zinc, Lead, Soy Oil, Guarseed, Chana, Pepper, and Jeera were the prominently traded commodities.

The table below indicates the group-wise and Commodity-wise volume and value of trade in the Commodity market during the year.

Volume of Trading and Value of Trade during the year 2010-11 in

Major CommoditiesVolume of Trading – In lakh tonne

Value - In ` Crore

Sr.No Name of the Commodity 2010-11

Volume ValueA Bullion

i Gold 0.14 2700607.00

ii Silver 7.24 2793280.23

iii Platinum 0.0000002 4.89

Total for A 7.38 5493892.12

B Metals other thanBullion

i Aluminum 110.17 114081.70

ii Copper 335.36 1239261.20

iii Lead 356.88 366422.24

iv Nickel 44.83 478789.31

v Steel 86.66 22759.03

Vi Tin 0.002 18.35

Vii Zinc 463.25 465375.27

viii Iron 12.56 965.89

Total for B 1409.72 2687672.99C Agricultural

commoditiesi Chana/Gram 523.59 126158.29

ii Wheat 26.78 3316.88

iii Maize 16.36 1730.06

iv Soy Oil 617.15 345286.26

v Mentha Oil 6.21 60527.10

vi Guarseed 1056.04 254690.88

vii Guar Gum 83.15 49942.57viii Potato 269.22 14428.17

Volume of Trading and Value of Trade during the year 2010-11 in

Major CommoditiesVolume of Trading – In lakh tonne

Value - In ` Crore

Sr.No Name of the Commodity 2010-11

Volume Valueix Chillis 11.31 8493.79

x Jeera(Cuminseed) 42.53 60864.48

xi Cordmom 0.77 10882.04

xii Pepper 42.25 84786.09

xiii Rubber 11.78 23846.92

xiv other agri 1461.21 411436i.10

Total for C 4168.35 1456389.62

D Energy 7220.12 2310958.58

E Other 0.00 29.04

Grand Total (A+B+C+D+E) 12805.57 11948942.35

Note: Natural Gas, Heating Oil & Gasoline Volumes are not included inthe Total Volume.

The table below indicates the group-wise and Commodity-wise volume and value of trade in the Commodity market during the year.

Volume of Trading and Value of Trade during the year 2011-12 in MajorCommodities

Volume of Trading – In lakh tonne/ Value - In ` Crore

Sr. No Name of theCommodity

2011-12

Volume Value

A Bullion

i Gold 0.17 4355098.64

ii Silver 10.11 5826848.58

iii Platinum 0.0000004 10.00

Total for A 10.27 10181957.22

B Metals other than Bullion

i Aluminum 131.73 145898.50

ii Copper 386.46 1565984.17

iii Lead 336.10 364264.87

iv Nickel 42.76 427336.21

v Steel 37.23 11510.97

vi Tin 0.0002 2.70

vii Zinc 372.85 375692.69

viii Iron 80.72 6030.61

Total for B 1387.85 2896720.73

C Agricultural Commodities

i Chana/Gram 947.98 306411.78

ii Wheat 22.43 2661.42

Volume of Trading and Value of Trade during the year 2011-12 in MajorCommodities

Volume of Trading – In lakh tonne/ Value - In ` Crore

Sr. No Name of theCommodity

2011-12

Volume Value

iii Maize 19.01 2294.48

iv Soy Oil 802.85 538383.46

v Mentha Oil 7.11 101410.51

vi Guar seed 733.10 338216.19

vii Guar Gum 69.02 100515.47

viii Potato 229.11 14156.71

ix Chilli 14.07 11611.26

x Jeera(Cumin seed) 37.38 55982.69

xi Cardamom 1.91 16373.87

xii Pepper 24.64 79518.79

xiii Rubber 7.86 16697.51

xiv Other Agri. Commodities 2025.61 611915.37

Total for C 4942.09 2196149.50

D Energy 7685.52 2851268.52

E Plastic 0.01 6.45

F Other 1.35

Grand Total (A+B+C+D+E+F) 14025.74 18126103.78

Note: Natural Gas, Heating Oil & Gasoline Volumes are not included in the TotalVolume.

