colloquia series oct domestic and global forces in the...

TRANSCRIPT

1

Key Insights

COLLOQUIA SERIESDomestic and Global Forces in the Evolving U.S. - China Relationship

OctO

ber

2013

GrOWtH DebAte treND ecONOMY VIeWS reSeArcH MArKet

For most of the past 30 years, both the United States and China have experienced impressive but unbalanced growth. For the U.S., this has been the result of over-consumption and under-saving by households and generally large government budget deficits. For China, it has been the result of frenetic export- and investment-led growth. However, forces are now shifting and each country must overcome key domestic challenges to transition to more stable growth. Professor Wescott offers an in-depth analysis of the factors which may change the rules of the game – US energy boom, Chinese rising labour costs, stronger demand for services in China. These factors will likely have powerful effects on trade balances and capital flows. How each country may respond to these challenges will potentially shape their relationship with one another and also with the rest of the world.

One important element in the China-US relationship is related to the future of corporate sector in China. Mauro Ratto, Head of Emerging Markets at Pioneer Investments, focus on this

factor, which is potentially crucial to drive the success of Chinese Government reforms in addressing imbalances. One of the main challenges Chinese corporations are facing involves a more efficient capital allocation between State-Owned and the private sector. Another key trend to monitor is the progress towards urbanization in respect to social issues and rural development. On the back of this macro framework, China‘s corporate sector needs to continue to rise in the value chain: the growth subsidies of the past are disappearing, as Renminbi appreciates and wage inflation erodes labour competitiveness. Identifying countries, sectors, and companies which will be in the condition to maximise the benefits of these new dynamics may unveil interesting investment opportunities.

Looking at the US perspective, Michael Temple, Director of Credit Research, U.S., discuss the energy renaissance in the United States and the “re-shoring” of manufacturing jobs to US. These new trends may have potential implications on the US labour market, on monetary policy and interest rates. The energy boom in US, reducing the needs for energy imports and US dependence from external sources, is seen as an important factor for shaping US foreign policy.

United States is increasingly committed to managing, in a constructive way, Chinese dominance in the Asia Pacific region rather than being mostly involved in the Middle East fragile equilibriums. Evolving China-US relationships go hand-to-hand with the progress in liberalization of Chinese financial system, and with more balanced current accounts. Inside this big picture, conditions underpinning a strong dollar are in place.

2

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

I. IntroductionFor most of the past 30 years, both the United States and China have experienced impressive but unbalanced growth. For the U.S., this has been the result of over-consumption and under-saving by households and generally large government budget deficits. For China, it has been the result of frenetic export- and investment-led growth, facilitated by the rapid migration of hundreds of millions of workers from farm fields to factories. However, forces are now shifting and each country must overcome key domestic challenges to transition to more stable growth.

Historical Realities in the Past Decade U.S. china

Corporate Structure Classic Western Corporation

State-owned enterprises

Demographics Steady moderate labor force growth

Rapid growth of labor force

Energy Scrambling for energy from global sources

Scrambling for energy from global sources

Technology Innovation leader Assembler of products invented elsewhere

Macro Balance Over-consuming/Under-saving households

Over-saving/Under-consuming households

Trade Large trade deficits Large trade surpluses

Finance/Capital Flows

Large budget deficits; heavy international borrowing

Large trade surpluses; mounting international reserves

Source: Keybridge Research, data as of 31 August 2013.

Two factors in particular will drive changes over the next decade: (1) the end of cheap labor in China, and (2) an energy renaissance in the United States. In recent decades,

Robert F. WescottRobert F. Wescott, PhD, is Founder and President of Keybridge Research LLC, an economic analysis firm in Washington, DC, that has served G-7 governments, major financial institutions, and Fortune 500 companies since 2001. Dr. Wescott concentrates on global macroeconomics, financial risks, and public policy research. He provides global asset allocation advice to well respected international financial firms (he is member of the Pioneer Investments Advisory Board) and is a regular speaker to business and financial audiences around the world. Dr. Wescott also testifies as an expert before U.S. Congressional committees on economic, financial, and energy policy matters. From 1999 until 2001, Wescott served as Special Assistant to the U.S. President for Economic Policy at the White House.

China’s rapid growth has been driven by its ability to assemble products at a lower cost than anywhere else in the world. Increasingly, however, demographic trends are pushing China’s labor costs upward, undermining its global competitiveness. At the same time, the U.S. is on the cusp of an energy renaissance that could offer its domestic manufacturers a comparative advantage over foreign competitors. Together, sharply higher unit labor costs in China and cheap energy in the U.S. are shifting the balance between the two countries. Over time, China is likely to be less of a global manufacturing center and the U.S. may become more of one, especially for energy-intensive products.

