chp & iaq equipment opportunities - … & iaq equipment opportunities technology discussion...

TRANSCRIPT

CHP & IAQ Equipment OpportunitiesTechnology DiscussionAugust 10, 2001

Presented by:John Cuttica, Energy Resource Center, UICRich Sweetser, EXERGY Partners Corp.John Kelly, GTI Distributed Energy Division

August 10, 2001

Video courtesy of Plug Power

Can You Hear the Footsteps?

Agenda

IntroductionUSDOE’s Perspective on DG/CHPCase Study and Technology OverviewEnergy Pricing OverviewDOE Midwest Region Application CenterApplication Center Support Options

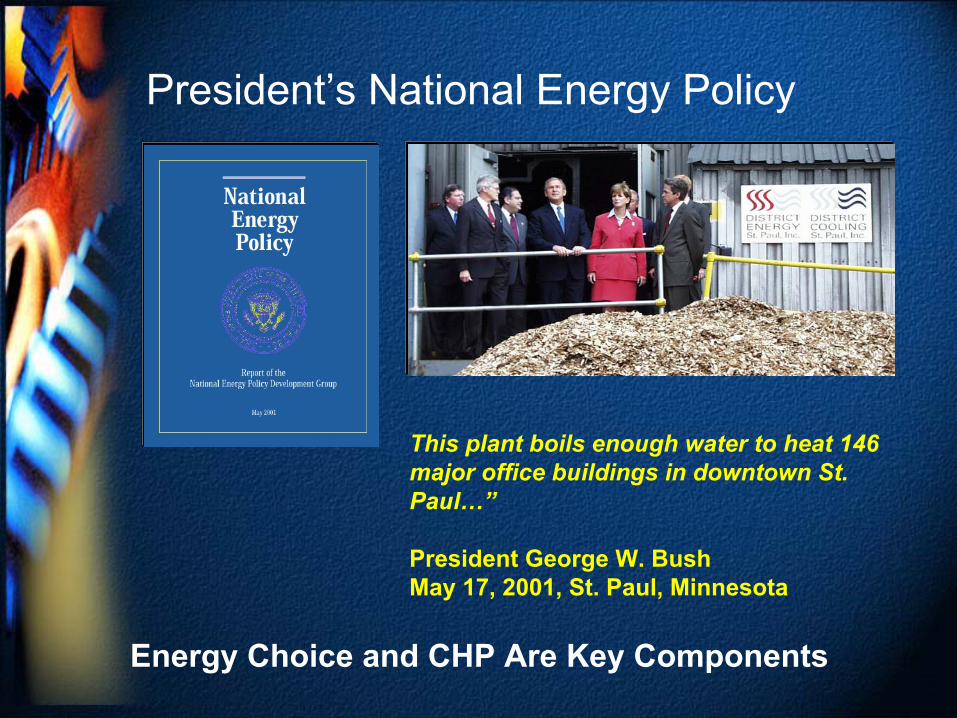

This plant boils enough water to heat 146 major office buildings in downtown St. Paul…”

President George W. BushMay 17, 2001, St. Paul, Minnesota

Energy Choice and CHP Are Key Components

President’s National Energy Policy

National Energy Policy on CHPCHP is environmentally preferred, cost effective, efficient, and reliable. CHP is defined as part of the distributed energy group of technologies that can reduced transmission and distribution (T&D) losses and defer the need to construct expensive new T&D assets. Distributed energy technologies also include: stationary fuel cells, landfill methane, small-scale wind, and photovoltaics. Location of CHP at or near the end-use site allows for use of waste heat and waste-fuels. Barriers to CHP are identified as:

Delay and difficulties obtaining air permits, including lack of recognition of CHPair quality benefits. Difficulties in siting due to local ordinances. Lack of standards governing utility interconnection. Inequitable tax treatment.

U.S. CHP Installations

Paper16%

Chemicals31%

Food9%

Refining13%

Metals5%

Other Ondustrial20%

Comml/Inst9%

52,800 MW – 1999

Source: U.S. DOE-EIA and Onsite-Sycom

Source:, OSEC

Other Industrial29%

U.S. CHP for Industry Potential

Paper30%

Chemicals11%

Food9%

Refining13%

Metals8%

Estimated CHP Potential: 88,000 MW

Source: U.S. DOE-EIA and Onsite Sycom

U.S. CHP for Buildings PotentialEstimated CHP Potential: 75,000 MW

Health Care24%

Education27%

Food Sales/Serv

10% Lodging7%

Office Buildings

21%

Other11%

Source: U.S. DOE-EIA and Onsite-Sycom

Office of DER Vision 2020

The United States will have the cleanest and most efficient and reliable energy system in the world by maximizing the use of affordable distributed energy resources.

Office of DER Mission 2020To lead a national effort to:

Develop the “next generation” of clean, efficient, reliable, and affordable distributed energy technologies;

Document the energy, economic, and environmental benefits of the expanded use of distributed energy resources and disseminate the findings widely; and

Implement deployment strategies, including national and international standards, that address infrastructure, energy delivery, institutional, and regulatory needs.

Slight Detour – Indoor Air Quality

IAQ Findings

Comfort to Productivity Link Made

It stands to reason that if you are comfortable you can be more productive than if you are not comfortable.

Professor P. Ole Fanger, D.Sc. Director, International Centre for Indoor Environment and Energy at the Technical University of Denmark, is the world’s leading expert on human interaction with indoor environments. Professor Fanger has recently published a series experimental results linking comfort to productivity and ventilation air and humidity control to improved comfort.

Desiccants eliminate common moisture problems in buildings

STOP

DUST M

ITES

ELIM

INATE

BACTERIA

ERADIC

ATE

MOLD D

AMAGE

PREV

ENT

CORROSION

FORGET

FUNGUS

DOE Working on Desiccant TechnologyDesiccant systems are widely used for energy recovery, to provide precision humidity control in industry and to control operating costs in today's supermarkets. Ongoing work at ORNL, at NREL and within industry has yielded significant advances in performance, applications and material cost reduction. Desiccant humidity control is expected to become an essential engineering tool to manage moisture within 21st

century buildings.

Desiccant Technology

Rotating Desiccant Wheel~ 20 rev/hr

Drive motor

ReactivationHeater

ReactivationAir

ReactivationSide

ProcessSide

Hot, Low RHWarm, High RH

Cool, High RH Warm, Low RHProcessAir

Rotating Desiccant Wheel~ 20 rev/hr

Drive motor

ReactivationHeater

ReactivationAir

ReactivationSide

ProcessSide

Hot, Low RHWarm, High RH

Cool, High RH Warm, Low RHProcessAir

Back on Track with CHP

Institutional and District Energy

> 172,148,208 sq ft of buildings connected to institutional and district energy systems. In 1999 customers totaling more than 21,783,280 sq ft of space had been added to institutional and district energy systems.

