cma students’ bulletin -...

TRANSCRIPT

FOLLOW US ON FOLLOW US ON

THE INSTITUTE OF COST ACCOUNTANTS OF INDIA(Statutory body under an Act of Parliament)

Headquarters: CMA Bhawan, 12, Sudder Street, Kolkata - 700 016Phone: +91-33-2252-1031/34/35/1602/1492/1619/7373/7143

Delhi office: CMA Bhawan, 3, Institutional Area, Lodhi Road, New Delhi - 110 003Phone: +91-11-2462-2156/2157/2158

Behind every successful business decision, there is always a CMA

BulletinBulletinBulletineee

www.icmai.in

VOL: 3, No.: 2 , February , 2018 ISSUECMA STUDENTS’CMA STUDENTS’

FINAL

Behind every successful business decision, there is always a CMA

TOLL FREE 18003450092 / 1800110910TOLL FREE 18003450092 / 1800110910TOLL FREE 18003450092 / 1800110910

For more details visit this Link: For more details visit this Link: For more details visit this Link:

http://icmai.in/NCC-2018/index.htmlhttp://icmai.in/NCC-2018/index.htmlhttp://icmai.in/NCC-2018/index.html

Message from

The Chairman

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

CMA Manas Kumar Thakur

Be a CMA, be a Proud Indian

Chairman,Training & Education Facilities (T& EF) Committee

Dear Students,

'The future belongs to those who believe in the beauty of their dreams'.

'Everyday do something that will inch you closer you to be a better tomorrow' and do it

now, sometimes 'later' becomes 'never'. Push yourself because no one else is going to do

it for you. Hard work beats talent when talent doesn't work hard. Don't stop when you

are tired. Stop when you are done.

Teach me and I will forget, show me and I will learn, involve me and I will understand- I

believe in the statement, hence, the effort of monthly publication of E-bulletin. Try to

utilise the most of it. You are having Mock Test Papers (MTPs), Revisionary Test Papers

(RTPs) and few more resources will get upload shortly. The Directorate of Studies is always

trying to boost up your energy by providing your preparation related materials and

updates. Please try to grab the maximum benefit out of those. Learned academicians are

putting their efforts by preparing those and you should honour their effort too. I sincerely

acknowledge their effort for providing you a better tomorrow.

Trust yourself and strive your progress; not perfection. Remember that 'No one is perfect

that's why pencils have erasers'. Problems are not stop signs they are guidelines. Thus,

running away from your problems is a race you will never win. In the middle of difficulty,

lies opportunity. Please try to believe in 'The capacity to learn is a gift; the ability to

learn is a skill; the willingness to learn is a choice'.

The difference between ordinary and extra-ordinary is just that little 'extra'. So, stay

positive, work hard and make it happen.

You are already aware that th58 National Cost Convention of your beloved

th thInstitute is going to be held on 16 and 17 March,2018 at Vigyan Bhawan, New

Delhi. It is our collective duty to successfully make the event a mega grand event.

Best of luck for your future endeavours,

i

CONTENTS

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Knowledge Update -

Massage from the Chairman -

Group : III Paper 13: Corporate Laws & Compliance (CLC) -

Submissions -

Practical advice -

Snapshots -

Message from the Directorate of Studies -

Group: III Paper 15: Strategic Cost Management- Decision Making (SCMD) -

Group: III Paper 16: Direct Tax Laws and InternationalTaxation (DTI) -

Group: IV Paper 17: Corporate Financial Reporting (CFR) -

Group: IV Paper 18: Indirect Tax Laws & Practice (ITP) -

Group: IV Paper 19: Cost & Management Audit (CMAD) -

Group: IV Paper 20: Strategic Performance Managementand Business Valuation (SPBV) -

Group: III Paper 14: Strategic FinancialManagement (SFM) -

Model Career Planer -

1

2

6

11

15

18

22

26

29

34

32

35

36

39

i

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

In this section of e-bulletin we shall have a series of discussion on each of these chapters to provide a meaningful assistance to the students in preparing themselves for the examination at the short end and equip them with sufficient knowledge to deal with real life complications at the long end.

KNOWLEDGEKNOWLEDGEKNOWLEDGEUpdateUpdateUpdate

1

Your Preparation Quick Takes

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Corporate Laws & Compliance (CLC)

Group - IIIPaper - 13Group - IIIPaper - 13Corporate Laws & Compliance (CLC)

C 20%

A 50%B 30%

Shri Subrata Kr. RoyCompany SecretaryM.S.T.C. Ltd.He can be reached at:[email protected]

2

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Learning Objectives:

Read the Study Material minutely.

For details or if you don't understand Study Material or the section is important to identify the

topic, then refer to Bare Act, otherwise reference to Bare Act is not necessary. For Company Law,

book by Avtar Singh is recommended. For other laws Institute Study Material is sufficient.

The words used in any of the texts as mentioned above should be understood by immediate

reference to the Dictionary.

The main points coming out in any of the provisions should be either underlined or written in

separate copy which has to be repeated again and again.

Theoretical knowledge should be adequate and clear before solving practical problems.

Don't write wrong English. It changes the meaning and therefore answer may be wrong even when

the student's conception is clear. Also don't make spelling mistakes.

6. to grant loans or give guarantee or provide

securities in respect of loans.

7. to approve financial statements and the Board's

report.

8. to diversify the business of the company.

9. to approve amalgamation, merger and

reconstitution.

10. to take over a company or acquire a controlling

or substantial stake in another company.

The following are the duties of Board:

1. A director of a company should act in

accordance with the articles of the company.

2. A director should act in act in good faith in order

to promote the objects of the company for the

benefit of its members, its employees, its

shareholders, itscommunity for the protection

of the environment and in the best interest of the

company.

3. A director shall exercise his duties with due and

reasonable care, skill and diligence and shall

exercise independent judgment.

4. A director shall not involve in a situation in

which he is directly or indirectly interested and

which conflicts with the interest of the company.

5. A director shall not achieve any undue

advantage or gain either by himself or through

his relatives.

6. A director shall not assign his office any

assignment so made will be void.

Managerial Remuneration (Section 197)

The total managerial remuneration payable by a public

company to its directors, whole-time directors and its

managers in respect of any financial year shall not exceed

Functions of the Board

How to answer questions in Examination- General

Advise

1) Don't read the whole question paper: Start writing a

question without wasting time.

2) Answer should be relevant. Read the question

carefully. Don't write whatever you know about the

topic.

3) Don't refer to sections unless you are quite sure

about the same.

4) Language should be clear and understandable.

Don't write wrong English or use wrong spellings.

5) Relate the number allotted against each question.

Normally one page for 5 marks is OK. In case

number allotted is less and you feel the answer will

be bigger then mention the points only.

6) In essay type or long answer, write with paragraphs

and points, so that the examiner finds it easy to

locate the actual answer.

7) Where answer has parts, attempt all answers serially

at one place only.

Powers and Duties of the Board (Section 179 & 166)

The Board of directors shall exercise the following

powers subject to the resolutions passed at the

meeting.

1. to make calls to shareholders in respect of

money unpaid on their shares.

2. toauthorise buy-back of securities under section

68.

3. to issue securities, including securities (in or

outside India)

4. to borrow monies.

5. to invest the funds of the company.

3

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

which at least one should be independent director.

The Board shall ensure that a company spends at least two

percent of the average net profit of the company made during

the three immediately preceding financial years.

Functioning of the Board:

1. Chairman of the Board chairs the meetings of the

Board. If the regular chairman is not present and

Articles of association permit, a director may be

appointed as a chairman of the meeting.