The Changing U.S.- China Economic Relationship

New Realities for the Next 10 Years U.S. chinaCorporate Structure Classic Western

CorporationTransition away from state-owned enterprises

Demographics Steady, moderate labor force growth

Shrinking labor force

Energy Energy renaissance, less reliance on foreign sources

Scrambling for energy from global sources

Technology Trying to maintain its lead as world leader in innovation

Trying to foster innovation

Macro Balance More balance between consumption & saving

More balance between consumption & saving

Trade More balanced trade More balanced trade

Finance/Capital Flows

Winding down of large debt & heavy international borrowing

Slow growth of international reserves

Source: Keybridge Research, data as of 31 August 2013.

3

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

research by the International Monetary Fund finds that China could begin to experience labor shortages within the next ten years.i In the past 30 years, China’s economy benefitted greatly as subsistence farmers moved from agriculture into the formal economy. Now, it appears that this transition is nearing completion as the country approaches what is known as the Lewis Turning Point—the situation that occurs when a country’s agriculture surplus labor becomes exhausted, industrial wages increase rapidly, profits are squeezed, and investment falls. These trends are being compounded by the effects of the longstanding one child policy, which are now being fully felt. As evidence, consider that China’s working-age population (aged 15-59) is already declining, decreasing by 3.5 million people in 2012. These demographic trends will put further upward pressure on wages and downward pressure on the saving rate, and are likely to materially change the country’s dynamics. Another effect of the tightening labor market is the increased frequency of labor disputes and strikes. As the gap between labor costs in China and developed countries continues to narrow and as labor strife increases, some of the attraction of moving production to China is likely to be lost.

A Changing Global Energy LandscapeAs the world’s two largest economies, the United States and China both have voracious appetites for energy to fuel their industrial engines. The U.S., in particular, historically has been a large importer of oil and natural gas. However, in the last few years the U.S.’s energy landscape has changed dramatically in large part because of increased deployment of unconventional natural gas technology—particularly horizontal drilling and hydraulic fracturing. Indeed, as recently as 2007, natural gas imports accounted for one fifth of American gas consumption. Now, the Department of Energy’s Energy Information Administration (EIA) projects that the U.S. will be a net exporter of natural gas by 2020.

This rapidly expanding supply of natural gas has brought a 70% drop in prices since 2008, to roughly $4.00 per million Btu today—about one third the average price in Europe and about a quarter the average price in Asia. The deployment of these same new drilling technologies is also allowing the U.S. to ramp up its domestic oil production, which the EIA estimates will allow the country to reduce its net imports of crude oil from more than 9 million barrels per day in 2010 to less than 7 million barrels per day by 2018.i Zhang, Moran (2013). “China’s Declining Labor Pool Approaching the ‘Lewis Turning Point’: IMF Paper.” International Business Times: February 4, 2013.

This analysis describes some of the key domestic challenges facing the U.S. and China in the coming years and how each country may respond. In addition to looking at the effects of rising wages in China and the U.S.’s new energy landscape, it also looks at the so-called “re-shoring” phenomenon in the U.S., the rise of U.S. service-sector exports to China, and the shifting trade and capital flow trends between the two countries. How the U.S. and China address these challenges and opportunities will shape the future of their relationships with one another and with the rest of the world in multiple spheres.

II. New RealitiesChina’s Rising Labor CostsRapid increases in China’s labor costs are the dominant factor driving the changing relationship between the United States and China. From 2001 to 2011, China’s unit labor costs increased by 77%, while unit labor costs in the U.S. were up just 10%. Hourly wages in Chinese manufacturing more than doubled between 2003 and 2008, increasing from $0.62 an hour in 2003 to $1.36 in 2008, and more recent estimates have found that wages nearly doubled again to more than $2.20 an hour by 2011 in several Chinese cities. While still sharply lower than average American wages of about $19 an hour, on a productivity-adjusted basis, these Chinese wage levels are beginning to undermine China’s global price competitiveness.

Demographics are the key factor pushing up wages in China. In the past, China’s “demographic dividend” helped keep wages low and saving rates high. However,

Unit Labor Costs2005=100 170 160 150 140 130 120 110 100 0

2005 2006 2007 2008 2009 2010 2011 2012

china U.S.Note: 2012 Q4 data are unavailable for China, so 2012 is an average of Q1, Q2, and Q3 unit labor costs Source: BLS; China National Bureau of Statistics

4

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

China is losing some of its competitive edge. For example, Lenovo, a Beijing-based computer maker, opened a new manufacturing line in North Carolina earlier this year, creating more than 100 U.S. jobs. While the company reported that it remains slightly cheaper to manufacture in China, it said it could offset somewhat higher U.S. labor costs by savings on logistics.