OPRYLAND Hotel and Convention Center

Case Study provided by:IC Thomason Associates, Inc.

Consulting EngineersNashville, TN

Typical Private Sector System

5 MW gas turbine systemwith heat recovery, chiller

1,000 RT double-effect absorption chiller

Inlet air cooler uses 300 RT of CW output

Operating since 1996

O&M costs reduced from $3 million /yr “pre-CHP” to $2 million/yr

University of IllinoisRepresenting Institutional Facilities

East Campus

Original Installation in 1993

Two Cooper-Bessemer 20-cylinder LSVB, 6.28 MW engines, installed in 1993, are also used at the east campus plant. Cooper-Bessemer's LSVB power engines are four cycle designed engines for high-horsepower, continuous-duty operation.

Seasonal Load East Campus

0

2

4

6

8

10

12

14

16

18

20

1 2 3 4 5 6 7 8 9 10 11 12

Month

Meg

awat

ts

Base LoadCooper Engines

Additional Units for Seasonal Load

Two Wartsila 18V28SG engines driving ABB generators rated 4.1 MW each were added in 2000 to pick up the east campus' seasonal load

Seasonal Load East Campus

0

2

4

6

8

10

12

14

16

18

20

1 2 3 4 5 6 7 8 9 10 11 12

Month

Meg

awat

ts

Base LoadCooper Engines

Seasonal LoadWartsila Engines

Heat Recovery System

4 – exhaust gas heat recovery systems Total rating: 8.8 MWth (30 MMBTUH)

2 – jacket water heat recovery systems (one each for the Cooper Engines) Total rating: 2.4 MWth (8 MMBTUHth)

Heating & CoolingHeating loop consists of;

Two dual fuel 22 MWth(75 MMBTUH) One 15 MWth(50 MMBTUH)

Cooling loop consists of;Three absorption chillers (decentralized) totaling 5.3 MWth (1,500 RT) One absorption chiller (central) totaling 3.5 MWth (1,000 RT)Three centrifugal chillers (central) totaling21 MWth (6,000 RT)

Financials

1993 Plant (2 – 6.28 MW Cooper Engines)Capital cost $15,000,000Annual operating savings ~$2,000,000Systems simple paid back in 7.5 years

2000 Plant AdditionAdding (2-4.2 MW Wartsila Engines)

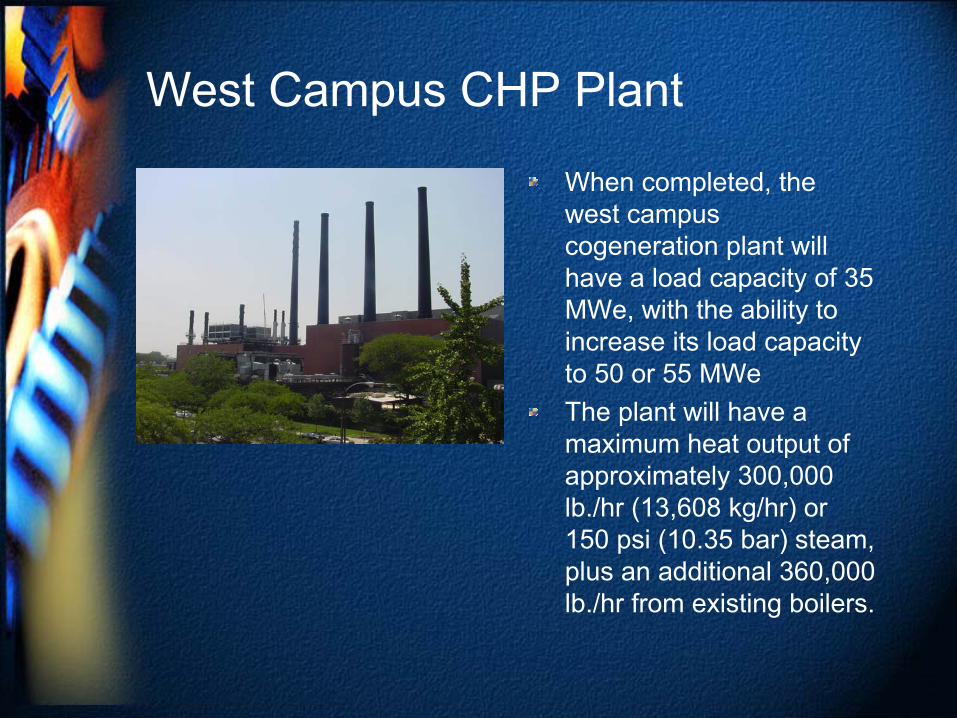

West Campus CHP Plant

West Campus CHP Plant

When completed, the west campus cogeneration plant will have a load capacity of 35 MWe, with the ability to increase its load capacity to 50 or 55 MWeThe plant will have a maximum heat output of approximately 300,000 lb./hr (13,608 kg/hr) or 150 psi (10.35 bar) steam, plus an additional 360,000 lb./hr from existing boilers.

Base Load Gas Turbines

Three Solar Taurus 70 combustion turbines.The turbines will each drive Ideal Electric generators. Output of 7 MWe per unit.

