clean energy finance: opportunities for state action · clean energy finance: opportunities for...

TRANSCRIPT

Clean Energy Finance: Opportunities for State Action

Colin Bishopp | July 25, 2014

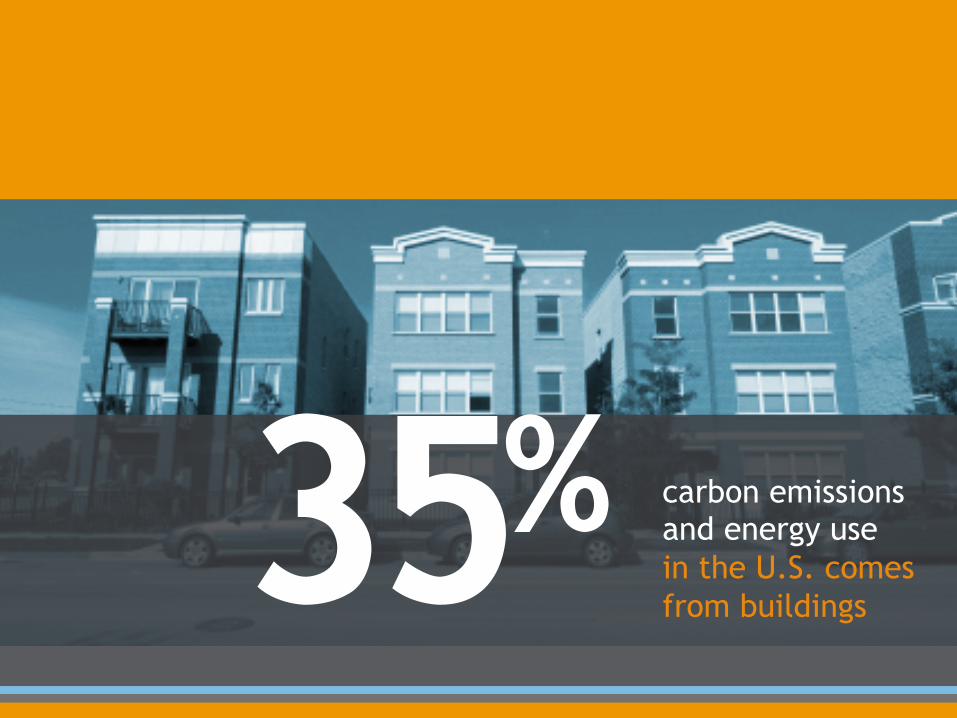

35% carbon emissions and energy use in the U.S. comes from buildings

Inside the $40+* billion/year Home Energy Improvement Market

HVAC $18 B

Windows & Doors $9 B

Home Performance & Solar $2.9 B

Roofs $12.5 B

Reactive Replacement

Proactive Performance

3

The home energy improvement market spans a broad spectrum from reactive equipment replacement to proactive home performance and renewable energy projects