Outside of the electronics and technology sectors, other companies are also announcing new manufacturing initiatives. For example, Starbucks, Caterpillar, Ford, and General Motors have each made recent announcements about shifting production and jobs back to the United States. A February 2012 survey by the Boston Consulting Group (BCG) found that 37% of U.S. manufacturers with sales of more than $1 billion said they were considering shifting production from China to the U.S.iii In all, BCG estimates that the manufacturing revival in the United States could bring in roughly 5 million jobs by 2020. While the true extent of the recent push for re-shoring in the U.S. remains to be seen, it is clear that this trend could lead to a fundamental shift in the economic relationship between the U.S. and China.

Service ExportsAnother factor that will shape U.S.-China economic interactions in coming years will be the shifting composition of the Chinese economy in the direction of services. In 2012, services accounted for less than 45% of China’s GDP. In comparison, the service sectors in the U.S., Germany, Japan, France, and the United Kingdom all

iii Plumer, Brad (2013). “Is U.S. Manufacturing Making a Comeback - Or is It Just Hype?”

America’s declining energy costs are now beginning to bring about a shift in industrial competitiveness. In a recent analysis at Keybridge Research, we found that the top 20 U.S. natural gas-intensive industries (fertilizers, industrial gases, flat glass, brick and clay tiles, gypsum, organic chemicals, etc.) experienced declines in their imports over the past six years, while imports of all other manufactured goods increased in the same period. While it may be too early to conclude definitively that the U.S. is developing a sustainable comparative advantage in energy, the country’s increased domestic production of natural gas seems likely to shift energy-intensive manufacturing to the United States.

In contrast, China is growing more dependent on expensive foreign sources of fuel. In 2011, China’s net imports of natural gas totaled 1 trillion cubic feet, and in December 2012, the country surpassed the U.S. as the world’s largest importer of oil—the first time in 40 years that the U.S. did not hold this title. China’s increasing dependence on expensive imported gas, in particular, is likely to reduce the competitiveness of some of its chemical, fertilizer, and other heavy industries. At least some of this production is likely to migrate to the U.S.

Increased “Re-shoring” in United States As China’s labor cost advantage dissipates and the United States capitalizes on its newfound energy boom, a number of U.S. companies are announcing plans to “re-shore” production—that is, shift production from overseas back to the United States. The Reshoring Initiative, a Chicago-based group that tracks examples of re-shoring, estimates that 50,000 jobs have been created in the U.S. as a result of re-shoring since 2010.ii While this only embodies roughly 10% of all manufacturing jobs created over the last three years, it represents a significant shift that is expected to gain further traction in coming years.

Of the jobs being re-shored to the U.S., the majority are coming from China. The electronics and technology sectors have been particularly vocal about their re-shoring plans. As one example, higher Chinese labor costs and cheaper U.S. energy prompted General Electric (GE) to shift manufacturing of its GeoSpring water heater from China to the U.S. When it made the switch, GE was able to reduce the product’s retail price by nearly 20% due to cost savings. Several Chinese electronics companies also have decided to set up factories in the U.S., another sign that

ii Moser, Harry and Kelley, Millar (2013). “The Reshoring Trend is Good for U.S. Engineers and America.” IEEE-USA Today’s Engineer: March 2013.

Examples of Re-shoring Electronic/Electrical Products back to the U.S.company Product re-shored FromApple Computers China

Digital Innovations Electronic Devices China

Electrolux Appliances Canada

Farouk Systems Appliances China

Foxconn LCD TVs China, Taiwan

GE Appliances China

Google Phones China

Lenovo PCs Asia

Seesmart Lighting China

Whirlpool Appliances China

Source: Keybridge Research, data as of 30 June 2013.

5

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

the RMB. By that year, the U.S. current account deficit had declined to 3% of GDP, and China’s current account surplus had fallen to about 2% of GDP.

In coming years, the economic forces described in this analysis—including rising wage costs in China and falling energy costs in the U.S.—seem likely to maintain and support these recent trends. With textiles, apparel, and footwear responsible for about one-sixth of Chinese exports and with global manufacturers now aggressively shifting such low-end assembly work to lower-cost countries, such as Vietnam, Cambodia, and Bangladesh, it is likely that rising wage costs in China will continue to reduce the competitiveness of these types of products and keep downward pressure on the country’s trade surpluses. Meanwhile, increased domestic energy production in the U.S. is likely to reduce the U.S. current account deficit by 1-2% of GDP, taking into account just the direct import substitution effects of more domestic energy production. Trade effects are likely to be even larger when allowing for increased exports of natural gas-intensive products.

accounted for more than 70% of each country’s respective economy. As China continues to develop and sees its wealth increase, services will become ever more important to its economy, and this should provide more opportunity for competitive U.S. service industries.

