ck power public company limited

TRANSCRIPT

0

CK POWER PUBLIC COMPANY LIMITED

Corporate Presentation

August 2014

1

Bangkok

Expressway

Public Company Limited (BECL)

TTW Public

Company Limited (TTW)

Ch. Karnchang

Public Company Limited (CK)

Public

CKP

Hydro Cogeneration Solar

SouthEast Asia

Energy Company Limited (SEAN)

Bangpa-in Cogeneration

Company Limited (BIC)

Nam Ngum 2

Company

Limited (NN2)

Bangkhenchai

Company Limited

Nakorn Ratchasima

Solar Company

Limited (NRS

Chiangrai Solar

Company Limited

(CRS)

56%

75%

65%

100%

30%

30%

Shareholder Strengths Developer Capability (Engineering, EPC)

Financial Strength

Corporate Governance

Check & Balance

Holding Strengths Funding Capability

Investment Channels

Diversified Portfolio

Subsidiaries Strengths

Long - Term Revenue Capability

Professional O&M Capability

Technical Expertise

31.78%

23.22% 25.00%

20.00%

15.15% 19.04%

Business Overview : Comprehensive Capability & Synergy Power

1

2

Nam Ngum2 (NN2)

Bangpa-In

Cogeneration 1 (BIC 1)

Bangpa-In

Cogeneration 2 (BIC 2)

Bangkhenchai

Solar (BKC)

Nakorn

Ratchasima Solar (NRS)

Chiangrai Solar (CRS)

Technology Hydro Power Cogeneration Power

Cogeneration Power

Solar Power Solar Power

Solar Power

Location Lao PDR Ayudthaya, Thailand

Ayudthaya, Thailand

Nakorn

Ratchasima, Thailand

Nakorn

Ratchasima, Thailand

Chiangrai, Thailand

Commercial

Operation started

IOD: March 2011

COD: January

2013

June 2013 June 2017 (Scheduled COD)

August 2012 March 2012 January 2013

Power

Purchase Agreement

25 Years with

EGAT 1/

25 Years with EGAT1/

25 Years with EGAT1/

5+automatic

every 5 years

with PEA2/

5+automatic

every 5 years with PEA2/

5+automatic

every 5 years with PEA2/

Generation Capacity

615 MW 117.5 MW

Steam 19.6 Ton/hr.

120 MW Steam 20 Ton/hr.

8 MW 6 MW 8 MW

CKP’s Shares 75% by SEAN3/ 65% 65% 100% 30% 30%

Other Shareholders

25% EDL GEN GPSC (PTT

Group) 25%,

Other 10%

GPSC (PTT

Group) 25%,

Other 10%

- Sonnedix Group 70%

Sonnedix Group 70%

Business Overview : Well Diversified Portfolio

2

Remark : 1/ EGAT = Electricity Generating Authority of Thailand 2/ PEA = Provincial Electricity Authority

3/ CKP owns 56% in SEAN, other shareholders are Ratchburi Electricity Generating Holding Plc. (RATCH) 33% and others 11%

3

NN2

Nam Bak

Xayaburi

BIC 1 & 2

BKC NRS CRS

Business Overview :

Leading AEC Player, First Thai Holding with Overseas Core Asset

Hydro Power

Cogeneration

Solar Power

3

4

CK Group has demonstrated a very

active timeline over the past several

years

Construction Period

Construction Period

Construction Period

PPA Finalization

PPA Finalization

COD

COD

PPA Finalization

Construction Period

Construction Period

CK Power embodies the expertise of the CK Group with its strong track record of

power project development, acquisition, construction and operation

2006

Solar

Co-

Generation

Hydro

2007 2008 2010 2011 2013 2012 2009

1. NN2

2. XPCL

3. NB

4. BKC

5. NRS

6. CRS

7. BIC 1

CA

Mar

MOU

(Feasibility Study)

May

MOU

(Feasibility Study)

Apr

MOU

(Detailed Feasibility Study)

