cia test preparation part iii - bfiia.org

TRANSCRIPT

©2012 Deloitte Touche Tohmatsu Jaiyos

Study Unit Six: Managerial Accounting

March 2012

CIA Test PreparationPart III

©2012 Deloitte Touche Tohmatsu Jaiyos

Agenda:

• Cost Management Terminology• Cost Behavior and Relevant Range• Absorption (Full) vs. Variable (Direct) Costing• Capital Budgeting• Budget Systems• Operating Budget Components• Transfer Pricing• Cost-Volume-Profit (CVP) Analysis• Relevant Costs• Cost Accumulation Systems• Process Costing• Activity-Based Costing• Responsibility Accounting

©2012 Deloitte Touche Tohmatsu Jaiyos

6.1 Cost Management Terminology

Basic Definition

a)A cost is the measure of a resource used up for some purpose

b)A cost object is any entity to which costs can be attached.

c)A cost driver is the basis used to assign costs to a cost object

©2012 Deloitte Touche Tohmatsu Jaiyos

6.1 Cost Management Terminology

©2012 Deloitte Touche Tohmatsu Jaiyos

6.1 Cost Management Terminology

Product Cost

1. Inventory costs2. Capitalized as part of finished goods inventory3. A component of cost of goods sold4. All manufacturing costs (DM, DL, VOH, FOH)

Period Cost

1.Expensed as incurred2.Not capitalized in finished costs3.Exclude from cost of goods sold4.All selling and administrative (S&A)

©2012 Deloitte Touche Tohmatsu Jaiyos

6.1 Cost Management Terminology

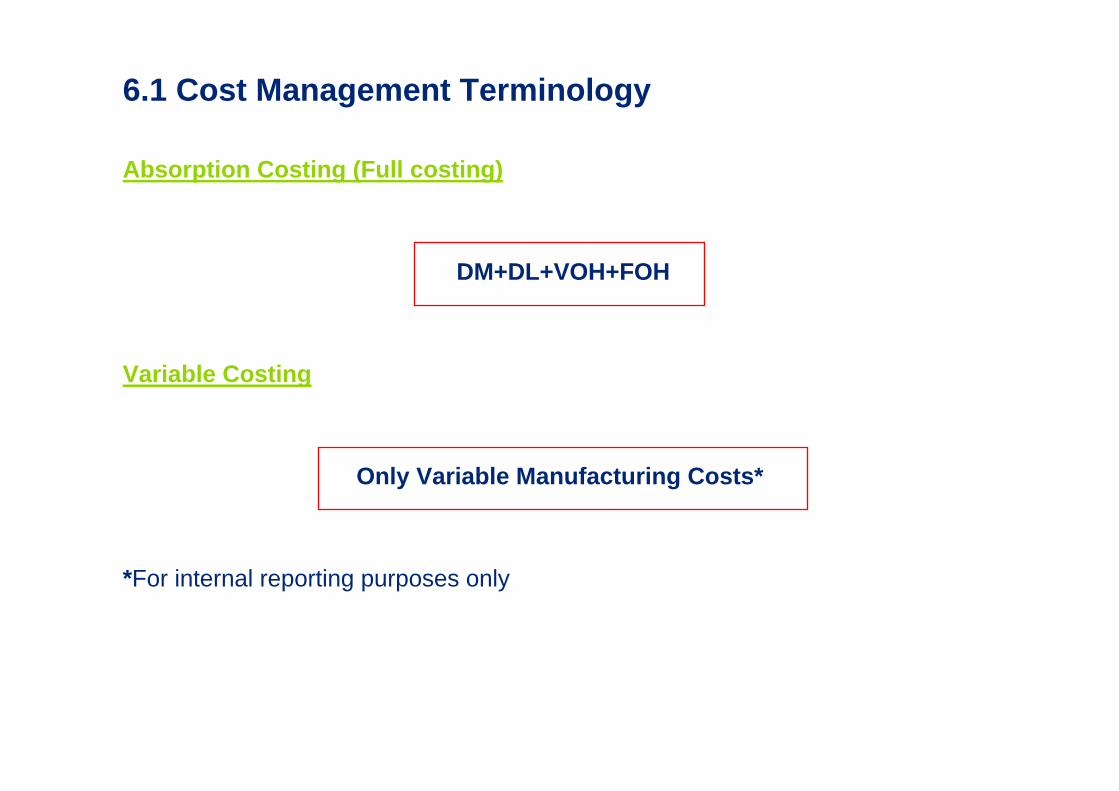

Absorption Costing (Full costing)

DM+DL+VOH+FOH

Variable Costing

Only Variable Manufacturing Costs*

*For internal reporting purposes only

©2012 Deloitte Touche Tohmatsu Jaiyos

6.1 Cost Management Terminology

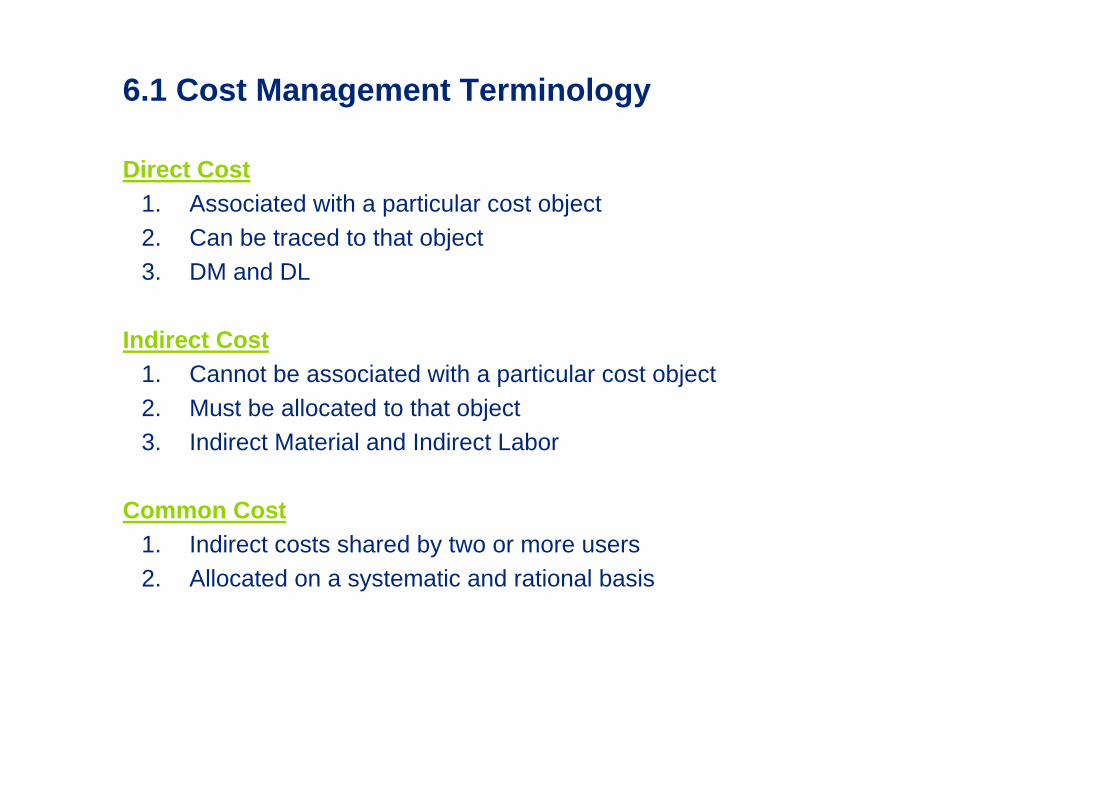

Direct Cost1. Associated with a particular cost object2. Can be traced to that object3. DM and DL

Indirect Cost1. Cannot be associated with a particular cost object2. Must be allocated to that object3. Indirect Material and Indirect Labor

Common Cost1. Indirect costs shared by two or more users2. Allocated on a systematic and rational basis

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

• A cost object is any entity to which costs can be attached. A cost driver is the basis used to assign cost object.

• The costs of manufacturing a product can be classified as one of three types: DM, DL, and MOH (indirect material, indirect labor, and factory operating costs)

• Product costs (inventoriable costs) are capitalized as part of finished goods inventory. They eventually become a component of cost of goods sold.

• Period costs are expensed as incurred. They are not capitalized in finished goods inventory and are thus excluded from cost of goods sold.

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review

1. Using absorption costing, fixed manufacturing overhead costs are best described as:

a) Direct period costs

b) Indirect period costs

c) Direct product costs

d) Indirect product costs

Answer (D): Fixed manufacturing overhead costs are indirect costs because they cannot be directly traced to specific units produced.

©2012 Deloitte Touche Tohmatsu Jaiyos

6.2 Cost Behavior and relevant Range

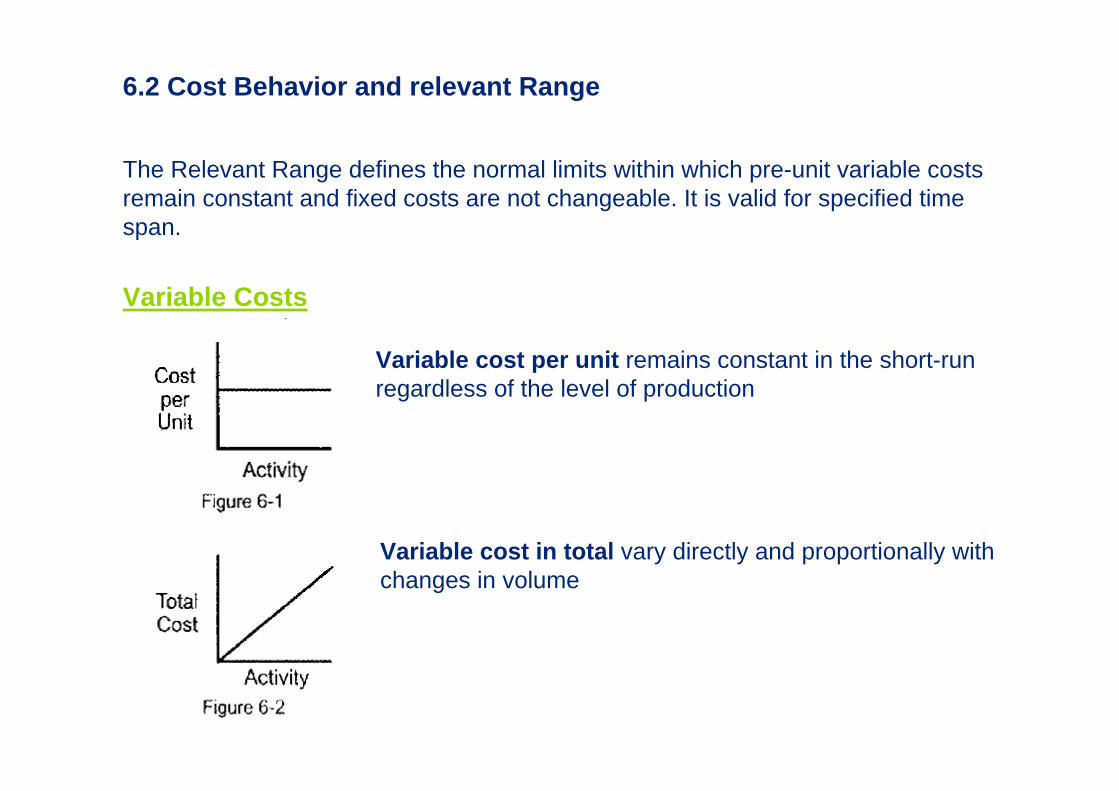

The Relevant Range defines the normal limits within which pre-unit variable costs remain constant and fixed costs are not changeable. It is valid for specified time span.