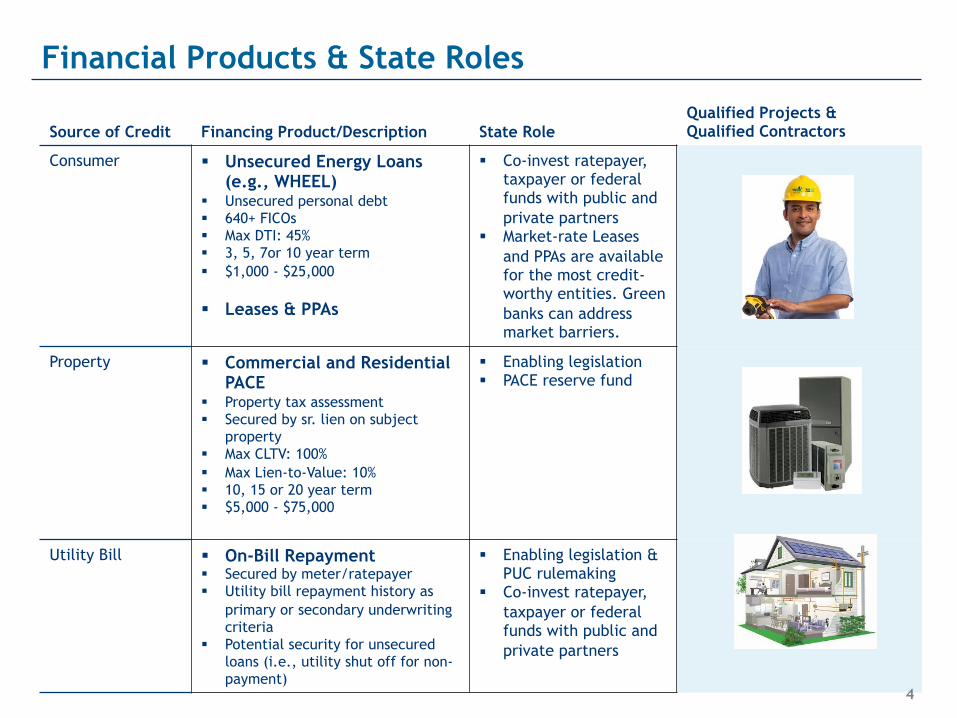

Source of Credit Financing Product/Description State Role Qualified Projects & Qualified Contractors

Consumer § Unsecured Energy Loans (e.g., WHEEL)

§ Unsecured personal debt § 640+ FICOs § Max DTI: 45% § 3, 5, 7or 10 year term § $1,000 - $25,000 § Leases & PPAs

§ Co-invest ratepayer, taxpayer or federal funds with public and private partners

§ Market-rate Leases and PPAs are available for the most credit-worthy entities. Green banks can address market barriers.

Property § Commercial and Residential PACE

§ Property tax assessment § Secured by sr. lien on subject

property § Max CLTV: 100% § Max Lien-to-Value: 10% § 10, 15 or 20 year term § $5,000 - $75,000

§ Enabling legislation § PACE reserve fund

Utility Bill § On-Bill Repayment § Secured by meter/ratepayer § Utility bill repayment history as

primary or secondary underwriting criteria

§ Potential security for unsecured loans (i.e., utility shut off for non-payment)

§ Enabling legislation & PUC rulemaking

§ Co-invest ratepayer, taxpayer or federal funds with public and private partners

Financial Products & State Roles

4

Benjamin Franklin: Patron Saint of Special Districts

37,000 Special Assessment Districts From Mosquito Abatement to Undergrounding of Utilities

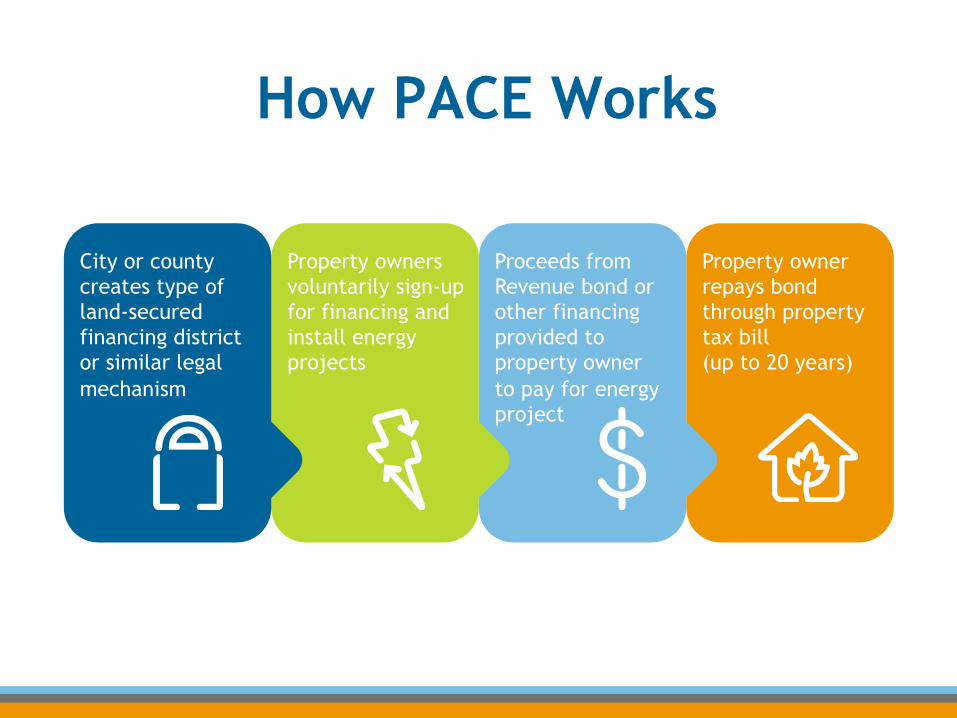

How PACE Works

Property owner repays bond through property tax bill (up to 20 years)

