chp 1 - oma

DESCRIPTION

Cost Management AccountingTRANSCRIPT

Overview to Cost and Management Accounting

In today’s business world, the resources available are very scarce.

Hence, every business unit must strive hard to obtain maximum output with the available input in order to ensure the optimum utilization of scarce resources.

The value of input is measured against the value of output.

In the present era of cut-throat competition, the need to study this subject is growing very fast.

Every businessman makes a constant effort to improve his/her business.

Waste management at hospital All waste from the district hospital is gathered and

thrown into piles behind the main hospital building. Every six months, the hospital director hires some laborers to shovel the waste into trucks and cart it off to the closest dump, which is located in a neighboring town. Frequently, people pick through the waste looking for items that they can use or sell, children play near the waste, and dogs are commonly seen poking their noses in the piles.

Who is at risk of infection from these practices? How can the waste-disposal problems here be

solved?

The staff who dispose of the waste, the laborers who cart the waste away, and members of the community in the neighboring town who scavenge or play in the waste are at risk. The community at large is also at risk from the spread of infection by animals that have access to the waste.

The waste disposal problems here can be solved by: Sorting medical waste from general waste at the point

at which it is generated to reduce the amount of waste requiring special handling

Building an incinerator or digging a pit to burn or bury the medical waste

Removing the waste more often Educating staff and the community about proper waste

disposal Ensuring that people and animals do not have access to

the waste while it is stored at the hospital.

Machine specifications 2. Cost of machine and maintenance required.

3. Utility consumption (electricity, water, labor etc) 4. Production cost 5. Details of raw materials (input, output, wastage) 6. Technical training and assistance required. 7. Total project investment 8. Return on investment

Industry / Product/ Activity Cost Unit Brick Making 1000 bricks Automobile Automobiles unit manufactured Cement Tonne of cement Coal Tonne of coal Electicity Kilowatt – hour (kwh) Professional Serice Chargeable hour Education Enrolled student Spinning Kg of yarn spun Textiles Meter of cloth produced Oil rfineing Per tone Passengers Transport Passenger kilometer Cargo Transport Tonne kilometer Toy making Batch of toys Ship Building Per ship Gas Cubic feet or cubic meter Mines Tonne of mineral extracted Hospital Patient day Sugar Tonne of sugar manufactured Credit control Account maintained Selling Customer call

Cost may be defined as 1. the amount of expenditure (actual or

notional) incurred on or attributable to a given thing, or

2. to ascertain the cost of a give nthing

Costing is the techniques and process of ascertaining costs .

Cost unit is a quantitative unit of product or service in relation to which costs are ascertained.

Cost unit is a unit of product or unit of service to which costs are ascertained by means of allocation, apportionment and absorption.

Cost object is any activity for which a separate measurement of costs is desired

Cost accounting is the process of accounting for cost.

Cost accounting is generally concerned with internal reporting for management requirement.

The development of cost accounting is of recent origin.

The Chartered Institute of Management Accountants, U.K. (CIMA) defines costing as ‘the technique and process of ascertaining costs.’

Costing is a tool to determine the cost of products or service.

Cost accounting – analysis and classification of costs or expenditure.

Cost accountancy – application of costing and cost accounting principles.

‘Cost Accounting is to serve management in the execution of policies and in the comparison of actual and estimated results in order that the value of each policy may be appraised and changed to meet the future conditions.’ To calculate cost per unit To prepare a correct cost analysis To ascertain the wastage in each process of

manufacture To provide necessary information for the

determination of selling price

To compute product-wise profit To serve the management in the valuation of

W-I-P To install and implement cost control systems To advice management for future expansion To establish an effective reporting system To guide the management in the preparation

and implementation of incentive schemes based on productivity and cost savings.

The functions of financial accounting are concerned with that of bookkeeping, i.e. maintenance of records of costs, debtors, and creditors, etc.

As per the company law requirements, the company has to maintain the accounts for their adoption by the shareholders in the Annual General Meeting.

• Financial accounting doesn’t aims at continuous reporting of financial data, which the cost accounting does

• Financial accounts will not reveal the data by jobs, process, products, etc.

• It provides only historical data, and it would be too late for any corrective action.

• It does not provide data for adequate control over materials, labour, and overheads.

• In financial accounting, there are no systems to set predetermined estimates, standards, or budgets.

• Purpose• Forms of Accounts• Recording• Items of Costs• Analysis of Profits• Control• Periodicity• Nature of Transaction• Inventory Valuation• Figures

• To quote J. Batty, ‘Management Accountancy is the term used to describe the accounting methods, systems and techniques, which coupled with special knowledge and ability, assists management in its tasks of maximizing profits or minimizing losses.

• Management Accountancy is the blending together into a coherent whole, financial accounting, cost accountancy and all aspects of financial management.’

• Management Accounting is an extension of managerial aspects, of cost accounting.

• Thus, it is the accounting to assist the management in planning and decision-making.

• A great variety of accounting information is available to managers.

• The accountant chooses the information to be reported to a manager by:– Identifying the purpose for which the information is needed. – Determining the relevance of the information.

• The accountant has to identify the specific purpose for which cost accounting information is required by the manager.

