climate change risk assessment for the business, industry and

TRANSCRIPT

(Defra Project Code GA0204)

Climate Change Risk Assessment for the Business, Industry and Services Sector

January 2012 1Baglee, A., 1Haworth, A. and 2Anastasi, S. Contractors: HR Wallingford

1Acclimatise 2AMEC Environment & Infrastructure UK Ltd (formerly Entec UK Ltd) The Met Office Collingwood Environmental Planning Alexander Ballard Ltd Paul Watkiss Associates Metroeconomica

ii Business, Industry and Services

Statement of use See full statement of use on Page v Keywords: Climate, risks, business, tourism, financial services, industry Research contractor: HR Wallingford Howbery Park, Wallingford, Oxon, OX10 8BA Tel: +44 (0)1491 835381 (For contractor quality control purposes this report is also numbered EX 6433) Defra project officer: Dominic Rowland Defra contact details: Adapting to Climate Change Programme, Department for Environment, Food and Rural Affairs (Defra) Area 3A Nobel House 17 Smith Square London SW1P 3JR

Tel: 020 7238 3000 www.defra.gov.uk/adaptation Document History:

Date Release Prepared Notes 07/10/10 0.1 Entec UK Ltd Review copy for project team only 11/11/10 0.2 Entec UK Ltd Revised review copy for project

team only 22/11/10 1.0 HR Wallingford / Entec UK Ltd Draft for review

24/11/10 1.1 HR Wallingford / Entec UK Ltd.

Acclimatise Draft for peer review

01/02/11 2.0 HR Wallingford / Acclimatise Updated in response to peer review and Government Department review comments

31/03/11 3.0 HR Wallingford / Acclimatise Additional work added and updated in response to further review comments

13/05/11 3.0A HR Wallingford High-level concerns identified by Government Departments added (to be addressed in Release 4).

14/06/11 3.0A2 HR Wallingford Minor amendments

12/08/11 4.0 Acclimatise / HR Wallingford Major re-write: draft for external publication

21/10/11 4A Acclimatise / HR Wallingford Updated draft in response to comments

05/12/11 5 Acclimatise / HR Wallingford Updated draft in response to comments

13/01/12 6 Acclimatise / HR Wallingford Updated with final edits.

Business, Industry and Services iii

© Crown copyright 2012 You may use and re-use the information featured in this document/publication (not including logos) free of charge in any format or medium, under the terms of the Open Government Licence http://www.nationalarchives.gov.uk/doc/open-government-licence/open-government-licence.htm Any email enquiries regarding the use and re-use of this information resource should be sent to: [email protected]. Alternatively write to The Information Policy Team, The National Archives, Kew, Richmond, Surrey, TW9 4DU. Printed on paper containing 75% recycled fibre content minimum. This report is available online at: http://www.defra.gov.uk/environment/climate/government/

iv Business, Industry and Services

Business, Industry and Services v

Statement of use This report presents the research completed as part of the UK Climate Change Risk Assessment (CCRA) for a selected group of risks in the Business, Industry and Services sector. Whilst some broader context is provided, it is not intended to be a definitive or comprehensive analysis of the sector.

Before reading this report it is important to understand the process of evidence gathering for the CCRA.

The CCRA methodology is novel in that it has compared over 100 risks (prioritised from an initial list of over 700) from a number of disparate sectors based on the magnitude of the consequences and confidence in the evidence base. A key strength of the analysis is the use of a consistent method and set of climate projections to look at current and future threats and opportunities.

The CCRA methodology has been developed through a number of stages involving expert peer review. The approach developed is a tractable, repeatable methodology that is not dependent on changes in long term plans between the 5 year cycles of the CCRA.

The results, with the exception of population growth where this is relevant, do not include societal change in assessing future risks, either from non-climate related change, for example economic growth, or developments in new technologies; or future responses to climate risks such as future Government policies or private adaptation investment plans.

Excluding these factors from the analysis provides a more robust ‘baseline’ against which the effects of different plans and policies can be more easily assessed. However, when utilising the outputs of the CCRA, it is essential to consider that Government and key organisations are already taking action in many areas to minimise climate change risks and these interventions need to be considered when assessing where further action may be best directed or needed.

Initially, eleven ‘sectors’ were chosen from which to gather evidence: Agriculture; Biodiversity & Ecosystem Services; Built Environment; Business, Industry & Services; Energy; Forestry; Floods & Coastal Erosion; Health; Marine & Fisheries; Transport; and Water.

A review was undertaken to identify the range of climate risks within each sector. The review was followed by a selection process that included sector workshops to identify the most important risks (threats or opportunities) within the sector. Approximately 10% of the total number of risks across all sectors was selected for more detailed consideration and analysis.

The risk assessment used UKCP09 climate projections to assess future changes to sector risks. Impacts were normally analysed using single climate variables, for example temperature.

A final Evidence Report draws together information from the 11 sectors (as well as other evidence streams) to provide an overview of risk from climate change to the UK.

Neither this report nor the Evidence Report aims to provide an in depth, quantitative analysis of risk within any particular ‘sector’. Where detailed analysis is presented using large national or regional datasets, the objective is solely to build a consistent picture of risk for the UK and allow for some comparison between disparate risks and regional/national differences.

vi Business, Industry and Services

This is a UK risk assessment with some national and regional comparisons. The results presented here should not be used by the reader for re-analysis or interpretation at a local or site-specific scale.

In addition, as most impacts were analysed using single climate variables, the analysis may be over-simplified in cases where the consequence of climate change is caused by more than one climate variable (for example, higher summer temperatures combined with reduced summer precipitation).

Business, Industry and Services vii

Executive Summary This report for the Business, Industry and Services sector of the UK Climate Change Risk Assessment (CCRA) has used available evidence and expert opinion to consider the effects of climate change for this sector. The aim of the CCRA is to help the UK and devolved Governments identify priorities for action and implement necessary adaptation measures. The CCRA focuses on 11 sectors deemed as fundamental to the social, environmental and economic value in the UK, including the Business, Industry and Services sector. This assessment utilised the following sub-sectors as illustrative examples to highlight the range of climate-related issues and challenges the sector as a whole faces: financial services; tourism; food and beverage manufacturing; primary extractives (oil, gas and mining); and chemical manufacturing. Selection of these sub-sectors was effectively a sector based case study approach to illustrate the key business issues and provide a wide variety of characteristics that can be used as proxies for other sub-sectors.

Climate change is expected to be a key challenge for the Business, Industry and Services sector, both today and in the future. Failure to consider climate risk and adaptation into decision-making processes could have severe consequences for this sector with further impacts felt across all other sectors. Climate change does not necessarily create ‘new’ risks for the Business, Industry and Services sector. Climate change typically represents a change to existing risk profiles – in other words they are already issues facing business and industry on a daily basis. For example, storm-related impacts to transport infrastructure, on which business heavily relies, have already been experienced. Climate change simply represents a potential change in the duration and/ or frequency of occurrence of these impacts, and their subsequent effects on business operations.

Key messages

Climate change represents a challenge for the Business, Industry and Services sector, with both tangible and intangible asset value potentially affected. However, for those businesses that take on this challenge, there are potentially significant commercial and competitive advantages to be gained.

The Business, Industry and Services sector is vulnerable to climate change due to the combination of the sector’s climate sensitivity and adaptive capacity. Although the majority of the risks identified in this risk assessment fall into the category of climate sensitivity, a number of risks to the sector are the result of low adaptive capacity, and in particular, a low recognition of the need to act on climate change. This crucially needs addressing in order to minimise the potential risks and seize opportunities.

The Business, Industry and Services sector does not operate in a void; this report has highlighted the inter-connectivity between business and industry, national infrastructure provision and the natural environment. Any adaptation actions need to remain cognisant of these important inter-connections, considering any possible feedbacks and knock-on consequences.

The Business, Industry and Services sector is influenced to a very large degree by international issues including investments, supply of products and materials and international markets. Many of these are influenced by present-day climate and may be influenced by future climate change to

viii Business, Industry and Services

some degree. These externalities (whether in the UK or overseas) are vitally important for business continuity and growth and need to be fully explored and mapped.

Vulnerability of the sector to climate change The Business, Industry and Services sector is highly vulnerable to a changing climate, both extreme (acute) events and incremental (chronic) climate change. The impacts are likely to be felt across the spectrum of sub-sectors and from Small and Medium Enterprises (SMEs) to large multi-national corporations. The degree to which individual organisations are vulnerable to climate change depends on their level of sensitivity and adaptive capacity (both these elements are discussed in more detail below). Across the sector, current vulnerability to climate-related impacts can be divided into the following common themes:

Assets: Fixed and workforce (e.g. infrastructure damage, workforce exposure to health and safety risks).

Operations: Supply of services, customer demand and regulatory environment (e.g. financial performance, markets shift due to change in public attitudes and / or legislation).

Procurement: Raw materials, supply chain and logistics (e.g. supply of water, energy and materials, reliance on vulnerable transport networks).

Environment: Natural and built, plus local community (e.g. climate-sensitive resources and conflict over their use).

These impacts have the potential to create the following consequences for individual businesses and collective sub-sectors within the Business, Industry and Services sector:

Financial performance (revenue loss / gain)

Additional costs (capital expenditure (capex) and operational expenditure (opex))

Operational disruption

Loss of staff work hours

Corporate reputation

Elevated stakeholder interest

Additional regulatory requirements

Contractual issues

Litigation

New market opportunities and product diversification.