Proceeds from Revenue bond or other financing provided to property owner to pay for energy project

Property owners voluntarily sign-up for financing and install energy projects

City or county creates type of land-secured financing district or similar legal mechanism

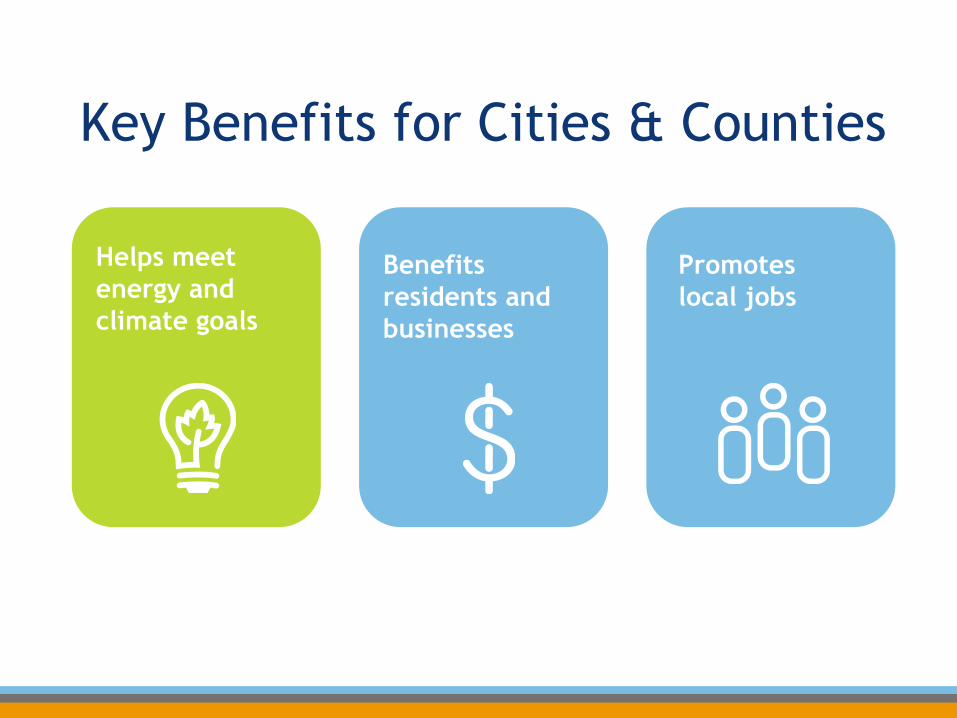

Key Benefits for Cities & Counties

Helps meet energy and climate goals

Promotes local jobs

Benefits residents and businesses

Key Benefits for Property Owners

Saves money on utility bills

Repayment can transfer to new owner

Not based on personal credit

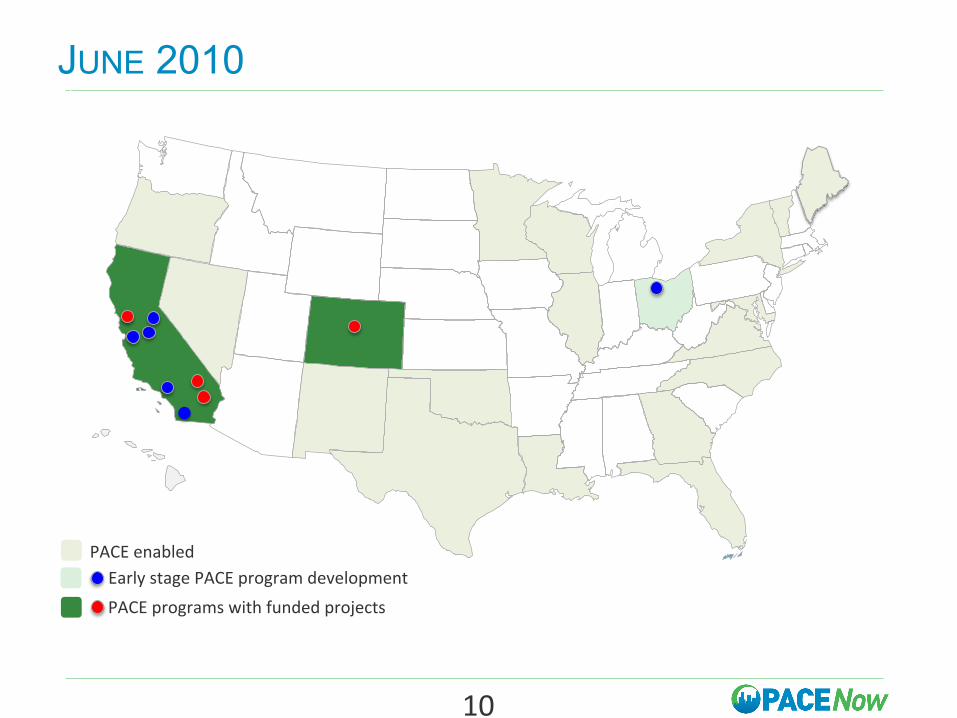

Early stage PACE program development

