city skyline, new york, usa for professional clients only japanese lessons: global macro and market...

TRANSCRIPT

For professional clients only

Japanese lessons: global macro and market outlook

Date: October 2012Prepared by: Philip Poole

INTERNAL (amend as appropriate)

Tripping up in Tokyo – will others fall?

Insert job number here

3

-3

-2

-1

0

1

2

3

4

5

6

7

82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

(%)

Inflation (y oy ) Policy rates

Japan’s malaise – route map for the wider developed world?

Source: Bloomberg, as at August 2012

Japan’s economic miracle came to a shuddering halt at the end of the ‘80s

An indebtedness overhang, banking crisis and policy mistakes all played a part compounded by ageing

Since then growth has been absent Deflation has been a persistent threat

despite loose monetary policy Government debt has spiraled to 230%

of GDP Equity valuations collapsed and

nominal bond yields stayed very low There are key lessons in this

experience for the rest of DM Europe risks a similar ‘lost decade’

and China needs to heed the warnings

Insert job number here

4

Poor demographics will weigh on DM growth

Source: UN, as at September 2012

0

5

10

15

20

25

30

35

40

45

Japan-1980

Japan-2010

Japan-2020

China-1980

China-2010

China-2020

UK-1980

UK -2010

UK -2020

US -1980

US-2010

US-2020

Percentage aged 0-14 (% of total)

Percentage aged 65 or over (% of total)

Insert job number here

5

Ageing will also keep pressure on government finances

Ageing tends to curb growth depressing activity–sensitive government revenues

As populations age less people pay in and more people try to take out of the system (pensions, health care)

This combination will keep up pressure to reform public sector finances

Source: World Bank development indicators, as at July 2012

8

10

12

14

16

18

20

22

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Pub

lic s

ocia

l exp

endi

ture

% G

DP

Insert job number here

6

Lessons from Japan

Growth is likely to be in short supply in the developed world Developed world inflation likely to remain low with a deflationary overhang Compensating for low growth by stimulating investment can backfire badly Flooding the world with liquidity does not guarantee recovery Monetary policy should not be tightened prematurely but largely loses its

potency to stimulate where there is a balance sheet overhang Fix ‘zombie’ banks as quickly as possible or recovery will be further delayed Ageing necessitates pro-active reform of public sector finances or it will add to

fiscal problems Japan also needs to heed Europe’s mistakes - or else investors could lose

confidence and bond yields move sharply higher

Insert job number here

7

Fast forward – the current massive monetary stimulus has not revived DM growth…

Source: Federal reserve website, BOJ, BOE, ECB, as at July 2012

High unemployment and spare capacity reduce inflation risks

And with DM fiscal policy tightening, monetary policy will need to take the strain

This combination is likely to keep DM monetary policy very loose

Labour market developments will be key in determining action by central banks

Weak employment data persuaded the Fed to turn the liquidity tap back on with QE3 and an open ended commitment

Rates could be cut further in Europe But the reality is that DM monetary policy

has lost much of its potency The transmission mechanism through to

the real economy is broken

0

1

2

3

4

5

6

7

8

9

05/0

6

09/0

6

01/0

7

05/0

7

09/0

7

01/0

8

05/0

8

09/0

8

01/0

9

05/0

9

09/0

9

01/1

0

05/1

0

09/1

0

01/1

1

05/1

1

09/1

1

01/1

2

05/1

2

Siz

e o

f ce

ntr

al b

anks

' bal

ance

sh

eet

(U

SD

tiil

lion

at

curr

ent

exch

ang

e ra

te)

BOE

BOJ

ECB

FED

Insert job number here

8

…or significantly dented high unemployment

Source: Bloomberg, date as at September 2012

3

4

5

6

7

8

9

10

11

Mar-04

Sep-04

Mar-05

Sep-05

Mar-06

Sep-06

Mar-07

Sep-07

Mar-08

Sep-08

Mar-09

Sep-09

Mar-10

Sep-10

Mar-11

Sep-11

Mar-12

US Japan Eurozone UK Asia

Insert job number here

9

The eurozone crisis is not over

Solving the eurozone’s problems will require a multi-year work out, whether or not it holds together

There are two key requirements: to clean up the existing mess and to convince markets that it won’t happen again

The debt swap for Greece was an important step forward As are efforts to recapitalise Spanish banks – the first time enough cash has been put

on the table to do the job Yields have to be brought down to sustainable levels for Italy and Spain if the crisis is

to abate The ECB’s new OMT programme should help to cap yields in the short-term... …but can only buy time not fix the problem A solution will necessitate implementation of credible fiscal adjustment plans To be successful it will also require macro stabilisation and concrete moves towards

fiscal union

Insert job number here

10

Eurozone macro deterioration is the additional concern

Growth is declining in most EZ countries and the unemployment trajectory is worrying

Source: Bloomberg, HSBC Global Asset Management, as at September 2012

2

4

6

8

10

12

14

16

18

20

22

24

01/00

01/01

01/02

01/03

01/04

01/05

01/06

01/07

01/08

01/09

01/10

01/11

01/12

Spain Greece France Italy

(%)

-8

-6

-4

-2

0

2

4

6

8

03/00

03/01

03/02

03/03

03/04

03/05

03/06

03/07

03/08

03/09

03/10

03/11

03/12

% y

oy

Germany France Italy Spain

GDP growth Unemployment rate

Insert job number here

11

What will drive EM growth if DM demand is structurally weak?

