commercial banking (ch17, 18 & 19) – bus322 1 commercial banking banks’ balance sheet bank...

TRANSCRIPT

Commercial Banking (ch17, 18 & 19) – BUS322 1

Commercial Banking

Banks’ Balance Sheet

Bank Management

Off-Balance-Sheet Activities

Banks’ Income Statement

Banks’ Regulations

Commercial Banking (ch17, 18 & 19) – BUS322 2

Ten Largest U.S. Banks

Commercial Banking (ch17, 18 & 19) – BUS322 3

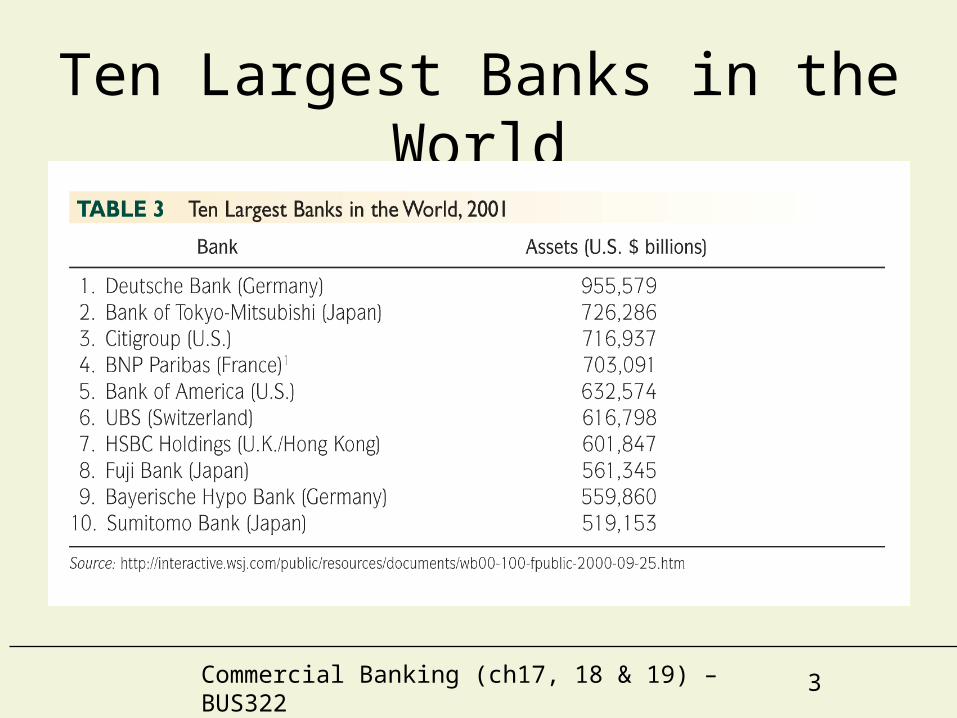

Ten Largest Banks in the World

Commercial Banking (ch17, 18 & 19) – BUS322 4

Uniform Bank Performance Report (UBPR)

• A comprehensive analytical too created by the FDIC on a quarterly report requirement

• Contain banks’ profitability and risk information in a consistent and uniformed basis

• To obtain information: http://www2.fdic.gov/ubpr and then follow instruction

Commercial Banking (ch17, 18 & 19) – BUS322 5

The Bank Balance Sheet

Commercial Banking (ch17, 18 & 19) – BUS322 6

Assets – Uses of FundsReservesCash Items in Process of CollectionA check written on an account at another bank is deposited in bank A and the funds for this check have not yet been received from the other bank.

