@chrishartza @investmentsolza africa must try harder november 2014

TRANSCRIPT

@chrishartZA @InvestmentSolZA

AFRICA MUST TRY HARDERNOVEMBER 2014

INVESTMENT DESTINATIONS 2

DEVELOPED MARKETS

AFRICANGROWTH

INVESTMENTEVERGREENS

EMERGING MARKET

LESSONS

AFRICA MUST TRY HARDER

INVESTMENT SOLUTIONS 3

The Developed World: scoring own goals

InvestorObjectives

MacroeconomicManagement

Debt Trap

FinancialRepression

Emulate?Haven?

INVESTMENT SOLUTIONS 4

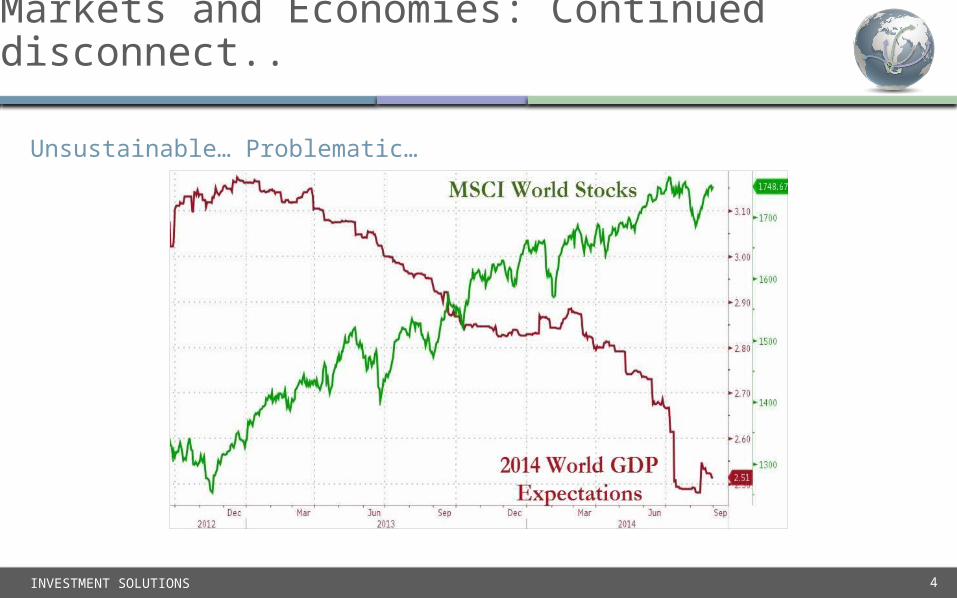

Markets and Economies: Continued disconnect..

Unsustainable… Problematic…

INVESTMENT SOLUTIONS 5

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

Est

im...

0

5

10

15

20

25

30

35

40

45

50

GD

P p

er

ca

pit

a /

10

00

US

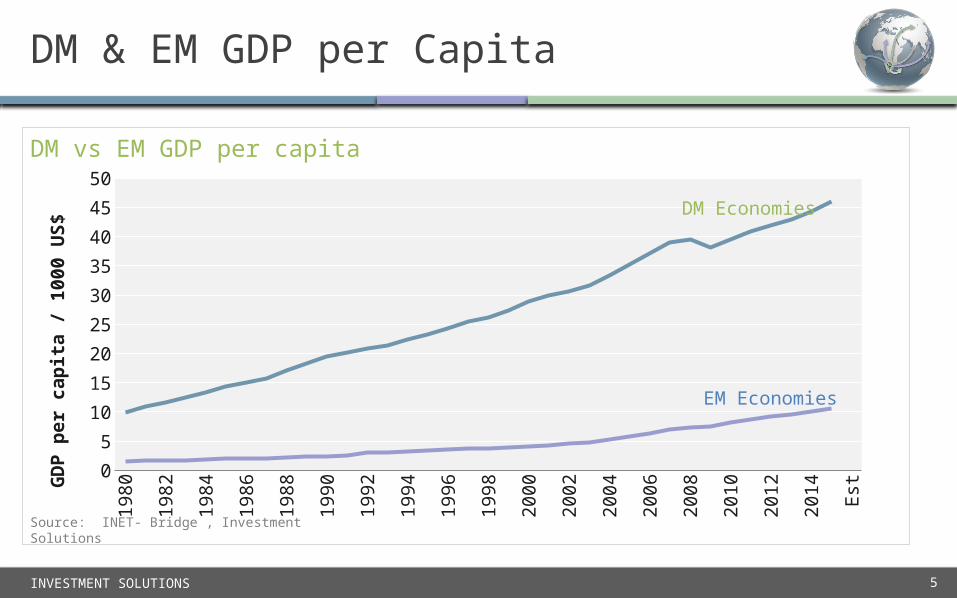

$ DM Economies

EM Economies

DM & EM GDP per Capita

DM vs EM GDP per capita

Source: INET- Bridge , Investment Solutions

INVESTMENT DESTINATIONS 6

DEVELOPED MARKETS

AFRICAN GROWTH

INVESTMENT EVERGREENS

EMERGING MARKET

LESSONS

AFRICA MUST TRY HARDER

7

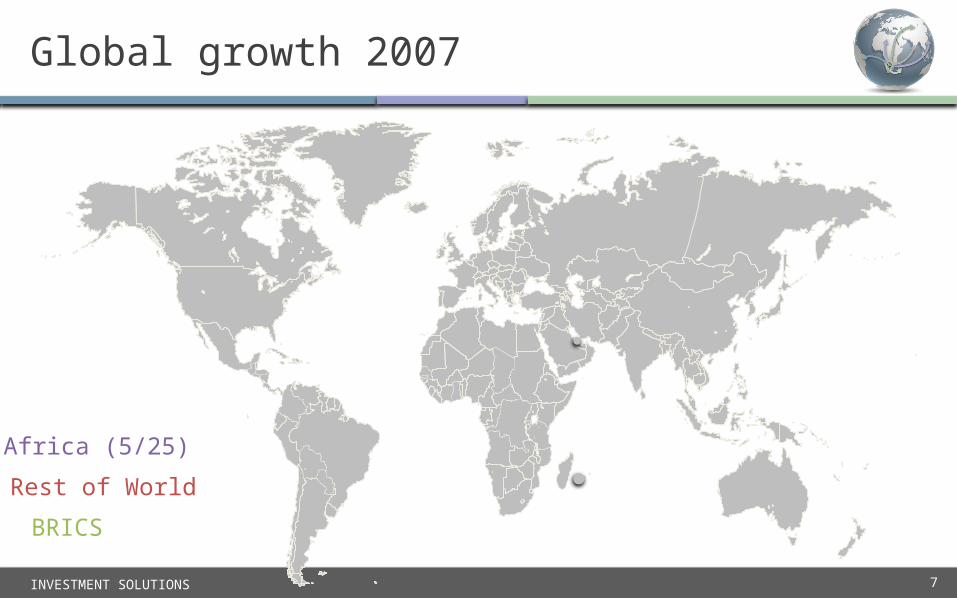

Global growth 2007

INVESTMENT SOLUTIONS

Rest of World

Africa (5/25)

