colonial first state investments listening?

TRANSCRIPT

Colonial First State Investments

Resources – Should I still be listening?

Dr Joanne Warner Senior Portfolio Manager, Global ResourcesMatthew Webb National Manager, Investments

This presentation is given by a representative of Colonial First State Investments Limited AFS Licence 232468, ABN 98 002 348 352 (Colonial First State). The presenter does not receive specific payments or commissions for any advice given in this presentation. The presenter, other employees and directors of Colonial First State receive salaries, bonuses and other benefits from it. Colonial First State receives fees for investments in its products. For further detail please read our Financial Services Guide (FSG) available at colonialfirststate.com.au or by contacting our Investor Service Centre on 13 13 36.

All products are issued by Colonial First State. Product Disclosure Statements (PDSs) describing the products are available from Colonial First State. The relevant PDS should be considered before making a decision about any product.

This presentation is intended for adviser use only and does not take into account a client’s individual objectives, financial situation or needs. You should assess whether the information is appropriate for your clients and make sure they consider talking to a financial adviser before making an investment decision. Stocks mentioned should not be considered as recommendations.

The information is taken from sources which are believed to be accurate but Colonial First State accepts no liability of any kind to any person who relies on the information contained in the presentation.

Past performance is no indication of future performance.

This presentation cannot be used or copied in whole or part without our express written consent.

© Colonial First State Investments Limited 2006.

Disclaimer

Agenda

g Market update

g What does China mean for resources?

g Our solution

g Our process

g How resources fit in a portfolio

+5 year bull market in Resources

Compound annual returns

Source: Colonial First State Investments Ltd, RimesAll returns in AUD before fees for Wholesale Global Resources Fund

31 July 2006Before fees 3 6 1 2 3 5 7AUD Mths Mths Year Years Years Years YearsWholesale Global Resources Fund -7.0% 0.8% 42.6% 35.6% 34.6% 23.8% 24.0%

HSBC Global Mining Accumulation index -6.1% 6.0% 60.6% 40.8% 35.3% 20.9% 19.7%

S&P/ASX 300 Resources Accumulation index -5.3% 4.6% 41.0% 43.2% 40.5% 26.5% 22.0%

MSCI World Energy index (Net) 0.1% 1.4% 21.1% 24.7% 25.2% 7.3% 9.6%

Performance - before fees (AUD)

On the back of increased commodity prices stock prices have risen strongly…

0

50

100

150

200

250

300

350

400

May-03 Aug-03 Nov-03 Feb-04 May-04 Aug-04 Nov-04 Feb-05 May-05 Aug-05 Nov-05 Feb-06 May-06

MSCI All Countries World Information Technology Index (lagged 6 years)

HSBC Global Mining Index

Source: Bloomberg, HSBC, MSCI. 3 Years ending 31 May 2006, All data in USD.

Technology Index (lagged 6 years)

Global Mining Index

Is this a bubble?

Rio Tinto - Price vs Consensus Earnings

5 year move in base metal prices

copper

zincnickellead

aluminium

400

300

200

100

Index

ABN-AMRO Base Metal Price Index 34 years (nominal)

34 YEAR ABN-AMRO BASE METAL PRICE INDEX (Nominal - Money of the Day) ABN AMRO Base Metal Price Index now at all time high up 340% since October 2001 price low

0

25

50

75

100

125

150

175

200

225

250

275

300

72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Low Nov. 1993(Index = 67)

Low Dec. 1982(Index = 56)

Low Nov. 1977(Index = 54)

Low Nov. 1972 (Index value = 41)

Low Dec. 1986(Index = 60)

Peak April 1974(Index = 83)

Peak Feb. 1980(Index = 110)

Peak Aug. 1983Up 50%; Down 29%

(Index 84)

Peak Jan. 1995(Index = 127)

Low Dec. 1998(Index = 66)

Peak March 2000(Index = 105)

Trough October 2001(Index = 68)

ABN-AMRO Base Metal Price Index Consumption Value Weightings

January 2000 =100Al 43%, Cu 30%, Ni 11%, Zn 11%, Pb 3%, Sn 2%

"First Oil Shock" Boom duration 17 mths. Trough to peak 102%. Peak to trough 40%

"Second Oil Shock" Boom duration 27 mths.