Nov

Construction

Completion

Dec Mar

Partnership with PTT

International, EGCO and

BECL

Mar

PPA Submission to

Lao PDR

Mar

Construction Start

Mar

Jan

PPA Signed

(8 MW)

Jul Aug

PPA Signed

(6 MW)

Dec

PPA Signed

(8 MW)

Dec

Mar

Jan

PPA Application

Submission

Aug Nov

PPA Application

Submission

Sep Sep

Jun

Acquisition

by CKP

Jun

Acquisition

by CKP

Jun

Acquisition

by CKP

Dec

Nov

8. BIC 2

COD IOD

COD

COD

Construction Period

PPA

signed

PPA

signed

PPA

signed

CK Acquisition

of BKC

May

CK Acquisition

of NRS

Mar

CK Acquisition

of CRS

Jun

BIC Acquisition

by CKP

Dec

COD and PPA Signed

MOU

CA, Construction, Acquisition and

PPA submission

Construction Period

Financial cost reduction

Project Development

Agreement (PDA)

Apr

2014

Tariff MOU

July

9. New SPPs MOU

(Partnership with an

industrial estate)

Dec

MOU

(Partnership with an

industrial estate)

July

Interest Rate

Reduction

Interest Rate

Reduction

Interest Rate

Reduction

Nov

Nov

April

Business Overview : Development & Operational Excellence

4

5

Sales increased by 62% yoy

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

500

1,000

1,500

2,000

2,500

NN2 BKC BIC Cash Profit Margin

3,269 MB

2,021 MB

Cash Profit is EBITDA adjusted by profit sharing and gain/loss on exchange rate

MB

5

Cash Profit

Margin

Main contributor for sales growth is BIC 1

Change in fuel mix led to new benchmark for cash profit

margin

Cost components

49%

33%

3%

12%

3%

Fuel costs

Depreciationexpenses

Royalty fee

Operation andMaintenance

Other costs

1H/2014 1H/2013 Change

Cost of Sales 1.977 816 1,161

IA Amortization 260 247 14

SG&A 223 235 (12)

Financial 621 649 (28)

Unit: Million Baht

Financial Performance:

1H2014 Profit before fx grew by 330 % YoY

6

Leverage Opportunity

25,730

11,328

21,832

485

2,183

31

-

10,000

20,000

30,000

40,000

50,000

60,000

Conso Separate

Current Liabilities

Non-CurrentLiabilities

Equity

0.93 times 0.05 times DE Ratio

MB

CKP 490

SEAN 18,230

BIC 4,028

BKC 597

Total 23,345

Outstanding Loan (MB), As of June 30, 3014

Avg cost of debt: 5.03%

6

Financial Performance:

Healthy Capital Structure with low gearing

7

2014

Operating : 755 MW

2017

Target : 875 MW

2019

Target : 2,320 MW

2020 Onward

Target : 4,280 MW

Additional :

• 120 MW from BIC 2

• Upsides from Domestic

Renewables (Target 100 MW)

Additional :

• 160 MW from Nam Bak

• 1,285 MW from Xayaburi

Additional :

• 1,000 MW from

Cross – Border

• 960 MW from

8 Cogeneration

Projects

CKP Outlooks : Growth Roadmap

Solid Project Pipeline and Strong

Growth Plan with 27% CAGR growth in

Total MW Capacity during 2014 - 2020

7

8

Project Location Capacity SCOD Progress Remarks

Hydro Power Nam Bak (NB)

Xayaburi (XPCL)

New Cross-Border

Project

Lao PDR

Lao PDR

Cross-

Border

160 MW

1,285 MW

Target

1,000 MW

Y.2018

Y.2019

Y.2020

onward

Obtained Project

Development

Agreement

Construction work as

of June 2014 more

than 40 %

Preliminary Studies

Preparing Power

Purchase Agreement

and Concession

Agreement

On schedule

High potentials

CKP strong position

Cogeneration

Bangpa-in

Cogeneration

Project 2 (BIC 2)