Deposits at Other BanksSecurities – debt securities only

– US government and agency securities– State and local gov. (municipal) securities– Others (investment-grade securities)

Bank Loans

Commercial Banking (ch17, 18 & 19) – BUS322 7

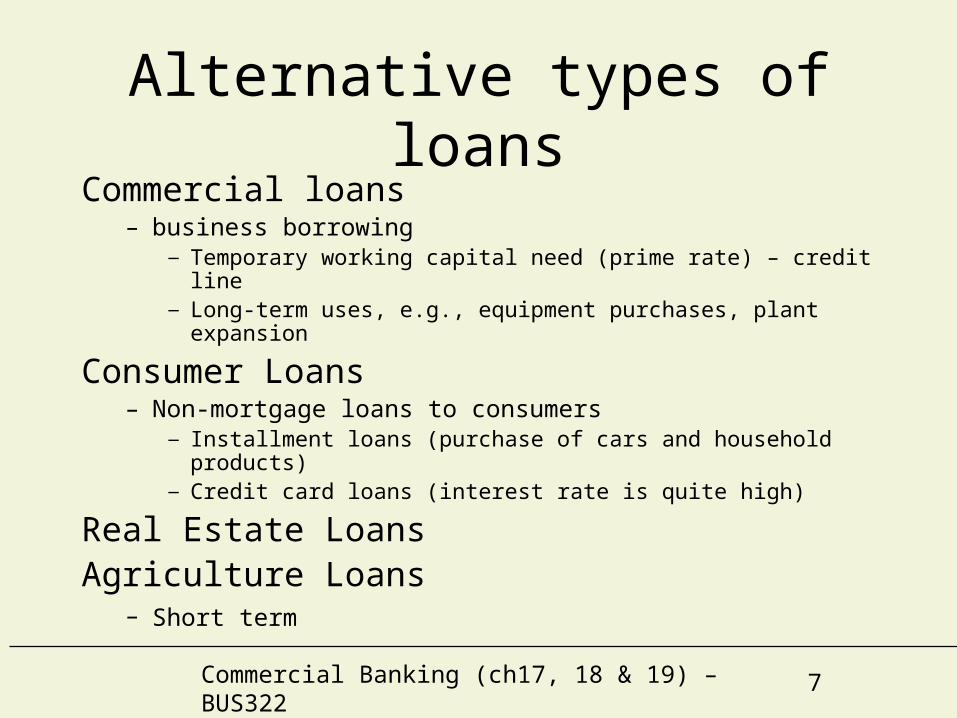

Alternative types of loansCommercial loans

– business borrowing — Temporary working capital need (prime rate) – credit line— Long-term uses, e.g., equipment purchases, plant expansion

Consumer Loans– Non-mortgage loans to consumers

— Installment loans (purchase of cars and household products)— Credit card loans (interest rate is quite high)

Real Estate LoansAgriculture Loans

– Short term

Commercial Banking (ch17, 18 & 19) – BUS322 8

Liabilities and Equity – Sources of Funds

Checkable Deposits non-interest-bearing checking accounts (demand deposits)

interest-bearing NOW (negotiable order of withdrawal)

money market deposit account (MMDAs)

Nontransaction Deposits Saving Accounts

Time Deposits: small-denomination & large-denomination

Borrowing discount loan and other borrowings

Bank Capital

Commercial Banking (ch17, 18 & 19) – BUS322 9

Bank Management

1. Liquidity management

2. Asset management

A. Managing credit risk

B. Managing interest-rate risk

3. Liability management

4. Managing capital adequacy

Commercial Banking (ch17, 18 & 19) – BUS322 10

Liquidity Management Reserve requirement = 10%, Excess reserves = $10 million

Assets Liabilities

Reserves $20 million Deposits $100 million

Loans $80 million Bank Capital $ 10 million

Securities $10 million

Commercial Banking (ch17, 18 & 19) – BUS322 11

Deposit outflow of $10 million

Assets Liabilities

Reserves $10 million Deposits $ 90 million

Loans $80 million Bank Capital $ 10 million

Securities $10 million

With 10% reserve requirement, bank still has excess reserves of $1 million: no changes needed in balance sheet