Up 103%; Down 49%

Stock Market Crash of Oct.1987 Twin Peaks June 88 & Jan. 89

Duration 18mths Up 195%; Down 62%(Index value = 178)

Dissolution of Soviet Union. Massive Inventory Build, MOU Duration 14

mths.Up 89%; Down 48%

Asian Crisis Boom duration 15 mths.

Up 59%; Down 35%

Not a super cycle a VESUVIAN cycle!Liquidity driven boom. Acute fund attention on back of low inventory, tardy supply response and China syndrome Duration 56 mths, up 340% (Index value = 300)

Source: Nick Moore, Commodity Analyst, ABN-AMRO, June 2006

Outlook for the sector

g Economic growth drives demand

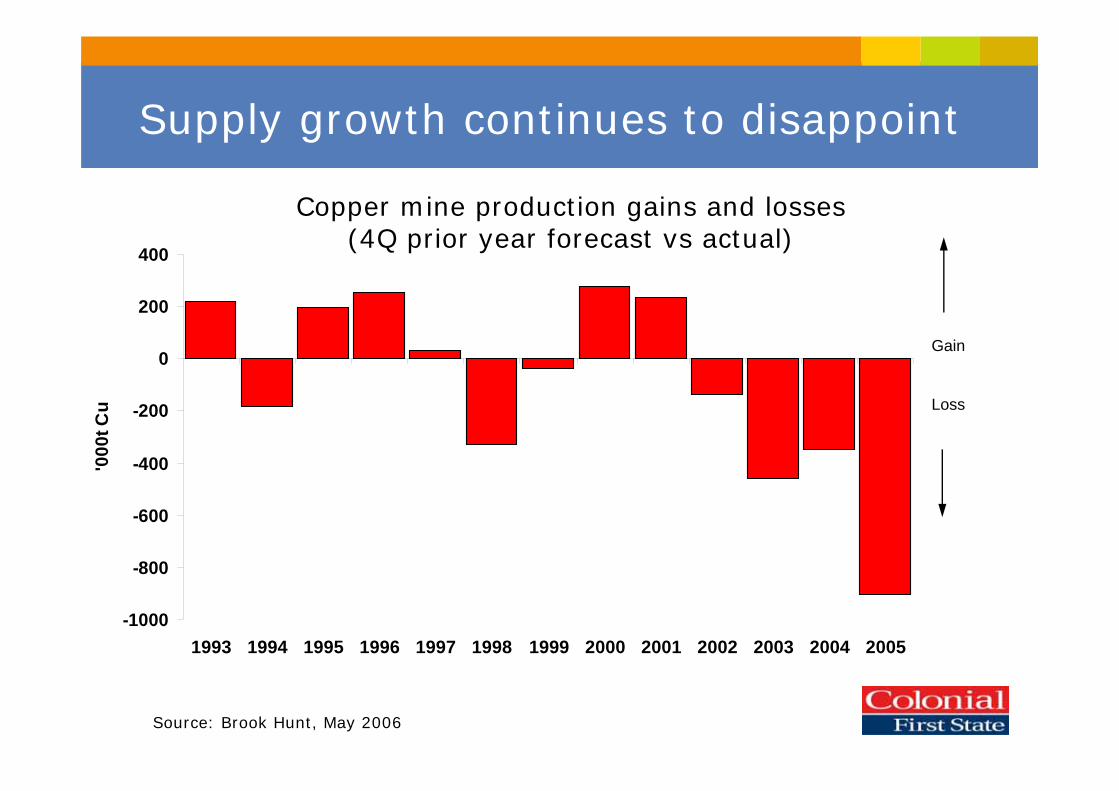

g Production growth continues to disappoint – expect disruptions and shortages to continue for some time yet

g Low inventories make prices vulnerable to spikes – also likely to stimulate further substitution

g Speculators are pushing prices higher introducing added volatility and risk

g Consolidation should improve shareholder returns and enhance corporate discipline

Supply growth continues to disappoint

-1000

-800

-600

-400

-200

0

200

400

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

'000

t Cu

Gain

Loss

Copper mine production gains and losses (4Q prior year forecast vs actual)

Source: Brook Hunt, May 2006

Investment fund inflows into commodities have lowered inventories and added to price rises

