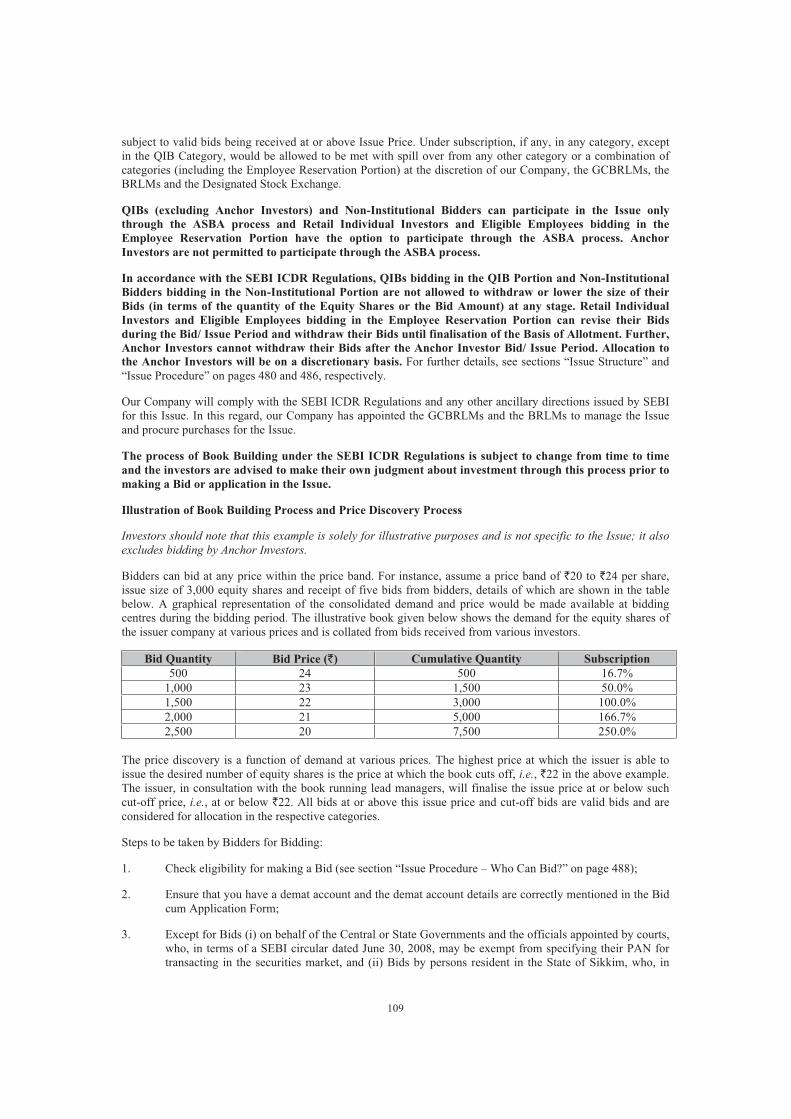

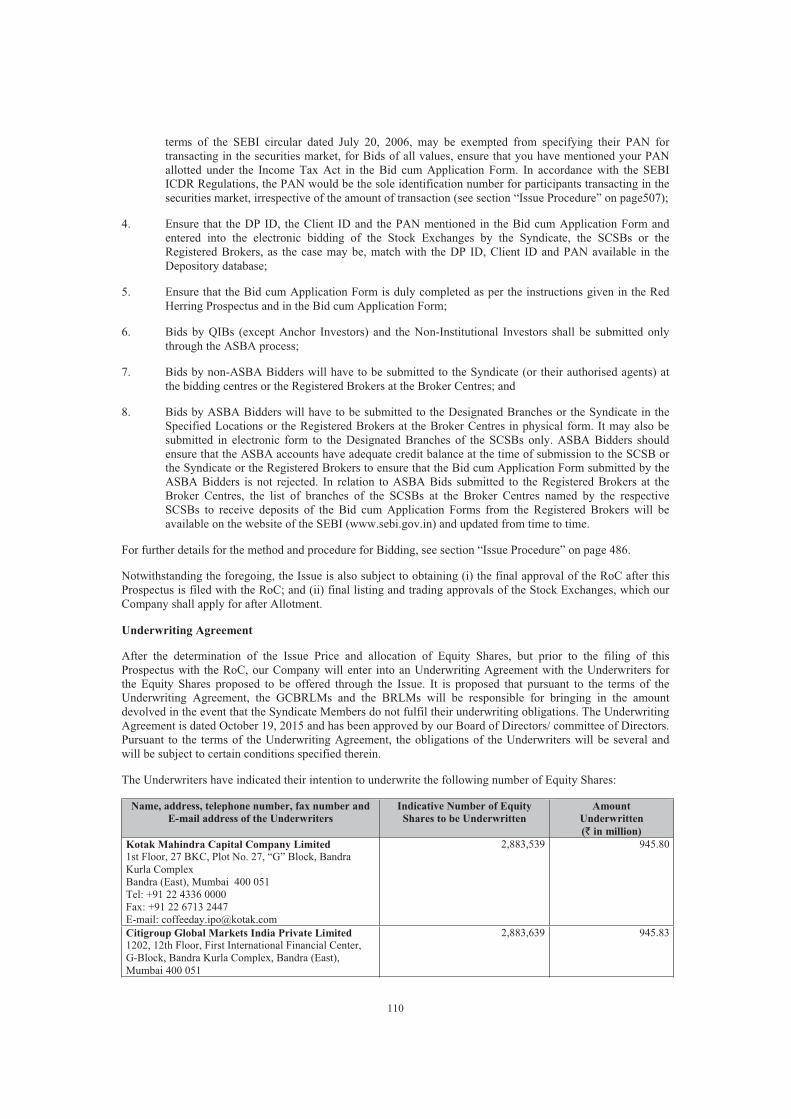

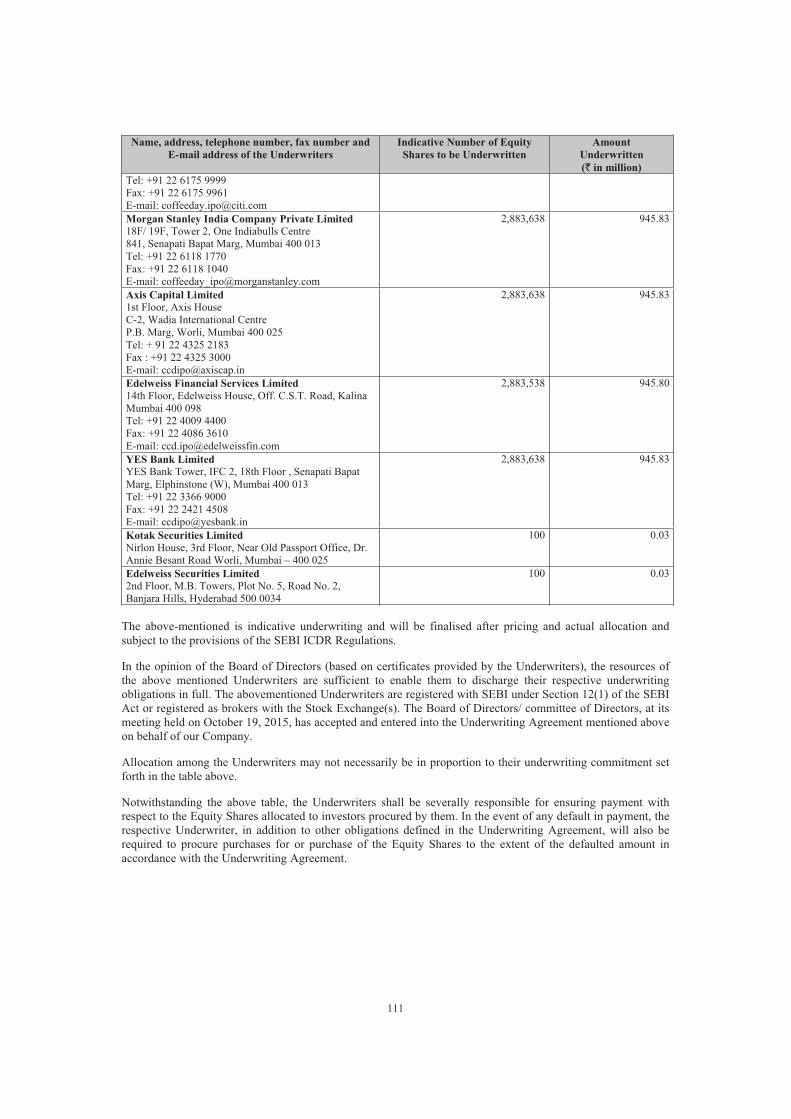

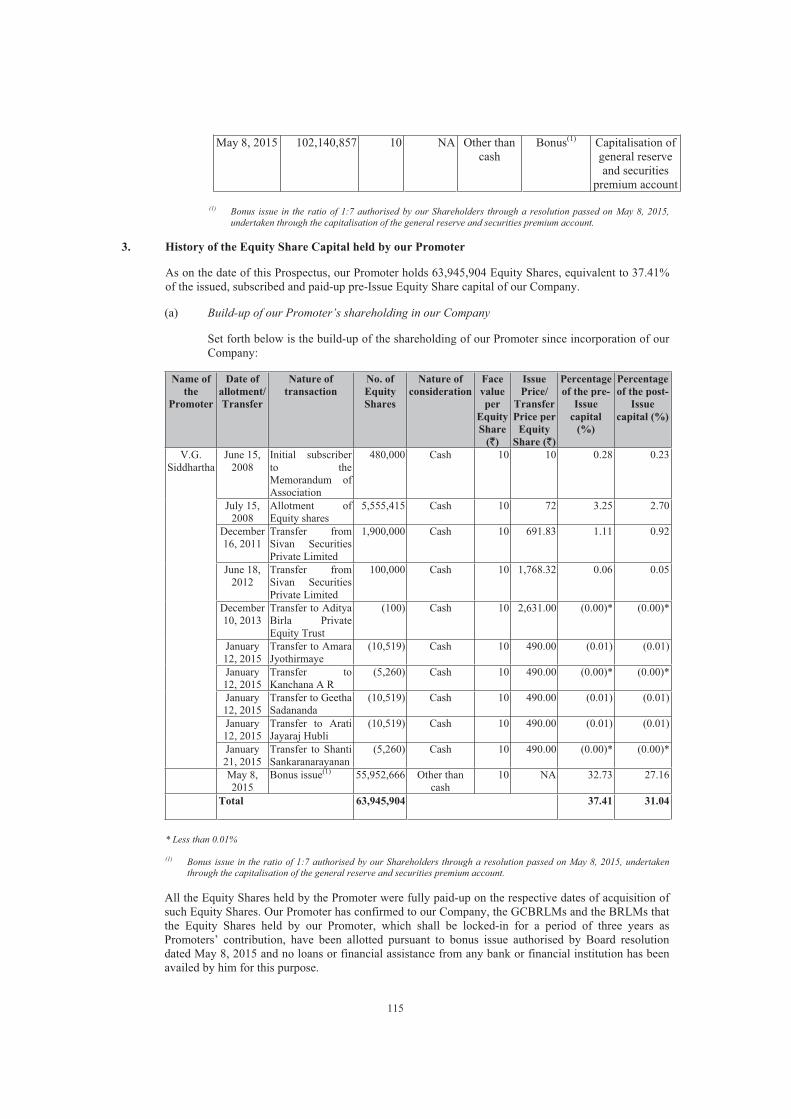

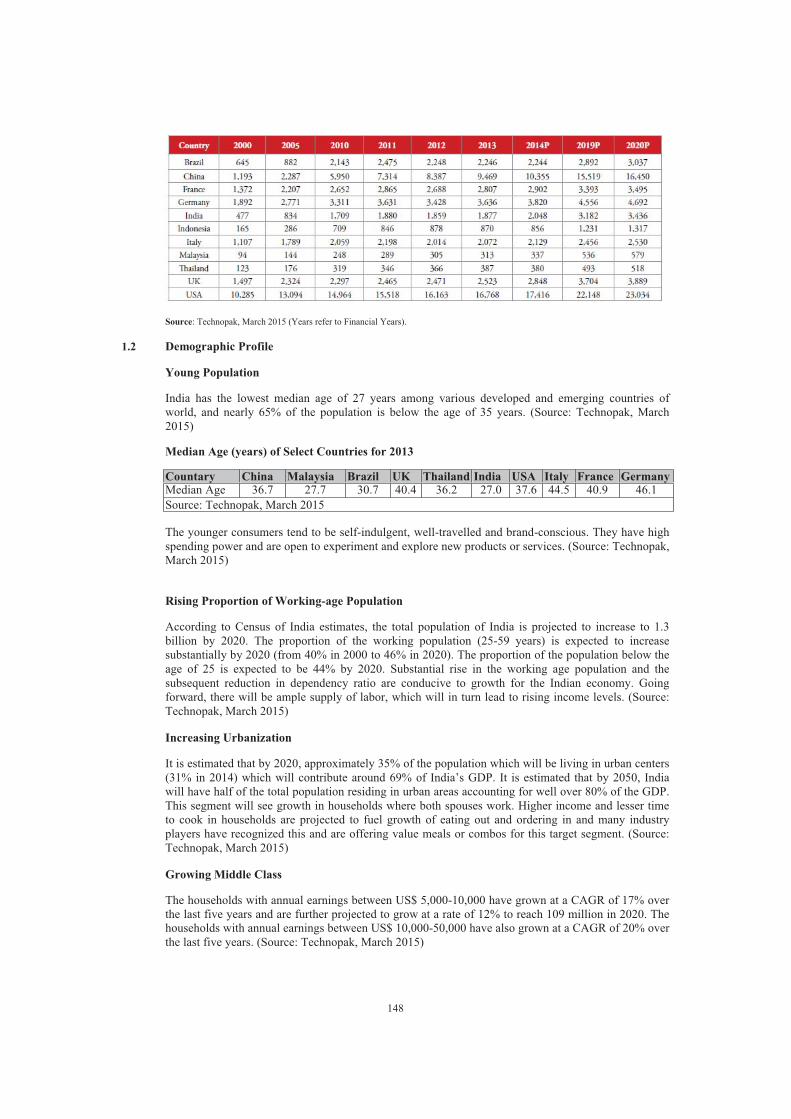

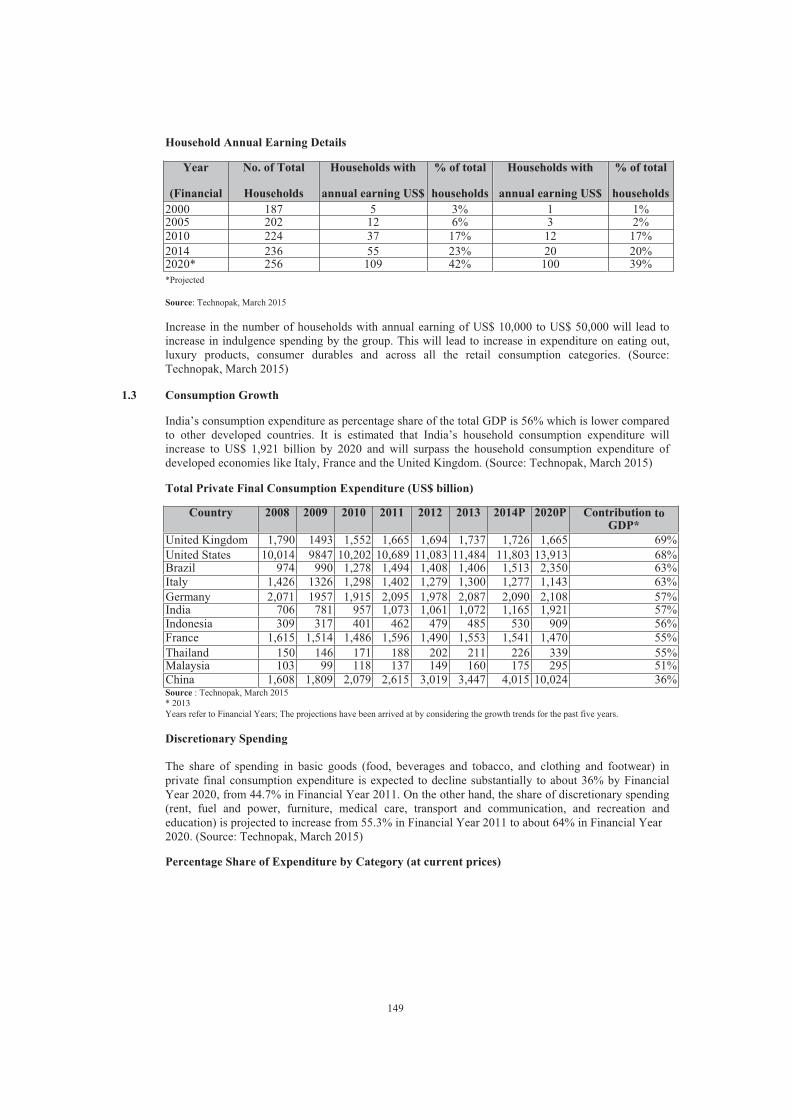

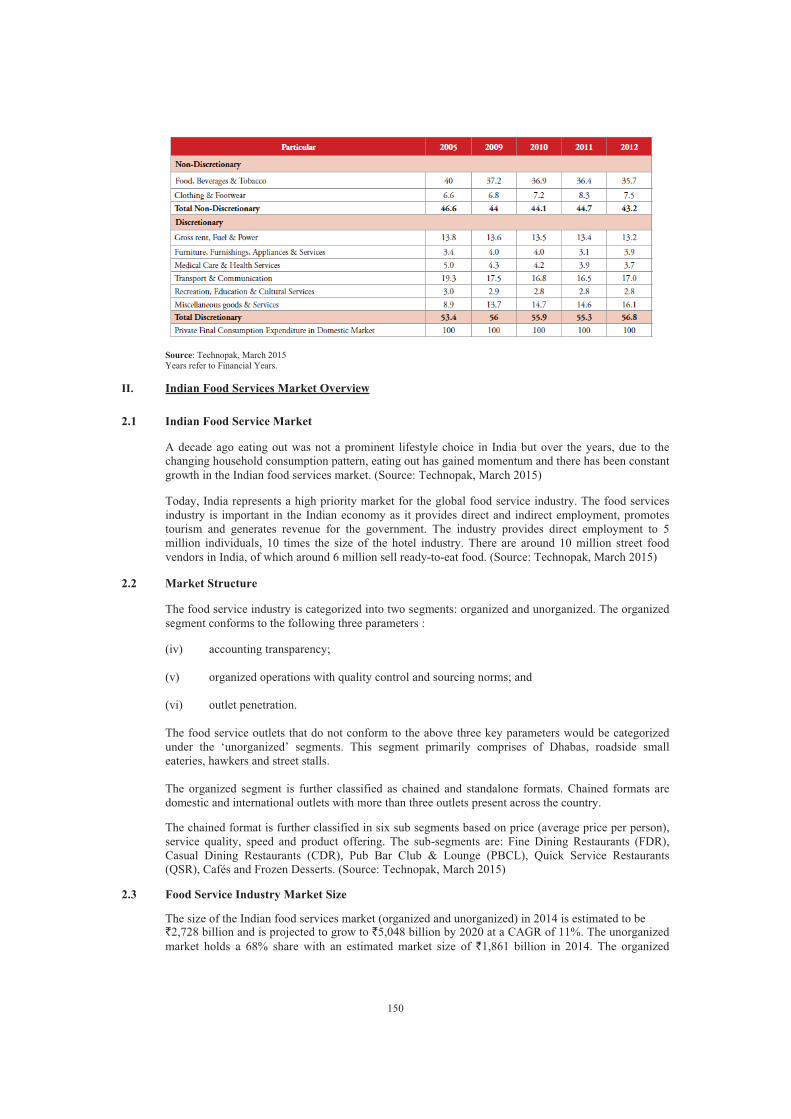

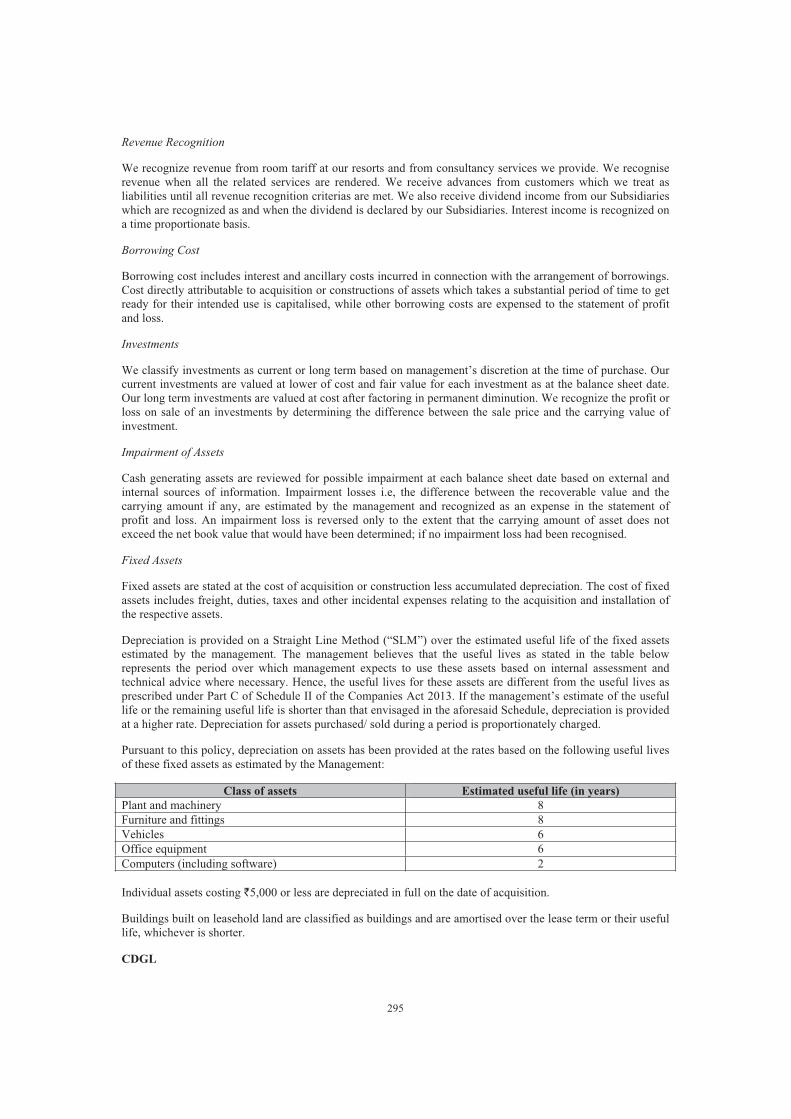

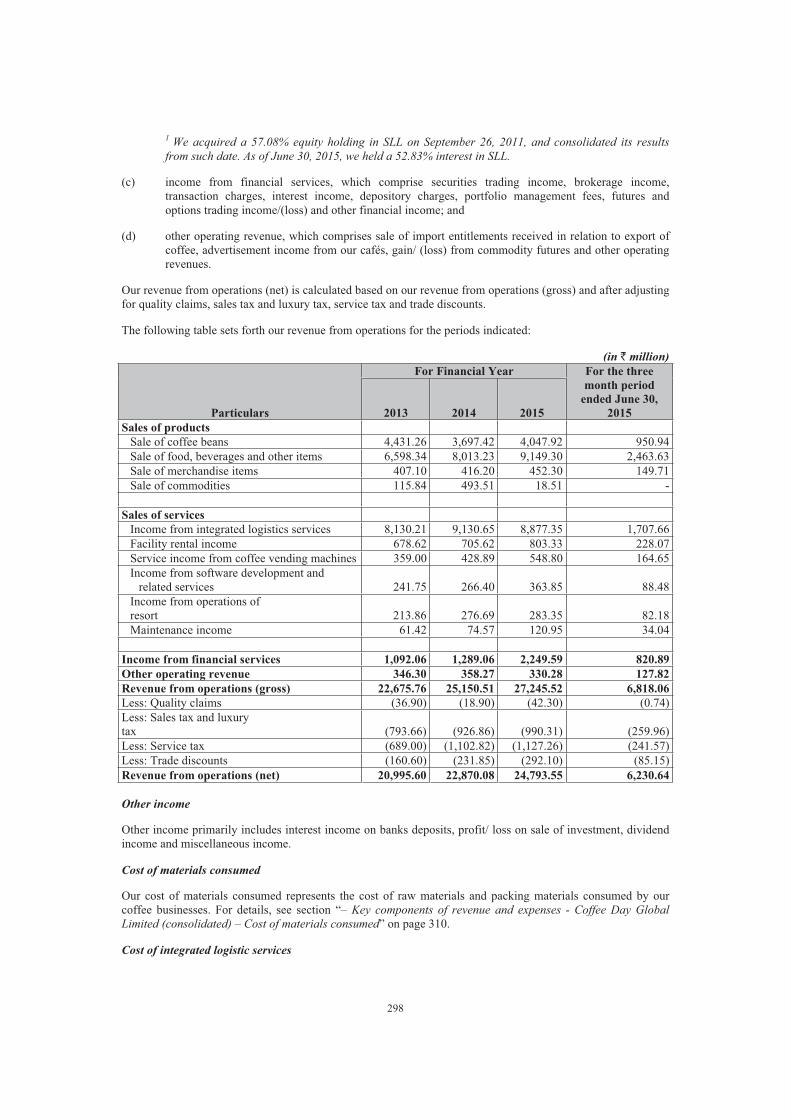

coffee day enterprises limited - morgan stanley

TRANSCRIPT

PROSPECTUSOctober 19, 2015

Please read Section 32 of the Companies Act, 2013100% Book Built Issue

COFFEE DAY ENTERPRISES LIMITEDOur Company was originally formed as a partnership firm constituted under the Indian Partnership Act, 1932 on February 1, 2008 under the name Coffeeday Holding Co. Coffeeday Holding Co. was thereafter converted from a partnership firm to a private limited company under Part IX of the Companies Act, 1956 as Coffee Day Holdings Company Private Limited and a fresh certificate of incorporation was issued by the Registrar of Companies, Bengaluru, Karnataka (“RoC”) on June 20, 2008. The name of our Company was changed to Coffee Day Resorts Private Limited and a fresh certificate of incorporation consequent upon change of name was issued by the RoC on January 25, 2010. Subsequently, the name of our Company was changed to Coffee Day Enterprises Private Limited and a fresh certificate of incorporation consequent upon change of name was issued by the RoC on August 6, 2014. Our Company was converted into a public limited company consequent to a special resolution passed by our Shareholders at the EGM held on January 17, 2015 and the name of our Company was changed to Coffee Day Enterprises Limited. A fresh certificate of incorporation consequent upon conversion to public limited company was issued by the RoC on January 21, 2015. For details of change in the name and registered office of our Company, see section “History and Certain Corporate Matters” on page 218.

Registered and Corporate Office: 23/ 2, Coffee Day Square, Vittal Mallya Road, Bengaluru 560 001, Karnataka, IndiaContact Person: Sadananda Poojary, Company Secretary and Compliance Officer; Tel: +91 80 4001 2345; Fax: +91 80 4001 2650

E-mail:[email protected]; Website: www.coffeeday.comCorporate Identification Number: U55101KA2008PLC046866