New 8 Cogeneration Power Plants

Thailand

Thailand

120 MW

120 x8 MW

Total 960 MW

Y.2017

Y.2020 onward

EPC Contract within

Q4/2014

Identified locations

and 2 MOUs signed

with Industrial Estates

Cost saving from

common facilities

and long-term

shared O&M

Awaiting the

solicitation announcement

Renewable Solar and Wind Power

Thailand Target

100 MW

Y.2014 onward

Identified locations

and preparing

proposals

Monitor for M&A opportunities

Tariff is under

reviewing

New Thailand Power

Development Plan to

emphasize on renewables

CKP Outlooks : Developing Projects

8

9

Thailand’s Installed Capacity will grow more

than 40% in the next decade

Power Development Plan (PDP) indicates

the new additional capacity for each year

Electricity Authority of Thailand (EGAT) is

the major off-taker from Private Power

Companies

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Installed Capacity Demand

43,157

30,231

60,477

44,521

MW

Forecasted Thailand Electricity Demand during 2015 – 2025 (PDP 2010 Rev.3)

Political Situation has no negative impact on Power Industry

No change in Power Industry Structure and existing

Power Purchase Agreement (PPA)

Resolutions on pending issues such as Renewable

Power Tariff are expected

New PDP is being prepared with the tendency of

increasing Renewable Energy portion

CKP Outlooks : Domestic Outlooks

Source: Thailand PDP 2010 Revision 3

9

10

EGAT :

10,308 MW Private :

21,651MW

IPP1/ : 7,540 MW

Cogeneration:

4,320 MW

Renewable :

4,939 MW

Cross-Border

Purchasing :

4,852 MW

Monitor the next IPP Bidding

BIC 2 received PPA , COD on 2017

Prepare for new 8 projects total 960 MW

Target 100 MW Renewable, Solar and Wind

Prepare for new Tariff Structure

XPCL received PPA , COD on 2019

Target 1,000MW for Cross-Border and

selling to neighboring countries

CKP ‘s Plan for each segment during 2015-2025

According to the current PDP, the 21,651 MW will be allocated to Private Power Companies during 2015 – 2025