Climate change risks and opportunities for the sector The initial scoping of climate-related impacts to the Business, Industry and Services sector (termed the ‘Tier 1 analysis’) identified more than 120 risks. These risks were subsequently scored, based on the magnitude of consequence for economic, environmental and social categories, together with the likelihood of the consequence

Business, Industry and Services ix

occurring, and the highest scoring or ‘key’ risks were selected for more detailed analysis (termed the ‘Tier 2 analysis’). This report presents the findings of the Tier 2 analysis. The key risks identified for the Business, Industry and Services sector were:

1. Reduced returns for UK financial institutions’ investments due to the absence of mainstreaming climate risk and adaptation into decision-making processes (BU1).

2. An increase in monetary losses as a result of an increasing proportion of UK tourist assets (natural and built) at risk from flooding (BU2).

3. A decrease in water (groundwater and surface water) availability for industrial usage (BU3).

4. An increase in monetary losses as a result of interruption to business from flooding (BU4).

5. A decrease in productivity and revenues due to ICT loss/ disruption (BU5)

6. Increased exposure for mortgage lenders (BU6).

7. An increase in insurance industry exposure due to flooding (BU7).

8. An expansion of new or existing tourist destinations in the UK (BU8).

9. A decrease in output for UK businesses due to an increase in supply chain disruption as a result of extreme events (BU9).

10. Loss of staff hours due to high internal building temperatures (BU10).

The assessment team believes that these risks, identified as a result of the scoring methodology, are consistent with those typically expected for Business, Industry and Services. They are also consistent with comments made by stakeholders on their perception of the ‘top’ risks to this sector in the UK, albeit without consideration of the wider international perspective (e.g. global supply chains).

Sensitivity Knowledge of the sensitivity of both the sector as a whole and the assessment end-point risks to particular climate variables is of enormous value in determining the likely future response under a changing climate. The five sub-sectors of Business, Industry and Services sector that this report focuses on are highlighted as having a number of features that make them particularly sensitive to the physical effects of climate change. These include reliance on:

Large fixed assets (e.g. chemical manufacturing near large main rivers or coastline)

Complex supply chains (e.g. food and beverages)

Natural assets (e.g. tourism).

It is important to stress that it should not be assumed that these sub-sectors would bear the majority of the risks from climate change.

The climate sensitivities of the key risks identified for the Business, Industry and Services sector are summarised in the table below. The table also shows whether the risks are direct or indirect result of climate change.

x Business, Industry and Services

Risk Sensitivity to climate change

Reduced returns and/or increased risks of UK financial institutions’ investments due to the absence of mainstreaming climate risk and adaptation into decision-making processes (BU1).

Indirect impact

At the moment, there is limited substantive evidence of the consequences of changes in climate on UK financial institutions. It is difficult to establish a clear and direct link between climate-related impacts and financial institution performance. Research strongly shows, however, that the sector faces considerable risks that could potentially be material to investment return and/or risk. Further, there is recognition by researchers, stakeholders and financial institutions themselves that sensitivity to some of the risks of climate change could be high in the short term. It is the case of the reputational implications of a changing climate, as well as the investor pressures for climate change adaptation disclosure and mainstreaming. As such, the exposure of financial institutions to climate change is known, but uncertainties are too high and available information too limited to quantify risks.

An increase in monetary losses as a result of an increasing proportion of UK tourist assets (natural and built) at risk from flooding (BU2).

Indirect impact

The financial implications for the tourism industry are directly linked to the number of tourist assets at risk of flooding. This risk is relatively sensitive to climate change, and in particular, ‘extreme events’ in the short term. Over a long time period, incremental sea level rise may exacerbate this issue further and thus the risk may become more frequent and less associated with ‘extreme’ events. Some amelioration of the risk may be afforded, however, through insurance and other risk transfer methods.

A decrease in water (groundwater and surface water) availability for industrial usage (BU3).

Direct impact

There is a strong and obvious link between water resources availability and precipitation. However, this ought to be put within the context of Public Water Supply (PWS) abstraction, which constitutes the vast majority of the water abstracted in the UK. As such, the availability of water for industrial applications may be more a function of the effectiveness of water resource management for PWS in making efficiency savings that allow for industrial abstractors to maintain operations.

An increase in monetary losses as a result of interruption to business from flooding (BU4).

Indirect impact

Like tourism assets, the risk of fluvial and tidal flooding is relatively sensitive to climate change, and in particular, ‘extreme events’. Over a long time period, incremental sea level rise and projected increases in rainfall may exacerbate this issue further and thus the risk may become more frequent and less associated with ‘extreme’ events.

A decrease in productivity and revenues due to ICT loss/ disruption (BU5).

Indirect impact

Both incremental and extreme events may play a part in the loss of ICT productivity. Although the majority of ICT equipment will operate well within the projected climatic ranges for temperature and humidity, it is recognised in this assessment that the risks for remote rural workers are most pronounced where there is greatest reliance on single electricity and telecommunications connections. Moreover, this risk is relatively sensitive to climate change, and in particular, ‘extreme events’ such as flooding.

Increased exposure for mortgage lenders (BU6).

Indirect impact

This risk is relatively insensitive to climate change due to the fact that there is not a direct link between a changing climate and the provision of mortgages. The availability of insurance cover is an important ‘middle-step’ and this will be subject to economic forces and risk management practices within the insurance sector. As such, any effect on mortgage lending will be the result of a complex interaction of physical climatic effects, incidents of flooding and an economic and societal response.

An increase in insurance industry exposure due to flooding (BU7).

Indirect impact

As per the risk above, this risk is also relatively insensitive to direct climate change effects as this will be the result of a complex interaction of physical climatic effects, incidents of flooding and an economic (insurance) and societal response.

Business, Industry and Services xi

Risk Sensitivity to climate change

An expansion of new or existing tourist destinations in the UK (BU8).

Indirect impact

With its close connections to the environment and climate itself, tourism is considered to be highly sensitive to climate. This is especially the case for this opportunity, because an increase in the attractiveness of the UK as a “sun, sea and sand” tourism destination is dependent on ameliorating climatic conditions (increased temperature and decreased precipitation).

A decrease in output for UK businesses due to an increase in supply chain disruption as a result of extreme events (BU9).

Indirect impact

Because supply chains are complex and dependent on a network of interconnected, yet independent, elements, it is not possible to develop a clear and direct causal link between climate change and supply chain disruption. Many climatic factors (e.g. heat, precipitation, melting, flooding) can break supply chains, making a single response function too simplistic.

Loss of staff hours due to high internal building temperatures (BU10).

Direct impact

High temperatures in the workplace have shown to affect productivity. There is a clear link with temperature, although other parameters such as humidity and ventilation are also important. As such, there is a high degree of sensitivity to climate change and the ability to adapt is likely to vary across the business and industry sector.

A high-level summary of the numerical results and associated costs for each risk analysed in this assessment are presented in the table below.

Risk Numerical results and costs

Reduced returns and/or increased risks of UK financial institutions’ investments due to the absence of mainstreaming climate risk and adaptation into decision-making processes (BU1).

Unavailable (qualitative assessment only)

An increase in monetary losses as a result of an increasing proportion of UK tourist assets (natural and built) at risk from flooding (BU2).

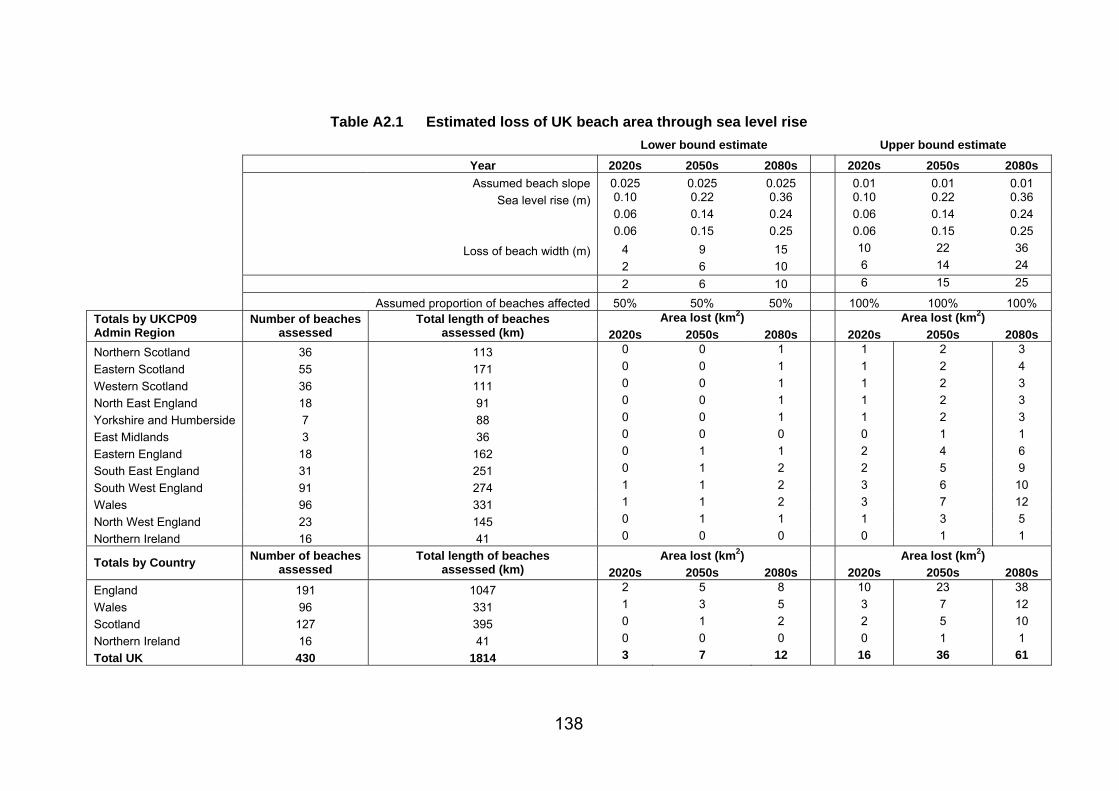

Impact of sea level rise on UK beach area: 3 – 16 km2 of beach is projected to be lost by the 2020s, 12 – 61 km2 (or 3%-7% of total beach area) by the 2080s.

