collection: barr, william: files folder title: [bob jones ... · 00-1473 - s.ct.no. 01-1 .·. bob...

TRANSCRIPT

Ronald Reagan Presidential Library

Digital Library Collections

This is a PDF of a folder from our textual collections.

Collection: Barr, William: Files

Folder Title: [Bob Jones & Goldsboro] (7)

Box: 2

To see more digitized collections visit:

https://reaganlibrary.gov/archives/digital-library

To see all Ronald Reagan Presidential Library inventories visit:

https://reaganlibrary.gov/document-collection

Contact a reference archivist at: [email protected]

Citation Guidelines: https://reaganlibrary.gov/citing

National Archives Catalogue: https://catalog.archives.gov/

. :·.· --... """ -· .. • ... ·

-~·l-.J.~--~: . ·· .. . . ·: ':- : ·,

e:j. v

. . . . .

'

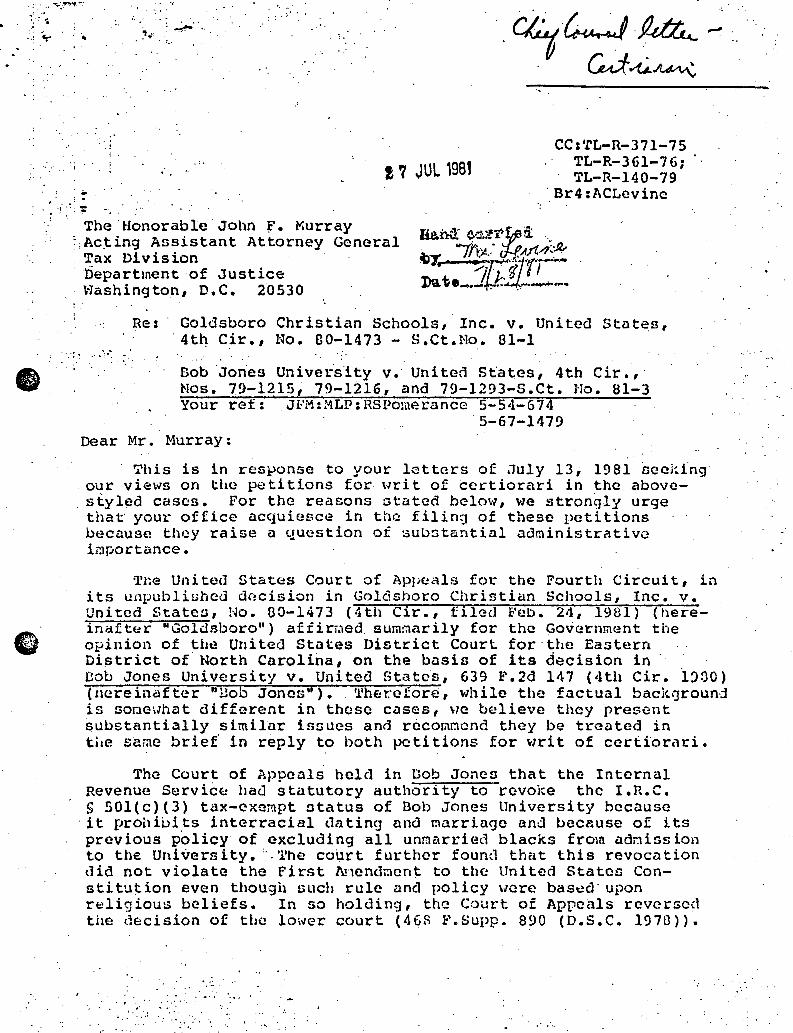

-; . ! 7 JUL 1981

Gd~.I'~

CC : 'l'L-R- 3 71-7 5 TL-R-361-761

· TL-R-140-79 'Br4:ACLevinc

• -1 ·• -, '~

The Honorable John f. Xurray ~ Ac~ing Ansistant Attorney General

Tax Division

. ;

tiepartment of Justice Washington, D.C. 20530

Re:· Goldsboro Christian Schools,· Inc. v. United States, · 4tq Cir., No. 00-1473 - s.ct.No. 01-1

.·. Bob Jones Univer.s1ty v. Unitecl States, 4th Cir.,· Nos. 79-1215, 79-1216, and 79-1293-S.Ct. no. 81-3 Your ref: JFM:MLP:RSPomerance 5-54-674

5-67-1479 Dear Mr. Murray:

?his is in response to your letters of .'July 13, 1981 occldng our views on the petitions for. writ of certiorari in the abovestyled cases. l"or the reasons otated below, we strongly urge that your office acquiesce in the filing of these petitions because they raise a question of sub~tantial administrative ii:1portance.

'11l~e Uni te<l States Court of Appc:als for the Fourth Circuit, in its unpubliuhcd dncision in Goldsboro Christiun Schools, Inc. v. United States, No. 00-1473 (4th Cir., filed Feb. 24, 1981) (hereinr.tf ter "Goldsboro"} afiirri'\ed summarily for the Government the opinion of tl:~ United States District CourL for·the Eastern District of North Carolina, on the basis of its decision in Cob JoneG University v. United States, 639 ~"'.2d 147 (4th Cir. l'.)00) (ucreinafter "l!ob Jones") •. '!'her.afore, while the factual backqround is sor:1ei1hat different in these cases, we believe they presant substantially similar istJucs and rcco1ancnd they be treated in the same brief· in reply to both pc ti tions for writ of ccrtiorciri.

Tho Court of Appeals held in Dob Joneo that the Internal Revenue Servicf;! ha<l statutory authority to re:voke the I.R.C. S 50l(c)(3) tax-exempt ntatus of Bob Jones University because

· it proh iL>i ts interracial dating and r.ia.rriogc and because of its prcv ious policy of excluding all unrnari.·ied blacks from adniss ion to the University. : .. 'l'he court further found that this revocc:ition did not violate the First 1\.ncndi'Jcnt to the United States Constitution even though r;uch rule ;:incl policy \/ere bas~a· upon r~ligiou~ boliefs. In so holding, the Court of Appeals rcvcrGcd the decision of the lower court (468 r'.Supp. 890 (D.s.c. 1970)) •

.. :·· . .-.: : ·.• .. : ..

. ' . ..... ·. : ~~

. ··~ .

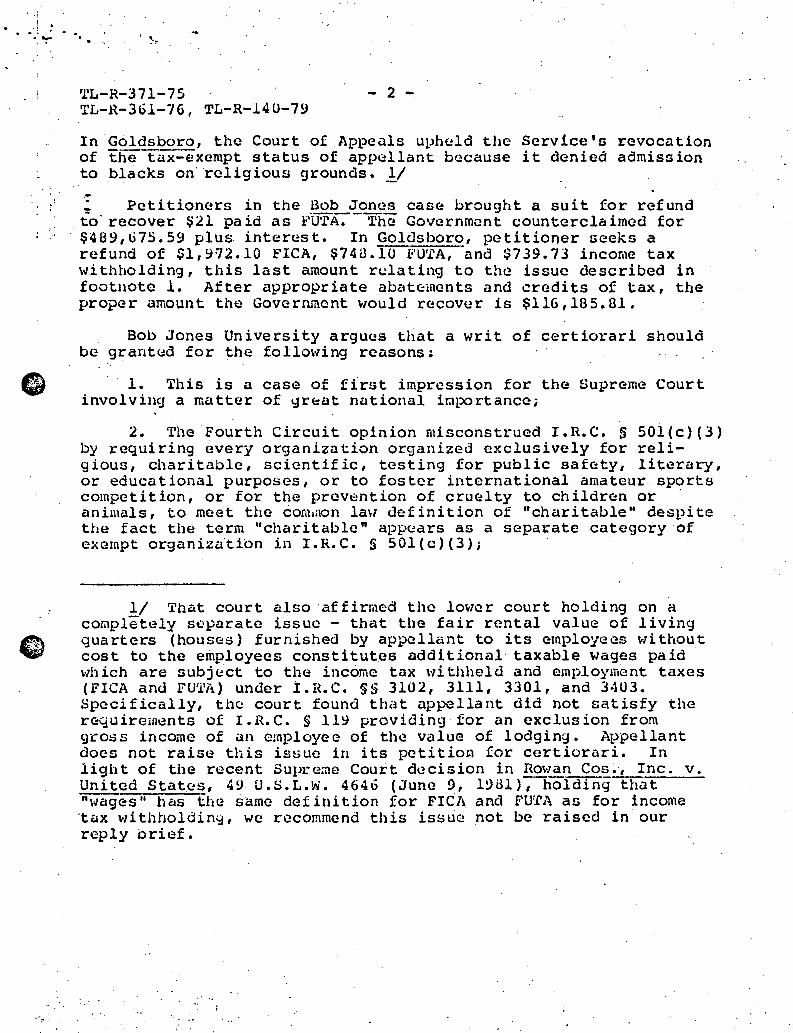

'l'L-R-371-75 - 2 -TL-R-361-76, TL-R-140-79

In Goldsboro, the Court of Appe~ls upheld the Service's revocation of the tQx-exampt status of app~llant because it denied admission to blacks on· rclig ious grounds •. !./

_ Petitioners in the Bob JonGs case brought a suit for refund to· recover ~21 pa id as li'u·rA:"'"- 'l'hc Gov~rnmi:?nt countercla imcd for $489,675.59 plus interest. In Goldsboro, petitioner Geeks a refund of $1,912.10 FICA, ~74o.10 Ii'U'l'A, ·and $739.73 income tax withholding, this last amount relating to the issue described in footnote l. After appropriate abate:rncnts and credits of tax, the prop~r amount the Government would recovur is $116,185.01.

Bob Jones University argues that a writ of certiorari should be grant(;!d for the following rcu.sons:

l. This is a case of first impression for the Supreme Court involving a matter of 11r&at nlltional iraportance;

2. The Fourth Circuit opinion misconstrued I.R.C. 5 50l(c)(3) by requiring every organization organized exclusively for religious, charitable, scientific, testing for public safety, literary, or educational purposes, or to foster international amateur sports competition, or for the prcvtintion of cru~lty to children or · animals, tO meet the COnl1rlOl1 la\.I definition Of "charitable" despite the fact the term "charitable" appears as a separate category of exempt organizati"on in I.R.C. § 50l(c)(3);

l/ That court also affirmed the lower court holding on a completely separate issue - that the fair rental value of living quarters (houses) furnished by appellant to its employees without cost to the employees constitutes additional· taxable wages paid which are subjuct to the income tax withheld and employment taxes (l"ICA and FU'..i.'A) under .t.n.c. §§ 3102, 3111, 3301, and 3403. Specifically, the court found that nppcllant did not satisfy the requirements of I.R.C. § llY providing for an exclusion from gro~s income of an employee of the value of lodging. Appellant docs not raise this issue in its pctitio~ for certiorari. In light of the recent Supreme Court decision in nowan Cos .. , Inc. v. United States, 49 U.B.L.w. 4646 (June 9, 1981), holding that "wages" has the same definition for FICA and FU'.£',\ as for income ·tux with holding, we recommend this issue not be raised in our reply brief •

: . .;... •..: ....

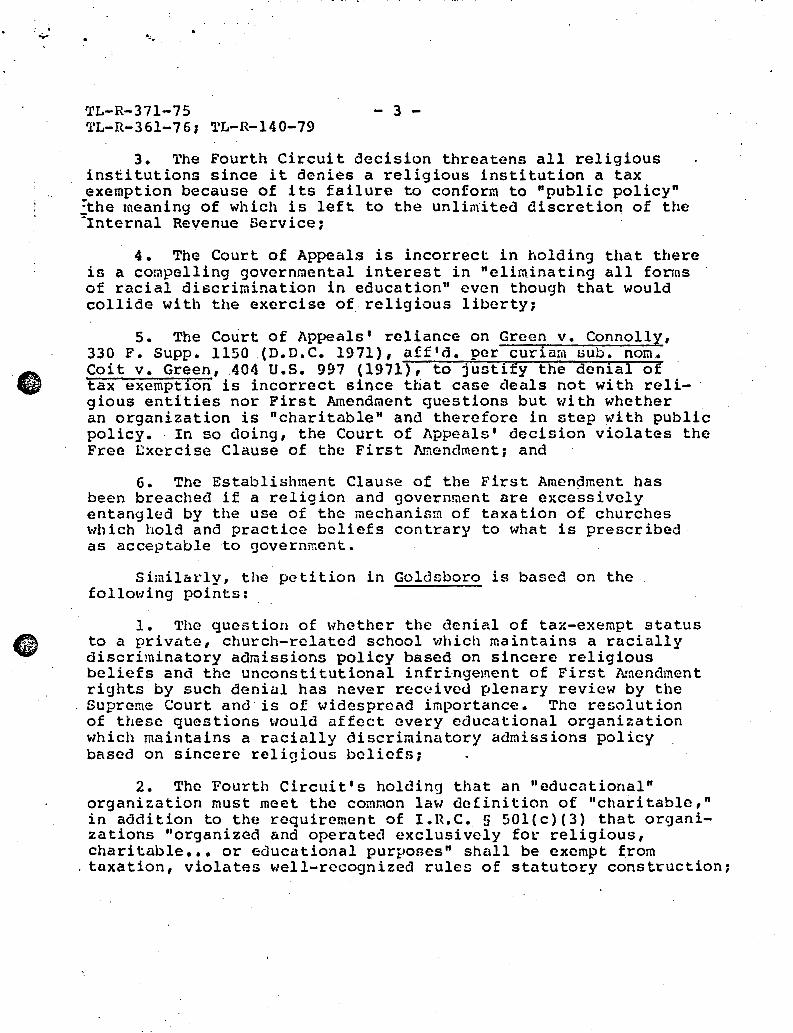

TL-R-371-75 - 3 -TL-R-361-761 TL-R-140-79

3. The Fourth Circuit decision threatens all religious institutions since it denies a religious institution a tax exemption because of its failure to conform to "public policy" ~he meaning of which is left to the unlimited discretion of the -Internal Revenue Service~

4. The Court of Ap~als is incorrect in holding that there is a compelling governmental interest in "eliminating all fonns of racial discrimination in education" even though that would collide with the exercise of religious liberty1

s. The Court of Appeals' reliance on Green v. ConnollX, 330 F. Supp. 1150 (D.D.C. 1971), aff'd. per curiam sub. nom,. Coit v. Green, .404 U.S. 997 (1971), to justify the denial of tax exemption is incorrect since that case deals not with religious entities nor First Amendment questions but with whether an organization is "charitable" and therefore in step with public policy. In so doing, the Court of Appeals' decision violates the Free Exercise Clause of the First Amendmenti and

6. The Establishment Clause of the First Amendment has been breached if a religion and government are excessively entangled by the use of the mechanism of taxation of churches which hold and practice beliefs contrary to what is prescribed as acceptable to government.