Liquidity Management

Commercial Banking (ch17, 18 & 19) – BUS322 12

Liquidity ManagementNo excess reserves

Assets Liabilities

Reserves $10 million Deposits $100 million

Loans $90 million Bank Capital $ 10 million

Securities $10 million

Deposit outflow of $ 10 million

Assets Liabilities

Reserves $ 0 million Deposits $ 90 million

Loans $90 million Bank Capital $ 10 million

Securities $10 million

With 10% reserve requirement, it has $9 million reserve shortfall

Commercial Banking (ch17, 18 & 19) – BUS322 13

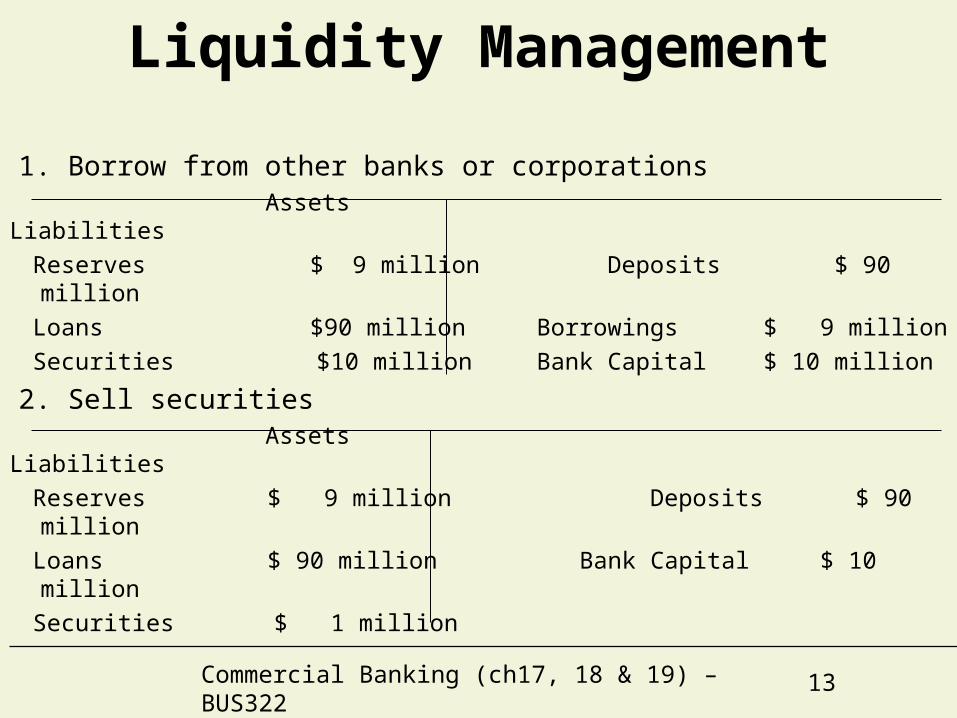

1. Borrow from other banks or corporations

Assets Liabilities

Reserves $ 9 million Deposits $ 90 million

Loans $90 million Borrowings $ 9 million

Securities $10 million Bank Capital $ 10 million

2. Sell securities Assets Liabilities

Reserves $ 9 million Deposits $ 90 million

Loans $ 90 million Bank Capital $ 10 million

Securities $ 1 million

Liquidity Management

Commercial Banking (ch17, 18 & 19) – BUS322 14

Liquidity Management3. Borrow from Fed Assets Liabilities

Reserves $ 9 million Deposits $90 million

Loans $90 million Discount Loans $ 9 million

Securities $10 million Bank Capital $10 million

4. Call in or sell off loans Assets Liabilities

Reserves $ 9 million Deposits $ 90 million

Loans $81 million Bank Capital $ 10 million

Securities $10 million

Conclusion: excess reserves are insurance againstabove 4 costs from deposit outflows

