chss review report - · pdf filethis document contains the draft report of the chss review...

TRANSCRIPT

DRAFT REPORT OF CHSS REVIEW COMMITEE

This document contains the draft report of the CHSS review

committee. As decided in the meeting held with recognised

Unions/Associations a copy of the report is made available in the web

site. All Office bearers of Associations and Unions are requested to

submit their suggestions/views on the report by 31st December, 2006.

Suggestions may be sent to:

Under Secretary (Administration), DAE

Anushakti Bhavan, CSM Marg, Mumbai 400 001

By normal mail or Email: [email protected] (please mark subject as

‘CHSS Review Committee’)

November 21, 2006

1

DRAFT REPORT OF THE CHSS REVIEW COMMITTEE

The Department of Atomic Energy vide its order No.7(4)/2004-

CHSS/IR&W/8067 dated 31st October, 2005 constituted a committee

consisting of the following members to review the existing provisions of

Contributory Health Services Scheme (CHSS).

1) Shri V.P. Raja - Chairman Additional Secretary (I&M), DAE

2) Shri P. Venugopalan - Member Controller, BARC

3) Dr. D.K. Jaitly - Member Head, Medical Division, BARC

4) Shri P.M. Pawar - Member Deputy Controller of Accounts, BARC

5) Shri V. Dayalan - Member Officer on Special Duty (R&D), DAE

6) Shri P.P. Madhavan Kutty - Member Secretary Under Secretary, DAE

Consequent on the transfer of Shri V. Dayalan as CAO, IGCAR,

Shri M. Venugopalan, Deputy Secretary (A / IR&W), DAE replaced

Shri Dayalan as a Member of the Committee.

The terms of reference to the committee are as follows:-

1) examine the issues relating to eligibility criteria of dependents in

terms of age, income, residence and relationship with the employee,

etc.

2) review the existing facilities for other systems of medicines vis-à-vis

CHSS facilities

2

3) review the eligibility of beneficiaries for different classes of

accommodation, revision of subscription, checks and balance to

prevent misuse of the facilities

4) examine the issue of the long term sustainability of the current

subscription based CHSS and explore the possibility of replacing it

with medical insurance scheme

5) work out the financial implication of its recommendations along with

a proposal to finance the same without adding to the cost to the

exchequer.

The committee may call for suggestions from the recognized

Service Associations/Unions of the Department and data, if any, required

from various authorities operating the scheme and will also invite any

officer to attend its meetings.

The Committee was required to submit its report to the Department

before March 31, 2006.

The salient features of the scheme are:

The CHSS was introduced in the Department in the year 1962 by

Late Dr. H.J. Bhabha, the founder of the Nuclear Research Programme in

the country. Although all other Central Government employees were

covered either under the CGHS or CS(MA) Rules, there was an

imperative need with a legal obligation for a unique and distinctly

different medical care having regard to the functional intricacies of the

organization and hence a separate scheme i.e. CHSS was set up

exclusively in the Department. This was especially taking into account

the fact that the nature of occupation of Scientists and other employees

demanded evolving a high level medical care system involving not only a

3

routine treatment facility but a sort of medical auditing supported with a

research input as a matter of abundant caution in the area of nuclear

radiation. In the initial stage the scheme had covered only Mumbai based

units. However, as the activities of the Department expanded and

laboratories and plants were set up at different units, the scheme was

extended mutatis mutandis to many other places. In fact, in tune with the

growth of the Department, the CHSS has also recorded a phenomenal

expansion as an inbuilt system of the whole set up as a pathway to health

care in the Department and at present the scheme is in operation in 13

places like Mumbai, Tarapur, Kota, Talcher, Chennai, Kalpakkam,

Vadodara, Hyderabad, Indore, Manuguru, Tuticorin, Kolkata and

Mysore. The scheme is being administered by the following authorities:

Place Administering Year of Authority introduction

Mumbai & Mysore - Director, BARC 1962/2002

Tarapur - Station Director, TAPS 1967

Kota - Station Director, RAPS 1965

Talcher/Manuguru - Chief Executive, HWB 1977/1988 Vadodara/Tuticorin 1998/1998

Kalpakkam/Chennai - Director, IGCAR 1993/1993

Indore - Director, CAT 1986

Kolkata - Director, VECC 1998

Hyderabad - Chief Executive, NFC 2003

Scope and Application

In addition to DAE employees, the scheme covers the staff of

NPCIL, TIFR, TMC, SINP, IMSc and AEES. Employees of ECIL, IRE,

UCIL, IOP, IPR and HRI are not covered under the scheme.

4

Beneficiaries of the scheme shall not be entitled to claim

reimbursement under Central Services (Medical Attendance) Rules, 1944

for treatment availed under the modern systems of medicare while in their

concerned CHSS station.

The Scheme covers both the serving and retired employees and

their family members. Family for the purpose include employee’s

wife/husband as the case may be, dependent children upto 25 years and

dependent parents. The Scheme also provides for inclusion of one of the

dependent relatives of an employee on payment of additional contribution

equal to the average per capita expenditure. Under the Scheme, a

beneficiary is entitled to medical treatment both as an out patient and

inpatient in the Departmental Hospitals or referral hospitals recognized

under the Scheme. Treatment under the Scheme includes for both

ordinary ailments and also for specialized treatment for acute and chronic

diseases like cancer, heart ailments etc. and no cost ceiling limits have

been prescribed for any treatment. The Scheme also provides for

Pathological investigations and X-rays examinations, maternity facilities,

reimbursement of expenses incurred in medical emergencies etc.

The Committee was constituted to examine in depth the issues

listed on pages 1-2 and suggest improvements for running the scheme and

also examined the financial viability of the scheme. In other words, the

main task assigned to the Committee was to come up with suggestions/

recommendations to make the Scheme to offer better services and at the

same time make it financially more viable by generating the required

funds to meet its running cost, on a sustained basis. The “cost-

effectiveness” of various facilities provided under the scheme was also to

be looked into by the Committee.

5

As a first step towards modification of the provision of the

Scheme, a statement on about 30 points based on the queries/

clarifications sought by various units in the past was prepared. The

statement was sent to the Heads of Units eliciting their comments and

also suggestions, if any, to improve the Scheme for the consideration of

the Committee. The Committee also collected various statistical

information from the offices concerned relating to CHSS. The data so

collected and tabulated in a statement form are furnished as Annexures.

The committee held seven meetings. After detailed deliberations,

the Committee recommends the following additions/modifications/

amendments to be made in the Scheme:-

Point-1. Inclusion of dependent relatives on payment of normal contribution at 1% of the pay in lieu of per capita expenditure as existing in Clause 18.1.

Existing provision (Clause 18.1)

The employees are not ordinarily permitted to register their

dependent relatives. Notwithstanding what has been stated above, in

extra-ordinary cases the administering authorities may allow an employee

to register under the scheme, one of his/her relatives, who is entirely

dependent upon and residing with him/her on payment of an additional

contribution, at a rate equal to the average per capita expenditure (without

any element of subsidy) borne by the scheme in the preceding year. This

additional contribution would be payable for a minimum period of one

year, even when benefits are availed of for a period shorter than this.

Further, before the request for registration in this regard is entertained,

the relative must have actually been staying with the employee concerned

6

for a minimum period of 60 days. Benefits of the scheme will be allowed

to relatives on the same scale as admissible to members of family.

The term, relative, for the above purpose, would be restricted to

brothers and unmarried and widowed sisters and such near relatives only.

Recommendation

After detailed discussion, it was decided that the existing provision on this can continue having regard to the following facts:

1. The contribution is payable by the employees concerned based on per-capita expenditure, i.e. without the element of subsidy.