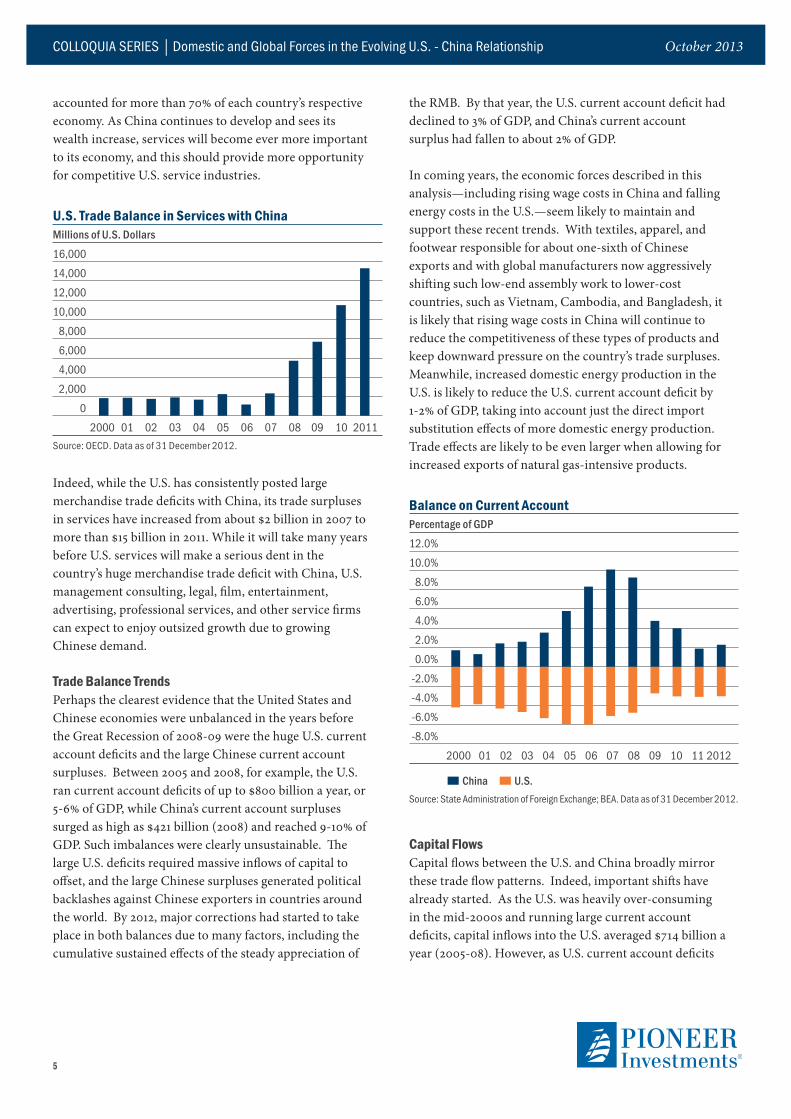

Indeed, while the U.S. has consistently posted large merchandise trade deficits with China, its trade surpluses in services have increased from about $2 billion in 2007 to more than $15 billion in 2011. While it will take many years before U.S. services will make a serious dent in the country’s huge merchandise trade deficit with China, U.S. management consulting, legal, film, entertainment, advertising, professional services, and other service firms can expect to enjoy outsized growth due to growing Chinese demand.

Trade Balance TrendsPerhaps the clearest evidence that the United States and Chinese economies were unbalanced in the years before the Great Recession of 2008-09 were the huge U.S. current account deficits and the large Chinese current account surpluses. Between 2005 and 2008, for example, the U.S. ran current account deficits of up to $800 billion a year, or 5-6% of GDP, while China’s current account surpluses surged as high as $421 billion (2008) and reached 9-10% of GDP. Such imbalances were clearly unsustainable. The large U.S. deficits required massive inflows of capital to offset, and the large Chinese surpluses generated political backlashes against Chinese exporters in countries around the world. By 2012, major corrections had started to take place in both balances due to many factors, including the cumulative sustained effects of the steady appreciation of

U.S. Trade Balance in Services with ChinaMillions of U.S. Dollars 16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

2000 01 02 03 04 05 06 07 08 09 10 2011Source: OECD. Data as of 31 December 2012.

Balance on Current AccountPercentage of GDP12.0%

10.0%

8.0%

6.0%

4.0%

2.0%

0.0%

-2.0%

-4.0%

-6.0%

-8.0%

2000 01 02 03 04 05 06 07 08 09 10 11 2012

china U.S.Source: State Administration of Foreign Exchange; BEA. Data as of 31 December 2012.

