coal-as fuel option

DESCRIPTION

Coal-As Fuel Option. R.L. Mattoo GM (Fuel Management), NTPC. Synopsis. Power sector scenario Fuel Options Coal as viable fuel Issues and way forward. Power Infrastructure In India. As on Dec .’05. PRESENT CAPACITY MIX FUELWISE. INDIAN POWER SECTOR. - PowerPoint PPT PresentationTRANSCRIPT

Coal-As Fuel Option

R.L. MattooGM (Fuel Management), NTPC

Synopsis

• Power sector scenario

• Fuel Options

• Coal as viable fuel

• Issues and way forward

Power Infrastructure In India As on Dec .’05

5.00%2.70%

9.90%

0.90%

55.60%

25.90%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

PRESENT CAPACITY MIX FUELWISE

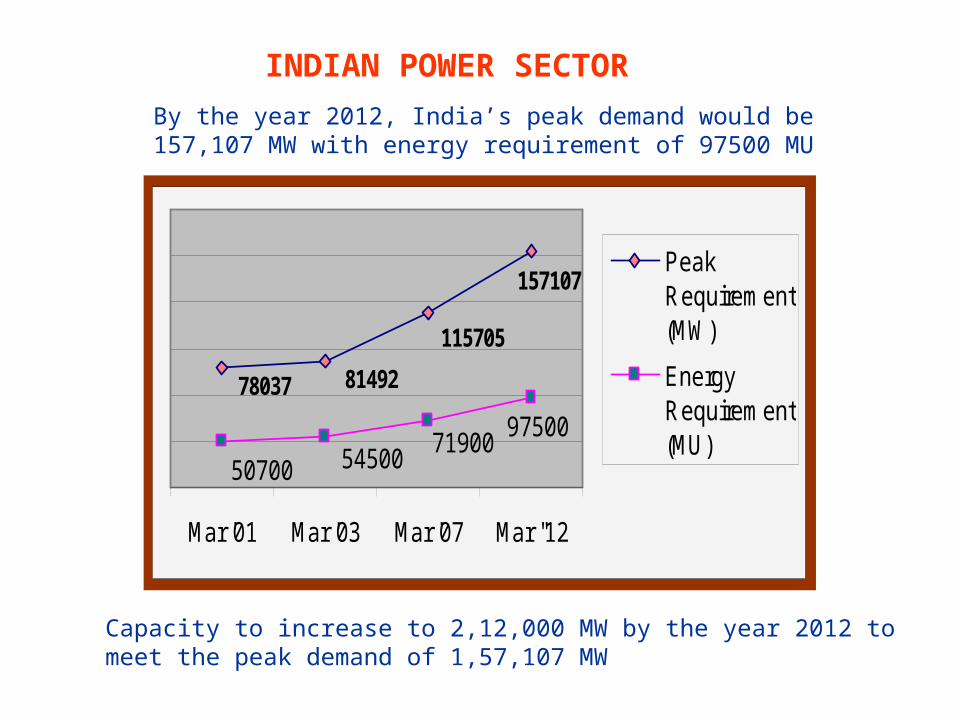

9750071900

5450050700

78037 81492

115705

157107

Mar '01 Mar '03 Mar '07 Mar ''12

PeakRequirement(MW)

EnergyRequirement(MU)

INDIAN POWER SECTOR

Capacity to increase to 2,12,000 MW by the year 2012 to meet the peak demand of 1,57,107 MW

By the year 2012, India’s peak demand would be 157,107 MW with energy requirement of 97500 MU

11th Plan : Capacity Addition Plan

Tentative/- type wise

Type Total (MW)

Hydro 12,000

Thermal 46905

Indigenous Coal 28155

Imported Coal 10000

Lignite 1750

Gas/ LNG 7000

Nuclear 3160

Total 62065

Factors Affecting Choice of Fuels

• Fuel Options determinants:

– Availability– Affordability– Reliability– Environment friendliness

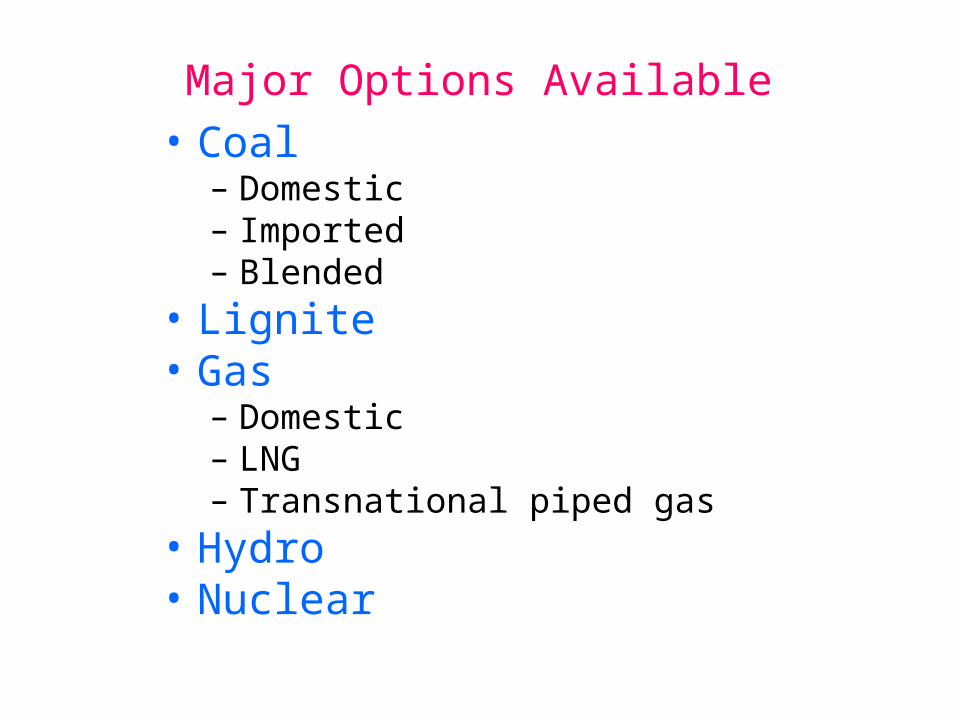

Major Options Available

• Coal– Domestic– Imported– Blended

• Lignite• Gas

– Domestic– LNG– Transnational piped gas

• Hydro • Nuclear

16.5 13.5 2.1

76 103.5 35.5

92.5 117 37.4

0%

10%20%

30%

40%50%

60%

70%

80%90%

100%

Proved Indicated Inferred

Total

Non Coking

Coking

COAL RESERVES IN INDIA (Billion Tes)

STATUS AS ON 1.1.05

At the present rate of extraction, coal and lignite resources in India are expected to last for about 140 years