2. The number of employees availing of this facility is very negligible.

3. It ensures medi-care facility to the dependent brothers, sisters, etc. which otherwise sometimes would be an handicap for certain young scientists even to continue their services in the Department.

Point 2. Inclusion of a provision for medical coverage to the Scientists/Engineers visiting foreign countries on deputation or tour. Existing provision

No provision

Recommendation

It is noted that one of the conditions for travel abroad covers taking

medical insurance and as such it was decided not to make any specific

provision in this regard in the Scheme. Moreover the scheme is only for

treatment within the Country.

7

Point 3. Extension of coverage to dependent daughter/son after completion of 25 years of age and reviewing the provisions regarding registration of children/parents with regard to computation of income, staying together etc.

Existing provision (Clause 4.1(b)

Children, step-children or legally adopted children upto 25 years of

age restricted to two. Addition in the number of children can be allowed

on payment of extra contribution in respect of each child in multiples of

one extra rate for each additional child. However, as a general exception,

payment of such contribution will not be applicable for inclusion of

children in case of twin/triplet birth in the second delivery even though

there is already one living child. Children beyond the age of 18 years and

upto 25 years will be eligible for continuation under the Scheme provided

they are not gainfully employed. However, in case of any hardship, in

individual cases, for justifiable reasons, a relaxation shall be made by the

Department, on the basis of recommendation of the Head of the Unit in

the matter of upper age limit.

Parents of the prime beneficiary who are wholly dependent on the

prime beneficiary and normally residing with the prime beneficiary and

further provided the monthly income of both the parents from all sources

does not exceed Rs.4000/-.

Recommendation

The Committee felt that the present restriction of upper age limit

upto 25 years in the case of dependent children is very much reasonable

in-as-much-as the children are expected to become matured for securing

employment at this stage. This is especially for the reason that there is

8

already a provision in the Scheme to relax the age limit beyond 25 years

in deserving cases. Life long coverage is also available to the children

who are physically/mentally challenged.

As regards the question of fixing an upper limit for computation of

income, it was noted that the present ceiling of Rs.4000/- p.m. was fixed

in the year 2000 and raising the same can be considered when the present

limit under the CGHS/CS(MA) Rules which is Rs.1500/- p.m. is revised.

The Committee felt that there is no necessity to change the stipulation

that dependent should stay together with the employee to continue as

family members.

Point 4. Removal of the restriction in regard to supply of artificial hearing aids to any one of the family members on one time basis. Existing Provision Testing of vision, treatment of eye-diseases and full dental-care

will be provided free of cost. Provision of goggles, etc. is not within the

purview of the Scheme. Artificial hearing-aids will be made available to

the employee or any one of his family members on a one-time basis, on

the recommendations of ENT specialist of BARC Hospital and on the

basis of audiogram given to him/her, identifying the degree and nature of

deafness. Payment will be made directly to the manufacturer identified

by BARC Hospital. Reimbursement can be made only if the referral note

is counter-signed by the ENT specialist of BARC Hospital and duly

approved by the Head, Medical Division, BARC.

Recommendation The Committee felt that restricting supply of artificial hearing aids

to any one of the dependent family members or the employees may

9

operate harshly on the beneficiaries and it would be reasonable to extend

the facility to all the family members and the employees as may be

needed from medical view point. However, the Committee decided to fix

periodicity and ceiling limit on the amount reimbursable in respect of the

same. Director, BARC may decide the periodicity and ceiling limit in

this regard in consultation with Head, Medical Division.

Point 5. Shifting of prime beneficiary membership to the employed spouse in the event of the employee taking voluntary retirement with the liability of paying enhanced contribution.

Existing provision (letter no.7/14/98-CHSS/IR&W/317 dated November 12, 2002)

When the spouse who is the prime beneficiary by virtue of drawing

higher pay retires from service on superannuation, the option to become

the prime beneficiary may be allowed either to the retiring employee or to

the spouse who is in service even if the pay of the latter is lower. When

the retiring employee becomes prime beneficiary the option to pay one

time contribution for life long registration will also be available to him /

her.

Recommendation

The Committee noted that the facility of shifting of prime

beneficiary membership to the employed spouse exists only in the case of

superannuation and that no specific provision exists in the event of an

employee taking voluntary retirement with the liability to pay enhanced

contribution, i.e. before completion of 30 years of service. The husband

and wife team being an integral unit within the definition of family for

any benefits, the Committee felt that if either of them quits service

whether by way of resignation, superannuation or voluntary retirement,

the event should be treated on the same footing. The Committee noted

10

that even where one of the spouses is employed in the private sector, the

entire family is eligible to CHSS cover without any extra contribution.

The recommendation, therefore, is that the facility of change over of the

prime beneficiary membership to the employed spouse should be

extended without extra liability even if the concerned employee resigns or

takes voluntary retirement before completion of 30 years of service.

Point 6. Reviewing the provisions relating to registration of parents.

Existing Provision (Clause 4.1 (b)

Parents of the prime beneficiary who are wholly dependent on the

prime beneficiary and normally residing with the prime beneficiary and

further provided the monthly income of both the parents from all sources

does not exceed Rs.4000/-

Recommendation

It was observed that in a large number of cases parents who are

staying with the Scientific Officers/Engineers working in remote places

are presently not being covered under the Scheme since their income has

just crossed the prescribed limit of Rs.4,000/- p.m. This results in

hardship to the officers adversely affecting their performance. Further,

exclusion of dependent parents from such a vital facility also contributes

to the reluctance of the officers in moving to the remotely located units

where they are posted. In the circumstances, it was felt that not only there

is no necessity to change the present provision in regard to registration of

parents on the basis of income limit but it was also decided that the

ceiling limit of Rs.4000/- p.m. could be relaxed in respect of the cases as

indicated above for extension of the treatment to the parents. However,

the parents so included would be entitled to get treatment only from the

dispensaries/departmental hospitals and not from the referral hospitals.

11

Further, the facility would cease to exist when the concerned employees

are transferred from the remote locations.

Point 7. Registration after retirement within a time gap.

Existing provision

Retired employees of the Department who opt for the benefits of

the Scheme and members of their families as defined under the Scheme,

subject to the following conditions:

(i) Employees should have put in a minimum of five years service in

the Department before his/her retirement.

(ii) Employees should pay the contribution in advance for a minimum

period of one calendar year and the contribution shall be with

reference to the pay drawn by him/her prior to

retirement/invalidation. Employees may also have an option to pay

one time contribution for ten years to be eligible for life long

registration. The option to join the Scheme any time after the

retirement will be available to the employees subject to the

payment of one time contribution for life long registration as

indicated or arrears of contribution from the date of retirement.

Recommendation

The Committee recommends that an option should be given to the

retiring employees to be exercised within one month from the date of

retirement whether to continue in the medical facility or otherwise. The

option once exercised shall be final and would not be reviewed. For

those who have already retired, the existing practice of allowing them

upto 3 years to come to the CHSS fold can continue.

12

Point 8. Specifying terms and conditions for extending the CHSS facility to NPCIL and aided institutions including adjustment of expenditure.

Existing provision (Clause 2.1.16)

The scheme can be extended to the employees of such

organizations under the administrative control/responsibility of the DAE

at its discretion on such terms and conditions as may be prescribed.

Recommendation

The Committee noted that CHSS facility to employees of NPCIL

and aided institutions has been extended under the above provision and is

governed by specific instructions and as such no re-look at the same is

necessary. However, the Committee noted that the percentage of

overhead charges as being included presently in the per capita

expenditure is totally inadequate and as such the same needs to be

revised. The Committee felt that a common formula can be worked out

for calculating the per-capita expenditure to bring uniformity. There

should not be any “hidden subsidy” provided by Government, while

extending the facility to NPCIL and aided institutions. It was also

decided that the system of making payment of per capita expenditure

could be changed so as to make the same on quarterly basis instead of

yearly basis as is the practice being followed now.