Similarly, the petition in Goldsboro is based on the following points:

1. The question of whether the denial of tax-exempt status to a private, church-related school which maintains a racially discriminatory admissions policy based on sincere religious beliefs and the unconstitutional infringement of First Amendment rights by such denial has never received plenary review by the Supreme Court and is of widespread importance. The resolution of these questions would af fcct every educational organization which maintains a racially discriminatory admissions policy based on sincere religious bclicfs7

2. The Fourth Circuit's holding that an "educational" organization must meet the common law definition of "charitable," in addition to the requirement of I.R.C. 5 50l(c)(3) that organizations "organized and operated exclusively for religious, charitable ••• or educational purposes" shall be exempt from

. taxation, violates well-recognized rules of statutory construction1

. . . ~ . ... . . ~ • ..•.

TL-R-371-75 - 4 -T~-R-361-76; TL-R-140-79

3. The Fourth Circuit's decision gives judicial approval to the unconstitutional exercise of legislative powers by the !nternal Revenu~ Service, an.adninistrativc agency1

4. · ~ince there is no evidence of any Congressional intent to deny tax-exempt status to educational organizations, like this appellant, the Fourth Circuit violated the holding of NLRD v. Catholic Bishop of Chicago, 440 U.S. 490, 507 (1979); and -

. s. The Fourth Circuit's decision, forcing the school either to cease practicing its sincere religious beliefs because they are contrary to federal "public policy" as announced by the Internal Revenue Service or to incur a high tax burden, is an unconstitutional infringement of the school's rights under the Free Exercise Clause of the First Amendment.

. . We strongly urge that the Government acquiesce in the

petition for certiorari in both Bob Jones and Goldsboro because of the substantial administrative importance of the questions presented. The g~eat significanc~ of these issues has already been recognized by certain Supreme Court justices in a dissent to the denial .of a petition for writ of certiorari in Prince Edward School Foundation v. United States, U.S. ~~(No. 80-484), cert..!-denied Feb. 23, 1961 (81-1 U.S.~.C-.-~ 9203).

In Prine~ Edward, the U.S. 'District Court for thci District of Columbia (the U.S. Court of Appeals for the District of · Columbia affirmed per curi~ in an unpublished opinion on June 30, 1980) upheld the Service's denial of tax-exempt status to a

. private school which discriminates in its admissions policy. Justice Rehnquist, who was joined by Justices Stewart and Po~cll, wrote that the validity of the 11Service's policy of denying tax-exempt status to private schools which have a racially discriminatory admissions policy is not apparent from a reading of the relevant provisionn of the 1954 Code." He states that, "[a}rguably," the separate references to the different types of organizations entitled to tax-exempt treatment in I.R.C. 5 50l(c)(3), "reflect Congress' lntcnt ~hat not all educational institutions must also be charitable institutions (as that term was used in the common law) in order to receive tax-exempt status."

Justice Rehnquist further states that "the authority of the Secretary of the Treasury to promulgate this policy regarding the tax status of private schools is sufficiently question~ble

. . .. . .... . . .,

'I'L-R-371-75 - 5 -TL-R-361-76, TL-R-140-79

to merit review by this Court," nnd "[t]he questions presented by this petition are of widespread importance." He concludos that the "time has come for this Court to d~al with the difficult. statutory and "constitutional questiono raised in this petition •••• "

....

-=- A concor,1i tant reason as to v1l1y tt1c c;ovorn1ncnt nhould urge the Supreme Court to grant a writ of certiorari is that tha Service has been stymied in the applicution of these principles by Congressional appropriation ridero. 'l'he Ashbrook Amendment (Section 103) to the Treasury, Postal Service, and General Government Appropriations Act, 1980, Pub. L. 96-74, 93 Stat. 559, prohibits the issuance of "revenue procedures in a~ area where legislation may be more appropriat1:1." House Committee on Appropriations, H.R,. Rep. No. 96-248, 96th Cong., lst Sess. at 14-15. Congress prohibited the Set"vicc from UE:>ing any funds appropriated to implement or enforce c:rny rule or procedure "which would cause the loss of tax-exempt status to private, religious, or church operated schools under Section 50l{c)(3) .•• unless in effect prior to August 22, 1978." The Ashbrook Amendment docs not apply to the instant suits because tax-exempt status wau denied prior to tlrnt date. The Dornan Amendment (Section 615) to the above-stated Act prohibited the Service from expending any funds for carrying out two proposed revenue procedure~> in this area (to be discussed subsequently). However, the point rcma ins that the Court, by deciding these cases, can clarify an issue \Jith such fnr-reaching ef feet.

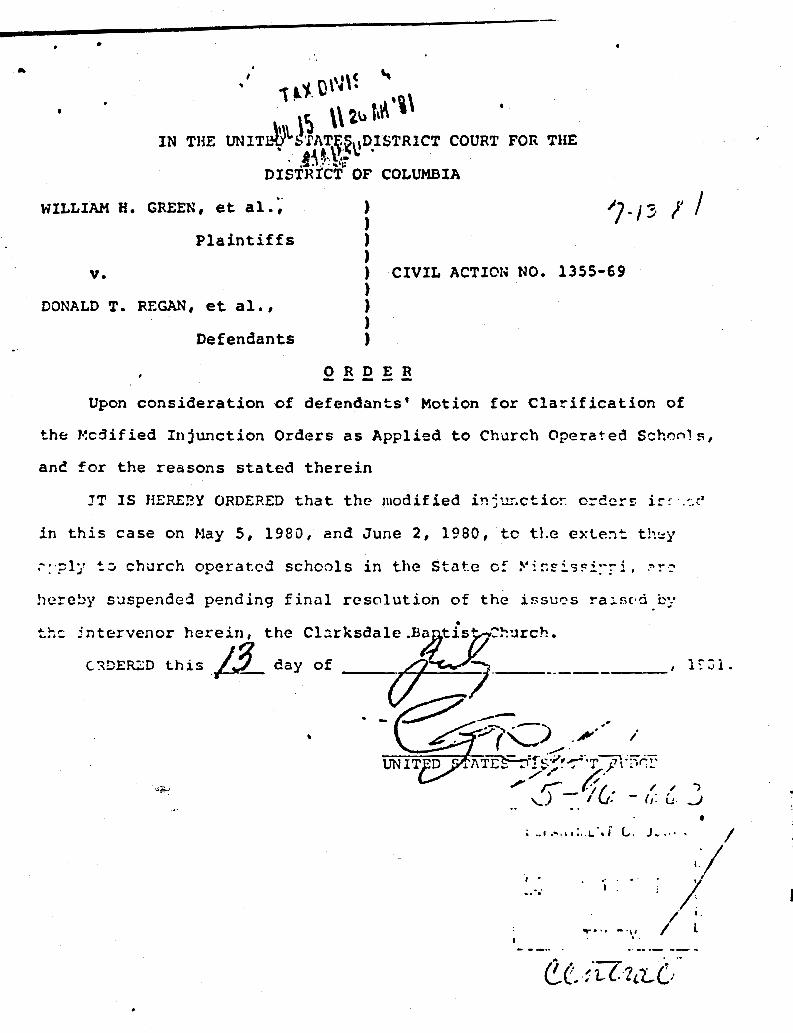

Specifically, Supreme Court review uill greatly facilitate the final resolution of Gruen v • .Regan, Civ. No. 1355-69 (D.D.C.) currently before the U.S. District Court for the District of Columbia, in which the Service is under an injunctive orde_r to investigate certain Nissiosippi private schools to determine if they qualify for tax exemption. •rwenty-nine church-operatell schools in Mississippi have been identified as potentially subject to the Court's order. One church-related nchool, the Clarksdale Baptist Church, has intervened and raif.;ed First Amendment issues. ?ursuant to the government's motion, the court has suspended the inJunctive order as it relates to the church schools - pe1~ing resolution of the issue by the intervenor.

In ~-;riqht v. Regan, 430 1'"'.Supp. 790 (D.D.C. 1979), E"CV'd and rem'd, o.c.c.A. No. U0-1124, (Ol-2 u.s.T.C. ' 9504), the United States Court of Appeals for the District of Colurnbi«

. . . . . . . • . -r .~ .... • . ~

TL-R-371-75 - 6 -TL-R-361-76; TL-R-140-79

on June 10, 1981, reversed Ju~ge Hart's dismissal of the case, ·:naldirig that nontaxpayer plaintiffs havo standing to sue to ~ornpel the Service to adopt, on a nationwide basis, standards ~reposed by them t~ deter~inc whether a private school is racially discriminatory and to revoke the tax exemptions of those schools which do not meet plaintiffs' standards. It is presently anticipated that the Government will seek a rehearing en bane and possibly a petition for a writ of certiorari, because the principle involved, whether a nontaxpaycr may compel a particular enforcement program against others, is one of great significance to the Service. The future course of the litigation would be greatly facilitated if the underlying substantive issues are clarified and determined by the Supreme Court. In this regard we understand that there are over 15,000 religious schools which might be affected should the plaintiffs' standing in Wright be upheld.

While we agree with petitioners that writs of certiorari should issue to review these qucstionn of great national importance, we nevertheless believe that the arguments made by pct·itioners in support of their petitions are incorrect. First, it is clear that Bob Jones University wraps itself in a religious mantle (framing the issues in its petition (at page (1)) purely in terms of religious beliefs), so as to better invoke the protections of the First Amendment Religion Clauses. Bob Jones University is a secular, educational institution "not affiliated with any religious denomination, but maintaining a fundamentalist orientation in its educational approach." (Bob Jones at 149). While the pervasive ethic at Bob Jones University is religious, it nevertheless offers some fifty accredited degrees and otherwise has all the accouterments of an institution of higher learning. we therefore believe that Bob Jonas University is a secular school and educational institution; this facti rather than its religious nature, should be emphasized in our brief.

The real question then is not whether religious organizations qualify for the tax exemption, but whether an educational organization which discriminate on the basis of .race in admissions policy should be denied the tax exemption. ·

" The Fourth Circuit's opinions in Bob Jones and Goldsboro are sound opinions. Ao to whether "charitable" is a oeparutc kind of organization eligible for tax exemption under I.R.C. § 50l(c)(3) or is to be viewed in the broad common law oense as

.....

..

' .. · ... .: ·-

A w

TL-R-371-75 - 7 -'l'L-R-361-76, TL-R-14 0-79

~equiring that an institution must not violate public policy, the Fourth Circuit correctly relics on the District Court opinion in Green v. Connolly, !>_l!.12.r~. In GE~£!!, the three judge court held "(t]he code must be construed and applied in conaonance w:i th the federal public policy against support for racial scgreifation of schools, public ancl private." 330 P. Supp. at 1103.

On page 10, footnote 9 of the Bob Jones petition, petitioner cites a 1923 published position of the service that "charitable" is to be used in its restrictive sense. This has been rejected by the Court itself in Simon v. Eastern Ry._Wc.:,~farc Ri9htf! Organization, 426 U.S. 2G (1976) \/herein the Court .stated that "charitable" is to be used in its generally accepted legal sense and not netrrowly, ·pointing to Rev. nu1·. 56-105, 1956-1 C.D. 202 that "charitable contemplates an implied public trust constituted for some public benefit ••• " Thus, there is no conflict with the Supreme Court on this raattar. Even so, we do not recomm.end opposing· certiorari on this ground because of the substantial . administrative irnportanc~ involved.

