clean energy outlook - dallas fed

TRANSCRIPT

Clean Energy Outlook

Logan Goldie-Scot

Head of Clean Power

November 20, 2020

Federal Reserve Bank of Dallas

1 November 20, 2020

Solar module price ($/W)

XP Curve = 28.8%

Wind turbine price ($/W)

XP Curve = 7.1%

Falling technology costs are key to the decarbonization of power and transport

Source: BloombergNEF

0.1

1

10

100

0 0 10 1,000

1976

$/W

2019e0

1

10

100

0 1 10 100 1,000

1985

$/W

2020

2010

2019

10

100

1,000

10,000

10 1,000 100,000

$/kWh

Batteries pack price ($/kWh)

XP Curve = 18%

Cumulative installed capacity (GW) Cumulative installed capacity (GW) Cumulative capacity (MWh)

2 November 20, 2020

Source: BloombergNEF Note: 2017 multi module efficiency was adjusted downwards from the 2018 PV manufacturing overview to reflect the industry average

instead of pure survey results.

PV is increasingly efficient

Average year-end PV module efficiency

15.8%16.3%

16.7%17.1%

17.6%18.0%

18.5%

19.3%

15.4%15.7%

16.0% 16.1% 16.3%16.6% 16.8%

17.1%

2012 2013 2014 2015 2016 2017 2018 2019

Mono module

Multi module

3 November 20, 2020

Source: BloombergNEFSource: BloombergNEF

Wind capacity factors are on the rise

Onshore wind Offshore wind

Wind capacity factors by technology

0%

15%

30%

45%

60%

2020 2025 2030 2035 2040 2045 2050

U.K.

Germany

U.S.

China

4 November 20, 2020

Source: BloombergNEF

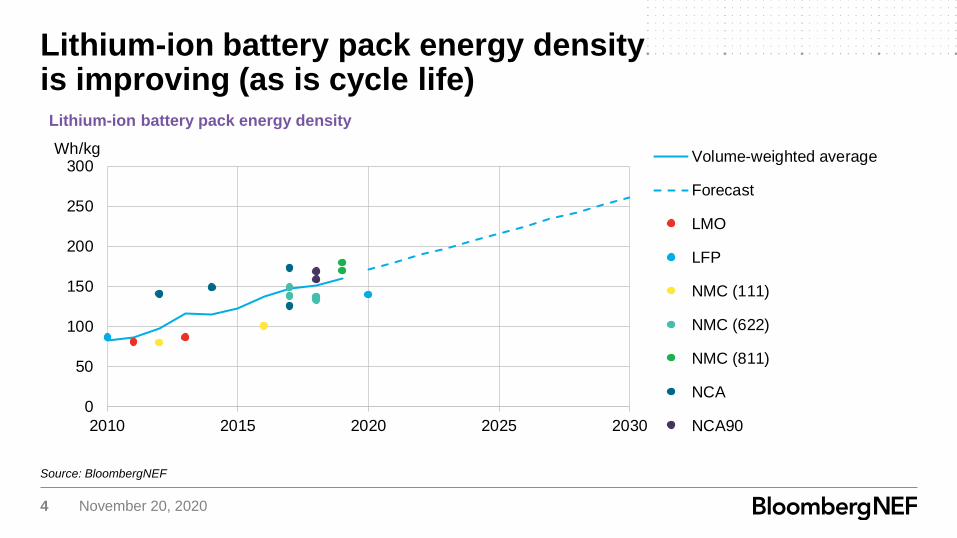

Lithium-ion battery pack energy density is improving (as is cycle life)Lithium-ion battery pack energy density

0

50

100

150

200

250

300

2010 2015 2020 2025 2030

Wh/kgVolume-weighted average

Forecast

LMO

LFP

NMC (111)

NMC (622)

NMC (811)

NCA

NCA90

5 November 20, 2020

Source: BloombergNEF. Note: LCOEs exclude tax-credits (ITC & PTC) and curtailment. The LCOE range represents a range of costs and capacity factors. Battery

storage systems (co-located and stand-alone) presented here have four-hour storage. In the case of solar-and wind-plus-battery systems,the range is a combination

of capacity factors and size of the battery relative to the power generating asset (25% to 100% of total installed capacity).