Insert job number here

12

Headline inflation has fallen in key emerging markets

Falling inflation supports looser EM policy but watch out for food prices

Source: Bloomberg, Data as of September 2012

0

10

20

30

40

50

60

Brazil

Mexico

South A

fica

China

India

Indonesia

Thailand

Russia

Food Energy/fuel related items

Source: OECD, HSBC Global Asset management, date as at September 2012

But EM is vulnerable to food price shocks

%%

-4

-2

0

2

4

6

8

10

12

14

16

Sep-06

Jan-07

May-07

Sep-07

Jan-08

May-08

Sep-08

Jan-09

May-09

Sep-09

Jan-10

May-10

Sep-10

Jan-11

May-11

Sep-11

Jan-12

May-12

China Brazil Russia India (WPI)

INTERNAL (amend as appropriate)

Global recovery. All over bar the shouting?

Insert job number here

14

70

72

74

76

78

80

82

01/1

0

03/1

0

05/1

0

07/1

0

09/1

0

11/1

0

01/1

1

03/1

1

05/1

1

07/1

1

09/1

1

11/1

1

01/1

2

03/1

2

05/1

2

07/1

2

-20

-15

-10

-5

0

5

10

01

/10

03

/10

05

/10

07

/10

09

/10

11

/10

01

/11

03

/11

05

/11

07

/11

09

/11

11

/11

01

/12

03

/12

05

/12

07

/12

-40

-30

-20

-10

0

10

20

30

01/1

0

03/1

0

05/1

0

07/1

0

09/1

0

11/1

0

01/1

1

03/1

1

05/1

1

07/1

1

09/1

1

11/1

1

01/1

2

03/1

2

05/1

2

07/1

2

-45

-40

-35

-30

-25

-20

-15

-10

-5

0

5

01/1

0

03/1

0

05/1

0

07/1

0

09/1

0

11/1

0

01/1

1

03/1

1

05/1

1

07/1

1

09/1

1

11/1

1

01/1

2

03/1

2

05/1

2

07/1

2

Global data has mostly disappointed

Source: HSBC Global Research, as at September 2012

US activity surprise index Eurozone activity surprise index

Japan activity surprise index China activity surprise index

Insert job number here

15

Manufacturing PMIs confirm loss of global growth momentum

Source: Bloomberg, date as at September 2012

30

35

40

45

50

55

60

65

Sep-06

Jan-07

May-07

Sep-07

Jan-08

May-08

Sep-08

Jan-09

May-09

Sep-09

Jan-10

May-10

Sep-10

Jan-11

May-11

Sep-11

Jan-12

May-12

China Eurozone US

Insert job number here

16

…and point to more contraction

> 50 + rising > 50 + falling or < 50 + falling < 50 + rising or > 50 + unchanged < 50 + unchanged

Data unavailable at time of release

Source: Markit, data for PMI’s as at Sept 2012. US data refers to ISM manufacturing

17

China’s economic activity has slowed...

Source: CEIC, HSBC Global Asset Management

25

30

35

40

45

50

55

60

65

Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12

0

5

10

15

20

25% yoy

Official PMI, lhsHSBC Manufacturing PMI, lhsIndustrial production, rhs

Manufacturing PMI vs. industrial production

42.1

20.9

-22.9

81.6

27.9

-2.4

-75

-50

-25

0

25

50

75

100

Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12

% yoy

-30

-20

-10

0

10

20

30

40% yoy

Total profit growth (Jan-May), lhsNo of loss-making enterprises, rhs

Industrial enterprises (financial data)

International trade

-40

-20

0

20

40

60

80

Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12

%; USDbn

Trade balance (USD bn; 3mma)Exports (yoy; 3mma)Imports (yoy; 3mma)

Real estate investment vs. construction

-40

-20

0

20

40

60

80

100

120

Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12

% YoY; 3mma

Real estate FAI

Floor space started (commodity building)

- External demand remains challenging and there appear to still be destocking pressure in the industrial sector - Economic slowdown has hurt enterprise profitability. Property construction/investment has also weakened

18

…but pro-growth policies support a soft-landing

Note: * MNI Business Sentiment Survey; ** PBOC 5000 Entrepreneur Survey diffusion index. Source: CEIC, HSBC Global Asset Management

China CPI & PPI inflation

-9-6-30369

1215182124

Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12

% yoy

Headline CPI Core CPIFood CPI PPI

- The PBOC cut interest rates twice within a month, on top of RRR cuts and window guidance to support loan growth . Lower inflation leaves more flexibility for further policy loosening. Growth will likely pick up modestly in 2H on further policy support and as effects of earlier easing continue to feed through