2. Quorum: minimum number of directors to be

present to make the meeting valid. If the quorum is

not present the meeting shall be automatically

adjourned to same place, time and venue on the

same day next week.

3. Each director has one vote. In case of a tie the

Chairman will have a casting vote subject to the

provisions in the Articles of Association.

4. Interested director shall not vote. ( Interest means

personal interest) (disclosure of interest under

section 184 is compulsory at the time of joining)

5. All decisions shall be simple majority decisions.

However unanimous decision shall be taken in case

of;

(a) Inter corporate investments above certain limit.

(b) Appointing any person as an MD of the company if

he is already an MD or a manager of one and not more

than one company .

6. Leave of absence: If a director is absent from 3

consecutive Board meetings without taking leave of

absence he will be disqualified from remaining a

director of the company.

7. Voluntary adjournment; The Board can

voluntarily adjourn its meeting. In case of automatic

adjournment the meeting stands adjourned to next

week same day, same time and same venue unless

another venue is fixed.

8. Adjournment of meeting and of deferment

consideration / decision of an item.

9. One Board meeting in each quarter is a must. No

limit for maximum number of meetings. There shall

not be a gap of 120 days between two meetings.

10. Minimum 7 days notice of the Board meeting must

be given to all directors staying even outside India.

11. Preponement and postponement of meetings can

be done.

Powers of the Board to be exercised only in a Board

meeting i.e. these item cannot be passed by through

resolution by circulation:

eleven-percent of the net profit which is calculated according

to section 198 except the remuneration shall not be deducted

from the gross profit.

The company can also give in also pay in excess of eleven

percent subject to special resolution in general meeting.

Further the company except with the approval of the

company in general meeting-

(i) the remuneration payable to one managing

director, whole-time director and manager

should not be more than of the five percent

net profit of the company and if there is

more than one such director then ten

percent of the net profit to all such directors

and managers taken together.

(ii) the remuneration payable to any other

director who are neither whole-time

director or manager

(A) one percent of the profit if there is a

managing director, whole time

director or a manager.

(B) three percent in any other case.

Political Contribution (Section 182)

A company other than a Government company and a

company which has been in existence for less than three

financial years may directly or indirectly contribute any

amount to political party provided a resolution of the Board

has been passed in this regard.

The aggregate of such amount shall not exceed seven and a

half percent of its net profit during the three immediately

preceding financial years.

The amount so contributed should be shown in the in its P/L

account giving particulars of the total amount contributed

and the name of the party which to which it has contributed.

Corporate Social Responsibility (Section 135)

Every company which has:

(i) a net worth of five hundred crore or more or;

(ii) turnover of one thousand crore or more or;

(iii) net profit of five or more during any

financial year,

shall constitute a Corporate Social Responsibility

committee consisting of three or more directors out of

4

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Most of the powers are to be exercised by the Board in a duly convened meeting. Other powers be exercised by resolution by

circulation. Resolution by circulation means that a resolution in draft.

In the Companies Act, 2013 the consent of majority of directors is needed instead of all directors.

All resolutions passed by circulation shall have to be mandatorily noted in the next board meeting and should be made part of the

minutes.

rdIf 1/3 of the directors want that the resolution have to be decided in the meeting then the chairperson should put the resolution to

be decided in the meeting.

5

Your Preparation Quick Takes

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Dr. Arindam DasAssociate Professor,Department of CommerceThe University of BurdwanHe can be reached at:[email protected]

A 25%B 20%

C 25% D 30%

Strategic Financial Management (SFM)

Group - IIIPaper - 14Group - IIIPaper - 14Strategic Financial Management (SFM)

6

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Learning objectives:

After studying this section on Strategic Financial Management, you will be able to:

Calculate security return and risk on the basis of single index model

Calculate covariance and standard deviation of the residuals in single index

model

Strategic Financial Management

Illustration 1

Annual return data are presented below for Stock X and the S&P Nifty Index for 12 years. Calculate the following:

a) The average return on stock X

b) The average return on the market

c) The variance and standard deviation of the stock X's return

d) The variance and standard deviation of the market portfolio's return

e) The covariance of the returns on stock X and the market portfolio

f) The correlation coefficient of the returns on stock X and the market portfolio

g) Beta for Stock X

h) Alpha for Stock X

i) The standard deviation of the residuals from the regression

Solution

a) The average return on stock X is:

YEAR STOCK-X (%) S&P Nifty (%)

2006 12.05 12.28

2007 15.27 5.99

2008 - 4.12 2.41

2009 1.57 4.48

2010 3.16 4.41

2011 - 2.79 4.43

2012 -8.97 -6.77

2013 - 1.18 -2.11

2014 1.07 3.46

2015 12.75 6.16

2016 7.48 2.47

2017 -0.94 - 1.15

7

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

b) The average return on the market portfolio is:

Table showing the necessary calculations for SD, Variance and Covariance

( c) The variance and standard deviation of the stock X's return are:

(d) The variance and standard deviation of the market portfolio's return are:

(e) The covariance of the returns on stock X and the market portfolio is:

12RXtt=1R =X 12

12.05 + 15.27 - 4.12 + 1.57 + 3.16 - 2.79 - 8.97 - 1.18 + 1.07 + 12.75 + 7.48 - 0.94= = 2.946%

12

12

Rmtt=1R =m12

12.28 + 5.99 + 2.41 + 4.48 + 4.41 + 4.43 - 6.77 - 2.11 + 3.46 + 6.16 + 2.47 - 1.15= = 3.005%

12

Year

2006 9.104 82.883 9.275 86.026 84.44

2007 12.324 151.881 2.985 8.910 36.79

2008 -7.066 49.928 -0.595 0.354 4.2

2009 -1.376 1.893 1.475 2.176 -2.03

2010 0.214 0.046 1.405 1.974 0.3

2011 -5.736 32.902 1.425 2.031 -8.17

2012 -11.916 141.991 -9.775 95.551 116.48

2013 -4.126 17.024 -5.115 26.163 21.1

2014 -1.876 3.519 0.455 0.207 -0.85

2015 9.804 96.118 3.155 9.954 30.93

2016 4.534 20.557 -0.535 0.286 -2.43

2017 -3.886 15.101 -4.155 17.264 16.15

Total 613.84 250.90 296.91

R - RXt X 2

R - RXt XR - Rmmt

2R - Rmmt R - R R - RmmtXt X

212

R - RXt X 613.842 t=1σ = = = 51.15X 12 12= 51.15 = 7.15%σ

X

212

R - Rmmt 250.902 t=1σ = = = 20.91m12 12

σ = 20.91 = 4.57%m

8

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

(f) The correlation coefficient of the returns on stock X and the market portfolio is:

� �

(g) The beta of stock X is:

(h) The alpha of stock X is:

( i ) each year's residual is security X's actual return that year minus the return that year predicted by the regression. The

regression's predicted yearly return is:

The residual for each year is then:

So we have the following:

Since the sample residuals sum to 0 (because of the way the sample alpha and beta are calculated), the sample mean of the

sample residuals also equals 0 and the sample variance and standard deviation of the sample residuals are:

12R - R R - RmmtXt X 296.91t=1σ = = = 24.74Xm 12 12

σ 24.74Xmρ = = = 0.757Xm σ σ 7.15×4.57mX

σ 24.74Xmβ = = = 1.1832X σ 20.91m

α = R -β R = 2.946% - 1.183×3.005% = -0.609%mX X X

R =α +β R mtX XX,t,Predicted

ε = R - RXt Xt X,t,Predicted

Year

2006 12.05 13.92 -1.87 3.5

2007 15.27 6.48 8.79 77.26

2008 -4.12 2.24 -6.36 40.45

2009 1.57 4.69 -3.12 9.73

2010 3.16 4.61 -1.45 2.1

2011 -2.79 4.63 -7.42 55.06

2012 -8.97 -8.62 -0.35 0.12

2013 -1.18 -3.11 1.93 3.72

2014 1.07 3.48 -2.41 5.81

2015 12.75 6.68 6.07 36.84

2016 7.48 2.31 5.17 26.73

2017 -0.94 -1.97 1.02 1.04

Sum: 0.00 262.36

RXt RX,t,Predicted

εXt2εXt

9

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

12 12ε - ε εXt X Xt 262.362 t=1 t=1σ = = = = 21.863εX 12 12 12

ω = 21.863 = 4.676%εX

= + βαR Ri mi i

R = -0.609 + 1.183×3.005 = 2.946%X

R = 2.946%A2σ = 51.15A

2SIMσ = β β σmij i j

SIMσ = 1.183×1.021×20.91 = 25.254AB

SIMσ = 57.433;SIMσ = 49.568AC BC

Illustration 2

Compute the mean return and variance of return for Stock X in Illustration 1 using

(a) The single-index model

(b) The historical data

Solution

(a) The Sharpe single-index model's formula for a security's mean return is

Using the alpha and beta for stock X along with the mean return on the market portfolio from Illustration 1 we have:

The Sharpe single-index model's formula for a security's variance of return is:

Using the beta and residual standard deviation for stock X along with the variance of return on the market portfolio from Problem 1

we have:

(b) From Illustration 1 we have:

Illustration 3

On the basis of the following information, compute covariance between the returns on a pair of securities according to the Sharpe

single-index model:

Beta for stock A = 1.183

Beta for stock B = 1.021

Beta for stock C = 2.322

The variance of the market portfolio = 20.91

Solution: According to the Sharpe single-index model, the covariance between the returns on a pair of stocks is

Using the betas for stocks A and B along with the variance of the market portfolio we have:

Similarly:

10

0 2 2σ = 1.183×20.91 + 4.676 = 51.14X

2=

2 2 2 2i i m i

Your Preparation Quick Takes

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

CMA (Dr.) Sreehari ChavaCost & Management Consultant,Nagpur, Maharastra,He can be reached at:[email protected]

B 50%

C 30%A 20%

A Cost Management 20%B Strategic Cost Management Tools and Techniques 50%C Strategic Cost Management - Application of Statistical Techniques in Business Decisions 30%

Strategic Cost Management -Decision Making (SCMD)

Group - IIIPaper - 15Group - IIIPaper - 15Strategic Cost Management -Decision Making (SCMD)

11

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Learning Objectives:

The Strategic cost management framework provides a clear plan of attack for addressing costs and decisions that affect them. It helps to get answers on:

Is there a plan for strategic cost management?

Have the controlling functions for each significant cost in the organization been identified?

Are there resources devoted to finding or obtaining new approaches to breaking cost barriers?

Is cost modelling being used or is there an active effort to develop or buy cost modelling capability?

Marginal Costing & Evaluation of Alternatives

01.00 Concept

Marginal Costing is the technique of presenting cost data wherein variable costs and fixed costs are shown separately for

managerial decision-making. It is simply a method to find out the impact of changes in the volume of output on profit.

Marginal costing technique has given birth to the concept of contribution wherein contribution is calculated as Sales revenue

less variable cost (marginal cost). Contribution may be defined as the profit before the recovery of fixed costs. Contribution is

excess of the Sales Value over the Variable Cost. It represents the margin available to meet the Fixed Costs. Excess of

Contribution over Fixed Cost denotes the Profit. The ratio of Contribution to Sales is known as Profit Volume (PV) Ratio. We,

thus, have the derivations:

Contribution = Sales – Variable Costs

Profit = Contribution – Fixed Costs

Profit Volume Ratio = (Contribution / Sales) x 100

Sales = Contribution / Profit Volume Ratio

Fixed costs will be the same for any volume of sales and production provided that the level of activity is within the 'relevant

range'; Revenue will increase by the sales value of the item sold; Cost will increase by the variable cost per unit and Profit will

increase by the amount of contribution earned from the extra item. The total contribution margin generated by an entity

represents the earnings available to pay for the fixed expenses and to pool into the profit.

02.00 Problem (Paper 17 June 2016)

A manufacturing company currently operating at 80% capacity has received an export order from Middle East, which will

utilise 40% of the capacity of the factory. The order has to be either taken in full and executed at 10% below the current domestic

prices or rejected totally. The current sales and cost data are given below:

Sales Rs. 16.00 lakhs

Direct Material Rs. 5.80 lakhs

Direct Labour Rs. 2.40 lakhs

Variable Overheads Rs.0.60 lakhs

Fixed Overheads Rs. 5.20 lakhs

The following alternatives are available to the management:

(I) Continue with domestic sales and reject the export order.

(II) Accept the export order and allow the domestic market to starve to the extent of excess of demand.

(III) Increase capacity so as to accept the export order and maintain the domestic demand by:

(i) Purchasing additional plant and increasing 10% capacity and thereby increasing fixed overheads by Rs.

65,000, and

12

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Serial Description Workings Rs.Lakhs

1 Capacity Given – 80%

2 Sales Given 16.00

3 Variable Costs

a. Direct Material

b. Direct Labour

c. Variable Overheads

d. Sub Total

Given

5.80

2.40

0.60

8.80

4 Contribution (2 - 3) 7.20

5 Fixed Costs Given 5.20

6 Profit (4 – 5) 2.00

Serial Description Workings Rs.Lakhs

1 Capacity Export 40% + Domestic 60%

2 Sales 7.20 + 12.00 19.20

3 Variable Costs

a. Direct Material

b. Direct Labour

c. Variable Overheads

d. Sub Total

(5.80 / 80%)

(2.40 / 80%)

(0.60 / 80%)

7.25

3.00

0.75

11.00

4 Contribution (2 - 3) 8.20

5 Fixed Costs Given 5.20

6 Profit (4 – 5) 3.00

(ii) Working overtime at one and half time the normal rate to meet balance of the required capacity.

Required: Evaluate each of the above alternatives and suggest the best one.�

03.00 Solution

Alternative (i): Continue with domestic sales and reject the export order.

Alternative (ii): Accept the export order and allow the domestic market to starve to the extent of excess of demand

This alternative envisages utilization of 40% of the capacity for the export order and 60% of the capacity for the domestic

market. The export order is to be executed at 10% below the current domestic prices. The value of the export order, accordingly

works out to: ((16.00 / 80) x 100 ) X 40% X 90% = Rs.7.20 lakhs. The value of the domestic sales works out to: ((16.00 / 80) x

100 ) X 60% = Rs.12.00 lakhs.

Alternative (iii): Increase capacity so as to accept the export order and maintain the domestic demand by:

(i) Purchasing additional plant and increasing 10% capacity and thereby increasing fixed overheads

by Rs. 65,000, and

(ii) Working overtime at one and half time the normal rate to meet balance of the required capacity.

13

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Serial Description Workings Rs.Lakhs

1 Capacity Export 40% + Domestic 80%

2 Sales 7.20 + 16.00

3 Variable Costs

a. Direct Material

b. Direct Labour

c. Variable Overheads

d. Overtime Premium

e. Sub Total

(5.80 / 80%) x 120%

(2.40 / 80%) X 120%

(0.60 / 80%) x 120%

(2.40 / 80%) X 10% X 50%

8.70

3.60

0.90

0.15

13.35

4 Contribution (2 - 3) 9.85

5 Fixed Costs (5.20 + 0.65) 5.85

6 Profit (4 – 5) 4.00

Suggestion: Alternative (iii) with the highest profit of Rs.4.00 lakhs works out to be the best.