91.69156.15 247.84

30.0322.21 52.24

0%

20%

40%

60%

80%

100%

CIL Others Total

Extractable Reserves

Total Reserves

EXTRACTABLE COAL RESERVES IN INDIA

FIG IN BILLION TONNES

LIGNITE

Reserves

Around 30,300 million tes

Location

About 88% of reserves located in state of Tamil Nadu

Balance (about 12%) located in Rajasthan, Gujarat, J&K & Kerala

Limitation – Suitable only for pit head generation

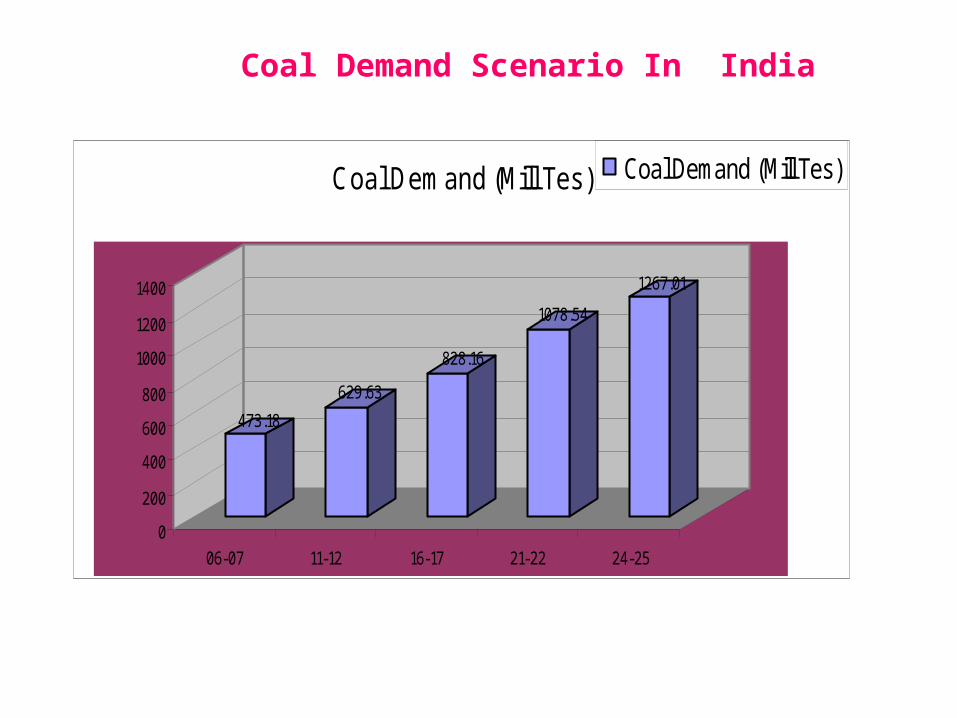

Coal Demand Scenario In India

473.18

629.63

828.16

1078.54

1267.01

0

200

400

600

800

1000

1200

1400

06-07 11-12 16-17 21-22 24-25

Coal Demand (Mill Tes) Coal Demand (Mill Tes)

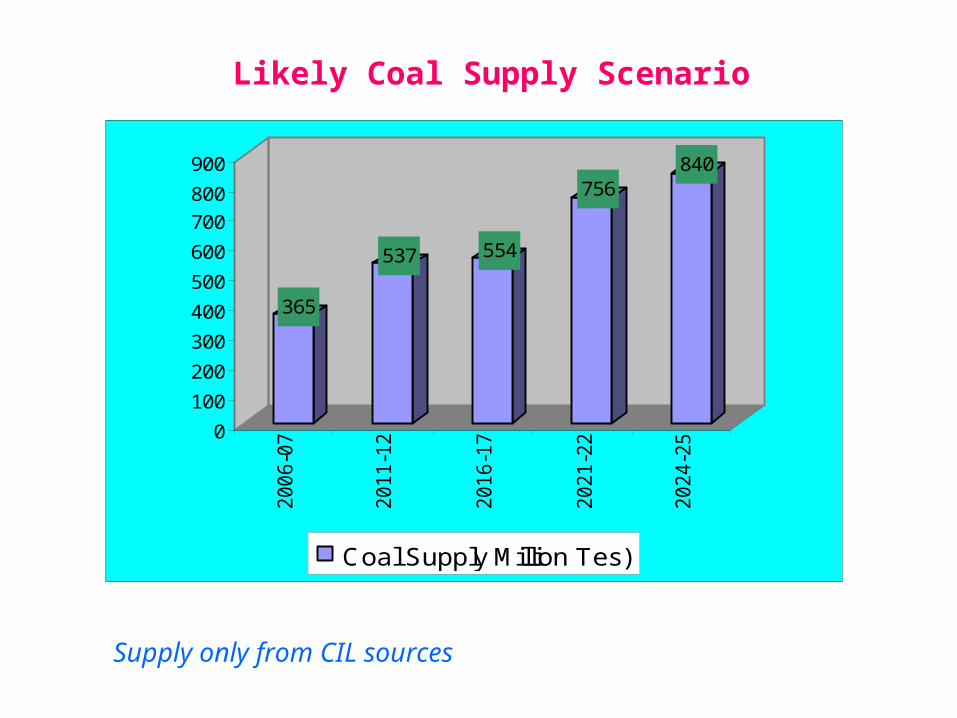

365

537 554

756840

0

100

200

300

400

500

600

700

800

900

2006-0

7

2011-1

2

2016-1

7

2021-2

2

2024-2

5

Coal Supply Million Tes)