CKP’s BIC 2 and Xayaburi already secure Power Purchase Agreement

Preparing for each segment expansion during 2015 - 2025

CKP Outlooks : Thailand Power Development Plan

1/ IPP = Independent Power Producer with over 100 MW contracted capacity

Additional Capacity during 2015-2025

Source: Thailand PDP 2010 Revision 3

10

11

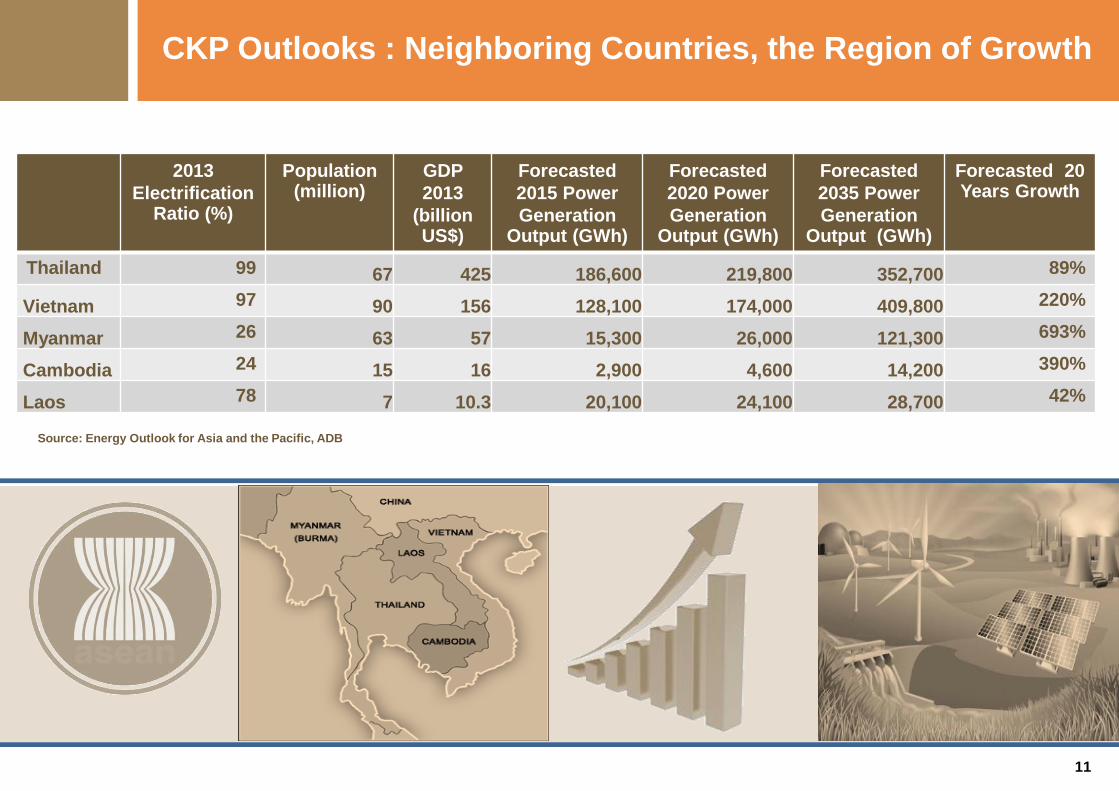

2013

Electrification Ratio (%)

Population (million)

GDP

2013

(billion US$)

Forecasted

2015 Power

Generation Output (GWh)

Forecasted

2020 Power

Generation Output (GWh)

Forecasted

2035 Power

Generation Output (GWh)

Forecasted 20 Years Growth

Thailand 99 67 425 186,600 219,800 352,700 89%

Vietnam 97 90 156 128,100 174,000 409,800 220%

Myanmar 26 63 57 15,300 26,000 121,300 693%

Cambodia 24 15 16 2,900 4,600 14,200 390%

Laos 78 7 10.3 20,100 24,100 28,700 42%

Source: Energy Outlook for Asia and the Pacific, ADB

CKP Outlooks : Neighboring Countries, the Region of Growth

11

12

Over 13,000 MW Hydro Power Potentials and CKP’s proven track record in project development

Potentials in transmitting to Thailand

River basin

Hydropower

Project

Capacity (MW)

In

Operation Construction Planned

1. Nam Tha Nam Tha 1 168

2. Nam Ou Nam Ou 2,5,7 540

Nam Ou 1,3,4,7 616

3. Nam Ngum Nam Ngum 1 155

Nam Ngum 2 615 Nam Ngum 3,4 511 Nam Ngum 5 120 Nam Lik 100

Nam Mung 3 40

Nam Leuk 60

4. Nam Ngiep Nam Ngiep 1 278

Nam Ngiep 2 180

5. Nam Theun Nam Theun 1 523

Nam Theun 2 1,075 Theun Hinboun 440 Nam Hai 800

6. Xedon Xexet 1,2 121

7. Xekong Xekong 3 105 Xekong 4,5 550

Xepian-

Xenamnoy 319

Houay Ho 155 Xekaman 1,3 540 Xekaman 2,4 850

8. Mekong Xayaburi 1,285 Others (8) 8,769

Total 2,986 2,545 13,384

CKP Outlooks : Lao PDR

Source: www.poweringprogress.org, Mekong River Commission, EDL 12

13

5

4

3

2

1

6

7

8

9

10

In Operation Planned

River Basin No. Hydropower Project Capacity (MW)

In Operation Construction Planned

Salween

1 Upper Thanlwin 2,400

2 Nawngpha 1,000

3

Ta Sang or 7,110

Mong Tong

(7,000)