BRICS

INVESTMENT SOLUTIONS 8

Global growth 2015: Africa & Asia

Rest of World

Africa (14/25)

BRICS

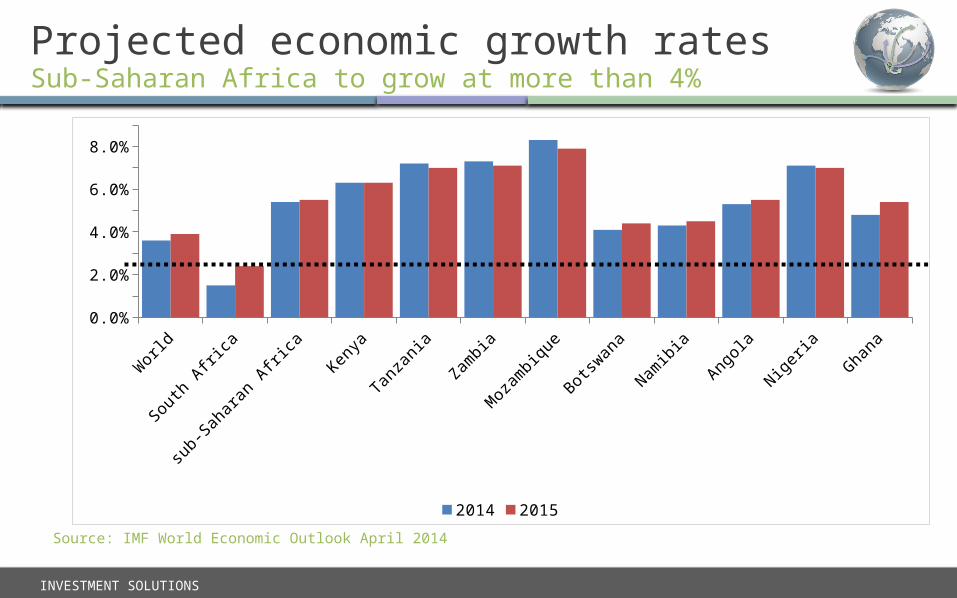

Projected economic growth ratesSub-Saharan Africa to grow at more than 4%

Source: IMF World Economic Outlook April 2014

Wor

ld

South

Afri

ca

sub-

Sahar

an A

frica

Kenya

Tanza

nia

Zambi

a

Moz

ambi

que

Botsw

ana

Namib

ia

Angol

a

Niger

ia

Ghana

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

2014 2015

INVESTMENT SOLUTIONS

INVESTMENT SOLUTIONS

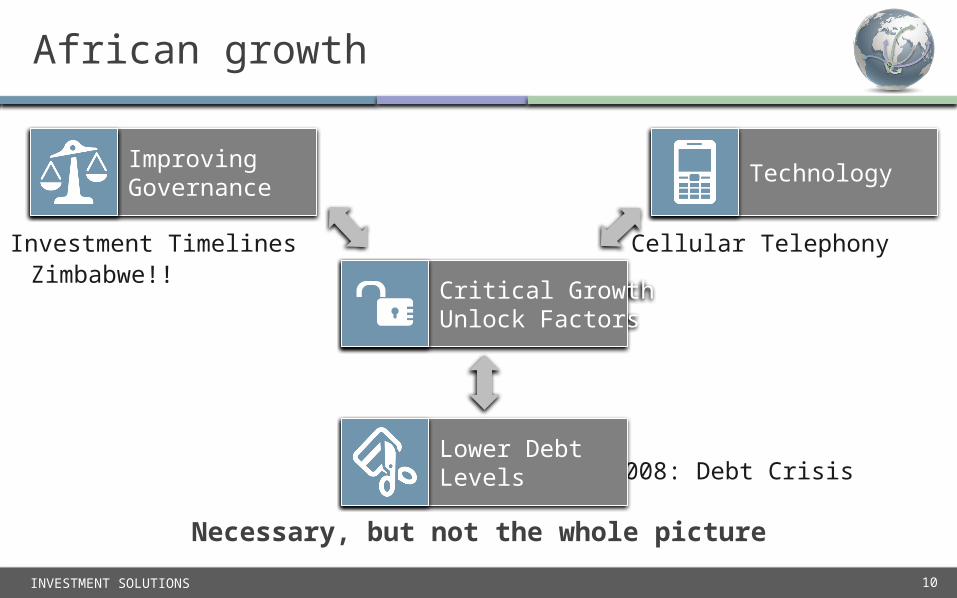

African growth

10

Investment Timelines Cellular Telephony

2008: Debt Crisis

Zimbabwe!!