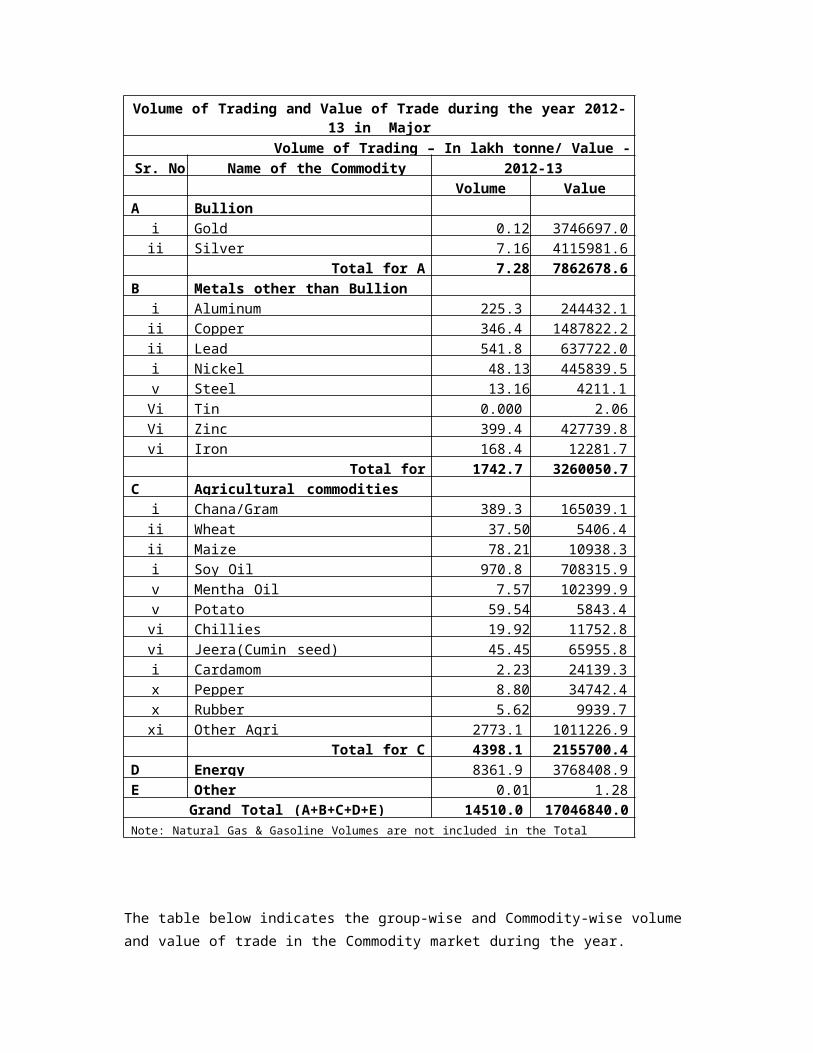

The table below indicates the group-wise and Commodity-wise volume and value of trade in the Commodity market during the year.

Volume of Trading and Value of Trade during the year 2012-13 in Major

Commodities

Volume of Trading – In lakh tonne/ Value - In ₹ Crore

Sr. No Name of the Commodity 2012-13

Volume Value

A Bullion

i Gold 0.12 3746697.03

ii Silver 7.16 4115981.63

Total for A 7.28 7862678.65

B Metals other than Bullion

i Aluminum 225.32 244432.17

ii Copper 346.49 1487822.25

iii Lead 541.81 637722.04

iv Nickel 48.13 445839.56

v Steel 13.16 4211.11

Vi Tin 0.0002 2.06

Vii Zinc 399.40 427739.82

viii Iron 168.45 12281.76

Total for B 1742.76 3260050.77

C Agricultural commodities

i Chana/Gram 389.36 165039.10

ii Wheat 37.50 5406.46

iii Maize 78.21 10938.34

iv Soy Oil 970.81 708315.97

v Mentha Oil 7.57 102399.93

vi Potato 59.54 5843.42

vii Chillies 19.92 11752.80

viii Jeera(Cumin seed) 45.45 65955.88

ix Cardamom 2.23 24139.38

x Pepper 8.80 34742.45

xi Rubber 5.62 9939.76

xii Other Agri 2773.10 1011226.92

Total for C 4398.11 2155700.42

D Energy 8361.92 3768408.97

E Other 0.01 1.28

Grand Total (A+B+C+D+E) 14510.08 17046840.09

Note: Natural Gas & Gasoline Volumes are not included in the Total Volume.

The table below indicates the group-wise and Commodity-wise volume and value of trade in the Commodity market during the year.