Total Commodity Index Funds

0

10

20

30

40

50

60

70

80

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

$USb

n

Index funds - share of cash-three month open interest on LME

0%

5%

10%

15%

20%

25%

30%

35%

40%

copper Aluminium Zinc Nickel Lead

% o

f tot

al

2001 2002 2003 2004 2005

Source: Macquarie Research estimates, May 2006Source: Macquarie Research estimates, May 2006

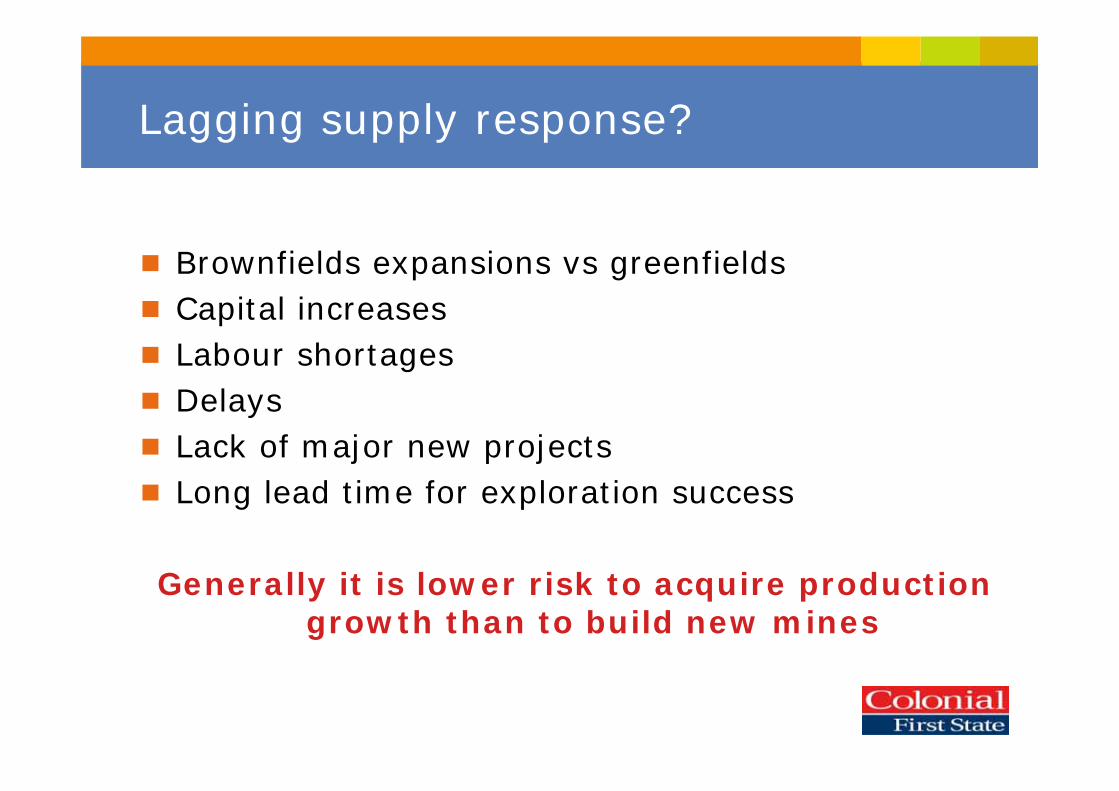

Lagging supply response?

g Brownfields expansions vs greenfieldsg Capital increasesg Labour shortagesg Delaysg Lack of major new projectsg Long lead time for exploration success

Generally it is lower risk to acquire production growth than to build new mines

Greater consolidation –> more supply side discipline?