13

Point 9. Specifying the places covered under CHSS in Mumbai so as to ensure inclusion of those who are staying outside the limit of the Brihan Mumbai/Navi Mumbai and also giving second option to those opted out of the Scheme in the past;

& Point 10. Providing 2

nd option to those opted out of the Scheme

earlier under changed circumstances like opening of new dispensaries, etc. Existing provision Employees of the Department of Atomic Energy who are staying

outside the limits of Brihan Mumbai and who have been exempted once

from the Scheme shall not be re-admitted to the scheme unless they shift

their residence to Brihan Mumbai. Similarly, an employee, who has been

a resident in Brihan Mumbai but shifts his/her residence outside the limits

of Brihan Mumbai may opt out of the Scheme consequent upon which

he/she will cease to be a member of the scheme with effect from the date

of receipt of such intimation by the Medical Division, BARC.

Contribution towards the Scheme will not be recoverable from him from

the succeeding month. A new entrant to the service of the Department

with Headquarters at Mumbai who stays outside Brihan Mumbai will be

given choice to opt out of the Scheme. The option once exercised shall

be final and he/she will not be allowed to rejoin the scheme unless he/she

shifts his residence to Brihan Mumbai.

Recommendation As per the above provision while membership is compulsory for

those who are staying within the Brihan Mumbai/Navi Mumbai, for those

staying outside, there is an option for availing the facility which is final

once exercised. However, it was noted that an opportunity was given in

the year 1995 to come within the fold of the Scheme on the basis of the

14

request of those who had opted out in the past and remained outside the

Scheme. Now, that with the setting up of dispensaries in places like

Dombivili, etc. a number of persons are interested to become members.

The Committee felt that it would be appropriate to give one more option

to come under the Scheme to these persons in the changed circumstances.

Point 11. Reviewing eligibility of beneficiaries for different classes of accommodation in referral hospitals.

Class of accommodation

Existing Provision

Sl.No. Category Classification of staff according to pay range

Type of accommodation

1 A Rs.4590/- or below General Ward 2 B More than Rs.4590/- but below

Rs.8000/- Room with four

beds 3 C Rs.8000/- to Rs.11500/- Room with two

beds 4 D Rs.11501/- and above Semi Private

Ward

Recommendation

After a detailed discussion on the issue of reviewing the eligibility

in the wake of increase in subscription on account of merger of DP with

basic pay, the Committee recommended that revised eligibility criteria

would be as under:

Sl.No. Category Classification of staff according to pay range

Type of accommodation

1 A Rs.6885/- or below General Ward 2 B More than Rs.6885/- but

below Rs.12000/- Room with four

beds 3 C Rs.12000/- to Rs.17250/- Room with two

beds 4 D Rs.17251/- and above Semi Private Ward

15

Point 12. Expanding the liberalized emergency scheme and reviewing the ceiling limit for confinement and maternity benefits including revising the flat rates, and also treatment for infertility etc.

Existing provision (Clause 15.5)

The reimbursable amount for outdoor and domicile treatment shall

be restricted to Rs.1500/- and for in patient treatment the reimbursable

amount shall be the actual restricted to Rs.5000/-. However, in deserving

cases, Director, BARC may authorize reimbursement of charges over and

above those indicated above.

Recommendation

It was noticed that the suggestions received from the Units favour

an increase in the ceiling for reimbursement as fixed above. The

Committee, therefore, felt that an upward revision in respect of the

reimbursable charges from the existing rates as indicated below which

were fixed in the year 1998 would be reasonable:-

Existing Proposed Outdoor & Domiciliary Rs.1500/- Rs.3000/-

In-patient Rs.5000/- Rs.15000/-

Confinement charges Rs.750/- Rs.2500/-

Since infertility is not considered as a disease, there is no scope for

bringing the same under the ambit of treatment in the Scheme especially

looking at the prohibitive cost involved for the purpose.

16

Point 13. Reviewing the reciprocal arrangements made with Department of Space and making reciprocal arrangements with other Departments.

Existing provision

No provision exists in this regard in the Scheme but arrangement

for the purpose was made separately.

Recommendation

The Committee felt that the existing reciprocal arrangement as

finalized in the year 1995 with the Department of Space is working well.

However, there is no scope for establishing similar arrangement with

other Departments.

Point 14. Provisions regarding extending the facility to transferees/ deputationists/persons on Foreign Service, etc. to and from the Units.

Existing provision (Clauses 2.1.4 (a) & (b)

(a) Employees of the Department temporarily transferred to other

organizations at Mumbai under the administrative control/

responsibility of the Department and members of their families

residing with them provided they pay contribution to the scheme and

are not beneficiaries of any other Health Scheme. Specific orders

will, however, have to be issued by the Department in each case.

(b) Employees of the Department while on deputation or on foreign

service to Government Departments/Undertakings at Mumbai and

members of their families residing with them provided they pay

contribution and are not beneficiaries of any other health scheme.

An option shall be exercised by the Government Servant concerned

17

for availing of the CHSS facilities. Specific orders will, however,

have to be issued by the Department in each case.

Recommendation

The Committee noted that provisions exist in the Scheme to take

care of the needs of such categories of persons as indicated above and as

such there is no need to add anything further specifically in this regard.

Point 15. Extending the CHSS facility to the persons working at Tarapur but staying in Mumbai and vice-versa.

Existing provision

No specific provision exists in this regard in the Scheme.

Recommendation

Since the employees residing in Mumbai and working at Tarapur

and vice versa are covered under the Scheme based on the place of

residence, there is no need for making any specific provision in this

regard.

Point 16. Provision for Ayurvedic and Homeopathy treatment both for serving and retired employees.

Existing Provision

CHSS is concerned with extending treatment under Allopathic

system only. However, treatment under Indian system of medicines viz.

Ayurvedic and Homeopathy are extended to serving employees and their

dependents under CS (MA) Rules 1944. CS(MA) Rules 1944 is not

applicable to retired employees.

Recommendation

The Scheme does not envisage treatment under Ayurvedic and

Homeopathy systems. Hence, no action seems to be necessary.

18

Point 17. Liberalization of the provisions for eye treatment in the matter of replacement of spectacles, dental treatment/artificial dentures and provision for supply of artificial appliances, hearing aids, etc.

Existing provision (Clauses 8.3, 8.4 and 8.5)

Employees whose pay does not exceed Rs.7000/- p.m. and

members of their families will be eligible for reimbursement for purchase

of spectacles from registered opticians upto Rs.100/- only. Replacements

shall be at the cost of the employee concerned.

Recommendation

Since the existing rate of Rs.100/- for the reimbursement of cost of

spectacles was fixed in the year 1998, it is recommended to raise the

ceiling to Rs.300/-. The Committee also recommends an increase in the

existing ceiling of artificial dentures (by 3 times) as indicated below:

Concessional Rates chargeable for Artificial Dentures supplied under the CHSS of the Department of Atomic Energy

----------------------------------------------------------------------------------------------- Sl.No. Type of dentures Upto Between Between Over Rs.4590/- Rs.4591/- Rs.8001/- Rs.11501/- p.m. to to Rs.8000/- Rs.11500/- ----------------------------------------------------------------------------------------------- Rs. Rs. Rs. Rs. 1. Full dentures 300/- 600/- 900/- 1200/- (artificial set of teeth, upper and lower) 2. Full dentures 150 300 600 900 (artificial set of teeth upper) 3. Partial dentures one 30 60 90 120 tooth 4. Partial dentures 15 30 60 90 additional teeth -----------------------------------------------------------------------------------------------

19

Point 18. Listing out the inadmissible treatments, medicines, preparations, food and other auxiliary items.