PACE programs with funded projects

JUNE 2010

10

PACE enabled

10

PACE programs with funded projects

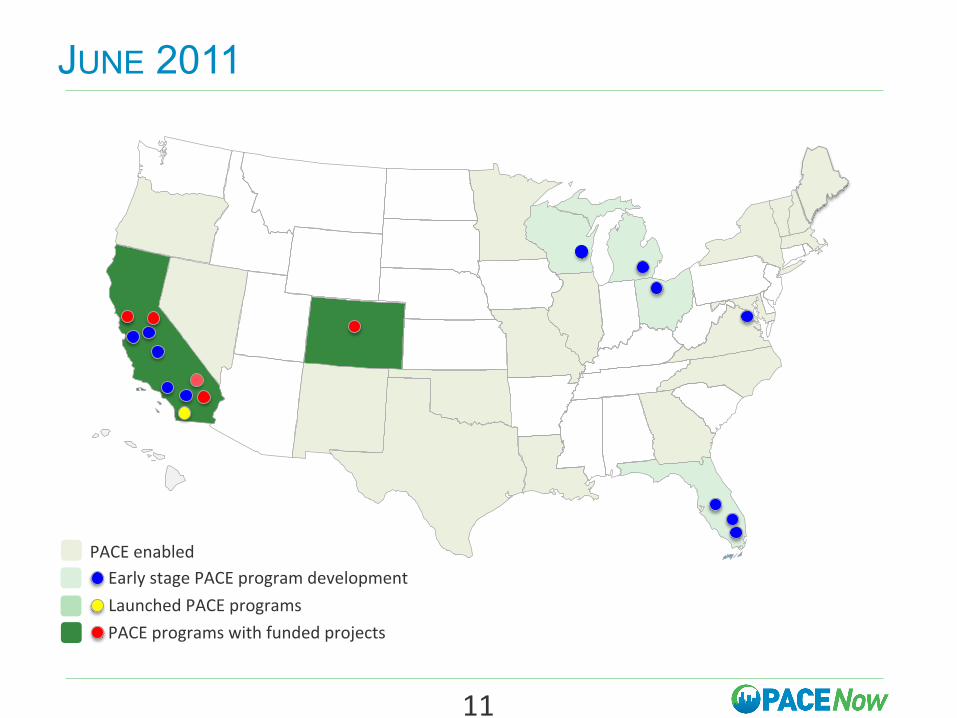

JUNE 2011

11

Early stage PACE program development Launched PACE programs

PACE enabled

11

PACE programs with funded projects

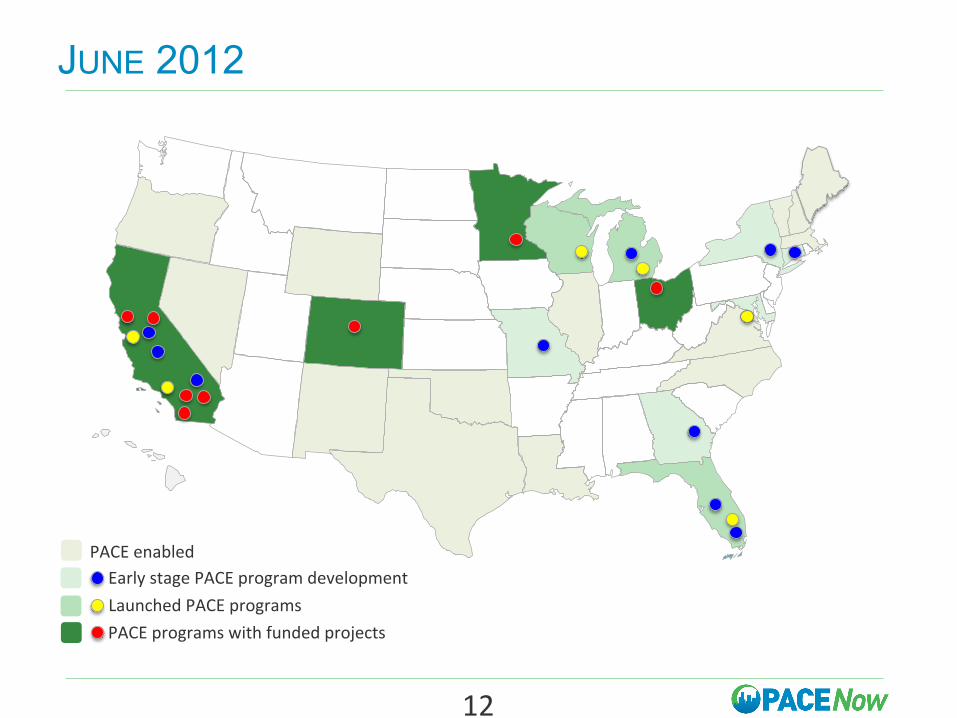

JUNE 2012

12

Early stage PACE program development Launched PACE programs

PACE enabled

12

PACE programs with funded projects

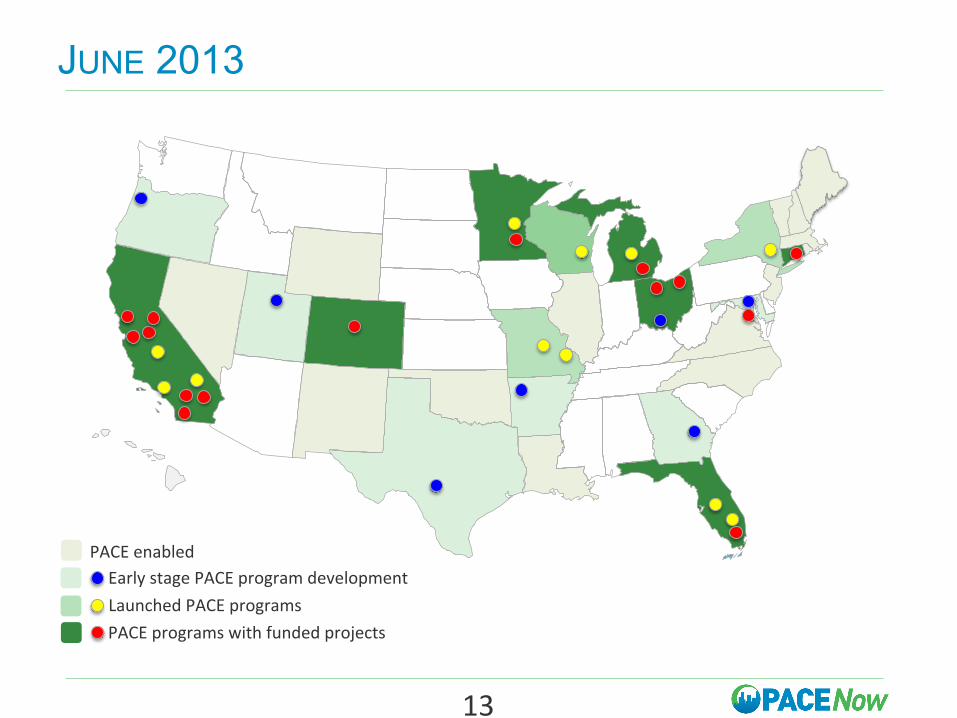

JUNE 2013

13

Early stage PACE program development Launched PACE programs

PACE enabled

13

New legislaBve effort

PACE programs with funded projects