Inflation

-2

0

2

4

6

8

10

12

14

16

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

Jan-1

2F

eb-1

2M

ar-

12

Apr-

12

May-1

2Jun-1

2

CNY trn Bank loans entrust & trust loans

Bank acceptance bills Corporate bonds & equity

Equity financing Total

Total social financing

10

15

20

25

30

35

Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12

% yoy

M2 Loan Deposit

Monetary indicators

0

10

20

30

40

50

60

70

80

Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12

Lending attitude of banks**

Availability of credit* (current)

Availability of credit* (future)

Business surveys on bank credit availability

Improvement of credit availability

Insert job number here

19

-8.0

-7.0

-6.0

-5.0

-4.0

-3.0

-2.0

-1.0

0.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Proj

ecte

d fe

dera

l bud

get d

efic

it as

a p

erce

ntag

e of

GD

PFiscal cliff If current policies are extended

Slipping over the edge? The US fiscal cliff

There is an on-going political polarisation between Democrats and Republicans

Fiscal paralysis looks inevitable in the run up to elections and potentially beyond

Under these circumstances the approaching ‘fiscal cliff’ starting in Q1 2012 represents a challenge

On balance we expect a political accommodation to be reached that reduces fiscal drag from 4-5% of GDP to 1-2%

A deal could settle on rolling tax cuts and other allowances in exchange for raising the debt ceiling

Source: CBO, as at July 2012

Any forecast, projection or target where provided is indicative only and is not guaranteed in any way.

Insert job number here

20

US Germany

Japan China

Source: Consensus Economics, as at September 2012

2012 Real GDP growth forecasts (%) 2012 CPI forecasts (%)

Growth forecasts cut but still a little optimistic

INTERNAL (amend as appropriate)

Investment themes

Insert job number here

22

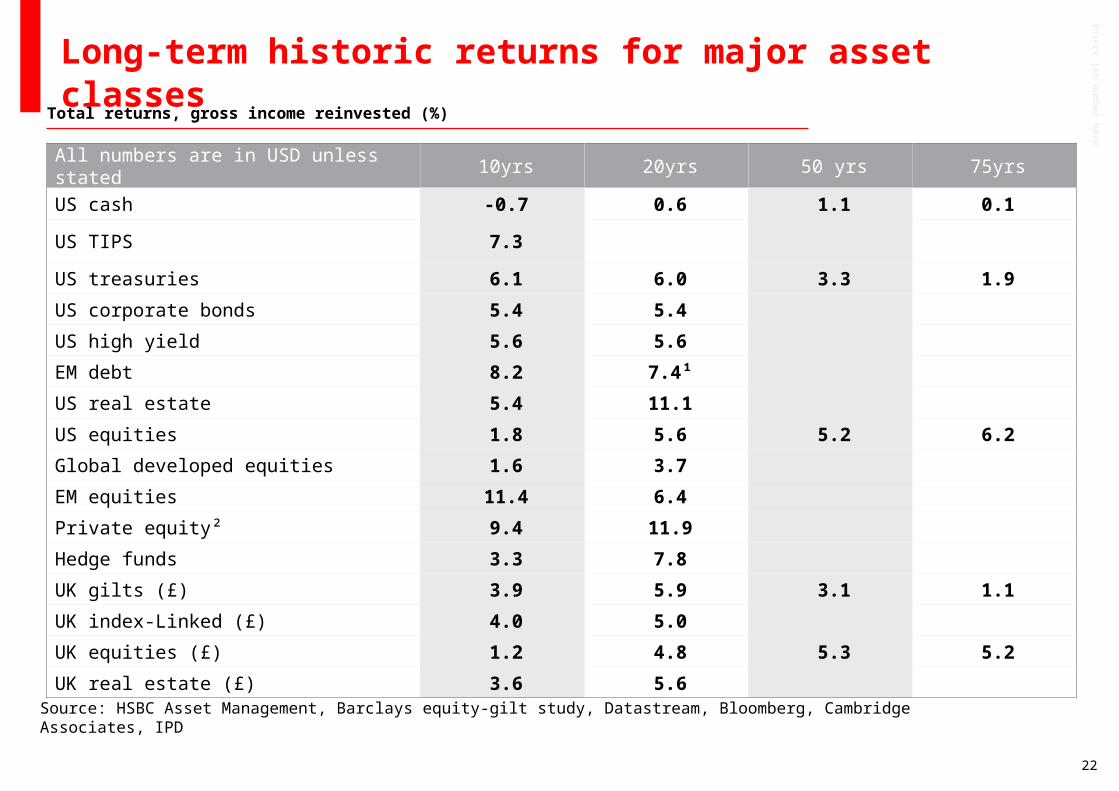

Long-term historic returns for major asset classes

Total returns, gross income reinvested (%)

All numbers are in USD unless stated 10yrs 20yrs 50 yrs 75yrs

US cash -0.7 0.6 1.1 0.1

US TIPS 7.3

US treasuries 6.1 6.0 3.3 1.9

US corporate bonds 5.4 5.4

US high yield 5.6 5.6

EM debt 8.2 7.4¹

US real estate 5.4 11.1

US equities 1.8 5.6 5.2 6.2

Global developed equities 1.6 3.7

EM equities 11.4 6.4

Private equity² 9.4 11.9

Hedge funds 3.3 7.8

UK gilts (£) 3.9 5.9 3.1 1.1

UK index-Linked (£) 4.0 5.0

UK equities (£) 1.2 4.8 5.3 5.2

UK real estate (£) 3.6 5.6

Source: HSBC Asset Management, Barclays equity-gilt study, Datastream, Bloomberg, Cambridge Associates, IPD