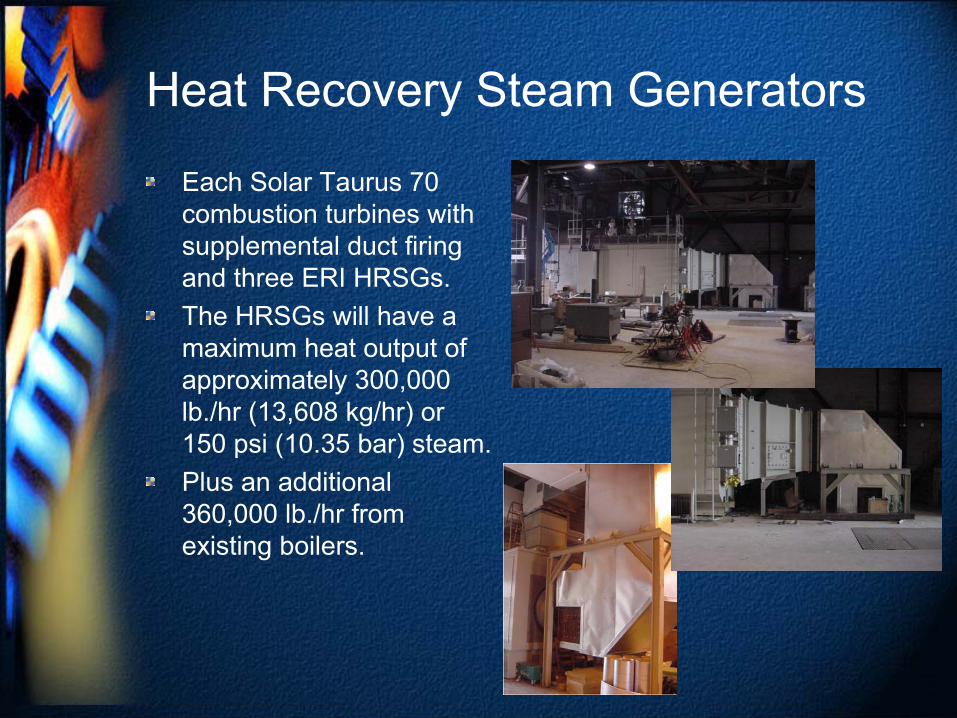

Heat Recovery Steam Generators

Each Solar Taurus 70 combustion turbines with supplemental duct firing and three ERI HRSGs.The HRSGs will have a maximum heat output of approximately 300,000 lb./hr (13,608 kg/hr) or 150 psi (10.35 bar) steam.Plus an additional 360,000 lb./hr from existing boilers.

Engines

Three 5.2 MW Wartsila18V34SG lean burn, reciprocating engines will drive ABBgenerators.The Wartsila engines currently have no heat recovery. The engines are equipped with catalytic oxidizers for pollution control

Financials

2001 Plant 3 – 5.0 MWe Wartsila Engine/Generators3 – 7.0 MWe Solar Gas Turbines3 – HRSGs 45.4 kg/hr (360,000 lb/hr) steamCapital cost $38,000,000Annual operating savings ~$6 to 8,000,000Systems simple paid back in 4.75 to 6.5 years simple payback

Hospital

Three 1,200 rpm natural gas Engine Generators With Heat Recovery 3.45 MWe(125 psi Steam) to 700 Ton Double Effect Absorption Chiller11 MMBTUH W.J. Heat Recovery. System Eff. 73% $890,000 / Yr Savings

Institutional

Four 1200 rpm natural gas Engine Generators3.1 MWe240 F Hot Water W.J. Heat Recovery5.0 mmBtu/Hr To Main Campus Heating Loop.System Eff. 50$600,000 / Yr Savings

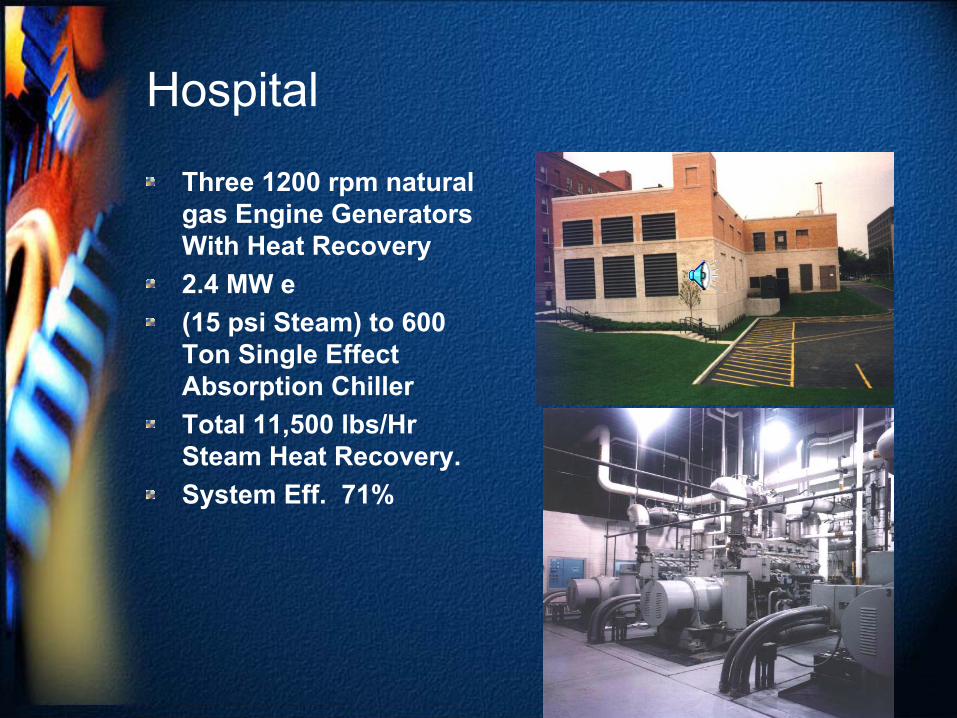

Hospital

Three 1200 rpm natural gas Engine Generators With Heat Recovery 2.4 MW e(15 psi Steam) to 600 Ton Single Effect Absorption ChillerTotal 11,500 lbs/Hr Steam Heat Recovery.System Eff. 71%

Industrial

Seven 1200 rpm natural gas Engine Generator4.9 MW eWith Heat Recovery of 15 Psi Steam for Heating & Process.Total Steam Production of 15,000 Lbs/Hr.Pay Back in under 3 Years and provides Power to Cool the Entire Manufacturing Floor

The Future of the Technological Base

Distributed Energy ResourcesLiBr Absorption Chillers

20104 Broad market penetration through

25% cost reduction 30% more efficiency and integration with BCHP systems

20004 Good technologies,

but limited penetration

Distributed Energy ResourcesDesiccant Dehumidifiers

20004 Niche market equipment

for high value humidity control applications

20104 Mainstream humidity control using

new solid desiccant materials & new liquid technologies resulting in 50% cost reductions