Recommendation

The Committee felt that it is neither necessary nor practicable to

identify in an exhaustive manner the inadmissible medicines / treatment,

food and other auxiliary items in a health care scheme like CHSS. Not

only that, wherever doubts arises concerning these issues, the relevant

provisions of CS(MA) Rules could be invoked.

Point 19. Specifying the delegation of powers including payment to referral hospitals.

Recommendation

The Committee noted that adequate powers have been delegated to

the administering authorities or at lower levels in this regard and this

system is working satisfactorily.

Point 20. Deleting provisions relating to discretionary relaxations and making them more specific.

Recommendation

The CHSS being a medi-care system to take care of a large number

of beneficiaries, certain relaxations should be essential in a discretionary

way either in the matter of treatment or implementation of various

provisions as may be necessary so as to make the same flexible. Such

discretions are exercised with due caution by the concerned authorities as

demanded by circumstances and necessity so as to ensure proper care and

20

benefits to the concerned. The Committee, therefore, felt that no change

in the provisions in the Scheme in this regard is necessary.

Point 21. Reviewing the provision for registration of family members on the death of the employee.

Existing Provision

The spouse of a deceased employee and other family members of

the deceased employee registered under the CHS Scheme may continue

to avail of the benefits, provided the deceased employee had completed a

minimum of one year’s service in the Department and the spouse pays the

contribution last paid by the deceased employee and provided further, the

spouse and other members of the family are otherwise eligible for the

continued registration under the scheme. The scale of pay of the post last

held by the employee will be the basis for determining the entitlement.

Recommendation

The Committee noted that the existing provisions are adequate to

take care of the family of a deceased employee. However, it was felt that

the facility of lifelong membership as in the case of retired employees can

be extended to the family as a matter of option.

Point 23. Provision of periodical increase in contribution.

Existing provision (Clause 13.2)

For the medical service provided under the scheme a monthly

contribution shall be recovered. Contribution will be recoverable at the

following rates:

(a) member of AEC and their family Rs.260/-

(b) visiting Scientists / Fellows / Professors Rs.260/- and their family

21

(c) Employees and their family 1% of the basic pay + DP (d) All trainees 1% of stipend/ scholarship/fellowship

Recommendation

The Committee noted that presently contribution towards the

scheme is recovered at the rate of 1% of Pay + DP. The contribution

received is automatically increased on account of the accrual of increment

every year and subsequently on promotion to higher grades.

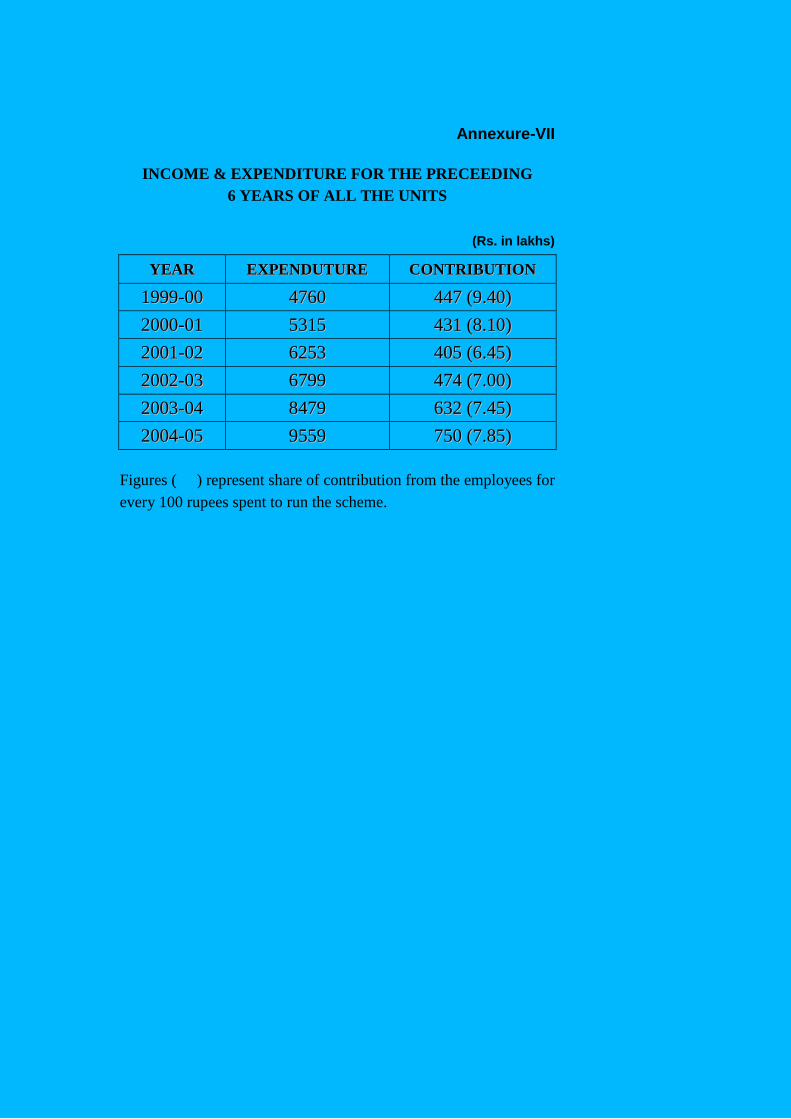

The Committee noted the income and expenditure under the

scheme for the last six years and carefully perused the Statistics presented

in Annexures VII, VIII, IX and X. It is clear that the annual expenditure

under the scheme is rising rather steeply. The expenditure has doubled in

the last five years, indicating an average 14% annual rate of growth in

expenditure. 92 to 93 percent of the expenditure is borne by the

Government Budget, while the contribution from the employees is only 7

to 8 percent.

The Committee noted that the increased expenditure is because of a

variety of factors, notable amongst them being

- The increasing age – profile of the beneficiaries.

- The ever growing new medical-treatment technologies and

medical diagnostic technologies

- Increased number of referrals.

While the Committee is in favour of continuous improvement in

the Health care facilities provided to employees, a question which

cropped up again and again was “whether the present system of

22

contribution leads to cost-effective health care? or can better systems be

though of ? ”

One thing was quite clear to the Committee “who pays for medical

care”, does influence both the quality of medical care and its cost-

effectiveness. Often a given medical problem can be treated in more than

one way. Choices among these depend not only on how serious the

problem is, but also on “who picks up the bill.” When CHSS

(Government) picks up the bill, the more expensive treatment becomes

more likely, than when the individual pays. Comprehensive health care

coverage – like the CHSS – reduces the price that people pay for routine

health care. The law of demand states that this will increase people’s use

of it.

When patients pay for their own medical treatments, they are more

apt to establish priorities, so that someone with a fractured leg is far more

likely to go to a doctor, than someone with a minor headache. But, when

both are treated free of charge to the patient, these people with minor

ailments may take up as much of doctor’s time and medical resources that

those with more serious medical conditions must be forced to wait. The

Anushakti Nagar dispensaries and the BARC Hospital is a case in point.

The everyday familiar scene is a crowd of retired employees and their

dependants (many with minor ailments), crowding out the more urgent

cases which require greater time of the Doctors.