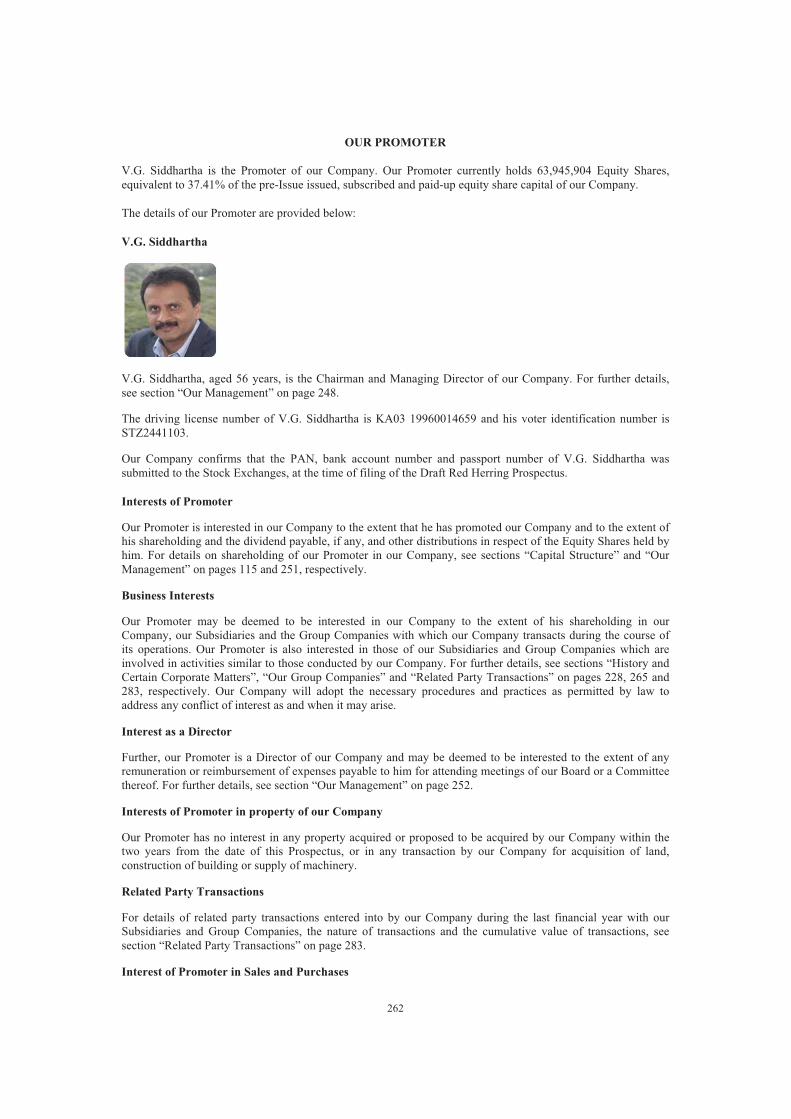

OUR PROMOTER: V.G. SIDDHARTHAPUBLIC ISSUE OF 35,060,975 EQUITY SHARES OF FACE VALUE OF `10 EACH (“EQUITY SHARES”) OF COFFEE DAY ENTERPRISES LIMITED (“COMPANY” OR “ISSUER”) FOR CASH AT A PRICE OF `328 PER EQUITY SHARE (INCLUDING A SHARE PREMIUM OF `318 PER EQUITY SHARE) AGGREGATING TO `11,500 MILLION (“THE ISSUE”). THE ISSUE COMPRISES A NET ISSUE TO THE PUBLIC OF 34,603,659 EQUITY SHARES (THE “NET ISSUE”) AND A RESERVATION OF 457,316 EQUITY SHARES AGGREGATING TO `150 MILLION FOR SUBSCRIPTION BY ELIGIBLE EMPLOYEES (AS DEFINED HEREIN) (THE “EMPLOYEE RESERVATION PORTION”). THE ISSUE WOULD CONSTITUTE 17.02% OF OUR POST-ISSUE PAID-UP EQUITY SHARE CAPITAL AND THE NET ISSUE TO THE PUBLIC WOULD CONSTITUTE 16.80% OF OUR POST-ISSUE PAID-UP EQUITY SHARE CAPITAL.THE FACE VALUE OF EQUITY SHARES IS `10 EACH. THE ISSUE PRICE IS `328 PER EQUITY SHARE AND IS 32.8 TIMES THE FACE VALUE OF THE EQUITY SHARESIn case of any revision to the Price Band, the Bid/ Issue Period will be extended by at least three additional Working Days after such revision of the Price Band, subject to the Bid/ Issue Period not exceeding 10 Working Days. Any revision in the Price Band and the revised Bid/ Issue Period, if applicable, will be widely disseminated by notification to BSE Limited (“BSE”) and the National Stock Exchange of India Limited (“NSE”), by issuing a press release, and also by indicating the change on the websites of the GCBRLMs and the BRLMs and at the terminals of the Syndicate Members.In terms of Rule 19(2)(b)(iii) of the Securities Contracts (Regulation) Rules, 1957, as amended (“SCRR”), this is an Issue for at least 10% of the post-Issue paid-up Equity Share capital of our Company. The Issue is being made in accordance with Regulation 26(1) of the SEBI ICDR Regulations, through the Book Building Process wherein 50% of the Net Issue shall be Allotted on a proportionate basis to Qualified Institutional Buyers (“QIBs”), provided that our Company has allocated 60% of the QIB Portion to Anchor Investors on a discretionary basis, out of which one-third was reserved for domestic Mutual Funds only, subject to valid Bids being received from domestic Mutual Funds at or above the Anchor Investor Issue Price, in accordance with the SEBI ICDR Regulations. 5% of the QIB Portion (excluding the Anchor Investor Portion) shall be available for allocation on a proportionate basis to Mutual Funds only, and the remainder of the QIB Portion shall be available for allocation on a proportionate basis to all QIB Bidders (other than Anchor Investors), including Mutual Funds, subject to valid Bids being received at or above the Issue Price. Further, not less than 15% of the Net Issue shall be available for allocation on a proportionate basis to Non-Institutional Bidders and not less than 35% of the Net Issue shall be available for allocation to Retail Individual Bidders in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Issue Price. All potential investors, other than Anchor Investors, may participate in this Issue through an Application Supported by Blocked Amount (“ASBA”) process providing details of their respective bank account which will be blocked by the Self Certified Syndicate Banks (“SCSBs”). QIBs (except Anchor Investors) and Non-Institutional Bidders are mandatorily required to utilise the ASBA process to participate in this Issue. For details, see section “Issue Procedure” on page 486.

RISK IN RELATION TO THE FIRST ISSUEThis being the first public issue of our Company, there has been no formal market for the Equity Shares. The face value of the Equity Shares is `10 and the Issue Price is 32.8 times the face value.The Issue Price (determined and justified by our Company in consultation with the GCBRLMs and the BRLMs as stated under the section “Basis for Issue Price” on page 140) should not be taken to be indicative of the market price of the Equity Shares after the Equity Shares are listed. No assurance can be given regarding an active or sustained trading in the Equity Shares or regarding the price at which the Equity Shares will be traded after listing.

GENERAL RISKSInvestments in equity and equity-related securities involve a degree of risk and investors should not invest any funds in the Issue unless they can afford to take the risk of losing their entire investment. Investors are advised to read the risk factors carefully before taking an investment decision in the Issue. For taking an investment decision, investors must rely on their own examination of our Company and the Issue, including the risks involved. The Equity Shares in the Issue have not been recommended or approved by the Securities and Exchange Board of India (“SEBI”), nor does SEBI guarantee the accuracy or adequacy of the contents of this Prospectus. Specific attention of the investors is invited to the section “Risk Factors” on page 24.

ISSUER’S ABSOLUTE RESPONSIBILITYOur Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Prospectus contains all information with regard to our Company and the Issue, which is material in the context of the Issue, that the information contained in this Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this Prospectus as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect.

LISTINGThe Equity Shares offered through the Red Herring Prospectus are proposed to be listed on the BSE and the NSE. Our Company has received an ‘in-principle’ approval from the BSE and the NSE for the listing of the Equity Shares pursuant to their letters dated July 17, 2015. For the purposes of the Issue, the Designated Stock Exchange shall be NSE.

GLOBAL CO-ORDINATORS AND BOOK RUNNING LEAD MANAGERS

Kotak Mahindra Capital Company Limited1st Floor, 27 BKC, Plot No. 27, “G” Block, Bandra Kurla ComplexBandra (East), Mumbai 400 051Tel: +91 22 4336 0000Fax: +91 22 6713 2447E-mail: [email protected] grievance E-mail: [email protected]: www.investmentbank.kotak.comContact Person: Ganesh RaneSEBI Registration No.: INM000008704

Citigroup Global Markets India Private Limited1202, 12th Floor, First International Financial Center, G-Block, Bandra Kurla Complex, Bandra (East), Mumbai 400 051Tel: +91 22 6175 9999Fax: +91 22 6175 9961E-mail: [email protected] grievance E-mail: [email protected]: http://www.online.citibank.co.in/rhtm/citigroupglobalscreen1.htmContact Person: Udayan KejriwalSEBI Registration No.: INM000010718

Morgan Stanley India Company Private Limited18F/ 19F, Tower 2, One Indiabulls Centre841, Senapati Bapat Marg, Mumbai 400 013Tel: +91 22 6118 1770Fax: +91 22 6118 1040E-mail: [email protected] grievance E-mail: [email protected]: http://www.morganstanley.com/about-us/global-offices/india/Contact Person: Najmuddin SaqibSEBI Registration No.: INM000011203

BOOK RUNNING LEAD MANAGERS ( in alphabetical order) REGISTRAR TO THE ISSUE

Axis Capital Limited1st Floor, Axis HouseC-2, Wadia International CentreP.B. Marg, Worli, Mumbai 400 025Tel: + 91 22 4325 2183Fax : +91 22 4325 3000E-mail: [email protected] grievance E-mail : [email protected]: www.axiscapital.co.inContact person: Lohit SharmaSEBI Registration Number: INM000012029

Edelweiss Financial Services Limited14th Floor, Edelweiss House, Off. C.S.T. Road, KalinaMumbai 400 098Tel: +91 22 4009 4400Fax: +91 22 4086 3610E-mail: [email protected] grievance E-mail:[email protected]: www.edelweissfin.comContact Person: Amit SoodSEBI Registration No.: INM0000010650

YES Bank LimitedYES Bank Tower, IFC 2, 18th Floor , Senapati Bapat Marg, Elphinstone (W), Mumbai 400 013Tel: +91 22 3366 9000Fax: +91 22 2421 4508E-mail: [email protected] grievance E-mail: [email protected]: www.yesbank.inContact Person: Dhruvin MehtaSEBI Registration No.: INM000010874

Link Intime India Private LimitedC-13, Pannalal Silk Mills Compound, L.B.S. MargBhandup (West) , Mumbai 400 078Tel: +91 22 6171 5400Fax: +91 22 2596 0329E-mail: [email protected] grievance E-mail: [email protected]: www.linkintime.co.inContact Person: Sachin AcharSEBI Registration No.: INR000004058

BID/ ISSUE PROGRAMMEBID/ ISSUE OPENED ON October 14, 2015(1)

BID/ ISSUE CLOSED ON October 16, 2015(1) The Anchor Investor Bid/ Issue Period opened and closed one Working Day prior to the Bid/ Issue Opening Date i.e October 13, 2015.

TABLE OF CONTENTS

SECTION I: GENERAL ..................................................................................................................................... 1

DEFINITIONS AND ABBREVIATIONS......................................................................................................... 1PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA.................................................... 19FORWARD-LOOKING STATEMENTS........................................................................................................ 22

SECTION II: RISK FACTORS........................................................................................................................ 24

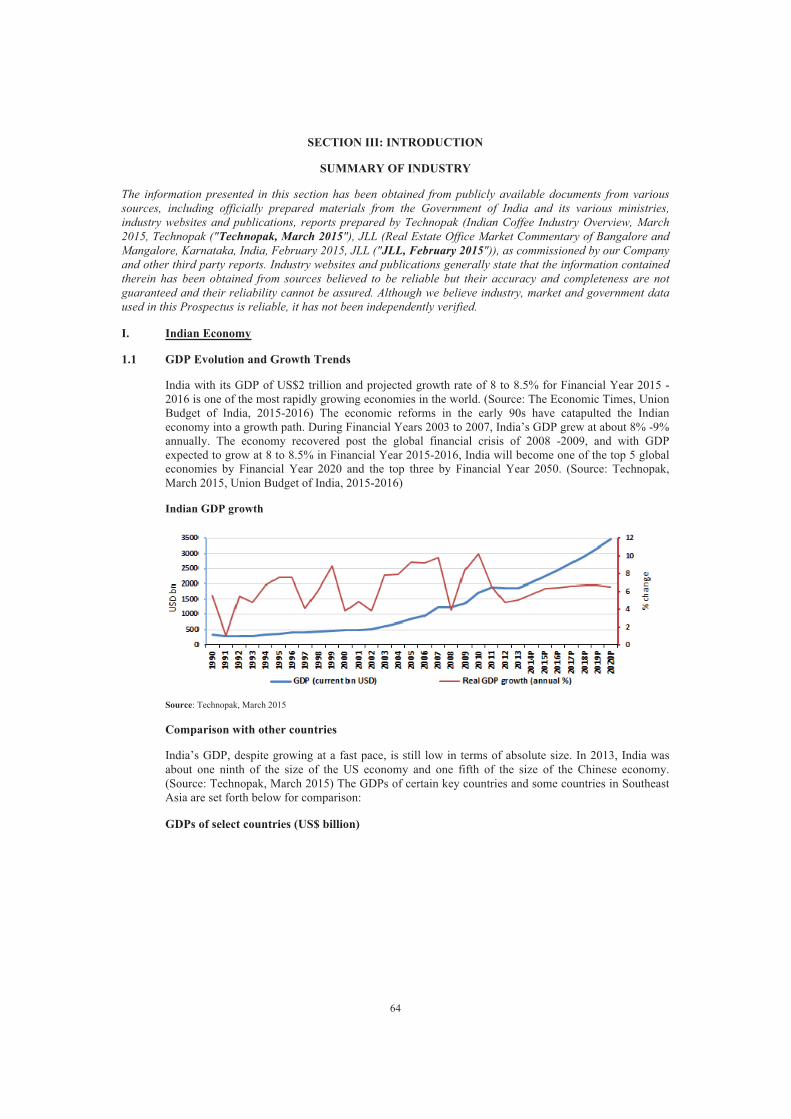

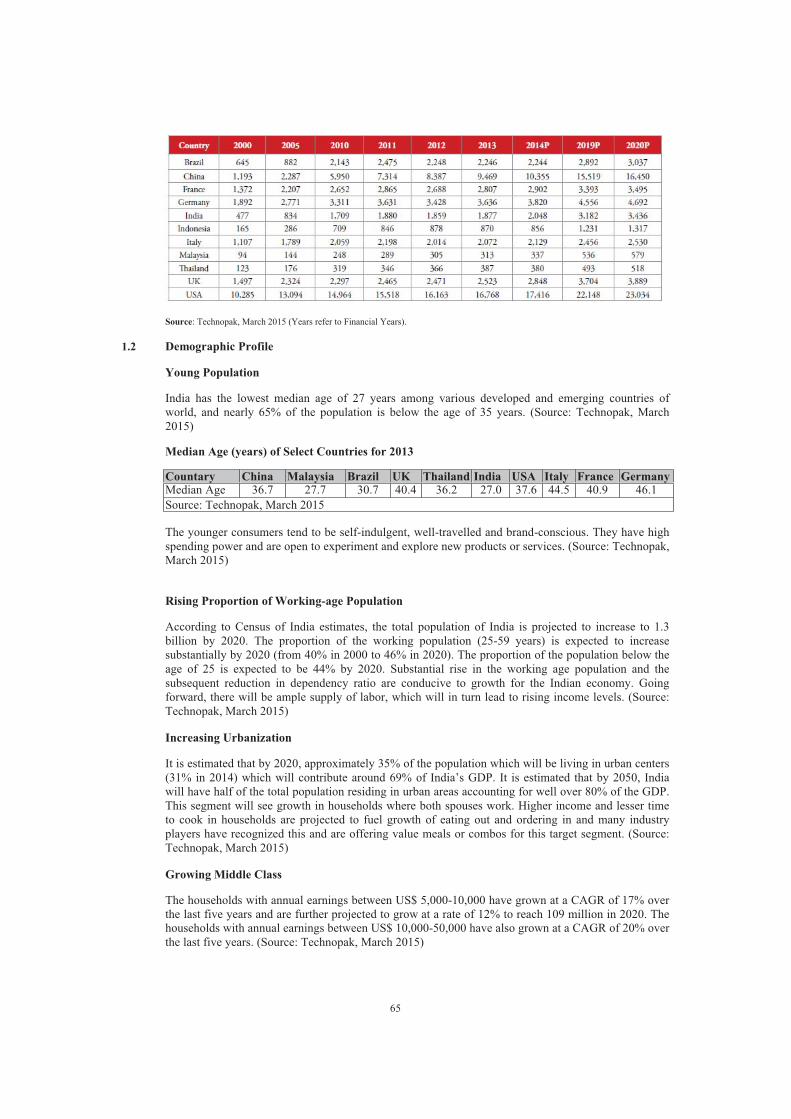

SECTION III: INTRODUCTION .................................................................................................................... 64