Variable Costs

Variable cost per unit remains constant in the short-run regardless of the level of production

Variable cost in total vary directly and proportionally with changes in volume

©2012 Deloitte Touche Tohmatsu Jaiyos

6.2 Cost Behavior and relevant Range

Fixed Costs

Fixed Costs in Total remain unchanged in the short run regardless of production level.

Fixed Cost per unit vary indirectly with the activity level.

©2012 Deloitte Touche Tohmatsu Jaiyos

6.2 Cost Behavior and relevant Range

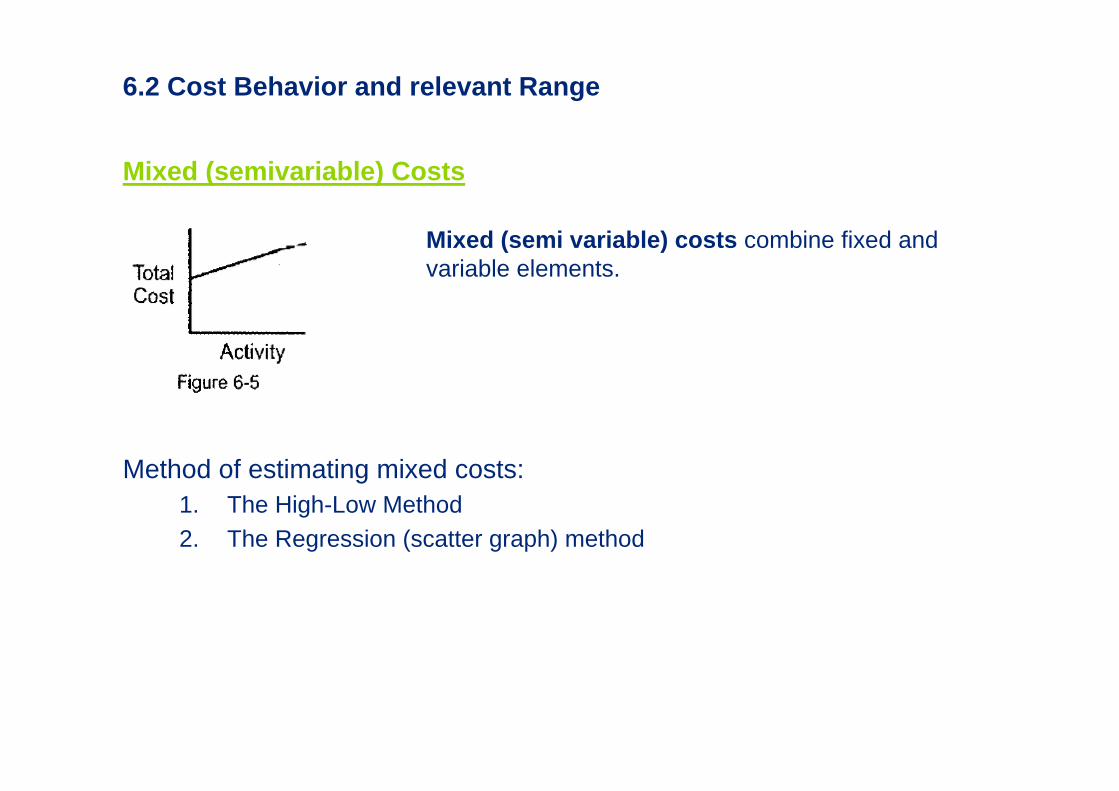

Mixed (semivariable) Costs

Method of estimating mixed costs:1. The High-Low Method2. The Regression (scatter graph) method

Mixed (semi variable) costs combine fixed and variable elements.

©2012 Deloitte Touche Tohmatsu Jaiyos

6.2 Cost Behavior and relevant Range

©2012 Deloitte Touche Tohmatsu Jaiyos

6.2 Cost Behavior and relevant Range

©2012 Deloitte Touche Tohmatsu Jaiyos

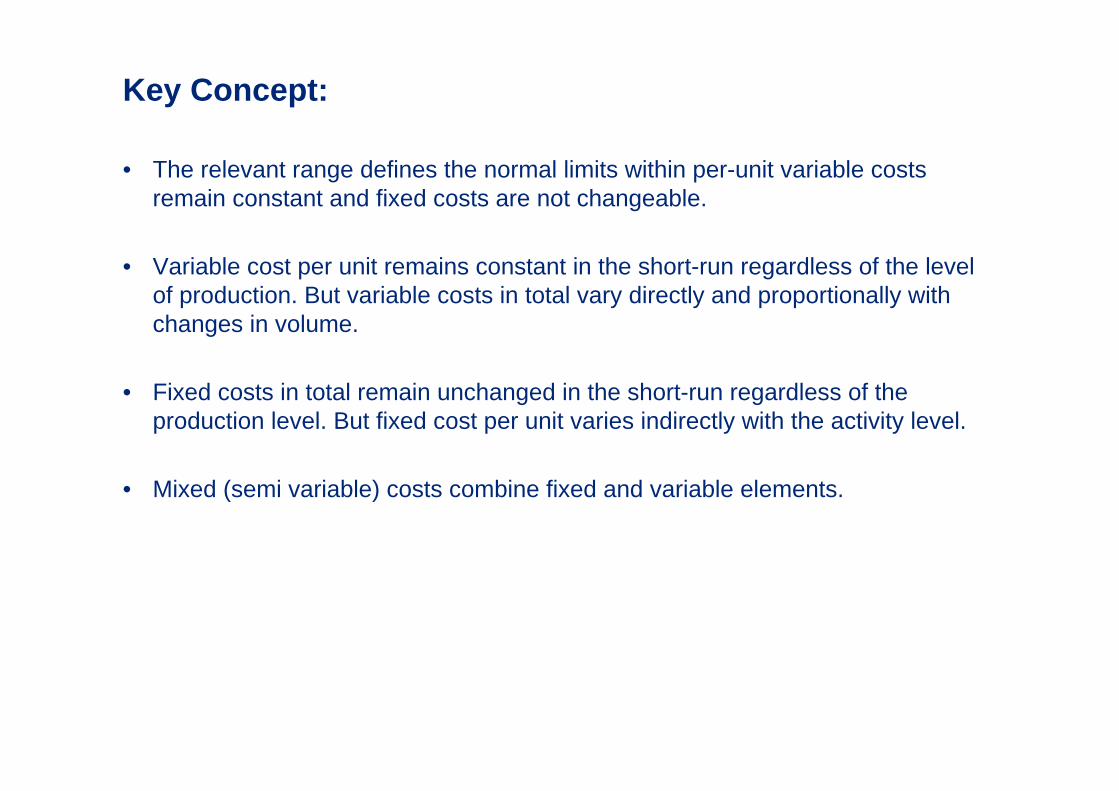

Key Concept:

• The relevant range defines the normal limits within per-unit variable costs remain constant and fixed costs are not changeable.

• Variable cost per unit remains constant in the short-run regardless of the level of production. But variable costs in total vary directly and proportionally with changes in volume.

• Fixed costs in total remain unchanged in the short-run regardless of the production level. But fixed cost per unit varies indirectly with the activity level.

• Mixed (semi variable) costs combine fixed and variable elements.

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review1. An assembly plant accumulates its variable and fixed manufacturing overhead costs in a

single cost pool, which is then applied to work in process using a single application base. The assembly plant management wants to estimate the magnitude of the total manufacturing overhead costs for different volume levels of the application activity base using a flexible budget formula. If there is an increase in the application activity base that is within the relevant range of activity for the assembly plant, which one of the following relationships regarding variable and fixed costs is true.

a) The variable cost per unit is constant, and the total fixed costs decrease

b) The variable cost per unit is constant, and the total fixed costs increase.

c) The variable cost per unit and the total fixed costs remain constant

d) The variable cost per unit increases, and the total fixed costs remain constant

Answer (C): Total variable cost changes when changes in the activity level occur within the relevant range. The cost per unit for a variable cost is constant for all activity levels within the relevant range. Thus, if the activity volume increases within the relevant range, total variable costs will increase. A fixed cost does not change when volume changes occur in the activity level within the relevant range. If the activity volume increases within the relevant range, total fixed costs will remain unchanged.