Wind and PV are among the cheapest forms of generation in the U.S.United States levelized cost of electricity

26 32

84

3360

193

3952

69

13659 50

56

105

59

84

77

157340

106

0

50

100

150

200

250

300

350

400

Onshorewind

Tracking PV Offshorewind

CCGT Coal Nuclear Onshorewind +storage

Fixed-axisPV + storage

OCGT Utility-scalebattery (4h)

$/MWh (nominal)

6 November 20, 2020

Wind and PV grow to 56% of global electricity generation in 2050

Source: BloombergNEF, IEA

56%

wind &

PV

24% fossil fuels

76% zero carbon

Global electricity generation

Coal

Gas

Oil

Nuclear

Hydro

Wind

Solar

Other

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1970 1980 1990 2000 2010 2020 2030 2040 2050

7 November 20, 2020

Source: BloombergNEF

PV, wind and energy storage is a least-cost combination to 70-80% renewablesShare of wind and solar as % of total annual generation

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2015 2020 2025 2030 2035 2040 2045 2050

Germany

Italy

Iberia

U.S.

Canada

Brazil

China

India

Average

8 November 20, 2020

Source: BloombergNEF

In the U.S., renewables and gas have thrived over the last decade at the expense of coalNet U.S. power generation additions (GW)

-30

-20

-10

0

10

20

30

40

2005 2007 2009 2011 2013 2015 2017 2019

Wind

Sub-Bituminous

Solar (DG)

Solar

Nuclear

Lignite

Gas OC / Steam

Gas CC

Bituminous

9 November 20, 2020

Source: BloombergNEF

Coal and nuclear continue to struggle based on economics aloneCoal and nuclear capacity retirements, United States

-40

-30

-20

-10

0

2015 2020 2025 2030 2035 2040 2045 2050

GW

Nuclear

Coal

10 November 20, 2020

Source: BloombergNEF

Wind, solar and gas (in the 2020s) continue to thriveU.S. power generation capacity additions (GW)

-15

-10

-5

0

5

10

15

20

25

30

2015 2020 2025 2030 2035 2040 2045 2050

GWSmall-scale batteries

Utility-scale batteries

Other

Solar thermal

Small-scale PV

Utility-scale PV

Offshore wind

Onshore wind

Biomass

Geothermal

Pumped hydro

Hydro

Nuclear

Oil

Peaker gas

Combined-cycle gas

Coal

11 November 20, 2020

Source: BloombergNEF

Renewables overtake gas as the leading source of generation in 2041U.S. gross generation (TWh)

0

1,000

2,000

3,000

4,000

5,000

6,000

2015 2020 2025 2030 2035 2040 2045 2050

Other

Solar thermal

Small-scale PV

Utility-scale PV

Offshore wind

Onshore wind

Biomass

Geothermal

Hydro

Nuclear

Oil

Peaker gas

Combined-cycle gas

Coal

12 November 20, 2020

Source: BloombergNEF Note: ETS stands for Energy Transition Scenario

Wind and solar make up some 60% of total installed capacity in California in the ETSInstalled power generation capacity (GW) in California, Economic Transition Scenario

0

50

100

150

200

250

300

350

2012 2020 2025 2030 2035 2040 2045 2050

Small-scale batteries

Utility-scale batteries

Other

Solar thermal

Small-scale PV

Utility-scale PV

Offshore wind

Onshore wind

Biomass

Geothermal

Pumped hydro

Hydro

Nuclear

Oil

Peaker gas

Combined-cycle gas

Coal

13 November 20, 2020

Source: BloombergNEF

Meeting California state goals requires much more capacity (solar+storage)Installed power generation capacity (GW) in California, Renewable Portfolio Standard Scenario

0

50

100

150

200

250

300

350

2012 2020 2025 2030 2035 2040 2045 2050

Small-scale batteries

Utility-scale batteries

Other

Solar thermal

Small-scale PV

Utility-scale PV

Offshore wind

Onshore wind

Biomass

Geothermal

Pumped hydro

Hydro

Nuclear

Oil

Peaker gas

Combined-cycle gas

Coal

14 November 20, 2020

Net-zero pledges of top global

economies

1. United States

2. China

3. Japan

4. India

5. Germany

6. United Kingdom

7. France

8. Italy

9. Brazil

10. Canada

11. Russia

12. South Korea

U.S. federal policy changes could be similarly impactful

Source: Bloomberg

×

×

×

×

15 November 20, 2020

The U.S. currently lags behind Europe and China in terms of EV sales

Passenger electric vehicle sales (millions)

2.3

0.040.1 0.2

0.30.5

0.7

1.1

1.9

2.1

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020e

Rest of world

Japan and Korea

North America

Europe

China

Source: BloombergNEF. Includes BEVs and PHEVs

16 November 20, 2020

Policy Performance Corporate actions

Transitions are slow, right up until they’re not

Source: VolkswagenSource: Jean Chung/Bloomberg Source: Tomohiro Ohsumi/Bloomberg

17 November 20, 2020

Source: BloombergNEF

Passenger vehicles electrify quickly from the mid-2020s based on economics

Electric vehicle share of global new vehicle sales

0%

10%

20%

30%

40%

50%

60%

70%

80%

2020 2025 2030 2035 2040

Buses

Two-wheelers

Passenger vehicles

Light commercial

Medium commercial

Heavy commercial

18 November 20, 2020

Two ways to think about O&G transition strategies

Shareholder pressure and

ESG considerations

Disclosure

requirements

Alignment to

political goals in

home markets

Social license to

operate

The business rationale for

investing in new and clean

energy

1 2

19 November 20, 2020

Shell at BNEF New York Summit, 2019

We believe we can be the largest

electricity power company in the world in

the early 2030s.