SUMMARY OF INDUSTRY .......................................................................................................................... 64SUMMARY OF OUR BUSINESS................................................................................................................... 73SUMMARY OF FINANCIAL INFORMATION............................................................................................. 82THE ISSUE ...................................................................................................................................................... 99GENERAL INFORMATION......................................................................................................................... 100CAPITAL STRUCTURE ............................................................................................................................... 112OBJECTS OF THE ISSUE............................................................................................................................. 124BASIS FOR ISSUE PRICE ............................................................................................................................ 140STATEMENT OF TAX BENEFITS.............................................................................................................. 144

SECTION IV: ABOUT OUR COMPANY .................................................................................................... 147

INDUSTRY OVERVIEW.............................................................................................................................. 147OUR BUSINESS............................................................................................................................................ 175REGULATIONS AND POLICIES ................................................................................................................ 211HISTORY AND CERTAIN CORPORATE MATTERS ............................................................................... 218OUR MANAGEMENT.................................................................................................................................. 245OUR PROMOTER......................................................................................................................................... 262OUR GROUP COMPANIES ......................................................................................................................... 265RELATED PARTY TRANSACTIONS......................................................................................................... 283DIVIDEND POLICY ..................................................................................................................................... 284

SECTION V: FINANCIAL INFORMATION............................................................................................... 285

FINANCIAL STATEMENTS........................................................................................................................ 285MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OFOPERATIONS ............................................................................................................................................... 286FINANCIAL INDEBTEDNESS .................................................................................................................... 327

SECTION VI: LEGAL AND OTHER INFORMATION............................................................................. 418

OUTSTANDING LITIGATION AND MATERIAL DEVELOPMENTS..................................................... 418GOVERNMENT AND OTHER APPROVALS............................................................................................. 452OTHER REGULATORY AND STATUTORY DISCLOSURES.................................................................. 456

SECTION VII: ISSUE INFORMATION....................................................................................................... 476

TERMS OF THE ISSUE ................................................................................................................................ 476ISSUE STRUCTURE..................................................................................................................................... 480ISSUE PROCEDURE .................................................................................................................................... 486RESTRICTIONS ON FOREIGN OWNERSHIP OF INDIAN SECURITIES ............................................... 540

SECTION VIII: MAIN PROVISIONS OF ARTICLES OF ASSOCIATION ........................................... 541

SECTION IX: OTHER INFORMATION ..................................................................................................... 635

MATERIAL CONTRACTS AND DOCUMENTS FOR INSPECTION ....................................................... 635DECLARATION ........................................................................................................................................... 638

1

SECTION I: GENERAL

DEFINITIONS AND ABBREVIATIONS

This Prospectus uses certain definitions and abbreviations which, unless the context otherwise indicates or implies, shall have the meaning as provided below. References to any legislation, acts, regulations, rules, guidelines or policies shall be to such legislation, act or regulation, as amended from time to time.

General Terms

Term Description

“our Company”, “theCompany”, “the Issuer” or“CDEL”

Coffee Day Enterprises Limited, a company incorporated under the Companies Act, 1956 and having its Registered Office at 23/ 2, Coffee Day Square, Vittal Mallya Road, Bengaluru 560 001, Karnataka, India

“we”, “us” or “our” Unless the context otherwise indicates or implies, refers to our Company together with its Subsidiaries

Company Related Terms

Term Description

ABC Employees Trust ABC Employees’ Welfare Trust

AHL Amalgamated Holdings Limited

AHHL AlphaGrep Holding HK Limited

ANCDIL A.N. Coffee Day International Limited

Articles of Association Articles of Association of our Company, as amended

ASPD Average Sales Per Day, for any reporting period is calculated by dividing total gross sales (including taxes) from outlets (including sale of certain merchandise items by AHL in the Café Coffee Day outlets, franchised sales andairline sales) by the number of days the same were operational. All airlines sales are considered as one unit operational for all days in a year/ period. Allthe merchandise sales by AHL are considered as sale in the respective outlets

ASPL AlphaGrep Securities Private Limited

Auditors/ Statutory Auditors Statutory auditors of our Company, namely, B S R & Co. LLP, Chartered Accountants

BOLPL Bergen Offshore Logistics Pte Limited

Board/ Board of Directors Board of Directors of our Company or a duly constituted committee thereof

CCCW Classic Coffee Curing Works

CCD 27,160,000 and 35,998,232 compulsorily convertible debentures of ourCompany of face value of `100 each, issued and allotted to KKR Mauritius PE Investments II Limited and Arduino Holdings Limited (subsequentlytranfererred to NLS Mauritius LLC), pursuant to subscription agreements dated March 12, 2010 and March 27, 2010, respectively

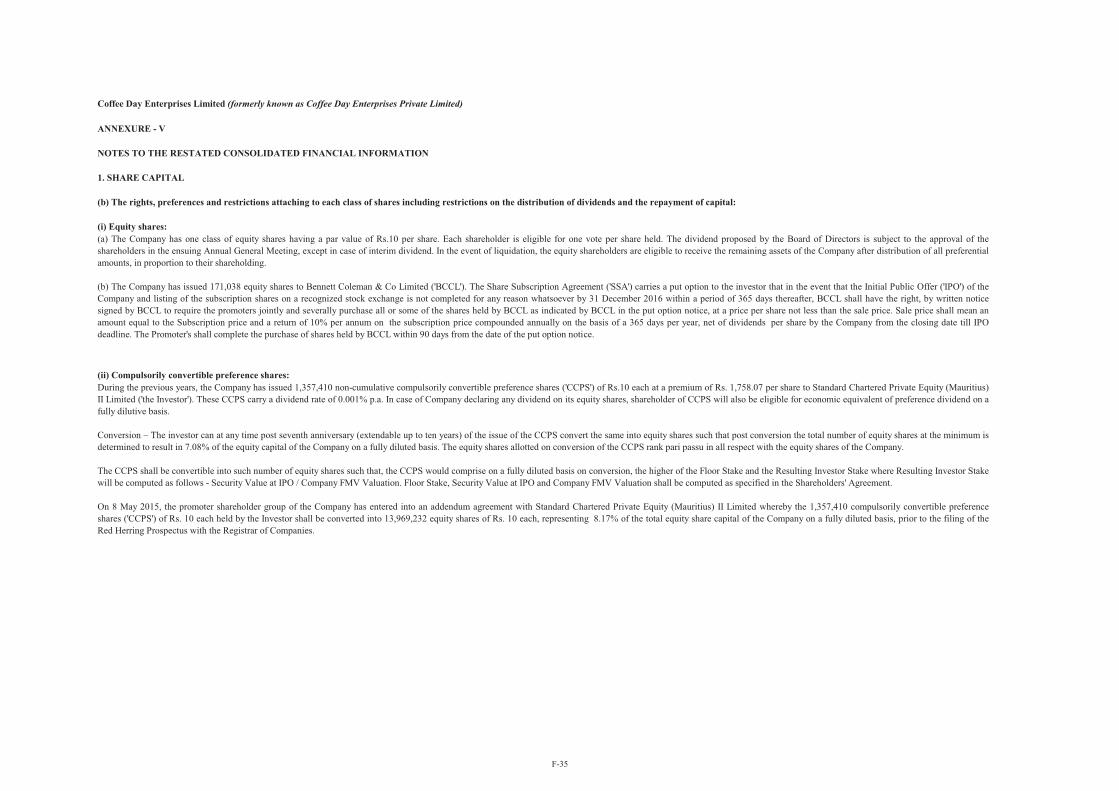

CCPS 1,357,410 0.001% compulsorily convertible preference shares of our Company of face value of `10 each, issued and allotted to Standard Chartered Private Equity (Mauritius) II Limited pursuant to the share

2

Term Description

subscription cum shareholders agreement dated February 5, 2010

CDBFRPL Coffee Day Bare Foot Resorts Private Limited

CDCPL Coffee Day Consolidations Private Limited

CDCZ COFFEE DAY CZ a.s.

CDGKG Coffee Day Gastronomie und Kaffeehandels GmbH

CDGL Coffee Day Global Limited (formerly known as Amalgamated Bean Coffee Trading Company Limited)

CDHRPL Coffee Day Hotels and Resorts Private Limited

CDNRPL Coffee Day Natural Resources Private Limited

CDPIPL Coffee Day Properties (India) Private Limited

CDRMPL Coffee Day Resorts (MSM) Private Limited

CDTL Coffee Day Trading Limited (formerly known as Global Technology Ventures Limited)

CEPL Chandrapore Estates Private Limited

CLL Coffee Lab Limited

Corporate Office Corporate office of our Company located at 23/ 2, Coffee Day Square, Vittal Mallya Road, Bengaluru 560 001, Karnataka, India

CWPPL Chetan Wood Processing Private Limited

DFFCPL Dark Forest Furniture Company Private Limited

Director(s) Director(s) of our Company

DITPL Devadarshini Info Technologies Private Limited

Equity Shares Equity Shares of our Company of face value of `10 each

GCCWL Ganga Coffee Curing Works Limited

GCEPL Gonibedu Coffee Estates Private Limited

Global Edge Global Edge Software Private Limited

GVIL Giri Vidhyuth (India) Limited

Group Companies Companies, firms, ventures, etc. promoted by our Promoter, irrespective of whether such entities are covered under Section 370(1B) of the Companies Act, 1956 or not

For details, see section “Our Group Companies” on page 265

IFC International Finance Corporation

Ittiam Ittiam Systems Private Limited

KEL Kumergode Estates Limited

3

Term Description

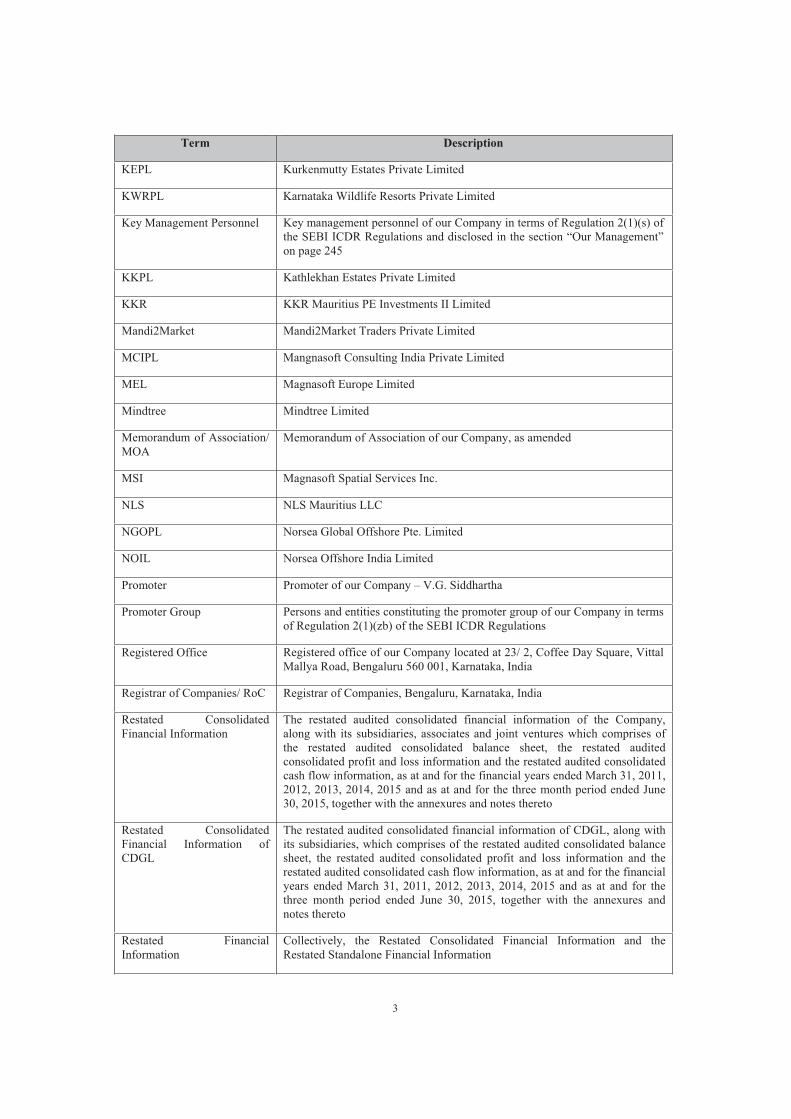

KEPL Kurkenmutty Estates Private Limited

KWRPL Karnataka Wildlife Resorts Private Limited

Key Management Personnel Key management personnel of our Company in terms of Regulation 2(1)(s) of the SEBI ICDR Regulations and disclosed in the section “Our Management”on page 245

KKPL Kathlekhan Estates Private Limited

KKR KKR Mauritius PE Investments II Limited

Mandi2Market Mandi2Market Traders Private Limited

MCIPL Mangnasoft Consulting India Private Limited

MEL Magnasoft Europe Limited

Mindtree Mindtree Limited

Memorandum of Association/ MOA

Memorandum of Association of our Company, as amended

MSI Magnasoft Spatial Services Inc.