4 Ywathit 4,000

5 Wei Gyi Dam

(Mae Sarieng 1) *4,800

6 Daywin

(Mae Sarieng 2) *600

7 Hay Gyi 1,360

21,270

Myitnge 8 Yeywa 790

Shweli

9

Shweli 1 600

Shweli 2 460

Shweli 3 360

Dapein

10

Dapein I 168

Dapein II 240

Over 40,000 MW Hydro Power Potential identified by ADB

20,000 MW Hydro Power Potentials in Salween River Alone

Strength in Natural Gas Supply

Potentials in transmitting to Thailand

CKP Outlooks : Myanmar

Source* : EGAT International Company Limited

www.salweenwatch.org

http://www.burmariversnetwork.org 13

14

Project Earliest COD

1) P.Malaysia - Singapore (New) 2018

2) Thailand - P.Malaysia

• Sadao - Bukit Keteri Existing

• Khlong Ngae - Gurun Existing

• Su Ngai Kolok - Rantau Panjang 2015

• Khlong Ngae – Gurun (2nd Phase, 300MW) 2016

3) Batam - Singapore 2015-2017

4) Thailand - Lao PDR

• Roi Et 2 - Nam Theun 2 Existing

• Sakon Nakhon 2 – Thakhek – Then Hinboun (Exp.) Existing

• Udon Thani 3- Nabong – Nam Ngum 2 Existing

• Mae Moh 3 - Nan - Hong Sa 2015

• Ubon Ratchathani 3 – Pakse – Xe Pian Xe Namnoy 2018

• Khon Kaen 4 – Loei 2 – Xayaburi 2019

• Thailand – Lao PDR (New) 2015-2023

5) Lao PDR - Vietnam 2011-2016

6) Thailand - Myanmar 2016-2025

7) Vietnam - Cambodia (New) 2017

8) Lao PDR - Cambodia 2016

9) Thailand - Cambodia (New) 2015-2020

The Status of the Asian Power Grid Project

(Indochina Peninsula)

14 Source : EGAT

15

CK Power is the flagship power development company of CK Group:

Diversified portfolio

AEC Player

Stable stream of income

Experienced management with development and operational excellence

Solid project pipeline

High growth company

Key Takeaways

CKP has unique competitive

advantage :

• Comprehensive capability

from development to EPC

to Operation

• Synergy Power

15

16

Appendix

16

17

Nam Ngum 2 Hydro Power Plant

17

Year

PE Tariff SE Tariff EE Tariff

USD /

kwh

THB /

kwh

THB /

kwh

THB /

kwh

IOD period 0.02475 0.963 1.253 1.060

COD Date + 6

years after COD 0.02475 0.965 1.255 1.062

Thereafter 0.02668 1.041 1.353 1.145

NN2 Tariff Structure:

• Annual Target -

Primary Energy (PE) 2,218 million kwh / yr

Secondary Energy (SE) 92 million kwh / yr

• NN2 may sell Excess Energy (EE) at EE rate

during “Excess Energy Month”, which is when

reservoir water level is over 374.5m ASL.

• NN2 may also sell energy as PE/ SE account

after NN2 reaches its annual target and use PE/

SE account as credit in subsequent shortage

years. This mechanism enhances NN2 revenue

stability.

Tariff Structure:

IOD period = Mar 26, 2011 to Deb 31, 2012

COD Date = Jan 1, 2013

Off Taker: Electricity Generating Authority of Thailand (EGAT), 25 years

Stable revenue stream with Annual Target , Take -or -Pay basis, and the

Energy Account for the over-target electricity

No fuel cost and low O&M cost lead to higher margin, average 60% of

gross profit and 80% of EBITDA margin

Low operation risk

17

18

June 2014 Operation – Nam Ngum 2

2013

Month

Declaration (MWh) Reservoir Level

Energy Account (MWh)

PE* SE** EE*** (m.asl) PE SE

JAN 193,000 371.2

FEB 184,766 370.6

MAR 189,513 368.8

APR 189,153 362.5

MAY 187,121 355.0

JUN 193,690 354.0

JUL 169,752 363.7

AUG 220,000 15,399 374.4

SEP 238,000 49,807 150,672 373.7

OCT 220,000 30,000 371.5 3,206

NOV 200,000 371.5

DEC 128,920 372.3 95,916

Account Drawdown

- - -

Total 2,313,916 95,206

* Primary Energy with Annual Target at 2,218,000 MWh ** Secondary Energy with Annual Target at 92,000 MWh *** Excess Energy Please find the details of Nam Ngum 2 Tariff Structure in the Appendix