Insert job number here

23

Estimated prospective real returns for major asset classes

Source: HSBC, Cambridge Associates, Datastream

Real returns: pecking order of assets (% real return)

(0.5)

0.00.5

1.5

3.03.5 3.7 4.0

4.5

6.0

9.5

(2)

0

2

4

6

8

10

Cash GlobalILBs

Govtbonds

IG Credit EM debt(USD)

RealEstate

HY Credit EM debt(local)

GlobalEquity

EM Equity PE

Core beta-based return

Heterogeneous asset

Insert job number here

24

Look familiar? Japanese and US bond yields and inflation

-4

-2

0

2

4

6

8

10

12

14

16

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

US CPI 10 year US bond yields

-3

-2

-1

0

1

2

3

4

5

6

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Japan CPI 10 year Japanese bond yields

Source: Bloomberg, as at September 2012

Insert job number here

25

Negative US data surprises have helped drag down yields

Source: Bloomberg, HSBC Global Asset management, data as at August 2012

-50

-40

-30

-20

-10

0

10

20

30

40

Ma

r-01

Se

p-0

1

Ma

r-02

Se

p-0

2

Ma

r-03

Se

p-0

3

Ma

r-04

Se

p-0

4

Ma

r-05

Se

p-0

5

Ma

r-06

Se

p-0

6

Ma

r-07

Se

p-0

7

Ma

r-08

Se

p-0

8

Ma

r-09

Se

p-0

9

Ma

r-10

Se

p-1

0

Ma

r-11

Se

p-1

1

Ma

r-12

0

1

2

3

4

5

6

US Supr index (lhs) US 10 year yields (rhs)US surprise index (lhs) US 10 year yield (rhs)

Insert job number here

26

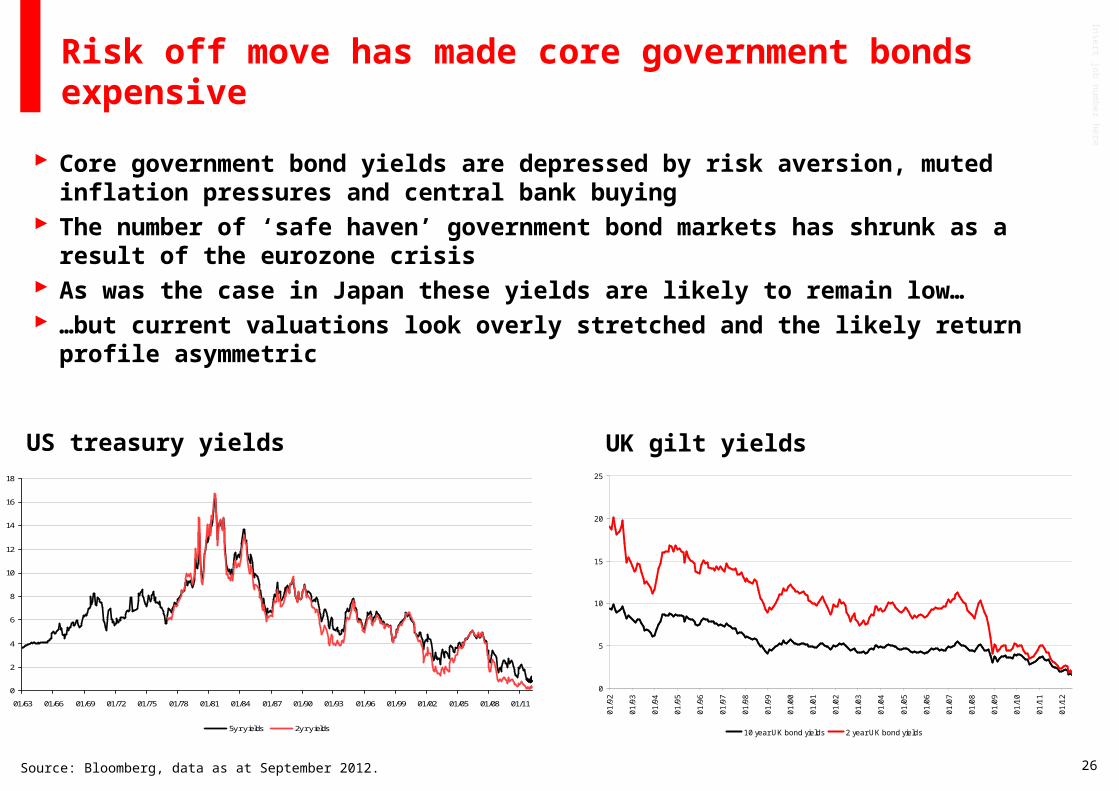

Risk off move has made core government bonds expensive

Core government bond yields are depressed by risk aversion, muted inflation pressures and central bank buying

The number of ‘safe haven’ government bond markets has shrunk as a result of the eurozone crisis

As was the case in Japan these yields are likely to remain low… …but current valuations look overly stretched and the likely return profile asymmetric

Source: Bloomberg, data as at September 2012.