Number of tourist visitor attractions and facilities at risk of flooding (Flood Zone 3) in England: 33,069 buildings. Preventative expenditure, through cost of flood bunds around buildings: £9 million by 2050s and £18 million by 2080s.

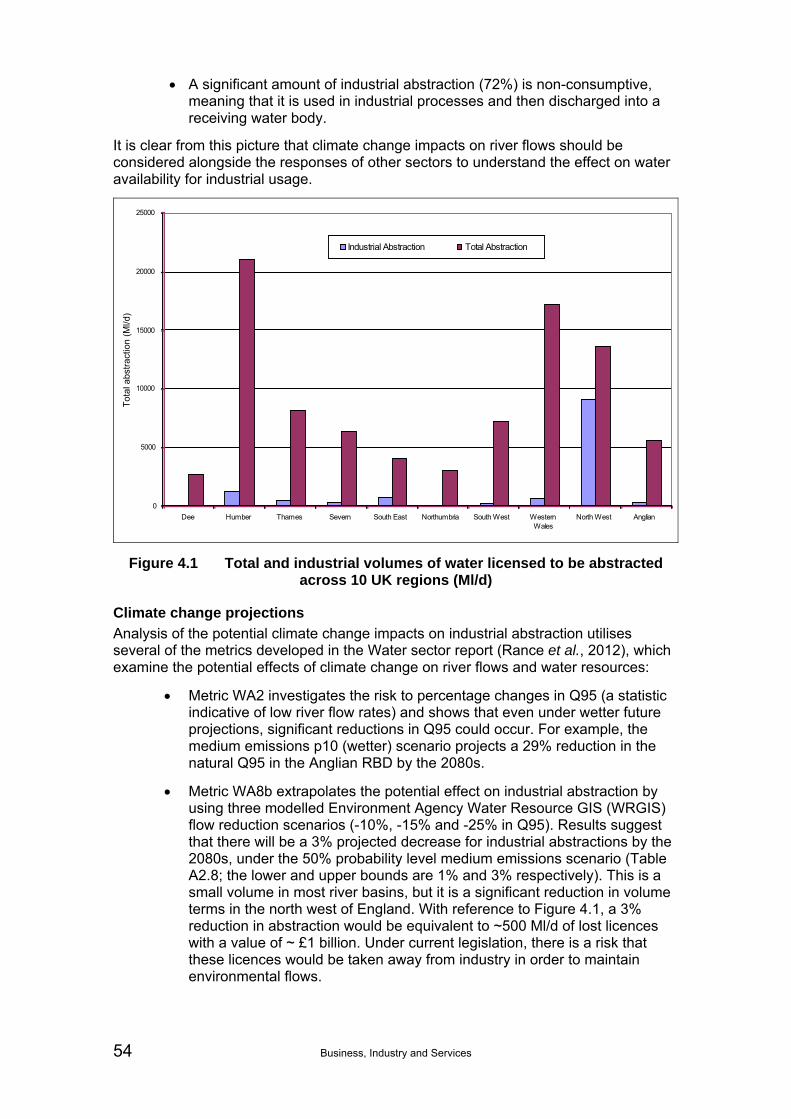

A decrease in water (groundwater and surface water) availability for industrial usage (BU3).

Modelled flow reduction scenarios: between 2% to 3% decrease for industrial abstractions by the 2080s. Change in total value of industrial abstractions that may be prevented if catchments switch from being sustainable to unsustainable in England and Wales: £3.5 million across all time periods.

An increase in monetary losses as a result of interruption to business from flooding (BU4).

Estimated average annual cost to businesses from disruption due to flooding: £24-50 million by the 2020s, £26-72 million by the 2050s and £34-96 million by the 2080s (current figure: £20 million).

A decrease in productivity and revenues due to ICT loss/ disruption (BU5).

Unavailable (qualitative assessment only)

Increased exposure for mortgage lenders (BU6).

Number of residential properties in England and Wales at “significant likelihood” of fluvial and tidal flooding: between 530,000 and 1.5 million by the 2050s and between 700,000 and 2.1 million by the 2080s. Mortgage fund value at risk: £1 to 8 billion and £2 to 9 billion by the 2050s and 2080s, respectively.

An increase in insurance industry exposure due to flooding (BU7).

Annual insurance payout costs for flooding in the UK could increase from a present-day annual average of £200 - £300 million, to £250-400 million by the 2020s and £0.5-1 billion by the 2080s.

An expansion of new or existing tourist destinations in the UK (BU8).

Unavailable (qualitative assessment only)

xii Business, Industry and Services

Risk Numerical results and costs

A decrease in output for UK businesses due to an increase in supply chain disruption as a result of extreme events (BU9).

Unavailable (qualitative assessment only)

Loss of staff hours due to high internal building temperatures (BU10).

Productivity losses due to workplace overheating: between 110% and 230% increase in staff days lost compared to baseline by the 2020s, 140-860% by the 2050s and 150-2,800% by the 2080s. This equates to financial losses of £1.1 billion to £15.2 billion by the 2080s (current estimate: £0.77 billion).

Adaptive capacity The ability of organisations to adapt to climate change is highly variable across the Business, Industry and Services sector and presents a particular challenge to this sector. Despite the large international body of evidence that suggests climate change is a reality, there is still a great deal of inertia within business and industry, with many companies solely considering climate change as a future issue.

There are a number of large, well-resourced and innovative national and multi-national companies based in the UK that are taking climate change adaptation seriously and therefore can demonstrate a high degree of sophistication in terms of climate change risk and opportunity management. On the other hand, the vast majority of organisations have yet to recognise climate change as a material risk, and if they have recognised it, it may only be considered as a long-term, future risk with little relevance to today’s challenges.

Interdependencies The Business, Industry and Services sector is intimately linked to all the other sectors included in the CCRA. From marine and fisheries to built environment, from biodiversity and ecosystem services to transport, business is reliant upon and supports many of the other sectors of the CCRA. Through this assessment, there have been a number of strong linkages that have been discussed; essentially the link between business and the strategic importance of national infrastructure (e.g. roads, rail, energy, telecommunications), as well as the importance of the natural environment (e.g. beaches to attract tourist visitors, or water resource availability for industrial abstraction). The message is clear, business does not operate in a void – these externalities (whether in the UK or overseas) are vitally important for business continuity and growth.

There are also a number of other business value drivers that are important to the Business, Industry and Services sector, such as exchange rates, changes in markets (e.g. consumer expectations), the cost of capital, changes in regulations and Government policy, changing patterns of labour, cost of energy and raw materials. These drivers may all be affected to a greater or lesser degree by climate change, and that these changes will vary going forward. Further analysis is required to understand the climate change effects on these drivers and therefore the overall cumulative effect (adverse or beneficial) for business as a whole.

On the international stage, UK business is once again intimately linked. The growth in globalisation and international supply chains means that there is a high dependence on a global response to climate change adaptation. In fact, the notion of a UK ‘only’ CCRA for business is not representative of the global market in which the UK operates. Climate change is a global problem, affecting UK-based companies working solely in the UK through to UK-listed multinational corporations that have interests in many of

Business, Industry and Services xiii

the countries that will face more severe climate change impacts than the UK. The UK tourist operators’ international interests are a good case in point.

Challenges to overcome In comparison to some other sectors (e.g. water or energy), the Business, Industry and Services sector is typified by a lack of available quantitative data on the potential impacts of climate change. Information that is currently collected is often considered commercially sensitive and remains undisclosed for confidentiality purposes. There is no regulatory requirement on most businesses to report on risks associated with either current and future impacts of climate change on its sector, or on its proposals for adapting to climate change (other than for those organisations who will report under the Adaptation Reporting Power). Some organisations disclose climate change-related information, however, under initiatives such as the Carbon Disclosure Project (CDP).

The report has identified a number of important challenges the Business, Industry and Services sector and Government needs to overcome. These are broadly aligned with a recent publication from the CBI1. In this document, the CBI identifies a number of challenges for business and industry, including:

The challenge of mainstreaming climate change considerations into standard business practices.

Meeting adaptation goals whilst maintaining other corporate goals with respect to sustainability.

There will be an increasing expectation for corporate reporting to disclose material climate-related risks.

Some businesses will be challenged to ‘go it alone’ and the sharing of non-commercially sensitive climate change adaptation information within or across should be encouraged.

Challenges to business will cover six key areas – supply chains, assets, operations, markets, regulatory compliance and business reputation.

To overcome these challenges and provide a robust link between the physical impacts of climate and the risks facing the Business, Industry and Services sector, numerous parties will need to be involved, including climate scientists, risk analysts, the private sector and Government. Individual businesses, and particularly those organisations with a naturally low adaptive capacity, will require a great deal of information sharing and support. Without this, there will be a constant challenge for business and industry to effectively adapt to climate change, build long-term resilience and take the competitive advantage.

1 CBI, 2010. ‘Whatever the weather: managing the risks from a changing climate’

xiv Business, Industry and Services

Business, Industry and Services xv

Key Term Glossary The key terms are defined below.