2014

Month

Declaration (MWh) Reservoir Level

Energy Account (MWh)

PE* SE** EE*** (m.asl) PE SE

JAN 185,923 370.6

FEB 174,122 368.2

MAR 188,326 358.9

APR 188,343 350.6

MAY 159,797 343.9

JUN 105,562 343.9

JUL

AUG

SEP

OCT

NOV

DEC

Account Drawdown

Total

18

19

MWh (m.asl) Electricity Production (MWh) and Reservoir Level (m.asl)

NN2’s Operation decreased month-on-month from seasonal factor and decrease year-on-year due to

less water inflow in 2014

However, NN2 water level as of July 30, 2014 picked up to the planned level

As of June 2014, the PE and SE account was 196,211 and 8,770 MWh respectively

Stable revenue stream with Annual Target , Take -or -Pay basis, and the Energy Account for the over-

target electricity

325

330

335

340

345

350

355

360

365

370

375

380

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

2014 Electricity 2013 Electricity 2014 Resorvoir Level 2013 Resorvoir Level 2012 Resorvoir Level2

June 2014 Operation – Nam Ngum 2

19

20

EGAT Tariff Average Portion

Capacity Payment Availability payment of contracted capacity with monthly FX adjustment.

15%

Energy Payment For the fuel cost with monthly Gas Price adjustment 75%

Fuel Saving Payment

For the efficiency of electricity and steam generation. 10%

Industrial Users Tariff

Refer to the Standard Industrial Tariff with some discount

Monthly adjustment due to the changes in the Standard Industrial Tariff

Steam Tariff

Refer to natural gas price with monthly adjustment

Off-takers Contracted Period Started date

EGAT 90.0 MW 25 yrs. June 2013

APCB Electronics (Thailand) Co.,Ltd. 10.0 MW 15 yrs. June 2013

Nippon Super Precision Co.,Ltd. 4.2 MW 15 yrs. June 2013

MMC Tools (Thailand) Co.,Ltd. 3.0 MW 15 yrs. December 2013

Takei Plastic (Thailand) Co.,Ltd. 1.5 MW 15 yrs. December 2013

Quality Construction Products Plc. (Steam) 19.6 ton/hr. 15 yrs. October 2013

BIC 1 Tariff Structure

Off Taker: EGAT and Industrial Users (IUs)

Stable revenue stream with minimum Take-or-Pay Basis

Energy Payment and IUs’ adjustable tariff mitigate fuel cost fluctuation

Steam Revenue is upside

Bang Pa-in Cogeneration Project 1

20 20

21

June 2014 Operation– Bang Pa-in Cogeneration 1

0

2,250

4,500

6,750

9,000

0

17,500

35,000

52,500

70,000

NOV'13 DEC'13 JAN'14 FEB'14 MAR'14 APR'14 MAY'14 JUN'14

EGAT Industrial Users - Electricity Industrial User - Steam

MWh Ton Electricity Production (MWh) and Steam Production (Ton)

BIC1’s Operation increased month-on-month, no unplanned maintenance schedule during June

Stable revenue stream with minimum Take-or-Pay Basis

21

22

Electricity Customers PPA (MW) JAN’14 FEB’14 MAR’14 APR’14 MAY’14 JUN’14

Electricity Produced (MWh) EGAT 90.0 53,918 49,978 57,154 50,858 51,967 54,784 APCB Electronic Thailand Co., Ltd. 12.0 5,052 4,799 5,468 4,605 4,645 4,974 Nippon Super Precision Co.,Ltd. 4.2 1,743 1,724 1,946 1,556 1,447 1,498 MMC Tools (Thailand) Co.,Ltd. (started Dec 1, 2013) 3.0 1,026 1,206 1,494 1,505 1,597 1,554 Takei Plastic (Thailand) Co.,Ltd. (started Dec 8, 2013) 1.5 435 461 565 521 579 566

Heat Rate (BTU/KWh) 7,751 7,758 7,665 7,849 7,781 7,768 Steam Customer – Quality Construction Products Plc. (Q-CON)

Contracted Capacity (Ton/Hr.)