Capital FlowsCapital flows between the U.S. and China broadly mirror these trade flow patterns. Indeed, important shifts have already started. As the U.S. was heavily over-consuming in the mid-2000s and running large current account deficits, capital inflows into the U.S. averaged $714 billion a year (2005-08). However, as U.S. current account deficits

6

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

have moderated in more recent years, capital inflows have as well. From 2009 to 2012, for example, U.S. capital inflows averaged a significantly smaller $395 billion per year—that is, U.S. capital inflows in the past four years have been running at only a little more than half of the pace of the previous four years.

Meanwhile, as China was running huge trade surpluses of up to $421 billion per year during 2006 to 2008, its international reserves were jumping by $250 to $500 billion per year, and its capital inflows into the U.S. averaged $123 billion a year (2006-09). These were years when China’s purchases of U.S. Treasury bonds jumped sharply and represented a stunning shift from the 1990s, when China’s total capital inflows into the U.S. averaged just $7 billion a year. More recently, however, China’s trade surpluses have decreased notably, from an average of $339 billion per year (2007-09) to an average of just $189 billion per year (2010-12), and as a result, its accumulation of international reserves has slowed significantly. For example, its capital inflows into the U.S. have dropped to just $31 billion per year (2010-12).

Moving forward, capital flows between the U.S. and China will likely reflect the two countries’ overall trade balances more than their bilateral flows. There may be some rebound effect in 2013 as the U.S. economy continues to recover from the Great Recession of 2008-09 faster than its international trade partners do, including Europe, Japan, Latin America, and most of the rest of the world. With relatively faster growth in the U.S., its imports and trade deficit may bounce up, and, as a result, there may be

some temporary acceleration in Chinese purchases of U.S. assets in 2013 and perhaps 2014. However, the broader trends described above, including falling Chinese global wage competitiveness and rising U.S. energy independence, suggest that capital flows between the U.S. and China are likely to be more moderate in the next few years, and certainly smaller than they were in the 2006-09 period. Of course, with China currently holding $1.15 trillion of U.S. government debt, the two countries will continue to be inextricably linked financially for decades.

III. ConclusionFor most of the past 30 years, both the U.S. and China have experienced unbalanced growth. Now, each country must address new realities and move to more balanced growth. The key challenge for China will be to move up the value-added curve—to adapt from being the world’s low-cost factory to innovator and service provider. Meanwhile, the U.S. needs to exploit its newfound energy capabilities, use this energy to drive the continuing re-shoring of industrial activity, and keep its overall trade balance at manageable levels. Because of these changing dynamics, the relationship between the U.S. and China will inevitably evolve. In particular, trade imbalances between the two countries seem destined to become smaller over time. As a result, bilateral capital flows are also likely to be smaller in coming years, and likely much smaller than they were in the 2006-09 period, when the magnitude of the flows was truly stunning. Over the longer term, how the countries respond to these new realities and challenges will shape their relationship with one another and also with the rest of the world.

7

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

What are the main challenges that Chinese corporations may have to face in the next decade? The future of the private sector is strongly connected with the effort of the government to address imbalances and deliver a sustainable growth path in China.

Balancing capital allocation between the State-Owned Enterprises (SOEs) and the private firms is one of the key challenges that the Government is facing. SOEs, which have close connection with politics, have benefitted from preferential conditions in terms of access to credit and to business opportunities, sometimes embarking in projects with low internal rate of return and showing a total factor productivity growth which is estimated to be one third that of the private sector. Excessive investment of the last decade is in part attributable to the dominance of SOEs. Progress in terms of resizing the public sector has been done, and the private sector is absorbing more and more resources. Redesigning the role of SOEs in a perspective of efficiency and transparency could help to foster a sustainable expansion.

A second important challenge concerns urban development, which may also help to progress in the transition to a consumption-led growth model. Cities are the engine of Chinese expansion, in terms of consumption, as the urban saving rate is much higher than the rural one. But cities are also the pivot for future development in terms of production: the benefits of economies of scale in production and distribution, the possibilities of technology spillovers and innovation, all justify the measures enforced by the Government to encourage urbanization. At the same time rural development cannot be left behind: increased

Mauro RattoMauro Ratto is Head of Emerging Markets at Pioneer Investments. In this role, he is responsible for leading a highly skilled investment team working on debt and equity strategies that covers Asia, Latin America, Emerging Europe, the Middle East and Africa. Prior to his current appointment, Mauro was Head of Investment Management Europe and Asia.

With the contribution of Marco Mencini, Head of Equities – Emerging Markets and Andrea Salvatori, Head of Global EM & LatAM Equities.

regulation on land property rights, limiting the practice of expropriations, is in the agenda of the Government but needs to be implemented to ensure economic progress and social well-being go hand to hand.

These factors could have a material impact at a corporate level and on sectors that could benefit more from an enlarged consumption base, like the auto sector, technology and telecoms to mention few.