1996 28 companies

US$132bn

2005 15 companies

US$423bn

Source: Falconbridge

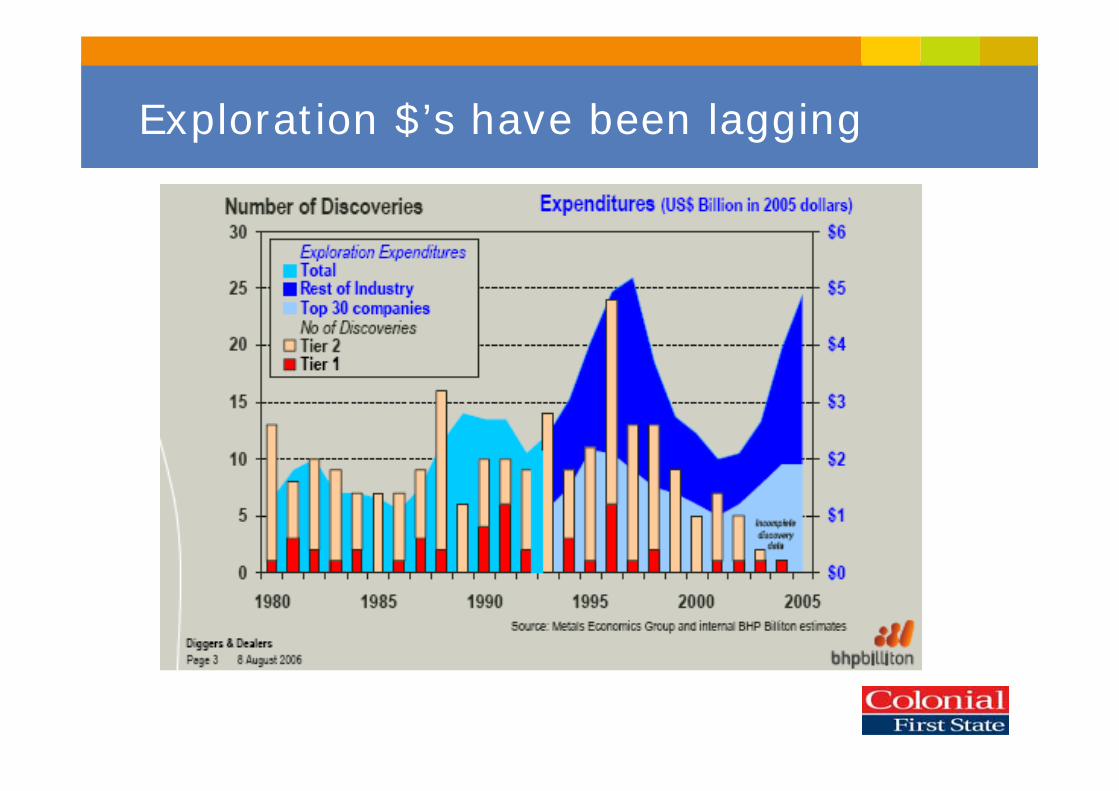

Exploration $’s have been lagging

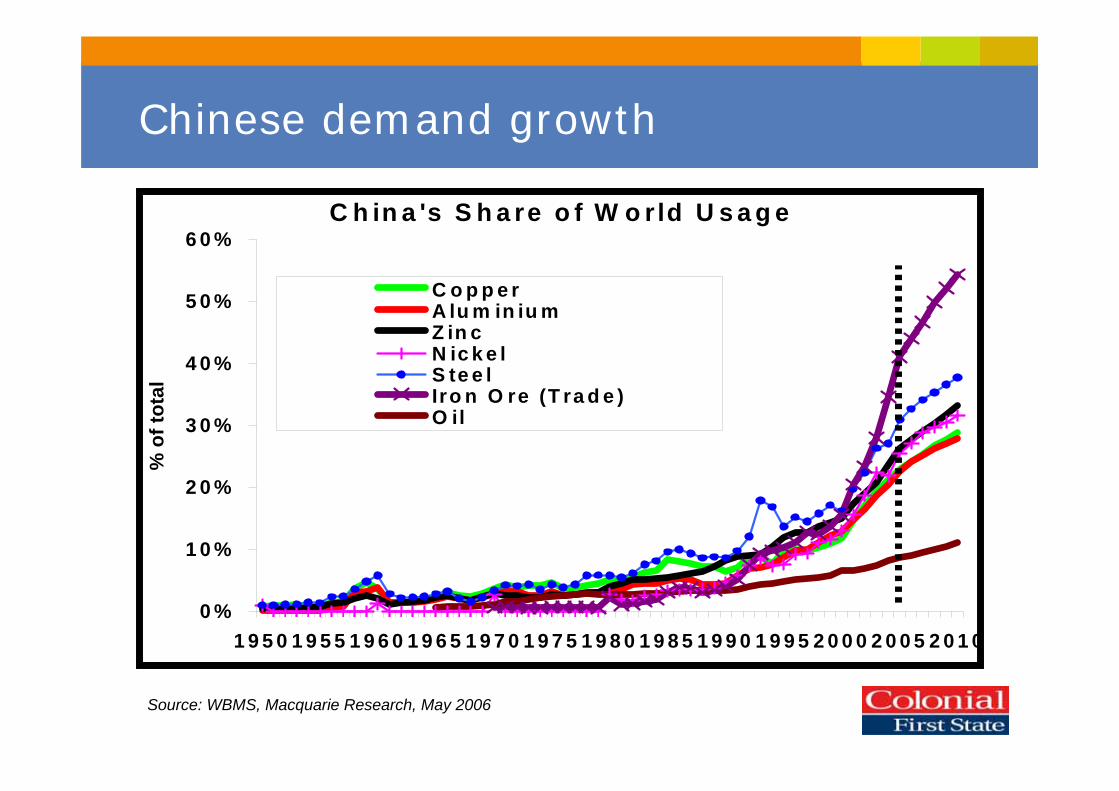

Why are the miners so serious about China?

Chinese demand growth

Source: WBMS, Macquarie Research, May 2006

C h in a 's S h a re o f W o r ld U s a g e

0 %

1 0 %

2 0 %

3 0 %

4 0 %

5 0 %

6 0 %

1 9 5 0 1 9 5 5 1 9 6 0 1 9 6 5 1 9 7 0 1 9 7 5 1 9 8 0 1 9 8 5 1 9 9 0 1 9 9 5 2 0 0 0 2 0 0 5 2 0 1 0