JAN’13 FEB’14 MAR’14 APR’14 MAY’14 JUN’14

Steam Produced (Ton) 19.6 9,159 8,649 8,693 6,089 7,649 7,560

June 2014 Operation– Bang Pa-in Cogeneration 1

22

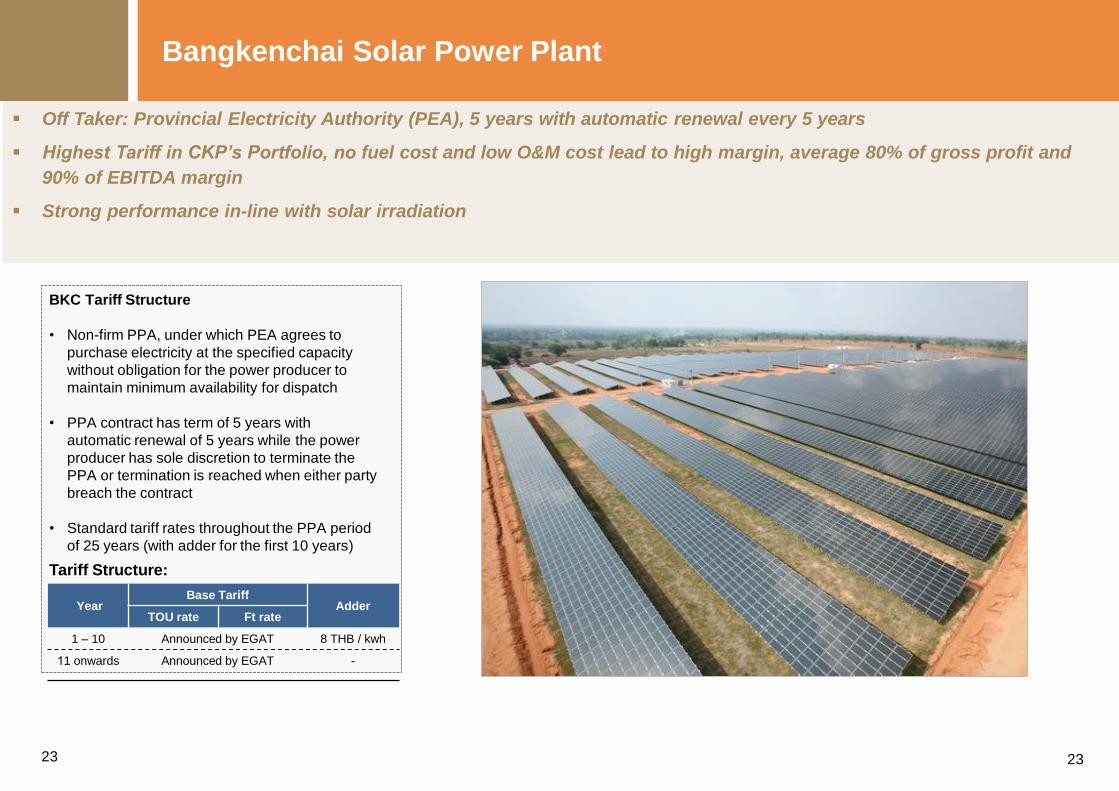

23

BKC Tariff Structure

• Non-firm PPA, under which PEA agrees to

purchase electricity at the specified capacity

without obligation for the power producer to

maintain minimum availability for dispatch

• PPA contract has term of 5 years with

automatic renewal of 5 years while the power

producer has sole discretion to terminate the

PPA or termination is reached when either party

breach the contract

• Standard tariff rates throughout the PPA period

of 25 years (with adder for the first 10 years)

Tariff Structure:

Year Base Tariff

Adder TOU rate Ft rate

1 – 10 Announced by EGAT 8 THB / kwh

11 onwards Announced by EGAT -

Off Taker: Provincial Electricity Authority (PEA), 5 years with automatic renewal every 5 years