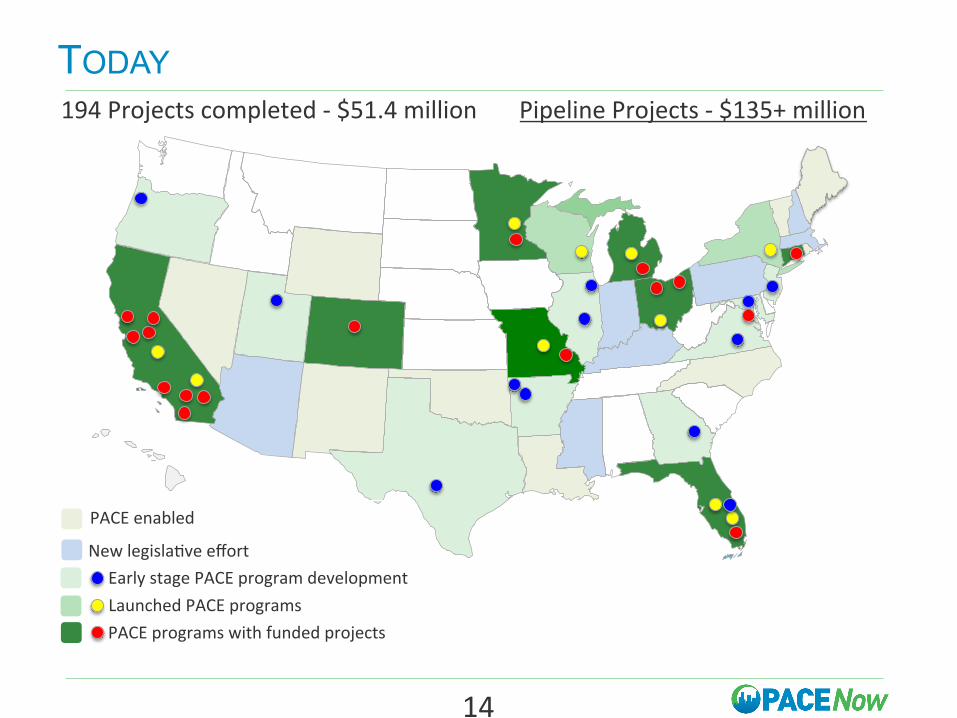

TODAY 194 Projects completed -‐ $51.4 million Pipeline Projects -‐ $135+ million

Early stage PACE program development Launched PACE programs

PACE enabled

14

15

Commercial PACE Key Program Elements

§ Most programs follow “open market” model. One program administrator, but multiple capital providers. Capital providers compete to provide lowest cost capital and best terms to property owners.

§ Most programs require consent of primary mortgage lender before PACE lien is placed on property. This reduces regulatory risk and respects relationship between property owner and mortgage lender.

§ Underwriting guidelines include: no bankruptcy for 3 years; no property tax delinquencies for 3 years; no notices of default or foreclosure for 5 years.

§ Most programs financed through transaction fees (closing costs)

CaliforniaFIRST Commercial PACE

17 Counties, 127 Cities Launched: Sept 2012

" Sponsor: CSCDA. Member counties and cities vote to opt into the program.

" Pipeline: $44 million. 76 active

applications. " “Open Market” approach allows

commercial property owners to choose best capital provider and financing terms. Mortgage lender consent required.

" 2 Projects financed Dec 2013 " Program administered by Renewable

Funding.