04.00 Learnings

The problem is a good example to understand the methodology for evaluation of various alternatives with the help of marginal

costing.

14

Your Preparation Quick Takes

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Direct Tax Laws and InternationalTaxation (DTI)

Group - IIIPaper - 16Group - IIIPaper - 16Direct Tax Laws and InternationalTaxation (DTI)

CA Vikash Mundhra He can be reached at:[email protected]

A 50%C 20%

B 30%

15

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Learning Objectives:

To develop basic idea about the problem of International double taxation

To get acquainted with the methods of reliefs

To have acquaintance with the basic provisions of the provisions of the Indian

Income-tax Act regarding reliefs for double taxation.

Thin Capitalization

A company is typically financed or capitalized through a

mixture of debt and equity. The way a company is capitalized

often has a significant impact on the amount of profit it reports

for tax purposes as the tax legislations of countries typically

allow a deduction for interest paid or payable in arriving at the

profit for tax purposes while the dividend paid on equity

contribution is not deductible. Therefore, the higher the level

of debt in a company, and thus the amount of interest it pays,

the lower will be its taxable profit. For this reason, debt is often

a more tax efficient method of finance than equity.

Multinational groups are often able to structure their

financing arrangements to maximize these benefits. For this

reason, country's tax administrations often introduce rules

that place a limit on the amount of interest that can be

deducted in computing a company's profit for tax purposes.

Such rules are designed to counter cross-border shifting of

profit through excessive interest payments, and thus aim to

protect a country's tax base.

Under the initiative of the G-20 countries, the Organization

for Economic Co-operation and Development (OECD) in its

Base Erosion and Profit Shifting (BEPS) project had taken up

the issue of base erosion and profit shifting by way of excess

interest deductions by the MNEs in Action plan 4. The OECD

has recommended several measures in its final report to

address this issue.

In view of the above, sec. 94B was inserted in line with the

recommendations of OECD BEPS Action Plan 4, to provide

that interest expenses claimed by an entity to its associated

enterprises shall be restricted to 30% of its earnings before

interest, taxes, depreciation and amortization (EBITDA) or

interest paid or payable to associated enterprise, whichever is

less.

The provisions are enumerated here-in-below:

Applicable to

Indian company, or a permanent establishment of a foreign

company in India, being the borrower

Permanent establishment includes a fixed place of

business through which the business of the enterprise is

wholly or partly carried on.

Conditions

a) The borrower has debt issued by a non-resident, being an

associated enterprise of such borrower.

Debt means any loan, financial instrument, finance

lease, financial derivative, or any arrangement that

gives rise to interest, discounts or other finance

charges that are deductible in the computation of

income chargeable under the head "Profits and gains

of business or profession";

b) He incurs any expenditure by way of interest or of similar

nature exceeding � 1 crore;

c) Such expenditure is deductible in computing income

chargeable under the head "Profits and gains of business or

profession"

Effect

If all the aforesaid conditions are satisfied then, excess interest

shall not be deductible in computation of income under the

said head.

Excess interest means lower of the following:

a) An amount of total interest paid or payable in excess of

30% of earnings before interest, taxes, depreciation and

amortisation (EBITDA) of the borrower in the previous

year; or

b) Interest paid or payable to associated enterprises for

that previous year

Taxpoint

Guarantee: Where the debt is issued by a lender which is

not associated but an associated enterprise either provides

an implicit or explicit guarantee to such lender or deposits a

corresponding and matching amount of funds with the

lender, such debt shall be deemed to have been issued by an

associated enterprise.

Exception: The provision of sec. 94B is not applicable to

an Indian company or a permanent establishment of a

16

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

foreign company which is engaged in the business of

banking or insurance.

Where for any assessment year, the Carry forward:

interest expenditure is not wholly deducted against income

under the head "Profits and gains of business or

profession", so much of the interest expenditure as has not

been so deducted, shall be carried forward to the following

assessment year(s), and it shall be allowed as a deduction

against the profits and gains, if any, of any business or

profession carried on by it and assessable for that

assessment year to the extent of maximum allowable

interest expenditure.

No interest expenditure Maximum carried forward:

shall be carried forward for more than 8 assessment years

immediately succeeding the assessment year for which the

excess interest expenditure was first computed.

Example

Computation of interest expenses disallowed u/s 94B: ����� � in crore

Particulars Case 1 Case 2 Case 3

EBIDTA of the Indian Borrower 100 100 100

30% of the above [A] 30 30 30

Interest payable to associated enterprise [B] 35 Nil 15

Interest payable to non-associated enterprise [C] Nil 35 20

Total Interest expense incurred [D = B + C] 35 35 35

Total interest expenses incurred in excess of 30% of EBITDA [E = D – A]

5 5 5

Interest payable to associated enterprise [B] 35 Nil 15

Excess interest [lower of (E) and (B)] being disallowed u/s 94B 5 Nil 5

17

Your Preparation Quick Takes

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Corporate Financial Reporting (CFR)

Group - IVPaper - 17Group - IVPaper - 17Corporate Financial Reporting (CFR)

A 30%E 15%

D 15%

C 20% B 20%

A GAAP and Accounting Standards 30%B Accounting if Business Comminations & Restructuring 20%C Consolidated Financial Statements 20%D Developments in Financial Reporting 15%E Government Accounting in India 15%

Shri Soumya MukherjeeAssistant Professor,Maharaja Manindra Chandra College He can be reached at:[email protected]

18

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Learning Objectives:

This paper is having a broad based content to cover many aspects of corporate financial reporting. Corporate financial reporting is becoming complex day by day as we are gradually shifting to rule based approach from principle best approach. The syllabus is well designed an it covers core aspect of financial reporting i.e. measurement of income and cash flow of along with reporting of financial position of the company. Furthermore, there is stress on supplementary disclosure aspects like value added statement, human resource accounting related reporting, sustain ability reporting etc. Overall, the paper is application oriented and demands high level of conceptual, analytical and application related skill from students. Accounting is core of this paper. Students not having accounting or commerce background should give special stress in this paper.

Ind AS on Investments Vis a Vis AS- 13 on Accounting for Investments

Introduction:

At the outset, it is ideal to invest some time to study the

different approach unleashed by Ind-AS on accounting of

investments as compared to AS-13 on 'Accounting for

Investments'. Before we understand the distinct approach of

Ind-AS on Investments, it is better to have a bird's eye view of

AS-13 on 'Accounting for investments'.

AS 13 in a Gist:

Under Indian GAP, Accounting Standard 13 regulates

Accounting for Investments. Investments are assets held by

an enterprise for earning income by way of dividends,

interest, and rentals, for capital appreciation, or for other

benefits to the investing enterprise. Assets held as stock-in-

trade are not 'investments'. It also covers an investment in

property that is an investment in land or buildings that are

not intended to be occupied substantially for use by, or in the

operations of, the investing enterprise.

Recognition and measurement based on Current

and long term investments in AS 13:

These investments are classified primarily as Current and

long term investments. A current investment is an

investment that is by its nature readily realisable and is

intended to be held for not more than one year from the date

on which such investment is made. On the other hand, a long

term investment is an investment other than a current

investment. This classification is the sheet-anchor to

measure the value of the investments. The carrying amount

for current investments is the lower of cost and fair value. On

the other hand, Long-term investments are usually carried at

cost. However, when there is a decline, other than temporary,

in the value of a long term investment, the carrying amount is

reduced to recognise the decline. This conservative approach

could be easily appreciated, since loss is recognised in Profit

and Loss; as against profit that is not that lucky enough to get

recognised in P/L. Why? For simple reason that profit is

reckoned when actually realised. Again, is it not a

conservative traditional approach?