'!'he legislative history of I.n.c. 5 50l(c)(3) verifies the foundation of the exemption in public policy dthat the Government is compunsated for the loss of revenue ••• by the benefits resulting from the promotion of the general welfare." H.R. Rep. No. 1:320, 7Sth Cong. 3d Sess. 19 (1939).

As the Fourth Circuit further stated, the Gree?n court correctly noted th<:tt tax bcnefita such as deductions-and exclusions generally are subject to limitation on public policy grounds. See Tank Truck Rentals v. Commissioner, 356 U.S. 30 (195B) whero the Court held that a busJ.neBs d-eduction under I.R.C. § 162 could not be allowed if "sharply d~f incd 11 pui.>lic policy would be frustrated. 356 U.G .. at 33. 2/

2/ 'l'hc Green holding is ::;till viable even though Justice Hehnquist statc:d in his dissent from denial of petition for certiorari in Prince Edua~£, suE._L.:_f!, footnote 1, that Gre_cn 's af f irmance in Coi t_v. Gi:_ucf!., supr~_, lacks prccedcntial wu igh t. because no adversarial controversy remained in Green by the time the case reached the Court. Sec Bob Jones v. Simon •116 U.S. 725, 740 (l!J74).

. •._ ..

TL-R-371-75 - 8 -TL-R-361-7_6; TL-R-l4 0-79

The racial policies of Bob Jones University and Goldsboro Christian Schools, Inc. violate "the clearly defined public policy, ~coted in the Constitution, condemning racial discrimination ~nd, more specifically, the government policy against subsidizing racial discrimination in education, public and private.w Bob Jones at 151. ·

Nor did the Fourth Circuit find that the nondiscrimination· policy violates the Free Exercise Clause of the First Arncnd~ent; rather, it found the governmental interest in eliminating all forms of racial discrimination in education to be compelling. Brown v. Board of Education, 347 U.S. 483 (1954)1 (private action as well as public) ~unyon v. Mccrary, 427 U.S. 160 (1975).

What is significant here in terms of the First Amendment, is that i( tax exemption is denied, the University is not prohibited frora adhering to its policy. Even if the policy is abandoned, the University can still teach its religious doctrines. Students at nob Jones University arc not forced to violate their beliefs nor arc they forced to marry or date outside of their race. Dob Jones at 154. ·

On page 11 of the petition in Bob Jones, petitioner states that the Service has sought to proscribe religious freedom in a proposed revenue procedure which would have denied tax exemption to religious schools colely on the basis of racial criteria and without regard to religious criteria. PROPOSED REVENUE PROCEDURE ON PRIVATE TAX-EXEMP'l' SCHOOLS, 43 Fed. Reg. 37296 (1978}. Petitioner indicates that under this proposed procedure, an Old Order Amish or Orthodox Jewish school would lose its tax exemption. However, petitioners have failed to mention that the Service announced a revised proposed revenue procedure on February 9,·:. 1979 (published at 44 Fed. Reg. 9451 (Feb. 13, 1979), which would have in effect excepted from the application of this policy, schools where special circumstances "limit the school's ability to attract minority students, such as an emphasis on special programs or special curricul~ which by. their nature are of interest only to identifiable groups which are not composed of a significant number of minority students, so long as such programs or curricula are not offered for the.purpose of excluding minorities."

. "l

. ·• . . •· .. -- ... •. •;- ......

TL-R-371-75 - 9 -TL-R-361-76, TL-R-140-79

Finally, the C9urt of Appeals rejects the argument that the nondiscriminatory policy violates the I::ntablishment Clc1use of the: First Amendment which requires that a law reflect a secular

. legislative purpose, have a pri1:tary effect that neither advances ni>r inhibits religion, and avoid excessive entanglement with religion. It holds that the compelling notice of the governmental interest here overrides conflicting r~ligious practices, as in Reynolds v. United Stateo, 98 U.S. 145 (l87U) and prince v. M~scachusetts, 3il U.S. 158 (1944), even though religions that do not cmga<:Je in such practice are favored. Hor docs the Court of Appeals find that there is created the kind of excessive entanglement with religion found in !1LHB_y...!._£_~~oli£_.!!ishop of Chicaao, su;era. Moreover, the petitioner's discussion on page 13 ot its petition -- that these protections are guaranteed to a church-- is belied by the fact that Bob Janos University, even though pervasively and religiously inotivutcd, is a secular educational institution.

Catholic .Uishoe is also referred to in the: Goldsboro petition for the: proposition that when a feder.:ll statutory requirement is extendtd to religious institutions thcrt?by raising subGtantial constitutional issues under tho Religion Clauses of the First A!nendmcnt, that that extension must not be left to implication but instead must be "clearly and affirmatively expressed" by the Congress. Catholic Bisho~ at.501.

However, in finding a Pirst Amcndmf~nt infringement, in Cntholic Bishop, the Court found that NLnn jurisdiction over the alleged unfair labor practices would first require inquiry into the good_ faith of t.he position assert ca by the clergy ad111inistrat ion and tho school's religious mission, and second, the NLRB's det.crmination of "terms and condi tiono of employment" would involve the Board in "nearly everything that goes on in the schools." Id at 502-03.

By contrast, the Court of Appeals in these cases, correctly conclud~d there vas a much narrm1cr 1scope of governm~nt involvement -- the only inquiry being whether the school maintains rucially neutral policies. n [':l"']he uniform application of the rule to all religiously operated schools i1voids the necessity for a potentially entangling inquiry into-whetllcr a racially restrictive pr~cticc is the result of sincere religious belief.

·., ........... ,. .............. ____ .

. . . .: .. .. . :--· .... . • ..

TL-R-371-75 - 10 -TL-R-361-76; TL-R-140-79

The provision-in question involves minimum intrusion into the -operation of the school while serving important government · ·:-interests." ·Bob Jones at 155. (Emphasis in original.) In ~footnote 10, the Court of Appeals found that taxation itself involves some degree of government involvement and is in·evi table

·whether the tax exemption is granted or denied. Walz v. Tax Commission·of New York, 397 U.S. 664, 647-75 (1970). "We do not think the administrlltion of tax laws or the "hazard of churches supporting government' violate the 'excessive entanglement' prong of the Establishment Clause."

As to the ·Goldsboro petition's first reason for granting the writ,. we agree.· However, wc do not agree with the extension of that argument that the Fourth Circuit' decision would empower the Service to deny tax-exempt status to a Catholic-supported hospite)l that refuses to permit abortions to be performed in its operating·roorns based on its sincere religious belief$ because the hopital's policy violates federal public policy as defined in- Roe v. Wade, 410 U.S. 113 (1973). These are, of course, not the facts of this case nor is it even known what anyone would do in that situation.

The remaining arguments in the Goldsboro petition have alreacy been addressed. However, we-would further add that the second and third arguments (p. 9 of the petition) are not reasons for Supreme Court review but ar9uments why petitioner thinks the Fourth Circuit was wrong. An stated earlier the Sc:rvice did not exceed its administrative powers. Green, supra. As to the fourth reason, Catholic Bisho_E., supra, is distinguishable as stated above. There is no infringement of First Amendment rights for the reasons stated above.

The petition in Goldsboro (pages 14-16) indicates the Fourth Circuit failed to toke account of thd vacillating position of the Service over the years with respect to tax-exempt status of educational organizations which maintain racially discriminatory admissions policies. No doubt, a policy such as this one is an evolving one. Noreover, the Green cusc·supports the Service position. Such a position as is now being taken is not a subjective and arbitrary judgment by Service bureaucrats (page 23 of the petit~on) but an expression of public policy recognized in the legislative history, and by the Court in Eastern Kentucky, supra.

. ..

: i

>.

'""" n,,w,.I\ tnev. tH:SUJ \li&rDOn Attached Version of Form 1937) *U.S. GOVERNMENT PRINTING OFFICE-3956M 6180 321·339

. ·-.··~ :·· '; ..... . ...... ..

1'

Code

Surname

Date

TL-R-371-75 - 11 -TL-R-361-761 TL-R-140-79

We agree with the first part of the statement on page 19 of ~he Goldsboro petition that the Ashbrook Amendment does not apply ~o this case. This legislation does not mean, however, as .petitioner states, that the prohibition expressed in the Ashbrook Amendment nevertheless applies to this case. If Congress had intended the Ashbrook Amendment to apply to these cases, it would not have imposed the condition that the legislation does not apply to the loss of tax-exempt status prior to August 22, 1978.

CONCLUSION

We strongly urge acquiescence in the petition for writ of certiorari in Bob Jones University and Goldsboro because the questions presented are of substantial administrative importance. The proper standard to apply in determining the tax exemption of ari educational institution which discriminates in its admissions policy is of great national significance. For the other reasons stated above, we disagree with the arguments made by the petitioners in support of their tax exemption.

If additional information is needed, please call Alan c. Levine at 566-3256.

·LEVINE/dvs/7-22-81

,.... Initiator '\"'"1 ~;L: 'J-· . ~ ...... -:::

=-, .. ~ "/ QI t .t..-~ •• I

Reviewer

,. .....

Sincerely,

JEROME D. SEBASTIAN Acting Chief Counsel

Reviewer Reviewer Reviewer

-···•.

- . ·- ·.-· --·-·----·· -·-· -· ---------- .. _, __ .. -- _ _,_ -·-· _ ... _ ... __ ... _ ...... ________ .... __ . ____ ..,___ . -··---

P.c:1orable Tre:..,t IDtt lb.se of Reprt'.sentatives Uas1'.i.1\.~on, DC 20515

Dear Mr. Lott:

.-----~·--·-·· -'·--·--- -·- -- -··- --· -----·-:-- ...

July 17. 1931

On l:·e;.;.slf of Co!Tmissioner E~::a_r, I em admc;'7led.~ receipt of your letter dated July 10, 1981, rer;nrding the continuin~ litigation in <:r~en v. llcc::~. l·~e appreciate rceeiving YJ\% nddi.tionci.1 viev13 tt"t .. ~~ -di £ ' d .. ,,. ... L...... .... n.:.-t-· 1.u.J..S n"lttCr e:u. .. 1av-e or.·:r.arc-2 1..4!:-r.l ... o O'.Jr l."'1ga"'icn .uJ.v.L.:>l.Ort.

l-:'ith kind rcgn:rcls,

Sincer.~ly,

Charles H. ~··:'h~lcr Ansistc:mt to t:l'-..e Ca:!nissio:li>..r

. ?toted by DTR 81-10652

INFORMATION

Date: July 14, 1981

MEMORANDUM FOR: SECRETARY REGAN THRU: Deputy Secretary McNarnar(Vf'3)

From: Peter J. Wallison~ Subject: Mississippi Schools Matter

Surname

Initials Date

A Deputy Chief Counsel of the Internal Revenue Service advised me today that the subject of the Service's position

. on delaying the revocation of tax exemptions for certain Mississippi schools arose at a court conference on a related matter late last week. The court made no ruling.

_After the court session, the Justice Department attorney who is handling the matter spoke with counsel for the petitioners, and it was his impression that the petitioners were content to await the expiration of the 45-day period requested by the Service before taking any further action. This appears to end controversy on the matter until mid-August.

cc: Dennis Thomas Ann McLaughlin

Initiator Reviewer

Wallis on

Reviewer Reviewer Reviewer

LC hew

Ex. Sec.

S18kancke

Form OS-3129 Department of Trusury

.. •

IN THE

\•\< " , .. ~. t)\ ~ • •

· ~ \\ ~u f,~ i\ UNITL~\.~.l'AT~~\!DISTRICT COURT FOR THE

•.. j~·':~ .. ; . DISTRICT OF COLUMBIA

WILLIAM H. GREEN, et al.~ ) , Plaintiffs

v.

DONALD T. REGAN, et al.,

Defendants

) ) ) CIVIL ACTION NO. 1355-69 ) ) ) )

0 R D E R - - - - -Upon consideration of defendants' Motion for Cla~ification of

the P.cdified Injunction Orders as Appli~d to Church Operated Sch~n1s,

anc for the reasons stated therein

!TIS HEREBY ORDERED that the modified injur.ctic~~ c:-ccrs i::-~·.:.(1

in this case on May 5, 1980, and June 2, 1980, to tl.e exle:i-:. th~y

:-:·?1:,.~ -t.:, church operated schools in the State cf ~·i~~is!!!:--;.i, ."'!"·::'

herc!.)y suspended pending fin al re solution of the i~sut:>s :ra .:..sc·d. by

in t~rvenor herein, the Cl:.rksdale .B'1Jtis0:~".lrch.

OU>ER::D this J':? day of -~---f--../- . v ~7 ----

--~---6:;,?r"C) Al'.... / /'

~ A Tr:'~-~·f~ ~.;.r,,_.:· .. " 11 ;;)r.Y. J. ...... /""-"'" .. /:)· • ·-

,. r:-_If/, ~ /' I '-) I lJ. - (1. LI· ....)

' 1~::;1. ---

• ' ........ ,,: .. '-·,; L. J~.... I

. .-; , . . •j !'

/ I.

I l

I

<~ ':y :.)" .. _ ..

•

- . .;.-1 ... ~- !

1' I I.

l I

•.