ImprovingGovernance

Necessary, but not the whole picture

Technology

Critical GrowthUnlock Factors

Lower DebtLevels

INVESTMENT SOLUTIONS 11

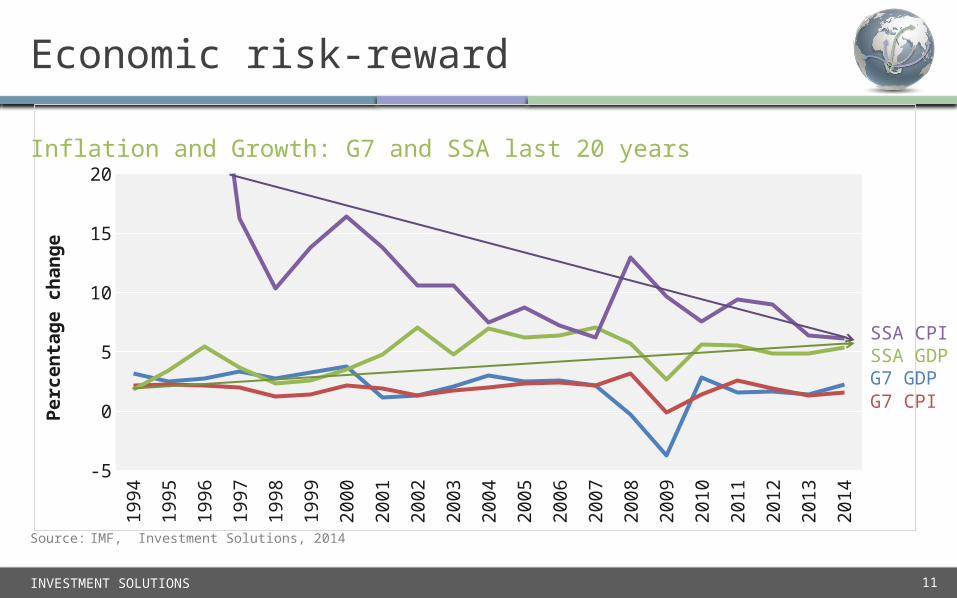

Economic risk-reward

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

-5

0

5

10

15

20

Pe

rce

nta

ge

ch

an

ge

Inflation and Growth: G7 and SSA last 20 years

Source: IMF, Investment Solutions, 2014

G7 GDPG7 CPI

SSA GDPSSA CPI

INVESTMENT SOLUTIONS 12

SSA GDP / Capita

Middle Income Counties

Low Income Countries

2000

`

INVESTMENT SOLUTIONS 13

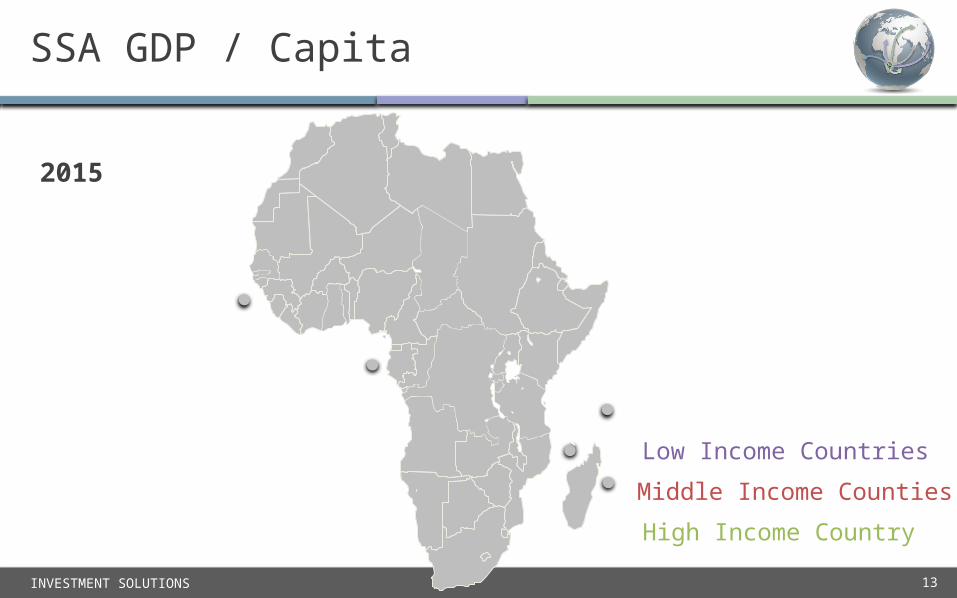

SSA GDP / Capita

2015

`

Middle Income Counties

Low Income Countries

High Income Country

INVESTMENT SOLUTIONS 14

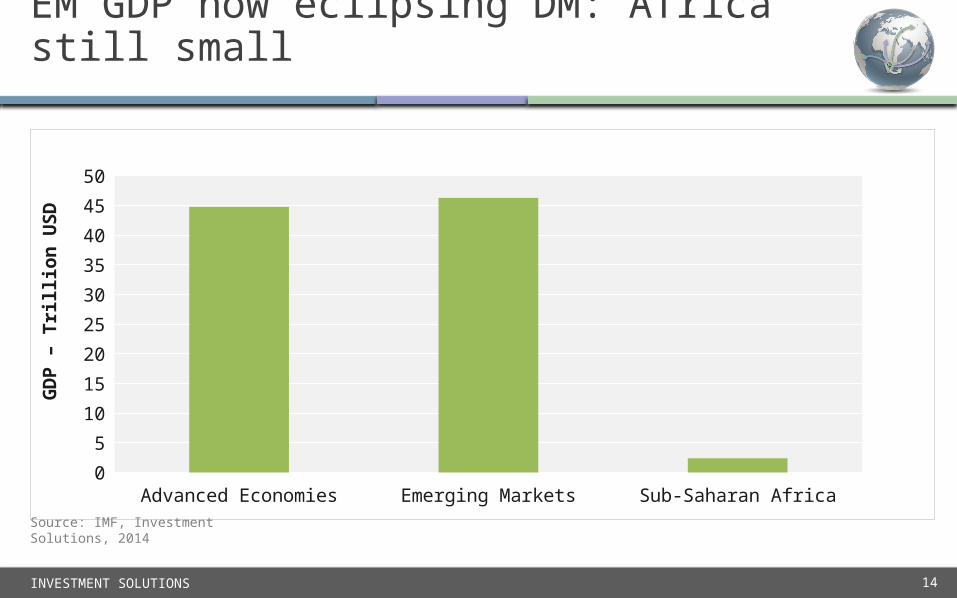

EM GDP now eclipsing DM: Africa still small

Advanced Economies Emerging Markets Sub-Saharan Africa0

5

10

15

20

25

30

35

40

45

50

GD

P –

Tri

llio

n U

SD

Source: IMF, Investment Solutions, 2014

INVESTMENT DESTINATIONS 15

DEVELOPED MARKETS