% o

f tot

al

C o p p e rA lu m in iu mZ in cN ic k e lS te e lIro n O re (T ra d e )O il

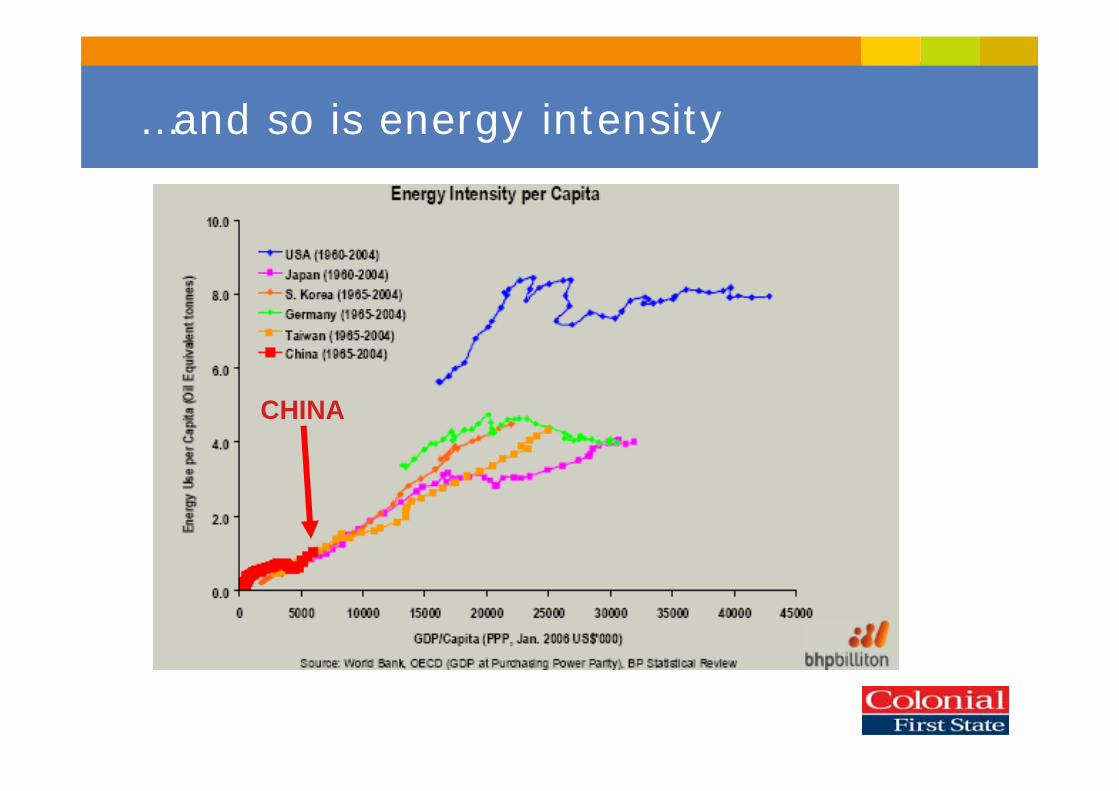

China’s metal intensity is growing…

CHINA

…and so is energy intensity

CHINA

Urbanisation, China 2005 - 2010

About 100 million new urban dwellers in five years. . . and another 300 million by 2020

g Housing

g Road & Rail

g Power

g Water

Source: Research Works, May 06

Chinese urbanisation

* Tier 1 city defined as registered population >4.5m and GDP/capita > US$3,000, Tier 2 city defined as either registered population >4.5m or GDP/capita > US$3,000, Tier 3 city defined as registered population 1.5-4.5m and GDP/capita US$1,500 – US$3,000. Source: WEFA-WMM; China macro model; Mckireey analysis; BHP Billiton.

Colonial First State Investments

Our approach

Things we get excited about

g World class assets

g Low cost producers

g Organic EPS growth

g Strong financials

g Strong management

Quality companies + growth = superior returns with lower risk

Investing in the lower half of the cost curve

0

50

100

150

200

250

300

0 500 1000 1500Cumulative Production (Au t)