What a contrast in Ind. AS?

While As 13 has within its ambit

1. assets that have no physical existence and are represented

merely by certificates or similar documents (e.g., shares)

2. as well assets that exist in a physical form (e.g., buildings),

Ind.AS 40 is only dealing on investment Property, leaving

the investments in financial instruments to the better

cares of Ind. ASs 109/1o7/113 relating to recognition,

measurement, disclosures and fair value measurements.

As a result, Ind. AS sails, why? Rather flies on a different

fast tract to catch up with IFRS regime. That is the

scenario changing totally from a mere conservative

approach under AS 13, to a pulsating fair value /

amortised cost approach as the case may be for

measurement of financial assets. If we have to move with

the time and catch up with global trend, there is no run

away route but to follow suit especially when investors

more so stakeholders are spread across worldwide. India

is, in fact, in the list of a few countries in the word that has

to catch up with the global phenomenon. Investments in

Financial Assets could be either in equity or debt

instruments and are valued based on the following

Business models.

Equity Instruments:

Equity instruments are those that meet the definition of

equity from the perspective of the issuer as defined in Ind. AS

32.

1. Equity instruments that are held for trading are

19

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

necessarily required to be classified as FVTPL.

2. For all other equities, management has an option to

make an irrevocable election on initial recognition, on

an instrument-by-instrument basis, to present changes

in fair value in OCI rather than profit or loss. Therefore,

it is not accounting policy. If this election is made, all fair

value changes, excluding dividends that are a return on

investment, will be included in OCI. There is no

recycling of amounts from OCI to profit and loss (for

example, on sale of an equity investment), nor are there

any impairment requirements. However, the entity

might transfer the cumulative gain or loss within equity.

Investments in Debt instruments:

i. Financial assets held:

a)to collect contractual cash flows and

b) they represent the financial asset of cash flows that

are solely payments of principal and interest on the

principal amount outstanding(SPPI), is initially

measured at fair value and subsequently at amortised

cost.

ii. To achieve by both collecting contractual cash flows and

selling financial assets and (b) the contractual terms of

the financial asset give rise on specified dates to cash

flows that are solely payments of principal and interest

on the principal amount initially and subsequently

measured at fair value through Other Comprehensive

income (FVTPL). Financial assets included within the

FVTOCI category are initially recognized and

subsequently measured at fair value. Movements in the

carrying amount are recorded through OCI, except for

the recognition of impairment gains or losses, interest

revenue as well as foreign exchange gains and losses

which are recognized in profit and loss. Where the

financial asset is derecognized, the cumulative gain or

loss previously recognized in OCI is reclassified from

equity to profit or loss.

iii. In the case of a residual category in the sense they do not

meet the criteria of FVTOCI or amortized cost. at fair

value through profit or loss(FVTPL)

Further, the following factors are to be properly stitched into

the measurement of financial assets.

i. Transaction costs depending on Business Model

ii. Impairment of financial assets as per Ind. As 109 to be

applied retrospectively subject to certain exemptions

iii. Reclassification of financial assets under the aegis of the

Ind. AS 109

iv. Hedge accounting as stipulated by the said Ind. As.

Accounting policies are to be in place as prescribed in the

various Business models as enunciated above.

Fair Value Measurement:

Ind. As 113 on Fair Value Measurement does not deal

with the issue as to what should be measured at fair

value and at what point of time, that is within the

domain of the respective Ind. ASs. But, Ind. AS 113

dwells on the multiple valuation models to decide as to

which is to be followed on a particular situation.

Computation of fair value is reasonably easy for quoted

investments.

Computation of fair value may not be a cake walk for

unquoted investments. At times, it will turn out to be a

herculean task depending on value adjustment required

to arrive at the fair value.

In the separate (non-consolidated) financial statements

of the investor, the investments in subsidiaries

associates or joint ventures are carried at cost or as

financial assets in accordance with Ind. AS 109, unless

they meet the criteria to be classified as 'held for sale'

under Ind. AS 105, 'Non-current assets held for sale and

discontinued operations

Investment Property under Ind. AS 40:

Reverting back to Ind. As. 40 on 'Investment Property' that is

an investment in land or buildings that are not intended to be

occupied substantially for use by, or in the operations of, the

investing enterprise. This category includes also such

property under construction or development. Any other

properties are accounted for as property, plant and

equipment (PPE) or inventory as the case may be.

Initial measurement of an investment property will be at cost.

But, subsequent measurement of investment properties are

to be carried at cost less accumulated depreciation and any

accumulated impairment losses.

Policy and Disclosure:

An entity shall adopt as its accounting policy the cost model

prescribed in paragraph 56 to all of its investment property

and disclose. The next logical question that crops up and

hence to be addressed is whether fair valuation is permitted.

The Ind. AS 40 does not permit fair value for subsequent

measurement, though IFRS allows discretionary option.

20

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

However, the Ind.AS mandates that it is to be measured for its fair value under the guidance of Ind. AS 113 on fair value

measurement for the limited purpose of disclosure. If there has been no such valuation, that fact shall be disclosed. Disclosure

required under Para 79 of the said Ind-AS on depreciation methods, Gross Carrying amount and at the close with reconciliations

as suggested in Para 79.

Conclusion:

It goes without saying that the impact of fair valuation of financial assets will at times be highly disturbing especially for financial

assets valued at FVTPL, particularly when share markets behave funny on 30th March. Equity investments valued at FVTOCI

may not impact Profit and loss per- say; but there is no recycling of amounts from OCI to profit and loss (for example, on sale of an

equity investment. For Debt Instruments valued at amortised cost, the Profit and Loss will be influenced by the Effective rate of

Interest. The consequential workloads on the preparation of IT Returns need to be envisaged. The valuation of unquoted

investments is going to be like chasing the shadow at times, if not more often than not. Judgment has to play its role judicially. For

Investment companies, it may be a real labour pain since the value of investments on closing day matters for financial results. The

transition year is going to be a tough one especially when Indian physic has yet to experience that. Electing the appropriate

policies and consequential disclosure requirements will be a quite big challenge waiting in the horizon that the auditing

community has to reach out.

21

Your Preparation Quick Takes

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Indirect Tax Laws & Practice (ITP)

Group - IVPaper - 18Group - IVPaper - 18Indirect Tax Laws & Practice (ITP)

A Advanced Indirect Tax - Laws & Practice 80%B Tax Practice and Procedures 20%

B 20%

A 80%

Shri Abhik Kr. MukherjeeAssistant Professor,Dep. of Business AdmisitrationThe University of Burdwan He can be reached at:[email protected]

22

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Learning objectives:

After studying this section, you will having an understanding of:

Change in family structure post-introduction of Goods & Services Tax;

Central-level indirect taxes and levies subsumed by Goods & Services Tax;

State‐level indirect taxes and levies subsumed by Goods & Services Tax;

Body of indirect tax law under the GST regime;

Different types of levies under GST Statutes;

Applicability of the new levies under GST regime;

Comparison between the new levies.

FAMILY OF TAXES UNDER THE GOODS AND

SERVICES TAX REGIME IN INDIA

Introduction

In the arena of indirect taxes, 2017 has been a milestone year for

the Indian economy. This year witnessed the birth of a new

member in the family of Indian indirect taxes, it being the

Goods and Services Tax (GST). GST is a value-added tax levied

on most goods and services sold for domestic consumption.

Before the introduction of the Goods and Services Tax (GST),

the Central Government was empowered to levy excise duty on

manufacture or production of goods in India, service tax on the

provision of services, central sales tax on inter-state sales of

goods and the State Governments were empowered to levy the

state-level sales tax on the intra-state sale of goods.