©2012 Deloitte Touche Tohmatsu Jaiyos

6.3 Absorption (Full) vs. Variable (Direct) Costing

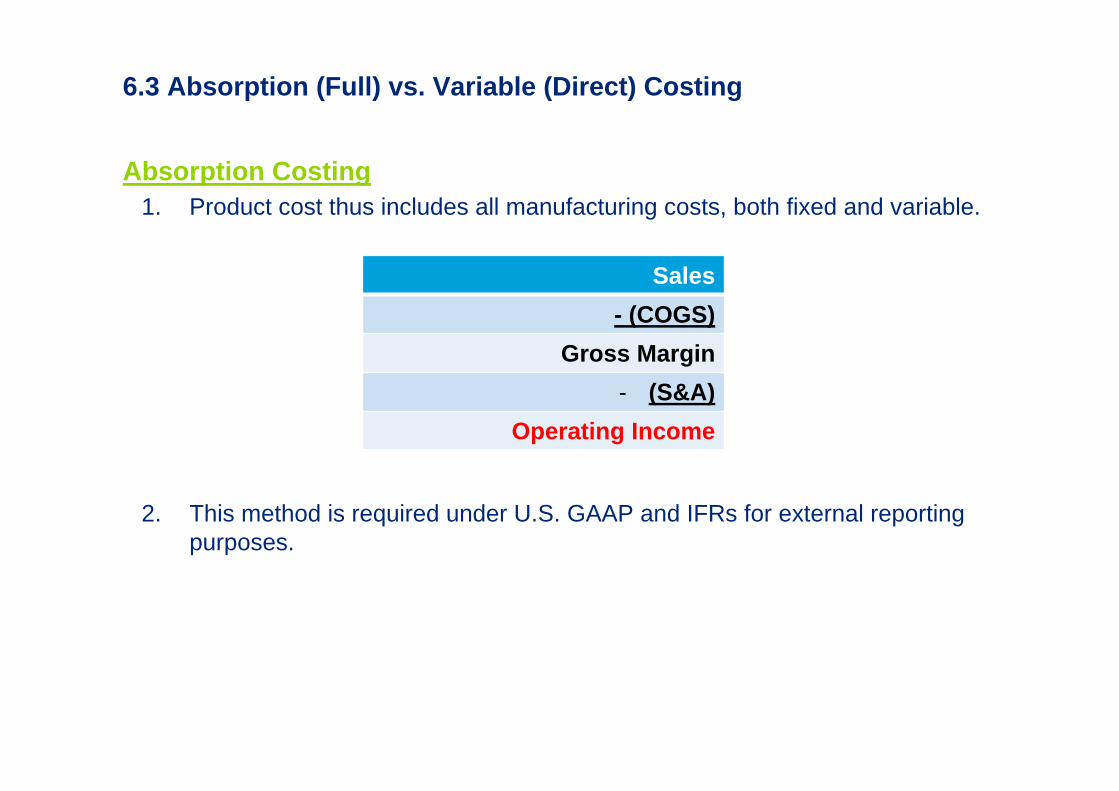

Absorption Costing1. Product cost thus includes all manufacturing costs, both fixed and variable.

2. This method is required under U.S. GAAP and IFRs for external reporting purposes.

Sales- (COGS)

Gross Margin- (S&A)

Operating Income

©2012 Deloitte Touche Tohmatsu Jaiyos

6.3 Absorption (Full) vs. Variable (Direct) Costing

Variable Costing1. Product cost includes only variable manufacturing cost.

2. This method is also called contribution margin reporting.

Sales- (Variable COGS)

- (Variable S&A)Contribution Margin

©2012 Deloitte Touche Tohmatsu Jaiyos

6.3 Absorption (Full) vs. Variable (Direct) Costing

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

• Under absorption costing, the fixed portion of manufacturing overhead is included in the cost of each product. Product cost thus includes all manufacturing costs, both fixed and variable. Absorption-basis cost of goods sold is subtracted from sales to arrive at gross margin.

• Variable costing is more appropriate for internal reporting. Product cost includes only variable manufacturing costs. Variable-basis cost of goods sold and the variable portion of S&A expenses are subtracted from gross margin to arrive at contribution margin.

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review1. A company manufactures and sells a single product. Planned and actual production in its

first year of operation was 100,000 units. Planned and actual costs for that year were as follows:

The company sold 85,000 units of product at a selling price of US $ 30 per unit. Using absorption costing, the company’s operating profit was:

a) US $750,000b) US $900,000c) US $975,000d) US $1,020,000

Answer (B): Revenue (85,000*30) – COGS (85,000*10) – Nonmanufacturing costs (500,000+300,000) = Operating Profit 900,000

Manufacturing NonmanufacturingVariable US $600,000 US $500,000Fixed 400,000 300,000

©2012 Deloitte Touche Tohmatsu Jaiyos

6.4 Capital Budgeting

©2012 Deloitte Touche Tohmatsu Jaiyos

6.4 Capital Budgeting

©2012 Deloitte Touche Tohmatsu Jaiyos

6.4 Capital Budgeting

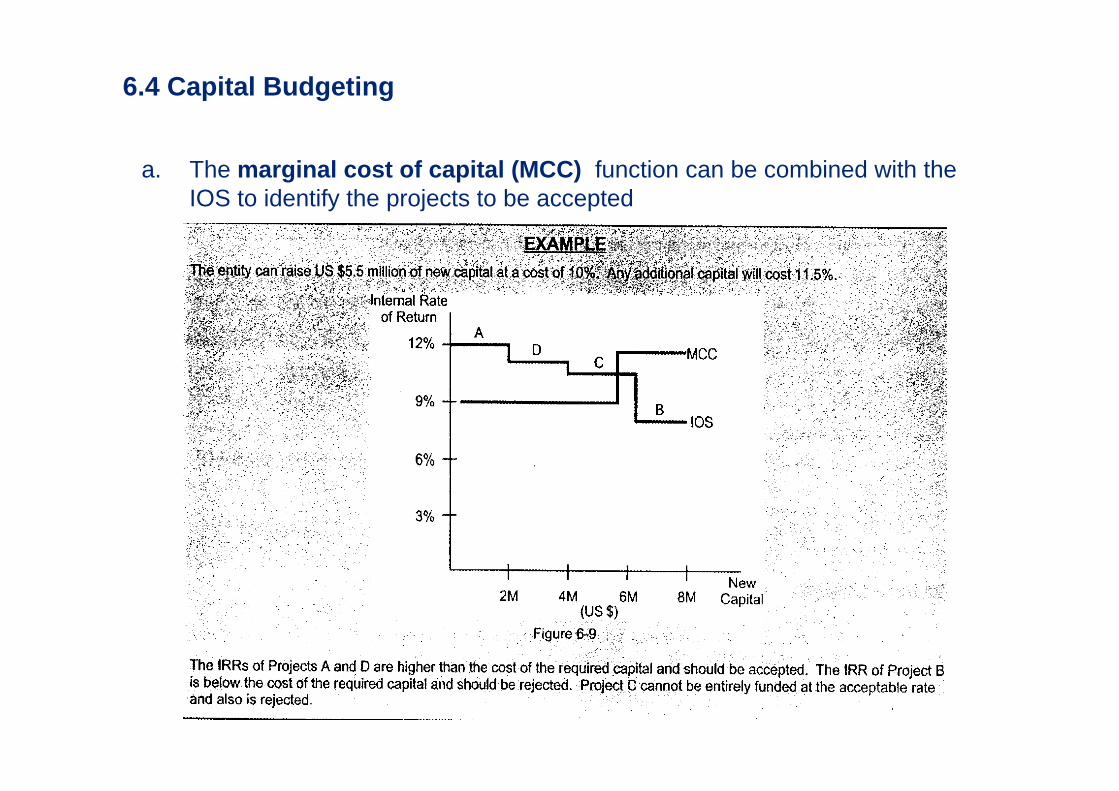

6. An investment opportunity schedule (IOS) is a graph useful in determining the optimal capital budgets.

©2012 Deloitte Touche Tohmatsu Jaiyos

6.4 Capital Budgeting

a. The marginal cost of capital (MCC) function can be combined with the IOS to identify the projects to be accepted

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

• Capital budgeting is the process of planning and controlling investments for long-term projects. A capital project should only be undertaken if management expects it will increase shareholder value.

• The NPV method for projecting the profitability of an investment expresses a project’s return in dollar terms. NPV nets the expected cash inflows andoutflows related to a project, then discount them at the hurdle rate, also called the desired rate of return.

• The IRR method express a project’s return in percentage terms. The IRR of an investment if the discount rate at which the investment’s NPV equals zero.

• The payback period is the number of years required to recover the original investment.

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review1. Everything else being equal, the internal rate of return (IRR) of an investment project will

be lower if:

a) The investment cost is lower

b) Cash inflows are received later in the life of the project

c) Cash inflows are larger

d) The project has a shorter payback period.

Answer (B): The IRR is the discount rate at which the NPV of a capital project is zero. Because the PV of a dollar is higher the sooner it is received, projects with later CF will have lower NPV for any given discount rate than will projects with earlier CF, if other factors are constant. Hence, projects with later CF will have a lower IRR.

©2012 Deloitte Touche Tohmatsu Jaiyos

6.5 Budget Systems

Purposes of a Budget

1. A formal management plan stated in monetary terms:• A planning tools• A control tool• A motivational tool• A means of communication and coordination

Master Budget2. The master budget, also called comprehensive budget or annual profit

plan, consists of the organization’s operating and financial plans for a specified period

©2012 Deloitte Touche Tohmatsu Jaiyos

6.5 Budget Systems

©2012 Deloitte Touche Tohmatsu Jaiyos

6.5 Budget Systems

©2012 Deloitte Touche Tohmatsu Jaiyos

6.5 Budget Systems

Kaizen

7. Kaizen means continuous improvement, and kaizen budgeting assumes the continuous improvement of products and processes.

Static and Flexible Budgeting

8. A Static Budget is based on only one level of sales or production. A Flexible Budget is a series of budgets prepared for various levels of activity within the relevant range.

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

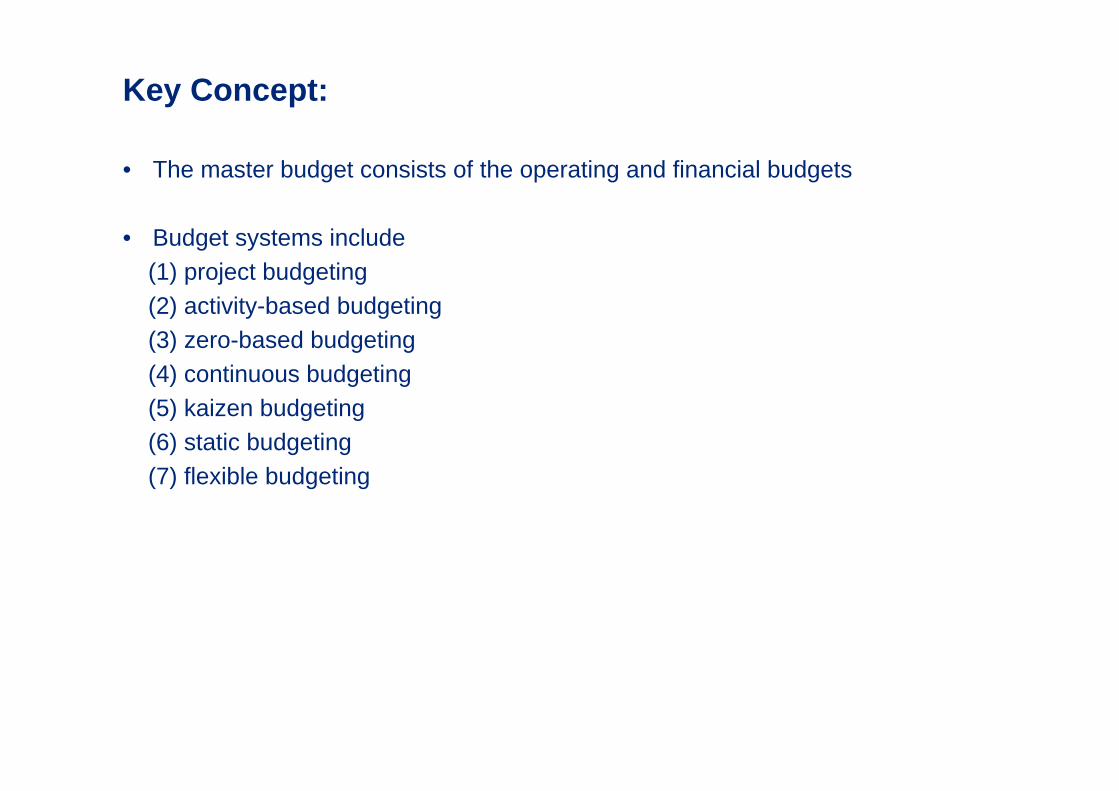

• The master budget consists of the operating and financial budgets

• Budget systems include (1) project budgeting (2) activity-based budgeting(3) zero-based budgeting(4) continuous budgeting(5) kaizen budgeting(6) static budgeting(7) flexible budgeting