Engines

20004 25 - 40% 4 2-3 grams/kWh NOx

20074 50% Efficiency4 < 1.5 grams/kWh NOx

Advanced Turbines

20104 Small (< 10 MWe) Gas Turbine

Efficiency > 40% LHV

20004 Maximum Small (< 10 MWe)

Gas Turbine Efficiency at 33% LHV

Microturbines

20004 17-30% Efficiency (LHV)4 Double digit ppm NOx

20074 40% Efficiency (LHV)4 Single digit ppm NOx

Fuel Cells for Buildings

20004 $4500/kW

20104 $1500/kW

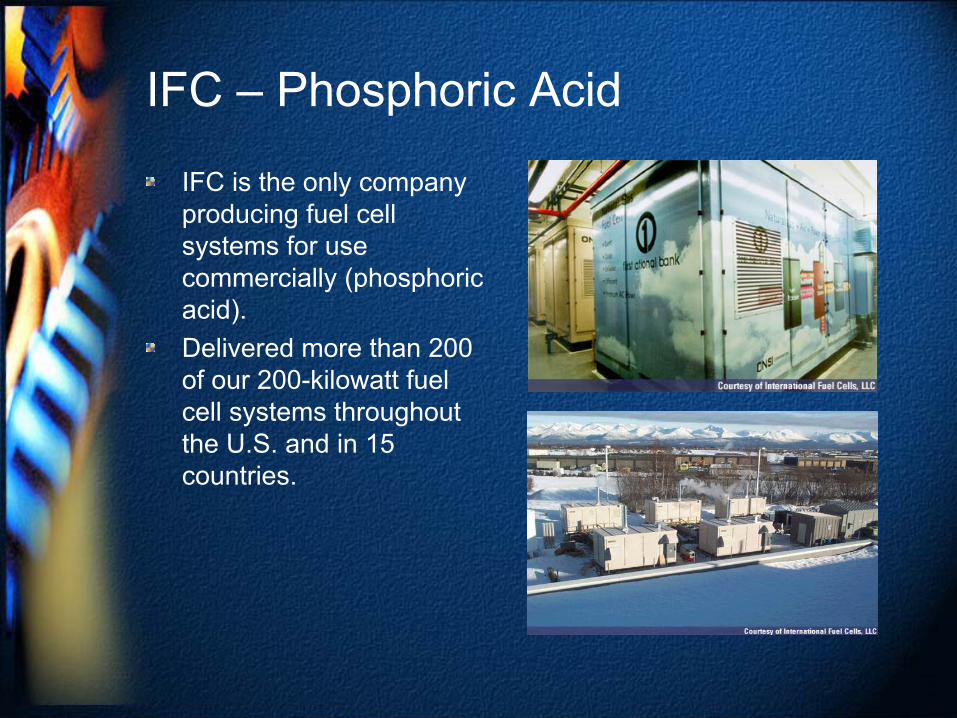

IFC – Phosphoric Acid

IFC is the only company producing fuel cell systems for use commercially (phosphoric acid). Delivered more than 200 of our 200-kilowatt fuel cell systems throughout the U.S. and in 15 countries.

GE/Plug Power PEMImagine your own reliable supply of electricity in a compact, quiet, self-contained package - a fuel cell called the HomeGen. This new energy system now under development, will generate electricity at your home. Because it HomeGen is fueled by natural gas or LPG -- it will be both efficient and environmentally friendly . Installed in your back yard, the HomeGen fuel cell is being designed to provide 100% of your home's energy needs.

Fuel Cell Energy – Molten Carbonate

FuelCell Energy is developing its Direct FuelCell® (DFC®) for use in stationary applications. Our three main products—a 300 kW, a 1.5 MW and a 3 MW—are designed to meet a variety of applications. For example, the 300 kW single stack DFC power plant is a skid-mounted, compact unit, which can be used to add incremental capacity or to gain operational familiarity with DFC power plants. Ideal customers include light industrial, small buildings and other applications requiring 250 kW to 1 MW of power.

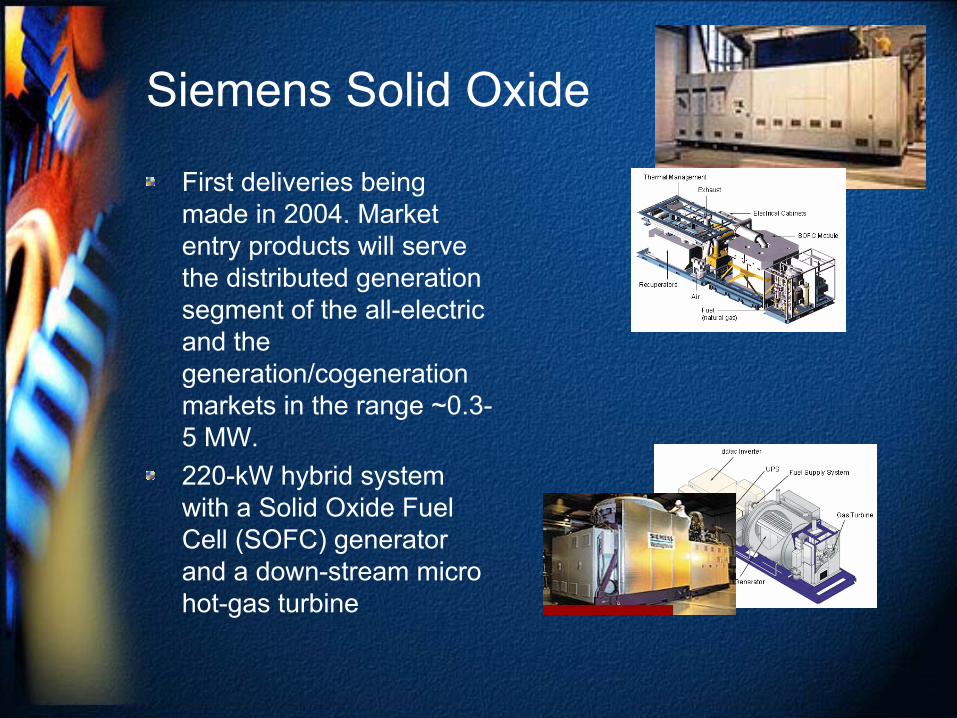

Siemens Solid Oxide

First deliveries being made in 2004. Market entry products will serve the distributed generation segment of the all-electric and the generation/cogeneration markets in the range ~0.3-5 MW. 220-kW hybrid system with a Solid Oxide Fuel Cell (SOFC) generator and a down-stream micro hot-gas turbine

The Future of CHP Packaged and Modular Systems

Capstone~ $3 million

United Technologies ~ $ 2.8 million

NiSource~ $0.8 million

GTI, Waukesha, Trane ~ 2.5 million

Honeywell~ $4.3 million

Burns & McDonald, Solar & Broad USA

$3 million

Ingersoll-Rand~2.3 million

Energy Pricing Overview

0

4

8

12

16

20

24

28

32

Trill

ian

Cubi

c Fe

et

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Year

Other

Residential

Commercial

Industrial

Power Gen

Natural Gas Consumption (TCF)