Adaptation (IPCC AR4, 2007)

Autonomous adaptation – Adaptation that does not constitute a conscious2 response to climatic stimuli but is triggered by ecological changes in natural systems and by market or welfare changes in human systems. Also referred to as spontaneous adaptation.

Planned adaptation – Adaptation that is the result of a deliberate policy decision, based on an awareness that conditions have changed or are about to change and that action is required to return to, maintain, or achieve a desired state.

Adaptive Capacity - The ability of a system to design or implement effective adaptation strategies to adjust to information about potential climate change (including climate variability and extremes), to moderate potential damages, to take advantage of opportunities, or to cope with the consequences (modified from the IPCC to support project focus on management of future risks) (Ballard, 2009). As such this does not include the adaptive capacity of biophysical systems.

Adaptation costs and benefits

The costs of planning, preparing for, facilitating, and implementing adaptation measures, including transition costs.

The avoided damage costs or the accrued benefits following the adoption and implementation of adaptation measures.

Consequence - The end result or effect on society, the economy or environment caused by some event or action (e.g. economic losses, loss of life). Consequences may be beneficial or detrimental. This may be expressed descriptively and/or semi-quantitatively (high, medium, low) or quantitatively (monetary value, number of people affected etc).

Impact - An effect of climate change on the socio-bio-physical system (e.g. flooding, rails buckling).

Response function - Defines how climate impacts or consequences vary with key climate variables; can be based on observations, sensitivity analysis, impacts modelling and/or expert elicitation.

Risk - Combines the likelihood an event will occur with the magnitude of its outcome.

Sensitivity - The degree to which a system is affected, either adversely or beneficially, by climate variability or change.

Uncertainty - A characteristic of a system or decision where the probabilities that certain states or outcomes have occurred or may occur is not precisely known.

Vulnerability - Climate vulnerability defines the extent to which a system is susceptible to, or unable to cope with, adverse effects of climate change including climate variability and extremes. It depends not only on a system’s sensitivity but also on its adaptive capacity. 2 The inclusion of the word ‘conscious’ in this IPCC definition is a problem for the CCRA and we treat this as anticipated adaptation that is not part of a planned adaptation programme. It may include behavioural changes by people who are fully aware of climate change issues.

xvi Business, Industry and Services

Business, Industry and Services xvii

Acknowledgements This report incorporates inputs from a number of organisations, in addition to those consulted during the draft of the scoping reports. The following organisations have contributed to this work.

Association of British Insurers

Cambridge Programme for Sustainability Leadership

Department for Culture, Media and Sport (Northern Ireland)

English Heritage

Environment Agency (Northern Ireland)

Food and Drink Federation

Historic Scotland

IBM

Intellect UK

Mercer

National Parks Authority

National Trust

Natural England

Office of National Statistics

Scottish Natural Heritage

VisitEngland

We also wish to acknowledge the author of the costs assessment (Chapter 6), Alistair Hunt.

xviii Business, Industry and Services

Business, Industry and Services xix

Contents Statement of use v

Executive Summary vii

Key Term Glossary xv

Acknowledgements xvii

Contents xix

1. Introduction 1

1.1 Background 1

1.2 Scope of the Business, Industry and Services Sector Report 3

1.3 Overview of the Business, Industry and Services sector 4

1.4 Policy Context 6

1.5 Structure of this report 9

2. Methods 11

2.1 Introduction: CCRA Framework 11

2.2 Outline of the method used to assess impacts, consequences and risks 12

2.3 Identify and characterise the impacts 14

2.4 Assess vulnerability 14

2.5 Identify the main risks 15

2.6 Assess current and future risk 15

2.7 Report on risks 16

3. Impacts and Risk Metrics 18

3.1 Introduction and Tier 1 analysis 18

3.2 Cross-sectoral and indirect risks 23

3.3 Selection of Tier 2 impacts 27

3.4 Identification of risk metrics 36

4. Sector Risk Analysis 38

4.1 Introduction and response functions 38

4.2 Estimates of changes in selected climate change scenarios 39

5. Socio-Economic Change 89 5.1 Introduction 89

5.2 Estimates of changes in selected social and economic futures 90

6. Costs 94

6.1 Introduction 94

6.2 Economic impacts 95

6.3 Presentation of results, uplifts and discounting 97

7. Adaptive Capacity 103

xx Business, Industry and Services

7.1 Overview 103

7.2 Assessing structural and organisational adaptive capacity 103

7.3 Adaptive Capacity in the Business, Industry and Services Sector 105

8. Conclusions 107

8.1 Key findings 107

8.2 Limitations of current methodology 107

8.3 Challenges to overcome 108

9. References 109

Appendices 119 Appendix 1 Policy background, scoring of Tier 1 impacts and risk scoring

explanation 121

Appendix 2 Response functions and the application of climate projections 137

Appendix 3 Economic impacts 165

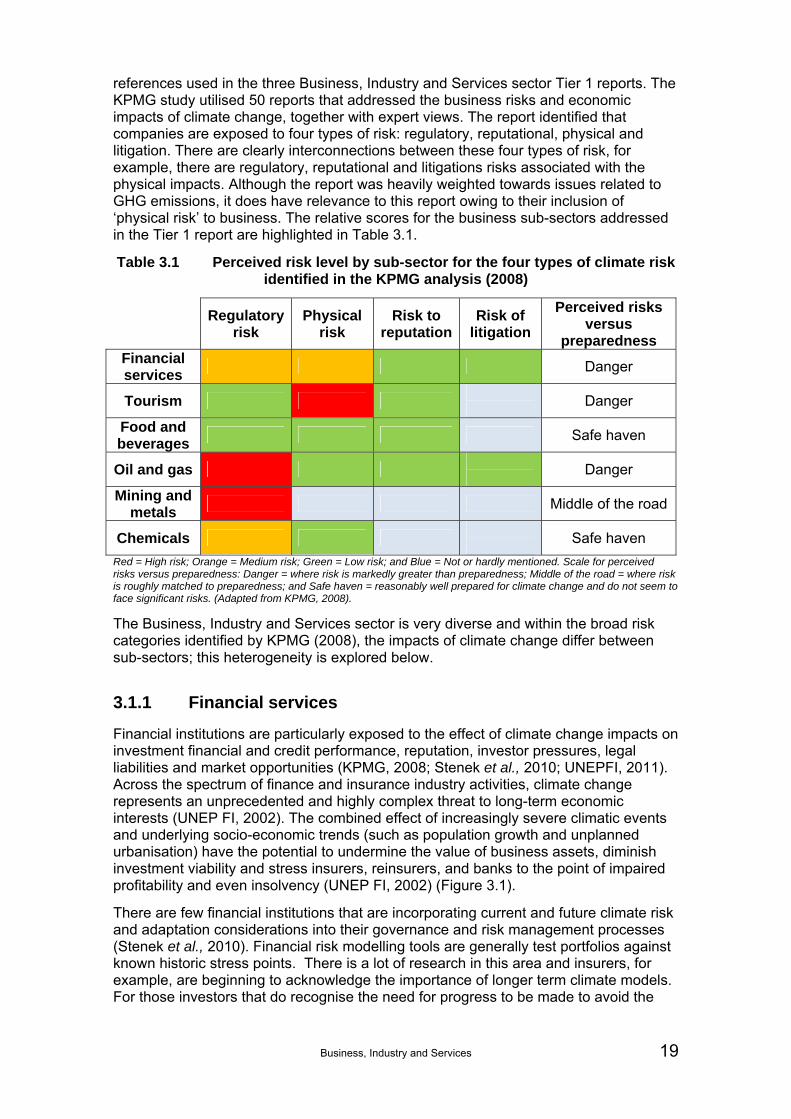

Appendix 4 Social Vulnerability Checklist 169 Tables Table 3.1 Perceived risk level by sub-sector for the four types of climate risk identified in the KPMG analysis

(2008) 19 Table 4.1 Selection of response functions 38 Table 5.1 Socio-economic change summary, with extreme scenarios highlighted where applicable 91 Table 6.1 Summary of results in £million per annum 96 Figures Figure 2.1 Stages of the CCRA (yellow) and other actions for Government (grey) 11 Figure 2.2 Steps of the CCRA Method (that cover Stage 3 of the CCRA Framework: Assess risks) 13 Figure 3.1 Potential climate change impacts on the financial sector (assuming no adaptation) 20 Figure 3.2 Systematic map for the Business, Industry and Services sector based on 4th pass cause of “water