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review1. The major appeal of zero-based budgeting is that it

a) Solves the problem of measuring program effectiveness.

b) Relates performance to resource inputs by an integrated planning and resource-allocation process.

c) Reduces significantly the time required to review a budget.

d) Deals with some of the problems of the incremental approach to budgeting

Answer (D): The traditional approach to budgeting is the merely increase last year’s amounts by a given percentage or increment. Zero-based budgeting divides programs into packages of goals, activities, and required resources. The cost of each package is then recalculated, without regard to previous performance.

©2012 Deloitte Touche Tohmatsu Jaiyos

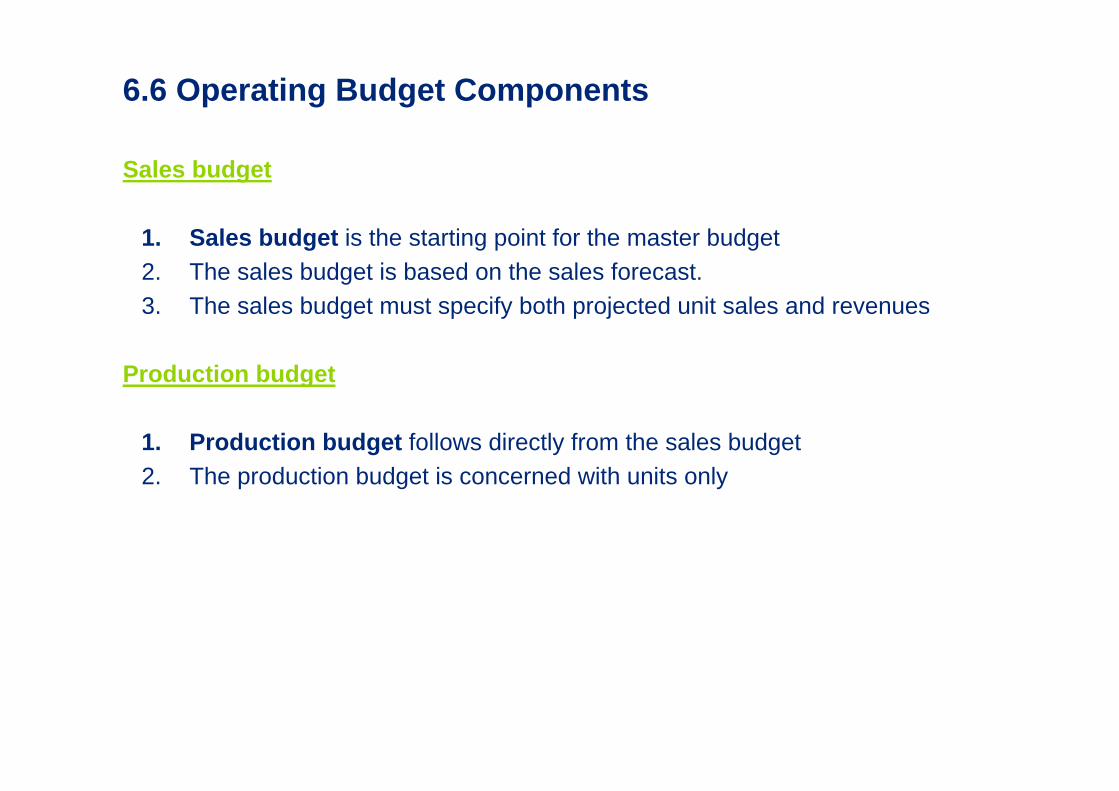

6.6 Operating Budget Components

Sales budget

1. Sales budget is the starting point for the master budget2. The sales budget is based on the sales forecast.3. The sales budget must specify both projected unit sales and revenues

Production budget

1. Production budget follows directly from the sales budget2. The production budget is concerned with units only

©2012 Deloitte Touche Tohmatsu Jaiyos

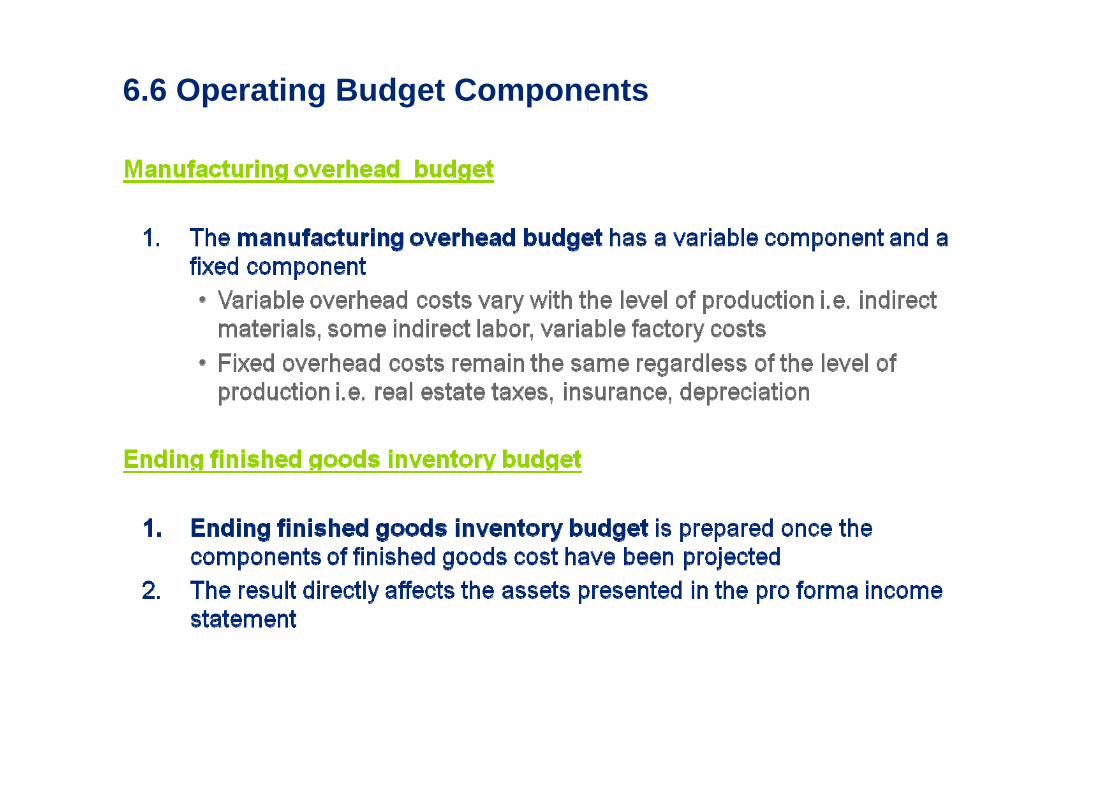

6.6 Operating Budget Components

Direct material and direct labor budgets

1. Follow directly from the production budget2. The direct materials budget is concerned with both units and input prices3. The direct labor budget depends on wage rates, amounts, and types of

production, numbers and skill levels of employees, fringe benefits.

Cost of fringe benefits

1. Must be derived once the cost of wages has been determined

©2012 Deloitte Touche Tohmatsu Jaiyos

6.6 Operating Budget Components

©2012 Deloitte Touche Tohmatsu Jaiyos

6.6 Operating Budget Components

©2012 Deloitte Touche Tohmatsu Jaiyos

6.6 Operating Budget Components

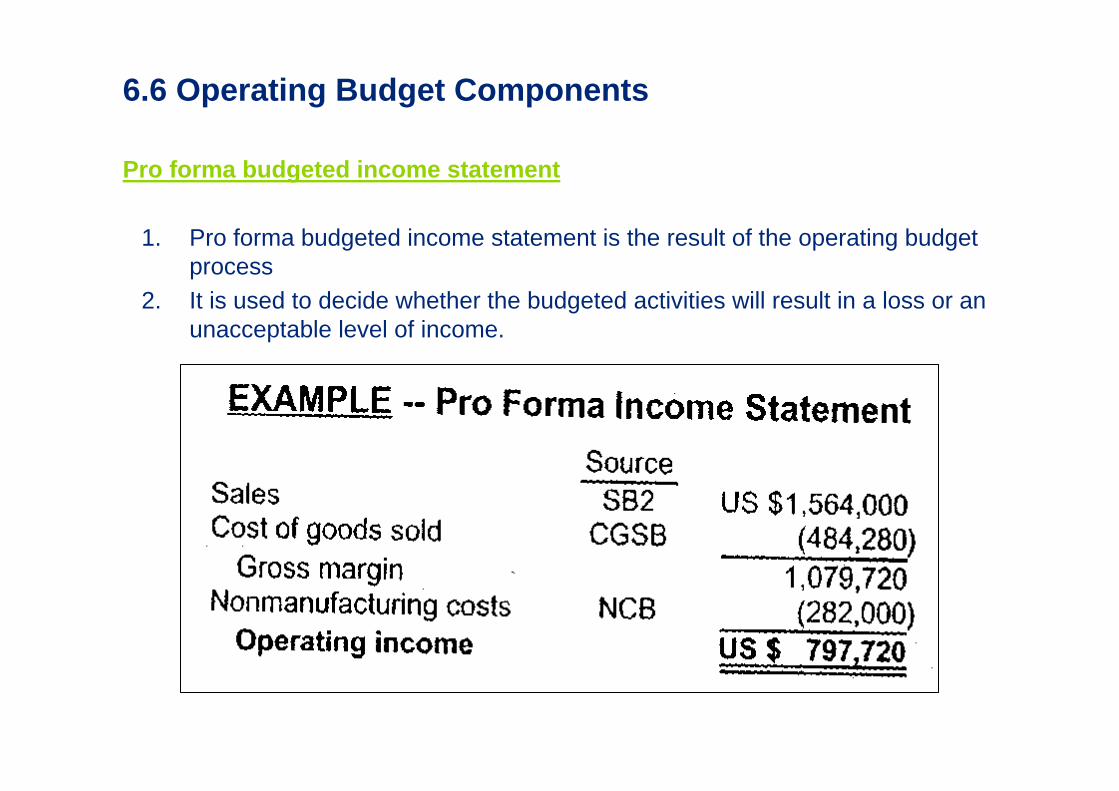

Pro forma budgeted income statement

1. Pro forma budgeted income statement is the result of the operating budget process

2. It is used to decide whether the budgeted activities will result in a loss or an unacceptable level of income.

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

• In the operating budget, the emphasis is on obtaining and using current resources.