Yet another issue discussed by the Committee was the issue of

“Moral Hazard” with reference to CHSS, “Moral Hazard” means that if

beneficiaries believe that major expenses are covered under CHSS, they

have less incentive to go in for preventive health. In order to mitigate,

moral hazard, CHSS could make it mandatory for beneficiaries to have

23

annual medical check-ups and perhaps link contribution to the medical

SHAPE of individual employees.

Keeping all the above considerations in mind, the Committee felt

that besides a certain mandatory contribution from all employees, a

mixture of Government payment and private payment by the patient may

mitigate to some extent the “Free Rider Problem” and the “Moral Hazard

Problem” inherent in the operation of scheme like the CHSS.

Beneficiaries can be charged some extra amount in the case of the

employees/families who make frequent visits to the dispensary/hospital.

This would not only reduce the crowd but also curb the tendency of

unnecessarily taking advantage of the facility. The Committee also felt

that a certain percentage of expenditure incurred towards treatment at

referral hospital in respect of dependent relatives/ parents beyond certain

age could be worked out and recovered from the prime beneficiary. The

exact extra amounts and percentage to be paid needs to be worked out.

Once such a system is worked out, and an estimate of the extra

income that will accrue to the CHSS is computed, one can consider

reducing the mandatory contribution from the present rate of 1% to a

suitable figure (say 0.75 percent or so), so that the net kitty of

contribution to CHSS remains at the same level as it exists at present.

After trying this out for a couple of years, one will get data to establish

whether the proposed changes have significantly contributed to increasing

cost-effectivenss of CHSS. Thereafter the question of making further

changes in the contribution can be re-examined.

24

Point 24. Reducing the gap between subscription and expenditure &

Point 25. Checks to avert misuse of the facilities under CHS Scheme.

Recommendation

It was generally seen that under the Scheme in Mumbai, referrals

are being made to various hospitals costing about Rs.20 crores per annum

on an average but at the same time this does not fetch a commensurate

discount. It came to the notice of the Committee that one of the reasons

for the reluctance on the part of the hospitals to allow discount at the

expected level is because of the delay in settling the bills. It also came to

the notice that as per the existing procedure the bills when received from

the concerned hospitals in CHSS office have to essentially move to

various authorities before it finally reaches Accounts for making

payment. The bills are usually sent by hospitals in a consolidated way

for treatment in respect of a set of patients for different ailments and on

receipt, the same are first distributed among the concerned Medical

Officers for certification and thereafter submitted for approval to the

Head, Medical Division or Director, Bio-Medical Group or Director,

BARC according to the value. The bills as approved are then received

back in the BARC Hospital and from there sent to Accounts Division for

scrutiny and payment with the approval of the appropriate authority.

Quite often there is an upward revision in the charges in respect of certain

facilities or services in some of the hospitals and unless the new charges

are approved by the appropriate authority such bills will have to be kept

pending. This apart, duplication or inaccuracy of charges are also

common and these are to be checked and rectified before payment. After

going through the above process sometimes it takes 3 to 9 months before

the cheque is actually released. Since timely payment is the essence of

any such dealings and it is vital to ensure that the bills are promptly

25

settled so as to sustain the demand for appropriate discount from the

hospitals, BARC would be undertaking an in-depth study of the problems

involved in a holistic way and suggest ways and means to cut down the

undue delay in the matter of release of payment. Entering into an MOU

with the hospitals would be one of the measures to avoid unexpected

increase in the charges. Similarly, the Committee felt that the areas

where higher rate of discount would be feasible could be identified while

procuring medicines and other items, by way of directly procuring the

items from the manufacturers consolidating orders for commonly stocked

medicines etc. The Committee observed that although the BARC

Hospital is set up with multi-disciplinary medical facilities, lack of

trained doctors in certain core fields like Cardiology, Nephrology, Gastro,

etc. is a major handicap in affording proper treatment with the result that

the patients are required to be referred to hospitals of specialization. If a

cadre of trained Medical Officers in the essential fields as indicated above

is built up with a scaled-up in-house infrastructure as existing in Army or

Railway Hospitals, outside referrals could be considerably reduced

bringing about a substantial saving in the expenditure. Similarly

outsourcing the services of doctors at the Dispensary level is also one of

the measures for effecting economy in expenditure.

Another reason for the very high expenditure on referrals is the

cost of “defensive medicine” – namely asking a patient to undergo a large

number of unnecessary diagnostic tests only to “rule out such and such

possibility”. This practice has perhaps entered the medical profession in

India from the American practice (where the threat of lawsuits forces

doctors to take up costly ‘malpractice insurance’). To keep some kind of

check on the referral hospitals, BARC Medical Division, should institute

a annual review of “total payments” made to various hospitals every year

and replace one or two hospitals based on some well thought out

26

parameters (from which it can be concluded that a particular hospital was

not relatively speaking cost-effective). Such a practice will hopefully

“send a message” to the hospitals that no hospital can take the “BARC

Account” for granted.

Point 26. Conversion of CHSS as an autonomous body.

Recommendation

It is felt that this is not a practicable proposition.

Point 27. Checks & Balances

It has been noticed that the number of AMAs appointed under the

scheme wherever Department Hospitals/Dispensaries are not available

appears to be on higher side. It is seen from a report submitted by a

Committee that in some cases the average visit of the patients to each

AMAs are very low in general and in certain cases it is as low as two in a

year. The retention of large number of AMAs is not justifiable and

should be drastically pruned in a phased manner. Presently, AMAs are

paid retainer fee @ Rs.400/- p.m (only at Hyderabad). The annual

expenditure incurred on account of fees to these AMAs is around Rs.4.25

lakhs in one of the centres. Once the number of AMAs is reduced, the

expenditure will also stand reduced to that extent.

As per the existing practice in Hyderabad, a beneficiary can

directly approach either an AMA or Zonal Hospital with the CHSS card

without any referral letter from the Medical Officer of the concerned

DAE unit and can avail inpatient facilities from the approved hospital

under the scheme. Further, the beneficiary can also avail medical

treatment for the same disease from different hospitals located in the

27

same locality according to his choice. This is possible because there is no

mechanism to check the treatment being availed from multiple hospitals.

It is necessary to introduce some mechanism which will show the details

of the medical treatment availed by the individual when he approaches

different hospitals for various treatments. It is also noticed that

sometimes more than 3 – 4 zonal hospitals are approved in the same

location. It is possible that the number of approved zonal hospitals in

such localities can be reduced. It is understood that charges towards

supply of medicines from the medical shops of the zonal hospitals and

referral hospitals are at MRP. There is ample scope for availing discount

from the medical shops if negotiations are made with them.

Point 28. Any other points - Exploring the possibility for introduction

of Health Insurance Scheme.

The Committee had an indepth discussion on the possibility of

introducing health insurance scheme in order to ensure long term

sustainability of the current subscription based CHSS and possibility of

its replacement with medical insurance scheme. The suggestions in

regard to introduction of the Insurance Scheme would need a careful

assessment of such schemes and the experience of others to ascertain that

the character and benefits provided under CHSS are not altered. The

aim should be to improve the quality of medical services provided under

CHSS. In fact the scheme should be one of the attractions (perks) to

young scientists/engineers to join the department. While achieving this

aim, there should be innovative checks and balances to curb leakages in

the Scheme, to prevent abuses/misuse of the Scheme and to make the

scheme cost-effective.

28

Hence, the committee recommended that for the time being the

present CHS Scheme should continue with the modifications

recommended.

The Committee also felt that the report should contain its

recommendations on following points:

1. Existing infrastructure facilities in the Departmental Hospitals/ dispensaries.

2. Decentralisation of some of the services at dispensary level. 3. Preventive health care programme. 4. Health Promotion scheme. 5. Health Economics.