Added 15 TCF – InterstateTippled Storage

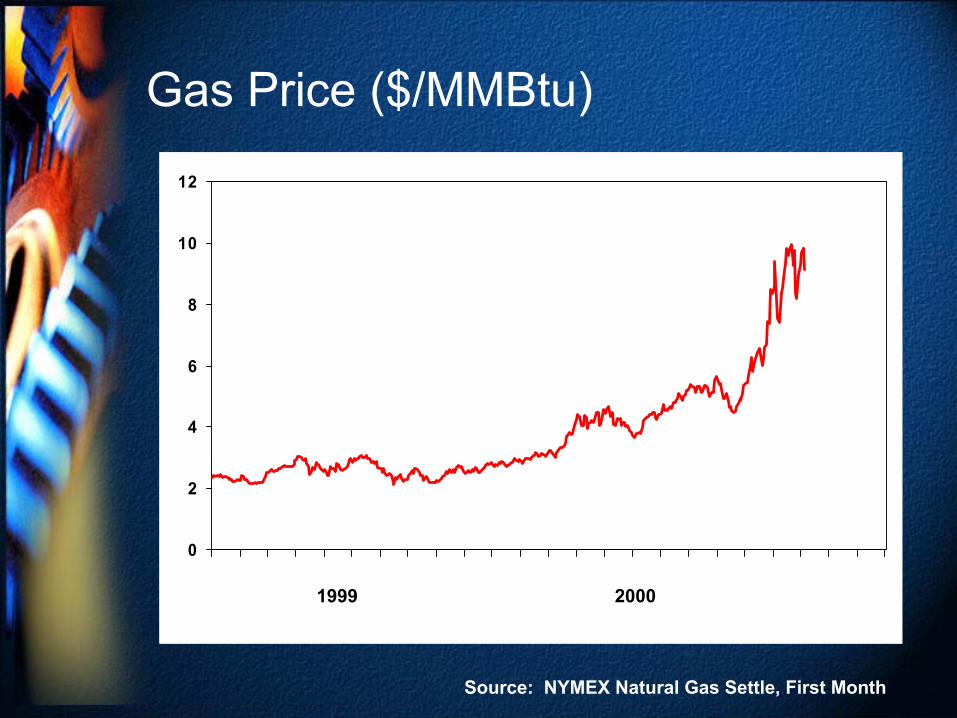

Gas Price ($/MMBtu)

0

2

4

6

8

10

12

1999 2000

Source: NYMEX Natural Gas Settle, First Month

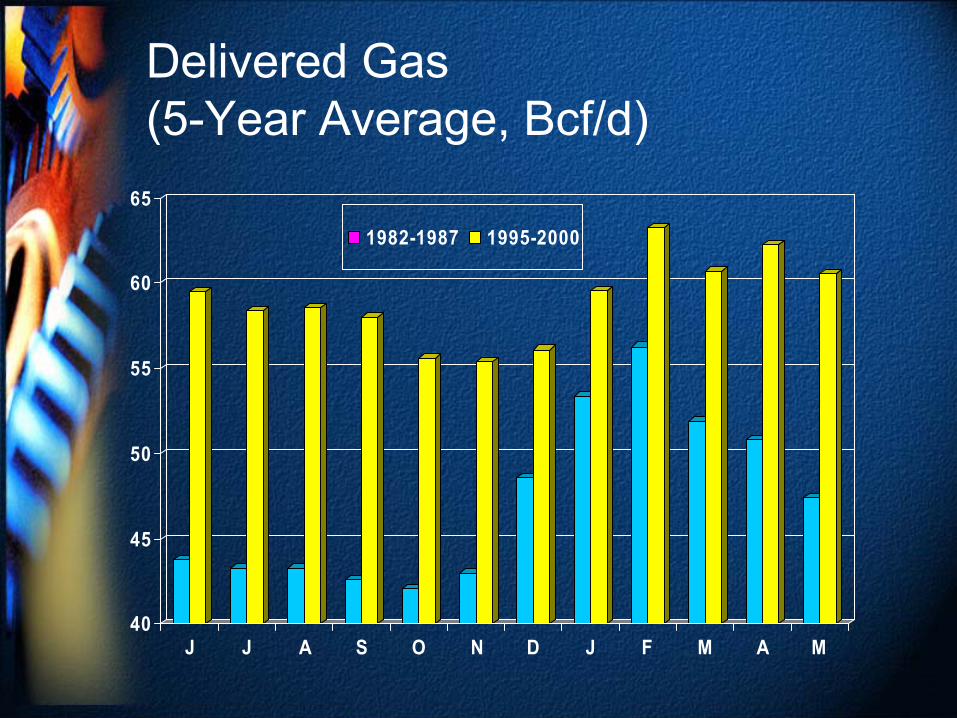

Delivered Gas (5-Year Average, Bcf/d)

40

45

50

55

60

65

J J A S O N D J F M A M

1982-1987 1995-2000

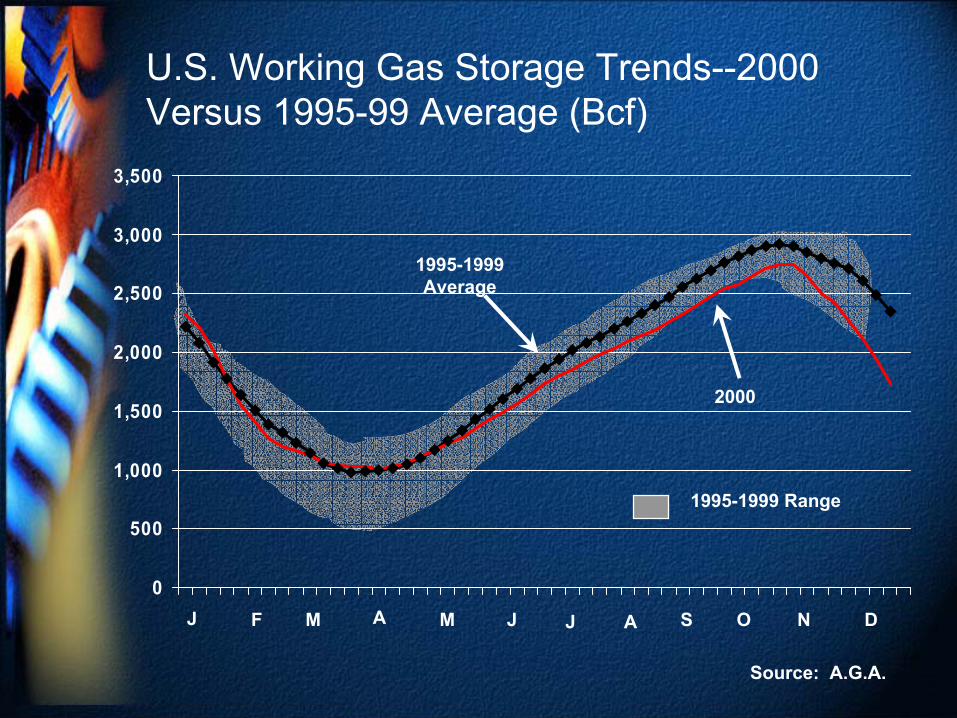

U.S. Working Gas Storage Trends--2000 Versus 1995-99 Average (Bcf)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1995-1999 Average

1995-1999 Range

2000

J F M A M JJ A S O N D

Source: A.G.A.