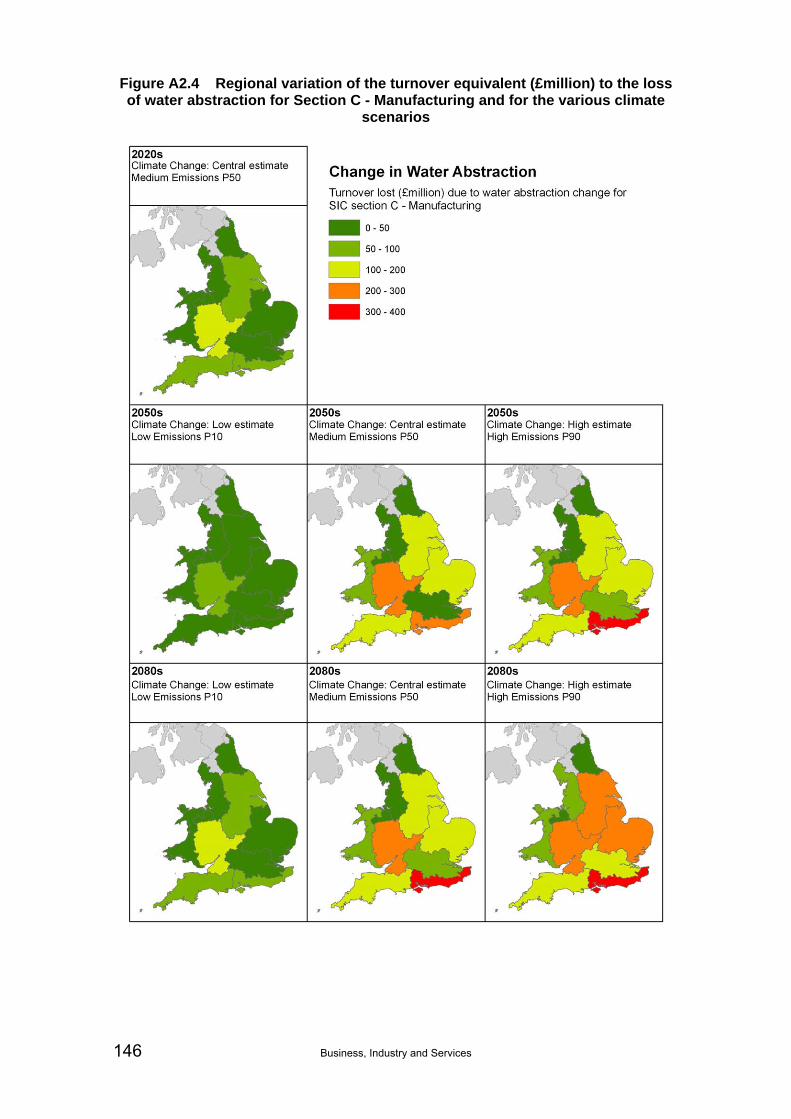

demand” 27 Figure 4.1 Total and industrial volumes of water licensed to be abstracted across 10 UK regions (Ml/d) 54 Figure 4.2 Cost of business interruption in the UK (£m) due to flooding 59 Figure 4.3 Insurance payout for weather related claims in the UK (£m) 69 Figure 4.4 Developments in Tourism Comfort Index (TCI) 73 Boxes Box 4.1 Examples of consequences of climate-related events on financial and credit performance of ‘real

sector’ investments 41 Box 4.2 Major on-going stakeholder-led developments pushing for climate change adaptation

mainstreaming 43 Box 4.3 Community and governmental opposition to mining project in Chile fuelled by climate-related

concerns 43 Box 4.4 Example of impact of average changes in climate on investments 46 Box 4.5 Impacts of floods of summer 2007 on tourism and leisure sector 50 Box 4.6 Impact of 2007 floods on businesses 57 Box 4.7 Case Study: Flooding at BT Exchange in Paddington, London 63 Box 4.8 Case study: 2007 flooding and the impact on transport infrastructure 82

Business, Industry and Services 1

1. Introduction

1.1 Background

It is widely accepted that the world’s climate is being affected by the increasing anthropogenic emissions of greenhouse gases into the atmosphere. Even if efforts to mitigate these emissions are successful, the Earth is already committed to significant climatic change (IPCC, 2007).

Over the past century, the Earth has warmed by approximately 0.7°C3. Since the mid-1970s, global average temperature increased at an average of around 0.17°C per decade4. UK average temperature increased by 1°C since the mid-1970s (Jenkins et al., 2009), however recent years have been below the long-term trend highlighting the significant year-to-year variability. Due to the time lag between emissions and temperature rise, past emissions are expected to contribute an estimated further 0.2°C increase per decade in global temperatures for the next 2-3 decades (IPCC, 2007), irrespective of mitigation efforts during that time period.

The sorts of impacts expected later in the Century are already being felt in some cases, for example:

Global sea levels rose by 3.3 mm per year (± 0.4 mm) between 1993 and 2007; approximately 30% was due to ocean thermal expansion due to ocean warming and 55% due to melting of land ice. The rise in sea level is slightly faster since the early 1990s than previous decades (Cazenave and Llovel, 2010).

Acidification of the oceans caused by increasing atmospheric CO2 concentrations is likely to have a negative impact on the many marine organisms and there are already signs that this is occurring, e.g. reported loss of shell weight of Antarctic plankton, and a decrease in growth of Great Barrier coral reefs (ISCCC, 2009).

Sea ice is already reducing in extent and coverage. Annual average Arctic sea ice extent has decreased by 3.7% per decade since 1978 (Comiso et al., 2008).

There is evidence that human activity has doubled the risk of a very hot summer occurring in Europe, akin to the 2003 heatwave (Stott et al., 2004).

The main greenhouse gas responsible for recent climate change is carbon dioxide (CO2) and CO2 emissions from burning fossil fuels have increased by 41% between 1990 and 2008. The rate of increase in emissions has increased between 2000 and 2007 (3.4% per year) compared to the 1990s (1.0% per year) (Le Quéré et al., 2009). At the end of 2009 the global atmospheric concentration of CO2 was 387.2 ppm (Friedlingstein et al., 2010); this high level has not been experienced on earth for at least 650,000 years (IPCC 2007).

The UK government is committed to action to both mitigate and adapt to climate change5 and the Climate Change Act 20086 makes the UK the first country in the world

3 Global temperature trends 1911-2010 were: HadCRUT3 0.8°C/century, NCDC 0.7°C/century, GISS 0.7°C/century. Similar values are obtained if we difference the decadal averages 2000-2009 and 1910-1919, or 2000-2009 and 1920-1929. 4 Global temperature trends 1975-2010 were: HadCRUT3 0.16°C/decade, NCDC 0.17°C/decade, GISS 0.18°C/decade. 5 http://www.defra.gov.uk/environment/climate/government/

2 Business, Industry and Services

to have a legally binding long-term framework to cut carbon emissions, as well as setting a framework for building the nation’s adaptive capacity. The devolved administrations also have their own strategies and plans in this regard.

The Act sets a clear and credible long term framework for the UK to reduce its greenhouse gas (GHG) emissions including:

A legal requirement to reduce emissions by at least 80% below 1990 levels by 2050 and by at least 34% by 2020.

Compliance with a system of five-year carbon budget, set up to 15 years in advance, to deliver the emissions reductions required to achieve the 2020 and 2050 targets.

In addition it requires the Government to create a framework for building the UK's ability to adapt to climate change and requires Government to:

Carry out a UK wide Climate Change Risk Assessment (CCRA) every five years.

Put in place a National Adaptation Programme (NAP), covering England and reserved matters, to address the most pressing climate change risks as soon as possible after every CCRA.

The purpose of this first CCRA is to provide underpinning evidence, assessing the key risks and opportunities to the UK from climate change, and so enable Government to prioritise climate adaptation policies for current and future policy development as part of the statutory National Adaptation Programme which will begin from 2012. The CCRA will also inform devolved Governments’ policy on climate change mitigation and adaptation.

Climate Change Act: First 5 year Cycle

The Scope of the CCRA covers an assessment of the risks and opportunities to those things which have social, environmental and economic value in the UK, from the current climate and future climate change, in order to help the UK and devolved Governments identify priorities for action and implement necessary adaptation measures. The Government requires the CCRA to identify, assess, and where possible estimate economic costs of the key climate change risks and opportunities for the UK, and for Devolved Governments. The outputs from the CCRA will also be of value to other public and private sector organisations that have a stake in the sectors covered by the assessment.

The CCRA will be accompanied (in 2012) with a study on the Economics of Climate Resilience7 (ECR) that will identify options for addressing some of the priority risks identified by the CCRA, and will analyse their costs and benefits. This analysis will provide an overall indication of the scale of the challenge and potential benefits from acting; and, given the wide-ranging nature of possible interventions, will help to identify priority areas for action by Government on a consistent basis.

This will be followed by the first NAP. The NAP will set out:

objectives in relation to adaptation

proposals and policies for meeting those objectives

timescales

6 http://www.legislation.gov.uk/ukpga/2008/27/contents 7 http://www.defra.gov.uk/environment/climate/government/

Business, Industry and Services 3

an explanation about how those proposals and policies contribute to sustainable development.

The CCRA analysis has been split into eleven sectors to mirror the general sectoral split of climate impacts research; agriculture, biodiversity and ecosystem services, business, industry and services, built environment, energy, floods and coastal erosion, forestry, health, marine and fisheries, transport and water.

1.2 Scope of the Business, Industry and Services Sector Report

This Business, Industry and Services sector report is one of the 11 sector reports commissioned as part of the CCRA contract with HR Wallingford. It is a key step in the process of developing the evidence base required to deliver the UK CCRA to Parliament, as required by the Climate Change Act (2008), by January 2012.

This report gives an overview of the impacts of climate change for the Business, Industry and Services sector in the UK. The diverse nature of this sector has meant that it has not been possible to provide a comprehensive picture of all of the potential climate change risks that the sector is likely to face. For the purposes of this study, the assessment of risks and opportunities for the sector was based on a number of sub-sectors, specifically: financial services; tourism; food and beverages; primary extractives (oil, gas and mining) and chemical manufacturing. These sub-sectors are used as illustrative examples to highlight the range of climate-related issues and challenges the sector as a whole may face. They are of particular significance for three principal reasons:

They rely on large fixed assets (e.g. chemical manufacturing near large main rivers or coastline)

They have complex supply chains (e.g. food and beverages)

They rely substantially on natural assets (e.g. tourism).

