cic economics and policy forum the 2012 budget and construction simon rawlinson | march 2012

TRANSCRIPT

CIC Economics and Policy Forum

The 2012 Budget and ConstructionSimon Rawlinson | March 2012

30 March 2011 |

= £100 million

Source: HM Treasury

= £50 million

Budget 2012 – Unit of Comparison

30 March 2011 |

Plan for Growth Agenda

• Supply-side constraint

• Market failure

• Increasing the competitiveness of the tax system

• Transport and Energy Infrastructure• Low carbon infrastructure• Industrial capacity• Commercial space• Research and development Infrastructure• Housing

• Cost of delivery of infrastructure• Funding• Training and career development• Ease of engagement• Planning and regulation

• Competitiveness and certainty of business taxation

• Simplicity of operation• Support for investment and operation

30 March 2011 |

Source: HM Treasury

30 March 2011 |

Macro-economic background – GDP Growth

Forecast June ‘10 June ‘10 Nov ‘10 Mar‘11 Mar‘11

2011 GDP growth 2.6 2.3 2.1 1.7 0.8

2.9

2013/14

2.82.92.51.7GDP

growth

2015/162014/152012/132011/12FY

2.0

2013/14

3.02.70.80.8GDP

growth

2015/162014/1520122011Year• 2011 forecast 2011 to 2015 = 13.5%

• 2012 forecast 2011 to 2015 = 9.6%

30 March 2011 |

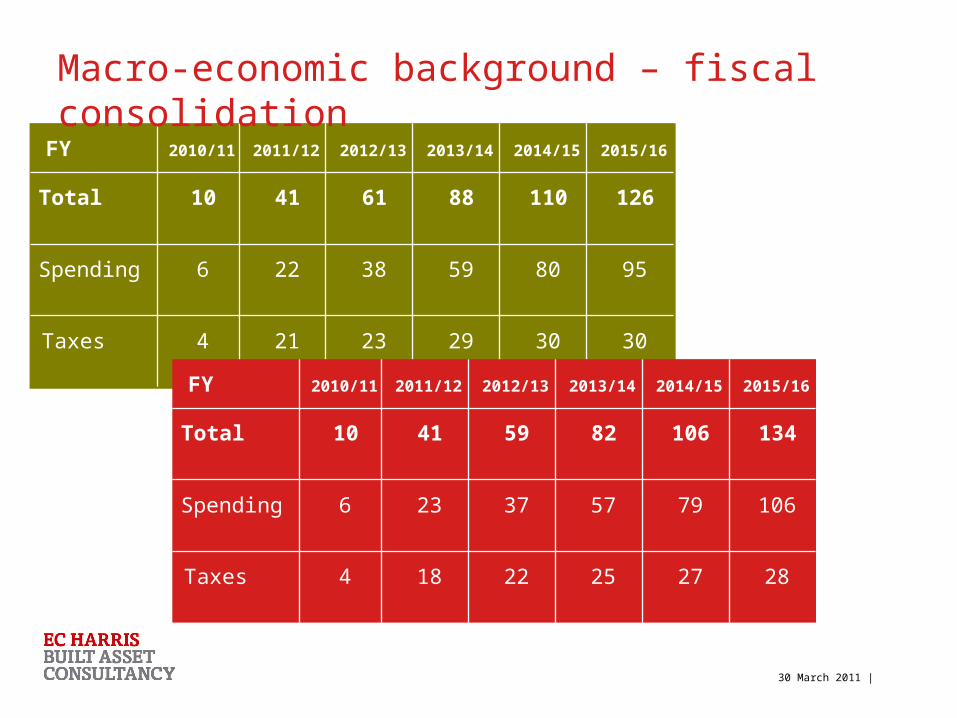

30

80

110

2014/15

12688614110Total

955938226Spending

23

2012/13

3029214Taxes

2015/162013/142011/122010/11FY

30

80

110

2014/15

12688614110Total

955938226Spending

23

2012/13

3029214Taxes

2015/162013/142011/122010/11FY

Macro-economic background – fiscal consolidation

30

80

110

2014/15

12688614110Total

955938226Spending

23

2012/13

3029214Taxes

2015/162013/142011/122010/11FY

27

79

106

2014/15

13482594110Total

1065737236Spending

22

2012/13

2825184Taxes

2015/162013/142011/122010/11FY

30 March 2011 |

Macro-economic background - rebalancing

• Higher Investment• Less net trade• Deeper cuts in Gov’t

consumption• More private consumption

30 March 2011 |

Macro-economic background – output gap

Source: NIESRSource: BoE

30 March 2011 |

National Infrastructure Plan

■ Infrastructure funding

– 60% to be privately funded – no constraint, but new models of finance needed

– 20% funded via a PPP model

– 2/3rds cost picked up by service users through charges

■ Enabling measures – attracting investment

– Planning Policy Framework

– Electricity Market Reform

– Major Infrastructure Planning Unit

– Green Investment Bank

– Business tax reform

£250bn of new projects

£26bn investment announced in November 2011

30 March 2011 |

Key Budget Measures – supply side efficiency■ Key measures – encouraging investment