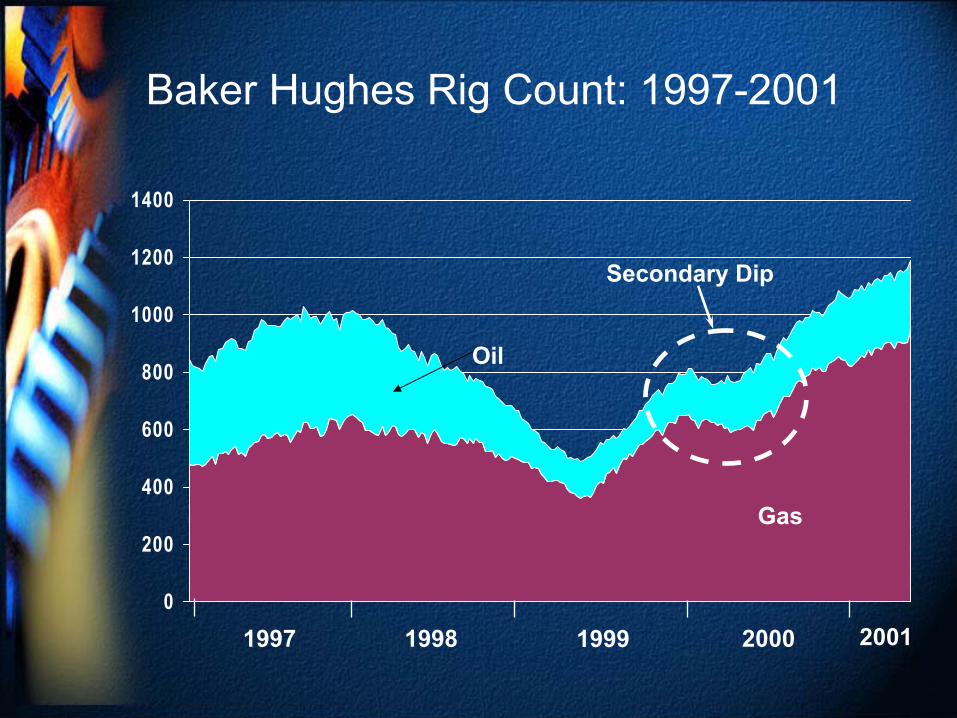

Baker Hughes Rig Count: 1997-2001

0

200

400

600

800

1000

1200

1400

Gas

Oil

1997 1998 1999 2000

Secondary Dip

2001

Lower-48 Gas Deliverability & Production (Bcf/d)

38

42

46

50

54

58

62

'91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05

Deliverability Production

History

GRI Baseline Report

0

200

400

600

800

1000

1200

1400

1600

1800

1990

1993

1996

1999

2005

2008

2013

2020

natural gas

Additions of Interstate Natural Gas Pipeline Capacity (billion cubic feet)

15 TCF AddedYet use remains at 1972 levels22 TCF 1999

WORKING GAS

BASE GAS

0

1000

2000

3000

4000

50006000

7000

8000

9000

10000

1930

1938

1945

1955

1960

1963

1975

1983

1993

1995

2005

2015

YEAR

BIL

LIO

N C

UB

IC F

EET

1970 – 4 TCF

2000 – 8 TCF

GRI Baseline Report

Underground Natural Gas Storage Capacity

5

32

14

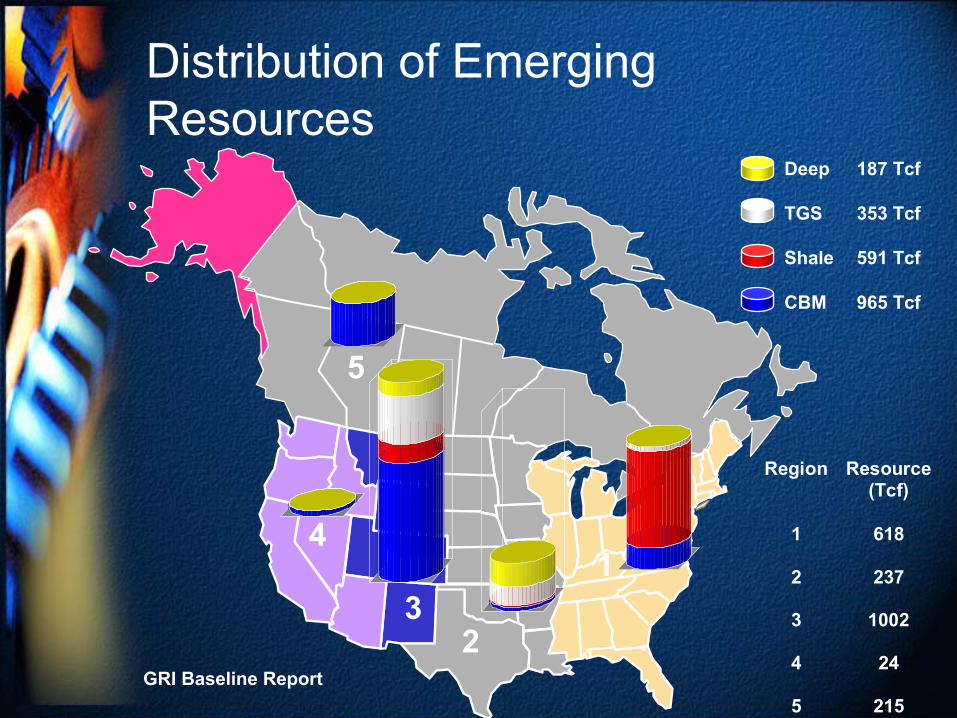

Distribution of Emerging Resources

Region Resource (Tcf)

1 618

2 237

3 1002

4 24

5 215

Deep 187 Tcf

TGS 353 Tcf

Shale 591 Tcf

CBM 965 Tcf

GRI Baseline Report

U.S. Working Gas Storage Trends (Bcf)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2000

1995-1999 Range

2001 (Act.)

J F M A M JJ A S O N D

Source: A.G.A.