The BARC Hospital was constructed and commissioned in the

mid-70’s. The capacity of the Hospital was planned to take care of about

30000 beneficiaries under the Contributory Health Services Scheme. The

number of beneficiaries have increased substantially and at present stands

around 80000. Though some minor expansions had been undertaken

some time back, the infrastructure available is insufficient to take care of

the present load on the system.

With the advances in medical field, a large number of innovative

therapeutic procedure diagnostic techniques, modern drugs and their

delivery systems and advanced monitoring & critical-care equipment

have become available to the doctors in the management of various

diseases. These advancements in the present day concept of holistic

Medicare have permitted the doctors to alter the course of the disease

process, halt its progress or cure the disease, thus improving the quality of

life.

29

The increase in the number of beneficiaries, the rise in the average

age, the development of modern methods, both in diagnosis and treatment

have all resulted in heavy pressure on the present infrastructure.

It is therefore necessary to provide additional facilities to the

existing infrastructure in the form of new technology in the medical field,

latest machinery and equipments, manpower, additional buildings etc in

the XI th Plan in order to keep pace with the changing trend and

methodology in the field of medicine and also to take care of the

increasing load on the long waiting list for appointments for various

Outdoor Patient Departments.

Decentralization : It is necessary to decentralize the health care

arrangements to the maximum extent feasible. It should be possible to

have poly clinic type of arrangement at least in some of the major

dispensaries, say one in western suburbs, another in the central suburbs

and one in the Navi Mumbai area, where the dispensaries should also

have facilities for pathology, dental, X-ray, etc. This will reduce the

number of patients referred to the Hospital at Anushaktinagar for availing

these services. It may also be possible to outsource the service like

pathology, X-ray etc. Once a dental chair is provided in a dispensary it

may be possible to enlist the services of part time private consultants in

dental care.

Health Promotion Scheme : Due to increase in colony population and

lack of understanding in basic public hygiene and sanitation, there

remains a constant threat of an epidemic out break. Maintaining the

hygiene and sanitation of the DAE colonies play very important role in

health promotion scheme sponsored by the Department. Medical

Division extends the logistic and reporting attributes to this agency.

30

Hospital and dispensaries also inform about the notifiable diseases to

BMC and in return receive vaccines and advices. To target and promote

good health it will be wise to promote health education among school

going children and young mothers. It is not an expensive idea to provide

professionally managed gymnasia, yoga centers, health clubs and

swimming pools in the colony which would promote positive health. In

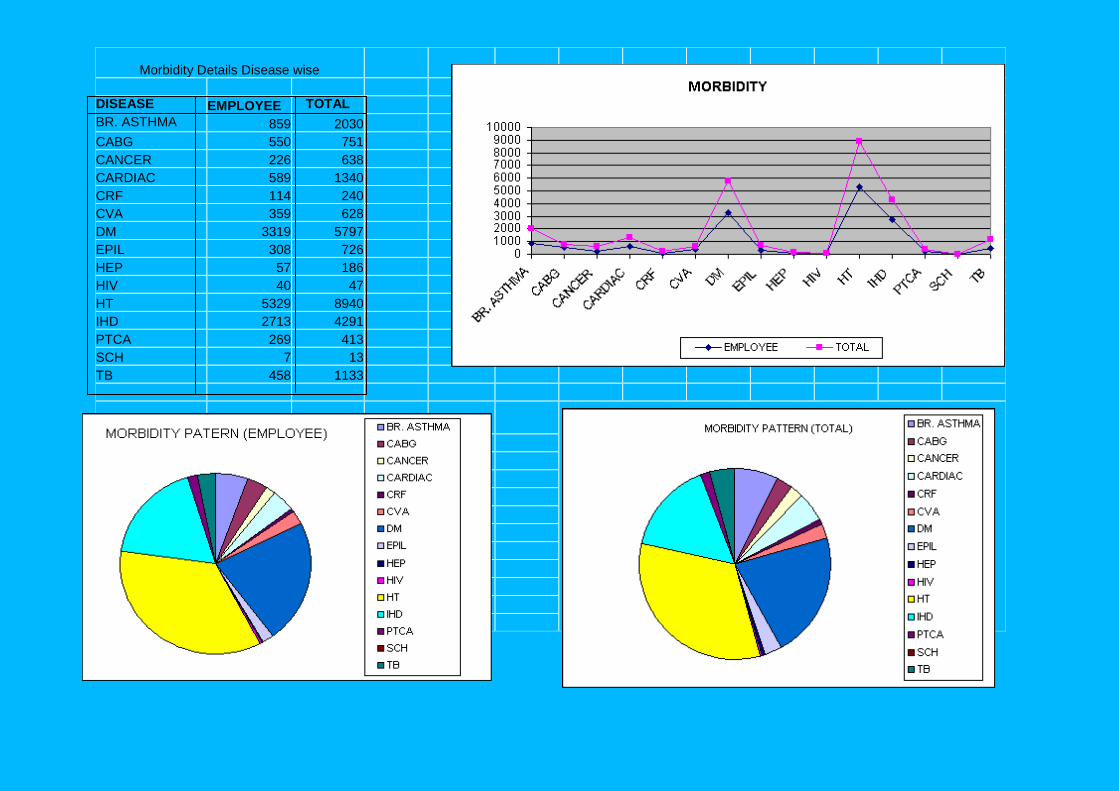

this context statement on morbidity details prepared by Head Medical

Division is very informative and useful. It gives an idea about disease

pattern prevailing in the departmental housing colony in Anushaktinagar.

Health Economics and Auditing : Different health care systems world

over use their resources in many different ways. Some systems are

hospital orientated i.e. highly technology dependent while others give

more emphasis on preventive aspects of the medicine i.e. community

orientated. Auditing makes us aware of the direction of the main focus of

our health expenditure, i.e. whether the major chunk of our budget goes

to cater too few patients suffering from chronic ailments of liver, kidney,

brain or congenital/genetic defects requiring long term medical coverage

or whether the focus is on common seasonal/preventable/lifestyle

diseases like malaria, tuberculosis, gastroenteritis, conjunctivitis, dengue,

chikangunia, diabetes, alcoholism, smoking and hypertension. A periodic

evaluation of the expenditure on both preventive and curative health and

questioning its cost-effectiveness should get institutionalized as one of

the functions of the Medical Division of BARC.