AFRICAN GROWTH

INVESTMENT EVERGREENS

EMERGING MARKET

LESSONS

AFRICA MUST TRY HARDER

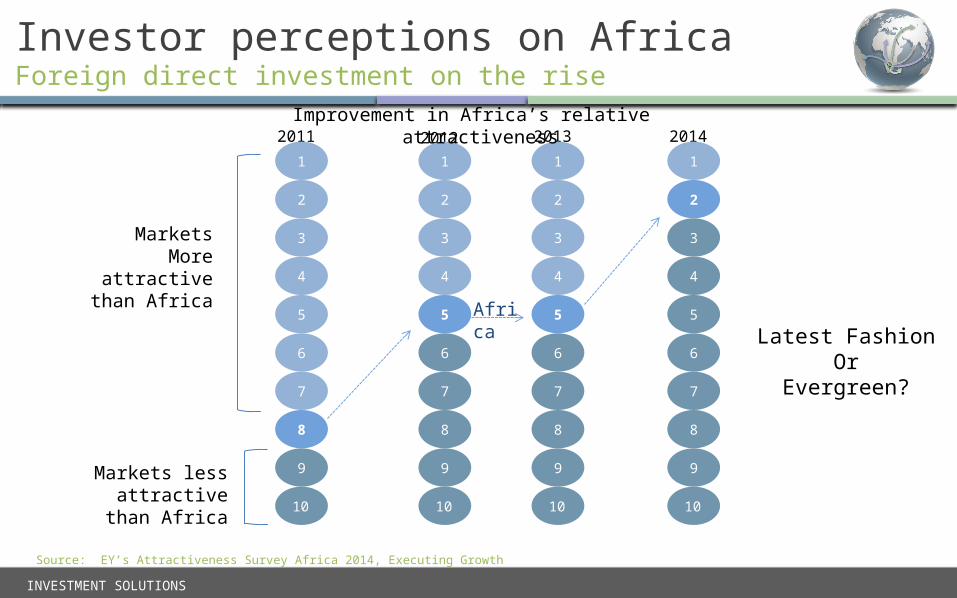

Investor perceptions on AfricaForeign direct investment on the rise

Source: EY’s Attractiveness Survey Africa 2014, Executing Growth

2011 2012 2013 2014

MarketsMore attractive

than Africa

Markets less attractive than

Africa

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

7

8

9

10

1

2

3

4

5

6

7

8

9

10

Improvement in Africa’s relative attractiveness

Africa

INVESTMENT SOLUTIONS

Latest FashionOr

Evergreen?

INVESTMENT SOLUTIONS 17

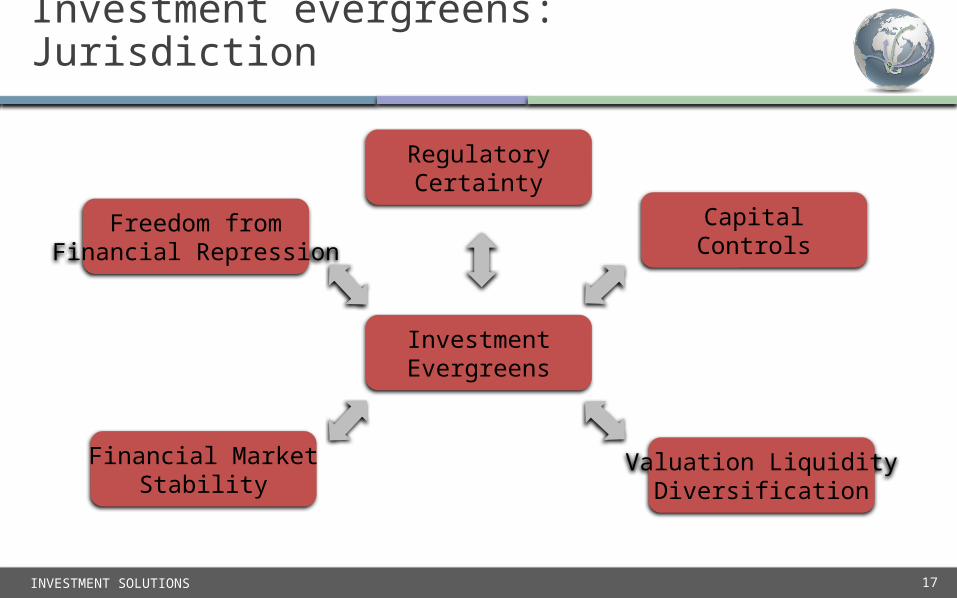

Investment evergreens: Jurisdiction

InvestmentEvergreens

Freedom fromFinancial Repression

CapitalControls

Valuation LiquidityDiversification

Financial MarketStability

RegulatoryCertainty

INVESTMENT SOLUTIONS 18

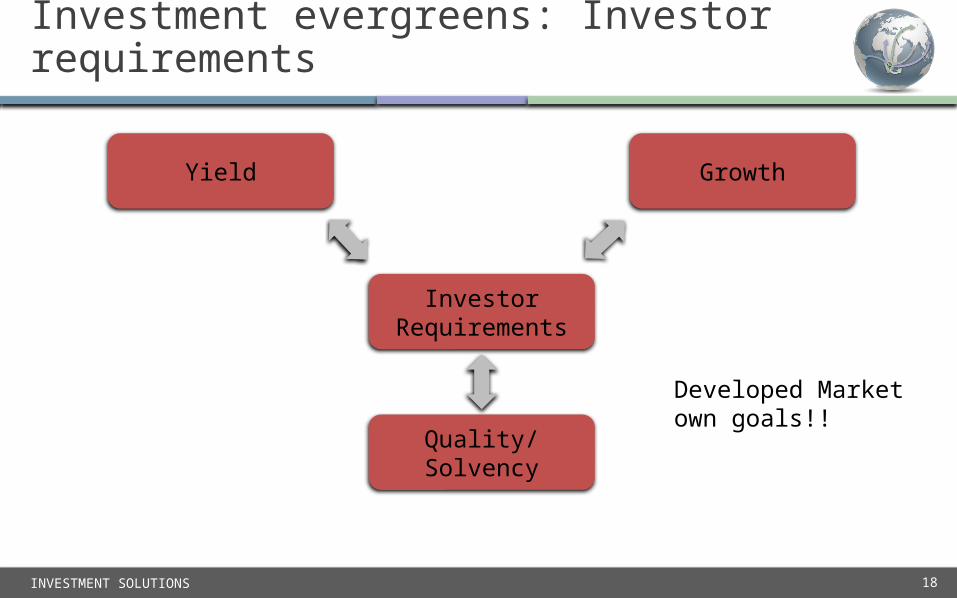

Investment evergreens: Investor requirements

InvestorRequirements

Yield Growth

Quality/Solvency

Developed Marketown goals!!