Do you believe that social disparities may interfere with the Government agenda in terms of economic growth? From a wider perspective, the big challenge for the Chinese economy is to broaden the benefits of growth, and to achieve a more balanced distribution of resources.

Chinese Corporations at the CrossroadPrivate Sector Gets Bigger as SOEs Slim – Distribution of Urban Employment 80%

70%

60%

50%

40%

30%

20%

10%

0%

31/03/1993 31/03/2003 28/06/2013Source: Bloomberg, National Bureau of Statistics of China, data as 15 September 2013.

Employed in State- Owned Units

74%65%

45%

25%

51%

24%

10%4%2%

Employed in Other Units

Employed in Collective-Owned Units

8

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

One of the consequences of overinvestments and export-led Chinese growth strategy has been the rise of inequality. Despite the fact that absolute poverty declined since China opened up to reforms, inequality rose substantially and at a very fast rate. The rural-urban income gap increased significantly and even if it is starting to decline, it remains high compared to the other Asian economies. Besides, inequality has been exacerbated by geography: notwithstanding improvements after the policies implemented since early 2000s, regional differences between costal and internal areas remain strong. While efforts are going in the direction of expanding the network of social protection, such as urban and rural minimum wage, or facilitating the access to medical assistance and education for rural areas, still a greater focus on these issues is needed to avoid social discontent and to allow an harmonious growth path.

Do you expect the competition coming from Asian labour rich economies and US energy renaissance may affect Chinese economy?The cost of doing business in China has increased in the last years, due to higher labour costs, environmental constraints, and higher controls. Some companies are moving production back to America, as production costs benefitted from the U.S. energy renaissance.

Encouraging the development of inner regions is containing the rise in Chinese wages: the 20 fastest growing cities are located inland, where wages are much lower than the coastal areas.

But the key factor in our positive assessment of Chinese corporations is that China is ramping up on the value chain. The giant HonHai, which employs 1.3 million people, offers extremely sophisticated solutions for the Western clients like Apple.

We believe that conditions are in place for China to progress in the path of innovation, to ramp up the value chain and serve the global trade not with more products but with more value. As a consequence of Chinese progress in this direction, we expect a reshaping of the geography of trade patterns, with potential opportunities arising in the markets well positioned to go along with China transition story.