Commercial Banking (ch17, 18 & 19) – BUS322 15

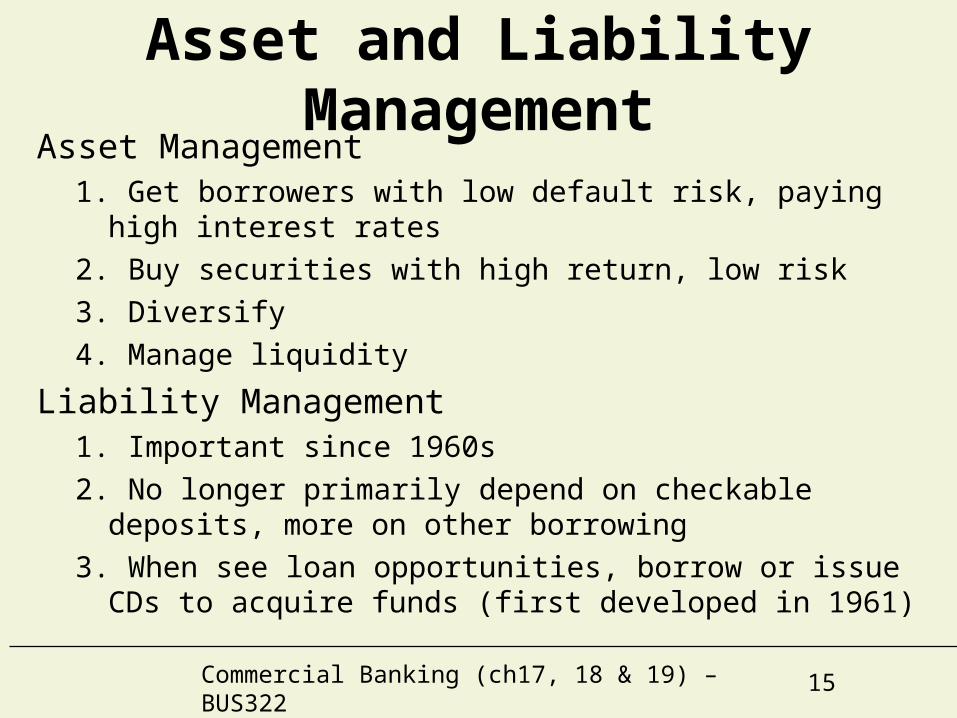

Asset and Liability ManagementAsset Management

1. Get borrowers with low default risk, paying high interest rates

2. Buy securities with high return, low risk

3. Diversify

4. Manage liquidity

Liability Management1. Important since 1960s

2. No longer primarily depend on checkable deposits, more on other borrowing

3. When see loan opportunities, borrow or issue CDs to acquire funds (first developed in 1961)

Commercial Banking (ch17, 18 & 19) – BUS322 16

Capital Adequacy Management1. Bank capital is a cushion that prevents bank failure2. Higher is bank capital, lower is return on equity

ROA = Net Profits/AssetsROE = Net Profits/Equity CapitalEM = Assets/Equity CapitalROE = ROA x EM (EM is equity multiplier)Capital , EM , ROE

3. Tradeoff between safety (high capital) and ROE4. Banks also hold capital to meet capital requirements5. Strategies for Managing Capital:

A. Sell or retire stockB. Change dividends to change retained earningsC. Change asset growth

Commercial Banking (ch17, 18 & 19) – BUS322 17

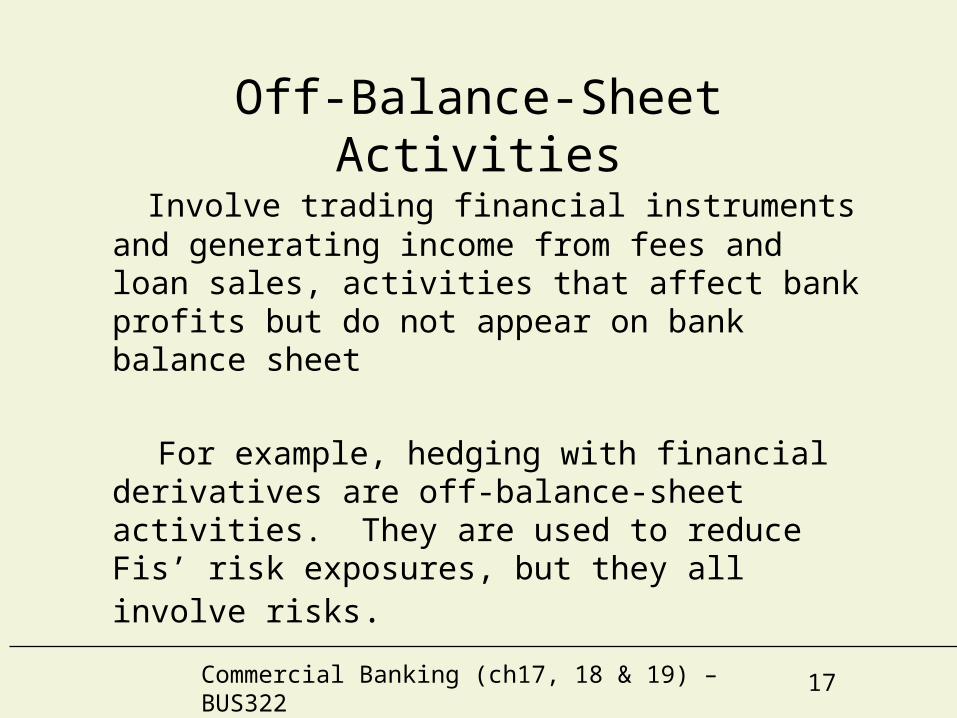

Off-Balance-Sheet Activities

Involve trading financial instruments and generating income from fees and loan sales, activities that affect bank profits but do not appear on bank balance sheet

For example, hedging with financial derivatives are off-balance-sheet activities. They are used to reduce Fis’ risk exposures, but they all involve risks.