• Information is relevant if it– Affects the accomplishment of the objectives of the decision maker. – Will change as a result of the decisions or choice made by the deci- sion

maker.• Historically, the Management Accountant was known as

‘Controller’ since he/she was in charge of all financial accounting and cost accounting functions.

• Line managers are directly responsible for attaining this objective as efficiently as possible.

• When a department’s primary task is to advise and serve other departments in the organization, it is a ‘staff’ department.

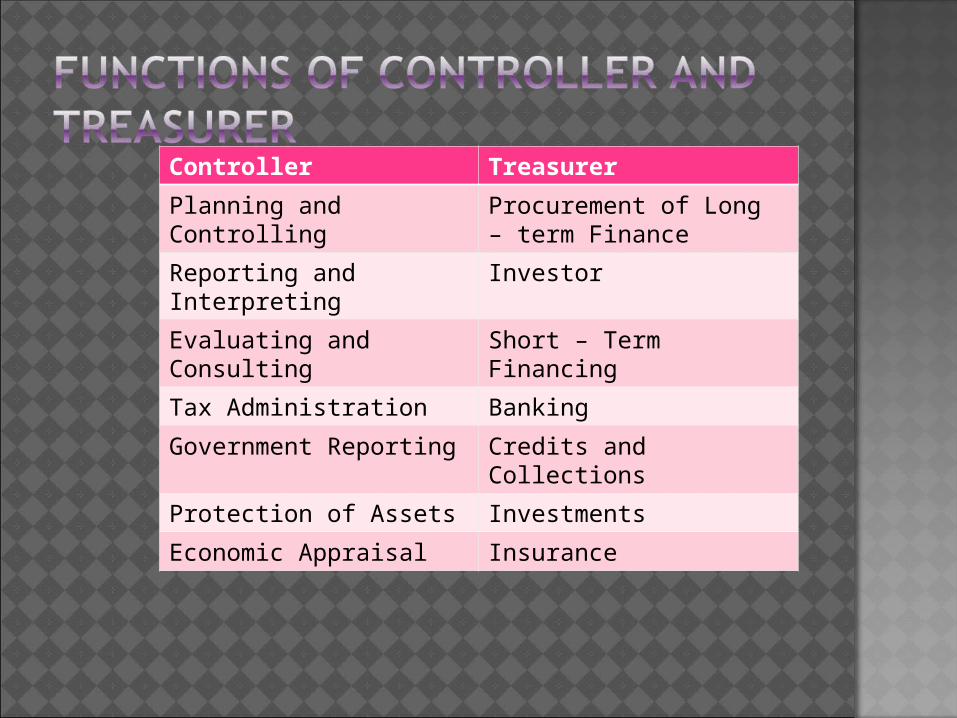

Controller Treasurer

Planning and Controlling Procurement of Long – term Finance

Reporting and Interpreting

Investor

Evaluating and Consulting

Short – Term Financing

Tax Administration Banking

Government Reporting Credits and Collections

Protection of Assets Investments

Economic Appraisal Insurance

• To determine the actual cost of each article, process, operation, service, department or segment of activity.

• To reveal and report inefficiencies in the form of material wastage, loss of time in material buying, storing, and issuing.

• To provide actual figures of cost comparison with estimates of costs and price fixing.

• To find out the degree of efficiency and productive capacity of men and machines and ideal standard for their working.

• To implement incentive wage plans for workers.• To reduce cost through budgetary control and standard costing.• To study trends at different volumes of output, and to determine

production policies and programs.• To ensure continuous check and adjustment of stores and

materials with the help of perpetual inventory.• To organize internal audit system, and interlocking of financial and

cost accounts to verify the accuracy of each other.• To furnish necessary data for the preparation of profit and loss

account and balance sheet at short intervals [e.g., monthly, quarterly, etc.] for each department or business as a whole.

• Price Fixation• Control on Unprofitable Activities• Useful Information• Cost Control• Provides Valuable Data• Effective Check• Preparation of Budgets and Regulations of

production• Fixation of Responsibilities• Independent Check• Prevention of Manipulation,

misappropriation, and frauds

Expensive Differences in Results Unnecessary Worthless Inapplicability

• Every concern must design its own costing system, keeping in view its peculiar problems.

• If financial books can afford the necessary information, separate costing system is not needed.

• Reasonable accuracy is enough, of course, this depends upon the nature of industry.

• As a rule, costing information should be collected as and when the work proceeds.

• Simple and Easy• Should suit the organization• Co-ordination and co-operation among

executives• Ensure proper accounting and allocation

of material• Cost accounts should be able to

reconcile with Financial accounts• It should be Economical

To the ManagementPlanningOrganizingControllingBudgetingDecision-makingPricingEvaluation of operating efficiency

To the Employees Incentive BonusHigher earnings through time and motion

studyOvertime paymentsBenefit of job evaluationContinuous employment and job security

• To the creditors– Can access more information in comparison

to Financial accounts– To ascertain the solvency, profitability

• To the government– More taxes through higher production– Useful in preparing import and export policy

• To the society– Lower prices through cost reduction– Better quality of products and services