The introduction of GST has been made with the objective of

'one nation, one tax' (one indirect tax, to be specific). In other

words, GST aims to be one indirect tax for the whole nation. It

would be a single tax on the supply of goods and services within

the country. But it is not yet fully achieved as some other taxes

prevail even after the introduction of GST (viz. Basic Customs

Duty). Thus, we can observe that the introduction of GST has

changed the structure of the indirect tax family of the Indian

economy. The introduction of GST has replaced some of the

members of the existing indirect tax family of India and has also

brought in newer members to the GST family. In the following

sections, we would focus on the taxes and levies that have been

replaced and also the new taxes that have been introduced in

the GST regime.

Indirect Taxes & Levies subsumed by GST

The introduction of GST has resulted in the merging of many

central-level and state- level taxes and levies with GST. They are

stated under:

Central-level Indirect Taxes & Levies subsumed by

GST

The following Central-level indirect taxes and levies have been

merged in GST:

Central Excise Duty

Excise Duty levied under the Medicinal and Toilet

Preparations (Excise Duties) Act, 1955

Additional Duties of Excise (Goods of Special Importance)

Additional Duties of Excise (Textile and Textile Products)

Service Tax

Additional Customs Duty – commonly known as

Countervailing Duty

Special Additional Duty of Customs

Central Cess and Surcharges in so far as they relate to

supply of goods and services.

State-level Indirect Taxes & Levies subsumed by GST

The following State-level indirect taxes and levies have been

merged in GST:

State Value Added Tax (i.e. State-level Sales Tax)

Central Sales Tax (levied by the Centre, but collected by the

State)

Entertainment Tax (except those levied by local bodies)

Purchase Tax

Octroi and Entry Tax

Luxury Tax

Taxes on advertisement

Taxes on lotteries, betting and gambling

State Cess and Surcharges in so far as they relate to supply

of goods and services.

Body of Law under Goods and Services Tax Regime

The above-mentioned developments have resulted in

23

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

significant changes in the body of laws of indirect taxes in India.

The new (both newly introduced and amended) statues relating

to indirect taxes that will be relevant in India during the GST

regime are mentioned below:

Constitution (One Hundred and First Amendment) Act,

2016.

Central Goods and Services Tax Act, 2017.

State Goods and Service Tax Act, 2017 of each State.

Union Territory Goods and Services Tax Act, 2017 of each

Union Territory.

Integrated Goods and Services Tax Act, 2017.

Goods and Services Tax (Compensation to States) Act,

2017

Rules made under the above Acts.

New Taxes and Levies under GST Statutes

GST, being a destination based tax, four different types of levies

have got introduced in the GST regime. They are:

Central Central Goods and Services Tax (CGST):

Goods and Services Tax (CGST) refers to the tax which is

levied by the Central Government of India on any supply

of goods and services taking place within a state i.e. intra-

state (within a state) transaction. It is one of the two taxes

charged on every intra-state transaction, the other one

being either State Goods or Services Tax (SGST) for the

States or Union Territory Goods and Services Tax

(UTGST) for the Union Territories. It is levied through

the Central Goods and Service Tax Act, 2017.

State Goods State Goods and Services Tax (SGST):

and Services Tax (SGST) refers to the tax which is levied

by the each State Government on any supply of goods and

services taking place between two or more states i.e.

inter-state (between states) transaction. This UTGST will

be charged in addition to the CGST. It is one of the two

taxes levied on every intrastate (within one state) supply

of goods and services. For any supply of goods/services

within a Steta the total levy is equal to the aggregate of

CGST & SGST. It is levied through the State Goods and

Service Tax Act of each State. The respective State

Government happens to be the sole claimer of the

revenue earned under SGST.

Union Territory Goods and Services Tax (UTGST):

The Union Territory Goods and Services Tax refers to the

GST applicable on the supply of goods and services

supply that takes place in any of the five Union Territories

of India, including Andaman and Nicobar Islands, Dadra

and Nagar Haveli, Chandigarh, Lakshadweep and

Daman and Diu. This UTGST will be charged in addition

to the CGST. It is one of the two taxes levied on every

intra-Union Territory (within one state) supply of goods

and services. For any supply of goods/services within a

Union Territory the total levy is equal to the aggregate of

CGST & UTGST. It is levied through the Union Territory

Goods and Service Tax Act of each Union Territory. The

respective Union Territory administration happens to be

the sole claimer of the revenue earned under UTGST.

Integrated Goods and Services Tax (IGST):

Integrated Goods and Services Tax (IGST) is applicable

on inter-state supply (i.e. any transaction taking place

between states) of goods and services, as well as on

imports. This tax will be collected by the Central

government and will further be distributed among the

respective states. IGST is charged when a product or

service is moved from one state to another. IGST is in

place to ensure that a state has to deal only with the Union

government and not with every state separately to settle

the interstate tax amounts. It is levied through the

Integrated Goods and Service Tax Act, 2017.

Applicability of the new levies under Goods and

Services Tax Regime

Since GST subsumed many indirect taxes and levies of both

central government (excise duty, service tax, custom duty, etc.)

and state governments (VAT, Luxury tax, etc.), each of the

governments now depend on GST for their indirect tax revenue.

Therefore, the GST rate is composed of two rates.

Levy on intra-state supplies: Intra-state supplies will be

charged with:

Both CGST and SGST; and In the case of State:

CGST and UTGST. In case of Union Territory:

Therefore, while making an intra-state sale (i.e. sale within the

same state), the CGST collected will go to the Central

Government and the SGST collected will go the respective State

Government in which sale is made; and while making an intra-

union territory sale (i.e. sale within the same Union Territory),

the CGST collected will go to the Central Government and the

UTGST collected will go the respective Union Territory

administration in which sale is made.