Commercial Banking (ch17, 18 & 19) – BUS322 18

Off-Balance-Sheet Activities1. Loan Sales

2. Fee income fromA. Foreign exchange trades for customers

B. Servicing mortgage-backed securities

C. Guarantees of debt

D. Backup lines of credit

2. Financial futures and options

3. Foreign exchange trading

4. Interest rate swaps

Commercial Banking (ch17, 18 & 19) – BUS322 19

Banks' Income Statement

Commercial Banking (ch17, 18 & 19) – BUS322 20

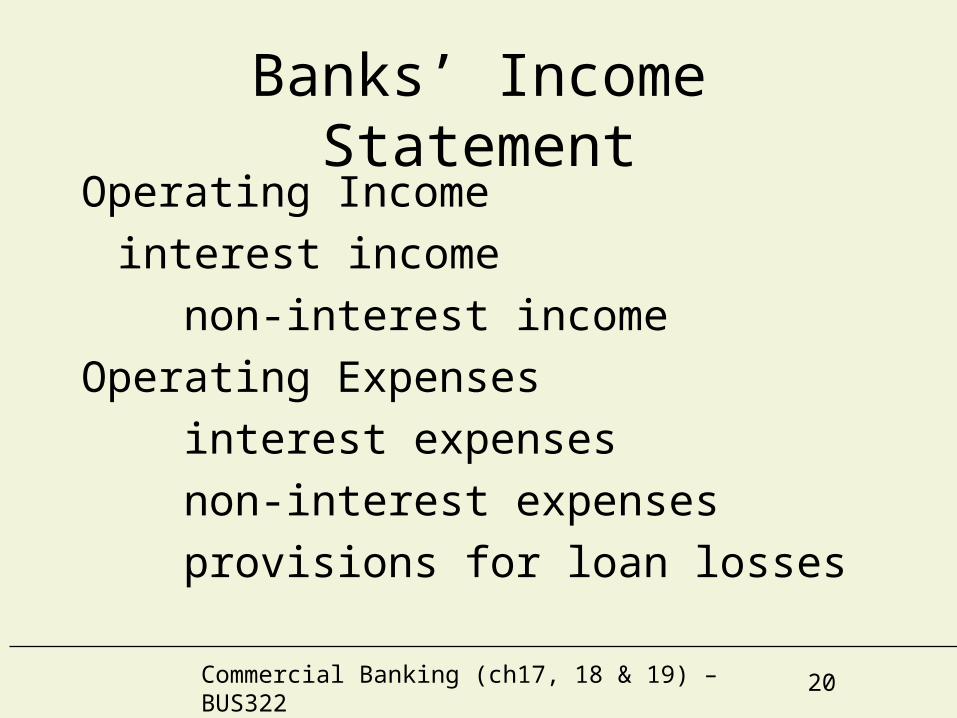

Banks’ Income StatementOperating Income

interest income

non-interest income

Operating Expenses

interest expenses

non-interest expenses

provisions for loan losses

Commercial Banking (ch17, 18 & 19) – BUS322 21

Income Statement

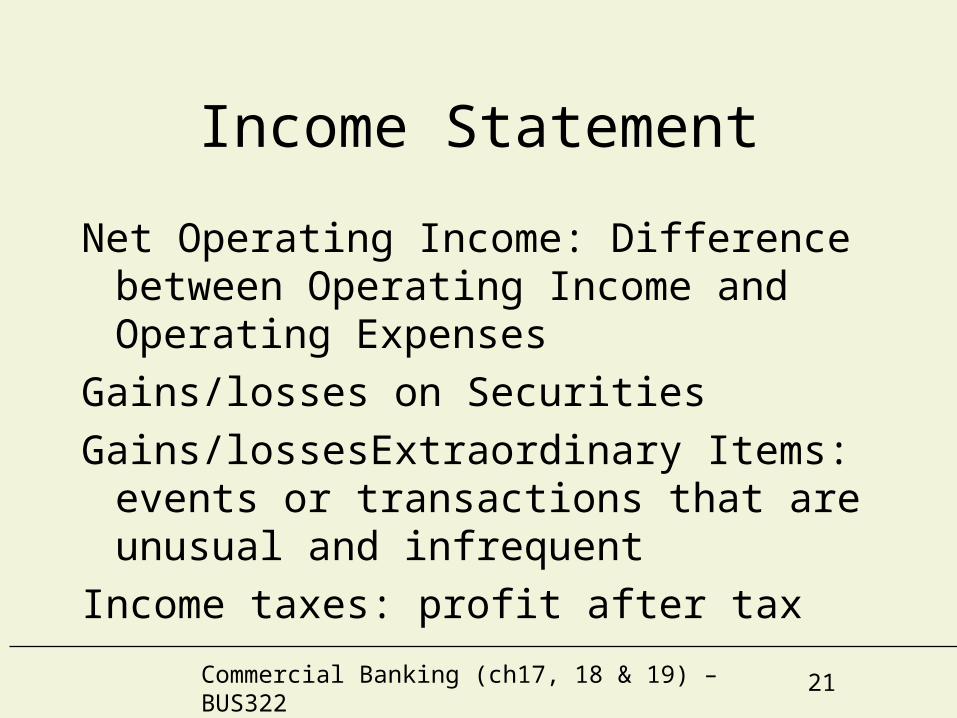

Net Operating Income: Difference between Operating Income and Operating Expenses

Gains/losses on Securities

Gains/lossesExtraordinary Items: events or transactions that are unusual and infrequent