US$/oz

Barrick (4.9%) Harmony

AVOID

BUY

GOLD COST CURVE

The tyres we’ve kicked

As at 31/12/05

Since inception 650+ mine and site visits to 48 countries

Average - 71 per year

Long Only Fund - Portfolio breakdown

Metals, 21.2%

Diversif ied, 29.6%

Other, 8.5%Coal, 7.3%

Gold, 17.7%

Energy, 16.2%

Wholesale Global Resources Fund As at 30 June 2006

Canada, 23%

USA, 13%

Brazil, 11%Australia,

22%

UK, 20%

Hong Kong, 7%

Peru, 1%South Africa, 5%

Long tail of 40-45 smaller growth stocks

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0 20 40 60

= $A 20 billion

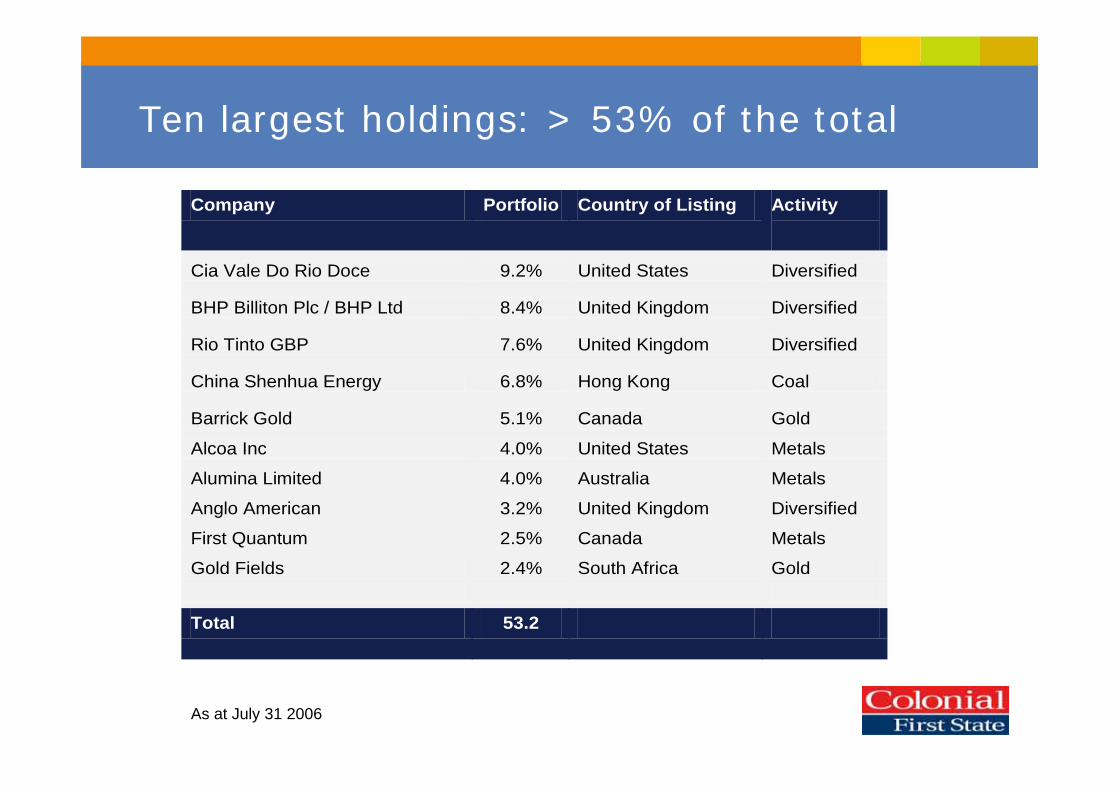

Company Portfolio Country of Listing Activity

Cia Vale Do Rio Doce 9.2% United States Diversified

BHP Billiton Plc / BHP Ltd 8.4% United Kingdom Diversified

Rio Tinto GBP 7.6% United Kingdom Diversified

China Shenhua Energy 6.8% Hong Kong Coal

Barrick Gold 5.1% Canada Gold

Alcoa Inc 4.0% United States Metals

Alumina Limited 4.0% Australia Metals

Anglo American 3.2% United Kingdom Diversified

First Quantum 2.5% Canada Metals

Gold Fields 2.4% South Africa Gold Total 53.2

Ten largest holdings: > 53% of the total

As at July 31 2006

Case study - CVRD #1 in Iron Ore

g World’s largest, highest grade, highest margin iron ore producer

g Supported by high quality businesses in alumina, transport, copper and other minerals

g Aggressive growth profile

g Excellent value

Low cost expansions

Source: CVRD

An outstanding pipeline of future projects

Source: CVRD

?

?

Quality stocks have generated strong returns in falling markets

Source: Colonial First State, HSBC. Data is before fees for life of fund to 30 June 2006. Fund Inception: June 1997

M onths of Outperformance (%)