0

2

4

6

8

10

12

14

16

18

01/63 01/66 01/69 01/72 01/75 01/78 01/81 01/84 01/87 01/90 01/93 01/96 01/99 01/02 01/05 01/08 01/11

5y r y ields 2y r y ields

0

5

10

15

20

25

01

/92

01

/93

01

/94

01

/95

01

/96

01

/97

01

/98

01

/99

01

/00

01

/01

01

/02

01

/03

01

/04

01

/05

01

/06

01

/07

01

/08

01

/09

01

/10

01

/11

01

/12

10 year UK bond yields 2 year UK bond yields

US treasury yields UK gilt yields

Insert job number here

27

Strong inflows into high yield and GEM bond space

Year-to-date flows into fixed income funds

Source: HSBC Global Research, EPFR, Data as at August 2012

High yield funds have attracted large inflows YTD exceeding USD37.5bn, equivalent to 18.3% of AuM

GEM bonds have also seen strong inflows of USD 17.5bn YTD (12.9% of AuM)

Within GEM, Latam has seen the strongest inflows YTD, equivalent to 13.1% of AuM

Asia has seen YTD inflows equivalent to 7.9% of AuM

Insert job number here

28

High yield corporate spread pick-up remains attractive

Wider corporate credit spreads reflects flight to quality and are not credit-specific

Although low growth will likely hit earnings, corporate fundamentals are generally supportive of credit markets

In particular, corporate balance sheets are mostly in good shape

This should help to shield corporates from the impact of bank de-leveraging

But investors need to look closely at individual credit fundamentals

Source: HSBC Global Asset Management and Bloomberg, data as at August 2012

0

2

4

6

8

10

12

14

16

18

08/0

0

02/0

1

08/0

1

02/0

2

08/0

2

02/0

3

08/0

3

02/0

4

08/0

4

02/0

5

08/0

5

02/0

6

08/0

6

02/0

7

08/0

7

02/0

8

08/0

8

02/0

9

08/0

9

02/1

0

08/1

0

02/1

1

08/1

1

02/1

2

0

2

4

6

8

10

12

BarCap HY Index ( lhs) Raio of Barcap HY over 5yr UST (%, rhs)

Insert job number here

29

Despite inflows, the relative spread over the underlying treasury yield remains wide

EM debt attractive given credit quality and low risk free rate

Source: JP Morgan and Bloomberg, data as at September 2012.

0

200

400

600

800

1000

1200

01/0

0

01/0

1

01/0

2

01/0

3

01/0

4

01/0

5

01/0

6

01/0

7

01/0

8

01/0

9

01/1

0

01/1

1

01/1

2

0

100

200

300

400

500

600

700

JP Morgan EMBI Global index spread (lhs)

Ratio of JPM EMBI spread over 5yr UST (5, rhs)

Insert job number here

30

0

2

4

6

8

10

12

14

16

09/8

2

09/8

4

09/8

6

09/8

8

09/9

0

09/9

2

09/9

4

09/9

6

09/9

8

09/0

0

09/0

2

09/0

4

09/0

6

09/0

8

09/1

0

S&P 500 earning yield 10 year bond yields

Equity yields attractive relative to government bond yields

US UK

Source: Bloomberg, September 2012

0

1

2

3

4

5

6

7

07/0

2

01/0

3

07/0

3

01/0

4

07/0

4

01/0

5

07/0

5

01/0

6

07/0

6

01/0

7

07/0

7

01/0

8

07/0

8

01/0

9

07/0

9

01/1

0

07/1

0

01/1

1

07/1

1

01/1

2

FTSE div yield 10 yields 10 year bond yields

Insert job number here

31

Equity markets - what’s cheap relative to history?

Source: OECD, HSBC Global Asset management, date as at September 2012

DM forward PE relative to own valuation history (5 yr average)

EM forward PE relative to own valuation history (5 yr average)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Russia

Chin

a

India

Asia

ex J

apan

Bra

zil

GE

Ms

Kore

a

Mala

ysia

Indonesia

Turk

ey

South

Afric

a

Thaila

nd

Mexic

o

0.00

0.20

0.40

0.60

0.80

1.00

1.20

Italy

Spain

Fra

nce

Germ

any

Unite

d K

ingdom

Europe x

UK

Japan

U.S

.A

Insert job number here

32

EM and DM sector valuations

Source: OECD, HSBC Global Asset management, date as at September 2012

Price to book relative to DM 5 yr average

Price to book relative to EM 5 yr average

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Health C

are

Consum

er Staples

Consum

erD

iscretionary

Financials

Telecom

munication

Services

Utilities

Energy

Industrials

Materials

Information

Technology

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Information

Technology

Consum

erD

iscretionary

Utilities

Consum

er Staples

Telecom

munication

Services

Industrials

Financials

Health C

are

Materials

Energy

Insert job number here

33

0

10

20

30

40

50

60

01/10

03/10

05/10

07/10

09/10

11/10

01/11

03/11

05/11

07/11

09/11

11/11

01/12

03/12

05/12

07/12

2012 2013

100

110

120

130

140

150

160

170

01/10

03/10

05/10

07/10

09/10

11/10

01/11

03/11

05/11

07/11

09/11

11/11

01/12

03/12

05/12

07/12

2012 2013

DM earnings expectations. Bad news now in the price?