– National Loan Guarantee Scheme

– R&D tax credits

– Enterprise zones – some with 100% capital allowances

– Employee ownership

– Simplified regulation

• Red Tape Challenge results - £3.3bn compliance cost reduction

• Contaminated land guidance - £140m per year

– Simplified taxation

■ Key measures – increasing capacity

– Planning Policy Framework

– Pension fund infrastructure model – including project funding

– Roads funding model – based on successful utilities models

– Super connected broadband – 10 second tier hubs

– Additional rail investment - £130m to expand Northern Hub

– Aviation review

30 March 2011 |

Key Budget Measures – small business investment

■ Cashflow-based taxation for small business below the VAT threshold

– Affects 3million enterprises

– Revenues up to £77,000

■ Small business employment incentive

■ Simplified business regulation

– Environmental regulation - £1bn pa

– Simplified HSE arrangements for SMEs

– Reduced producer responsibility for SMEs

30 March 2011 |

Key Budget Measures – capital investment announcements

■ £150m - Get Britain Building

■ £130m – Manchester Rail Hub

■ £270m – Growing Places Fund

■ £115m – Armed Forces Accommodation

■ £60m – Aerospace Innovation Centre

■ £100m – University Research Facilities

■ £50m – Second Wave Super-fast Broadband

■ £150m – Tax Incremental Funded projects

£20bn – National Loans Guarantee Scheme

• Assured low cost borrowing

£700m – Business Finance Partnership

• £1.2bn in total

• £100m via unconventional channels

£1.2bn – Local Authority earn-back model

£2bn – pension investment vehicle

X 20X 480

30 March 2011 |

Impact on Sectors

Housing and Regeneration. • New Buy – 100,000 homes• Stamp Duty Land Tax• Get Britain Building - £150m• Social Housing REITs• Accelerated release of Gov’t Land

Education and R&D

• £100m for R&D facilities• £60m Aerodynamics Centre• Normalisation of VAT for public and private universities

Local Government

• TIF arrangements for all LA’s - £150m funding• LA earn-back model - £1.2bn – six cities to follow• 5 new EZs with 100% capital allowances

Transport • Pension Infrastructure Platform• Ownership and financing for National Road Network • A14 proposals - Summer 2012 • £130m Northern Hub, £56m Bexhill to Hastings

Energy and Carbon Change

• “Unlocking” of 4GW of energy projects – radar interference• CFT exemption for gas-fired CHP• Gas generation strategy Autumn 2012• CRC reform

30 March 2011 |

Key Budget Measures – devil in the detail?

■ Impact of the replacement CRC tax

■ Cost of the Carbon Price Floor - £1.6bn pa from 2016

■ Growing Places funding – sourced from Departmental Savings

■ VAT equalisation for repairs to listed buildings

■ Capping of the total value of tax reliefs

■ VAT equalisation for providers of university education

30 March 2011 |

Overall impact on construction markets?

?

?

?

Source: CPA

2010 2011 2012 2013 2014 2015

Housing - Public 54.0 2.0 -20.0 -6.0 -2.0 3.0

Housing - Private 17.3 6.0 2.0 6.0 7.0 8.0

Public non-housing 31.4 -3.3 -23.5 -12.6 -9.2 0.0

Infrastructure 25.7 9.7 1.6 2.4 8.3 6.3

Industrial 19.6 -8.1 2.3 5.4 4.5 3.0

Commercial -1.8 0.0 -5.2 0.4 5.8 4.8

Total new work 12.1 0.8 -7.5 -1.3 3.8 4.4

30 March 2011 |

Joining it all up

■ Headline measures will have a limited impact on the industry

■ Capital investment driven by the private sector – some progress here

■ Progress on many key supply side initiatives

■ Impact of regulatory reform will be felt from now on

■ The 2011 budget is fiscally neutral but supportive of business

■ Limited positives for construction – as part of a wider solution

CIC Economics and Policy Forum

The 2012 Budget and ConstructionSimon Rawlinson | March 2012