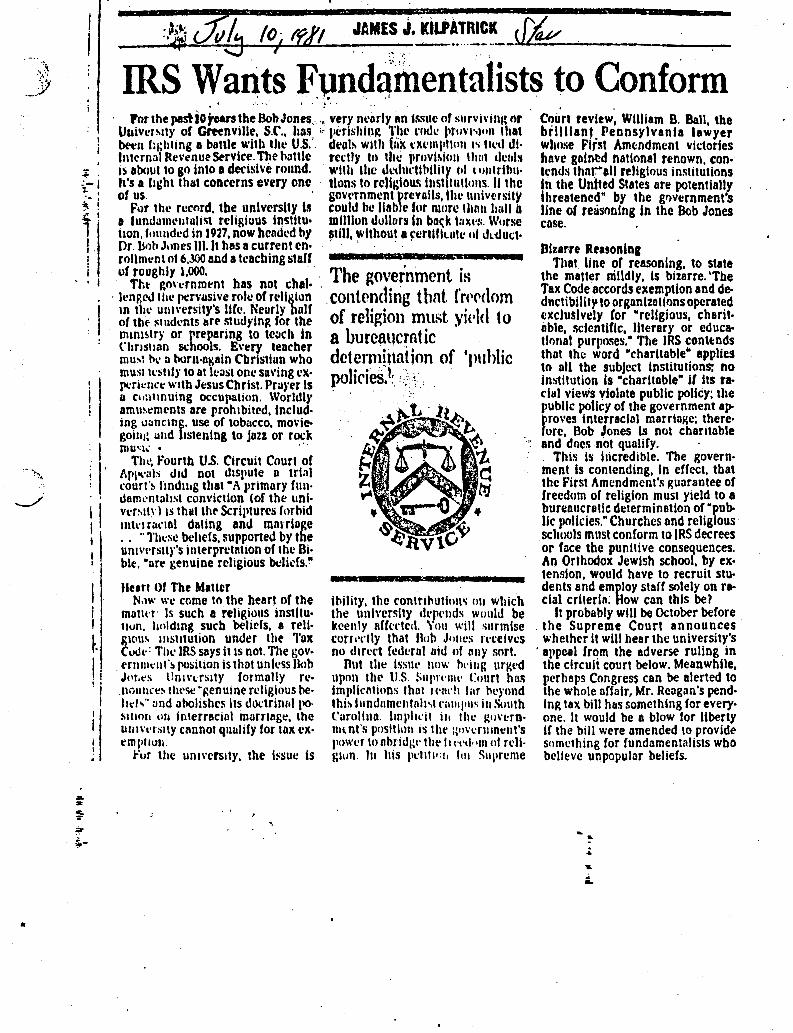

:~ J:4 /Oi tp/I ~ME~~. ICll.P~Till~~-- ..... (/4 ...... ~---------IRS Wants Fund~l'fnenta1ists to Conform

' . . ~ • . . , I ·,

· Pnrthe past lo tears the Bob Jones ...• very m·arly an issue of survi\'illft or Uuivcrsuy or GmnvilJe. s.r .. ha!i. •·· Jicrishln~ 1'1ll' l'Oth: t1r11v1·.ion that bt>t-n f:ghtmg a battle with the U.S.' dt'uh~ with fiix "''u:mi1111111 1s t1l'll di· lntl.'rnal Re\'enue Service. The hattle rcc:tly h> the vrovlslou I hut Llc111!1 is about to go into 1 dec-1i;ive round. ¥'lib lhc dl'LlnrUNlity C•I \ 1111trllm· It's a fight that concerns e\•ery one · tions to reUi;iou!i tnsllltlltons. II the of us. · gov\•rnmcnt t>revalts, Uw university

f ,n the record. tbe university I~ could bt? Uable lor mnte lhnn halt a a fundatnl'lltuh~t religious institu• million dollors ln ba(k tmwi;. Worse taon. founded in 1927, now bended by still, wUhout a ~crttfkutc of lkduct· Or. U•)ll Junes Ill. It hos a current en· · · · rollmcnt of 6,300 and a teaching staff --·--·:1111•-nm._ .... _ _._ .. ,

. .

Court review, Wutiam B. Ball, the brUUant_ Pennsylvania lawyer whose Flr5t Am<:ndment victories hove gaf nt?d national renown. con· tends thnl-'ell religious in1ilitutions In the Untted States ore potentially threatened" by the government's line of reasoning in the Bob Jones case.

Bliarre Rtasonlna

ur roughly i.ooo. The aoverninent is · I · Tht g<wcrnmt-nt has not chal· n

· lt'ngoo thL' pt:masiverolc ofrcUglun . COl1i.(lnding t hot. f'rt'Nlom

That line or reasoning, to state the matter mildly, is bizarre. 'Tbe Tax Code accords exemption and de· dnctibility to organizations operated cxcJusJvely for "religious, charit· oble, scientific, literary or educa· t1011a1 purposes: The IRS conttnds that the: word "charitable• applies to all the subject institution$! no in!\1itution is "charitoble" if its racial views violate public policy; \he public potlcy of the government approves interracial marriage; there· fore, Bob Jones is not charitable

~-

m thl' Ulll\'ersi1)"s life. Neurly hnlf of rel1' 01'011 IDll."t .u1'<•l<I to or tllf lit 11d~nts lift' sl\ld)'ing ror the ..., .. .J

mm1stT)' Or rreparing lO teach in 8 bUfCaUCffit iC l'lmstum 51.:hools. £\'er)' teacher · · · mu .. t hl' a born·ogain Cbrislian who dctcm~jl\ation of 'public must tc~11l)' to at least one su\'ing ex· polirfos.t'.. ';,\~.· ·' . pcricnl·e with Jesus Christ. Prayer ls a cu:mnuing occupation. Worldly amu~~ments are prohibited, lnclud· ing \lancing. use of tobacco, rno\·iegoini.: and hstentng to jon or rock PIU"I\ •

.. ThL', t•ourtb U.S. Circuit Court of

J\Pl"'"ls did not d1s1iute o trial courl'l> hndu1g that •A 11rimnry hm· daml•ntahst conviction (of the uni· vcr~ltY) IS lhut lhr Scril'IUres forbid mkl rnl·1nl dating and mnnioge . . .. 1'hcs\? bL'hefs, supponed by the umvrrsnr·~ interprclnllon of the Bi· blc. •are genuine religious beliefs.~

Hurt Of The Maner N.w.· we come to the heart of the

m11thr Is such a religious instltu· ttun. hnldmg sucb beliefs, a reli· g\Clt1l> 111stitution undt?r the 1'ox Cvlk: Tile IRS S&ys it 1s not. TJ1e gov·

. t'rlllll\'111':; ro:;ition is that unll''iS Bob JPt.t•s ll m \'t:rMty for molly n.•· noum·e!- lht•se ·genuine religious he· ht:!~" and atiolishcs its d1.X:trin11l tl0-ssuo11 011 interr11ci11l marnage, the u111\·t·rs1ty cannot quulify ror lox ex· emp11011.

Fur the university, the i~suc is

'·

ibility, the contrihu!lono; on which the university dl'Jll'llds would be keenly nffl·l·tcd. '011 will surmise corfl•rrly that Bob J1111cs rl·cetvcs no thrcrt federal aid of any sort.

Rut lht! lss\ll' nnw !wing urged upon the U.S. ~11pn·mt· Court has lrnplicntions thnt tt·arh liir hl'}'ond thb l11nd11mrr1lnh..,t n1111p11~ it1 South Carolina. lm11hdt ih lhc l(o\'crn· Ull nrs poslthm is tht• :~nwrnmeut's 11owcr to nhridgt· tht' I 11·1•11· •m ol rcli· g1un. In his 11l'l1t11:1i lot Supreme

" and docs not qualify . . This ls h\credible. The govern· ment ts contending, in effect, that the First Amendment's guarantee of freedom of religion must yield to a bureaucratic determination of ·public policies.~ Churches and religious schools must conform to IRS decrees or face the punitive consequences. An Orrhodox Jewish school, by ex· tension, would have to recruit stu· dents and employ staff solely on r• cial criterln; How can this be?

It probably will be October before . the Supreme Court announces

whether It wUI hear the university's · appeal from the adverse ruling in

the circuit court below. Meanwhile, perhaps Congress can be alerted to the whole affair, Mr. Reagan's pend· tng tax bill h11s something for every· one. It would be a blow for liberty if the bill were amended to provide something for fundamentalists who believe unpopular beliefs .

.. . ...

. ___ .. _.. __ ,_ ... -····-. :_ ···-- ---- --·------------··-··- ···- .. - .... - -·-- __ _. . - -·--- ·--

'·· \ ~

~@<·~.··. . - -'. '·•.. . :

Dc1>artmc11t of tlu• Trl.'nsur$ \l·asJ1iru?ton, l>.C. 20220

.. ·····

Date: JUL 1 1$81 .

To: Joh~ E. Cho~~ton Ass1stca11t St>~rt:-tary (Tox P"-'l it.:}')

Su 1>.it•t•t: Pr iv a tt s~hvol ~

Thi=> rE::>~onds br it: fly to )'o"ur memorandum of JuriE:: 26, 1961 (attached). As to whether the segregated status of a ~rivatE: school (as well as similar public policy, non-t~~ question&) may b~ decided by an agency other than the IRS, th~ followin~ ~ossibilities ma} be ex~lored:

1. The Cod~ could provide for a certification .... ruct:dur~ ur.a~r which the det~rmination (~, of se~regated status) would be made by the a~~ro~riate office ir. Govt:rr.n.ent and the r.:sult ct:rtified to the· Service, which would acccf-t that certification as conclusive f;:.·· tax ~ur~o~~£. Thus, the Code could provide that a scho~l would not bt- denied ext::m~tion (or be an ineligible reci~i~nt or charitable contributions) by rE:ason of eiscri~ination, unless it is certified as discriminatory by th~ a~Fro~riate agency. The apfropriate agency "'ould be that agt:ncy charged with developing civil rights policy gt:nerolly, or with res~ect ~o education specifically, such os the Civil Rights Division or the Justice De~artment, the U.S. Co~ffiission on Civil Rights, or the Office of Civil Rights in the Dt:partment of Education.

Ct::rtification i;.roc4;:dures are not u11con1mon in the Coo~. Fur exgm~le, whether a building qualifies for the special tax bt:11t:f its accorded historic structures d~pends u~on a c~rtification by the Department of the Interior (section 191)1 tht: eli~itility of an employee for purposes of th~ ~m~loyer's targett:d jots credit is ~ad~ p~rsuant to a certific.btivn by tht: Stott £rt,Floyment Sel: 1•rity Agency (section 51(6)(12), as imFleniented by th· Service and the Dei.-ar tn;t:nt of Le:sbor) 1 and whether a pollution control

Buy U.S. Sa11ings Bonds Rtgularly on the r., . .'roll Sa11ings Plwn

..

-~ . . ·'·-- ~·-----· ------·--·--.·-· -

-2-

facility qualifies for 60 month amortization depends upon a certification by a state authority to either the Department of the Interior, or of Heal th and Human Services, which' in turn certifies th~ facility to Treasury (section 169(d)) •

. (I suspect that there are- other examE'les in the Code.)

Issues in th~ privbte schools area would include having thE ap~rofriat~ civil rights agency agree to assum~ jurisdiction, ~nd the pos&ibility of effectively including the investigation or pur~ly ~rivate schools into that agency's pc>l ic ies chlC E rogr on.s.

2. in conjunctio~ with, or an alternative to, agency certification, Congress ma~ provide that the issue will be determined by the courts. Thus, for ~xam~le, Congress could create a private right of action by certain plaintiffs (such as civil rights groups, on whom standing could be sp~cific~lly conferred) directly against an exe~ft school to challenge that school's exem~tion on discrin:ination grounds. Exerr.ption would depend on the outcome of that litigation. Oe novo ~roceedings could or could not b~ required for schools previously acjudicatec discriminatory in "non-tax" pro~e~din~s.

This alternative would raise a host of issues such as Congress' authority to confer st~nding, and its authority to limit judicial resolution to a case by case d~t~rmination.*/ Additional issu~s would include definin3 the clas& of plaintiffs so as to appropriat~ly limit a school's ex~osure to litiggtion, anc the charge that leaving enforceruent entirely or frimarily to the private sector is ah abdic~tiun of r~sponsbility by the Government.

*/In thi& connection it should bt noted that th~ Court of Appeals for the District of Columbia Circuit recently reversed tht District Court decision (Wright) which dismissed a suit seekin~ to ap~ly Green (the Mississip~i case) notionwid~.

.. ;

- -·- -·.\- ··- - --------··· 4 • ··-·----·-·--·-·-- -- ~. -

-3-

l do not thi11k that there are ony other in1:>tance& in the Code where a d~tern.ination for tax ~urfoses is made solely by reference to litigation in which the servic~ is not a party. We could investi~at~, ho~ever, whether oth~r statutes (.!.:..9.:., environmental laws) d~pt:md primarily on private sector li.tigation for epforcen1ent.

Please advise if you would like these alternative~ pursued furth~r and/or additional alt~rnativ~s dev~loped.