Source: OECD, HSBC Global Asset management, date as at September 2012

80

85

90

95

100

105

110

115

03/10

05/10

07/10

09/10

11/10

01/11

03/11

05/11

07/11

09/11

11/11

01/12

03/12

05/12

07/12

2012 2013

154

159

164

169

174

179

184

189

194

199

204

03/10

05/10

07/10

09/10

11/10

01/11

03/11

05/11

07/11

09/11

11/11

01/12

03/12

05/12

07/12

2012 2013

US UK

Europe Japan

Inde

xed

earn

ings

Inde

xed

earn

ings

Inde

xed

earn

ings

Inde

xed

earn

ings

Insert job number here

34

80

100

120

140

160

180

200

220

01/1

0

03/1

0

05/1

0

07/1

0

09/1

0

11/1

0

01/1

1

03/1

1

05/1

1

07/1

1

09/1

1

11/1

1

01/1

2

03/1

2

05/1

2

07/1

2

2012 2013

EM earnings expectations. Bad news now in the price?

Source: OECD, HSBC Global Asset management, date as at September 2012

China India

Brazil Russia

4

4.5

5

5.5

6

6.5

7

01/1

0

03/1

0

05/1

0

07/1

0

09/1

0

11/1

0

01/1

1

03/1

1

05/1

1

07/1

1

09/1

1

11/1

1

01/1

2

03/1

2

05/1

2

07/1

2

2012 2013

40

45

50

55

60

65

01/10

03/10

05/10

07/10

09/10

11/10

01/11

03/11

05/11

07/11

09/11

11/11

01/12

03/12

05/12

07/12

2012 2013

15000000000

17000000000

19000000000

21000000000

23000000000

25000000000

27000000000

29000000000

31000000000

01/10

03/10

05/10

07/10

09/10

11/10

01/11

03/11

05/11

07/11

09/11

11/11

01/12

03/12

05/12

07/12

2012 2013

Inde

xed

earn

ings

Inde

xed

earn

ings

Inde

xed

earn

ings

In

dexe

d ea

rnin

gs

Insert job number here

35

Many EM currencies look undervalued relative to DM

Source: IMF World Economic Database, data as at September 2012 – PPP estimates for 2011. Any forecast, projection or target where provided is indicative only and is not guaranteed in any way.

% under / over valued versus USD on PPP PPP versus USD Spot

% under/over valued

CHF 1.66 0.92 80%JPY 106.8 78.4 36%AUD 1.58 1.31 21%EUR 0.83 0.77 8%BRL 1.81 2.01 -10%CLP 401.1 470.5 -15%RUB 22.8 30.7 -26%IDR 6603 9463 -30%TRL 1.22 1.79 -32%MXN 8.63 12.75 -32%HUF 143.9 215.5 -33%CNY 4.17 6.32 -34%PLN 1.97 3.12 -37%MYR 1.91 3.05 -37%PHP 25 41.6 -40%THB 17.5 30.8 -43%TWD 15.7 29.4 -47%INR 19.1 53.9 -65%