* * *

Annexure-I

UNIT-WISE CHSS REGISTRATIONS AS ON 1st OCTOBER, 2006

Unit Prime Spouses Children Parents Dependents Total

AEES 396 246 438 74 - 1154

AERB 163 118 150 41 - 472

BARC 12063 8942 14057 3473 21 38556

BRIT 426 348 590 135 1 1500

CISF 262 35 42 - - 339

DAE 334 247 437 101 - 1119

DCS&EM 1008 866 1640 316 - 3830

DPS 641 423 795 177 - 2036

HWB 254 193 333 56 - 836

IRE 3 3 4 1 - 11

ISRO 36 25 34 8 - 103

NFC 6 5 7 3 - 21

NPCIL 1884 1454 2251 555 4 6148

RAPS 2 1 1 1 - 5

TIFR 1484 968 1384 443 1 4280

TMC 1557 856 1548 184 - 4145

Total 20519 14730 23711 5568 27 64555

RETIRED POPULATION

Retired 6444 5670 1069 304 - 13487

V. Retired 747 598 214 51 - 1610

Late Employee 1334 - 372 36 - 1742

Total 8525 6268 1655 391 0 16839

Grand Total 29044 20998 25366 5959 27 81394

Annexure-II

CHSS REGISTRATION AS ON

1st OCTOBER, 2006 IN MUMBAI

PRIME 29044

SPOUSES 20998

CHILDREN 25366

PARENTS 5959

DEPENDENTS 27

TOTAL 81394

Annexure-III

CHSS BENEFICIARIES AS ON 01.11.2005 - MUMBAI

Age Group Exployees - Age-wise

00 –– 1177 1188003366 UUppttoo 3355 66667766

1188--2255 1100778888 3366--4455 55776633

2266--3355 1100007744 4466--5555 55006699

3366--4455 1111229933 5566--6600 22776655

4466--5555 99996633

5566--6655 1100332266 Total

6666--7755 66770066

AAbboovvee 7755 33000033 EEmmppllooyyeeeess 2288447766

SSppoouusseess 2200667722

CChhiillddrreenn 2255114455

PPaarreennttss 55887711

DDeeppeennddeennttss 2266

Annexure-IV

CHSS REGISTRATION AS ON 01.12.2005 – MUMBAI

Disp. No. Disp. Name Prime Spouses Children Parents Deps. Total

1 * OYC 597 370 404 54 1 1426

2 * A. Bhavan 795 524 500 186 0 2005

3&5 * Mistry Ngr. 1506 908 1013 366 1 3794

4 •Bandra 649 436 333 115 1 1534

6 Chembur 2069 1442 1361 353 0 5225

7 •Ghatkopar 3270 2183 2594 763 2 8812

8 Deonar (W) 4920 3968 6003 1145 6 16042

9 Deonar (E) 4119 2809 3497 706 8 11139

10 Vashi 3712 2818 2494 607 4 9635

11 Andheri 2554 1779 1683 496 0 6512

12 Mandala 3088 2592 4239 880 3 10802

14 •Dombivili 1275 985 1135 279 0 3674

TOTAL 28554 20814 25256 5950 26 80600

* Dispensaries working in "Single Shift"

Annexure-V

CHSS BENEFICIARIES - 2004-05

Unit No. of Beneficiaries No. of Beneficiares Total

Retired Dependents Serving Dependents

BARC (M) 8023 9853 19696 45304 82876

GSO-K 798 1124 6484 18133 26539

VECCQ 135 232 634 1668 2669

RMP 23 31 778 2188 3020

NFC 320 467 4452 13707 18946

HWP(B) 113 125 522 1353 2113

CAT 44 67 1337 3974 5422

RAPS-K 584 656 4200 13638 19078

TAPS 336 587 3843 10539 15305

HWP (TH) 2 4 244 722 972

HWP (M) 19 54 1919 7381 9373

HWP (TU) 84 105 477 1434 2100

10481 13305 44586 120041 188413

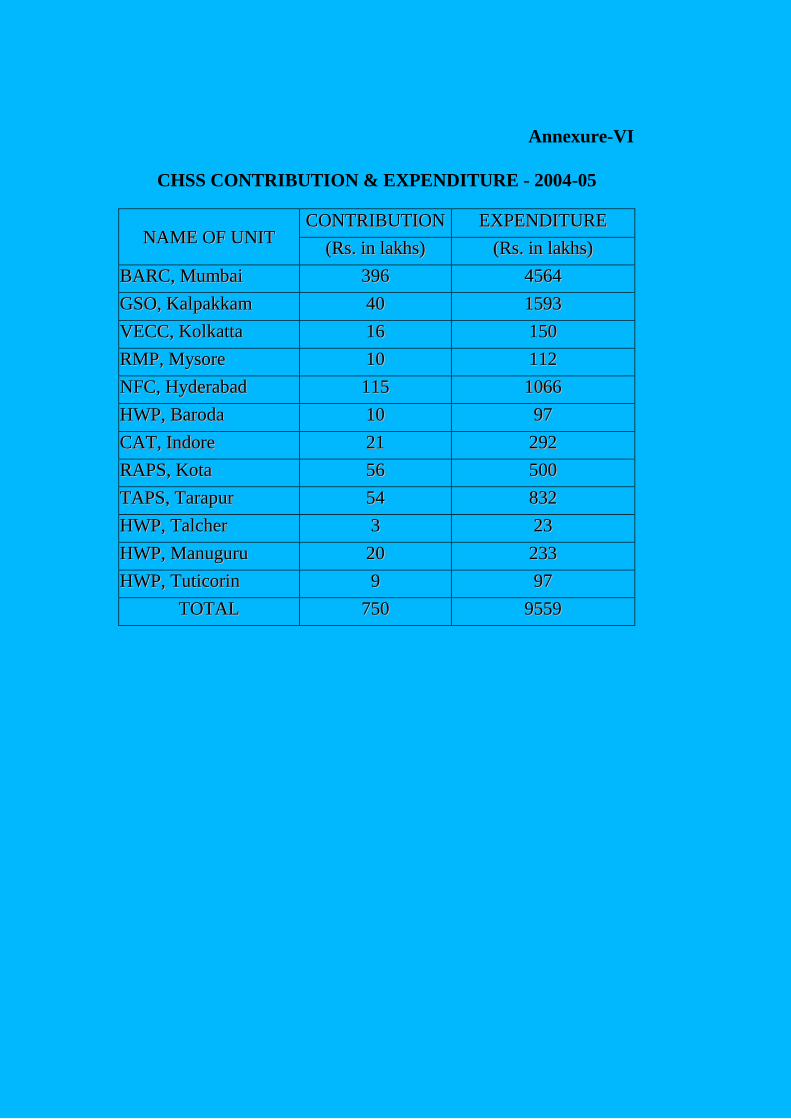

Annexure-VI

CHSS CONTRIBUTION & EXPENDITURE - 2004-05

NNAAMMEE OOFF UUNNIITT CCOONNTTRRIIBBUUTTIIOONN EEXXPPEENNDDIITTUURREE

((RRss.. iinn llaakkhhss)) ((RRss.. iinn llaakkhhss))

BBAARRCC,, MMuummbbaaii 339966 44556644

GGSSOO,, KKaallppaakkkkaamm 4400 11559933

VVEECCCC,, KKoollkkaattttaa 1166 115500

RRMMPP,, MMyyssoorree 1100 111122

NNFFCC,, HHyyddeerraabbaadd 111155 11006666

HHWWPP,, BBaarrooddaa 1100 9977

CCAATT,, IInnddoorree 2211 229922

RRAAPPSS,, KKoottaa 5566 550000

TTAAPPSS,, TTaarraappuurr 5544 883322

HHWWPP,, TTaallcchheerr 33 2233

HHWWPP,, MMaannuugguurruu 2200 223333

HHWWPP,, TTuuttiiccoorriinn 99 9977

TTOOTTAALL 775500 99555599

Annexure-VII

INCOME & EXPENDITURE FOR THE PRECEEDING

6 YEARS OF ALL THE UNITS

(Rs. in lakhs)

YYEEAARR EEXXPPEENNDDUUTTUURREE CCOONNTTRRIIBBUUTTIIOONN

11999999--0000 44776600 444477 ((99..4400))

22000000--0011 55331155 443311 ((88..1100))

22000011--0022 66225533 440055 ((66..4455))

22000022--0033 66779999 447744 ((77..0000))

22000033--0044 88447799 663322 ((77..4455))

22000044--0055 99555599 775500 ((77..8855))

Figures ( ) represent share of contribution from the employees for

every 100 rupees spent to run the scheme.