Within these sub-sectors, the study has made no distinction based on business size; the risks to Small and Medium Enterprises (SMEs) through to large multi-national corporations has been considered. It is important to highlight that although the focus of the CCRA is on risks in the UK, the inherent international nature of the Business, Industry and Services sector (e.g. UK banks, pension funds and insurers operate in a global market place) means that it is difficult to ignore potential climate impacts in areas outside the UK. However, the international dimensions of climate change, specifically the effects of climate change that could occur outside of the UK and could give rise to threats and opportunities, has been addressed in a recent Foresight Report (2011a). Consequently, the emphasis in this report is placed on UK-based risks and opportunities.

Our analysis follows a predetermined CCRA methodology as expressed in Chapter 2 of this report. Evidence in this report has been obtained from published literature, established datasets and consultation with a range of stakeholder organisations. The consultation process was initiated as a part of an earlier ‘Tier 1’ set of studies (Acclimatise, 2010a, Acclimatise, 2010b, Acclimatise, 2010c) and continued into this phase of work, the selection and analysis of ‘Tier 2’ risks. These organisations are acknowledged in the preface to this report. Our analysis was also undertaken in consultation with UK Government departments including Defra, the Department for Business, Innovation and Skills (BIS), HM Treasury, and the Department of Energy and Climate Change (DECC). The devolved administrations of Scotland, Wales and

4 Business, Industry and Services

Northern Ireland were also consulted to establish a complete picture of the UK and acknowledge differences in climate change policy frameworks.

1.3 Overview of the Business, Industry and Services sector

The Business, Industry and Services sector is extremely diverse. It incorporates a wider range of activities from financial services and retail to manufacturing and food production. These industries occur at a range of scales. Midcap firms (with turnovers between £25 million and £500 million) provide over 20% of UK jobs while, at the same time, there are over 4.8 million registered small and medium enterprises (SMEs) that account for half of all private sector output (HM Treasury, BIS 2011). The varied nature of these activities is mirrored by the subsectors’ uneven geographies. BIS illustrated this with reference to the financial services subsector: “The Greater South East account[ed] for 60% of total UK activity in financial intermediation and more than half of total UK output from real estate, renting and business services in 2006.” (HM Treasury, BIS, 2011).

The IMF forecasts that the world economy will grow by $20 trillion in today’s prices between 2010 and 2015. It expects advanced economies such as the UK to contribute around $8.5 trillion (IMF, 2010). The Business, Industry and Services sector will be the main driver of growth in the UK. BIS has highlighted ‘green’ growth as an area that offers important opportunities for UK firms as the sector emerges from recession. The low-carbon and environmental goods and services sector was estimated to be worth £112 billion in 2008-09 (HM Treasury, BIS, 2011).

The economic case for the taking action to adapt to climate change was made strongly in the 2006 Stern Review on the economics of climate change, which stated that; “many adaptation options… will provide benefits in excess of costs” (Stern, 2006).

This study is based on an analysis of a number of climate risks identified in five sub-sectors of the Business, Industry and Services sector:

Financial services

Tourism

Food and beverages

Primary extractives (oil, gas and mining)

Chemical manufacturing.

Each of these sub-sectors play an important role in driving growth in the UK economy, and each will be affected by the impacts of climate change in a variety of ways.

1.3.1 Financial Services

The UK financial services sub-sector consists of banks, asset managers, insurers, pension funds and other financial service providers. As well as being a significant driver of the UK economy in its own right, it also supports other sectors by providing credit and services to businesses and households. In 2008, it was responsible for 9% of total economic output and contributed 14% of the Treasury’s fiscal revenue (HM Treasury, 2009; Turner et al., 2010). The UK is considered to be an international centre for finance, with inward and outward financial investment flows amounting to more than £10 trillion per year (Bank of England, 2010). This sub-sector employs over 1 million people, and financial services are one of the UK’s largest export industries (HM

Business, Industry and Services 5

Treasury, 2011). In 2008, the countries that received the most investments from UK-owned financial institutions were in the developed world, though emerging markets represent a significant total share of foreign investments (HM Treasury, 2009).

1.3.2 Tourism

According to a recent study by Deloitte and Oxford Economics (2010) tourism was worth £115.4bn to the UK economy in 2009 – equivalent to 8.9% of total UK Gross Domestic Product (GDP). This makes it the UK’s fifth largest “sector”. Approximately 2.6 million people work in tourism accounting for 1 in 12 UK jobs (ibid). On a regional scale, tourism contributes £96.7bn to the economy in England (8.6% of GDP), £11.1bn in Scotland (10.4%), £6.2bn in Wales (13.3%) and £1bn in Northern Ireland (4.9%) (ibid). Over the next decade, the UK’s visitor economy is forecast to be one of the best performing sub-sectors, with above average growth at 3.5% in Gross Value Added (GVA) terms (ibid).

1.3.3 Food and Beverages Manufacturing

Food and beverages is the UK’s largest manufacturing sub-sector and employs over 400,000 people (Defra, 2010, UK Trade & Investment, 2010). The UK is the second most productive food and drinks manufacturer in the world. It contributed GVA £21.8 billion to the UK economy in 2009 (ONS/DEFRA Food Statistics Pocketbook 2009; UKTI, 2010). The Cabinet Office (2008) estimates that in 2008 the sub-sector and its supply chain accounted for 7% of GPD. In 2007, the UK attracted £8.4bn of new overseas investment from food and drink manufacturers (ONS Foreign Direct Investment 2007 Report, 2009). The sub-sector is comprised of over 7,000 enterprises operating almost 10,000 factories (UK Trade and Investment, 2010).

1.3.4 Primary Extractives

Oil and gas production from the UK continental shelf accounted for over 75% of the UK’s total primary energy in 2008 (Oil and Gas UK, 2009). The UK is the largest producer of both oil and gas in the EU and is fourteenth highest globally. Oil and gas is the highest tax contributing sub-sector in the UK, paying £6.9 billion in corporate taxes in 2009-10 (Oil and Gas UK, 2010). In 2010, the sub-sector contributed £27 billion to the economy and directly employed 32,000 people (Oil and Gas UK, 2009). The UK coal sub-sector supports some 10% of all UK electricity supplies (DECC, 2010). With respect to metals and minerals, British-based mining companies deliver two thirds of global iron ore output, the majority of the world’s diamonds, platinum and titanium, and a significant proportion of other metals and minerals (London Mining Network, 2010). UK-listed mining companies together enjoy around half the market capital available to the world’s ten biggest miners (Nostromo Research, 2009).

1.3.5 Chemical Manufacturing

The UK chemicals sub-sector is the largest exporter in UK manufacturing and accounts for approximately 1.5% of GDP (UKTI 2009). UK-based turnover exceeds £57bn and the industry employs over 180,000 people (Chemical Industries Association, 2010). This is a sub-sector where Small and Medium Enterprises (SMEs) play a key role. There are more than 3,100 chemical companies in the UK, with a high proportion being located in the north of England and Scotland.

6 Business, Industry and Services

1.3.6 Cross-Sectoral Linkages

The diverse nature of the sub-sectors within the Business, Industry and Services sector means that the climate risks are wide ranging. Perhaps unsurprisingly there is considerable overlap between the risks faced by the Business, Industry and Services sector and sectors covered by other CCRA reports.

Cross-sectoral linkages include:

Coastal erosion and sea level rise putting tourist assets at risk (Flooding).

Sea level rise and coastal inundation and erosion affect business and industrial assets (Flooding).

Increased flooding impacts on the insurance sub-sector due to increased payout frequency and value (Flooding).

Reduced groundwater levels and increased demand putting pressure on industry and agri-business (Agriculture, Water).

Disruption to port activities due to extreme weather and sea level rise negatively impacting supply chains (Marine).

Subsidence and landslips disrupt road, rail and port facilities and impact on supply chains (Transport).

Negative impact on cultural heritage impacts tourism industry (Built environment).

Loss of staff hours due to increases in internal building temperatures (Built environment).

In light of this the findings of this report should be taken in the context of the other CCRA sector studies, as is considered in the CCRA Evidence Report (CCRA, 2012).

1.4 Policy Context

1.4.1 Introduction

The Business, Industry and Services sector in the UK is administered and regulated by a large number of bodies, reflecting the range of industries and the scales at which they operate. This section presents the main policy instruments and institutions that govern the specific risks (outlined in Chapters 3 and 4) to the five sub-sectors that are the focus of this report.

BIS, HM Treasury, the Bank of England, UK Trade and Investment (UKTI) and trade bodies such as the CBI, administer and communicate UK business policy. Their principal focus is ensuring that the UK remains an attractive place in which to do business. They promote sustainable growth and support businesses to mainstream climate change adaptation policy into their management systems. This is especially important in this sector as much of the responsibility for governing climate adaptation remains with the individual businesses themselves.

For the purposes of the Business, Industry and Service Sector report, it is more instructive to give a picture of the policy framework that governs the risks outlined in Chapters 3 and 4. As such the bullet point text below is not an exhaustive description of all the activities/responsibilities associated with each principal regulatory body. Rather it highlights specific responsibilities that relate to the risks in this report.

Business, Industry and Services 7

Principal regulatory bodies include:

Defra: Leads in England on effective approaches to flood and coastal erosion risk management; managing water resources balanced with growth in the housing sector; and on planning policy for green infrastructure and biodiversity.

BIS: A supporting role for business in mainstreaming adaptation, enabling industries to respond to the future needs and opportunities presented. Supporting research and innovation through partners such as the Technology Strategy Board and Research Councils.