Likely Coal Supply Scenario

Supply only from CIL sources

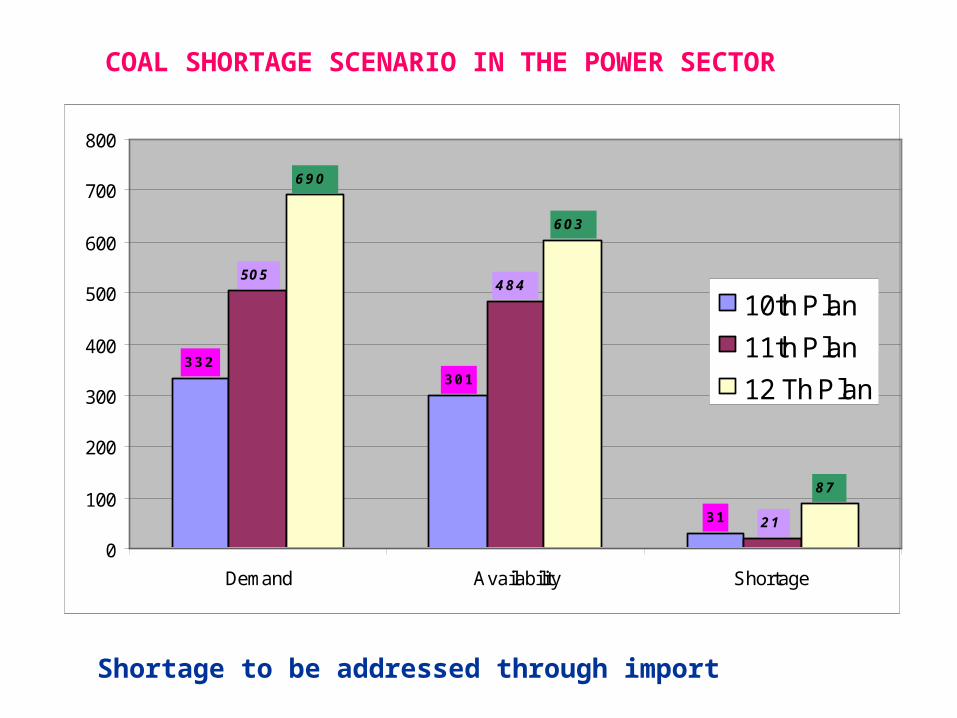

332301

31

505484

21

690

603

87

0

100

200

300

400

500

600

700

800

Demand Availability Shortage

10th Plan

11th Plan

12 Th Plan

COAL SHORTAGE SCENARIO IN THE POWER SECTOR

Shortage to be addressed through import

Coal shortage envisaged due to:Coal shortage envisaged due to:

•Long term linkage accorded on normative PLF Long term linkage accorded on normative PLF of 68.5% and 80% for stations coming after of 68.5% and 80% for stations coming after 1996, whereas the national average is +70% 1996, whereas the national average is +70% PLF. (some of the stations like those of NTPC PLF. (some of the stations like those of NTPC operating at +90% PLF)operating at +90% PLF)

•Delay in development of linked minesDelay in development of linked mines

COAL AVAILABILITY vis-à-vis SHORTAGECOAL AVAILABILITY vis-à-vis SHORTAGE

RESULT - NEED TO AUGMENT COAL AVAILABILITY

INDIGENOUS FUEL RESOURCES: GAS

LOCATION BALANCE RECOVERABLE RESERVE (As of 1st April

2005)•ONSHORE 340 BCM•OFFSHORE 761 BCMGRAND TOTAL 1101 BCM

(MOP&NG Basic statistics)

GAS RESERVES ARE ADEQUATE ONLY FOR ABOUT 34 YEARS AT PRESENT LEVEL OF GAS CONSUMPTION.

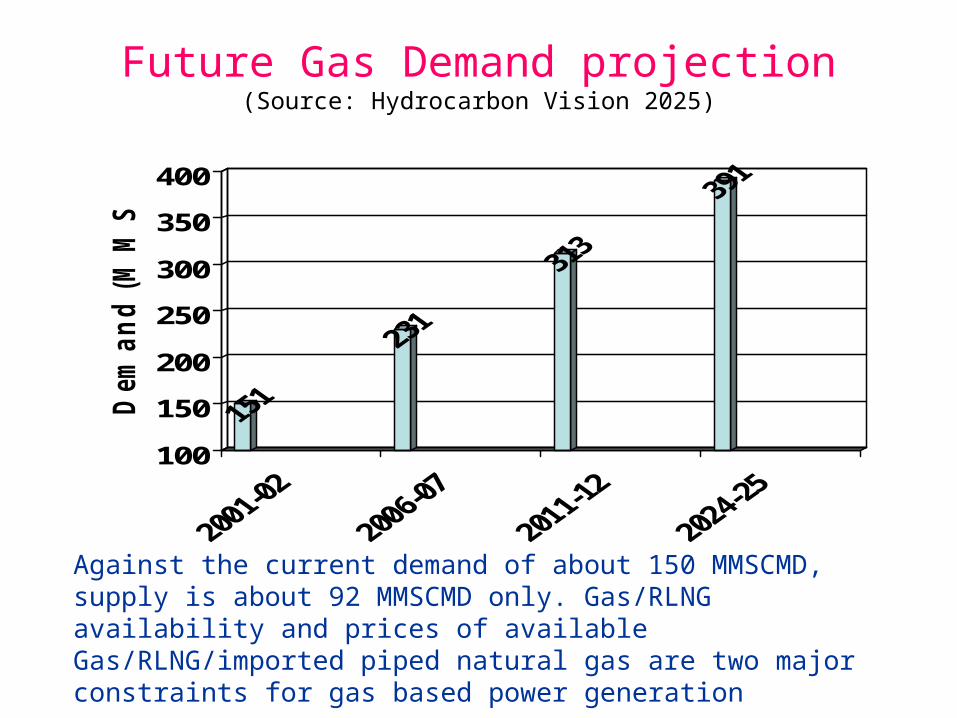

Future Gas Demand projection(Source: Hydrocarbon Vision 2025)