Maarten Wetselaar, Integrated Gas &

New Energies Director, Shell

“

20 November 20, 2020

Interested in learning more about BNEF?

Contact: Brent Smelter, Commercial Director (BNEF)

Email: [email protected]

21 November 20, 2020

Copyright

© Bloomberg Finance L.P. 2020. This publication is the copyright of Bloomberg Finance L.P. in connection with BloombergNEF. No portion of this document may be

photocopied, reproduced, scanned into an electronic system or transmitted, forwarded or distributed in any way without prior consent of BloombergNEF.

Disclaimer

The BloombergNEF ("BNEF"), service/information is derived from selected public sources. Bloomberg Finance L.P. and its affiliates, in providing the

service/information, believe that the information it uses comes from reliable sources, but do not guarantee the accuracy or completeness of this information, which is

subject to change without notice, and nothing in this document shall be construed as such a guarantee. The statements in this service/document reflect the current

judgment of the authors of the relevant articles or features, and do not necessarily reflect the opinion of Bloomberg Finance L.P., Bloomberg L.P. or any of their

affiliates (“Bloomberg”). Bloomberg disclaims any liability arising from use of this document, its contents and/or this service. Nothing herein shall constitute or be

construed as an offering of financial instruments or as investment advice or recommendations by Bloomberg of an investment or other strategy (e.g., whether or not

to “buy”, “sell”, or “hold” an investment). The information available through this service is not based on consideration of a subscriber’s individual circumstances and

should not be considered as information sufficient upon which to base an investment decision. You should determine on your own whether you agree with the

content. This service should not be construed as tax or accounting advice or as a service designed to facilitate any subscriber’s compliance with its tax, accounting or

other legal obligations. Employees involved in this service may hold positions in the companies mentioned in the services/information.

The data included in these materials are for illustrative purposes only. The BLOOMBERG TERMINAL service and Bloomberg data products (the “Services”) are

owned and distributed by Bloomberg Finance L.P. (“BFLP”) except (i) in Argentina, Australia and certain jurisdictions in the Pacific islands, Bermuda, China, India,

Japan, Korea and New Zealand, where Bloomberg L.P. and its subsidiaries (“BLP”) distribute these products, and (ii) in Singapore and the jurisdictions serviced by

Bloomberg’s Singapore office, where a subsidiary of BFLP distributes these products. BLP provides BFLP and its subsidiaries with global marketing and operational

support and service. Certain features, functions, products and services are available only to sophisticated investors and only where permitted. BFLP, BLP and their

affiliates do not guarantee the accuracy of prices or other information in the Services. Nothing in the Services shall constitute or be construed as an offering of

financial instruments by BFLP, BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affi liates of an investment strategy or

whether or not to “buy”, “sell” or “hold” an investment. Information available via the Services should not be considered as information sufficient upon which to base an

investment decision. The following are trademarks and service marks of BFLP, a Delaware limited partnership, or its subsidiaries: BLOOMBERG, BLOOMBERG

ANYWHERE, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG PROFESSIONAL, BLOOMBERG TERMINAL and BLOOMBERG.COM. Absence of

any trademark or service mark from this list does not waive Bloomberg’s intellectual property rights in that name, mark or logo. All rights reserved. © 2020 Bloomberg.

Copyright and disclaimer

Coverage.

Clean energy

Advanced transport

Commodities

Digital industry

BloombergNEF (BNEF) is a leading provider

of primary research on clean energy,

advanced transport, digital industry,

innovative materials, and commodities.

BNEF’s global team leverages the world’s

most sophisticated data sets to create clear

perspectives and in-depth forecasts that

frame the financial, economic and policy

implications of industry-transforming trends

and technologies.

BNEF research and analysis is accessible via

web and mobile platforms, as well as on the

Bloomberg Terminal.

Client enquiries:

Bloomberg Terminal: press <Help> key twice

Email: [email protected]

Learn more:

about.bnef.com | @BloombergNEF

Logan Goldie-Scot