Levy on inter-state supplies: The inter-state supplies of

goods or services or both will be charged with Integrated Goods

24

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

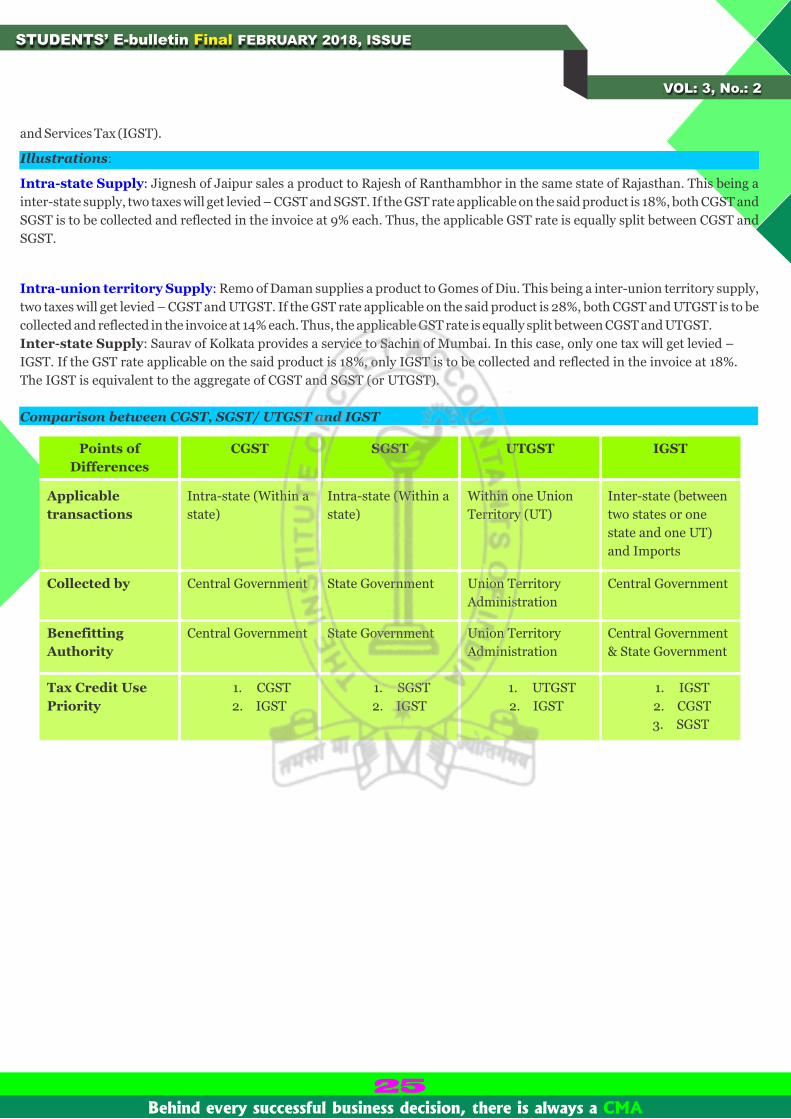

Points of

Differences

CGST SGST UTGST IGST

Applicable

transactions

Intra-state (Within a

state)

Intra-state (Within a

state)

Within one Union

Territory (UT)

Inter-state (between

two states or one

state and one UT)

and Imports

Collected by Central Government State Government Union Territory

Administration

Central Government

Benefitting

Authority

Central Government State Government Union Territory

Administration

Central Government

& State Government

Tax Credit Use

Priority

1. CGST

2. IGST

1. SGST

2. IGST

1. UTGST

2. IGST

1. IGST

2. CGST

3. SGST

and Services Tax (IGST).

Illustrations:

Intra-state Supply: Jignesh of Jaipur sales a product to Rajesh of Ranthambhor in the same state of Rajasthan. This being a

inter-state supply, two taxes will get levied – CGST and SGST. If the GST rate applicable on the said product is 18%, both CGST and

SGST is to be collected and reflected in the invoice at 9% each. Thus, the applicable GST rate is equally split between CGST and

SGST.

Intra-union territory Supply: Remo of Daman supplies a product to Gomes of Diu. This being a inter-union territory supply,

two taxes will get levied – CGST and UTGST. If the GST rate applicable on the said product is 28%, both CGST and UTGST is to be

collected and reflected in the invoice at 14% each. Thus, the applicable GST rate is equally split between CGST and UTGST.

Inter-state Supply: Saurav of Kolkata provides a service to Sachin of Mumbai. In this case, only one tax will get levied –

IGST. If the GST rate applicable on the said product is 18%, only IGST is to be collected and reflected in the invoice at 18%.

The IGST is equivalent to the aggregate of CGST and SGST (or UTGST).

Comparison between CGST, SGST/ UTGST and IGST

25

Your Preparation Quick Takes

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Cost & Management Audit (CMAD)

Group - IVPaper - 19Group - IVPaper - 19Cost & Management Audit (CMAD)

A Cost Audit 35%B Management Audit 15%C Internal Audit, Operational Audit and other related issues 25%D Case Study on Performance Analysis 25%

A 35%D 25%

B 15%C 25%

CMA S S SonthaliaPracticing Cost Accountant,BhubaneswarHe can be reached at:[email protected]

26

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Learning Objectives:

To verify the correctness of the cost accounting records.

To find out whether the principles of cost accountancy have been fully and

correctly applied in maintaining cost records.

To search for the deficiencies in the cost record system of the company.

To attain efficiency in cost accounting systems and procedures

Clause (b) of sub-section (1) of section 2 of the Cost and Works Accountants Act, 1959 defines “Cost Accountant” who holds a valid certificate of practice under sub-section (1) of section 6 of the Cost and Works Accountants Act, 1959 and is in whole-time practice as cost accountant. Cost Accountant includes a Firm of Cost Accountants and a LLP of cost accountants.

A cost accountant holding certificate of practiced on part time basis is not entitled to conduct cost audit. Thus, only a cost accountant in whole-time practice can conduct cost audit. Further that no person appointed under section 139 of the Companies Act 2013 as an auditor of the company shall be appointed as cost auditor.

Appointment process

1 On achieving the turnover in the previous year i.e say as on

31.03.218 (financial year 2017-18),the cost auditor need

to be appointed within one hundred and eighty days of the

commencement of next financial yeari.e by 27.09.2018

(financial year 2018-19)

2 Before the appointment of cost auditor a written consent

and a certificate is to be obtained from him or it, as

provided in sub-rule (1A) of the CCRA Rule 2014

containing that.

a. The cost auditor firm is eligible for appointment and is

not disqualified for appointment under the Act, the

Cost and Works Accountants Act, 1959(23 of 1959)

and the rules or regulations made thereunder;

b. The individual or the firm, as the case may be,

satisfies the criteria provided in section 141 of

theAct, so far as may be applicable;

c. The proposed appointment is within the limits laid

down by or under the authority of

the Act; and

d. The list of proceedings against the cost auditor or

audit firm or any partner of the audit firmpending

with respect to professional matters of conduct, as

disclosed in the certificate, is true andcorrect.”;

Disqualification for appointment as Cost auditor

As per provisions of Sec.141 (3) of The Companies Act 2013, the

Topic: Provisions and procedures for

appointment of Cost Auditor

Introduction

Section 148 of the Companies Act, 2013, contains the provisions relating to Cost Audit.

As per Sec.148 (3) of the Companies Act 2013 and Chapter X, the audit under sub-section (2) shall be conducted by a Cost Accountant in practice who shall be appointed by the Board of Directors of company who will also approve the remuneration and scope of work of the cost auditor

However where the company also have Audit Committee, appointment and remuneration approved by Boardis on the recommended of the audit committee.

Applicability of cost audit to the Companies

Rule 6 of the Companies (Cost Records and Audit) Rule 2014,(CCRA Rule 2014) as amended contains the provisions.

As per the rule the companies are classified in to two sectorsand applicability of cost audit is based on the Turnover of the respective sector company.

a. Regulated Sector industries

b. Non-regulated Sector industries

For Regulated Sector companies the overall annual turnover of the company from all its products andservices during the immediately preceding financial year is rupees fifty crore or more and the aggregate turnover ofthe individual product or products or service or services for which cost records are required to be maintained is rupees twenty five crore or more.

For Non-regulated Sector companies the overall annual turnover of the company from all its products and services during the immediately precedingfinancial year is rupees one hundred crore or more and the aggregate turnover of the individual product or productsor service or services for which cost records are required to be maintained is rupees thirty five crore ormore.

Who can be appointed as a cost auditor?

Only a Cost Accountant, as defined under section 2(28) of the Companies Act, 2013, can be appointed as a cost auditor.

27

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

followings are not eligible for appointment as cost auditor.

i. A body corporate other than a limited liability

partnership registered under the Limited Liability

Partnership Act, 2008;

ii. An officer or employee of the company;

iii. A person who is a partner, or who is in the

employment, of an officer or employee of the

company;

iv. A person who, or his relative or partner—

v. Is not holding any security of or interest in the

company or its subsidiary, or of its holding or associate

company or a subsidiary of such holding companynot

exceeding face value one thousand rupees:

vi. Is indebted to the company, or its subsidiary, or its

holding or associate company or a subsidiary of such

holding company, in excess of such amount as may be

prescribed; or

vii. Has given a guarantee or provided any security in

connection with the indebtedness of any third person

to the company, or its subsidiary, or its holding or

associate company or a subsidiary of such holding

company, for such amount as may be prescribed;

viii. A person or a firm who, whether directly or indirectly,

has business relationship with the company, or its

subsidiary, or its holding or associate company or

subsidiary of such holding company or associate

company of such nature as may be prescribed;

ix. A person whose relative is a director or is in the

employment of the company as a director or key

managerial personnel;

x. A person who is in full time employment elsewhere or

a person or a partner of a firm holding appointment as

its auditor, if such persons or partner is at the date of

such appointment or reappointment holding

appointment as auditor of more than twenty

companies;

xi. A person who has been convicted by a court of an

offence involving fraud and a period of ten years has

not elapsed from the date of such conviction;

xii. Any person whose subsidiary or associate company or

any other form of entity, is engaged as on the date of

appointment in consulting and specialised services as

provided in section 144.