17

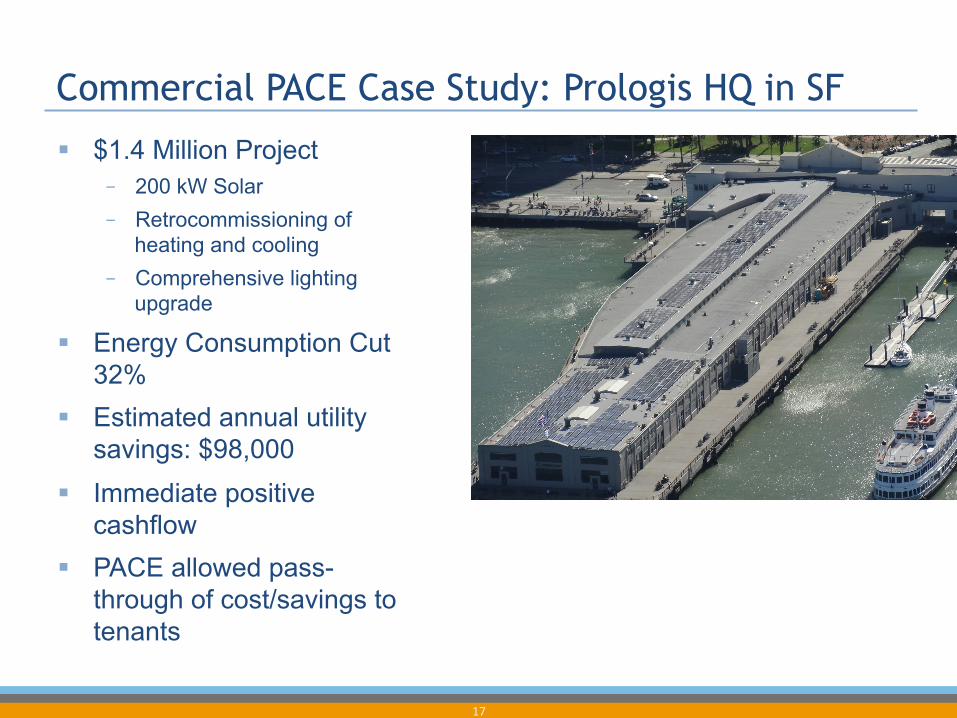

Commercial PACE Case Study: Prologis HQ in SF

§ $1.4 Million Project – 200 kW Solar – Retrocommissioning of

heating and cooling – Comprehensive lighting

upgrade

§ Energy Consumption Cut 32%

§ Estimated annual utility savings: $98,000

§ Immediate positive cashflow

§ PACE allowed pass-through of cost/savings to tenants

18

The Hammer Falls on Residential

§ FHFA guidance letter July 6, 2010 – Asserts PACE creates “safety and soundness

concerns.” Authorize punishment of PACE properties and communities.

– Asserts PACE violates mortgage contract and can be considered an act of default.

– Threatens to require larger down payments for all mortgages issued in PACE communities.

– Threatens to tighten underwriting requirements to make it harder for buyers to qualify for new mortgages in communities that offer PACE financing.

– Fannie and Freddie respond: issue statement that they will not purchase mortgages for properties with PACE liens.

19

Attempts to Restore Residential PACE 2011-12

§ Bi-Partisan Legislation introduced in Congress July 2011

§ Lawsuits filed in California, Florida, New York 2010-13 – 9th Circuit judge ruled that FHFA had violated the Administrative Procedures Act

and required a public rulemaking process on PACE.

– On appeal, the 9th Circuit Court of Appeals overturned the judge’s ruling and said that FHFA had acted as a “conservator” and not as a “regulator”

20

Residential PACE Regains Momentum in California

§ Jan. 2012: HERO Program Launched in Riverside County, CA – 7,000 residential projects for a total of approximately $130 million funded.

0 known defaults. On resale, lien has been paid off in some cases.

§ Sonoma County, CA residential program remains in business since 2010

– 1,885 residential projects for a total of approximately $30 million funded. 0 known defaults.

§ In 2013, 50 additional local governments in CA have voted to offer residential PACE financing

§ March 2014: California establishes $10 million residential PACE reserve to protect Fannie, Freddie in the event of home foreclosure on home with PACE lien.

21

2013-14: Gov. Brown Establishes $10M PACE Reserve

§ Governor and legislature set aside $10 million for PACE reserve in 2013-14 budget

§ California PACE reserve program to specifically address FHFA’s concerns

§ In the event of foreclosure, Fannie and Freddie will be able to recover outstanding PACE assessments

§ February 18, 2014: CAEATFA board (a unit of the California Treasury) unanimously voted to approve PACE reserve regulations

§ The reserve became operational in mid-March

§ CSCDA voted March 6, 2014 to re-launch residential PACE

22

CaliforniaFIRST Residential Program Launches Northern California Launch August 4 Alameda County Marin County Monterey County Napa County Sacramento County San Mateo County Santa Clara County Santa Cruz County Solano County Yolo County Southern California Launch September 2 San Benito County San Luis Obispo County Tulare County Kern County Fresno County Ventura County San Diego County

23

Hawaii GEMS Program Green Energy Market Securi1za1on & On-‐Bill Repayment

Hawaii State Department of Business, Economic Development & Tourism hTp://energy.hawaii.gov