0%

10%

20%

30%

40%

50%

60%

70%

80%

Al l Mar kets Rising Mar kets Fal l ing Mar kets

1.19%- Falling Markets

-0.35%- Rising Markets

0.26%Monthly Average Excess Return

0.85Beta

0.55%Information Ratio

7.56%Tracking Error

4.18%Annual Excess Return

Resources offer low correlation with other sectors

Source: Datastream, Colonial First State. 10 Years ending 31 May 2006, all data in USD. Correlation co-efficients: HSBC Global Mining Index vs MSCI Sub Indices

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0M

SCI W

orld

Nas

daq

Ener

gy

Mat

eria

ls

Indu

stria

ls

Con

sD

iscr

etio

nary

Con

s St

aple

s

Hea

lth C

are

Fina

ncia

ls IT

Tele

com

Serv

ices

Util

ities

Efficient frontier

Source: Bloomberg, HSBC, MSCI. Data in AUD, 15 Years ending 30 June 2006.

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

12.00%

13.00%

10.00% 11.00% 12.00% 13.00% 14.00% 15.00% 16.00% 17.00% 18.00% 19.00% 20.00%

Annual Volatility (% pa)

Ann

ual R

etur

n (%

pa)

100% MSCI AC World Free Index

100% HSBC Global Mining Index

20% HSBC/80% MSCI

Outlook

g Global commodity supply has tightened

g Few greenfield projects in the wings

g Chinese demand likely to continue

g US and European demand?

Compound annual returns

31 July 2006 Oct-04 Oct-03 Oct-02 Oct-00 Oct-98

After fees 1 2 3 5 7AUD Year Years Years Years YearsWholesale Global Resources Fund 42.6% 35.6% 34.6% 23.8% 24%

Focus on Quality

Which session are you in?1. PIMCO2. Principal Global Investors3. Colonial First State4. Deutsche Asset Management5. Challenger Financial Services

Gizmo time

Please rate the overall quality of this session…1. awful2. Poor3. Mediocre4. Good5. Very good6. Great!

Gizmo time