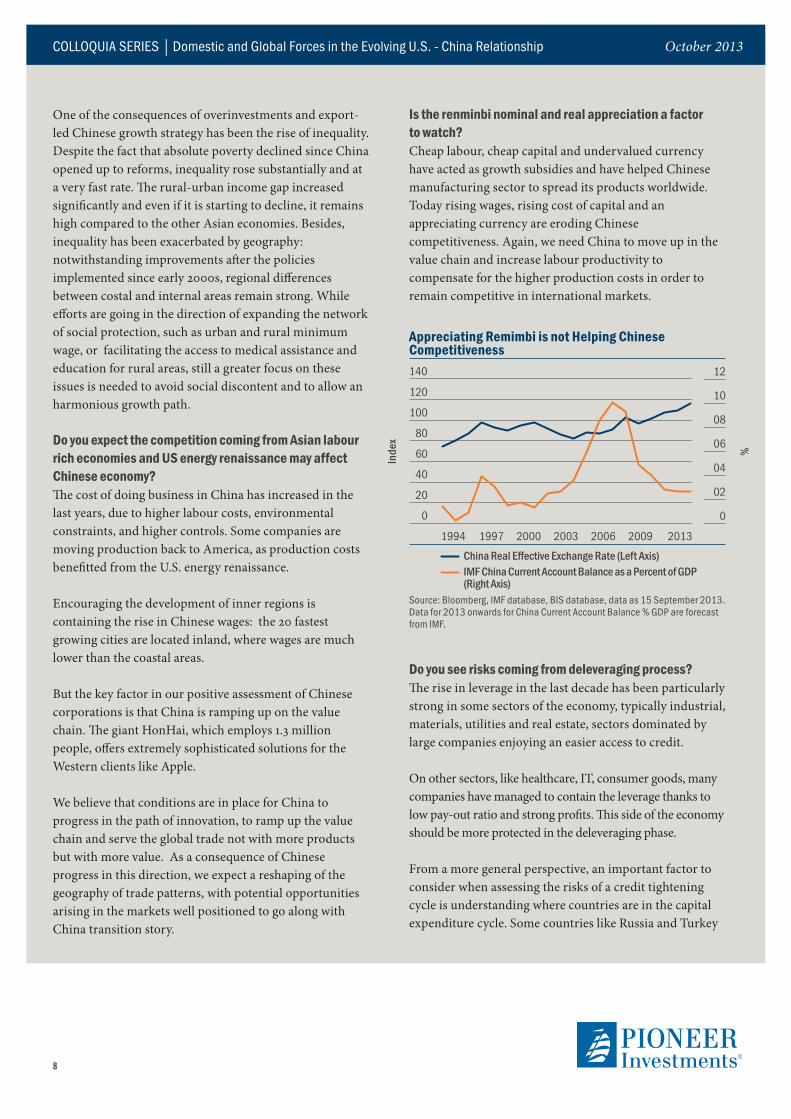

Is the renminbi nominal and real appreciation a factor to watch?Cheap labour, cheap capital and undervalued currency have acted as growth subsidies and have helped Chinese manufacturing sector to spread its products worldwide. Today rising wages, rising cost of capital and an appreciating currency are eroding Chinese competitiveness. Again, we need China to move up in the value chain and increase labour productivity to compensate for the higher production costs in order to remain competitive in international markets.

Appreciating Remimbi is not Helping Chinese Competitiveness140

120

100

80

60

40

20

0

1994 1997 2000 2003 2006 2009 2013

China Real Effective Exchange Rate (Left Axis) IMF china current Account balance as a Percent of GDP (Right Axis)

Source: Bloomberg, IMF database, BIS database, data as 15 September 2013. Data for 2013 onwards for China Current Account Balance % GDP are forecast from IMF.

Inde

x

%

12

10

08

06

04

02

0

Do you see risks coming from deleveraging process?The rise in leverage in the last decade has been particularly strong in some sectors of the economy, typically industrial, materials, utilities and real estate, sectors dominated by large companies enjoying an easier access to credit.

On other sectors, like healthcare, IT, consumer goods, many companies have managed to contain the leverage thanks to low pay-out ratio and strong profits. This side of the economy should be more protected in the deleveraging phase.

From a more general perspective, an important factor to consider when assessing the risks of a credit tightening cycle is understanding where countries are in the capital expenditure cycle. Some countries like Russia and Turkey

9

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

tend to be trapped in an old capital stock. Brazil’s industry is maybe in a worst situation, being penalized by years of underinvestment: the export boom in primary goods drove the currency over-valuation and undetermined the region’s competitiveness in the manufacturing sector. The Chinese corporate sector benefits from a relatively recent stock of capital, which is helping to shape a more balanced growth.

What are the distinctive features of your investment process?The evolving role of China in the global economy, and more in general, the complexity of Emerging Markets,

require deep research, local knowledge and extensive experience.

We have recently enlarged the investment team in order to allow for a higher degree of specialisation within the various teams on different strategies.

We engineer our portfolio construction process under a rigorous risk management system, and we put a strong emphasis on avoiding unwanted risk. On these premises we try to build stable alpha generation.

10

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

What will be the effect, if any, on U.S. competitiveness from the country’s energy renaissance and rising labour costs in China?Over the last decade, cutting edge exploration and extraction technologies have allowed companies in the U.S. to uncover and produce gas and oil resources which were previously inaccessible. After steadily declining for 30 years, oil production began to increase starting in 2008. According to EIA projections, the trend is likely to continue through the remainder of this decade, leading to a significant reduction in energy import dependence. The sharp increase in natural gas production has also resulted in a dramatic drop in natural gas prices. Today, they are only a fraction of the prices paid in Europe and Asia. Given that many global industrial and transportation sectors are reliant on natural gas, the U.S. could have a distinct competitive advantage.

At the same time that U.S. based companies are experiencing a competitive boost from a lower-cost energy, they are also becoming more competitive – from a relative basis – in terms of labor costs. China, the major destination of manufacturing outsourcing from the U.S. over the last two decades, is experiencing rapid wage inflation. Much of this is intentional as the Chinese are focused on developing a more consumer-centric economy as a counter-balance to their export reliance. As a result, the huge labour cost differential with other countries is rapidly shrinking.

Both of these trends are helping to drive the “re-onshoring” of manufacturing jobs in the U.S., and we believe this will be a longer-term secular shift.

Do you think the insourcing is going to have material effects on job creation and GDP growth rate?While the insourcing trend will have positive implications for the U.S. economy and job creation in particular, we think a massive migration of production to U.S. from China is quite unlikely. Insourcing will result in modest gains overall as companies build on to existing manufacturing facilities or develop new, more automated plants (that will need far fewer workers than those erected in the last century). We also believe that foreign companies will shift production on the margin to the U.S. as cost benefits from energy and productive labor combine with the high cost of transportation and regulatory considerations (such as the potential for trade barriers. Both trends over the next several years should add to the cyclical upswing in employment in the U.S. and help propel faster economic growth.

U.S.: Towards a Balanced Expansion

Michael TempleMichael Temple is Senior Vice President of Pioneer Investment Management, Inc., the U.S. investment division of Pioneer Investments, and Director of Credit Research, U.S. He is responsible for oversight of Pioneer Investments’ U.S. credit research department. His duties include independent research of credits, sector analysis, and co-ordination of research efforts in high yield, bank loan, investment grade, emerging markets and municipal credit.