100

150

200

250

300

350

400

Dem

an

d (

MM

SC

MD

)

Against the current demand of about 150 MMSCMD, supply is about 92 MMSCMD only. Gas/RLNG availability and prices of available Gas/RLNG/imported piped natural gas are two major constraints for gas based power generation

•Fixed cost of Generation for coal based & Gas Based Plants are comparable.•Thus,for Gas/R LNG to compete – it has to be on fuel cost component basis

Price Benchmark - Coal - the Competing Fuel contdcontd……

Fixed cost of Generation (Levelized)

0.875

0.89

Coal Proj. Gas Proj.

Figs in Rs/kwhFigs in Rs/kwh

Assumptions: Coal Proj Gas ProjCapital Cost 42 32(Rs Million /MW)Life (Years) 25 15

0

20

40

60

80

100

120

140

0 100 500 1000 1500Distance from mine (Kms)

Fuel

cost

(pai

se/ k

wh)

Washed

Raw

0.5

1.11.6

2.1

0.0

2.6

3.6

3.1

Gas ($/MMBTU)

Variable (Fuel) cost of Generation

OTHER INDIGENOUS FUEL RESOURCES:LIMITATIONS

Other resources like crude oil, coal bed methane, renewable energy sources etc. are meagre and not capable of catering to our energy requirements in the long run.

Gas and crude oil prices are volatile in the international market and coal import is a much cheaper option than import of oil and gas especially at coastal locations.

Conclusion - Coal is likely to remain our mainstay fuel for energy generation till 2031-32. However, current shortage is a cause of concern.

Coal Shortage – The Way Forward• Stepping up domestic coal production by allotting blocks

to central and state public sector units and for captive mines to notified end users

• Coal Import – needs creation of necessary infrastructure.

Will also put pressure on domestic coal industry to be efficient. NTPC has imported about 3 million tes of coal in 2005-06.

• Amendment in Coal Mines Act to facilitate (a) private participation in coal mining for purposes other than those specified and (b) offering of future coal blocks to potential entrepreneurs.

• Technology for economic exploitation of coal lying at greater depths

Issues of concern with the coal sector

• Pricing

– 70% of the domestic coal is dedicated to power generation.

– Fuel cost constitutes about 65% of the total cost of generation

– Since the dismantling of APM, coal prices have been taken for arbitrary escalation with no transparency

– The opening of the sector to private players will bring in competition and prices will be determined by market dynamics

– Till such time, a regulatory mechanism needs to be put in place to put a check on arbitrary price hike.