Appointment provisions

(1) Every company after appointment shall inform the cost

auditor concerned of his or its appointment and file a

notice of such appointment with the Central

Government within a period of thirty days of the Board

meeting in which such appointment is made or within a

period of one hundred and eighty days of the

commencement of the financial year, whichever is

earlier.

(2) Thenotice of appointmentis filed through electronic

mode, in form CRA-2, along with copy of Board

resolution, consent letter of cost auditor and the fee as

specified in Companies (Registration Offices and Fees)

Rules, 2014.

(3) If any default is made in complying with the provisions

of section 148, the company and every officer of the

company who is in default shall be punishable in the

manner as provided in sub-section (1) of section 147.

(4) For delay in filing intimation with Central Govt., the

company is liable pay normal fee plus additional fees

based on period of delay which could be 12 Times of

Nominal fees for delay beyond 180 Days.

(5) Every cost auditor appointed on his or her appointment

shall continue in such capacity till the expiry of one

hundred and eighty days from the closure of the

financial year or till he submits the cost audit report, for

the financial year for which he has been appointed.

(6) The cost auditor appointed under these rules may be

removed from his office before the expiry of his term,

through a board resolution after giving a reasonable

opportunity of being heard to the Cost Auditor and

recording the reasons for such removal in writing. On

removal the company need to file another Form CRA-2

with the Central Government enclosing the relevant

Board Resolution to this effect.

(7) The cost auditor has also right to resign as a cost auditor

of the company.

(8) Any casual vacancy in the office of a cost auditor, whether

due to resignation, death or removal, shall be filled by

the Board of Directors within thirty days of occurrence

of such vacancy and the company shall inform the

Central Government in Form CRA-2 within thirty days

of appointment of new cost auditor.

28

Your Preparation Quick Takes

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Strategic Performance Managementand Business Valuation (SPBV)

Group - IVPaper - 20Group - IVPaper - 20Strategic Performance Managementand Business Valuation (SPBV)

A 50%

B 50%

Dr. Amalendu BhuniaProfessor,Department of Commerce,University of KalyaniHe can be reached at:[email protected]

29

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

Learning Objectives:

I strongly recommend getting your basics from study materials first and then moving over in

solving numerical sums from professional examinations in the last 5 terms.

Internationally famous books and video tutorials have no substitute.

Learn alone but discuss with your fellow examiners at regular intervals.

Best way of learning is teaching. Learn an issue by writing manually as far as possible.

Next, try to teach it to another examinee. You will get reciprocal treatment from him/her.

Let you grow together!

30

Organic or Internal Growth of a Business

Corporate plans are usually crafted to encourage profitability

and growth factors of the valuation of a company. Generally

company's growth flourishes shareholders' value. Another

views assert that extreme growth may cause decrease in

shareholders' value. In theory, investors endeavour to predict

potential growth of business and markdown the anticipation

for prospect into the present value of the stock price. Stock

prices vary with understanding and anticipation gap.

Companies make additional shareholder value merely when

they go beyond those investors' anticipations. When the

company proclaims lesser growth rate than investors had

already economical into the stock price, its stock price reduces

because investors approved their overvalued growth

outlooks. Nevertheless, to reinstate stock price, management

habitually tries to accomplish a growth rate considerably

higher than the reasonable growth rate of the company

wherein they work. While tackled with force to grow up,

management is bound to support negative net present value

plans or make their leverage levels to get supplementary

capital obligatory for the growth. However growth is valuable

just whilst the firm is rising healthily, specifically, profits

made are moreover rising in-line with sales income. If not,

profits give the augmented funding necessity stemming from

the sales growth, the company has to reduce its dividends or

augment its debt level. Both are pessimistically apparent by

the markets and generally result in share price go down, in

due course wiping out shareholder value.

Company growth can be accomplished through mergers and

acquisitions (external growth), and the enhance of its possess

assets or output in the course of the reinvestment of its cash

flows in existing businesses (internal or organic growth). Both

kinds of growth plans are commonly employed at the same

time and have benefits and problems. The gainful growth is

sustainable. Companies that employ stringently internal

growth may control price premiums however they moreover

neglect opportunities as they don't perform the right manner

of acquisitions. Companies that execute simply acquisitions

generally disburse an extremely high price and there is

complexity in making the premium back. Without a doubt, a

competent growth plan is hard and significant: each kind of

growth will have a major shock on the company's operational

and market performance.

Organic or internal growth is the rate of a business growth

through a company's own business activity. When a company

with help of its efficient management increases its growth

rate, it is known as organic or internal growth. Most business

enterprises are regularly faced with the confront of

flourishing and rising their business'. Businesses can desire to

make their in-house competencies, invest to make

competitive advantages, discriminate and innovate in the

product or service line. The advantages of the organic growth

are (i) capability to bring exceptional value plans., (ii) creating

brands and marketing channels to serve up customers

healthier, (iii) control and focus for growth plans. The

management is ready to take risks for which they arrange and

plan well and (iv) organizational effectiveness component of

the heart of the business.

Internal or organic growth gives more corporate power,

supports internal entrepreneurship as well as defends

organizational culture for diverse motives. At the outset,

managers have a superior awareness of their own company

and assets in addition to the internal investment is expected to

be healthier planned and resourceful. Besides, synergies may

furthermore be expensive to use, building it once more

attractive to invest internally. Likewise, internal or organic

growth satisfies top management techniques and firm

compositions variations that wipe out value in combinations.

Lastly, companies that are investing internally are

furthermore capable to make sustainable competitive

advantages because their value-creation procedures and

positions are less expected to be replica or emulated by other

firms. Internal growth strategies are more confidential as well

as less prone to any aggressive accomplishment from other

companies. This causes healthier incentives from the capital

Behind every successful business decision, there is always a CMABehind every successful business decision, there is always a CMA

STUDENTS’ E-bulletin FEBRUARY 2018, Final ISSUE

VOL: 3, No.: 2

31

market. The selection of growth form will have a straight shock on the company's plan and performance over and above on the

expansion of our economies.

It has been observed that in the short run, internal or organic growth is overwhelming the cash-flows of the companies because

the cash flow returns reduce around the dates of investment. On the other hand, in the longer run, internal or organic growth has a

positive shock on operational performance, once the companies had adequate time to raise their sales and comprehend

economies of scales or other cost cut plans. If a company has no merger or acquisitions or asset divestments in a year, in that case

it raises through its internal assets and the internal growth rate.

I expect that these above-mentioned tips come

useful for the Final Year CMA Students.

01.0 The Benevolent Bank

Imagine there is a bank that credits your account every

morning with Rs. 86,400/- for consumption during the day.

The basic fundamental is that the bank does not carry

forward any balance from day to day. Hence, at the end of

every evening the bank forfeits the unutilized balance. What

would you do? Draw out every rupee and use it before the

dusk, of course.

Each of one of us has such a generous bank that credits our

account every morning with 86,400 seconds (1,440 minutes