DECC: Responsible for coastal energy infrastructure; electricity infrastructure in flood risk areas; policy on energy demand for cooling buildings; and on methods for assessing energy efficiency to ensure that new build homes are energy efficient and have minimal demands for active cooling.

The Environment Agency: Enforces planning policy for flood and coastal risk management, water quality and green infrastructure in England and Wales. Environmental aspects of water resource management are regulated by the Environment Agency in England and Wales, by the Scottish Environment Protection Agency in Scotland and by the Northern Ireland Environment Agency in Northern Ireland.

Department for Communities and Local Government (CLG): Responsible for planning policy on housing, urban regeneration, and fire and rescue for England. This responsibility is also devolved to appropriate departments in Scotland and Northern Ireland and there is also further planning policy for Wales overseen by the Welsh Government. The CLG is also responsible for national policy on building regulations whether domestic, commercial or industrial.

Department of Health: Responsible for research for policy on heat waves.

HM Treasury, Department for Work and Pensions (DWP) and the Association of British Insurers through the Financial Inclusion Taskforce: Responsible for financial regulation and impacts of climate change for the mortgage and insurance industries.

Heritage bodies: Environmental impacts of industry on the natural environment are monitored to ensure they do not have a damaging impact. Heritage bodies play a particular role in supporting the tourism industry. Responsibility is devolved and is covered by: Natural England and English Heritage in England; the Countryside Council for Wales, Scottish Natural Heritage and the Northern Ireland Environment Agency.

Welsh Government: Responsible for flood and coastal erosion risk management; managing water resources; planning policy; biodiversity; Building Regulations; regeneration; fire and rescue; and health policy.

Scottish Government: Responsible for the implementation of its own Climate Change Act; managing flood risk; coastal flooding; building regulations; planning policy; and tourism.

Northern Ireland Executive: Responsible for some areas of planning policy, building regulations, tourism and transport.

8 Business, Industry and Services

1.4.2 UK Policy

The policy framework for managing the potential future risks of climate change is extremely diverse, reflecting the broad range of the risks that the Business, Industry and Services sector may face. Interdepartmental co-operation is essential to the success of the climate change adaptation framework. Many of the policies outlined in Table A1.1 require the co-operation of key stakeholders in the Business, Industry and Services sector.

The Adaptation Reporting Power contained in the Climate Change Act (2008) is the principle policy lever for the UK Government to influence businesses and help them to mainstream climate change adaptation into their management practices. It is only able to achieve its aims with the support and co-operation of those businesses that it asks to report. Defra has produced guidance to help businesses through the reporting process and has provided advice on ways in which they can implement climate change adaptation strategies. The UK Climate Impacts Programme (UKCIP) has also developed a number of tools that help business in this regard. UKCIP’s Business Areas Climate Assessment Tool (BACLIAT), for example, is a simple checklist that can be used to assess the potential impacts of climate change at an organisational level.

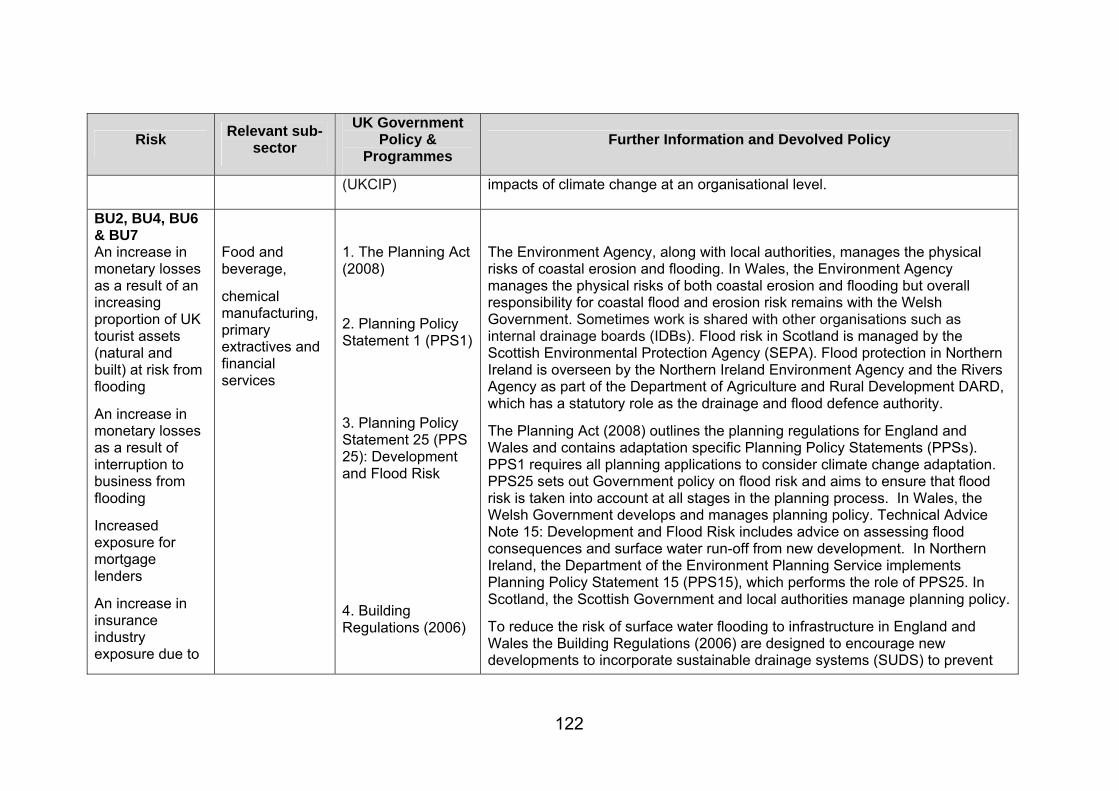

Policy that protects assets from flood risk and coastal erosion, and building regulations and planning policy play a vital role in protecting UK businesses and their supply chains from the negative impacts of climate change. There are a number of pieces of primary legislation that aim to manage these risks, they include: the Planning Act (2008), Planning Policy Statement 1 (PPS1), Planning Policy Statement 25 (PPS 25): Development and Flood Risk, Building Regulations (2006), the Flood and Water Management Act (2010) and the Civil Contingencies Act (2004).

Some of the key policy levers for managing climate change risk are shown in Table A1.1 in Appendix 1. The reference numbers (BU1, etc) refer to the risks analysed in this report, as listed in Table 3.3.

1.4.3 Devolved Policy

How policy is implemented varies across the devolved administrations. Some of the key differences are explored below.

Scotland

The Scottish Government is committed to implementing climate change adaptation policy through the Climate Change (Scotland) Act (2009), which governs Scottish climate policy. The Act requires public bodies in Scotland to ensure that they put measures in place to help with the implementation of an adaptation programme. The Act contains an adaptation reporting power, which requires public bodies to report on their adaptation strategies; however, unlike in England, there are currently no plans to use this power. Additionally, the adaptation reporting power in force in the English Climate Change Act (2008) is broader, enabling Government to require private businesses and organisations that perform a public function (such as utility companies) to report on their adaptation plans.

The Scottish Government and its agencies oversee adaptation policy. Scottish Enterprise, Scottish Environment Protection Agency and the Scottish Climate Change Impacts Partnership (SCCIP) have central roles in mainstreaming adaptation into the management strategies of Scottish businesses.

Wales

The Welsh Government sets out its vision for providing the conditions and framework to enable the private sector to grow and flourish in Economic Renewal: a new direction

Business, Industry and Services 9

(2010). A prominent sub-sector in Wales is tourism, which relies heavily on the condition of the environment. Consistent with its central organising principle of sustainable development, the Welsh Government’s Sustainable Tourism Framework (2007) highlights the need to manage and adapt to climate change as being of critical importance to the future of sustainable tourism in Wales.

One of the five priorities set out in Economic Renewal is the need for investment in high-quality and sustainable infrastructure. This priority is also recognised in the Welsh Government’s Energy Policy Statement, Spatial Plan and Transport Strategy.

Through the Climate Change Strategy for Wales, the Welsh Government is implementing an Adaptation Framework, which is designed to incorporate climate change adaptation into decision-making in the private, public and voluntary sectors. The Strategy was developed and is being delivered in Partnership with the Climate Change Commission for Wales that aims to drive action on climate change in Wales. The business community is represented on the Commission by the Confederation of British Industries (Wales) and the Federation of Small Businesses. The Climate Change Strategy and the Climate Change Communications and Engagement Strategy include commitments to engage with private sector organisations, highlighting the need for businesses to understand and plan for the threats and opportunities arising from a changing climate.

Planning Policy Wales helps to ensure the resilience of the built environment and reduce the risk of disruption to business activities as a result of climate change. This is supplemented by Technical Advice Notes (TANs), including TAN15 – Development and Flood Risk, and TAN22 - Sustainable Buildings. Building Regulations will be devolved in January 2012, after which time the Welsh Government will be able to set standards for new buildings, including non-domestic buildings, and intends to utilise these powers to improve further the resilience of the built environment to climate change.

Northern Ireland

The Climate Change Act (2008) is implemented in Northern Ireland by the Northern Irish Executive and the Adaptation Reporting Power operates here in the same way as it does in England. The Northern Ireland strategy for adaptation is laid out in the report ‘Preparing for a Changing Climate in Northern Ireland’ (2007).

Climate change adaptation policy in Northern Ireland is largely transposed from UK policy and is managed by a series of regional strategies (such as the Region Transportation Strategy for Northern Ireland), many of which fall under the Regional Development Strategy managed by the Department for Regional Development. Planning policy, as with the other UK regions, is devolved to local councils.