Job Creation in Oil and Gas Sector: A Direct Effect of Energy Renaissance200001800016000140001200010000 8000 6000 4000 2000 0

Jan 00 Aug 02 Mar 05 Oct 07 May 10 Apr 13

U.S. Employees Oil and Gas (Right Axis) U.S. Employees Manufacturing Total (Left Axis)

Source: Bloomberg, Bureau of Labor Statistics, data as 31 August 2013

thou

sand

s

thou

sand

s

250

200

150

100

50

0

11

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

Do you believe that U.S. reindustrialization could have an effect on U.S. monetary policy and accelerate the wind-down of Quantitative Easing?Yes. We believe that this trend is helping to push employment higher in the U.S. Since unemployment is one of the key variables targeted by the Fed for its QE program, any acceleration in employment will have ramifications on the size and timing of the withdrawal of QE. As indicators are generally pointing towards an increase in the pace of economic activity and employment continues to climb, we believe that the end of QE is approaching.

What could be the implications for financial markets?The gradual removal of excess monetary stimulus may put upward pressure to Government bond yields, which are still very close to their historic lows. Credit markets were also primary beneficiaries of QE as buyers of treasuries and mortgages sought higher yields away from government markets. The removal of QE could put upward pressure on compressed spread levels – indeed we believe the backup in credit spreads since May of this year was in large part the market anticipating this possibility.

How do you see the relationship between China and U.S. evolving in the coming years?In the last few years U.S. foreign policy has been characterized by a process of “rebalancing” from the Middle East towards the Asia Pacific Region. The main impetus for this change of focus has been the growing importance of the region to the global economy combined with China’s strengthening military capabilities. One critical imperative for U.S. foreign policy is to defuse the growing tensions between Japan and China resulting from the growing risk of Chinese ascendency over the trade routes in the South China Sea. So the efforts of U.S. foreign policy will likely continue to be directed at managing Chinese dominance in the region. In this context we’ll likely see the U.S. continue to strengthen alliances inside the Pacific region, increase the dialogue with Chinese authorities, and provide support to trade partners through further military presence in the region.

China has been an important buyer of U.S. treasuries in the last decade. Do you think this trend is going to reverse and what could be the impact on Treasury bond market?China’s accumulation of Treasuries over the last decade has caused consternation among many market pundits. The

worry is that China, in becoming a significant owner of Treasuries might, at some point, be able to dictate financing terms to the U.S. or cause economic pain by refusing to buy or even sell its stock of Treasuries. But we believe that, rather than evidence of some nefarious conspiracy theory, the accumulation of Treasuries was evidence of an immature capital market unable to provide attractive reinvestment alternatives for its citizens enormous savings (itself a consequence of a lack of social safety net) as the country maintained a tight control over its capital account. This is beginning to change. We believe that, in an effort to promote greater consumption, the Chinese authorities could shortly embark upon a significant restructuring of its financial markets that will include opening up its capital account. This could give its citizens access to investments that could provide higher returns. More consumption will also likely lead to a more balanced current account as higher imports offset the historically unbalanced export trends. Indeed, we are already seeing evidence of this as China’s trade surplus has begun to shrink. This would mean that China will become a less significant buyer of Treasuries - indeed, over the past several years, this has already begun to materialize.

The longer-term impact on the Treasury market by a decline in Chinese demand is uncertain. A number of other factors, including the demand for treasuries from U.S. investors and from other countries and the supply of treasuries which will be driven by the size of the U.S. current account and fiscal deficits (which are both on a downward trend), will also influence the market.

What is your view on dollar?We believe the conditions underpinning a strong U.S. dollar are in place. The perspective of resilient growth in United States which has already started to outperform global growth, the Fed soon starting to remove QE, a new wave of technology changes limiting U.S. dependence on energy imports all support the idea that capital flowing back to the U.S. is not just a transitory phenomenon.

12

COLLOQUIA SERIES │ Domestic and Global Forces in the Evolving U.S. - China Relationship October 2013

Important InformationUnless otherwise stated, all information contained in this document is from Pioneer Investments and is as of 01 October 2013.

Unless otherwise stated, all views expressed are those of Pioneer Investments. These views are subject to change at any time based on market and other conditions and there can be no assurances that countries, markets or sectors will perform as expected. Investments involve certain risks, including political and currency risks. Investment return and principal value may go down as well as up and could result in the loss of all capital invested.

This material does not constitute an offer to buy or a solicitation to sell any units of any investment fund or any service.

Pioneer Investments is a trading name of the Pioneer Global Asset Management S.p.A. group of companies.

Date of First Use: 01 October 2013.