Attachment

. . " . Department of the Treasury· l\ashington, D.C. 20220

MEMORANDUAI To:

Front:

Subject:

Mark Yecies Attorney-Advisor

John E. Chapoton ~· Assistant Secret~ry (Tax Policy) u Private Schools

The private school situation is now being handled by IRS in consultation with the Justice Department.

I still need to get back to the Secretary and the Commissioner on whether it might be feasible to have the question of whether a private school is segregated, as well as other similar public policy, non-tax questions, decided by some agency other than IRS with the tax effects flowir19 automatically from the decision of that other body. I want to get IRS out of this judgmental area that is unrelated to tax collection.

Could you make some suggestions? At this point, we do not of course need anything very definitive -just some possibilities.

(TD f 10·01.8 (IJ·7tl))

.AlE~lORAl\rDVAl 'fo: David G. G~ickrnen

De~uty Assistont Secretary (Tax Policy)

From:MC;.rk L. Yeci~s ,..\~\ Attorney-Advisor~'

Subject: Pr ivat~ Schools -- Cur rt:nt Status

Dut<!: JUN 2 1981

Per your request, this will sumrr.arize the current status of the private schools' issue.

l. Litigotion. In a significant development, the District Court granted the intervention motion made by certain church-related schools.~/ In response, the Service is prt:sently preparing n.ater ials to subrni t to the court on this issu~. These materials will inform the court of the problems encountered with church-related schools and will ask for guidance. You may recall thQt certain church-related schools have resisted sup~lying the Service with the information required by the injunction anc that the Service has contemplatec summons enforcen.ent proceedings.

2. Ad~inistrative Proceedings. In the court-mandated review of the Mississippi schools, seven were identified by the Service as s~-called "paragraph (l)" schools (i.e., schools adjudicated discriminatory or formed or expanded at the time ot comn1unity desegregation). Of these, revocation of exemption has been proposed for four (I believe}. These proposed revocations are in various stages of administrative review; to date no schools' exemption has been revoked.

*/The court denied a request to intervene made by certain Congressn1en, incl .. ;ding Senator Helms and Representative Lott.

Buy U. S Savings Bonds Rtgularl)' on thr Payroll Savings Plan

TD F 80· 02.1 Repltces TD F 10 • 01.8 which M1Y be ulld

-2-

3. ~evenuc Procedures. A set of proposals, which presents a range of options, has been drafted by Chief

·counsel and the Exempt ·organizations Division and sent to the Commissioner for review. I suspect that these proposals will be forwarded for policy conunittee consideration.

Please advise if you would lik~ any further information.

cc: Mr. McKee

~ --· ~·· ,. ---·· ._,._,..... . -- ...... ____ .... _ .. ____ ,. ___ .. ·. ---.-:-. -·---··--·· - . - . - - . , • -· •"• ·••U· •- • ••-

81-5259 TRE'rt LOTT

9nt Dis~ .~HIUll'PI l.tOO .. , .... - ........

WAin•-· D.C:. IOlll aoz.us-1n1

l

r l .....

REPU8L H WHIP -.. - -·- €ongress of t~t ltnitcb 6tates

J1ou~e of ~tprr•entatibtd IUasJJfn;fon, D.C. 20515

~ ............... _ •NISTltATIVI: ASSISTANI'

H. ANDERSON. .IL

... ...._ M,.,..._, Maaa1u- ----....._ ............... -

April 7. 1981

The Honorable John Murray Acting Assistant Attorney General Tax Division United States Department of Justice 10th and Constitution Avenue Washington. D.C. 20530

Dear Mr. Acting Assistant Attorney General:

I want to take this opportunity to thank you for taking the time to me~t with our delegation yesterday regarding the case of Green v. Miller. I especially appreciate your pointing

,out possible courses of action available to the schools in question. While your cont~ntion that the district court here in Washington is an inhospitable forum is well taken, my co~stituents may be excused for thinking that the government's litigation strategy so far has done little to advance their interests or to inhibit the plaintiffs.

I am more inclined to believe that the schools and their attorneys are the best judges of their own litigation strategy, and I find the government's failure to cooperate highly unsatisfactory. The failure to keep the plaintiffs out of court should logically result not in a separate effort to keep the adverse parties out of court, but in an effort to permit all interested parties to present their cases. I see little likelihood that the government's belated shift to· a position of neutrality will achieve the result desired by the schools.

For that reason, I put to you, as the government's chief litigating officer in this case, a simple question:

---

Will you file briefs on behalf of the Service in the appropriate courts in support of the intervention efforts by the Jackson, Hattiesburg, and Clarksdale schools?

You should know that I have determined, as of this juncture, that I am obligated to do everything in my power to help my consituents obtain a proper judicial resolution of the issues presented by this case. I have therefore agreed to join with other members of Congress to seek intervention in the Green case to request enforcement of the funding restrictions embodied in the Ashbrook and Dornan amendments.

l.

(

• ····-··-····-·-.. --·-----·-·····-···· - # •

• . '

. - \ . Page 2

The attorney in charge advises me that he plans to file that action along with the Clarksdale motion for intervention on Monday, April 13. .·

I will therefore appreciate your answer to my question at the earliest possible moment, in no case later than the -close of business on Thursday, April 9.

With kind regards and best wishes, I am

Sincerely yours,

· Trent Lott

TL/mbw cc: The Honorable Ronald Reagan

1 The Honorable William French Smith The Honorable Donald Regan The Honorable Roscoe Egger

..

,,

Date: April 3, 1981

MEMORANDUM FOR: Roscoe Egger, Commissioner (IRS) John Chapoton, Assistant Secretary (X)

From: Dennis Th~ Assistant~~ary (L)

·.

Subject: Meeting with Mississippi Congressional Delegation

Time and Date: 10:00 a.m. Monday, April 6

Place: . Senator Thad Cochran's Office 328 Russell Senate Off ice Building

Purpose: Tax Exempt Status of Private and Religious Schools in Mississippi.

Principals: Roscoe Egger John Chapoton Senator Thad Cochran (R-Ms.) Senator John Stennis CD-Ms.) Representative Jamie Whitten (D-Ms.) Representative David Bowen (D-Ms.) Representative ,G.V. (Sonny) Montgomery (D-Ms.) Representative Trent Lott (R-M~.) Representative Jon Hinson (R-Ms.)

Participants:

Initiator

Surname

John Murray, Acting Assistant Attorney General, Tax Division, Department of Justice

Stan Koppelman, Special Assistant to the Commissioner

Al Winborne, Assistant Commissioner Employee Plans & Exempt Organizations

Howard Schoenfeld, Special Assistant to the Commissioner (EO)

Lester Stein, Assistant to IRS Chief Counsel Rick Prendergast, Treasury, Legislative Affairs

Reviewer Reviewer Reviewer Reviewer Ex. Sec.

Prendergas -L

lnitia Is Date 7'"--, i;1 4/3 . ,,. 4/3

Form OS·3129 Department of Tr111ury

-2-

•

Biographies on the Mississippi Congressional Delegation are attached. ..--

Attachments

cc: Dennis Thomas Bruce Thompson Rick Prendergast Bill DeReuter Kathy Makris

John Murray Stan Koppelman Al Winf orne Howard Schoenfeld Lester Stein

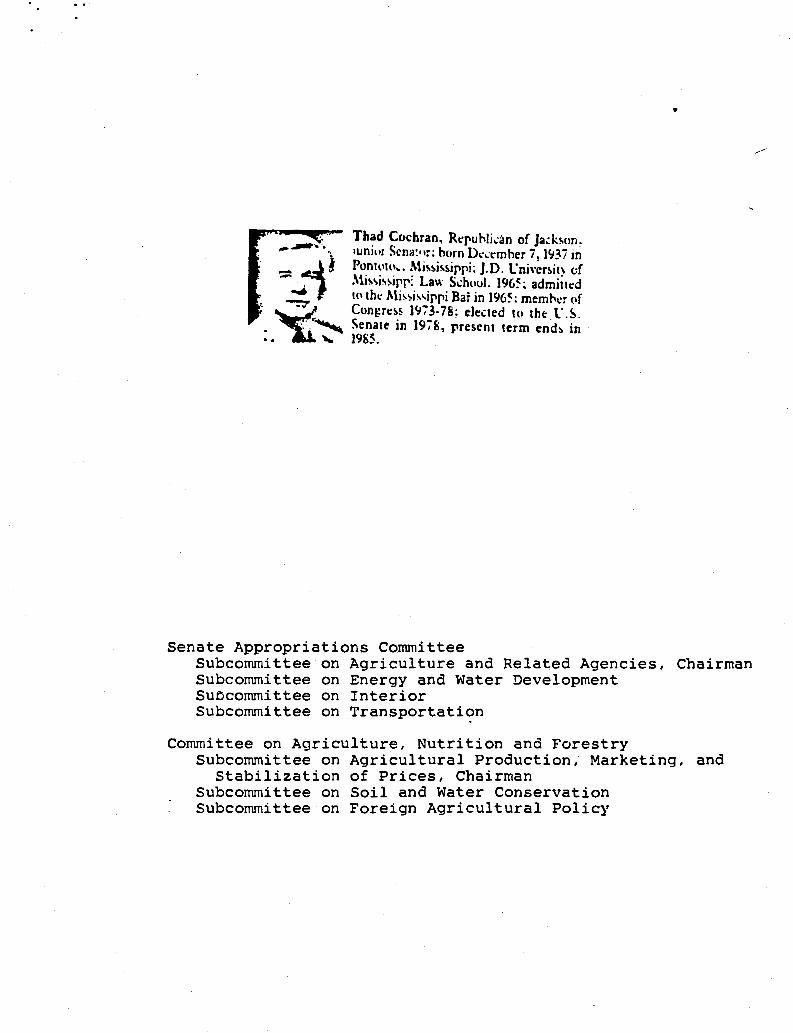

Thad Cochran, Rt'ruhli..:an of Ja.:k!.on. •uni"r Scna:11r: horn D.:'"·t'mher i. J'l3i in Ponllllo ... .\fo~i"~ippi: J.D. l"nh·~r~it\ <;f .\fo,i,~irr: Law Si:hool. 196~ ~ admiirt'd Ill the i\fo":>i.,,ippi Bar in 196~; memhi:r of Congn:~~ 1973-78; elected to tht l".~. Senate in 197fi, present term end!> in 1985.

Senate Appropriations Committee

•

Subcommittee on Agriculture and Related Agencies, Chairman Subcommittee on Energy and Water Development suocommittee on Interior Subcommittee on Transportation

Committee on Agriculture, Nutrition and Forestry Subcommittee on Agricultural Production, Marketing, and

Stabilization of Prices, Chairman Subcommittee on Soil and Water Conservation Subcommittee on Foreign Agricultural Policy

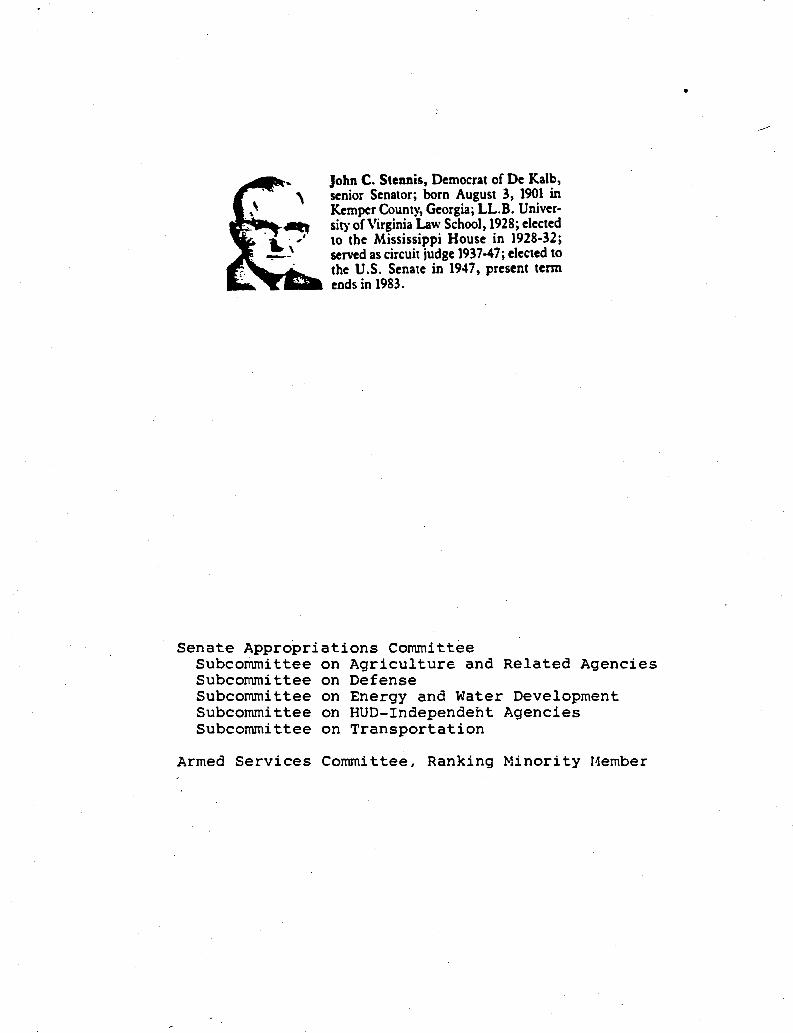

John C. Stennis, Democrat of De Kalb, senior Senator; born August 3, 1901 in Kemper County, Georgia; LL.B. University of Virginia Law School, 1928; elected to the Mississippi House in 1928-32; served as circuit judge 1937-47; elected to the U.S. Senate in 1947, present term ends in 1983.

