choosing and managing 3rd party valuation service providers

TRANSCRIPT

Practical Experience Gained in Choosing and Managing 3rd Party Valuation

Service Providers

Emerging Best Practice Approaches to Valuation Operations

London 17 May 2012

Steven LaRose Hurn

I. The Depth and Breadth of the Valuations UniverseA. Derivatives

i. OTC Derivatives

ii. Exchange Trades Derivatives

B. Cash

II. Choosing a third party provider: different organizational mandates determine which provider offers the best solution

III. A Due Diligence Primer

IV. Integrating CCP prices into the Valuation Process

The Depth and Breadth of the Valuations Universe

The Depth and Breadth of the Valuations Universe

i. OTC Derivatives – Rates:

• Vanilla :IRS (xcurrency, basis, inflation, SIFMA); volatility instruments (Bermudan options, caps/floors, CMS)

• Complex (callable range accruals, PRDCs, . . .)

– Credit: single name CDS, ABCDS, credit indices, index tranches (std & bespoke), synthetic CDOs; volatility instruments (credit swaptions)

– Equities: single name and index OTC options, CFDs, dividend swaps, TRS

– FX: FX forwards (including NDFs), FX variance swaps, simple and exotic FX options

– Commodities : energy, metals, weather - options and TRS– Structured products

The Depth and Breadth of the Valuations Universe

ii. Exchange Traded Derivatives

iii. Cash– Fixed Income

• Sovereign Debt

• Corporates, HY & EM

• Convertibles

• Mortgage backed (RMBS &CMBS), Agency & non-Agency

• Asset backed securities (ABS)

– Leveraged Loans

– Structured Finance

• CDOs, CLOs, CDO2

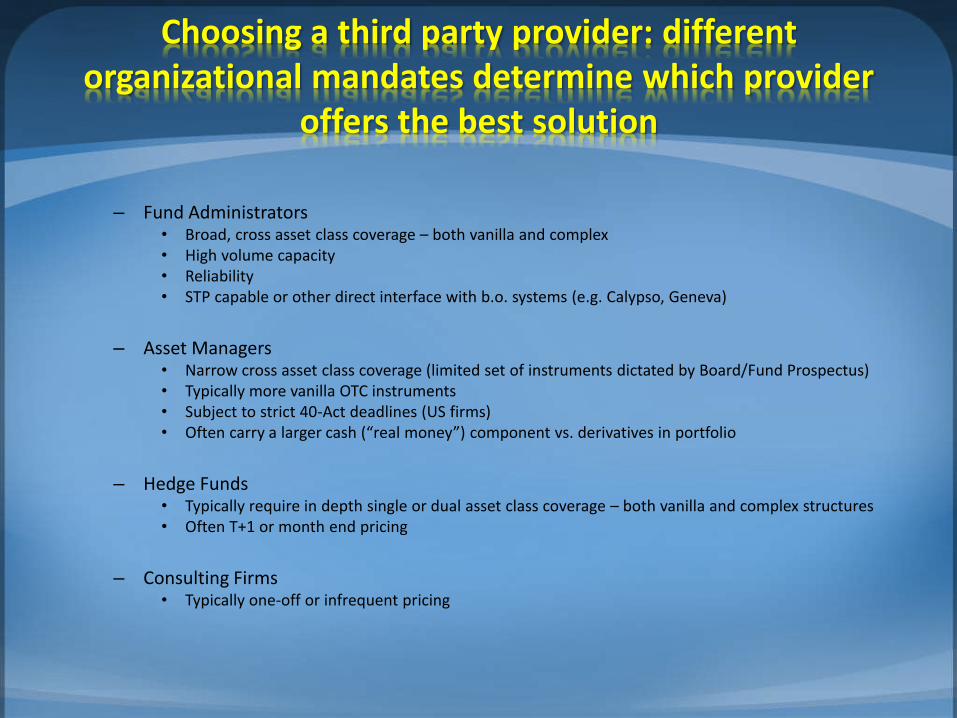

Choosing a third party provider: different organizational mandates determine which

provider offers the best solution

Choosing a third party provider: different organizational mandates determine which provider

offers the best solution

– Fund Administrators• Broad, cross asset class coverage – both vanilla and complex• High volume capacity• Reliability• STP capable or other direct interface with b.o. systems (e.g. Calypso, Geneva)

– Asset Managers• Narrow cross asset class coverage (limited set of instruments dictated by Board/Fund Prospectus)• Typically more vanilla OTC instruments• Subject to strict 40-Act deadlines (US firms)• Often carry a larger cash (“real money”) component vs. derivatives in portfolio

– Hedge Funds• Typically require in depth single or dual asset class coverage – both vanilla and complex structures• Often T+1 or month end pricing

– Consulting Firms• Typically one-off or infrequent pricing

A Due Diligence Primer

A Due Diligence Primer

– Management/Organizational Structure• Firm History – how long in the Valuations business• Structure of the Valuations Group

– Size and composition of the analyst team, supporting quants, et.al.– Point of contact/escalation path– Global coverage

– IT Infrastructure• Data centers – outsourced – backups

– If outsourced, is the Data center SASE16 –SOC2 compliant?

• Is there a Disaster Recovery/Business Continuity Plan– Are there offsite facilities for personnel to relocate ?

• What are the internal client data security policies –– Is the Valuations group alone or is the organization SASE16-SOC2 compliant ?– Are client accounts segregated ?– Secure username/password policies– Spreadsheet encryption

• Upload/download protocols– FPML/XML over https– ftp– formatted interface with Calypso/Geneva/Summit– interface with client proprietary b.o. system

A Due Diligence Primer

– Data Sourcing – Quality• Review data cleaning/scrubbing procedures in each asset class• Sourcing of volatility surface data in each asset class is crucial

– Methodology Documentation• Modelling standards and assumptions should be thoroughly documented

Data sourcing and methodology are the keys to transparency, as well to effective FAS157/IFRS 13 level determination

– Price Challenge Process• Written policy (turnaround time – SLAs)• Transparency

– OTC Derivatives – underlying curves and point volatilities– Cash –transactional prices (time stamped)

A Due Diligence Primer

• Additional Considerations

– OIS Discounting

– Liquidity Measures

– Bid/Offer side Valuations

– Multiple snap times

– SABR modelling for Rates and FX volatility structures

Integrating CCP prices into the Valuation Process

Integrating CCP prices into the Valuation Process

• LCH and ICE are currently providing settlement prices to valuations providers

• Prices in asset classes where there is active clearing are provided

• Timing is too late in the day for T0 – only valid for T+1 or month end pricing

Practical Experience Gained in Choosing and Managing 3rd Party Valuation

Service Providers

Questions, comments, observations :