-80% -60% -40% -20% 0% 20% 40% 60% 80% 100%

INR

TWD

THB

PHP

MYR

PLN

CNY

HUF

MXN

TRL

IDR

RUB

CLP

BRL

EUR

AUD

JPY

CHF

Insert job number here

36

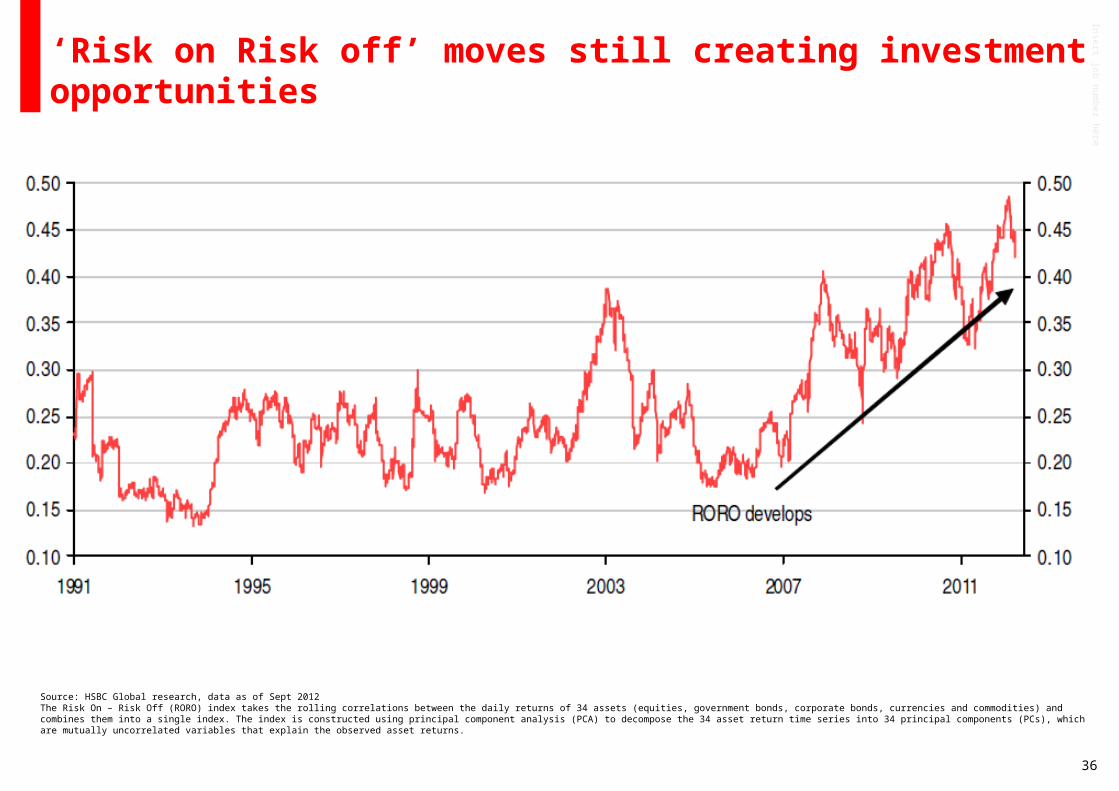

‘Risk on Risk off’ moves still creating investment opportunities

Source: HSBC Global research, data as of Sept 2012The Risk On – Risk Off (RORO) index takes the rolling correlations between the daily returns of 34 assets (equities, government bonds, corporate bonds, currencies and commodities) and combines them into a single index. The index is constructed using principal component analysis (PCA) to decompose the 34 asset return time series into 34 principal components (PCs), which are mutually uncorrelated variables that explain the observed asset returns.

Insert job number here

37

Macro drivers and long run investment themes

Bonds look expensive relative to

equities

Favour EM equity themes

Lock in HY corporate and EMD liquidity/risk

premia

Diversify currency exposure

Dividend yields look attractive relative to core govt bond yields

Upside to bonds capped by very low yields, downside more significant

Seek out attractively priced global stocks with exposure to emerging markets consumption and infrastructure spending themes

HY corporate and EMD credit fundamentals are generally strong

But spreads are still relatively wide

This remains an opportunity

Exposure to EM currencies to capture carry and appreciation

Undervalued EM currencies (CNY, INR KRW, MYR, SGD, MXP) vs. DM currencies

The burden of debt and ageing populations will likely keep DM growth below pre-crisis levels Inflation is unlikely to be a problem in DM over the immediate future Monetary policy to remain very loose (conventional and unconventional) but largely impotent Europe confronts a Japanese-style ‘lost decade’ and the US faces growth and fiscal challenges EM to grow less rapidly than in the past given headwinds but will continue to outperform DM

Insert job number here

38

Appendix 1: consensus global growth and inflation forecasts

Source: Consensus Economics, data as at August 2012.

Consensus revised lower than prior month Consensus revised higher than prior month