Senate Appropriations Committee Subcommittee on Agriculture and Related Agencies Subcommittee on Defense Subcommittee on Energy and Water Development Subcommittee on HUD-Independent Agencies Subcommittee on Transportation

Armed Services Committee, Ranking Minority Member

•

•

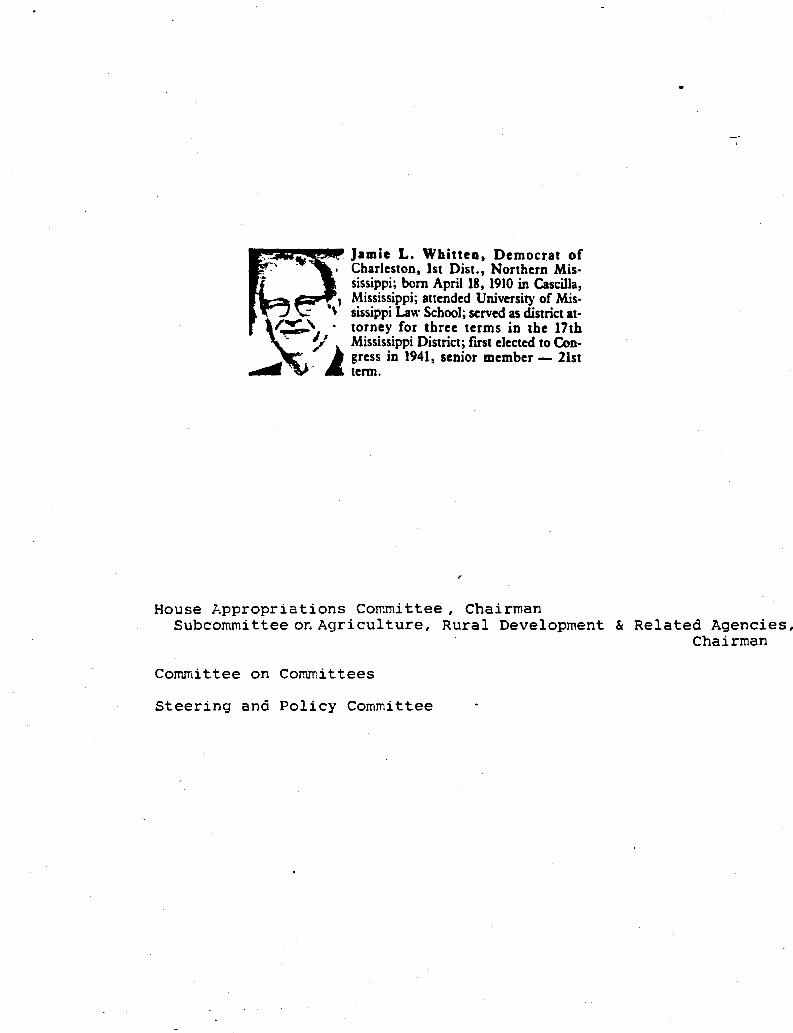

House hppropriations Committee, Chairman Subcommittee or, Agriculture, Rural Development & Related Agencies,

Chairman

Co~~ittee on Committees

Steering and Policy Committee

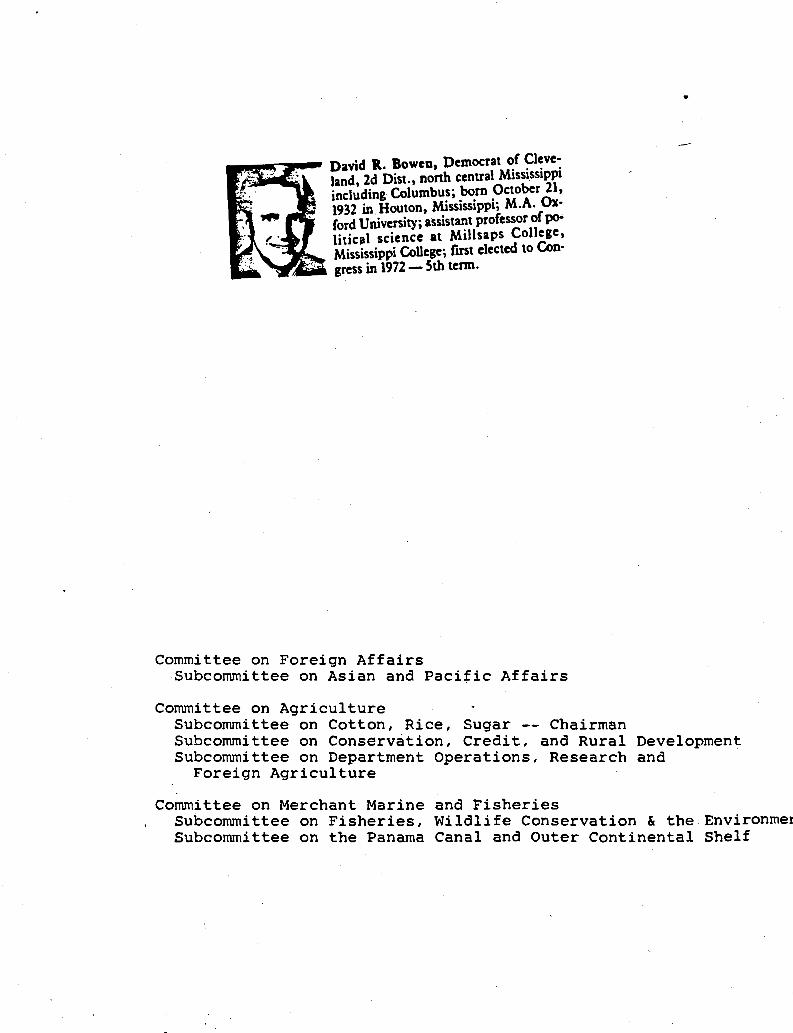

-IJlll!l!•~i..-• David Jl, Bowen, Democrat o_f ~l~ve: land, 2d Dist., nonh central Miss1ss1pp1 including Columbu~; ~rn .October 21, 1932 in. Houton, Miss1ss1pp1; M.A. Ox· ford University; assistant professor of political science at Millsaps College, Mississippi College; first elected to Con

~.-,&~ gress in 1972 - Sth term.

Committee on Foreign Affairs Subcommittee on Asian and Pacific Affairs

Committee on Agriculture

•

Subcommittee on Cotton, Rice, Sugar -- Chairman Subcommittee on Conservation, Credit, and Rural Development Subcommittee on Department Operations, Research and

Foreign Agriculture

Committee on Merchant Marine and Fisheries Subcommittee on Fisheries, Wildlife Conservation & the Environme~ Subcommittee on the Panama Canal and Outer Continental Shelf

I

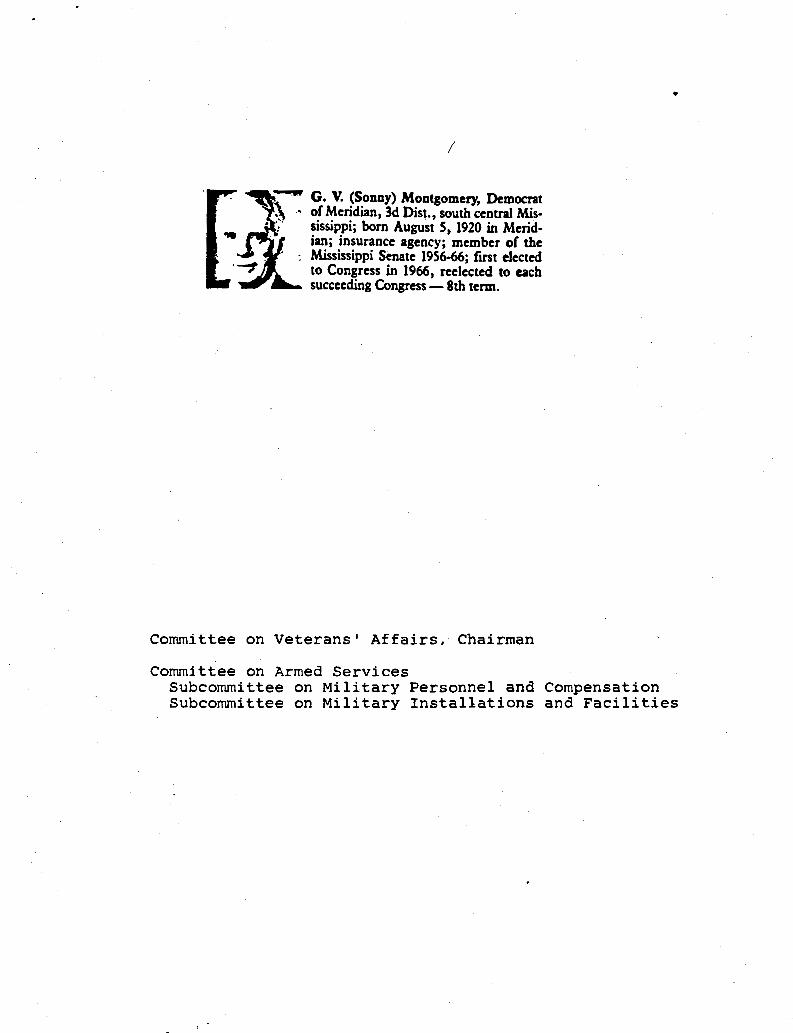

G. V. (Sonny) Montgomery, Democrat of Meridian, 3d Dist., south central Mississippi; born August S, 1920 in Meridian; insurance agency; member of the Mississippi Senate 1956-66; fU'St elected to Congress in 1966, reelected to each succeeding Congress - 8th term.

Committee on Veterans' Affairs, Chairman

Committee on Armed Services

•

Subcommittee on Military Personnel and Compensation Subcommittee on Military Installations and Facilities

Minority Whip

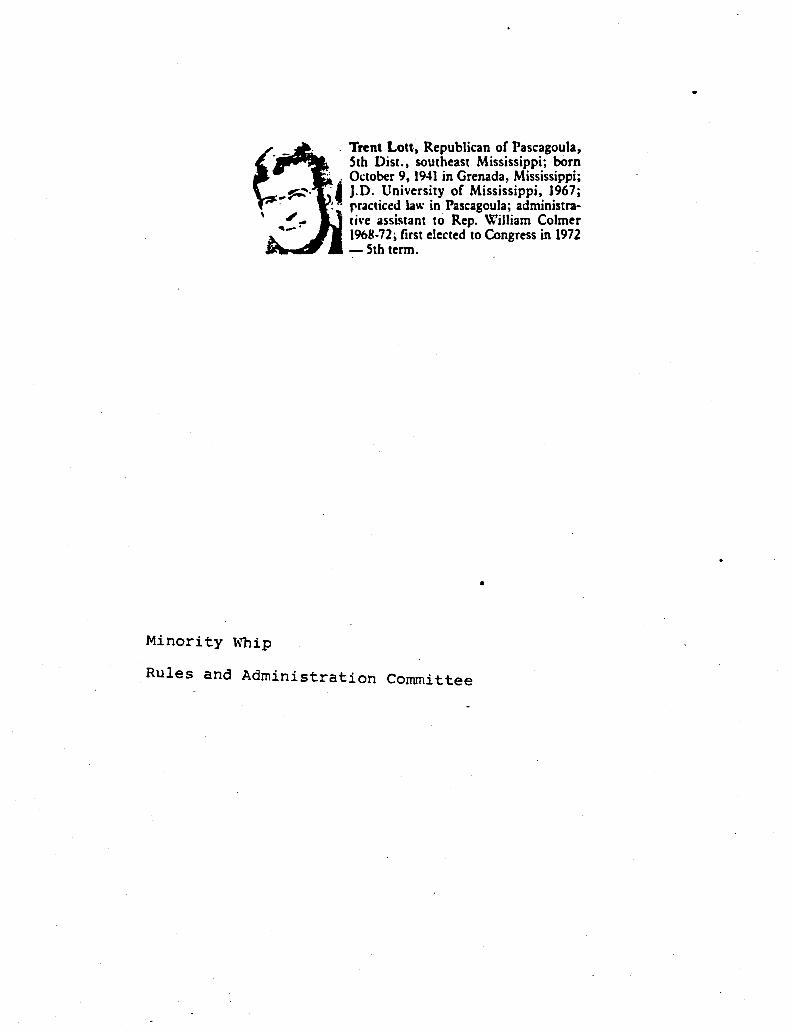

. Trent Lott~ Republican of Pascagoula, Sth Dist., southeast Mississippi; born

·' . October 9, 1941 in Grenada, Mississippi; · f. J.D. University of Mississippi, 1967; ! · rracticed law in Pascagoula; administra

ti\'e assistant to Rep. "'illiam Colmer 1%8-72; first elected to Congress in 1972 -Sth term.

•

Rules and Administration Committee

•

-~~ ... " .