• It contains the following budgets*:1. Sales2. Production3. Direct Materials4. Direct Labor5. Manufacturing Overhead6. Ending finished goods inventory7. Cost of goods sold8. Nonmanufacturing

*These budgets are used to prepare the pro forma income statement.

©2012 Deloitte Touche Tohmatsu Jaiyos

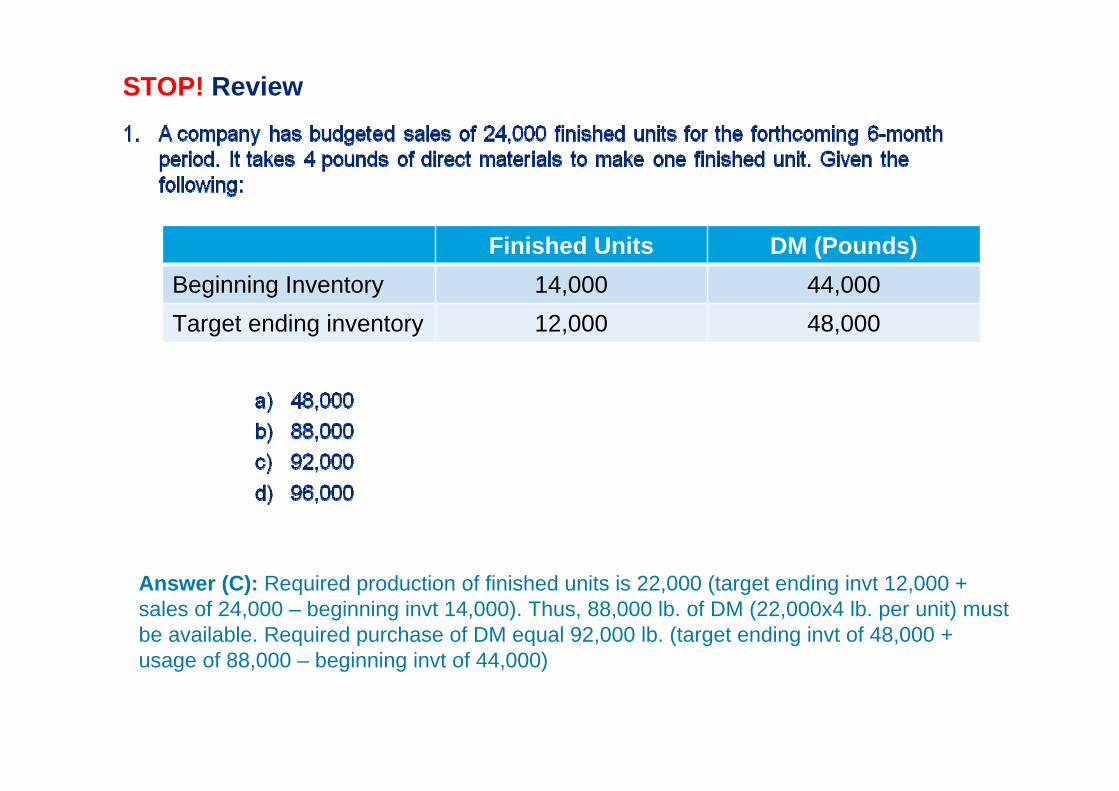

STOP! Review

Answer (C): Required production of finished units is 22,000 (target ending invt 12,000 + sales of 24,000 – beginning invt 14,000). Thus, 88,000 lb. of DM (22,000x4 lb. per unit) must be available. Required purchase of DM equal 92,000 lb. (target ending invt of 48,000 + usage of 88,000 – beginning invt of 44,000)

Finished Units DM (Pounds)Beginning Inventory 14,000 44,000Target ending inventory 12,000 48,000

©2012 Deloitte Touche Tohmatsu Jaiyos

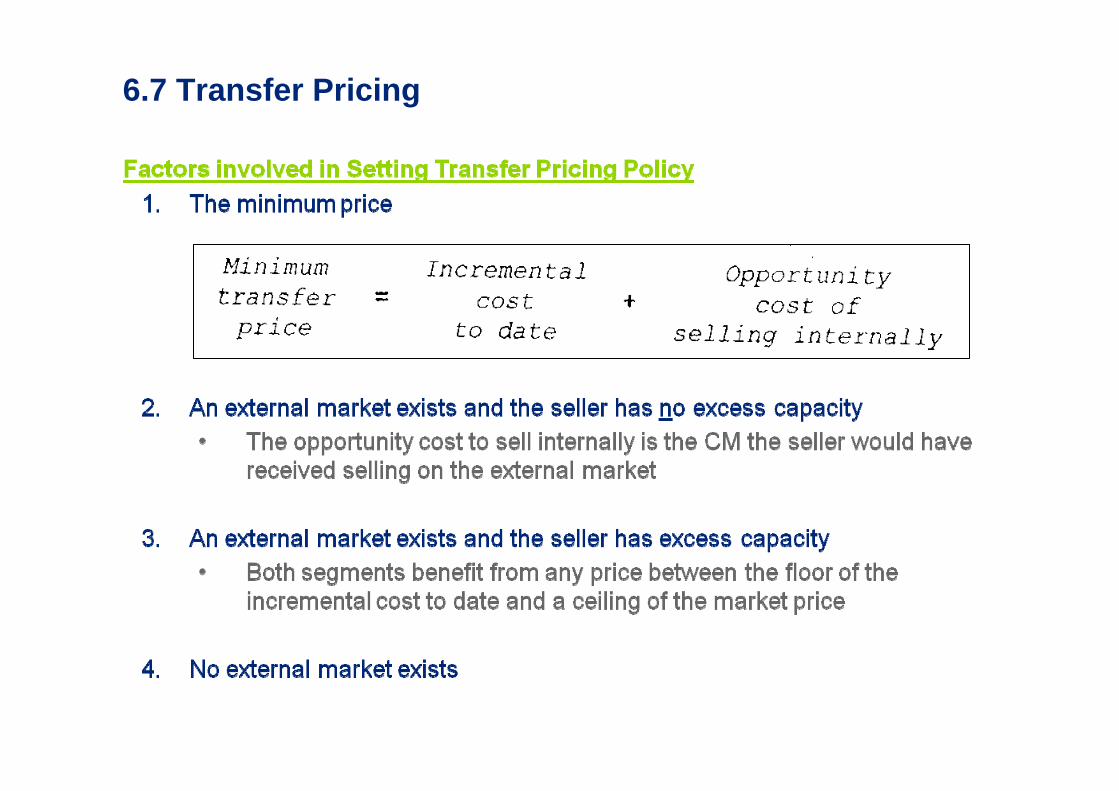

6.7 Transfer Pricing

©2012 Deloitte Touche Tohmatsu Jaiyos

6.7 Transfer Pricing

Methods

1. Cost plus pricing: sets price at the selling segment’s full cost of production plus a reasonable markup

2. Market pricing: uses the price the selling segment could obtain on the open market.

3. Negotiated pricing: gives the segments the freedom to bargain among themselves to agree on price

©2012 Deloitte Touche Tohmatsu Jaiyos

6.7 Transfer Pricing

©2012 Deloitte Touche Tohmatsu Jaiyos

6.7 Transfer Pricing

Multinational Considerations

1. When segments are located in different countries, taxes and tariffs may override any other considerations when setting transfer pricing

2. Exchange rate fluctuations, threats of expropriation and limits on transfers of profits outside the host country are additional concerns.

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

• Transfer prices are the amounts charged by one segment of an organization for goods and services it provides to another segment of the same organization.

• Three basic methods for determining transfer prices are: cost plus pricing, market pricing, and negotiated pricing

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review

Answer (B): The optimal transfer price of a selling division should be set at a point that will have the most desirable economic effect on the firm as a whole while at the same time continuing to motivate the management of every division to perform efficiently. Setting the transfer price based on actual costs rather than standard costs would give the selling division little incentive to control costs.

©2012 Deloitte Touche Tohmatsu Jaiyos

6.8 Cost-Volume-Profit (CVP) Analysis

©2012 Deloitte Touche Tohmatsu Jaiyos

6.8 Cost-Volume-Profit (CVP) Analysis

Cost-Volume-Profit Analysis

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

• Cost-volume-profit analysis (breakeven analysis) is a tool for understanding the interaction of revenues with fixed and variable costs

• The breakeven point is the level of output at which total revenues equal total expenses (operating income is zero)

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review

Answer (C): The breakeven (unit) = total fixed costs/unit contribution margin (4,950,000 total contribution margin/150,000 units sold). The breakeven point in unit sales is 46,080 (US $1,520,640 fixed costs/US $33 UCM)

Sales (150,000 Units) US $9,000,000Variable costs:

DM US $1,800,000

DL 720,000

MOH 1,080,000

Selling expenses 450,000

Fixed costs:

MOH US $600,000

Administrative exp 567,840

Selling Expenses 352,800

Income tax rate 40%

©2012 Deloitte Touche Tohmatsu Jaiyos

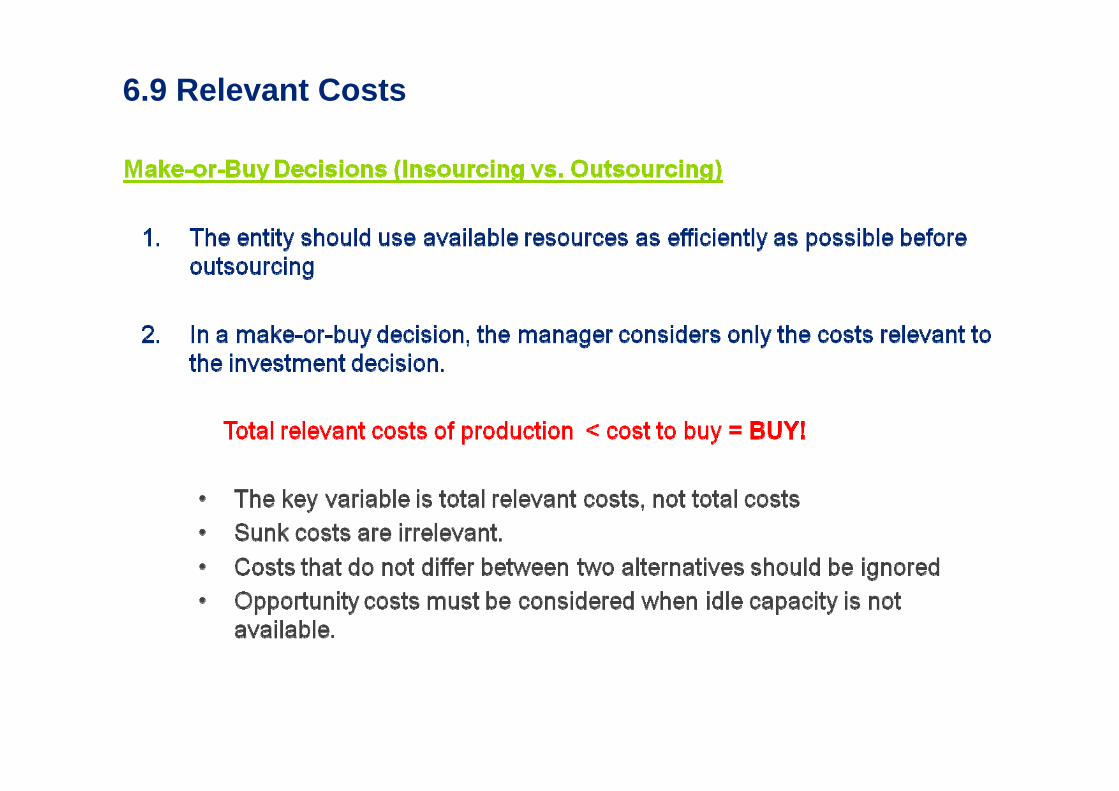

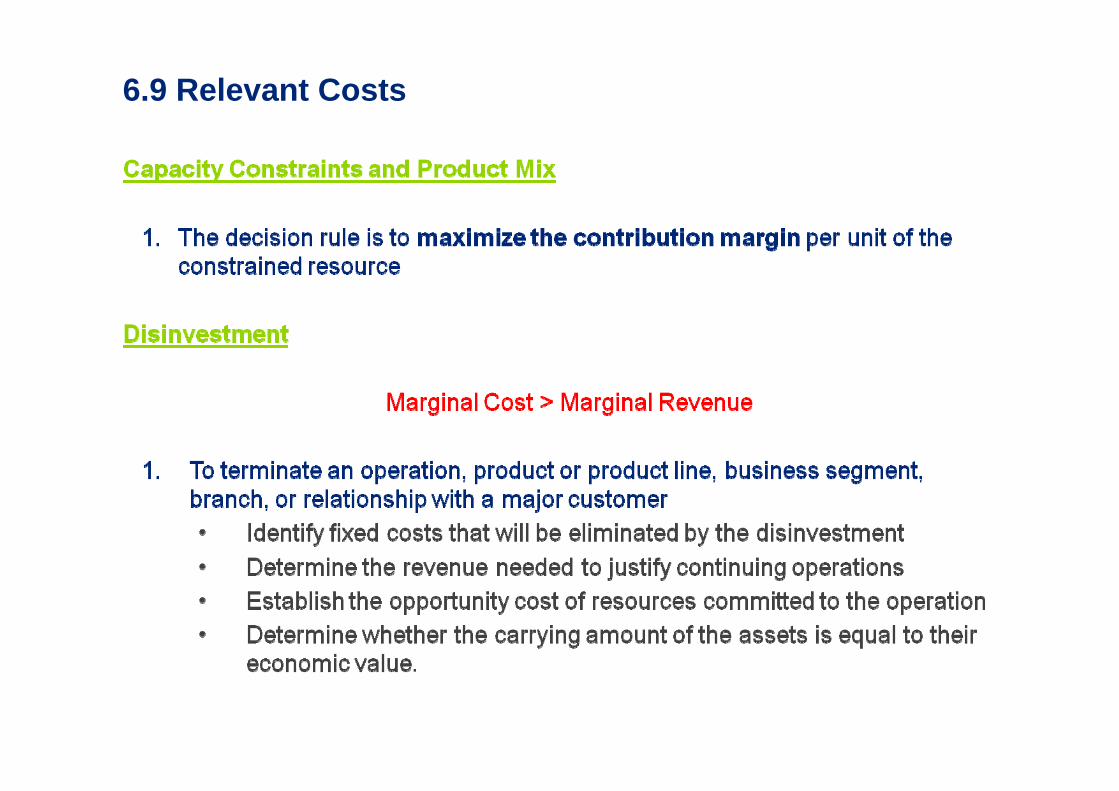

6.9 Relevant Costs

©2012 Deloitte Touche Tohmatsu Jaiyos

6.9 Relevant Costs

©2012 Deloitte Touche Tohmatsu Jaiyos

6.9 Relevant Costs

©2012 Deloitte Touche Tohmatsu Jaiyos

6.9 Relevant Costs

Sell-or-Proccess Further Decisions

1. The sell-or-process decision should be based on the relationship between the incremental costs (the cost of additional processing) and the incremental revenues (the benefits received)

Incremental cost < Incremental revenue = Process!

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

• The typical problem for which marginal (differential or incremental) analysis can be used involves choices among courses of action. The focus is on incremental revenues and costs.

• Applications of marginal analysis include make-or-buy decisions, special orders, disinvestment, and sell-or-process decisions.

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review

Answer (B): The revenue will increase by US $76,000 (10,000 units x 7.6). The cost will increase by US $60,000 [10,000 units x (3.0+1.0+0.8+1.2)]. Thus, acceptance of the special order will increase profit by US $16,000 ($76,000 - $60,000).

Variable costs:DM US $3.00

DL 1.00

MOH 0.8

Selling expenses 2.00

Fixed costs:

MOH US $90,000

Selling Expenses 60,000

©2012 Deloitte Touche Tohmatsu Jaiyos

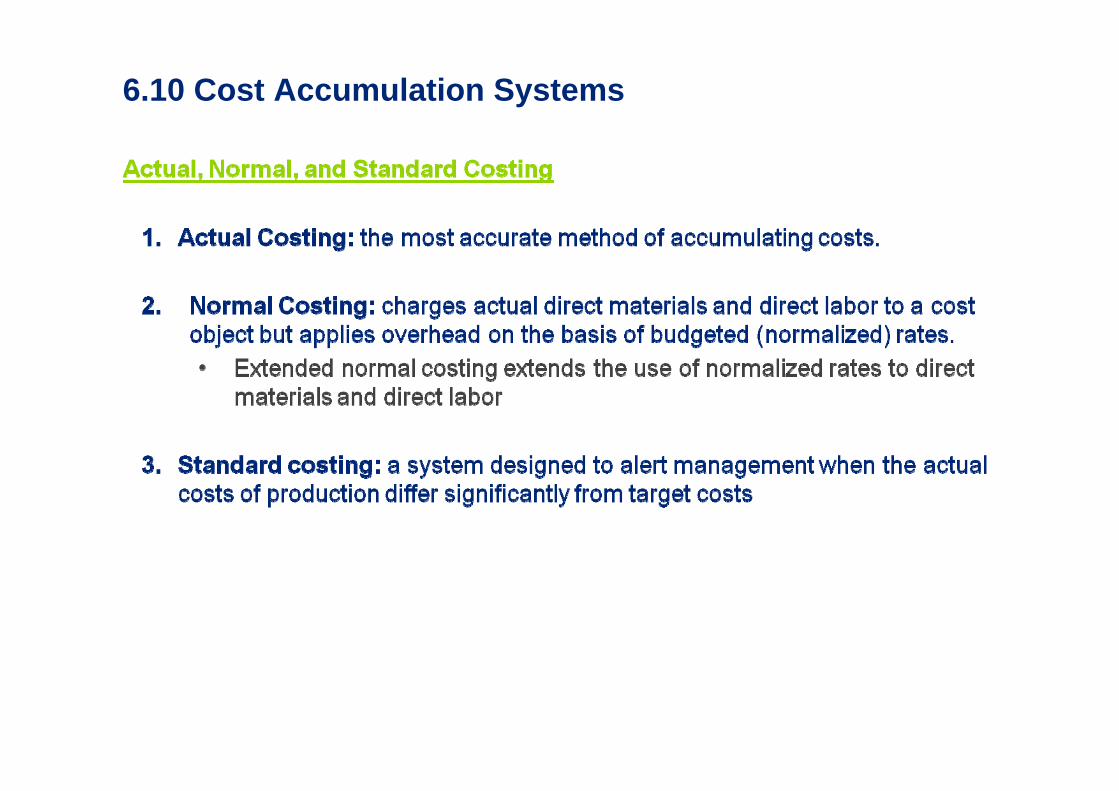

6.10 Cost Accumulation Systems

©2012 Deloitte Touche Tohmatsu Jaiyos

6.10 Cost Accumulation Systems

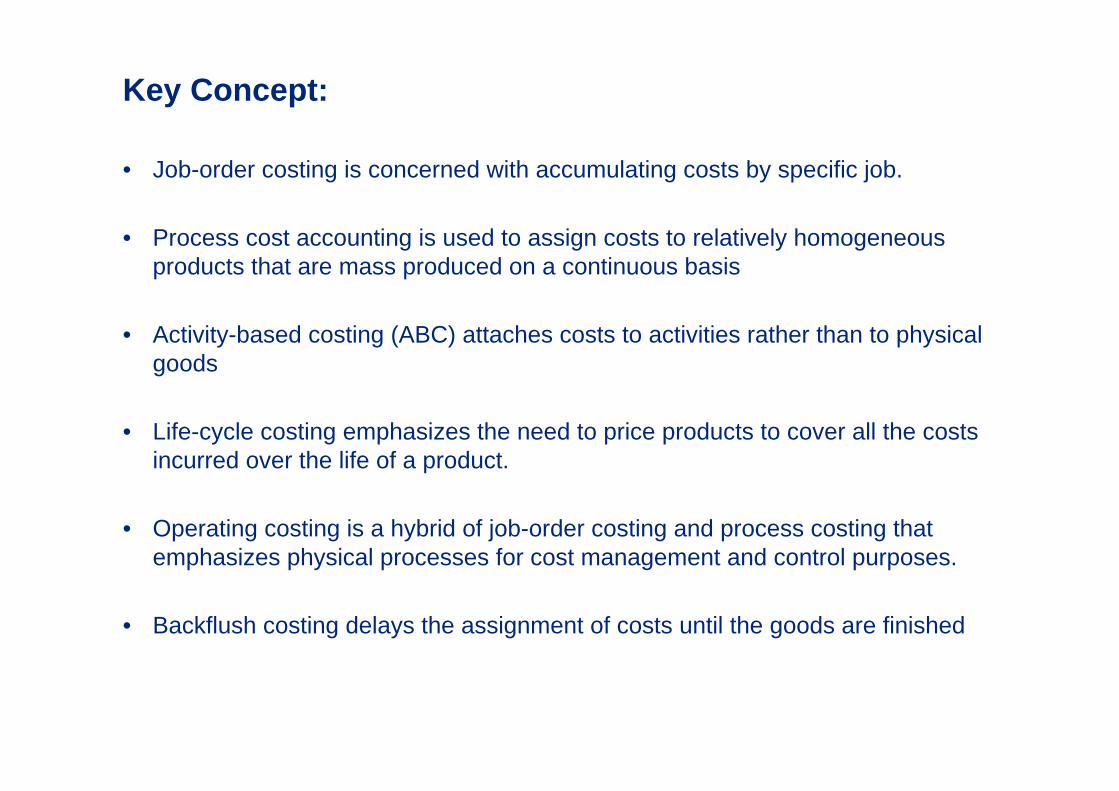

Cost Accumulation systems

1. Job costing: appropriate when producing products with individual characteristics or when identifiable groupings are possible.

2. Process costing: use when similar products are mass produced

3. Activity-based costing (ABC): attaches costs to activities rather than to physical goods.

4. Life-Cycle costing: emphasizes the need to price products to cover all the costs incurred over the life of a product

5. Operating cost: a hybrid of job-order and process costing and is used by entities whose manufacturing processes involve some dissimilar operations.

6. Backflush costing: delays the assignment of costs until the goods are finished

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

• Job-order costing is concerned with accumulating costs by specific job.

• Process cost accounting is used to assign costs to relatively homogeneous products that are mass produced on a continuous basis

• Activity-based costing (ABC) attaches costs to activities rather than to physical goods

• Life-cycle costing emphasizes the need to price products to cover all the costs incurred over the life of a product.

• Operating costing is a hybrid of job-order costing and process costing that emphasizes physical processes for cost management and control purposes.

• Backflush costing delays the assignment of costs until the goods are finished

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review

Answer (A): Job-order costing is used by organizations whose products or services are readily identified by individual units or batches. The advertising agency accumulates its costs by client. Job-order costing is the most appropriate system for this type of manufacturing firm.

©2012 Deloitte Touche Tohmatsu Jaiyos

6.11 Process Costing

©2012 Deloitte Touche Tohmatsu Jaiyos

6.11 Process Costing

©2012 Deloitte Touche Tohmatsu Jaiyos

6.11 Process Costing

©2012 Deloitte Touche Tohmatsu Jaiyos

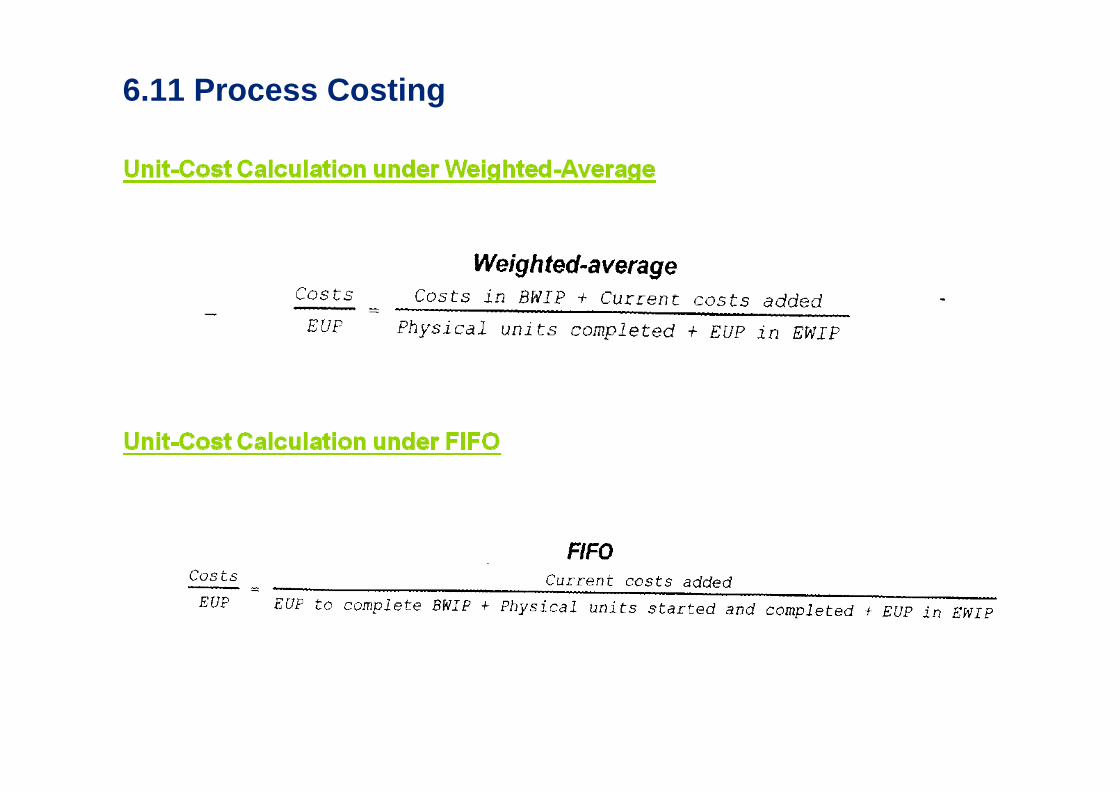

Key Concept:

• Process cost accounting is used to assign costs to similar products or service units that are mass produced on a continuous basis

• Equivalent units of production (EUP) are calculated to facilitate cost allocation when some units of output are not complete at the end of the period

• The weighted-average method of calculating EUP and unit costs essentially treats the work done on beginning work-in-process as if it had been done in the current period.

• The FIFO method calculates EUP and unit costs only for the work done and costs incurred in the current period

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review

Answer (C): Abnormal spoilage is spoilage that is not expected to occur under normal, efficient operating conditions. Because of its unusual nature, abnormal spoilage is typically treated as a loss in the period in which it is incurred.

