closing entries (part 2). closing entry #2 - expenses we want to clear the balance of each expense...

TRANSCRIPT

Closing Entries (Part 2)

Closing Entry #2 - Expenses

• We want to clear the balance of each expense account.

• Expenses have debit balances, so we need CREDIT entries to zero the accounts.

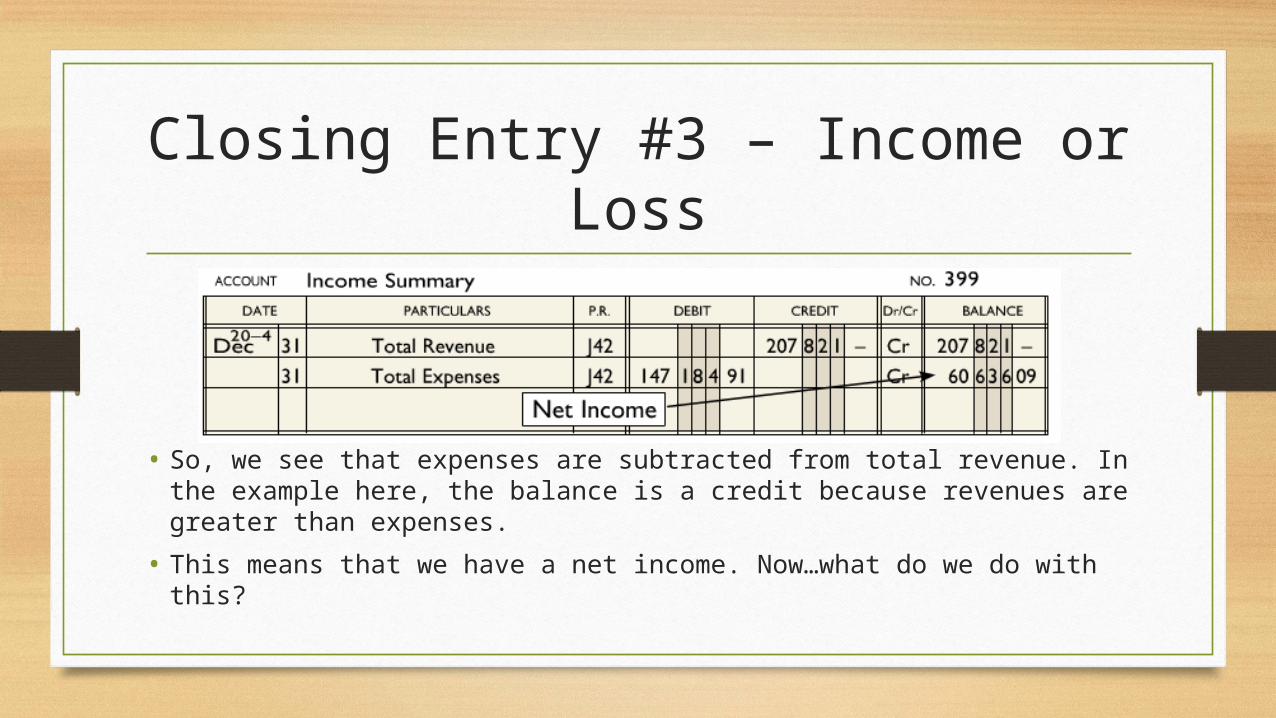

Closing Entry #3 – Income or Loss

• So, we see that expenses are subtracted from total revenue. In the example here, the balance is a credit because revenues are greater than expenses.

• This means that we have a net income. Now…what do we do with this?

Closing Entry #3 – Income or Loss

• Think of the equity equation:

Beginning Capital + Net Income…

Closing Entry #4 - Drawings

• If we think about the equity equation, we need to consider drawings to figure out our ending capital.

• The Drawings account always has a debit balance. This means we need a CREDIT entry to close it.

Closing Entry #4 - Drawings

• Looking at the closing entries, it is obvious why closing entries is important.

• The nominal accounts have all been closed.

• The Capital account now shows what equity actually is:

Beginning Capital ($28,895.42)Net Income ($60,636.09)+ -Drawings($42,000) =Ending Capital($47,531.51)

Post-Closing Trial Balance

We have to make sure that the ledger accounts are accurate.

We have to make a trial balance from theledger account balances.,

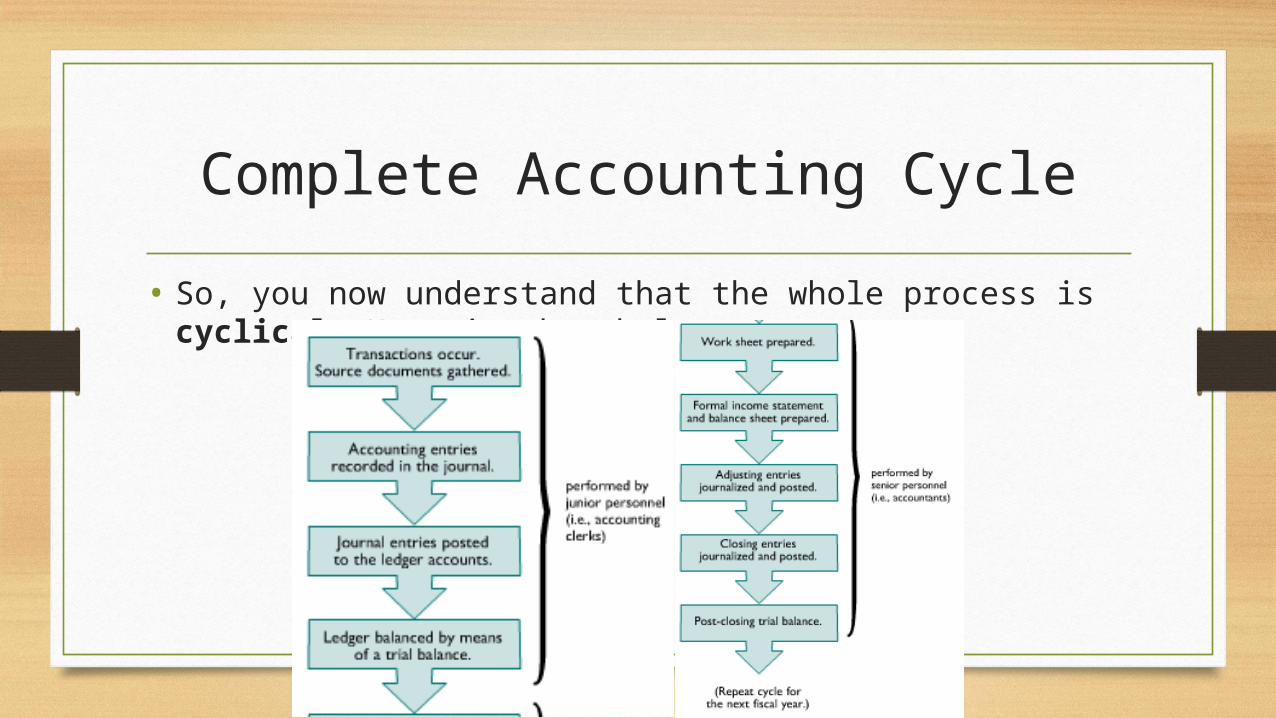

Complete Accounting Cycle

• So, you now understand that the whole process is cyclical. Here is the whole process.