Current Supply Situation

Production Situation ImprovingLower-48 Stakes Running At Over 98 Percent Of Deliverability In 2000Storage Situation Has Improved Rapidly Relative To Earlier Expectations

Milder Weather In Early 2001Slowdown In Economic Activity

Current Demand Situation

Mild Or “Normal” Winter Weather In January, February, And March And Slowdown In Economic Activity Moderated Demand In Early 2001Growing Gas Demand For Power Generation Still Driver Of Market, But Growing Interest In CoalClear Evidence Of Growing Summer Demand could Hold-Up PricesEconomic Weakness Will Help Industry Adjust In Near Term

WELLHEAD GAS PRICE SCENARIOS ($/MMBtu)

1

2

3

4

5

6

7

8

9

10

J M M J S N J M M J S N J M M J S N J M M J S N J

2000 2001

Base Case: $4.80

Cold Winter: $5.75

2002

Base Case: $4.50

Cold Winter: $5.25

Recession: $3.95

2003

Recession: $3.30

Base Case: $4.90

dgencost.pre

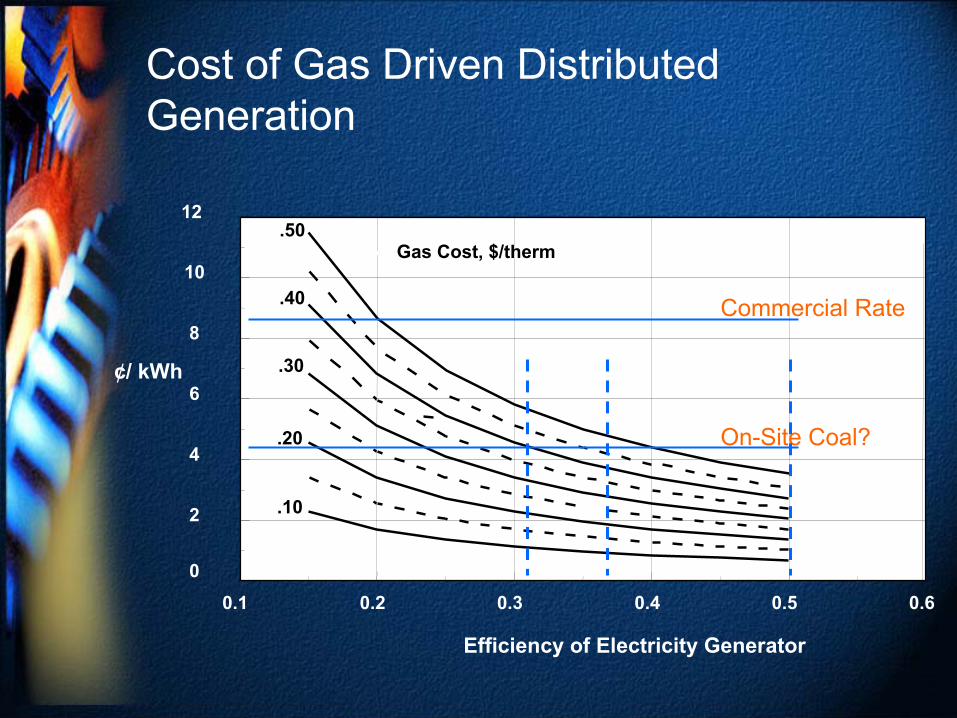

0.1 0.2 0.3 0.4 0.5 0.60

2

4

6

8

10

12

Efficiency of Electricity Generator

.10

.20

.30

.40

.50Gas Cost, $/therm

¢/ kWh

Cost of Gas Driven Distributed Generation

0200400600800

1,0001,2001,4001,6001,800

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Residential Commercial Industrial

DOE Projects 390 gigawatts needed

Total US Capacity is 740 gigawatts

Annual Electricity Sales by Sector(billion kilowatthours)

EnergyCrisis

VAV

1950 1960 1970 1980 1990

Ventilation

Rates

(cfm/person)

TightBuildings

ASHRAE Stds 62-73 62-81 62-89 62-??

SickBuildings

IAQ Concerns Lead to Increased Energy Costs

Pricing Overview

Service Generation

Fuel Emissions Market Power

Deregulated

T&D Regulated Ancillary Costs Regulated Taxes/Programs Regulated Stranded/ Deregulation Costs

Regulated

T&D, DOE Projections

2005 Projections2

cents/kw-hr Service CA NY IL TX

Electricity Generation 3.1 3.8 2.9 2.7 T&D 3.6 4.4 2.3 1.7 Taxes, Public Programs

0.2 0.8 0.5 0.2

Total 6.9 9.0 5.7 4.6 % Generation 44% 42% 48% 59%

Average Electricity Prices

T&D, Illinois

Service Charge Basic Service Charge 0.5 Delivery and Ancillary 4.3 Generation 3.2 Total 8.0

In Illinois only ~ 40% of the cost of electricity is attributed to generation

Commercial

25 MW

20 MW

10

10

15

5

25Cumulative Capacity Dispatched

Second-lowest

price unit

Lowest-cost, (Base Load) plant

Base load

Peaker

Cen

ts/k

Wh

MW

2

4

6

8

10

Nuclear

Coal and Gas

Gas and Oil

Time of Day Pool Pricing

0

5

10

15

20

25

30

35

40

45

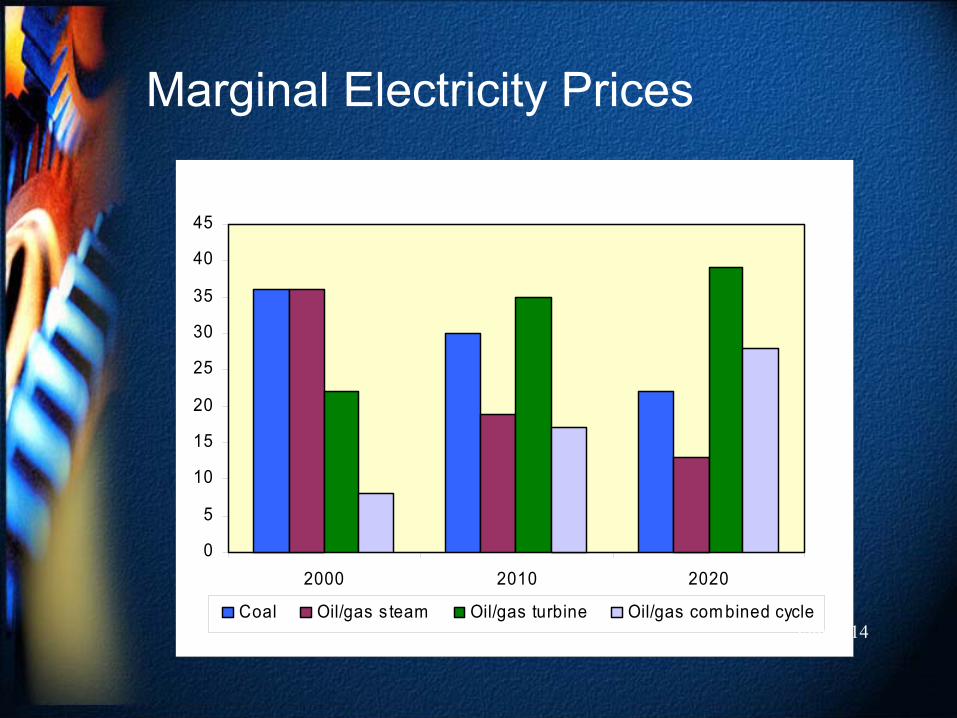

2000 2010 2020

Coal Oil/gas s team Oil/gas turbine Oil/gas com bined cycleFigure 14

Marginal Electricity Prices

Supply vs. Demand?