INVESTMENT DESTINATIONS 19

DEVELOPED MARKETS

AFRICAN GROWTH

INVESTMENT EVERGREENS

EMERGING MARKET

LESSONS

AFRICA MUST TRY HARDER

INVESTMENT SOLUTIONS 20

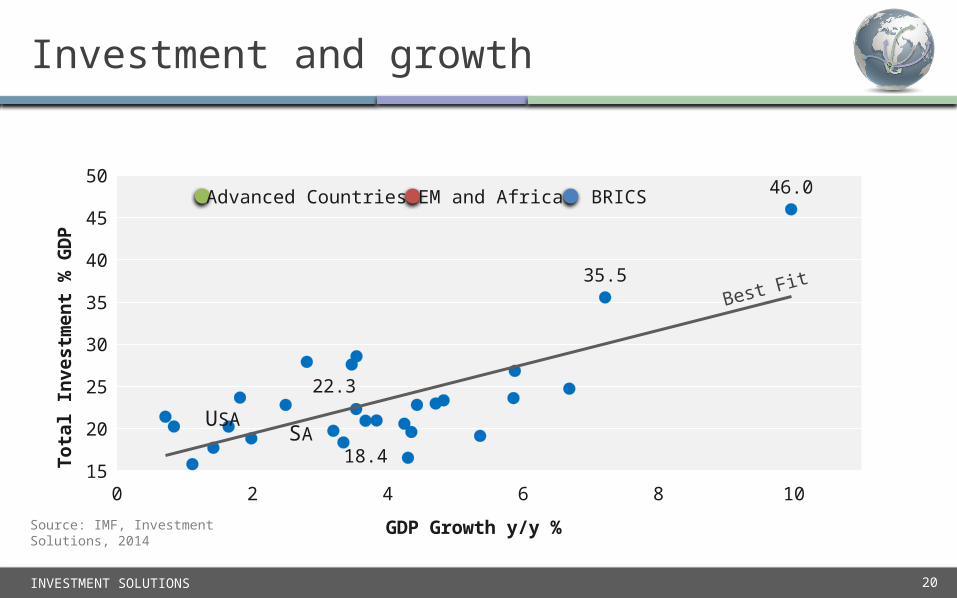

Investment and growth

0 2 4 6 8 1015

20

25

30

35

40

45

50

18.4

46.0

35.5

22.3

SAUSA

GDP Growth y/y %

Tota

l Inv

estm

ent %

GD

P

Best Fit

Source: IMF, Investment Solutions, 2014

Advanced Countries EM and Africa BRICS

INVESTMENT SOLUTIONS 21

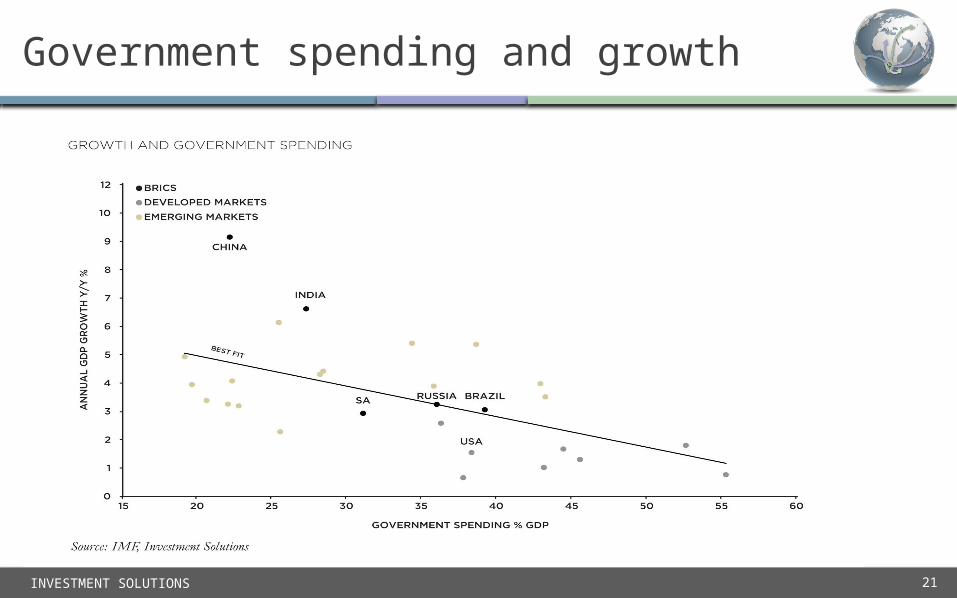

Government spending and growth

Source: INet

INVESTMENT SOLUTIONS 22

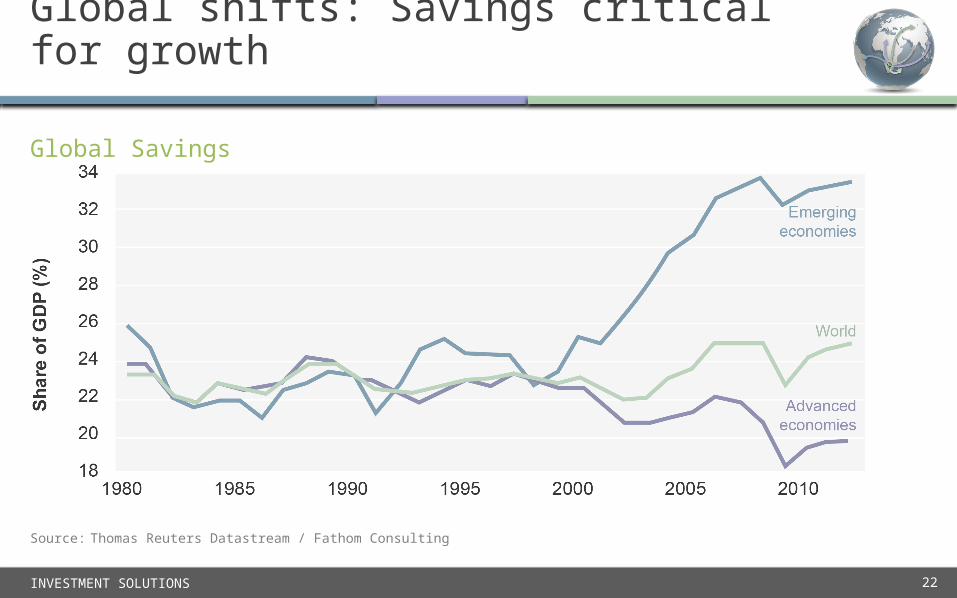

Global shifts: Savings critical for growth

Global Savings

Source: Thomas Reuters Datastream / Fathom Consulting

INVESTMENT SOLUTIONS 23

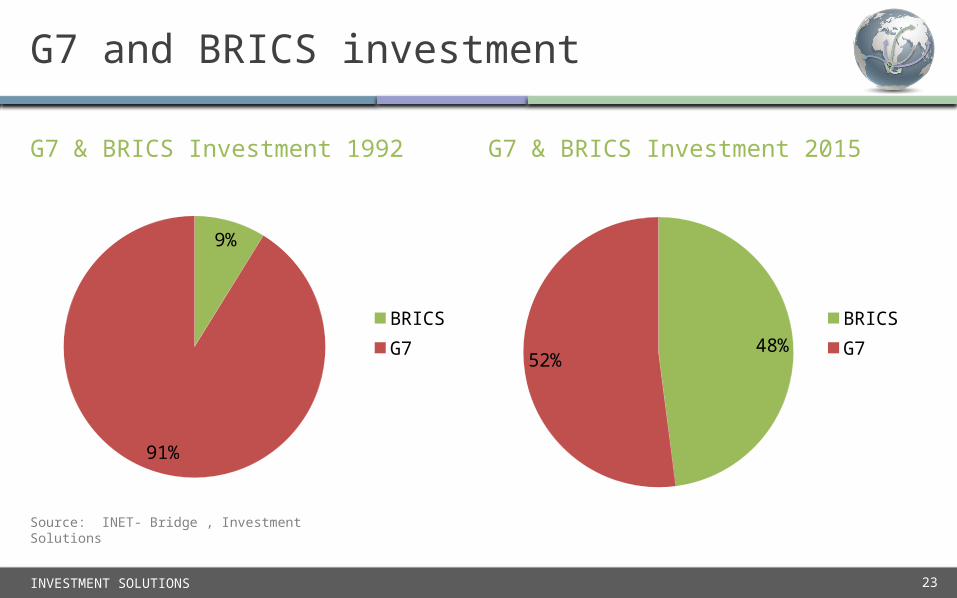

G7 and BRICS investment

G7 & BRICS Investment 1992

9%

91%

BRICSG7 48%

52%

BRICSG7

G7 & BRICS Investment 2015

Source: INET- Bridge , Investment Solutions

INVESTMENT SOLUTIONS 24

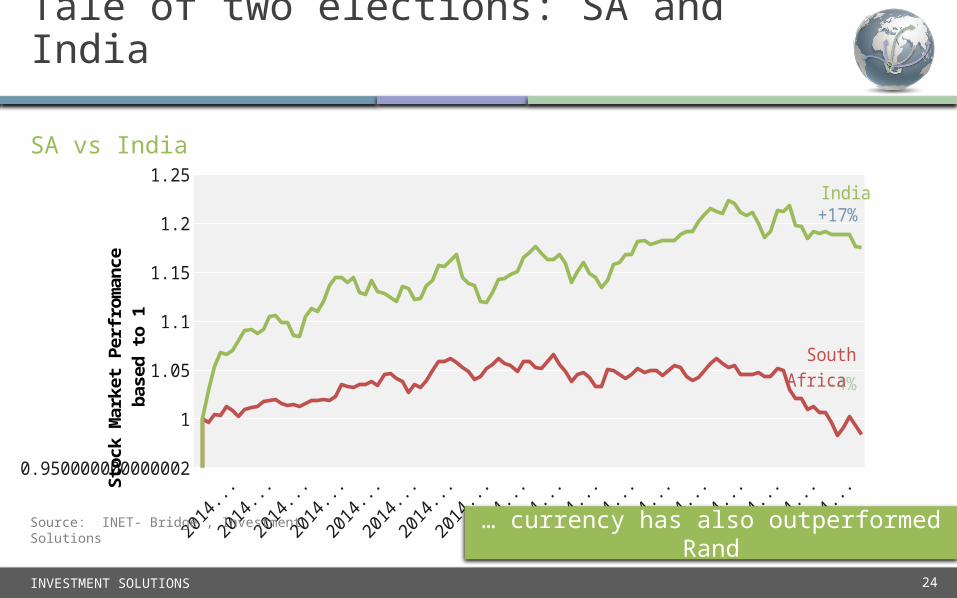