Highest Tariff in CKP’s Portfolio, no fuel cost and low O&M cost lead to high margin, average 80% of gross profit and

90% of EBITDA margin

Strong performance in-line with solar irradiation

Bangkenchai Solar Power Plant

23 23

24

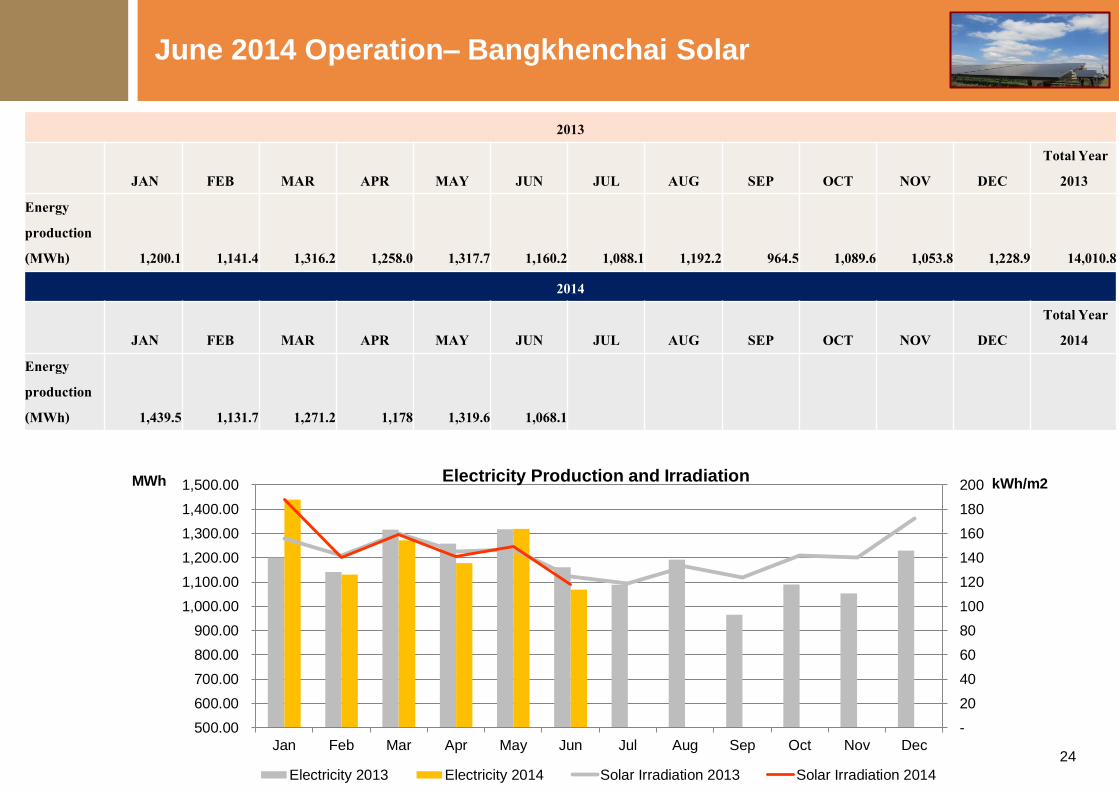

June 2014 Operation– Bangkhenchai Solar

-

20

40

60

80

100

120

140

160

180

200

500.00

600.00

700.00

800.00

900.00

1,000.00

1,100.00

1,200.00

1,300.00

1,400.00

1,500.00

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Electricity Production and Irradiation

Electricity 2013 Electricity 2014 Solar Irradiation 2013 Solar Irradiation 2014

2013

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Total Year

2013 Energy production (MWh) 1,200.1

1,141.4

1,316.2

1,258.0 1,317.7 1,160.2 1,088.1 1,192.2 964.5 1,089.6 1,053.8 1,228.9 14,010.8

2014

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC Total Year

2014 Energy production (MWh) 1,439.5 1,131.7 1,271.2 1,178 1,319.6 1,068.1

MWh kWh/m2

24