'

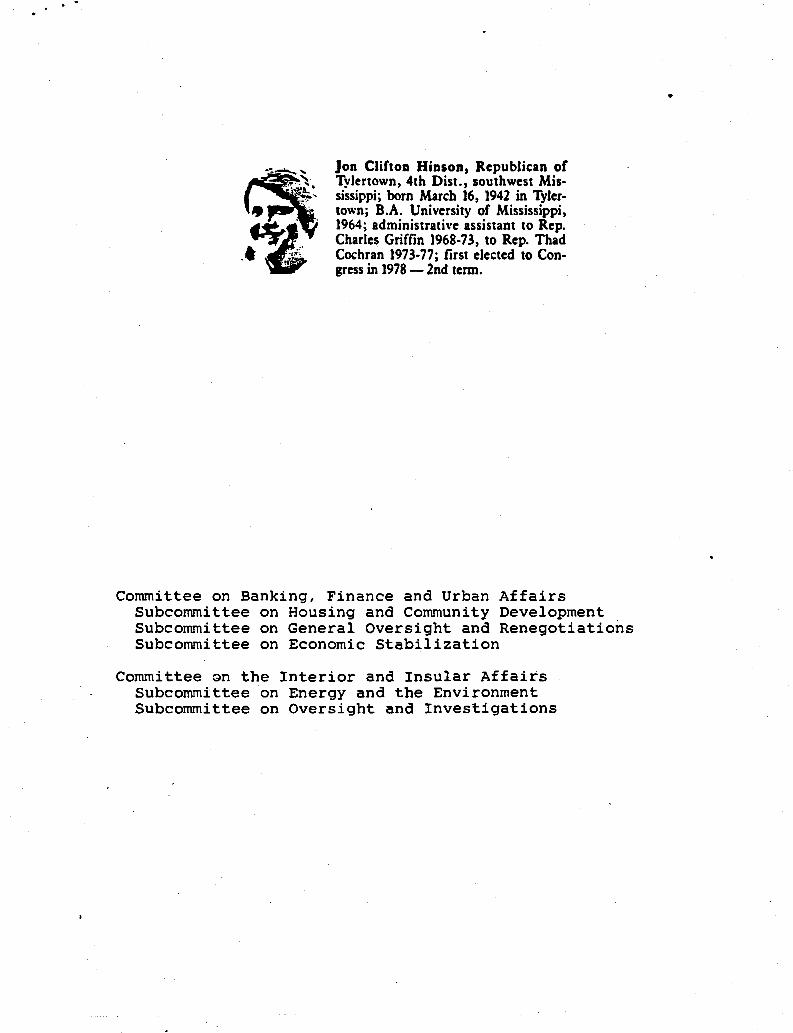

. :v Jon Clifton Hinson, Republican of Tylertown, 4th Dist., southwest Mississippi; born March 16, 1942 in Tylertown; B.A. University of Mississippi, 1964; administrative assistant to Rep . Charles Griffin 1968-73, to Rep. Thad Cochran 1973-77; first elected to Congress in 1978 - 2nd term.

Committee on Banking, Finance and Urban Affairs Subcommittee on Housing and Community Development Subcommittee on General oversight and Renegotiations Subcommittee on Economic Stabilization

Committee Gn the Interior and Insular Affairs Subcommittee on Energy and the Environment Subcommittee on Oversight and Investigations

•

D<!rmrtm<.»nt of t1w Trccumr)' \\·osJlin6?ton, l>.C. 20JJO

To: Juhn E. Chap1..•tun Assistant Secretary (Tax Pulicy)

From: Mark L. Yeci~s \\ \. \ Atturney-Adv1sur

J)atc: ,, r:. t" 2 I·., . \ •

Sul>.il'l'f: Private Schuuls -- "1eeting with Mississippi !'elegatiuni Respunse tu _Letter tu Secretary

As yuu may recall, by l tter tu Secretary Regan uf January 26, 1981 (attached), the Mississippi Cungressiunal delegatiun has requestea a meeting tu discuss the private schuuls issue. I understan~ that a meeting has tentatively been schedulea fur Munday, April 6, 1981, at 10:00 a.m. in Senatur Cuchran's uffice (328 Russell Buil~ing). Attending will be yuurself, the Cummissiuner, a representative (yet undetermined) frum the Justice Department, ana staff.

~hile staffers uf the ~ississippi delegatiun had been pressuring us (prirnarilt Rick Prendergast uf Legislative Affairs) fur this meeting, the scheduling uf the meeting has taken the heat uff. Additiunally, while there is less pressure tu respund in writing tu the incoming letter, I believe that a pulite response uver the Secretary's signature wuuld still be ap~rupriate. ~ttachec fur yuur revie~ is a craft respunse.

If the draft is acceptable, please advise an~ I will have letters tu each member uf the delegatiun prepared in final.

Attachments

cc: David t-lickman

TD F 10· 02.1

Wi 11 ia;i1 McKee Rick Ptendergast Stanley Kuppelmarr

Buy U.S. Savings Bonds Rtgularly on the Payroll Savings Pl.Jn

R1Dlec11 TD F 10 · 01 .8 which mey be ueed

1981

\

. . . . .,. -• •

Department. of the Treaaur, \\·aahintton, D.C. 20220

JfEJIORAl\'DVAI J>ote: February 26, 1981

Tu:

From:

Subjecat:

John E. Chapoton Assistant Secretary - Designate (Tax Policy)

~~'-~> TheodOf.e -s. ::>ims Attorney-Advisor·

The attached letter to the Secretary from the Mississippi Congressional Delegation

Congress, by riders to the most recent Treasury appropriations bill, bas prohibited the Internal Revenue Service from implementing a Revenue Procedure originally proposed in 1979 under which the tax exempt status of a number of private schools country-wide would have been reexamined. Despite the appropriations riders the Service is now under an injunctive order issued by the United States District Court for the District of Columbia requiring it to review the exemptions of .a numb~r of Mississippi schools.

The Mississippi letter deals with steps initiated by the Service in response to that order. The letter argues that the litigation that led to the District Court order was · essentially collusive, that it did not give the adversely affected schools an opportunity to be heard, and that in light of the appropriations riders the Treasury therefore should reconsider its willingness to proceed in compliance with the order.

I discussed 'this letter with Bill DeReuter of Legislative Affairs, who has advised me that the Mississippi delegation was pressing for a meeting promptly on this matter. Initially, I informed Mr. DeReuter that, in view of the visibility and senstivity of the issue, it might be imprudent for the Treasury to meet with the Mississippi delegation without participation by appropriate officials of the Service as we)l as of the Justice Department. Thereafter I ascertained fr~,m Stan Koppelman of the Commissioner• s office that this issue already has been raised with the Commissioner by Orie of the signatories to the letter (Lott). Evidently the Commissioner or his off ice has indicated to the Bill that there are a number of procedural steps that would

B11y V.S. Snings Bonds R~p/11rly on ib~ P11yroll Softngs Pion

TD F 10·02.1 ._,_ TD F tD • Dt • whid\ 111W - ulld

• • • .. . ,.

-2-

have to be taken before any school's exemption might actually be revoked, that such procedures will take time, and that the Commissioner is willing to brief interested Congressional officials after he has been confirmed.

In light of those discussions I asked Mr. DeReuter if he would ascertain from those on the Bill with whom he has been discussing this issue whether, in light of the probable delay before any school's exemption is revoked, they too would be willing to wait until yoo, the Commissioner and the appropriate Justice Department official (I am not certain whether it would be the head of the Civil Rights Division or the Tax Division) have been confirmed. Mr. DeReuter advised me.that this appears to be agreeable to those with whom he has been in contac~.

cc: Mr. McKee Mr. DeReuter Mr. Koppelman Ms. Goodman Mr. Yecies Ms. France ,

'·' . "' . lnten1al Revenue Service memorandum

Hren'· ;, ~ C' ~ • ·~ ~ ~~ 1

'. t. ' • . .

•

date: MM I 3 1111. l ".. :. f ~ t to: s. Allen WinJ:X>me .. .. .

: "' I .•. • •

from:

subject:

;

•

0 tUi f.,, I~ ,\ ; I l; ~1 S

Private Schools .

To the extent the Service can 't'Dtl ~ its optiCl'lS in this area with reqard to possible ncdification of the proposed revenue ptoeedure so ~ to achieve unifo:cm natiCJ'JWide admi.nistratim, I offer for a:m-sideratie11 ·the s~ticn set forth below dealing with hew the Seivice might go about enforcing the racial nondiscrirninatiCl'l requiranent.

~ primary su;JgeStioo is that the Service retOVe the "net" threatening mst schools. Sirrply, we ~d el:ilninate the cxmcept of a reviewable i: bx>l. I recumend that arrt further revised revenue procedure merely set

. c.ut private school au:li t procedures and guidelines that revenue agents would fellow on a case-by-case basis. ·

This further revised revenue procedure o::>uld still foll<::h.• the essence of the February 1979 procedure along with certain other m:xlifications. The thrust of the procedure would be to establish appropriate guidelines for agents to follc:M during the ~tion of a private school. 'lbese instructions would make clear that.an inference of racial discrimination can be drawn trilen the specific facts and cirClmStances of an individual case warrant it and that the standards foUCMed in Federal Court decisions such as N:>rwood and Brunfield wculd be applicable. However, the burden would be on the agent to develop and establish a prima facie case of intentional racial discrimination. Su::h a case o::>uld be established only where the agent cnild dsronstrate in aco::>rdanoe with existing Federal decisions that there was a relationship in fact bebo1een the fomation or expansion of the school and plblic sdlool desegregation in the area. Where a pri.na facie case w::>Uld be established, every opportunity 1«:IU.ld be made available to a school to overa:ne aey inference that might arise.

'the advantages of this prqx:>Sal are that there waild be no nationwide SUI:Vey, canvass, or net cast upon all private scOOc>ls. 01.ly tlx>se sch:x>ls cmpl.ained about, rand::ml.y selecteq or ~e specific reasons for suspecting rt:DXJTplianoe existed waild be selected for exmninatie11. 'nlus, the basis for the peraµ.ved threat to nost private sch::ols would be ftltDVed and 6el'vice contacts ahoul.d be understocd to be made all.y ai a case-by-ease apprcadl.

'1be chief disadvantage is that a truly racially discriminatory school ccul d CCl'\tinue to go unchecked with regard to its cxrrplianoe with the racial

.. .. -···. ·--· .

/.

/ -2-

s. Allen Winborne

nondiscrimination requiranent until an actual aunt is made. '!he risk is greater as tc ·church-related schools which do mt arx1 are not required to have exatption letters. However, possibly inc::reased or expanded enforcement of the certification rules for church schx>ls could be established. Ol balance, and even without expanded enforcertent of the certification rules, I believe the advantages of eliminating the _CXJilcept of "reviewable" scla>ls oub11ei9h the disadwntages. '

~. ·' . . ~ -· .. '·. , .. -1-

J_..t..c(_ ~

h

J ~T. • pi? t ~·'Ur!"li1\P

Pirector of. r,!~gai. ar.d Legislative ~~rvices

P.O. !!ox -1097 Whittier, !"al!forn!a 90G07

I a~ replying to your letter of February ~7, 19~1 to ~orner-'"'cr>uty 1'.ssiota..11t C~cretary Halperin.

F:nclosec": is a copy of the eiscussion :!raft. that you rec:ucstc'..1.

f'!'lclosure

~ ..

X!.C

(::f)0T)P :~'I\.~.

::?/~: /~J

rincercly,

.. ~· ... ~-~vid r.haJ:ow

?'·eputy ~·e): L09islative Cow1sel

I I --

FEBRUARY 27, 1981

DANIEL I. HALPERIN DEPUTY ASSISTANT SECRETARY TAS POLICY DEPARTMENT OF THE TREASURY WASHINGTON, D. C. 20220

DEAR MR. HALPERIN:

SINCE OUR ORGANIZATION JS IN NO WAY CONNECTED WITH CAPE WE HAVE NOT BEEN ABLE TO GET ACCESS TO YOUR DISCUSSION PAPER JN WHICH THEY ARE URGING THAT IRS PUBLISH ONE OF ITS REVENUE RULINGS.

THE ASSOCIATION OF CHRISTIAN SCHOOLS INTERNATIONAL JS THE LARGEST CHRISTIAN SCHOOL ORGANIZATION IN THE NATION, THE MATTER DISCUSStD IN THIS PAPER JS OF GREAT IMPORTANCE TO US, WE WOULD APPRECIATE GETTING A COPY AS QUICKLY AS POSSIBLE,

THANK YOU FOR YOUR COOPERATION JN THIS MATTER,

SINCERELY,

ASSOCl~T~~_}'Of CHRISTIAN S~OOLS INTERNAITONAL

·ft« //(/l/l~p PAT MURPHY, DIRECTOR OF ~GAL AND LEGISALTIVE SERVICES

PM:PM

.• . . . .. Attachment 3

DISCUSSI~N PAPER

FACTS

In the si tu:itions describC'd below, the donee organization operates a private school and i~ an orsanization des~ribed in section 170lc) of the Internal Revenue Code. In c3ch situ~tion ~ taxpayer who is a pllrent of a child who attends the school ni.;l'.CS a p:lymcnt to th1.• organization. In each situation, .. 1'.: cost of educating a child in the school h not less th3n the payrncnts made by the parent to the organization.