NLS NLS Mauritius LLC

NGOPL Norsea Global Offshore Pte. Limited

NOIL Norsea Offshore India Limited

Promoter Promoter of our Company – V.G. Siddhartha

Promoter Group Persons and entities constituting the promoter group of our Company in terms of Regulation 2(1)(zb) of the SEBI ICDR Regulations

Registered Office Registered office of our Company located at 23/ 2, Coffee Day Square, Vittal Mallya Road, Bengaluru 560 001, Karnataka, India

Registrar of Companies/ RoC Registrar of Companies, Bengaluru, Karnataka, India

Restated Consolidated Financial Information

The restated audited consolidated financial information of the Company,along with its subsidiaries, associates and joint ventures which comprises of the restated audited consolidated balance sheet, the restated audited consolidated profit and loss information and the restated audited consolidated cash flow information, as at and for the financial years ended March 31, 2011,2012, 2013, 2014, 2015 and as at and for the three month period ended June30, 2015, together with the annexures and notes thereto

Restated Consolidated Financial Information of CDGL

The restated audited consolidated financial information of CDGL, along with its subsidiaries, which comprises of the restated audited consolidated balance sheet, the restated audited consolidated profit and loss information and the restated audited consolidated cash flow information, as at and for the financial years ended March 31, 2011, 2012, 2013, 2014, 2015 and as at and for the three month period ended June 30, 2015, together with the annexures and notes thereto

Restated FinancialInformation

Collectively, the Restated Consolidated Financial Information and the Restated Standalone Financial Information

4

Term Description

Restated Standalone Financial Information

The restated audited standalone financial information of the Company, whichcomprises of the restated audited standalone balance sheet, the restated audited standalone profit and loss information and restated audited standalone cash flow information, as at and for the years ended March 31, 2011, 2012,2013, 2014, 2015 and as at and for the three month period ended June 30, 2015, together with the annexures and notes thereto

RSEPL Rajagiri and Sankhan Estates Private Limited

SEPL Sampigehutty Estates Private Limited

Shareholders Shareholders of our Company from time to time

SAOL Sical Adams Offshore Limited

SIAL Sical Infra Assets Limited

SIOTL Sical Iron Ore Terminals Limited

SIOTML Sical Iron Ore Terminal (Mangalore) Limited

SLL Sical Logistics Limited

SMART Sical Multimodal and Rail Transport Limited

SRPL Shankar Resources Private Limited

SSPL Sivan Securities Private Limited

SSSG Same Store Sales Growth means, for any reporting period, the percentage change in sales for the company-operated, and franchised outlets in India and airline sales, open for 13 months or longer as at the end of each respective year or period. For the stores meeting the above definition, the year-over-yearsales growth percentage is computed by comparing the cumulative gross sales (including taxes) for same months for a year which were in operation during both periods. The sales include merchandise sales by AHL as part of the CaféCoffee Day outlets , and franchised outlets in India and airline sales

SVGH Education Trust Shankarkoodige V. Gangaiah Hegde Education Trust

Standard Chartered Standard Chartered Private Equity (Mauritius) II Limited

Subsidiaries or individually known as Subsidiary

Subsidiaries of our Company namely:

1. A.N. Coffee Day International Limited

2. AlphaGrep Holding HK Limited

3. AlphaGrep Securities Private Limited

4. Amalgamated Holdings Limited

5. Bergen Offshore Logistics Pte Limited

6. COFFEE DAY CZ a.s.

7. Coffee Day Gastronomie und Kaffeehandels GmbH

8. Coffee Day Global Limited

5

Term Description

9. Coffee Day Hotels & Resorts Private Limited

10. Coffee Day Properties (India) Private Limited

11. Coffee Day Trading Limited

12. Coffee Lab Limited

13. Ganga Coffee Curing Works Limited

14. Giri Vidhyuth (India) Limited

15. Karnataka Wildlife Resorts Private Limited

16. Magnasoft Consulting India Private Limited

17. Magnasoft Europe Limited

18. Magnasoft Spatial Services Inc.

19. Mandi2Market Traders Private Limited

20. Norsea Global Offshore Pte. Limited

21. Norsea Offshore India Limited

22. Sical Adams Offshore Limited

23. Sical Infra Assets Limited

24. Sical Iron Ore Terminals Limited

25. Sical Iron Ore Terminal (Mangalore) Limited

26. Sical Logistics Limited

27. Sical Multimodal and Rail Transport Limited

28. Tanglin Developments Limited

29. Tanglin Retail Realty Developments Private Limited

30. Techno Commodity Broking Private Limited

31. Techno Shares & Stocks Private Limited

32. Way2Wealth Brokers Private Limited

33. Way2Wealth Capital Private Limited

34. Way2Wealth Commodities Private Limited

35. Way2Wealth Distributors Private Limited

36. Way2Wealth Illuminati Pte Limited

37. Way2Wealth Insurance Brokers Private Limited

38. Way2Wealth Realty Advisors Private Limited

39. Way2Wealth Securities Private Limited

6

Term Description

40. Wilderness Resorts Private Limited

TCBPL Techno Commodity Broking Private Limited

TDL Tanglin Developments Limited

TF Chennai Terra-Firma (Solid Waste Management) Chennai Private Limited

TRRDPL Tanglin Retail Realty Developments Private Limited

TPDMPL Tanglin Property Developments (Mumbai) Private Limited

TSSPL Techno Shares & Stocks Private Limited

VHPI Vaitarna Holding Private Incorporated

VHPL Vakrathunda Holding Private Limited

VTTPL Vaitarna Timber Trading Private Limited

WRPL Wilderness Resorts Private Limited

W2W Brokers Way2Wealth Brokers Private Limited

W2W Capital Way2Wealth Capital Private Limited

W2W Commodities Way2Wealth Commodities Private Limited

W2W Distributors Way2Wealth Distributors Private Limited

W2W Employees Trust Way2Wealth Employees Welfare Trust

W2W Insurance Way2Wealth Insurance Brokers Private Limited

W2W Realty Way2Wealth Realty Advisors Private Limited

W2W Securities Way2Wealth Securities Private Limited

W2W Singapore Way2Wealth Illuminati Pte Limited

Issue Related Terms

Term Description

Allot/ Allotment/ Allotted Allotment of Equity Shares pursuant to the Issue to successful Bidders

Allotment Advice Note or advice or intimation of Allotment sent to the Bidders who have been or are to be Allotted the Equity Shares after the Basis of Allotment has been approved by the Designated Stock Exchange

Allottee A successful Bidder to whom the Equity Shares are Allotted

Anchor Investor A Qualified Institutional Buyer, applying under the Anchor Investor Portion in accordance with the requirements specified in the SEBI ICDR Regulations

Anchor Investor Allocation Price

`322 per Equity Share

Anchor Investor Bid/ Issue October 13, 2015, being the day, one Working Day prior to the Bid/ IssueOpening Date, on which Bids by Anchor Investors were submitted and

7

Term Description

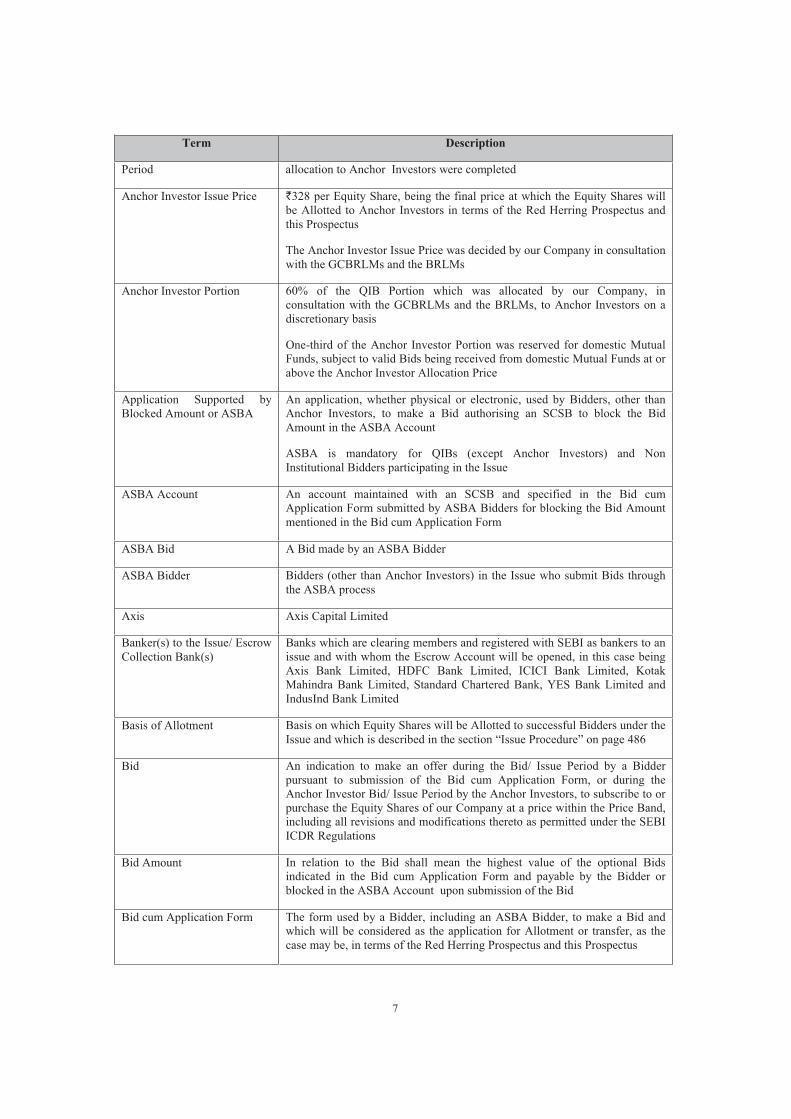

Period allocation to Anchor Investors were completed

Anchor Investor Issue Price `328 per Equity Share, being the final price at which the Equity Shares will be Allotted to Anchor Investors in terms of the Red Herring Prospectus andthis Prospectus

The Anchor Investor Issue Price was decided by our Company in consultation with the GCBRLMs and the BRLMs

Anchor Investor Portion 60% of the QIB Portion which was allocated by our Company, inconsultation with the GCBRLMs and the BRLMs, to Anchor Investors on a discretionary basis

One-third of the Anchor Investor Portion was reserved for domestic Mutual Funds, subject to valid Bids being received from domestic Mutual Funds at or above the Anchor Investor Allocation Price

Application Supported by Blocked Amount or ASBA

An application, whether physical or electronic, used by Bidders, other than Anchor Investors, to make a Bid authorising an SCSB to block the Bid Amount in the ASBA Account

ASBA is mandatory for QIBs (except Anchor Investors) and Non Institutional Bidders participating in the Issue

ASBA Account An account maintained with an SCSB and specified in the Bid cumApplication Form submitted by ASBA Bidders for blocking the Bid Amount mentioned in the Bid cum Application Form

ASBA Bid A Bid made by an ASBA Bidder

ASBA Bidder Bidders (other than Anchor Investors) in the Issue who submit Bids throughthe ASBA process

Axis Axis Capital Limited

Banker(s) to the Issue/ EscrowCollection Bank(s)

Banks which are clearing members and registered with SEBI as bankers to an issue and with whom the Escrow Account will be opened, in this case being Axis Bank Limited, HDFC Bank Limited, ICICI Bank Limited, Kotak Mahindra Bank Limited, Standard Chartered Bank, YES Bank Limited andIndusInd Bank Limited

Basis of Allotment Basis on which Equity Shares will be Allotted to successful Bidders under the Issue and which is described in the section “Issue Procedure” on page 486

Bid An indication to make an offer during the Bid/ Issue Period by a Bidder pursuant to submission of the Bid cum Application Form, or during the Anchor Investor Bid/ Issue Period by the Anchor Investors, to subscribe to or purchase the Equity Shares of our Company at a price within the Price Band, including all revisions and modifications thereto as permitted under the SEBI ICDR Regulations

Bid Amount In relation to the Bid shall mean the highest value of the optional Bids indicated in the Bid cum Application Form and payable by the Bidder orblocked in the ASBA Account upon submission of the Bid

Bid cum Application Form The form used by a Bidder, including an ASBA Bidder, to make a Bid and which will be considered as the application for Allotment or transfer, as the case may be, in terms of the Red Herring Prospectus and this Prospectus

8

Term Description

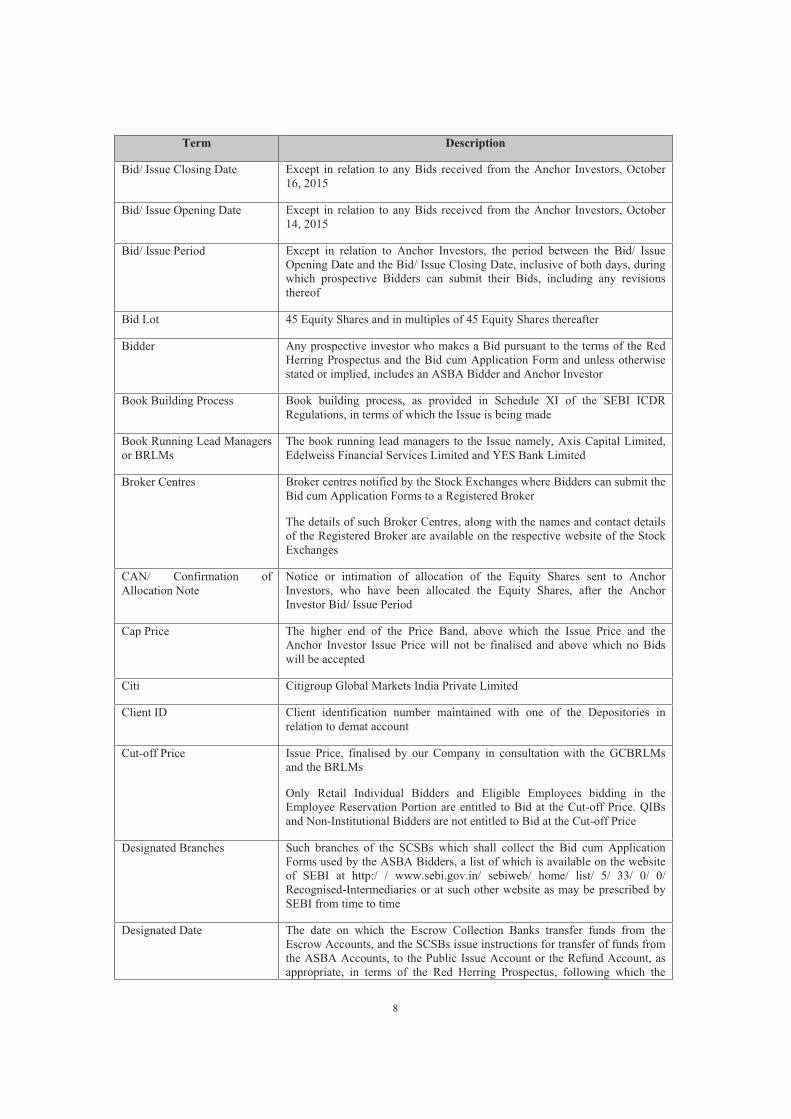

Bid/ Issue Closing Date Except in relation to any Bids received from the Anchor Investors, October16, 2015

Bid/ Issue Opening Date Except in relation to any Bids received from the Anchor Investors, October14, 2015

Bid/ Issue Period Except in relation to Anchor Investors, the period between the Bid/ IssueOpening Date and the Bid/ Issue Closing Date, inclusive of both days, during which prospective Bidders can submit their Bids, including any revisions thereof