2009 2010 2011 2012 F 2013F 2009 2010 2011 2012 F 2013FNorth America -2.6 3.0 1.8 2.2 2.1 -0.2 1.6 3.1 2 2United States -3.5 3.0 1.8 2.2 2.1 -0.3 1.6 3.2 2.0 2.0Canada -2.8 3.2 2.3 2.0 2.1 0.3 1.8 2.9 1.9 2.0Western Europe -4.1 1.9 1.5 -0.2 0.5 0.6 1.8 2.7 2.1 1.8Euro zone -4.2 1.7 1.6 -0.5 0.3 0.3 1.6 2.7 2.3 1.7France -2.6 1.4 1.6 0.1 0.5 0.1 1.5 2.1 2.0 1.7Germany -5.1 3.7 3.0 0.9 1.2 0.4 1.1 2.3 1.9 1.8Italy -5.2 1.2 0.4 -2.1 -0.5 0.8 1.5 2.7 3.0 2.0Spain -3.7 -0.1 0.7 -1.7 -1.4 -0.3 1.8 3.1 2.0 1.9UK -4.9 1.4 0.9 -0.2 1.4 2.2 3.3 4.4 2.6 1.9Switzerland -1.9 2.7 1.7 1.2 1.3 -0.5 0.7 0.2 -0.6 0.6Sweden -5.3 5.4 4.4 0.9 1.9 -0.3 1.3 2.9 1.2 1.4Norway -1.6 2.1 2.6 3.2 2.8 2.2 2.4 1.3 0.9 1.6Eastern Europe -5.2 4.5 4.6 2.7 3.3 6.3 6.6 6.3 6.3 5.3Hungary -6.7 1.2 1.5 -0.9 0.9 4.2 4.9 3.9 5.5 3.9Poland 1.6 3.8 4.1 2.8 2.8 3.5 2.6 4.3 3.8 2.7Czech Republic -4.1 2.2 1.8 -0.7 1.1 1.0 1.4 1.9 3.3 2.4Russia -7.8 4.0 4.2 3.8 3.7 8.8 8.8 6.1 6.3 5.7Turkey -4.8 9.0 8.1 2.7 4.3 6.3 8.6 6.5 9.2 6.8South Africa -1.7 2.8 3.1 2.5 3.3 7.1 4.3 5.0 5.8 5.5Israel 0.8 4.8 4.5 2.8 3.5 3.3 2.7 3.5 2.5 2.4Asia Pacific 1.9 7.0 4.4 5.0 5.0 0.8 2.6 3.6 2.6 2.8Japan -6.3 4.0 -0.6 2.5 1.4 -1.3 -0.7 -0.2 0.1 0.0Australia 1.4 2.7 1.9 3.4 3.1 1.8 2.8 3.5 1.8 3.0New Zealand -2.0 1.7 1.9 2.4 2.8 2.1 2.3 4.2 1.6 2.4China 9.2 10.4 9.2 7.9 8.3 -0.7 3.3 5.4 2.8 3.4South Korea 0.3 6.2 3.6 2.7 3.5 2.8 3.0 4.2 2.4 2.9Hong-Kong -2.7 7.0 5.0 2.1 4.0 0.6 2.3 5.3 4.4 3.8India 8.0 8.5 7.2 6.1 7.1 12.4 10.4 8.2 8.0 7.6Singapore -0.8 14.5 5.0 2.5 4.1 0.6 2.8 5.1 4.4 3.1Taiwan -1.9 10.9 4.4 2.0 4.0 -0.9 1.0 1.4 1.8 1.9Thailand -2.3 7.8 1.6 5.1 4.5 -0.9 3.3 3.9 3.1 3.2Latin America -1.7 6.3 4.1 3.0 3.8 5.7 6.6 6.8 5.8 6.3Brazil -0.6 7.5 2.9 1.9 4.0 4.3 5.9 6.5 4.9 5.4Chile -1.7 5.2 6.2 4.6 4.6 -1.4 3.0 3.8 2.4 3.0Colombia 1.5 4.3 5.2 4.3 4.6 2 3.2 3.6 3.2 3.2Mexico -6.1 5.4 3.9 3.8 3.5 3.6 4.4 3.5 3.8 3.7World -1.8 4.3 2.9 2.6 2.9 1.3 2.8 3.7 3.0 2.9

GDP Inflation

Insert job number here

39

Appendix 2: relative leverage

Source: OECD and HSBC Global Research, as at June 2012

2000 Current

Household debt (%

GDP)Govt debt (%GDP)

Household debt (% GDP)

Govt debt (%GDP)

US 74 55 99 98

UK 77 41 114 90

Japan 70 106 62 212

France 47 66 63 99

Spain 54 62 88 74

Italy 52 109 76 127

Eurozone avg 50 76 65 96

Brazil 16 67 18 66

Russia 1 57 10 11

China 7 10 24 17

India 11 73 13 76

Mexico 10 27 7 22

Turkey 67 77 47 48

South Africa 36 58 48 46

Poland 14 38 33 62

Insert job number here

40

Important information

This presentation is intended for Professional Clients only and should not be distributed to or relied upon by Retail Clients.The contents of this presentation are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, forany purpose.The material contained herein is for information only and does not constitute investment advice or a recommendation to any reader of this material to buy orsell investments.This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would becontrary to law or regulation. This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe toany investment.HSBC Global Asset Management (UK) Limited has based this presentation on information obtained from sources it believes to be reliable but which it hasnot independently verified. HSBC Global Asset Management (UK) Limited and HSBC Group accept no responsibility as to its accuracy or completeness.This presentation is intended for discussion only and shall not be capable of creating any contractual or other legal obligations on the part of HSBC GlobalAsset Management (UK) Limited or any other HSBC Group company. Care has been taken to ensure the accuracy of this presentation but HSBC Global

Asset Management (UK) Limited accepts no responsibility for any errors or omissions contained therein.This presentation and any issues or disputes arising out of or in connection with it (whether such disputes are contractual or non-contractual in nature, suchas claims in tort, for breach of statute or regulation or otherwise) shall be governed by and construed in accordance with English law.The views expressed above were held at the time of preparation and are subject to change without notice. Any forecast, projection or target whereprovided is indicative only and is not guaranteed in any way. HSBC Global Asset Management (UK) Limited accepts no liability for any failure to meet suchforecast, projection or target.The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Whereoverseas investments are held the rate of currency exchange may also cause the value of such investments to fluctuate. Investments in emerging marketsare by their nature higher risk and potentially more volatile than those inherent in established markets. Stockmarket investments should be viewed as amedium to long term investment and should be held for at least five years. The level of yield is not guaranteed and may rise or fall in the future.Any performance information shown refers to the past and should not be seen as an indication of future returns.HSBC Global Asset Management (UK) Limited provides information to Institutions, Professional Advisers and their clients on the investment products andservices of the HSBC Group.This presentation is approved for issue in the UK by HSBC Global Asset Management (UK) Limited, who are authorised and regulated by the FinancialServices Authority.www.assetmanagement.hsbc.com/ukCopyright © HSBC Global Asset Management (UK) Limited 2012 All rights reserved.

FP12-1237