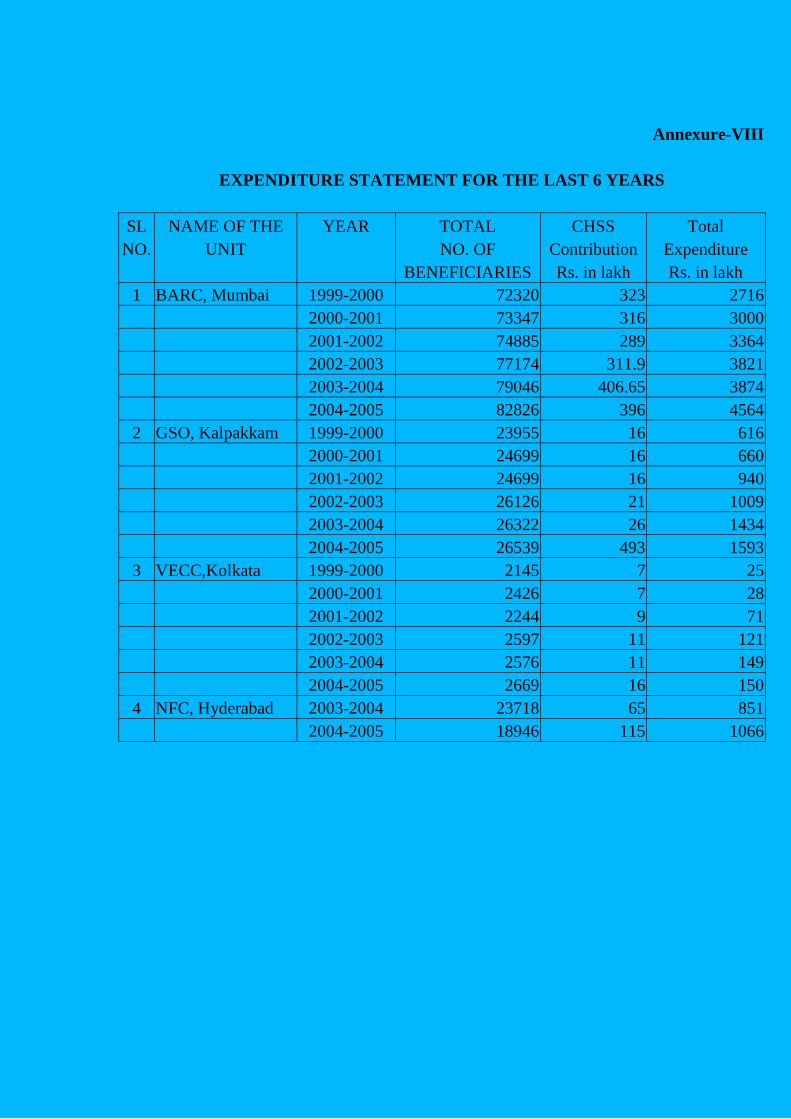

Annexure-VIII

EXPENDITURE STATEMENT FOR THE LAST 6 YEARS

SL NAME OF THE YEAR TOTAL CHSS Total

NO. UNIT NO. OF Contribution Expenditure

BENEFICIARIES Rs. in lakh Rs. in lakh

1 BARC, Mumbai 1999-2000 72320 323 2716

2000-2001 73347 316 3000

2001-2002 74885 289 3364

2002-2003 77174 311.9 3821

2003-2004 79046 406.65 3874

2004-2005 82826 396 4564

2 GSO, Kalpakkam 1999-2000 23955 16 616

2000-2001 24699 16 660

2001-2002 24699 16 940

2002-2003 26126 21 1009

2003-2004 26322 26 1434

2004-2005 26539 493 1593

3 VECC,Kolkata 1999-2000 2145 7 25

2000-2001 2426 7 28

2001-2002 2244 9 71

2002-2003 2597 11 121

2003-2004 2576 11 149

2004-2005 2669 16 150

4 NFC, Hyderabad 2003-2004 23718 65 851

2004-2005 18946 115 1066

Annexure-IX

Statement showing year-wise cases referred

to panel Hospital and Expenditure thereon (CHSS Mumbai)

(Rs. in lakhs)

Year No. of cases Total

2002-03 6226 1082.19

2003-04 6304 1331.81

2004-05 9426 1946.81 @

2005-06 10410 2176.20 @

@ Steep increase due to upward revision of rates by Panel Hospitals

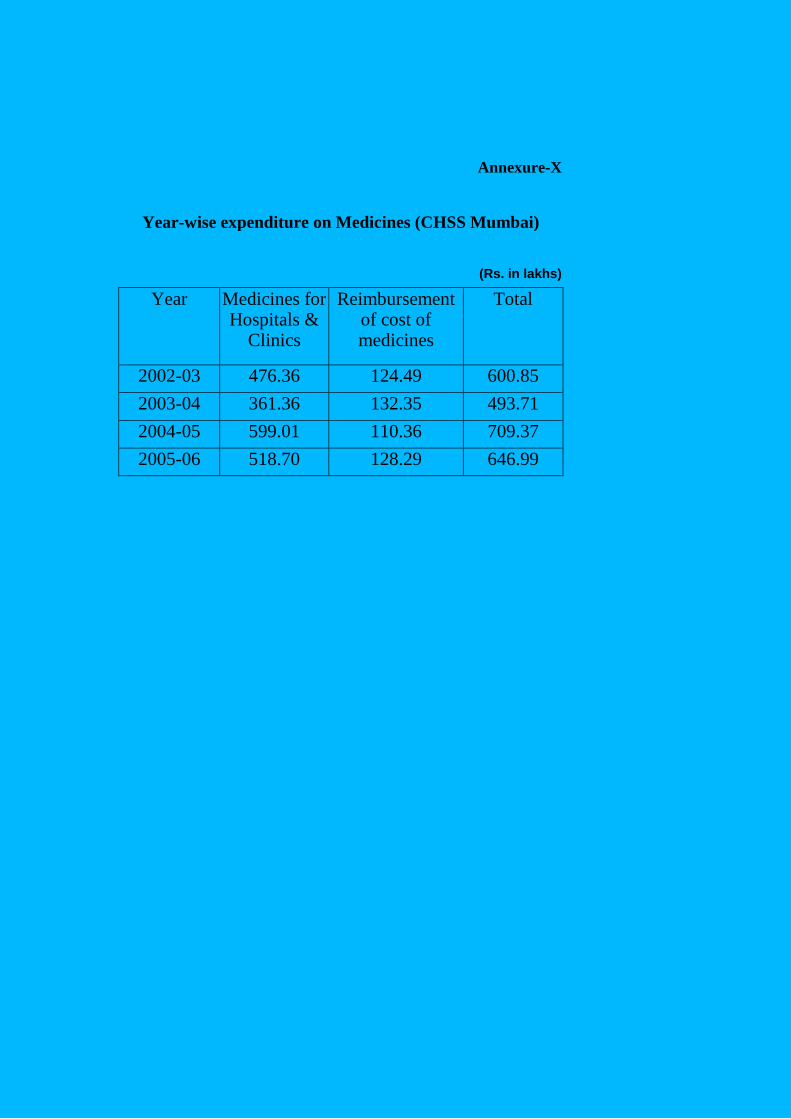

Annexure-X

Year-wise expenditure on Medicines (CHSS Mumbai)

(Rs. in lakhs)

Year Medicines for Hospitals &

Clinics

Reimbursement of cost of medicines

Total

2002-03 476.36 124.49 600.85

2003-04 361.36 132.35 493.71

2004-05 599.01 110.36 709.37

2005-06 518.70 128.29 646.99

Morbidity Details Disease wise

DISEASE EMPLOYEE TOTAL

BR. ASTHMA 859 2030

CABG 550 751

CANCER 226 638

CARDIAC 589 1340

CRF 114 240

CVA 359 628

DM 3319 5797

EPIL 308 726

HEP 57 186

HIV 40 47

HT 5329 8940

IHD 2713 4291

PTCA 269 413

SCH 7 13

TB 458 1133