24 24

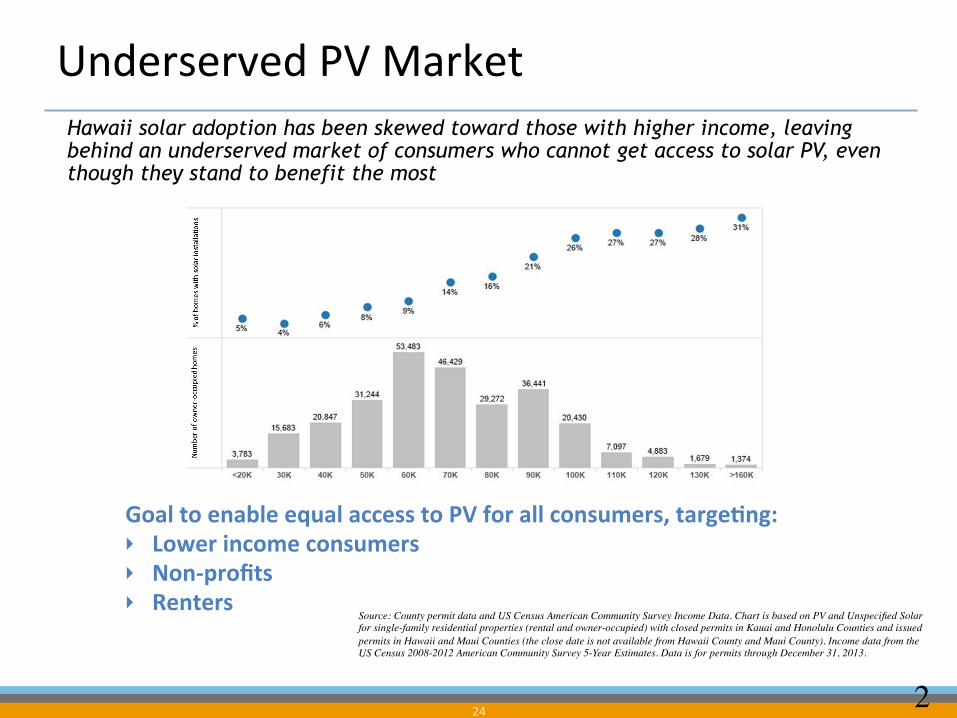

Underserved PV Market Hawaii solar adoption has been skewed toward those with higher income, leaving behind an underserved market of consumers who cannot get access to solar PV, even though they stand to benefit the most

Goal to enable equal access to PV for all consumers, targe1ng: } Lower income consumers } Non-‐profits } Renters

Source: County permit data and US Census American Community Survey Income Data. Chart is based on PV and Unspecified Solar for single-family residential properties (rental and owner-occupied) with closed permits in Kauai and Honolulu Counties and issued permits in Hawaii and Maui Counties (the close date is not available from Hawaii County and Maui County). Income data from the US Census 2008-2012 American Community Survey 5-Year Estimates. Data is for permits through December 31, 2013.

25

• Pursuant to Act 211 • Address financing barriers to help State meet clean energy goals (HCEI) • Balance policy goals with the risk of repayment to achieve an

appropriate return on a portfolio basis • Address underserved markets while expanding the market more

generally • Partner with private sector entities to deliver products to meet the

goals of the program

25

GEMS Program ObjecBves Established through enabling legislation. Objectives based on Act 211, Session Laws of Hawaii 2013, which established the legal framework for GEMS:

26

• Connecticut Clean Energy Finance and Investment Authority • Supports range of products in the market • Leveraged and unleveraged capital

• New York Green Bank • Target key barriers to achieving clean energy goals with “market-based”

approach

• Pennsylvania and Kentucky Financing Programs • WHEEL program for unsecured loans

• Key Lesson • State must be dynamic and flexible to address rapidly changing market

26

ExisBng Models Shift away from grant and rebate programs toward self-sustaining financing models

27 27

GEMS: On-‐Bill and Direct Bill Preference is to have the majority of portfolio on-bill to prove out the power of the utility bill as a repayment mechanism

• Aggregate Hawaiian Electric payment history is significantly better than traditional credit performance

• GEMS aims to demonstrate the power of using the

utility bill as a repayment mechanism in order to expand traditional underwriting criteria

• GEMS will utilize direct bill when necessary

Colin Bishopp | [email protected] | (202) 550-7570