1.5 Structure of this report

Following this introduction chapter, Chapter 2 presents the risk assessment methodology adopted in the CCRA. The subsequent and remaining chapters of the report then broadly follow the risk assessment steps outlined in Chapter 2 and Figure 2.2. Chapter headings and sub-headings clearly make reference the relevant step of the risk assessment methodology.

Chapter 3 provides an overview of the risks and opportunities identified for the sector. It is linked to the full list of identified risks located in Appendix 1.

Chapter 4 contains the main body of the analysis. In this chapter, an assessment and quantification of the key risks / opportunities is presented. For each risk identified for the Business, Industry and Services sector, the approach taken is to include as applicable:

10 Business, Industry and Services

An introduction and supporting evidence

Details of identified metrics and presentation of the “response function”

Incorporation of future climate change projections

Presentation of data assumptions and limitations

Conclusions

The majority of the technical and supporting information (data tables and figures) for the risk analysis is located in Appendix 2. These are referenced as necessary in the text (e.g. Table A2.* and Figure A2.*).

Chapter 5 considers the way in which the social and economic future of the UK may affect the risks and Chapter 6 presents possible economic impacts of the 10 selected risks.

Chapter 7 introduces the adaptive capacity of the Business, Industry and Services sector as a whole, as well as the sub-sectors this report focuses on. An assessment of current adaptive capacity across the sectors is the subject of an ongoing Defra study.

Finally, Chapter 8 summarises the main conclusions of this report, outlining the limitations of the current methodology, including strengths and weaknesses, together with the main challenges the Business, Industry and Services sector faces regarding climate change adaptation.

Business, Industry and Services 11

2. Methods

2.1 Introduction: CCRA Framework

The overall aim of the CCRA is to inform UK adaptation policy by assessing the main current and future risks (threats and opportunities) posed by the current climate and future climate change for the UK to the year 2100. The overall approach to the risk assessment and subsequent adaptation plan is based on the UK Climate Impacts Programme (UKCIP) Risk and Uncertainty Framework (UKCIP, 2003). The framework comprises eight stages as shown in Figure 2.1. The CCRA has undertaken the Stages 1, 2 and 3 as outlined below. Stages 4 and 5 will be addressed as part of a separate economic assessment, entitled the ‘Economics of Climate Resilience’, and the remaining stages will be implemented by the UK Government and Devolved Administrations. The framework presents a continual process that can adapt as new evidence and policy emerges; in the case of the CCRA the process will be revisited every five years.

Figure 2.1 Stages of the CCRA (yellow) and other actions for Government (grey)

Adapted from UKCIP (2003)

Stage 1 is defined by the aim of the CCRA project, to undertake an assessment of the main risks (including both threats and opportunities) posed by climate change that will have social, environmental and economic consequences for the UK.

Stage 2 established decision-making criteria for the study, which were used to inform the selection of impacts for analysis in Stage 3. These criteria are the social, environmental and economic magnitude of consequences and the urgency of taking adaptation action for UK society as a whole.

Stage 3 covers the risk assessment process. This involved a tiered assessment of risks with Tier 1 (broad level) identifying a broad range of potential impacts and Tier 2 (detailed level) providing a more detailed

12 Business, Industry and Services

analysis including quantification and monetisation of some impacts. A list of climate change impacts was developed based on eleven sectors with further impacts added to cover cross-cutting issues and impacts which fell between sectors. This list of climate change impacts is referred to as the ‘Tier 1 list of impacts’. This list contained over 700 impacts – too many to analyse in detail as part of this first CCRA. A consolidated list of the highest priority climate change impacts for analysis was developed and referred to as the ‘Tier 2 list of impacts’. This report presents the risk assessment for Tier 2 impacts.

The background to the framework and approach used for each of the first three stages is set out in more detail in the CCRA Method Report (Defra, 2010b). This chapter aims to summarise the CCRA method for the risk assessment stage (Stage 3 in the framework above) because this includes the specific steps for which results are presented in this report.

2.2 Outline of the method used to assess impacts, consequences and risks

The risk assessment presented in this report is the focus of Stage 3 in the CCRA Framework (see Figure 2.1). This was done through a series of steps as set out in Figure 2.2. These steps are explained in Sections 2.3 - 2.7 below and are discussed in more detail in the CCRA Method report (Defra, 2010).

The components of the assessment sought to:

Identify and characterise the impacts of climate change.

This was achieved by developing the Tier 1 list of impacts, which included impacts across eleven sectors as well as impacts not covered by the sectors and arising from cross sector links (presented in Chapter 3.1 and 3.2).

Identify the main risks for closer analysis.

This involved the selection of Tier 2 impacts for further analysis from the long list of impacts in Tier 1. Higher priority impacts were selected by stakeholder groups based on the social, environmental and economic magnitude of impacts and the urgency of taking action (presented in Chapter 3.3).

Assess current and future risk, using climate projections and considering socio-economic factors.

The risk assessment was done by developing ‘response functions’ that provide a relationship between changes in climate with specific consequences based on analysis of historic data, the use of models or expert elicitation. In some cases this was not possible, and a narrative approach was taken instead. The UKCP09 climate projections and other climate models were then applied to assess future risks. The potential impact of changes in future society and the economy was also considered to understand the combined effects for future scenarios (presented in Chapter 5).

Assess vulnerability of the UK as a whole.

This involved:

i. a high level review of Government policy on climate change in the eleven sectors (see Chapter 1 of this report)

Business, Industry and Services 13

ii. a high level assessment of social vulnerability to the climate change impacts (see Appendix 4 of this report)

iii. a high level assessment of the adaptive capacity of the sectors. This is the subject of an ongoing study by Defra to be reported later in 2012, but see Chapter 7 of this report for a preliminary view and Section 2.4 below for an overview of the approach).

Report on risks to inform action.

This report presents the results of the risk assessment for the Business, Industry and Services sector. The results for the other ten sectors are presented in similar reports and the CCRA Evidence Report (CCRA, 2012) draws together the main findings from the whole project, including consideration of cross-linkages, and outlines the risks to the UK as a whole.

Figure 2.2 Steps of the CCRA Method (that cover Stage 3 of the CCRA Framework: Assess risks)

14 Business, Industry and Services

2.3 Identify and characterise the impacts

Step 1 – Literature review and Tier 1 analysis

This step scoped the potential impacts of climate change on the UK based on existing evidence and collating the findings from literature reviews, stakeholder participation through workshops, correspondence with wider stakeholders and soliciting expert opinion. This work developed the Tier 1 list of impacts (see Appendix 1). The Tier 1 impacts have not been analysed in detail; high level discussion of these impacts is provided in Chapter 3 of this report.

Due to the natural diversity of the Business, Industry and Services sector, the Tier 1 analysis involved the scoping of climate change impacts and risks for the following three sub-sectors:

1. Financial services (banks, pension funds and insurance) and tourism (Acclimatise, 2010a)

2. Food and beverage manufacturing (Acclimatise, 2010b)

3. Primary extractive industries (oil, gas and mining) and chemical manufacturing (Acclimatise, 2010c).

Step 2 – Cross sectoral and indirect impacts

The Tier 1 lists for the eleven sectors in CCRA were compared and developed further to include cross-sectoral and indirect impacts. This was done by ‘Systematic Mapping’, which sets out a flow chart to link causes and effects in a logical process. The impacts that were identified in this step were added to the Tier 1 list of impacts.

2.4 Assess vulnerability

Step 3 – Review of Policy

Government policy on climate change develops and changes rapidly to keep pace with emerging science and understanding of how to respond through mitigation and adaptation. This report includes an overview of selected relevant policy in Chapter 1 as this provides important context for understanding how risks that are influenced by climate relate to existing policies. This information will be expanded in the Economics of Climate Resilience project and the National Adaptation Programme.

Step 4 – Social Vulnerability

The vulnerability of different groups in society to the climate change risks for each sector was considered at a high level through a check list. The completed check list for the Business, Industry and Services sector is provided in Appendix 4. This information is provided for context; it is not a detailed assessment of social vulnerability to specific risks. Note that this step is different from Step 10, which considers how future changes in society may affect the risks.

Step 5 – Adaptive Capacity

The adaptive capacity of a sector is the ability of the sector as a whole, including the organisations involved in working in the sector, to devise and implement effective adaptation strategies in response to information about potential future climate impacts. A high level initial overview of the adaptive capacity of the Business, Industry and Services sector has been carried out through literature review and is presented in Chapter 7. This information is provided for context. An assessment of adaptive capacity is ongoing and will be reported on later in 2012.

Business, Industry and Services 15

2.5 Identify the main risks

Step 6 – Selection of Tier 2 impacts

The Tier 1 list of impacts for each sector that resulted from Step 2 (see above) was consolidated to select the higher priority impacts for analysis in Tier 2. Firstly, similar or overlapping impacts were grouped where possible in a simple cluster analysis, which is provided in Chapter 3. Secondly, the Tier 2 impacts were selected using a simple multi-criteria assessment based on the following criteria:

the social, economic and environmental magnitude of impacts

overall confidence in the available evidence

the urgency with which adaptation decisions needs to be taken.

Each of these criteria were allocated a score of 1 (low), 2 (medium) or 3 (high) and the impacts with highest scores over all criteria were selected for Tier 2 analysis. The scoring for each sector was carried out based on expert judgement and feedback from expert consultation workshops (or telephone interviews). Checks were carried out to ensure that a consistent approach was taken across all the sectors. The results of the scoring process are provided in Appendix 1.

Step 7 – Identifying risk metrics