Bid Lot 45 Equity Shares and in multiples of 45 Equity Shares thereafter

Bidder Any prospective investor who makes a Bid pursuant to the terms of the RedHerring Prospectus and the Bid cum Application Form and unless otherwise stated or implied, includes an ASBA Bidder and Anchor Investor

Book Building Process Book building process, as provided in Schedule XI of the SEBI ICDRRegulations, in terms of which the Issue is being made

Book Running Lead Managersor BRLMs

The book running lead managers to the Issue namely, Axis Capital Limited, Edelweiss Financial Services Limited and YES Bank Limited

Broker Centres Broker centres notified by the Stock Exchanges where Bidders can submit the Bid cum Application Forms to a Registered Broker

The details of such Broker Centres, along with the names and contact details of the Registered Broker are available on the respective website of the Stock Exchanges

CAN/ Confirmation of Allocation Note

Notice or intimation of allocation of the Equity Shares sent to Anchor Investors, who have been allocated the Equity Shares, after the Anchor Investor Bid/ Issue Period

Cap Price The higher end of the Price Band, above which the Issue Price and the Anchor Investor Issue Price will not be finalised and above which no Bids will be accepted

Citi Citigroup Global Markets India Private Limited

Client ID Client identification number maintained with one of the Depositories in relation to demat account

Cut-off Price Issue Price, finalised by our Company in consultation with the GCBRLMsand the BRLMs

Only Retail Individual Bidders and Eligible Employees bidding in the Employee Reservation Portion are entitled to Bid at the Cut-off Price. QIBs and Non-Institutional Bidders are not entitled to Bid at the Cut-off Price

Designated Branches Such branches of the SCSBs which shall collect the Bid cum Application Forms used by the ASBA Bidders, a list of which is available on the website of SEBI at http:/ / www.sebi.gov.in/ sebiweb/ home/ list/ 5/ 33/ 0/ 0/Recognised-Intermediaries or at such other website as may be prescribed by SEBI from time to time

Designated Date The date on which the Escrow Collection Banks transfer funds from the Escrow Accounts, and the SCSBs issue instructions for transfer of funds from the ASBA Accounts, to the Public Issue Account or the Refund Account, as appropriate, in terms of the Red Herring Prospectus, following which the

9

Term Description

board of directors may Allot Equity Shares to successful Bidders/ Applicantsin the Issue

Designated Stock Exchange National Stock Exchange of India Limited

Draft Red Herring Prospectus or DRHP

The Draft Red Herring Prospectus dated June 25, 2015, issued in accordance with the SEBI ICDR Regulations, which does not contain complete particulars of the price at which the Equity Shares will be Allotted, Bid Lotand the size of the Issue, including any addendum or corrigendum thereto

Edelweiss Edelweiss Financial Services Limited

Eligible Employees All or any of the following:

(a) a permanent and full time employee of our Company or the Subsidiaries(excluding such employees who are not eligible to invest in the Issueunder applicable laws, rules, regulations and guidelines and our Promoterand his immediate relatives) as of the date of filing of the Red Herring Prospectus with the RoC and who continues to be an employee of our Company or the Subsidiaries, until Allotment; and

(b) a Director of our Company or Subsidiary, whether a whole time Director or otherwise, (excluding such Directors not eligible to invest in the Issueunder applicable laws, rules, regulations and guidelines and our Promoterand his immediate relatives) as of the date of filing the Red Herring Prospectus with the RoC and who continues to be a Director of our Company or Subsidiary until Allotment and is based and present in India as on the date of Allotment.

The maximum Bid Amount under the Employee Reservation Portion by an Eligible Employee shall not exceed `200,000

Eligible NRI(s) NRI(s) from jurisdictions outside India where it is not unlawful to make an offer or invitation under the Issue and in relation to whom the Bid cum Application Form and the Red Herring Prospectus will constitute an invitation to subscribe to or to purchase the Equity Shares

Employee Reservation Portion Portion of the Issue being 457,316 Equity Shares aggregating to `150 millionavailable for allocation to Eligible Employees, on a proportionate basis

Escrow Account Account opened with the Escrow Collection Bank(s) and in whose favour the Bidders (excluding the ASBA Bidders) will issue cheques or drafts in respect of the Bid Amount when submitting a Bid

Escrow Agreement Agreement dated October 9, 2014 entered into by our Company, the Registrar to the Issue, the GCBRLMs, the BRLMs, the Syndicate Members, the Escrow Collection Banks and the Refund Banks for collection of the Bid Amounts and where applicable, refunds of the amounts collected from the Bidders (excluding the ASBA Bidders), on the terms and conditions thereof

First Bidder Bidder whose name shall be mentioned in the Bid cum Application Form incase of joint Bids, whose name shall also appear as the first holder of the beneficiary account held in joint names

Floor Price The lower end of the Price Band, in this case being `316, subject to any revision thereto, at or above which the Issue Price and the Anchor Investor Issue Price will be finalised and below which no Bids will be accepted

General Information General Information Document prepared and issued in accordance with the

10

Term Description

Document/ GID circular (CIR/ CFD/ DIL/ 12/ 2013) dated October 23, 2013 notified by SEBI

Global Co-ordinators and Book Running Lead Managers or GCBRLMs

The global co-ordinators and book running lead managers to the Issuenamely, Kotak Mahindra Capital Company Limited, Citigroup Global Markets India Private Limited and Morgan Stanley India Company Private Limited

Issue The public issue of 35,060,975 Equity Shares of face value of `10 each for cash at a price of `328 each, aggregating to `11,500 million

The Issue comprises of Net Issue to the public aggregating to `11,350 millionand Employee Reservation Portion aggregating to `150 million

Issue Agreement The agreement dated June 25, 2015 between our Company, the GCBRLMsand the BRLMs, pursuant to which certain arrangements are agreed to in relation to the Issue

Issue Price

Allotted in terms of the Red Herring Prospectus.

The Issue Price was decided by our Company in consultation with the GCBRLMs and the BRLMs on the Pricing Date

Issue Proceeds The proceeds of the Issue that is available to our Company

Kotak Kotak Mahindra Capital Company Limited

Maximum RIB Allottees Maximum number of RIBs who can be allotted the minimum Bid Lot. This is computed by dividing the total number of Equity Shares available for Allotment to RIBs by the minimum Bid Lot

Monitoring Agency IFCI Limited

Morgan Morgan Stanley India Company Private Limited

Mutual Fund Portion 5% of the QIB Portion (excluding the Anchor Investor Portion), or 346,037Equity Shares which shall be available for allocation to Mutual Funds only

Mutual Funds Mutual funds registered with SEBI under the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996

Net Issue Issue less the Employee Reservation Portion

Net Proceeds Issue Proceeds less Issue expenses

For further information about use of the Issue Proceeds and the Issueexpenses, see section “Objects of the Issue” on page 124

Non-Institutional Bidders All Bidders that are not QIBs or Retail Individual Bidders or EligibleEmployees bidding in the Employee Reservation Portion and who have Bid for Equity Shares for an amount more than `200,000 (but not including NRIs other than Eligible NRIs)

Non-Institutional Portion The portion of the Net Issue being not less than 15% of the Net Issueconsisting of 5,190,549 Equity Shares available for allocation on a proportionate basis to Non-Institutional Bidders, subject to valid Bids being received at or above the Issue Price

Non-Resident A person resident outside India, as defined under FEMA and includes a non

328 per Equity Share, being the final price at which Equity Shares will be `

11

Term Description

resident Indian, FIIs and FPIs

Price Band Price band of a minimum price of `316 per Equity Share (Floor Price) and the maximum price of `328 per Equity Share (Cap Price) including revisions thereof

The Price Band and the minimum Bid Lot size for the Issue was decided by our Company in consultation with the GCBRLMs and the BRLMs and wasadvertised, at least five Working Days prior to the Bid/ Issue Opening Date, in all editions of the English national newspaper Business Standard , alleditions of the Hindi national newspaper, Business Standard, and Bengaluruedition of the Kannada newspaper, Vijayvani, each with wide circulation andsuch advertisement shall be made available to the Stock Exchanges for the purpose of uploading on their websites.

Pricing Date The date, October 19, 2015, on which our Company, in consultation with theGCBRLMs and the BRLMs, finalised the Issue Price

Prospectus This Prospectus dated October 19, 2015 to be filed with the RoC after the Pricing Date in accordance with Section 26 of the Companies Act, 2013, andthe SEBI ICDR Regulations containing, inter alia, the Issue Price that is determined at the end of the Book Building Process, the size of the Issue andcertain other information, including any addenda or corrigenda thereto

Public Issue Account Account opened with the Bankers to the Issue under section 40 of the Companies Act, 2013 to receive monies from the Escrow Account(s) on theDesignated Date and to which the funds shall be transferred by the SCSBs from the ASBA Accounts

QIB Category/ QIB Portion The portion of the Net Issue (including the Anchor Investor Portion) being 50% of the Net Issue consisting of 17,301,829 Equity Shares which shall be Allotted to QIBs (including Anchor Investors)

Qualified Institutional Buyers or QIBs

Qualified institutional buyers as defined under Regulation 2(1)(zd) of the SEBI ICDR Regulations

Red Herring Prospectus orRHP

The Red Herring Prospectus dated October 6, 2015 to be issued in accordance with Section 32 of the Companies Act, 2013 and the provisions of the SEBI ICDR Regulations, which will not have complete particulars of the price at which the Equity Shares will be offered and the size of the Issue

The Red Herring Prospectus will become the Prospectus upon filing with the RoC after the Pricing Date

Refund Account(s) The account opened with the Refund Bank(s), from which refunds, if any, of the whole or part of the Bid Amount (excluding refund to ASBA Bidders) shall be made

Refund Bank(s) Kotak Mahindra Bank Limited and YES Bank Limited

Refunds through electronic transfer of funds

Refunds through NECS, direct credit, RTGS or NEFT, as applicable

Registered Brokers Stock brokers registered with the stock exchanges having nationwide terminals, other than the Members of the Syndicate

Registrar to the Issue orRegistrar

Link Intime India Private Limited

Retail Individual Bidder(s) or Individual Bidders, other than Eligible Employees bidding in the Employee

12

Term Description

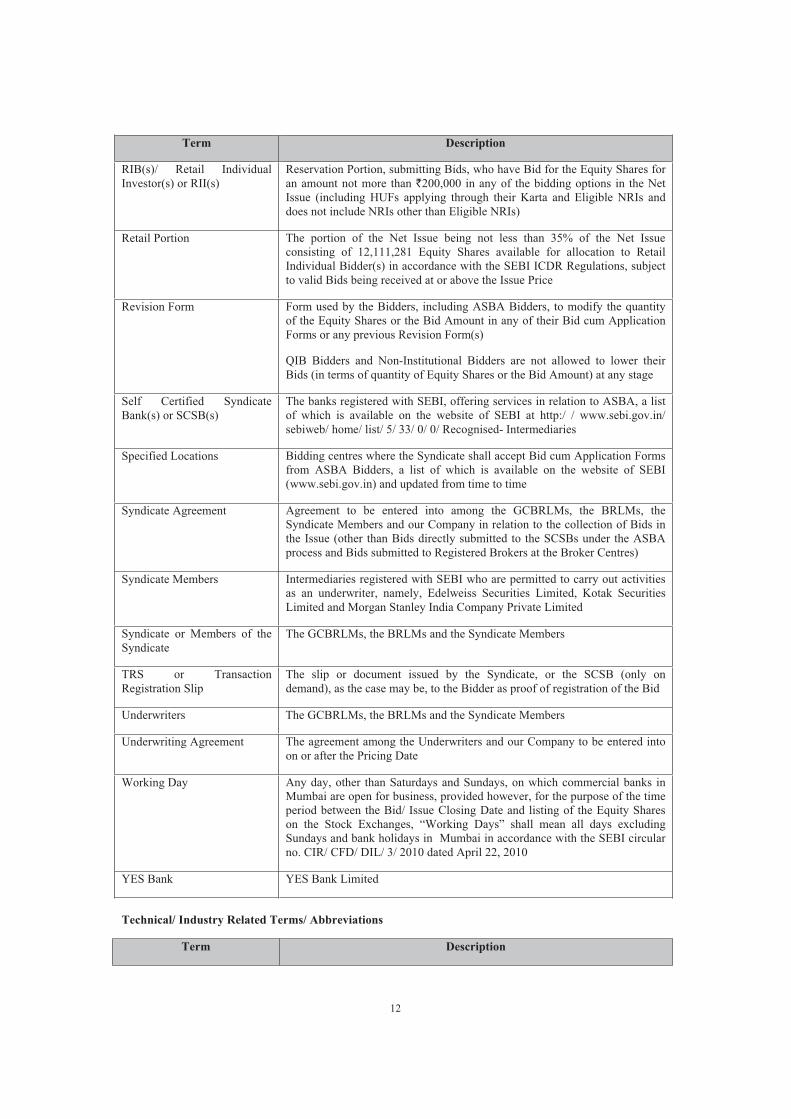

RIB(s)/ Retail Individual Investor(s) or RII(s)

Reservation Portion, submitting Bids, who have Bid for the Equity Shares for an amount not more than `200,000 in any of the bidding options in the NetIssue (including HUFs applying through their Karta and Eligible NRIs and does not include NRIs other than Eligible NRIs)

Retail Portion The portion of the Net Issue being not less than 35% of the Net Issueconsisting of 12,111,281 Equity Shares available for allocation to Retail Individual Bidder(s) in accordance with the SEBI ICDR Regulations, subject to valid Bids being received at or above the Issue Price

Revision Form Form used by the Bidders, including ASBA Bidders, to modify the quantity of the Equity Shares or the Bid Amount in any of their Bid cum Application Forms or any previous Revision Form(s)

QIB Bidders and Non-Institutional Bidders are not allowed to lower their Bids (in terms of quantity of Equity Shares or the Bid Amount) at any stage

Self Certified SyndicateBank(s) or SCSB(s)

The banks registered with SEBI, offering services in relation to ASBA, a list of which is available on the website of SEBI at http:/ / www.sebi.gov.in/sebiweb/ home/ list/ 5/ 33/ 0/ 0/ Recognised- Intermediaries

Specified Locations Bidding centres where the Syndicate shall accept Bid cum Application Formsfrom ASBA Bidders, a list of which is available on the website of SEBI (www.sebi.gov.in) and updated from time to time

Syndicate Agreement Agreement to be entered into among the GCBRLMs, the BRLMs, the Syndicate Members and our Company in relation to the collection of Bids in the Issue (other than Bids directly submitted to the SCSBs under the ASBA process and Bids submitted to Registered Brokers at the Broker Centres)

Syndicate Members Intermediaries registered with SEBI who are permitted to carry out activitiesas an underwriter, namely, Edelweiss Securities Limited, Kotak Securities Limited and Morgan Stanley India Company Private Limited

Syndicate or Members of the Syndicate

The GCBRLMs, the BRLMs and the Syndicate Members

TRS or Transaction Registration Slip

The slip or document issued by the Syndicate, or the SCSB (only on demand), as the case may be, to the Bidder as proof of registration of the Bid

Underwriters The GCBRLMs, the BRLMs and the Syndicate Members

Underwriting Agreement The agreement among the Underwriters and our Company to be entered into on or after the Pricing Date

Working Day Any day, other than Saturdays and Sundays, on which commercial banks in Mumbai are open for business, provided however, for the purpose of the time period between the Bid/ Issue Closing Date and listing of the Equity Shares on the Stock Exchanges, “Working Days” shall mean all days excluding Sundays and bank holidays in Mumbai in accordance with the SEBI circular no. CIR/ CFD/ DIL/ 3/ 2010 dated April 22, 2010

YES Bank YES Bank Limited

Technical/ Industry Related Terms/ Abbreviations

Term Description

13

Term Description

BRC British Retail Consortium

CBD Central Business District

CCI The Competition Commission of India

DCT Domestic Container Terminal

DTA Domestic Tariff Area

EBITDA Earnings Before Interest, Tax, Depreciation and Amortization

FDR Fine Dining Restaurants

F&G Fresh & Ground

GST Goods & Service Tax

HUL Hindustan Unilever Limited

ICD Inland Container Depots

IT/ITES Information Technology/Information Technology Enabled Services

JLL Jones Lang LaSalle Property Consultants (India) Private Limited

Jubilant Foodworks Jubilant FoodWorks Limited

KPI Key Performance Indicator

Lavazza Luigi Lavazza S.p.A.