LAW AND ANALYSIS

Section l 70(a) of the c,,dc p1.-oviiiei;, subject to certain Urnit3tions, for the allowance of a deJuction for charitable contributions or gifts to or for the use of organizations described in section 170(c), payment of which is made during the taxable year.

A contribution for purposes of section 170 of the Code is a voluntary trans• fer of money or property th.it is r.1ade wlth no expectation or procuring a ff.nan• cial benefit commensurate with the amount of the transfer. See section 1.170A•l (c)(S) of the Incor.e Tax Rcsul.:itio:lS and H.R. Rep. No. 133_7, -83d Cong., 2d Sess. A44 (1954). Tuition expenditures by a t.:ixpayer to an educ~tional institution are therefore not deductible as ch~r1t~ble contributions to the institution because they arie require<l p:'lp.icnts for which the taxpayer receives benefits presumabl~· equal in value to th<' amount paid. See Chllnning v. United St:ltes, 4 F. Supp. 33 (D. Mass.), nff 'd rcr curian 67 F.2d 98f, (1st Cir. 1933), S!!!• denied, 291 U.S. 685 (1934). Like11ise, pilyments made by a ta;)(payer on behalf of children attending parochi:ll or other chur·.:h•spi:>n$ored schools are not allowable deductions as contributiuns either to the school or to the religiou~ organization opu:·tinB the schc.,.,l if the p:-!}"mc1;ts nre: e&lrtnarkcd·for such children. Rev. Rul. !'>4-580, 19!'>4-2 C.B. 97. Hvwc·vcr, tt.c tact th:'lt the p:iyments are not earmarkf'd dot~ not nec:cr-::arily mc1:i th it the pJyments arc \!cductible. On the other hand, a ch.Jt'ital>l~ deduction !or ,, p:iyment to .:in orba11f:.ation that operates a school will not be deni~d solely because the payment ~as, to any substantial extent, nffsct by thL' fair n.nrket \'llluc of the services rernJered to the taxp:iyer in the nature of tuition.

(HC'TH:)

.:;. ___ .,,,_

Whether a trilnsf cr 0£ money by a parent to an organization that operates a school is a voluntary tran~f ~r that ls made with no expectation of obtaining a cotr.n~nsurate benefit depend~ upon ~hether a re~sonable person, taking all the !acts and circumstances of th~ case into account, would conclude that enroll· ment in the scho~l wa~ 1n no mnnner contingr.nt upon making the payment, that the payment wai: not m.ide pursuant to a plan (whether express or tmpl ied) to convert nondeductible tuition intc ch.:irit.1ble contributions, and that receipt of the bc:?efit was not otherwise dependent upon the makin~ of the payment.

In determining this issun, the presenc~ of one or more of the f ollo~ing factors crc~tes ~ presumption th~t the payment is not a charitable contribution: the e:dstence c-f u cont.ruct under which n taxp.:iyer agrees to make a "contribution" and "'hich contain:· provisio•.~ ensuring the ~dmission of the taxpayer's chilr'; a plan &.illowtnr t:1>'.pJyc-r~ either tu PiJY tuition o~ to tn.lkc "contributions'' in exch.:incc ·for schooling; the earul.lrkinr, of 11 contribution for the direct benefit of a part~cd .• r individu:il; or the otherwise-unexplained denial of admission or readmission to a school of children of taxpayers who are financially able, but who do not contributC'.

In oth<r c~~cs, a'though no ~in~le fa~tor m.iy be determinative, a combination of sever:il f~ctor~ may indicate that a pnyn~nt is not a charitable contribution. In these case>s 1 hcth cconorr.ic :ind noneconomic pressures pl.aced upon parents must be taken ir.to account. The f act,,ri. that the Service cirdinarily will look to inclu:ic, but arc not li!:iitcd to, the £ollowins: the ab~e>nce of a·significant tuitf~P char~e; sutstanlial or unu~ual pre~turc to contribute applied to parents of ~hildren attending 1 school; contributi~n appeals made as part of the admis• sions or enri:>llr .• cnt prciccss; the absenc~ of significant potential sources of revenue ior opcratin~ the school other th.1n contributions by parents of children attendin~ the r.~hool; ... nd other f.:ictors sucscsting that a contribution policy has been created as a me.ins oi &1voiding the clrnracterization of payments as tuition.

On the ctJ.cr bnd, if a c"r.itin3tion of such factors is not present, payments by a pArent will normilly const.itute deductible c~ntributions, even if the actual cost of educating the child exceeds lhc amount of any tuition charged for the child'::. cdl1: 'tion.

Situation 1

Organization J, ~hich opcr~tcs a priv~te t~honl, requests the taxp~yer to contribute $4·0~.)x for e.ich child c11rol led i:1 the schol)l. Parents who do n:-t make the $40Px cc.ntribution art" required t" pay $40l)X tuil.ion for each child enrolled in the school. Parcuti. who neither mDke th';° cont1·ihutio~ nor pay tui~ tion cannot e:nrol 1 their chi ldr,'n in the tel.col. The t;ixpaycr paid $400~ to !•

HOLDING

The taxp~jer is not entitled to a ch.:iritabl- contribution deduction for the payment to Org3niza·tion !• Because the tn~payer muse either ~ke the contribu• tion or pay the tuition ch.:irgc in order for hi~ or her child to attend J's school, admhsion is contin;:•·nt upon m.ildng n p3y111~11t etf $4no~. The t3Xp.lyer's payment is not vtil unl..:iry .:ind no deduc:tion b :ill owc-J.

(HOKE)

Situation 2

Organization!• which operates a priv~te school, solicits contributions trom par,nts of applicants for admission to the school during the period of the school's solicitation for enrollment of students or while the aprlicatlons are pending. The solicitation materiAls are part of the application materials or are otherwise in a f orin indicatin~ that parents of applicants have been singled out as a clas~ for solicitation. With the exception of a few parents, every parent who ls financially able makes a co11tribution or pledges to rn.ake a contri• bution to!• No tuition is charged. The taxr~yer paid $400~ to!• which amount was sugg~sted by !•

HOl.Dl~C

The taxpayer. i~ not entitled to a char·ttable contribution deduction for the payment to Org~niz~lion T. Because of the time and manner of the solicitation of contributions by !• a';d the fact that no tuition is charged, it is no.t reason• able to expect that u p~rcnt can obtAin the admission of his or her child to T's school \dthout milkinr, the suggested payr..ent. Under these circumstances, the - · payments made by th~ t~xp~ycr are in the n~ture of tuition, not voluntary contributions.

Situation 3

Organization !1_, which operates 1 private school, admits or readmits a significantly larger percentage of 3pplicants whose parents ho>ve made contributions to the organizat:~n than applicunts whose p~rcnts h~ve not made contributions. The taxpayc.:r pClid $400~ to Org;:inization .!!•

HOLDING

The taxp.1)•cr i·• not entitled to a charitable contribution deduction. The Service will ord!n&:1rily conclude that the parents of applicants are aware of the preference ~ivcn to applicants whose parents have made contributions. The Service will th~rcfore ordin~rily conclude th~t the parent could not reasonably expect to obt1in the admission of his or her child to the school without making the tr.ins!cr, reg1rdlcss of the m.inner or Umin~ of tht> solicitation by the or&aniz;ition. Tl1c Service wil 1 not so conclude, however, if the preference given to chil~ren of contributors i~ principally due tp some other reason.

Situ;lt:lon ~ .....

Orgar.:lzation 1• a society for rclisious instruction, has as its sole function the operation of a private ~~hool providing secular and religious education to the childr<:n of iu. M?mbcr~. No tuition is charged for &ittcnding the school, which is fu~ded through Y,'s gcner.Jl oper;1t1nc account. Contributions to the account are solicited from all society members, as well as from local churches and nonn:c.mbers. Perscms other th.in p;irc:wu of children attending the school ~o not contrib:JtE' &i ttiBlllf icant portion of the school's support. Funds norm.llly come lo 1 from p.Jrcnto: on ii r<'gul<lr, csL:1bli!>lu-d schedule. At times, parents are p~rsonally solicited by the school treasurer to contribute funds accordins to their financial ability. No student is refused admittance to the school becausP. of the failure of his or her parents to contribute to the school. The ta~payer p~id $400! t~ .Y•

(MORE) •

HOLDING

Under these circumst~nces, the Service will generAlly conclude that the payment is nondeductible. Unl~ss contributions from sources other than parents .~re of such magnitude that the &Ch()ol is not economically dependent upon parents• contributions, parents would ordinarily not be certain that the sehool could provide educoition~1l bcndits without their p.lymcnts. This conclusion ts further evidenced by the !act that p;ir,~nts contribute on a regular1 established schedule. In addition, the prus~urc plac~d on parents through the personal solicitation by th~ school tr<'.1:~urcr furthct· indic.1tes th.lt their p:iymcnts were not volunt;iry.

SituJtion 5

Orp. .• nizatfon ~ C'p1:r.1te!. :a priv.ltc ~chool that ch:irgcs :i tuition of $300~ per stu1.font. 111 .1dolti1l11, it i:.olicit.• contril.>utions from parents or students during perfods othc-r th:'lr the p~rlod o! the school's solicitation for student enroll menu or the period •f:cn applf cations to the school are pending. Solici• tation materials indicate thnt parents of students have ~een sin&led out as a class for solicitation ~nd the solicit:ition materials include a report of the organization's cost per ~tudent to op~ral<' the school. Susgested amounts of contributions based on .in individucll 's Ability to pay are provided. No unusual pressure to cont~ihutc i~ placed upon individuals with children in the school, and many parf':1ts do not contribute!. ln aduition,. the organization receives contributions trom rr .. .my former stutlents, parents of· former students, and others. T11e ta~pay~r paid $100~ tc Org~nization ~ in addition to the tuition payment.

HOLDING

Undr.r thc.;;c- circumst;mces, the Service will i~ner:illy conclude thnt the taxpayer is entit I cd t<., c:l'1im n ch.lritable contribution deduction of $100~. Because a charlt.:iblc org:miz.:ition norm.illy solicits those knO'-"Tl to have the greatest interest in the organiz.ltion, the fact that parent!= are singled out for a solicitation will not in it~elf create an inference that future admission or any other b~ncfits depend on a contribution from the parent.

Situatirn 6

Church ! C\penit.•::• aJ ~chool providint. SL·cular and relisious education that is attcnd1.:d both ~)' c-hildrcn of parent.s who arc mc:mben of ! and by children of nonmembers. Church ! rc~eivcs contributions from all. o! its m~mbers, which are placed in its £.'·nenl 01,c1l'lting fund and ~re expended when needed to support all chu:ch activitic-s, ll tubc;tantial port.ic'n of which are unrl'l~ted to the school. Most snembc-rs of Church! do not have children in tht: school, and a major portion of Church ~·<; expcm~<'·· .-ire attributable to its nonschool functions. The methods of soliciting contrl.1.Juti1in~ to Church! from church 1nemhers "ith children in the school art- t;ht san11: as the.: 1n1.:thvcls o! so lie iting contributians from mc."llbers without childn n in the sehool. Clwrch X has full control OVt'l" th~ use of the contri• butions that it rccciv1..·~. McmbL·rs who l1avc.- children enrolled in th.:? school arc not required to pay tuition for their chilJrcn, but tuition is charged for the children of 1101"'.znemh·~r~. T:lxpayc?r, cl me:nber of Church X whose child attends Ch•Jrc:h !'~ schoe>l,contribut.cd $:Or~ 10 Cliurch ! during the ye-Sr for it: general purpoc;cl>.

HOLDING

The s~rvir~ will ordinarily conclude that the taxpayer is allowed a charitable contribution deduc tiun of $20<.>is,. Because the facts indicate that the school i.s supported by the> church, that most c&>ntributorr; to the church are not parents of chUdrf'n enroll cd in the school, and that contributions frDlll parent members are solicited in the smn~ Dl3nn~r as contributions from other members, the taxpayer's cC'ntributions "'·U 1 b" considcr"·d charitable contributions, and not payments of tuition, unlei:;s t.11\ re- h ,;howir.l; that the contributions by members with childr('n iT'I the sc; . ..> • ..;l ar(• sisnificantly larger than those c,,f other m~mbers. The absence of a tuition charge is not det~rminative in view of th~se facts.

EFF~CT ON OTHER DOCUMENTS

The facts in Situation 4 are essentially the. same as in the case of Oppewal v• Canrnissioner, 468 F. 2d 1000 (1st Cir, 1972), on which Rev, Rul, 79-99 was based, Certain facts were not stated in that ruling, First, the •ole function of the or~anizatio11 wils the operntfon of a school, Second, there was an absence of significant potential sources of revenue for oper~ting the school other than contributions by parents. Third, funds normally came to the organization on a regular, established schedule. Fourth, when solicitations were made, parents were solicited on a pcrson~l basis by the school treasurer. Rev. Rule 79-99, 1979·1 CeBe 108, is hereby superseded,