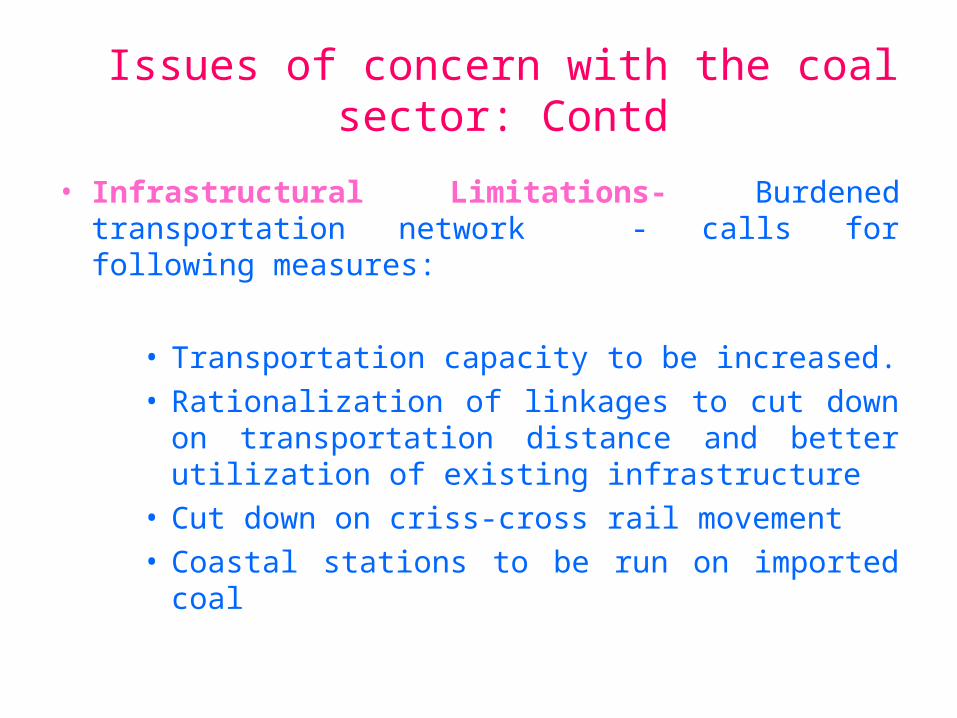

Issues of concern with the coal sector: Contd

• Infrastructural Limitations- Burdened transportation network - calls for following measures:

• Transportation capacity to be increased.• Rationalization of linkages to cut down on

transportation distance and better utilization of existing infrastructure

• Cut down on criss-cross rail movement • Coastal stations to be run on imported coal

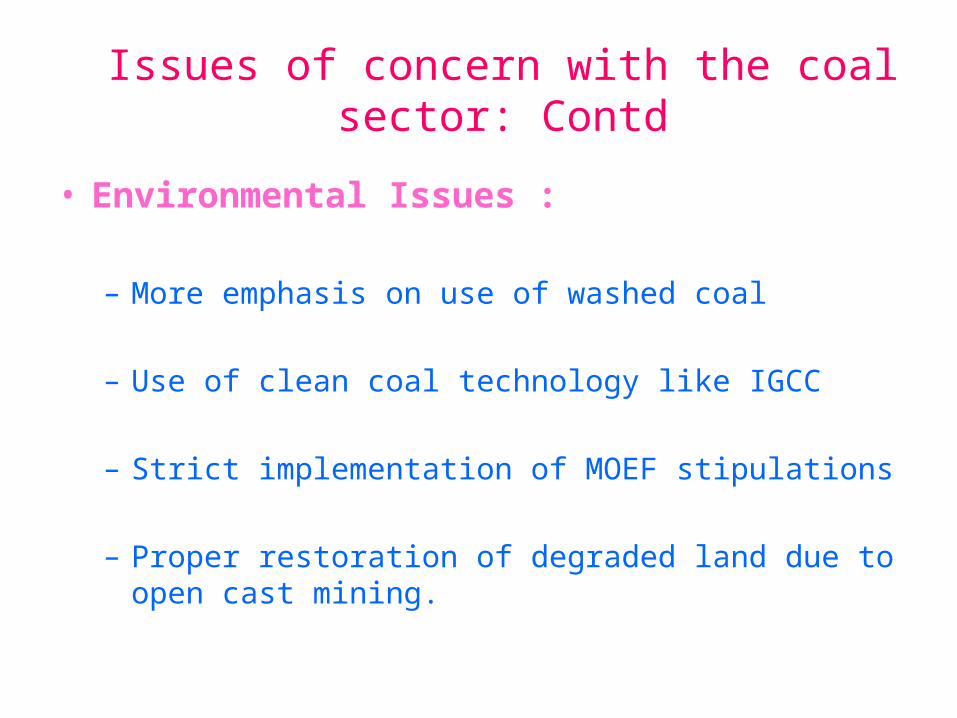

Issues of concern with the coal sector: Contd

• Environmental Issues :

– More emphasis on use of washed coal

– Use of clean coal technology like IGCC

– Strict implementation of MOEF stipulations

– Proper restoration of degraded land due to open cast mining.

Conclusion & Way Forward

• Coal shall remain mainstay for power generation in India.

• Allocation of captive blocks to end users.

• Allowing private participation

• This will also create a competitive environment and which will enable market driven pricing structure.

• Till such time, regulator to be put in place to ensure fair pricing of coal, proper development of infrastructure & efficient utilisation of resources in the coal sector.

• Keeping in view the longer gestation period of coal mines, faster clearances of coal projects needs to be undertaken so as to be commensurate with the commissioning of power plants.

• Coal washing and use of clean coal technology to be promoted.

• Transportation network bottlenecks to be reduced by judicious rationalization of linkages.

THANK YOU