Projected 390 gigawatts of new capacityOnly added 70 over past 10 years

Projected retirements could widen the gapEmissions restrictions could retire 50% of coal generationUsage Rising at 500+ billion killowatthours per decade

Electricity usage doubled over past 30 and growth is accelerating

As seen in CA shortages in supply impact prices

Market Power?

Restricted AccessPower PreferencesWithholding Power - In UK generators withheld power to raise pricesDistribution Constraints

Market Power is a phenomena where a seller/state is able to influence prices

After 10 years England still struggling with issue

Illinois

Transmission Lines

345 KV735-765 KV

Ozone Non-attainment

Entire County

40 miles:

78 sites, 5.8 GWe

60 miles:

94 sites, 8.2 GWe

Chicago

Part of County

Note impact on Emissions

Coal Emissions Reduction Costs?

SO2 allowances to rise from $90 to $300 per ton (<.1 cents/kW-hr)Coal contributes 90% of CO emissions from electricity generation

CO emissions credits $67 to $350 per ton (2 to 9 cents/kW-hr)

NOx allowances expected to cost approximately 0.2 cents/kWUS EPA expected to regulate particulate emissions

Conclusion – Grid Price Generation

Demand is likely to outstrip supplySystem constraints and permitting slow additions

Marginal Price is lowest priceElectricity cannot be storedCommercial daytime users will pay higher prices

T&D and ancillary costs key in many regionsUp to 20 cents/kW-hr in high cost areasSignificant Upgrades Underway

Natural gas will set the marginal price in many regionsMarket power will effect pricesEmissions control on CO unlikely

0.1 0.2 0.3 0.4 0.5 0.60

2

4

6

8

10

12

Efficiency of Electricity Generator

.10

.20

.30

.40

.50Gas Cost, $/therm

¢/ kWh

Cost of Gas Driven Distributed Generation

Commercial Rate

On-Site Coal?

DOE Midwest Region Application Center

Midwest Regional Application Center

Mission:Develop Technology Application Knowledge and the Educational Infrastructure Necessary to:

Reduce Perceived RisksFoster CHP for Buildings as a Viable:

Technical and Financial OptionEnergy and Environmental Option

Focus: (Foster Project Identification)EducationInformationProject Assistance

Midwest Regional Application Center

Partnership:University of Illinois at ChicagoEnergy Resources Center --- UIC/ERC

andGas Technology Institute --- GTI

Sponsorship:DOE Office of Power Technologies

Technical/Program Guidance:Oak Ridge National Laboratory --- ORNL

Midwest Regional Application Center

Leverage:DOE Chicago Regional OfficeIllinois DCCAEPA Region VMidwest CHP InitiativeDelta InstituteEnvironmental Law and Policy CenterBOMAASHRAEEquipment DistributorsMEEAAGCC

Regional Application Centers

Project Elements

Baseline Assessment / CharacterizationCase StudiesInformation RepositoryProject Support

Baseline Assessments (By State)

Document Acceptance / Opposition to BCHPIdentify / Contact Target CustomersIdentify Installations (Operating & Planned)Document Current Policy and Pricing (Electric & Gas)Identify Market Barriers & Market TrendsGuide Application Center Activities to Identify Projects.

Case Studies

Develop the Analysis Framework & ProtocolsCollect Information from Existing and New SitesDevelop a Database of Case StudiesDevelop Two-Dimensional Market Identification Matrices

Information Repository

Website --- Linked to Appropriate SitesDatabases --- Expandable for Other CentersCHP Literature/Reports/Presentations

Project Support

Standard OutreachWebsiteTool Kit

Case StudiesScreening SoftwareBaseline InformationContinuing Education CreditsGeneral Information

High ImpactStandard OutreachSWAT Team

High Impact Projects

Application --- Repeatable / Large Market ImpactEconomic --- Now / FutureSize --- Significant Impact

SWAT Teams

Mission:Apply “Expert” Talent to High Impact Projects to:

Provide Assistance to “Remove Perceived Risk”

Provide Assistance to Identify Technical Solutions”

SWAT Team Concept

On CallFocusedExpert

On CallFocusedExpert

On CallFocusedExpert

On CallFocusedExpert

Center TrainedBCHP SWAT Team

Leader

Center TrainedBCHP SWAT Team

Leader

Center TrainedBCHP SWAT Team

Leader

LocalProject

ChampionThe

Customer

Architects/EngineersSpecifiers

Building OwnersESCos

SWAT Team

Type of Experts

Diverse Group of Center SupportersRespected ProfessionalsKnowledgeable in CHP for Buildings & IndustryUnderstand Center Policies & Offerings

Key Technical IndividualsTrained in Application of CHP for Buildings & IndustryFirst Line of Technical Assistance to Owners, Developers, Consulting Engineers

Defined Experts Available to Team LeadersAnswer / Solve Specific ProblemsUniversities, National Labs, Industry

Local Project Champions

Team Leaders

Focused Experts

Application Center Support Options

Support Options

Revise SurveyDevelop process for CHP AssessmentsVendor QualificationEconomic Assessment Tools

Support Example

Museum of Science and IndustryMajor Renovation Project (HVAC and Electrical)Excellent Load Profile (Flat from 9:00 am to 10:00 pm)`Concept Definition and Economic Assessment1,250 kWe and DesiccantsTie into existing hot water loopHeating, kitchen, and AC reheat $200,000 in annual savingsFirst Cost of $1,000,000

Support Example, Barriers

Electrical Distribution SystemInterconnect

Utility StudyStandby Charges

Questions“Every morning in Africa, a gazelle wakes up. It knows it must run faster than the fastest lion or it will be killed. Every morning a lion wakes up. It knows it must outrun the slowest gazelle or it will starve to death. It doesn’t matter whether you are a lion or a gazelle: When the sun comes up you’d better be running.”