2014/05 2014/06 2014/07 2014/08 2014/09 2014/100.950000000000002

1

1.05

1.1

1.15

1.2

1.25

Sto

ck M

arke

t Per

fro

man

ce

bas

ed to

1

+17%

-4%

India

South Africa

Tale of two elections: SA and India

… currency has also outperformed Rand

SA vs India

Source: INET- Bridge , Investment Solutions

INVESTMENT DESTINATIONS 25

DEVELOPED MARKETS

AFRICAN GROWTH

INVESTMENT EVERGREENS

EMERGING MARKET

LESSONS

AFRICA MUST TRY HARDER

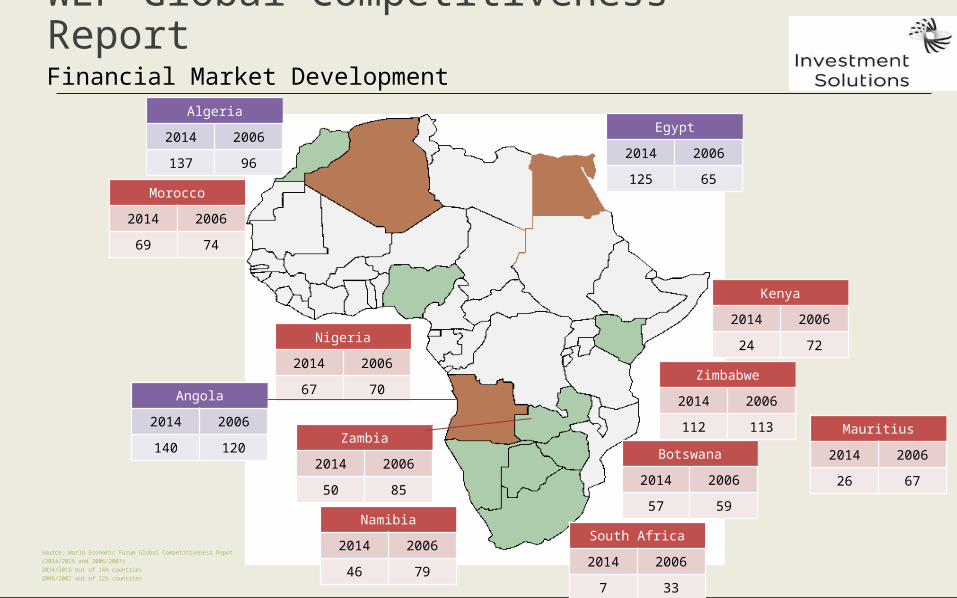

WEF Global Competitiveness ReportFinancial Market Development

Mauritius

2014 2006

26 67

Kenya

2014 2006

24 72

South Africa

2014 2006

7 33

Morocco

2014 2006

69 74

Botswana

2014 2006

57 59

Algeria

2014 2006

137 96

Namibia

2014 2006

46 79

Zambia

2014 2006

50 85

Egypt

2014 2006

125 65

Zimbabwe

2014 2006

112 113

Nigeria

2014 2006

67 70Angola

2014 2006

140 120

Source: World Economic Forum Global Competitiveness Repot (2014/2015 and 2006/2007)2014/2015 out of 144 countries2006/2007 out of 125 countries