MT Metric Tonne

R&D Research & Development

Technopak Technopak Advisors Private Limited

TEU Twenty-foot Equivalent Unit

Nestle Nestle India Limited

QSR Quick Service Restaurant

SBD Secondary Business District

SWOT Strengths-Weakness-Opportunity-Threats

Westlife Development Westlife Development Limited

YUM! Brands YUM! Brands, Inc.

Conventional and General Terms or Abbreviations

Term Description

AGM Annual General Meeting

AIF Alternative Investment Fund as defined in and registered with SEBI under the Securities and Exchange Board of India (Alternative Investments Funds)

14

Term Description

Regulations, 2012

AMFI Association of Mutual Funds in India

AS/ Accounting Standards Accounting Standards issued by the Institute of Chartered Accountants of India

ATM Automated Teller Machine

Bn/ bn Billion

BOT Build, operate and transfer

BOOT Build, operate, own and transfer

BSE BSE Limited

CAGR Compounded Annual Growth Rate

Category I Foreign Portfolio Investors

FPIs who are registered as “Category I foreign portfolio investors” under the SEBI FPI Regulations

Category II Foreign Portfolio Investors

FPIs who are registered as “Category II foreign portfolio investors” under the SEBI FPI Regulations

Category III Foreign Portfolio Investors

FPIs who are registered as “Category III foreign portfolio investors” under the SEBI FPI Regulations

CCTV Closed Circuit Television

CDSL Central Depository Services (India) Limited

CENVAT Central Value Added Tax

CESTAT Customs, Excise and Service Tax Appellate Tribunal

CIN Corporate Identity Number

CIT Commissioner of Income Tax

Coffee Board Indian Coffee Market Expansion Board

Companies Act Companies Act, 1956 and Companies Act, 2013, as applicable

Companies Act, 1956 Companies Act, 1956 (without reference to the provisions thereof that have ceased to have effect upon notification of the sections of the Companies Act, 2013) along with the relevant rules made thereunder

Companies Act, 2013 Companies Act, 2013, to the extent in force pursuant to the notification of sections of the Companies Act, 2013, along with the relevant rules made thereunder

CSR Corporate Social Responsibility

Depositories NSDL and CDSL

Depositories Act The Depositories Act, 1996

DIN Director Identification Number

15

Term Description

DP ID Depository Participant’s Identification

DP/ Depository Participant A depository participant as defined under the Depositories Act

EGM Extraordinary General Meeting

EPS Earnings Per Share

Equity Listing Agreement Listing Agreement to be entered into with the Stock Exchanges on which the Equity Shares of our Company are to be listed

EURIBOR Euro Interbank Offered Rate

FCRR Forward Contracts (Regulation) Rules, 1954

FCNR Foreign Currency Non-Resident

FDI Foreign Direct Investment

FEMA Foreign Exchange Management Act, 1999, read with rules and regulations thereunder

FEMA Regulations FEMA (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2000 and amendments thereto

FII(s) Foreign Institutional Investors as defined under the SEBI FPI Regulations

Financial Year/ Fiscal/ FY Unless stated otherwise, the period of 12 months ending March 31 of that particular year

FIPB Foreign Investment Promotion Board

FMC Forward Markets Commission

Food Authority Food Safety and Standards Authority of India

FPI(s) A Foreign Portfolio Investor as defined under the SEBI FPI Regulations

FVCI Foreign Venture Capital Investors as defined and registered under the SEBI FVCI Regulations

GDP Gross Domestic Product

GIR General Index Register

GoI or Government Government of India

HUF Hindu Undivided Family

ICAI The Institute of Chartered Accountants of India

IFRS International Financial Reporting Standards

Income Tax Act The Income Tax Act, 1961

Ind AS Indian Accounting Standards

India Republic of India

Indian GAAP Generally Accepted Accounting Principles in India

16

Term Description

IPO Initial public offering

IRDA Insurance Regulatory and Development Authority

ISO International Organisation for Standardization

IST Indian Standard Time

IT Information Technology

LEED Leadership in Energy & Environmental Design

LIBOR London Interbank Offered Rate

Mn Million

MSE Madras Stock Exchange Limited

N.A./ NA Not Applicable

NAV Net Asset Value

NBFC Non-banking financial company registered with the RBI

NECS National Electronic Clearing Services

NEFT National Electronic Fund Transfer

Notified Sections The sections of the Companies Act, 2013 that were notified by the Ministry of Corporate Affairs, Government of India

NR Non-resident

NRE Account Non Resident External Account

NRI A person resident outside India, who is a citizen of India or a person of Indian origin, and shall have the meaning ascribed to such term in the Foreign Exchange Management (Deposit) Regulations, 2000

NRO Account Non Resident Ordinary Account

NSDL National Securities Depository Limited

NSE The National Stock Exchange of India Limited

OCB/ Overseas Corporate Body

A company, partnership, society or other corporate body owned directly or indirectly to the extent of at least 60% by NRIs including overseas trusts, in which not less than 60% of beneficial interest is irrevocably held by NRIs directly or indirectly and which was in existence on October 3, 2003 and immediately before such date had taken benefits under the general permission granted to OCBs under FEMA. OCBs are not allowed to invest in the Issue

p.a. Per annum

P/E Ratio Price/ Earnings Ratio

PAN Permanent Account Number

PAT Profit After Tax

17

Term Description

PCB Pollution Control Board

RBI The Reserve Bank of India

RoC Registrar of Companies, Bengaluru

RoHS Restriction of the use of Certain Hazardous Substances

`/ Rs./ Rupees/ INR Indian Rupees

RTGS Real Time Gross Settlement

SCRA Securities Contracts (Regulation) Act, 1956

SCRR Securities Contracts (Regulation) Rules, 1957

SEBI The Securities and Exchange Board of India constituted under the SEBI Act, 1992

SEBI Act Securities and Exchange Board of India Act, 1992

SEBI AIF Regulations Securities and Exchange Board of India (Alternative Investments Funds) Regulations, 2012

SEBI Depository Regulations Securities and Exchange Board of India (Depositories and Participants)Regulations, 1996

SEBI FII Regulations Securities and Exchange Board of India (Foreign Institutional Investors) Regulations, 1995

SEBI FPI Regulations Securities and Exchange Board of India (Foreign Portfolio Investors) Regulations, 2014

SEBI FVCI Regulations Securities and Exchange Board of India (Foreign Venture Capital Investors) Regulations, 2000

SEBI ICDR Regulations Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009

SEBI VCF Regulations Securities and Exchange Board of India (Venture Capital Fund) Regulations, 1996

Securities Act U.S. Securities Act, 1933

SEZ Special Economic Zone

SEZ Board The Board of Approval set up under the SEZ Act

Sq. ft./ sq.ft. Square feet

STT Securities Transaction Tax

State Government The government of a state in India

Stock Exchanges The BSE and the NSE

Takeover Regulations Securities and Exchange Board of India (Substantial Acquisition of Shares and Takeovers) Regulations, 2011

18

Term Description

TAN Tax Deduction Account Number

UK United Kingdom

U.S./ USA/ United States United States of America

US GAAP Generally Accepted Accounting Principles in the United States of America

USD/ US$ United States Dollars

VAT Value Added Tax

VCFs Venture Capital Funds as defined in and registered with SEBI under the SEBI VCF Regulations

The words and expressions used but not defined herein shall have the same meaning as is assigned to such terms under the SEBI ICDR Regulations, the Companies Act, the SCRA, the Depositories Act and the rules and regulations made thereunder.

Notwithstanding the foregoing, terms in the sections “Statement of Tax Benefits”, “Financial Statements” and“Main Provisions of Articles of Association” on pages 144, 285 and 541, respectively, shall have the meaning given to such terms in such sections.

19

PRESENTATION OF FINANCIAL, INDUSTRY AND MARKET DATA

Certain Conventions

All references in this Prospectus to “India” are to the Republic of India, all references to the “U.S.” or “USA/United States” are to the United States of America.

Unless stated otherwise, all references to page numbers in this Prospectus are to the page numbers of this Prospectus.

Financial Data

Unless stated otherwise, the financial data in this Prospectus is derived from: i) the Restated ConsolidatedFinancial Information and Restated Standalone Financial Information of our Company, as at and for the financial years ended March 31, 2011, 2012, 2013, 2014, 2015 and as at and for the three month period ended June 30, 2015; and ii) the Restated Consolidated Financial Information of CDGL, as at and for the financialyears ended March 31, 2011, 2012, 2013, 2014, 2015 and as of and for the three month period ended June 30, 2015, prepared in accordance with sub-clause (i), (ii) and (iii) of clause (b) of sub-section (1) of section 26 of Chapter III of the Companies Act, 2013 read with rule 4 of the Companies (Prospectus and Allotment of Securities) Rules, 2014 and Indian GAAP, and restated in accordance with the SEBI ICDR Regulations.

In this Prospectus, any discrepancies in any table between the total and the sums of the amounts listed are due to rounding off. All figures in decimals have been rounded off to the second decimal and all percentage figures have been rounded off to two decimal places and accordingly there may be consequential changes in this Prospectus.

Our Company’s financial year commences on April 1 and ends on March 31 of the next year; accordingly, all references to a particular financial year, unless stated otherwise, are to the 12 month period ended on March 31of that year.

There are significant differences between Indian GAAP, US GAAP and IFRS. Our Company does not provide reconciliation of the financial information included in this Prospectus to IFRS or US GAAP. Our Company has not attempted to explain those differences or quantify their impact on the financial data included in this Prospectus and it is urged that you consult your own advisors regarding such differences and their impact on financial data included in this Prospectus. For details in connection with risks involving differences between Indian GAAP and IFRS, see “Significant differences exist between Indian GAAP and other accounting principles, such as U.S. GAAP and IFRS, which may be material to investors’ assessments of our financial condition” contained in this Prospectus on page 59. Accordingly, the degree to which the financial information included in this Prospectus will provide meaningful information is entirely dependent on the reader’s level of familiarity with Indian accounting policies and practices, the Companies Act and the SEBI ICDR Regulations. Any reliance by persons not familiar with Indian accounting policies and practices on the financial disclosures presented in this Prospectus should accordingly be limited.

Unless the context otherwise indicates, any percentage amounts, as set forth in the sections “Risk Factors”, “OurBusiness” and “Management’s Discussion and Analysis of Financial Conditional and Results of Operations” onpages 24, 175 and 286 respectively, and elsewhere in this Prospectus have been calculated on the basis of theRestated Financial Information of our Company and the Restated Consolidated Financial Information of CDGL,prepared in accordance with Indian GAAP and the Companies Act, 2013 and restated in accordance with the SEBI ICDR Regulations.

Currency and Units of Presentation

All references to:

“CZK” to Czech Koruna, the official currency of Czech Republic;

“€” to Euro, the official currency of European Union;

“HKD” to Hong Kong Dollar, the official currency of Hong Kong;

“Rupees” or “`” or “INR” or “Rs.” are to Indian Rupee, the official currency of the Republic of India;

20

“SGD” to the Singapore Dollar, the official currency of Republic of Singapore;

“USD” or “US$” are to United Sates Dollar, the official currency of the United States; and

“GBP” or “£” are to the British Pound, the official currency of United Kingdom.

Our Company has presented certain numerical information in this Prospectus in “million” units. One million represents 1,000,000 and one billion represents 1,000,000,000.

Exchange Rates

This Prospectus contains conversions of certain other currency amounts into Indian Rupees that have been presented solely to comply with the SEBI ICDR Regulations. These conversions should not be construed as a representation that these currency amounts could have been, or can be converted into Indian Rupees, at any particular rate or at all.

The following table sets forth, for the periods indicated, information with respect to the exchange rate between the Rupee and (i) CZK (in Rupees per CZK); (ii) the € (in Rupees per EUR); (iii) the HKD (in Rupees per HKD); (iv) the SGD (in Rupees per SGD); (v) the USD (in Rupees per USD); and (vi) the GBP (in Rupees per GBP):

Currency As on March 31, 2013(`̀)

As on March 31, 2014(`)

As on March 31, 2015(`)

As on June 30, 2015(`)

1 CZK 2.71 3.00 2.43 2.601 EUR 69.54 82.58 67.51 71.201 HKD 6.99 7.72 8.06 8.211 SGD 43.71 47.50 45.46 47.271 USD 54.39 60.10 62.59 63.751 GBP 82.32 99.85 92.46 100.12Sources: Bloomberg, RBI website

In case March 31 of any of the respective years is a public holiday, the previous calendar day not being a public holiday has been considered

Land, Property and Units of Presentation

Our Company has presented units of land and property in this Prospectus in ‘Acres’ and ‘square feet’, as the case may be.

Industry and Market Data

Unless stated otherwise, industry and market data used in this Prospectus has been obtained or derived from publicly available information as well as industry publications and sources.