Income taxes: profit after tax

Commercial Banking (ch17, 18 & 19) – BUS322 22

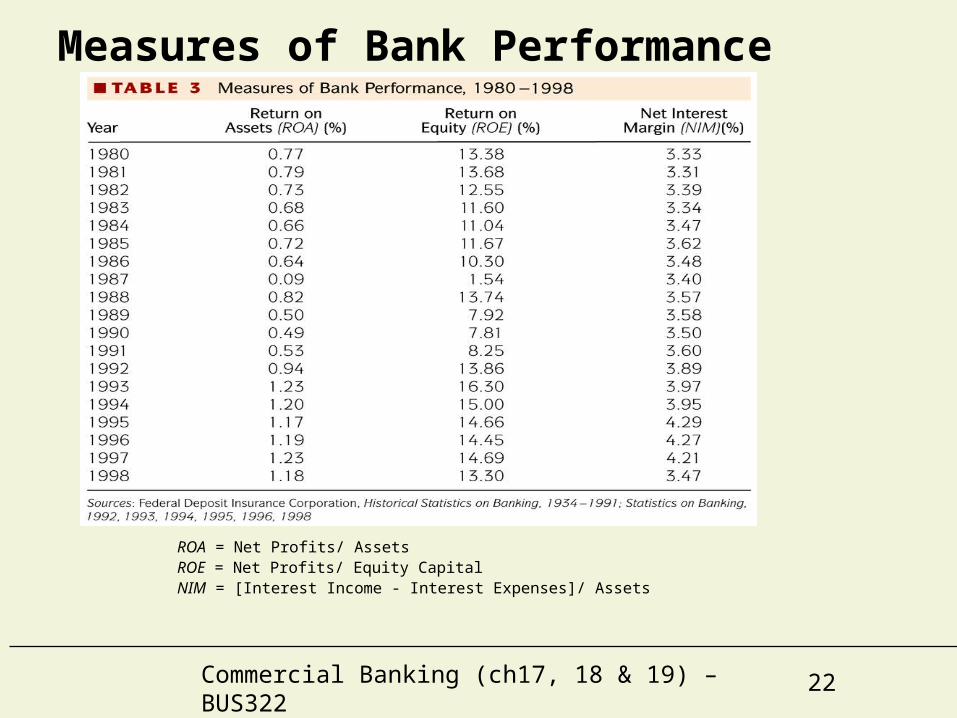

Measures of Bank Performance

ROA = Net Profits/ AssetsROE = Net Profits/ Equity CapitalNIM = [Interest Income - Interest Expenses]/ Assets

Commercial Banking (ch17, 18 & 19) – BUS322 23

Bank RegulationRegulatory Structure• A charter from state/federal gov is needed for

open a commercial bank– State bank – having state charter, regulated by state

agency

– National bank – having federal charter—Regulated by the office of Comptroller of Currency (issue

charter)—FDIC—Federal Reserve

Commercial Banking (ch17, 18 & 19) – BUS322 24

Branching RegulationsBranching Restrictions:

Anticompetitive

Response to Branching Restrictions

1. Bank Holding CompaniesA. Allowed purchases of banks outside state

B. BHCs allowed wider scope of activities by Fed

C. BHCs dominant form of corporate structure for banks

2. Nonbank BanksNot subject to branching regulations, but loophole closed in 1987

3. Automated Teller MachinesNot considered to be branch of bank, so networks allowed

Commercial Banking (ch17, 18 & 19) – BUS322 25

Bank Consolidation and Number of Banks

Commercial Banking (ch17, 18 & 19) – BUS322 26

Nationwide Banking and Bank Consolidation

Bank Consolidation: Why? 1. Branching restrictions weakened2. Development of superregional banks

Riegle-Neal Act of 19941. Allows full interstate branching2. Promotes further consolidation

Future of Industry StructureWill become more like other countries, but not quite:

Several thousand, not several hundred

Commercial Banking (ch17, 18 & 19) – BUS322 27

Separation of Banking and Securities

Industries: Glass-Steagall Case for Glass-Steagall

1. FDIC gives unfair advantage to banks2. Allowing banks into underwriting is dangerous because FDIC promotes

too much risk taking3. Potential conflicts of interest

Case Against Glass-Steagall1. Decreases competition2. Unfair to banks3. Hinders diversification

Will Separation Continue?No, Gramm-Leach-Bliley Financial Service Modernization Act of 1999 1) allow banks to underwrite insurance and securities and engage in real estate 2) allows securities firms and insurance companies to purchase banks

Commercial Banking (ch17, 18 & 19) – BUS322 28

Separation in Other Countries1. Universal banking: Germany

2. British-style universal banking

3. U.S./Japan separation

Separation of Banking and Securities Industries: Glass-Steagall

Commercial Banking (ch17, 18 & 19) – BUS322 29

Other Depositary InstitutionsThrifts (or thrift institutions)1. Mutual saving banks: depositors are owners of

firms

2. S&Ls (saving and loan Associations): getting deposits and make long-term mortgage loans

3. Credit unions: financial institutions that focus on servicing the banking and lending needs of its members