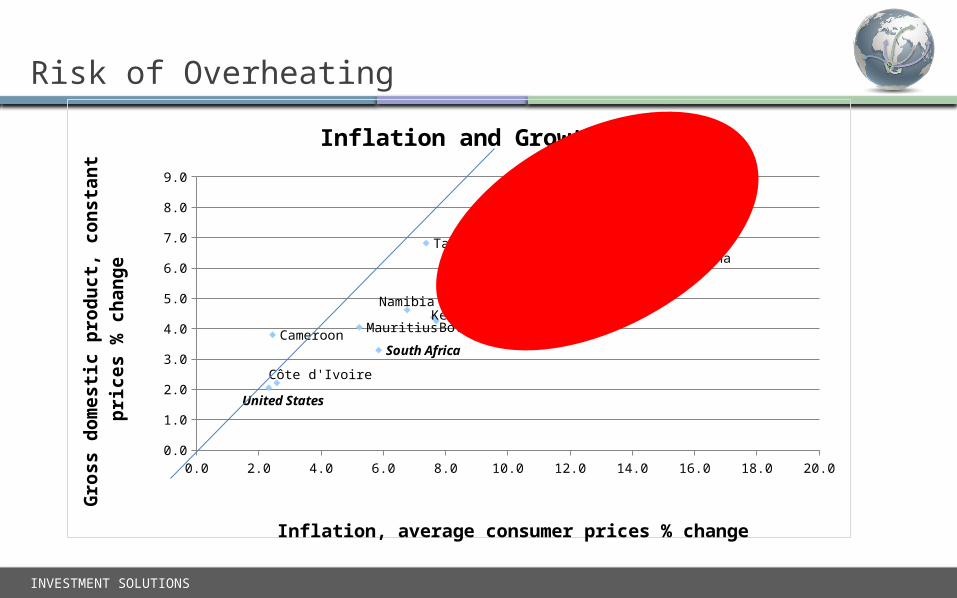

Risk of Overheating

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 20.00.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Botswana Cameroon

Côte d'Ivoire

Ethiopia

Ghana

Kenya Mauritius

Mozambique

Namibia

Nigeria

South Africa

Tanzania

Zambia

United States

Inflation and Growth

Inflation, average consumer prices % change

Gro

ss

do

me

sti

c p

rod

uc

t, c

on

sta

nt

pri

ce

s %

ch

an

ge

INVESTMENT SOLUTIONS

INVESTMENT SOLUTIONS 28

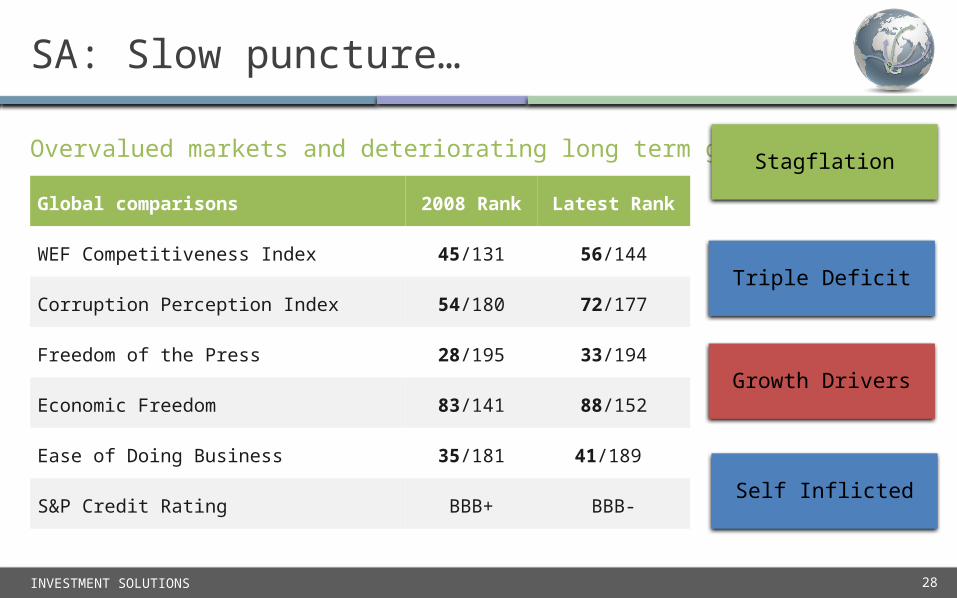

SA: Slow puncture…

Global comparisons 2008 Rank Latest Rank

WEF Competitiveness Index 45/131 56/144

Corruption Perception Index 54/180 72/177

Freedom of the Press 28/195 33/194

Economic Freedom 83/141 88/152

Ease of Doing Business 35/181 41/189

S&P Credit Rating BBB+ BBB-

Overvalued markets and deteriorating long term growth outlookStagflation

Triple Deficit

Growth Drivers

Self Inflicted

INVESTMENT SOLUTIONS 29

National Scars

National Transitions

EconomicValue Chains

Capital Allocation

Political Economy

Dynamics within BRICS…

BRICS ANALYTICAL LENSES

INVESTMENT SOLUTIONS 30

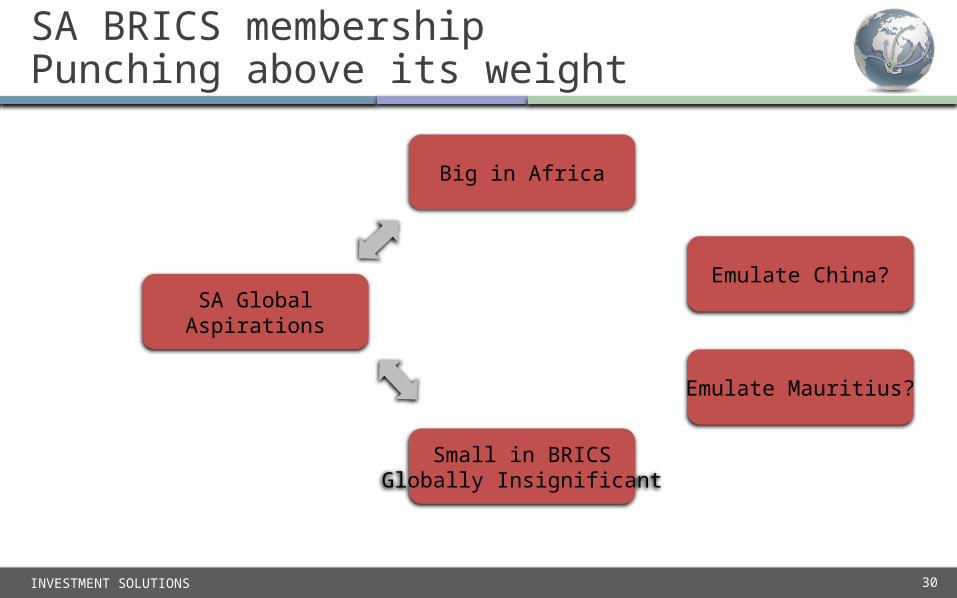

SA BRICS membershipPunching above its weight

SA GlobalAspirations

Big in Africa

Small in BRICSGlobally Insignificant

Emulate China?