Volume of Trading and Value of Trade during the year 2013-14 in Major

Commodities

Volume of Trading - In lakh tonne, Value - In ₹ crore

Sr. No Name of the Commodity 2013-14

Volume Value

A Bullion

i Gold 0.09 2513697.33

ii Silver 3.94 1795240.49

Total for A 4.03 4308937.82

B Metals other than Bullion

i Aluminum 129.07 137609.82

ii Copper 185.83 785562.21

iii Lead 326.49 406971.56

iv Nickel 22.05 190796.34

v Steel 1.72 483.71

vi Zinc 206.80 231896.17

vii Iron 106.42 8040.08

Total for B 978.37 1761359.89

C Agricultural commodities

i Chana/Gram 525.73 164754.94

ii Wheat 10.47 1637.22

iii Maize 47.30 6168.26

iv Soy Oil 417.69 290044.79

v Mentha Oil 4.60 41798.11

vi Guar Seed 45.73 24719.80

vii Guar Gum 8.09 12237.77

viii Potato 66.90 4239.66

ix Chillies 12.53 7537.48

x Jeera(Cumin seed) 22.48 28917.50

xi Cardamom 1.47 11310.62

xii Pepper 0.42 1600.70

xiii Rubber 6.43 10514.94

xiv Other Agri 2442.21 996920.17

Total for C 3612.03 1602401.96

D Energy 4238.33 2472095.31

Grand Total (A+B+C+D) 8832.76 10144794.98

Note: Natural Gas Volumes are not included in the Total Volume.

Trends in volume contribution on the National Exchanges:-

Major volume contributors: - Majority of trade has been concentrated in few commodities that

are

Non Agricultural Commodities (bullion, metals and energy)

Agricultural commodities with small market size (or narrow commodities) like guar, Urad,

Menthol etc.

Out of 17 recognized exchanges (6 National and 11 Regional Exchanges), Multi

Commodity Exchange (MCX), Mumbai, National Commodity and Derivatives Exchange

(NCDEX), Mumbai, National Multi Commodities Exchange, (NMCE), Ahmedabad, ACE

Derivatives Commodity Exchange (ACE), Mumbai, Indian Commodity Exchange, Ltd.

(ICEX), Mumbai, and Universal Commodity Exchange Ltd. (UCX), Navi Mumbai contributed 99.72% of the total value of the commodities traded during the year.

Total volume and value of trade during the (April 2013 to March 2014) in the major commodity

exchanges

Name of Exchange

Volume of Value (` in % share (In

Trade

Crore)

value

(In lakh tons) terms)

Multi Commodity Exchange of India 5305.81 8611449.07 84.89

Ltd., Mumbai

National Commodity & Derivatives 2745.43 1146328.09 11.30

Exchange Ltd., Mumbai

National Multi Commodity Exchange 310.23 152819.01 1.51

of India Ltd., Ahmedabad

Indian Commodity Exchange Ltd., 217.45 85664.19 0.84

Mumbai

ACE Derivatives & Commodity 52.13 46756.74 0.46

Exchange Ltd., Mumbai

Universal commodity Exchange Ltd.,Navi

Mumbai 133.07 73013.19 0.72

Grand total 8764.12 10116030.29 100.00

Note: Natural Gas volumes are not included in the Total Volume

Pattern on Multi Commodity Exchange (MCX):-

MCX is currently largest commodity exchange in the country in terms of trade volumes,

further it has even become the third largest in bullion and second largest in silver future trading

in the world. Coming to trade pattern, though there are about 100 commodities traded on MCX,

only 3 or 4 commodities contribute for more than 80 percent of total trade volume. As per recent

data the largely traded commodities are Gold, Silver, Energy and base Metals. Incidentally the

futures’ trends of these commodities are mainly driven by international futures prices rather than

the changes in domestic demand-supply and hence, the price signals largely reflect international

scenario. Among Agricultural commodities major volume contributors include Gur, Urad,

Menthol Oil etc. Whose market sizes are considerably small making then vulnerable to

manipulations. MCX is India’s leading commodity futures exchange with a market share of

84.89 per cent in terms of the value of commodity futures contracts traded in FY 2013-14. The

Exchange was the third largest commodity futures exchange in the world, in terms of the number

of contracts traded in CY2013, based on the Futures Industry Association’s annual volume

survey released in March 2014. Moreover, as per the survey, during CY 2014, MCX was the

world's largest exchange in silver and gold futures, second largest in copper and natural gas

futures, and the third largest in crude oil futures. MCX has forged strategic alliances with leading

international exchanges such as CME Group, London Metal Exchange (LME), Shanghai Futures

Exchange (SHFE) and Taiwan Futures Exchange (TAIFEX). The Exchange has also tied-up with

various trade bodies, corporate, educational institutions and R&D centers across the country.