©2012 Deloitte Touche Tohmatsu Jaiyos

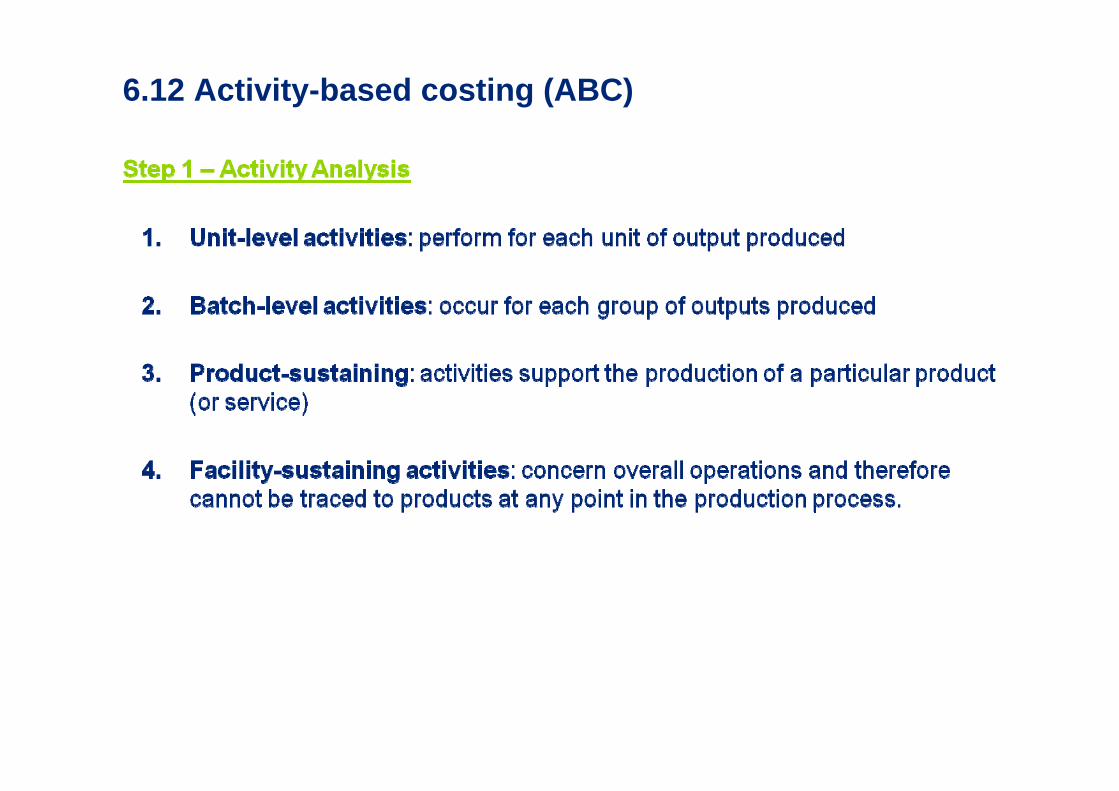

6.12 Activity-based costing (ABC)

©2012 Deloitte Touche Tohmatsu Jaiyos

6.12 Activity-based costing (ABC)

©2012 Deloitte Touche Tohmatsu Jaiyos

6.12 Activity-based costing (ABC)

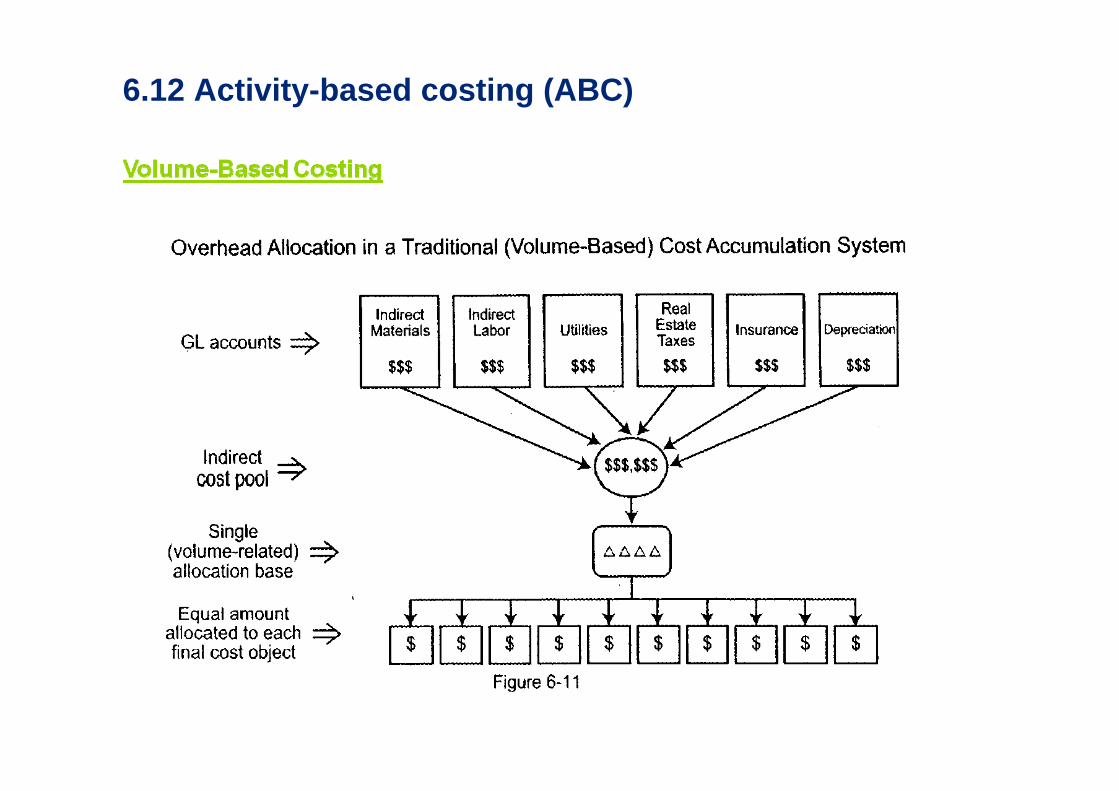

Volume-based system Activity-based system1. Accumulated costs in general

ledger accounts

2. Uses a single cost pool to combine the costs in all the related accounts

3. Selects a single driver to use for the entire indirect cost pool

4. Allocates the indirect cost pool to final cost objects

1. Identifies organizational activities that constitute overhead

2. Assigns the costs of resources consumed by the activities

3. Assigns the costs of the activities to final cost objects

©2012 Deloitte Touche Tohmatsu Jaiyos

6.12 Activity-based costing (ABC)

©2012 Deloitte Touche Tohmatsu Jaiyos

6.12 Activity-based costing (ABC)

©2012 Deloitte Touche Tohmatsu Jaiyos

6.12 Activity-based costing (ABC)

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

• Under ABC, indirect costs are attached to activities that are then rationally allocated to end products.

• An ABC system identifies organizational activities that constitute overhead, assigns the costs of resources consumed by the activities, and assigns the costs of the activities to final cost objects.

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review

Answer (B): An essential element of activity-based costing is driver analysis, which identifies the cause-and-effect relationship between an activity and its consumption of resources and for an activity and the demands made on it by a cost object. There is a direct causal relationship between the number of components in a finished product and the amount of material handling cost incurred.

©2012 Deloitte Touche Tohmatsu Jaiyos

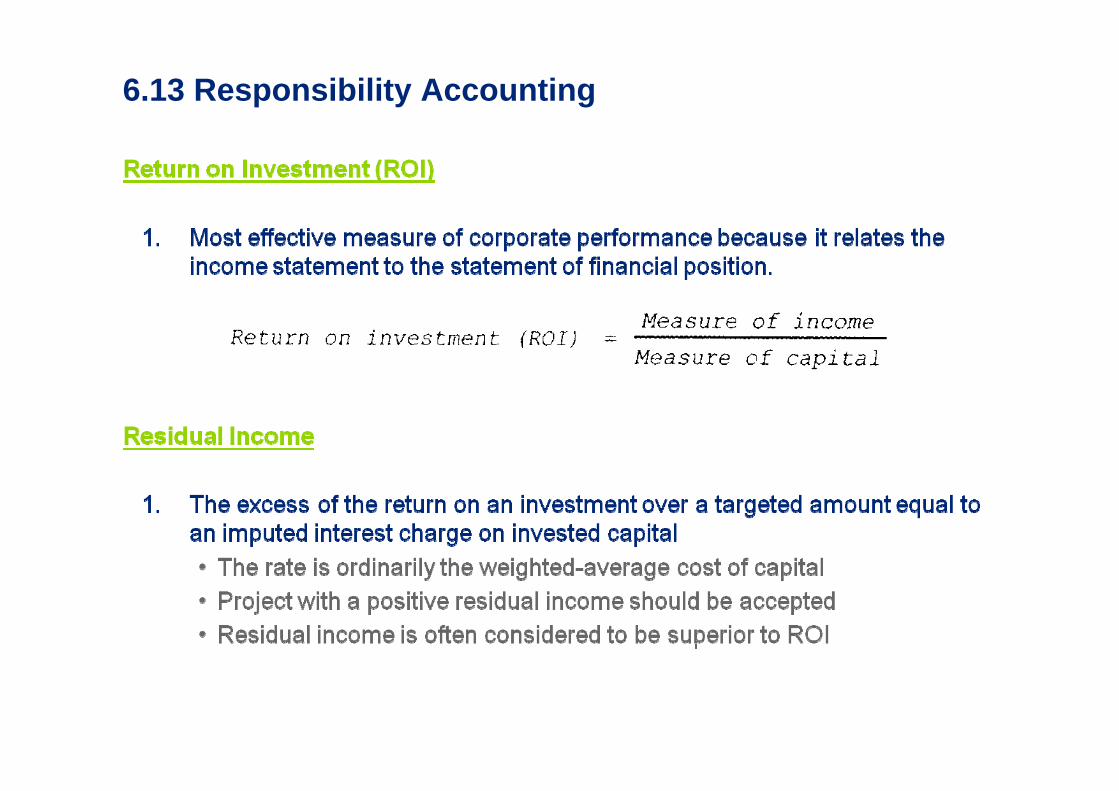

6.13 Responsibility Accounting

©2012 Deloitte Touche Tohmatsu Jaiyos

6.13 Responsibility Accounting

©2012 Deloitte Touche Tohmatsu Jaiyos

6.13 Responsibility Accounting

©2012 Deloitte Touche Tohmatsu Jaiyos

Key Concept:

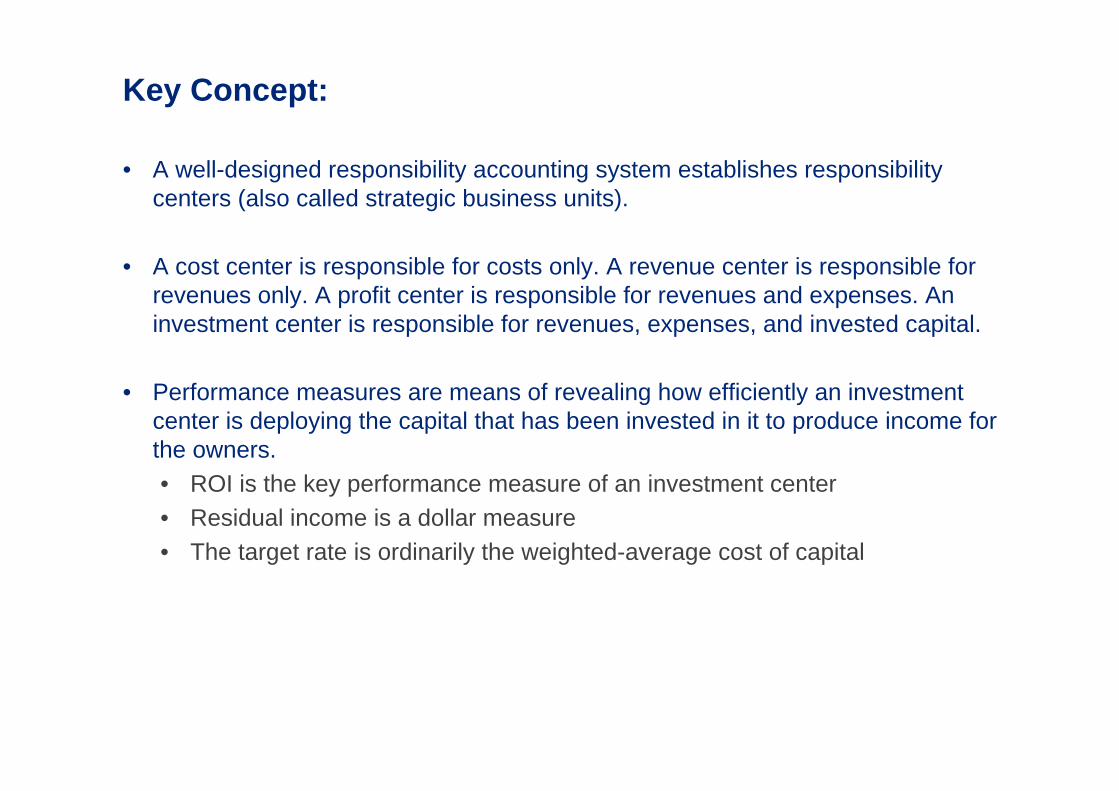

• A well-designed responsibility accounting system establishes responsibility centers (also called strategic business units).

• A cost center is responsible for costs only. A revenue center is responsible for revenues only. A profit center is responsible for revenues and expenses. An investment center is responsible for revenues, expenses, and invested capital.

• Performance measures are means of revealing how efficiently an investment center is deploying the capital that has been invested in it to produce income for the owners. • ROI is the key performance measure of an investment center• Residual income is a dollar measure• The target rate is ordinarily the weighted-average cost of capital

©2012 Deloitte Touche Tohmatsu Jaiyos

STOP! Review

Answer (D): A cost center is a responsibility center that is responsible for costs only. Of the alternatives given, variance analysis is the only one that can be used in a cost center. Variance analysis involves comparing actual costs with predicted or standard costs

©2012 Deloitte Touche Tohmatsu Jaiyos

Thank youAlisa Glankwamdee, CIA

E-mail : [email protected]: 081-949-4638