Emulate Mauritius?

INVESTMENT SOLUTIONS 31

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0

2

4

6

8

10

12

14

16

18

GD

P /

Capi

ta U

S$ '0

00

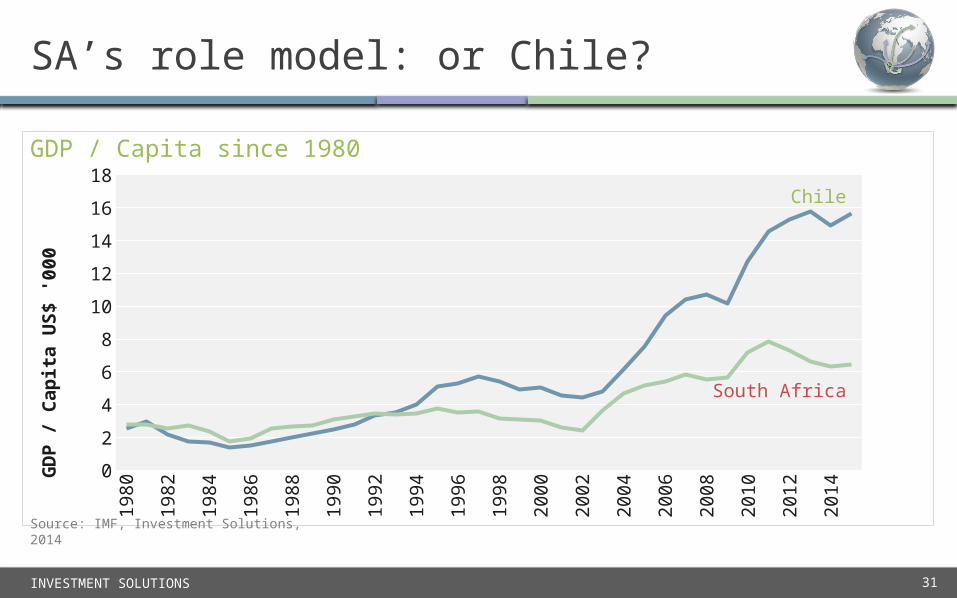

SA’s role model: or Chile?

GDP / Capita since 1980

Source: IMF, Investment Solutions, 2014

Chile

South Africa

INVESTMENT SOLUTIONS 32

SA’s role model: China or Mauritius.?

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

0

2

4

6

8

10

12

GD

P /

Capi

ta U

S$ ‘0

00

GDP / Capita since 1980

Overtaken by both

China

SA

Mauritius

Source: IMF, Investment Solutions, 2014

SSA: Tax differentials between jurisdictions

Country Income Tax Rate (%) Corporate Tax Rate (%) Tax Burden % of GDP

Hong Kong 15.0 16.5 14.2

Nigeria 24.0 30.0 4.7

Ghana 25.0 25.0 14.6

Mauritius 15.0 15.0 18.3

Zambia 35.0 35.0 19.3

Kenya 30.0 30.0 20.1

South Africa 40.0 28.0 27.3

Namibia 37.0 34.0 28.0

Lower tax burdens more competitive…

Source: Heritage foundation

INVESTMENT SOLUTIONS 34

Top Insights from ‘Half Way There’

3. Business is the source of all wealth

5. Corruption is an economic cancer

8. Effective institutions essential for democratic credibility

... SEE HALF WAY THERE FOR MORE..!

INVESTMENT SOLUTIONS 35

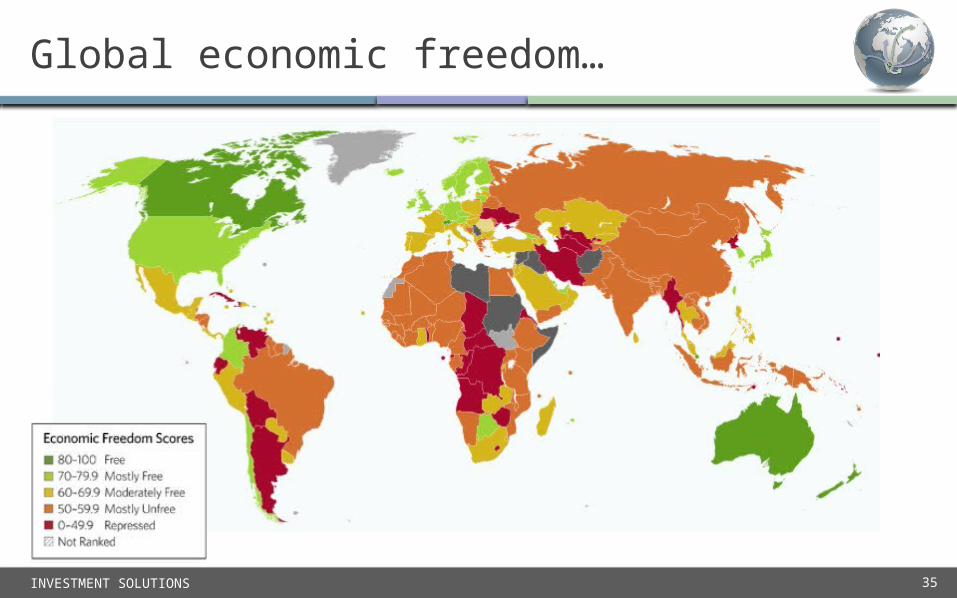

Global economic freedom…

INVESTMENT SOLUTIONS 36

Thank You

CHRIS HARTChief Strategist

Investment Solutions

sa.investmentsolutions.co.za

@chrishartZA

011 505 6041