Industry publications generally state that the information contained in such publications has been obtained from publicly available documents from various sources believed to be reliable but their accuracy and completenessare not guaranteed and their reliability cannot be assured. Although we believe the industry and market data used in this Prospectus is reliable, it has not been independently verified by us or the GCBRLMs or the BRLMsor any of their affiliates or advisors. The data used in these sources may have been reclassified by us for the purposes of presentation. Data from these sources may also not be comparable. Such data involves risks, uncertainties and numerous assumptions and is subject to change based on various factors, including those discussed in the section “Risk Factors” on page 24. Accordingly, investment decisions should not be based solely on such information.

In accordance with the SEBI ICDR Regulations, the section “Basis for the Issue Price” on page 140 includesinformation relating to our peer group companies. Such information has been derived from publicly available sources, and neither we, nor the GCBRLMs or the BRLMs have independently verified such information.

Further, in accordance with Regulation 51A of the SEBI ICDR Regulations, our Company may be required to undertake an annual updation of the disclosures made in this Prospectus and make it publicly available in the manner specified by SEBI.

21

The extent to which the market and industry data used in this Prospectus is meaningful depends on the reader’sfamiliarity with and understanding of the methodologies used in compiling such data. There are no standard data gathering methodologies in the industry in which the business of our Company is conducted, and methodologies and assumptions may vary widely among different industry sources.

22

FORWARD-LOOKING STATEMENTS

This Prospectus contains certain “forward-looking statements”. These forward-looking statements generally can be identified by words or phrases such as “aim”, “anticipate”, “believe”, “expect”, “estimate”, “intend”,“objective”, “plan”, “project”, “will”, “will continue”, “will pursue” or other words or phrases of similar import. Similarly, statements that describe our Company’s strategies, objectives, plans or goals are also forward-lookingstatements. All forward-looking statements are subject to risks, uncertainties and assumptions about us that could cause actual results to differ materially from those contemplated by the relevant forward-lookingstatement.

Actual results may differ materially from those suggested by the forward-looking statements due to risks or uncertainties associated with the expectations with respect to, but not limited to, regulatory changes pertainingto the industries in India in which our Company has businesses and its ability to respond to them, its ability to successfully implement its strategy, its growth and expansion, technological changes, its exposure to market risks, general economic and political conditions in India which have an impact on its business activities or investments, the monetary and fiscal policies of India, inflation, deflation, unanticipated turbulence in interest rates, foreign exchange rates, equity prices or other rates or prices, the performance of the financial markets in India and globally, changes in domestic laws, regulations and taxes and changes in competition in its industry. Important factors that could cause actual results to differ materially from our Company’s expectations include, but are not limited to, the following:

Our dependence on our ownership interests in our Subsidiaries to generate revenues and a lack of substantial operations and fixed assets within our Company.

Our Company’s indebtedness and any failure in the future to comply with the restrictive covenants under our loan agreements.

Dilution of our equity shareholding in CDGL and direct or indirect shareholding in other Subsidiaries.

Our inability to maintain and enhance the value of our brand and our customers’ connect with ourbrand, “Coffee Day” and “Café Coffee Day”.

The risks associated with leasing out premises for the operation of our Café Network outlets and the lack of stamped and registered lease agreements for the same.

Our inability to open new café outlets, penetrate deeper into existing geographic locations, expand our vending machine business and increase our exports and trading of coffee beans.

Downturn in the performance of the real estate market and information technology sector, in India and particularly in Bengaluru and Mangaluru.

Our inability to attract and retain key tenants at attractive rentals at our technology parks, inability tomaintain the attractiveness of our locations and any failure of our tenants’ businesses.

Any fall in global trading volumes, regional and global economic, instability in financial and political conditions and our dependence on a smaller number of customers for a significant portion of our logistics business.

Our inability to fund periodic capital expenditure, convert our existing terminal facilities and leasedvehicles and certain properties for operating our logistics business.

Inadequacy of our risk management policies and procedures to identify, monitor and manage risks in the financial services business.

The uncertainties associated with the financial services industry, including, fluctuating revenues and downturns and disruptions in the securities markets.

Any deterioration in the quality or reputation of the brand “The Serai” and the seasonal and cyclicalvolatility in the resorts business.

23

Our failure to obtain and periodically renew applicable permits and approvals to operate our businesses.

For further discussion of factors that could cause the actual results to differ from the expectations, see sections“Risk Factors”, “Our Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on pages 24, 175 and 286, respectively. By their nature, certain market risk disclosures are only estimates and could be materially different from what actually occurs in the future. As a result, actual gains or losses could materially differ from those that have been estimated.

We cannot assure investors that the expectations reflected in these forward-looking statements will prove to be correct. Given these uncertainties, investors are cautioned not to place undue reliance on such forward-lookingstatements and not to regard such statements as a guarantee of future performance.

Forward-looking statements reflect the current views of our Company as of the date of this Prospectus and are not a guarantee of future performance. These statements are based on the management’s beliefs and assumptions, which in turn are based on currently available information. Although we believe the assumptionsupon which these forward-looking statements are based are reasonable, any of these assumptions could prove to be inaccurate, and the forward-looking statements based on these assumptions could be incorrect. Neither our Company, our Directors, the GCBRLMs, the BRLMs nor any of their respective affiliates have any obligation to update or otherwise revise any statements reflecting circumstances arising after the date hereof or to reflect the occurrence of underlying events, even if the underlying assumptions do not come to fruition. In accordance with SEBI requirements, our Company, the GCBRLMs and the BRLMs will ensure that investors in India are informed of material developments until the time of the grant of listing and trading permission by the StockExchanges.

24

SECTION II: RISK FACTORS

Prospective investors should pay particular attention to the fact that our Company is incorporated under the laws of India and is subject to a legal and regulatory environment which may differ in certain respects from that of other countries. In making an investment decision, prospective investors must rely on their own examination of our Company and the terms of the Issue including the merits and risks involved in the investment. You should consult your tax, financial and legal advisors regarding particular consequences to you of investing in this Issue. This Prospectus also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the considerations described below and elsewhere in this Prospectus. Please see section “Forward-Looking Statements” on page 22.

Unless specified or quantified in the relevant risks factors below, we are not in a position to quantify the financial or other implication of any of the risks described in this section. Unless otherwise stated, the financial information of our Company used in this section has been derived from the Consolidated Financial Statements.

In this section, unless the context otherwise requires, references to “our Company” or to “the Company” refersto Coffee Day Enterprises Limited (“CDEL”) and/ or Coffee Day Global Limited (“CDGL”) and a reference to “we” or “us” or “our” refers to CDEL and/ or CDGL, our Subsidiaries, Joint Ventures and Associates. References to a “Financial Year” are to the 12 months ended March 31 of that year.

Risks Relating to Our Business and Our Industry

An investment in our Equity Shares involves risks. You should carefully review all of the information in this document and, in particular, the risks described below as they identify important factors that could cause our actual results to differ materially from our forward-looking statements and historical trends.

The following describes some of the significant risks that could affect us and the value of our Equity Shares. Additionally, some risks may be unknown to us and other risks, which we currently believe to be immaterial, could turn out be material in the future. All of these could materially adversely affect our business, financial condition, results of operations and prospects. You should also consider the information provided below inconnection with the forward-looking statements in this document and the warning statement regarding forward-looking statements at the beginning of this document.

If any of the following risks, or other risks that are not currently known or are now deemed immaterial, actually occur, our business, results of operations and financial condition could suffer. As a result, the trading price of, and the value of your investment in, our Equity Shares could decline, and all or part of your investment may be lost.

A. Risk Relating to Our Businesses

1. Our operations are conducted through our Subsidiaries. Therefore, our ability to pay dividends on the Equity Shares depends on our ability to obtain cash dividends or other cash payments from our Subsidiaries.

We currently conduct a substantial portion of our coffee and non-coffee business operations through our Subsidiaries. As our Company has no substantial operations or fixed assets, we have no significant sources of revenue other than the ownership interests in our Subsidiaries. Our Company’s income is therefore largely dependent on investment income and dividends from our Subsidiaries. As of June 30, 2015, our Company had 40 Subsidiaries. Our top four business segments, namely coffee business, logistics, financial services and technology parks contributed 51.64%, 33.04%, 8.97% and 4.07%,respectively, of our consolidated revenues for Financial Year 2015, and 54.45%, 25.57%, 12.97% and 4.61% for the three month period ended June 30, 2015, respectively.

The ability of our Subsidiaries to generate equity and investment returns and pay dividends depends on the success of their business operations, financial condition and ability to generate profits. In addition, our Subsidiaries may be restricted from giving us equity returns or paying dividends by contract, including financing arrangements, charter provisions, partners of the Subsidiaries or by the applicable laws and regulations of the various countries in which they operate.

We may not be able to monetize our investments in the Subsidiaries and may not derive fair value fromour investments. Therefore, eventually we may not be able to derive any investment income from the

25

Subsidiaries. Further, we cannot assure you that our Subsidiaries will generate sufficient profits and cash flows, or otherwise will prove willing or able to pay dividends to our Company. The inability of one or more of these entities to pay dividends could have a material adverse effect on our business, prospects, results of operations, cash flows and financial condition. In addition, our financial conditionand results of operations could be adversely affected should our equity stake in our Subsidiaries be diluted or in the event that they cease to be our Subsidiaries, which could in turn adversely affect our financial condition.

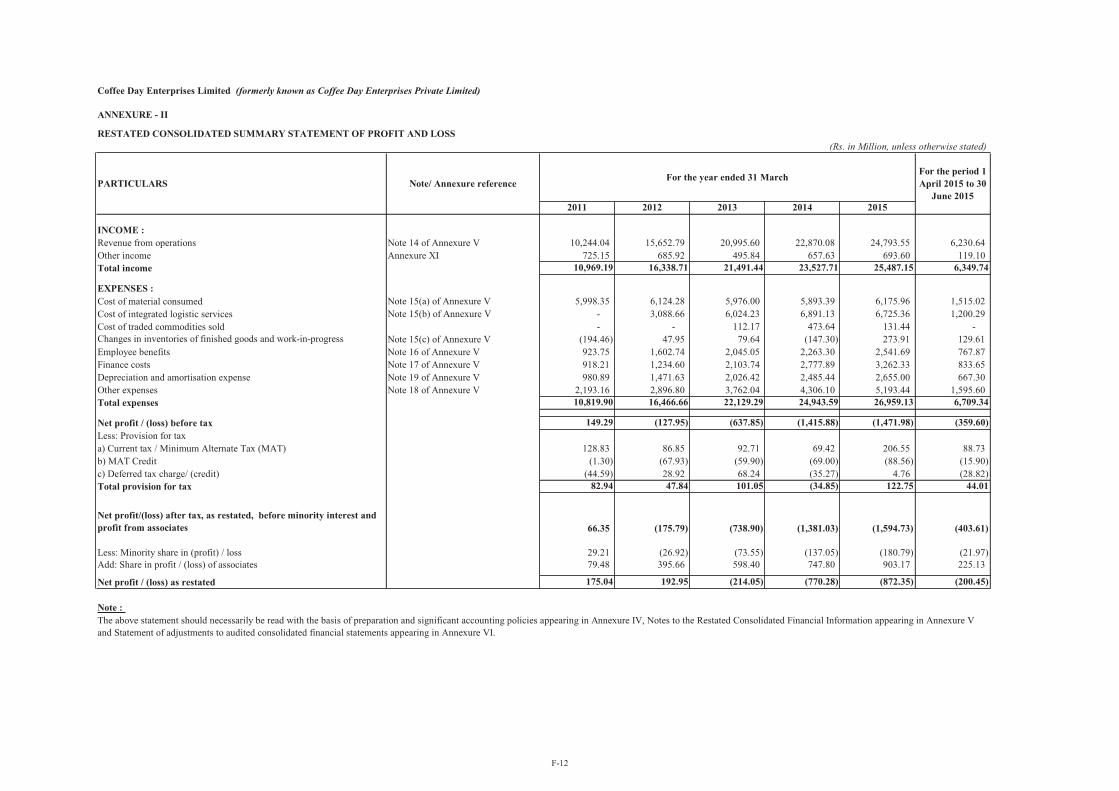

2. Our Company incurred losses in Financial Years 2013, 2014 and 2015, and the three month period ended June 30, 2015, which may adversely affect our business and financial performance.

We incurred losses on a consolidated basis for the Financial Years 2013, 2014 and 2015, and the threemonth period ended June 30, 2015 of `214.05 million, `770.28 million, `872.35 million and `200.45million, respectively. We cannot assure you that we will not incur losses in the future and any such losses could adversely affect our business and financial performance. Our consolidated financial results are on account of the result of operations of our various businesses undertaken through our subsidiaries. Based on the Restated Consolidated Financial Information for the Financial Years 2013,2014 and 2015, and the three month period ended June 30, 2015, the losses incurred by our Subsidiaries for the periods indicated are as below:

(in `million)Sr.No.

Business segment Segment results (losses)Financial Year Three month period

ended June 30, 20152013 2014 20151. Leasing of

commercial office space

(76.39) 172.62 181.00 124.01

2. Hospitalityservices*

(40.83) (38.59) (23.31) 10.09

3. Financial services (46.80) (7.03) 139.42 37.47*Including Company

In addition, our return on net worth has shown a downward trend, which stood at (3.29)% for the Fiscal Year ended March 31, 2013, (13.85)% for the Fiscal Year ended March 31, 2014, (16.39)% for the Fiscal Year ended March 31, 2015 and (4.39)% for the three month period ended June 30, 2015.

We cannot assure you that we will not incur losses in the future and any such losses could adversely affect our business and financial performance. For details, see section “Financial Information” on page285.

3. Our consolidated net indebtedness and our failure to comply with certain restrictive covenants under our loan agreements could adversely affect our financial condition and results of operations.

As of June 30, 2015, our consolidated net indebtedness totaled `27,622.47 million (total debt in accordance with the restated consolidated financials less convertible debentures, less loans from related parties and cash and bank balance including fixed deposit and margin money deposit with bank). We have entered into agreements for short-term and long-term loans and other borrowings. Some of these agreements contain requirements to maintain certain security margins, financial ratios and contain restrictive covenants relating to issuance of new shares, changes in capital structure, making material changes to constitutional documents, implementing any expansion scheme, incurring further indebtedness, encumbrances on or disposal of assets, paying dividends and making investments over certain thresholds. For further details, see section “Financial Indebtedness - Covenants” on page 414.Furthermore, some of our financing arrangements specify that upon the occurrence of an event of default, the lender shall have the right to, inter alia, cancel the outstanding facilities available for drawdown, declare the loan to be immediately due and payable with accrued interest and enforce rights over the security created. There can be no assurance that we will be able to comply with these financial or other covenants, or that we will be able to obtain the consents necessary to proceed with the actionswhich we believe are necessary to operate and grow our business, which may in turn have a material adverse effect on our business and operations.

26